T3 2020 HA3011 Advanced Financial Accounting Assignment

VerifiedAdded on 2022/12/29

|10

|2485

|1

Homework Assignment

AI Summary

This assignment delves into advanced financial accounting principles, examining the elements of financial reports with examples, and critically discussing the conceptual framework's nature and benefits. It identifies and analyzes McMillan Shakespeare Limited as a reporting entity, providing supporting examples. The assignment explores the differentiation between revenues and gains, evaluating its significance for financial statement users. It then explains and discusses property, plant, and equipment (PP&E), including impairment assessments, measurement, and valuation. The report covers various aspects of financial reporting including assets, liabilities, profit and loss, and the importance of reporting entities, revenues, and gains. The conclusion summarizes the findings and emphasizes the practical application of accounting principles in a real-world scenario.

Advanced Financial

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Elements of financial report with relevant examples and critically discuss the nature and the

benefits of the conceptual framework for accounting.................................................................1

2. Identify and critically discuss if allocated company is a reporting entity, provide detailed

and relevant examples and factors to support argument.............................................................2

3. Identify and discuss if allocated company show revenues and gains? In your view, do you

think differentiating revenues and gains is of a benefit to the users of the financial statements?

Explain and provide examples....................................................................................................3

4 Explain and discuss the list of Property, Plant and Equipment, including impairment

assessments in the financial statements and the related notes. How are these assets measured

and valued?..................................................................................................................................4

CONCLUSION ...............................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Elements of financial report with relevant examples and critically discuss the nature and the

benefits of the conceptual framework for accounting.................................................................1

2. Identify and critically discuss if allocated company is a reporting entity, provide detailed

and relevant examples and factors to support argument.............................................................2

3. Identify and discuss if allocated company show revenues and gains? In your view, do you

think differentiating revenues and gains is of a benefit to the users of the financial statements?

Explain and provide examples....................................................................................................3

4 Explain and discuss the list of Property, Plant and Equipment, including impairment

assessments in the financial statements and the related notes. How are these assets measured

and valued?..................................................................................................................................4

CONCLUSION ...............................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION

Accounting is a procedure of identifying financial transactions and recording in

accounting books. In this procedure includes various steps such as, summarizing, determining

and reporting financial transactions in proper manner. The advanced financial accounting use by

the organisation to present all the financial reports and business skills that are interpret at the

global professional atmosphere. This type of accounting includes accounting operations, local

currencies, merger of public holding companies and many others (Christensen, Nikolaev and

Wittenberg‐Moerman, 2016). This report based on the McMillan Shakespeare limited is

subsidiaries of Australia's biggest salary packaging base organisation and leading provider of

fleet and assets management and fleet financing. In this report cover conceptual framework

benefits, nature, measurement of PP&E and reporting entry. Along with presents revenues and

gains of selected organisation with examples and covers impairment of financial statements.

MAIN BODY

1. Elements of financial report with relevant examples and critically discuss the nature and the

benefits of the conceptual framework for accounting

McMillan Shakespeare limited is a market leading and trusted organisation that provides

salary packaging, novated leasing and connected with financial products & services. The

company recruit highly qualify team of above 1300 peoples across Australia, UK, New Zealand

for the management of largest public, charitable and private business entity. There are

mentioned different elements of financial report of McMillan Shakespeare limited such as:

Assets: The total written down value (WDV) of assets enhanced by 0.9% to $380.2

million at the financial year. Rather than number of units under management reduce by

5.5% to 20600 units. A portfolio sale out of $165.8 million at the particular year in case

of release capital led to an 18% reduce in the written down value of assets under assets

management to $118.1 million as at 30 June 2019 as per the pleasingly net amount

financed enhance to $986.9 million from $886.5 million in financial year 2018

(Ciapessoni and et.al, 2019).

Liabilities: It is presenting in balance sheet that categorised into two parts current and non

current. In the current liabilities consist of trade and other payable year 2019 95267 and

1

Accounting is a procedure of identifying financial transactions and recording in

accounting books. In this procedure includes various steps such as, summarizing, determining

and reporting financial transactions in proper manner. The advanced financial accounting use by

the organisation to present all the financial reports and business skills that are interpret at the

global professional atmosphere. This type of accounting includes accounting operations, local

currencies, merger of public holding companies and many others (Christensen, Nikolaev and

Wittenberg‐Moerman, 2016). This report based on the McMillan Shakespeare limited is

subsidiaries of Australia's biggest salary packaging base organisation and leading provider of

fleet and assets management and fleet financing. In this report cover conceptual framework

benefits, nature, measurement of PP&E and reporting entry. Along with presents revenues and

gains of selected organisation with examples and covers impairment of financial statements.

MAIN BODY

1. Elements of financial report with relevant examples and critically discuss the nature and the

benefits of the conceptual framework for accounting

McMillan Shakespeare limited is a market leading and trusted organisation that provides

salary packaging, novated leasing and connected with financial products & services. The

company recruit highly qualify team of above 1300 peoples across Australia, UK, New Zealand

for the management of largest public, charitable and private business entity. There are

mentioned different elements of financial report of McMillan Shakespeare limited such as:

Assets: The total written down value (WDV) of assets enhanced by 0.9% to $380.2

million at the financial year. Rather than number of units under management reduce by

5.5% to 20600 units. A portfolio sale out of $165.8 million at the particular year in case

of release capital led to an 18% reduce in the written down value of assets under assets

management to $118.1 million as at 30 June 2019 as per the pleasingly net amount

financed enhance to $986.9 million from $886.5 million in financial year 2018

(Ciapessoni and et.al, 2019).

Liabilities: It is presenting in balance sheet that categorised into two parts current and non

current. In the current liabilities consist of trade and other payable year 2019 95267 and

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

94588, contract liabilities (6051 to 8995), current tax, borrowings and many others. Some

amounts are increase and some are decreased. In the non current liabilities consist of

borrowings, unearned premium liability and many more.

Profit and loss: It is presenting profit and loss of company in particular financial year.

When company has goof revenues and lesser cost that time face profit positively.

Nature of conceptual framework: A conceptual framework is financial tool which is utilised by

the company to get a encompassing statement of a phenomenon. This tool is used by the business

entity in various areas and most commonly used to presents main concepts and relationship

between them that require to be studied. It is wide based in nature and principles when really

developing financial reports. With minor modifications provides basis for the FASB's standard

setting. This framework use for accounting and set effective standards with the intention of

providing the principal based accounting standard and setting board for becoming overly rules

based (Cobb, 2016).

Benefits: There are mentioned different benefits of this framework that achieved by the

McMillan Shakespeare limited company such as:

Develop and connected with the business entity of concepts as well as objectives

It is beneficial to increase financial statement users and understand financial reporting.

Improve comparability in various companies financial reporting

Provide a specific structure for sort out new and future practical problems.

Determined the transactions and reported how to presented and communicated with users.

2. Identify and critically discuss if allocated company is a reporting entity, provide detailed and

relevant examples and factors to support argument

A number of concepts of reporting entity are inherent in existing laws and regulations

that specify entities that should prepare general purpose financial reports. Those entity consider

as reporting entity who are following general purpose financial report to analysis the actual

position of business and efficiency to make future decisions. These decisions taking by the

company on financial information basis and use by various users like shareholders, lenders or

future investors. A non reporting entity are charged with non governance and analysed that there

are no users based on GPFR.

McMillan Shakespeare limited is a locally closely-held public listed company that

derives its sales as per the provision of salary business, vehicle leasing administration and other

2

amounts are increase and some are decreased. In the non current liabilities consist of

borrowings, unearned premium liability and many more.

Profit and loss: It is presenting profit and loss of company in particular financial year.

When company has goof revenues and lesser cost that time face profit positively.

Nature of conceptual framework: A conceptual framework is financial tool which is utilised by

the company to get a encompassing statement of a phenomenon. This tool is used by the business

entity in various areas and most commonly used to presents main concepts and relationship

between them that require to be studied. It is wide based in nature and principles when really

developing financial reports. With minor modifications provides basis for the FASB's standard

setting. This framework use for accounting and set effective standards with the intention of

providing the principal based accounting standard and setting board for becoming overly rules

based (Cobb, 2016).

Benefits: There are mentioned different benefits of this framework that achieved by the

McMillan Shakespeare limited company such as:

Develop and connected with the business entity of concepts as well as objectives

It is beneficial to increase financial statement users and understand financial reporting.

Improve comparability in various companies financial reporting

Provide a specific structure for sort out new and future practical problems.

Determined the transactions and reported how to presented and communicated with users.

2. Identify and critically discuss if allocated company is a reporting entity, provide detailed and

relevant examples and factors to support argument

A number of concepts of reporting entity are inherent in existing laws and regulations

that specify entities that should prepare general purpose financial reports. Those entity consider

as reporting entity who are following general purpose financial report to analysis the actual

position of business and efficiency to make future decisions. These decisions taking by the

company on financial information basis and use by various users like shareholders, lenders or

future investors. A non reporting entity are charged with non governance and analysed that there

are no users based on GPFR.

McMillan Shakespeare limited is a locally closely-held public listed company that

derives its sales as per the provision of salary business, vehicle leasing administration and other

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial services. It is reporting entity based organisation that follows all the accounting

standards and accordingly prepare their financial statements. When company do not based on

reporting entity so face many risk and do not get any opportunities (brahim and Haruna, 2017)

There are mentioned different factors of reporting entity such as:

Separation of management from those with an economic interest in the entity.

Extent and application of financial dependence

Efficiency to appoint and discard of government and administration bodies.

Efficiency to direct operations

For example: After the application of reporting entity company get many opportunities

positively and stakeholders provide value the additional information provided in a GPRF. When

company use the concept so effectively present their social responsibility and standing within the

community.

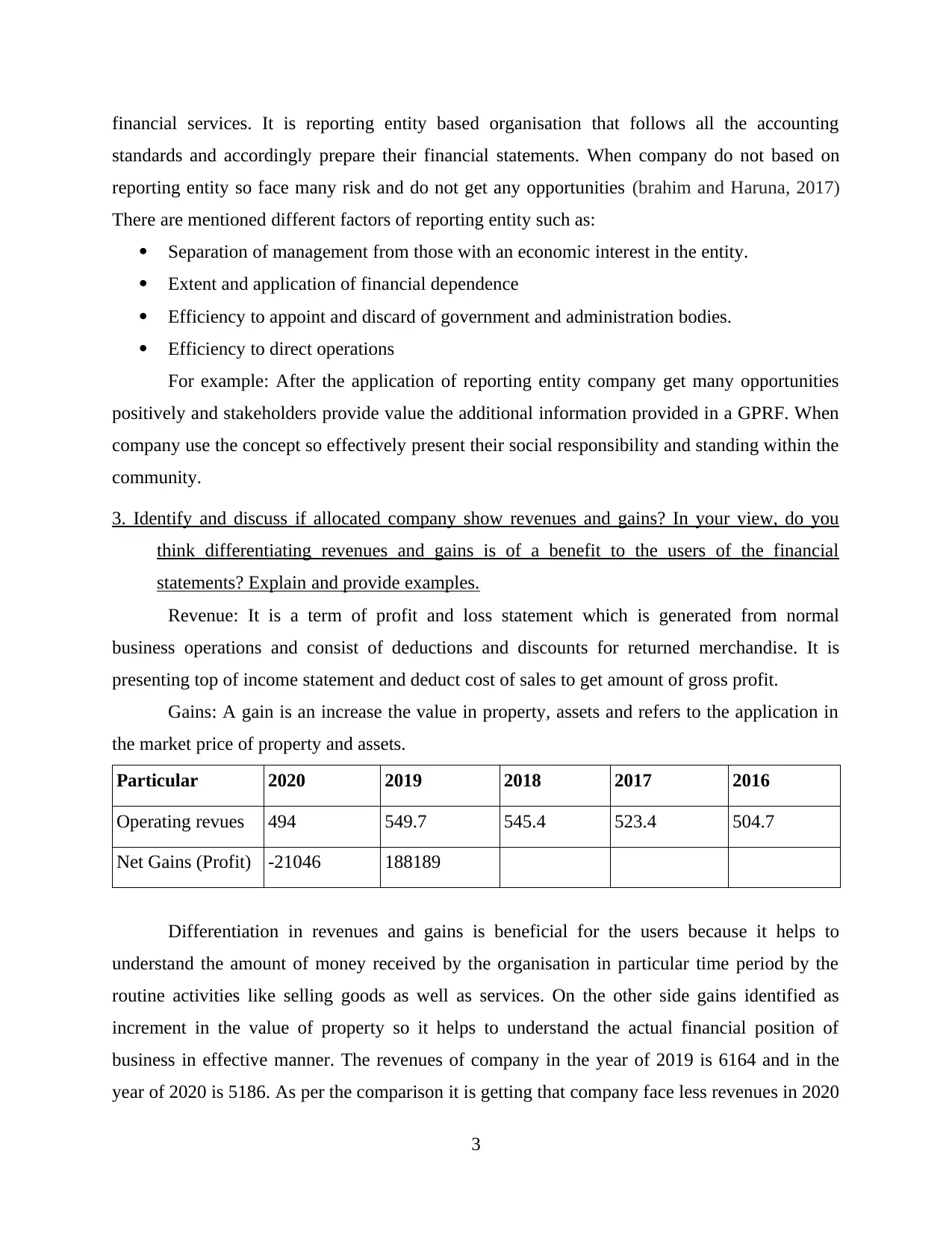

3. Identify and discuss if allocated company show revenues and gains? In your view, do you

think differentiating revenues and gains is of a benefit to the users of the financial

statements? Explain and provide examples.

Revenue: It is a term of profit and loss statement which is generated from normal

business operations and consist of deductions and discounts for returned merchandise. It is

presenting top of income statement and deduct cost of sales to get amount of gross profit.

Gains: A gain is an increase the value in property, assets and refers to the application in

the market price of property and assets.

Particular 2020 2019 2018 2017 2016

Operating revues 494 549.7 545.4 523.4 504.7

Net Gains (Profit) -21046 188189

Differentiation in revenues and gains is beneficial for the users because it helps to

understand the amount of money received by the organisation in particular time period by the

routine activities like selling goods as well as services. On the other side gains identified as

increment in the value of property so it helps to understand the actual financial position of

business in effective manner. The revenues of company in the year of 2019 is 6164 and in the

year of 2020 is 5186. As per the comparison it is getting that company face less revenues in 2020

3

standards and accordingly prepare their financial statements. When company do not based on

reporting entity so face many risk and do not get any opportunities (brahim and Haruna, 2017)

There are mentioned different factors of reporting entity such as:

Separation of management from those with an economic interest in the entity.

Extent and application of financial dependence

Efficiency to appoint and discard of government and administration bodies.

Efficiency to direct operations

For example: After the application of reporting entity company get many opportunities

positively and stakeholders provide value the additional information provided in a GPRF. When

company use the concept so effectively present their social responsibility and standing within the

community.

3. Identify and discuss if allocated company show revenues and gains? In your view, do you

think differentiating revenues and gains is of a benefit to the users of the financial

statements? Explain and provide examples.

Revenue: It is a term of profit and loss statement which is generated from normal

business operations and consist of deductions and discounts for returned merchandise. It is

presenting top of income statement and deduct cost of sales to get amount of gross profit.

Gains: A gain is an increase the value in property, assets and refers to the application in

the market price of property and assets.

Particular 2020 2019 2018 2017 2016

Operating revues 494 549.7 545.4 523.4 504.7

Net Gains (Profit) -21046 188189

Differentiation in revenues and gains is beneficial for the users because it helps to

understand the amount of money received by the organisation in particular time period by the

routine activities like selling goods as well as services. On the other side gains identified as

increment in the value of property so it helps to understand the actual financial position of

business in effective manner. The revenues of company in the year of 2019 is 6164 and in the

year of 2020 is 5186. As per the comparison it is getting that company face less revenues in 2020

3

as compare of 2019. Any gains arising from alteration in the fair value of the hedge contracts are

consider as across-the-board income to the extent of the effective portion of the cash flow and

ineffective portion recognised as income statement (Nicholls, 2020)..

Revenues generates by the organisation in the course of the entity like selling of goods

and services and on the other side gain present other item which is considered as the income

which may or may not occur in the business. When the business entity sales of goods in larger

manner in particular year so that time generate more revenues but on the other side company do

not sale out any property and assets so gain is not occurred in the business. Thus, differentiation

in the in revenues and gains is good for users to know financial health in proper manner and take

right decision effectively.

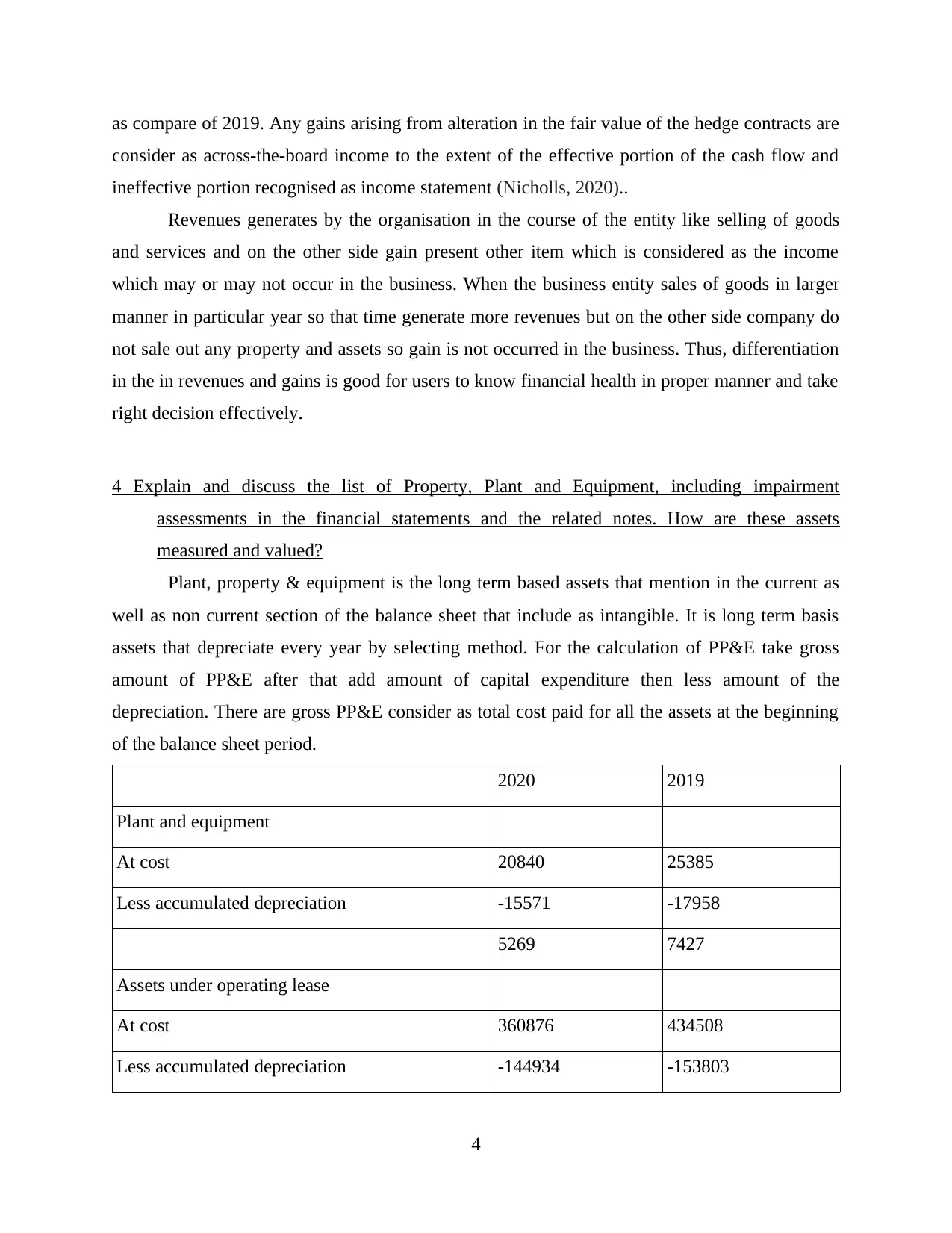

4 Explain and discuss the list of Property, Plant and Equipment, including impairment

assessments in the financial statements and the related notes. How are these assets

measured and valued?

Plant, property & equipment is the long term based assets that mention in the current as

well as non current section of the balance sheet that include as intangible. It is long term basis

assets that depreciate every year by selecting method. For the calculation of PP&E take gross

amount of PP&E after that add amount of capital expenditure then less amount of the

depreciation. There are gross PP&E consider as total cost paid for all the assets at the beginning

of the balance sheet period.

2020 2019

Plant and equipment

At cost 20840 25385

Less accumulated depreciation -15571 -17958

5269 7427

Assets under operating lease

At cost 360876 434508

Less accumulated depreciation -144934 -153803

4

consider as across-the-board income to the extent of the effective portion of the cash flow and

ineffective portion recognised as income statement (Nicholls, 2020)..

Revenues generates by the organisation in the course of the entity like selling of goods

and services and on the other side gain present other item which is considered as the income

which may or may not occur in the business. When the business entity sales of goods in larger

manner in particular year so that time generate more revenues but on the other side company do

not sale out any property and assets so gain is not occurred in the business. Thus, differentiation

in the in revenues and gains is good for users to know financial health in proper manner and take

right decision effectively.

4 Explain and discuss the list of Property, Plant and Equipment, including impairment

assessments in the financial statements and the related notes. How are these assets

measured and valued?

Plant, property & equipment is the long term based assets that mention in the current as

well as non current section of the balance sheet that include as intangible. It is long term basis

assets that depreciate every year by selecting method. For the calculation of PP&E take gross

amount of PP&E after that add amount of capital expenditure then less amount of the

depreciation. There are gross PP&E consider as total cost paid for all the assets at the beginning

of the balance sheet period.

2020 2019

Plant and equipment

At cost 20840 25385

Less accumulated depreciation -15571 -17958

5269 7427

Assets under operating lease

At cost 360876 434508

Less accumulated depreciation -144934 -153803

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

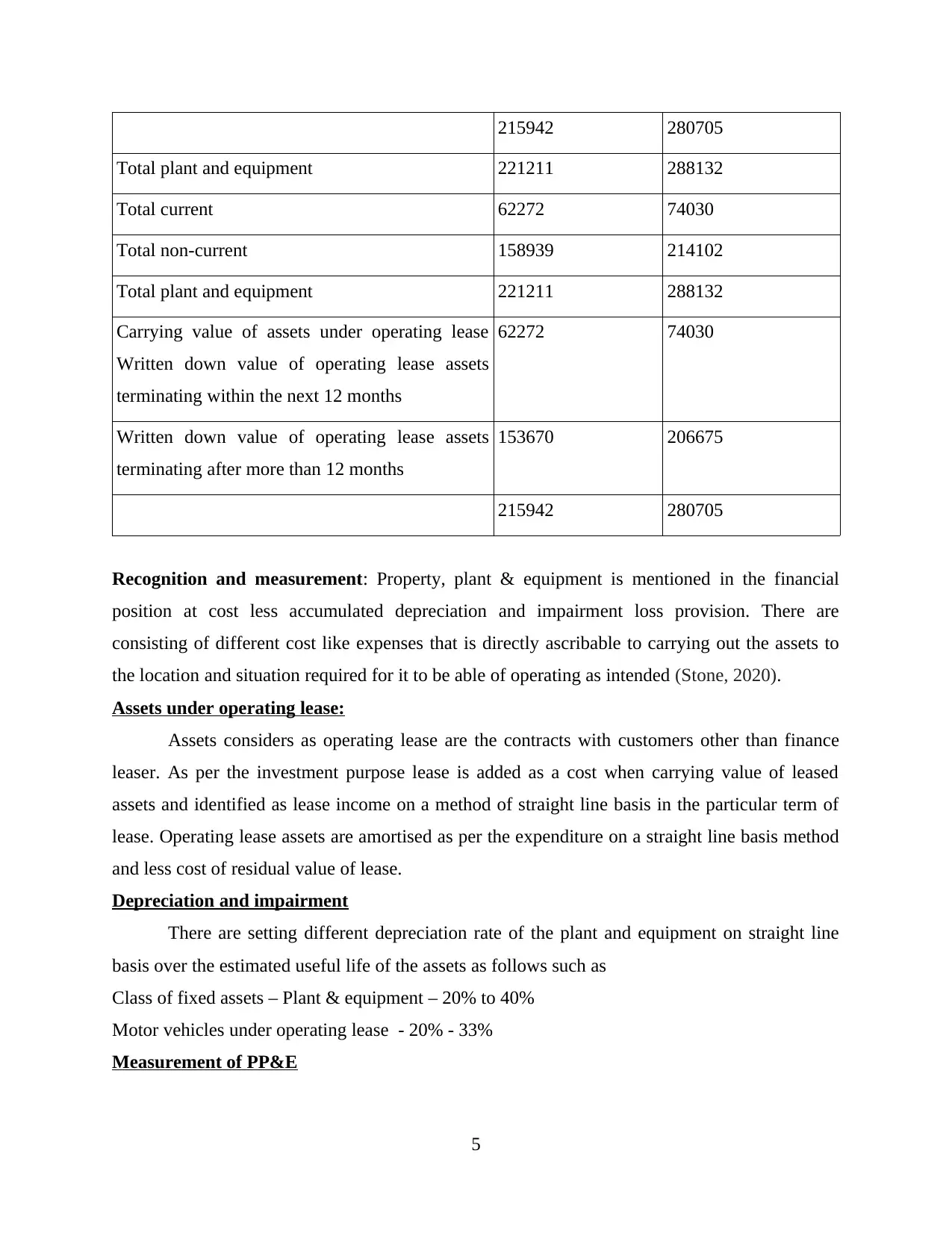

215942 280705

Total plant and equipment 221211 288132

Total current 62272 74030

Total non-current 158939 214102

Total plant and equipment 221211 288132

Carrying value of assets under operating lease

Written down value of operating lease assets

terminating within the next 12 months

62272 74030

Written down value of operating lease assets

terminating after more than 12 months

153670 206675

215942 280705

Recognition and measurement: Property, plant & equipment is mentioned in the financial

position at cost less accumulated depreciation and impairment loss provision. There are

consisting of different cost like expenses that is directly ascribable to carrying out the assets to

the location and situation required for it to be able of operating as intended (Stone, 2020).

Assets under operating lease:

Assets considers as operating lease are the contracts with customers other than finance

leaser. As per the investment purpose lease is added as a cost when carrying value of leased

assets and identified as lease income on a method of straight line basis in the particular term of

lease. Operating lease assets are amortised as per the expenditure on a straight line basis method

and less cost of residual value of lease.

Depreciation and impairment

There are setting different depreciation rate of the plant and equipment on straight line

basis over the estimated useful life of the assets as follows such as

Class of fixed assets – Plant & equipment – 20% to 40%

Motor vehicles under operating lease - 20% - 33%

Measurement of PP&E

5

Total plant and equipment 221211 288132

Total current 62272 74030

Total non-current 158939 214102

Total plant and equipment 221211 288132

Carrying value of assets under operating lease

Written down value of operating lease assets

terminating within the next 12 months

62272 74030

Written down value of operating lease assets

terminating after more than 12 months

153670 206675

215942 280705

Recognition and measurement: Property, plant & equipment is mentioned in the financial

position at cost less accumulated depreciation and impairment loss provision. There are

consisting of different cost like expenses that is directly ascribable to carrying out the assets to

the location and situation required for it to be able of operating as intended (Stone, 2020).

Assets under operating lease:

Assets considers as operating lease are the contracts with customers other than finance

leaser. As per the investment purpose lease is added as a cost when carrying value of leased

assets and identified as lease income on a method of straight line basis in the particular term of

lease. Operating lease assets are amortised as per the expenditure on a straight line basis method

and less cost of residual value of lease.

Depreciation and impairment

There are setting different depreciation rate of the plant and equipment on straight line

basis over the estimated useful life of the assets as follows such as

Class of fixed assets – Plant & equipment – 20% to 40%

Motor vehicles under operating lease - 20% - 33%

Measurement of PP&E

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For the buildings, equipment and vehicles cost for total of $1.2 million at the starting

point. Foe example, Started a business in the year of $1.2 million in PP&E and spend about

$300000 upgrading of some equipment and $100,000 purchasing new products so it provides a

total of $1.6 million worth of fixed assets. Depreciation apply by the company on fixed assets as

per the standard accounting methods and also use accelerated method that takes most of the

depreciation up front and over time (Watkins, 2020).

Impairment of PP&E

For the impairment take the carrying amount of PPE assets that exceeds its recoverable

amount. The carrying amount is analysed the value of the assets that mentioned in the balance

sheet after the accumulation depreciation and impairment losses.

CONCLUSION

As per the above report it has been concluded that advanced financial accounting use by

the organisations to present all the financial reports in effective manner. On the basis of this

report users determine the financial position of company and take effective investment decision.

Along with analysis the nature of conceptual framework of company and different advantages

achieve by the organisations. There are mentioned list of plant & property use by the company in

a financial year apply impairment assessment of assets. Moreover, differentiate the revenues and

gains and beneficial for users to identify actual position of business effectively.

6

point. Foe example, Started a business in the year of $1.2 million in PP&E and spend about

$300000 upgrading of some equipment and $100,000 purchasing new products so it provides a

total of $1.6 million worth of fixed assets. Depreciation apply by the company on fixed assets as

per the standard accounting methods and also use accelerated method that takes most of the

depreciation up front and over time (Watkins, 2020).

Impairment of PP&E

For the impairment take the carrying amount of PPE assets that exceeds its recoverable

amount. The carrying amount is analysed the value of the assets that mentioned in the balance

sheet after the accumulation depreciation and impairment losses.

CONCLUSION

As per the above report it has been concluded that advanced financial accounting use by

the organisations to present all the financial reports in effective manner. On the basis of this

report users determine the financial position of company and take effective investment decision.

Along with analysis the nature of conceptual framework of company and different advantages

achieve by the organisations. There are mentioned list of plant & property use by the company in

a financial year apply impairment assessment of assets. Moreover, differentiate the revenues and

gains and beneficial for users to identify actual position of business effectively.

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Christensen, H.B., Nikolaev, V.V. and Wittenberg‐Moerman, R., 2016. Accounting information

in financial contracting: The incomplete contract theory perspective. Journal of

accounting research. 54(2). pp.397-435.

Ciapessoni, E. and et.al, 2019. An advanced platform for power system security assessment

accounting for forecast uncertainties. International Journal of Management and

Decision Making. 18(3). pp.257-281.

Cobb, J. L., 2016. Critical and reflective thinking in an intermediate financial accounting course:

an action research study. Texas Christian University dissertation.

Ibrahim, A. and Haruna, J. A., 2017. Effects of flipped and conventional teaching approaches on

performance and retention ability of students in advance financial accounting in

AbuBakar Tafawa Balewa University Bauchi, Nigeria. Jurnal Psikologi Malaysia.

31(2).

Nicholls, J. A., 2020. Integrating financial, social and environmental accounting. Sustainability

Accounting, Management and Policy Journal.

Saud, S., Chen, S. and Haseeb, A., 2020. The role of financial development and globalization in

the environment: Accounting ecological footprint indicators for selected one-belt-one-

road initiative countries. Journal of Cleaner Production. 250. p.119518.

Stone, E. J., 2020. An Analysis of the Fundamentals and Professional Applications of Financial

Accounting.

Watkins, A., 2020. An Analysis of Case Studies Related to Financial Accounting Concepts and

Methods.

Yaakob, T.B.S.T., Yusoff, W.Z.W. and Yusoff, C.A.M., 2019. INNOVATION OF DPA6013

FINANCIAL ACCOUNTING 4 LEARNING SYSTEM USING HYBRID

APPLICATION FA4v1. International Journal Of Technical Vocational And

Engineering Technology (iJTveT). 1(1). pp.8-15.

8

Books and Journals

Christensen, H.B., Nikolaev, V.V. and Wittenberg‐Moerman, R., 2016. Accounting information

in financial contracting: The incomplete contract theory perspective. Journal of

accounting research. 54(2). pp.397-435.

Ciapessoni, E. and et.al, 2019. An advanced platform for power system security assessment

accounting for forecast uncertainties. International Journal of Management and

Decision Making. 18(3). pp.257-281.

Cobb, J. L., 2016. Critical and reflective thinking in an intermediate financial accounting course:

an action research study. Texas Christian University dissertation.

Ibrahim, A. and Haruna, J. A., 2017. Effects of flipped and conventional teaching approaches on

performance and retention ability of students in advance financial accounting in

AbuBakar Tafawa Balewa University Bauchi, Nigeria. Jurnal Psikologi Malaysia.

31(2).

Nicholls, J. A., 2020. Integrating financial, social and environmental accounting. Sustainability

Accounting, Management and Policy Journal.

Saud, S., Chen, S. and Haseeb, A., 2020. The role of financial development and globalization in

the environment: Accounting ecological footprint indicators for selected one-belt-one-

road initiative countries. Journal of Cleaner Production. 250. p.119518.

Stone, E. J., 2020. An Analysis of the Fundamentals and Professional Applications of Financial

Accounting.

Watkins, A., 2020. An Analysis of Case Studies Related to Financial Accounting Concepts and

Methods.

Yaakob, T.B.S.T., Yusoff, W.Z.W. and Yusoff, C.A.M., 2019. INNOVATION OF DPA6013

FINANCIAL ACCOUNTING 4 LEARNING SYSTEM USING HYBRID

APPLICATION FA4v1. International Journal Of Technical Vocational And

Engineering Technology (iJTveT). 1(1). pp.8-15.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.