Financial Accounting Report: Analysis of Barclays Financial Statements

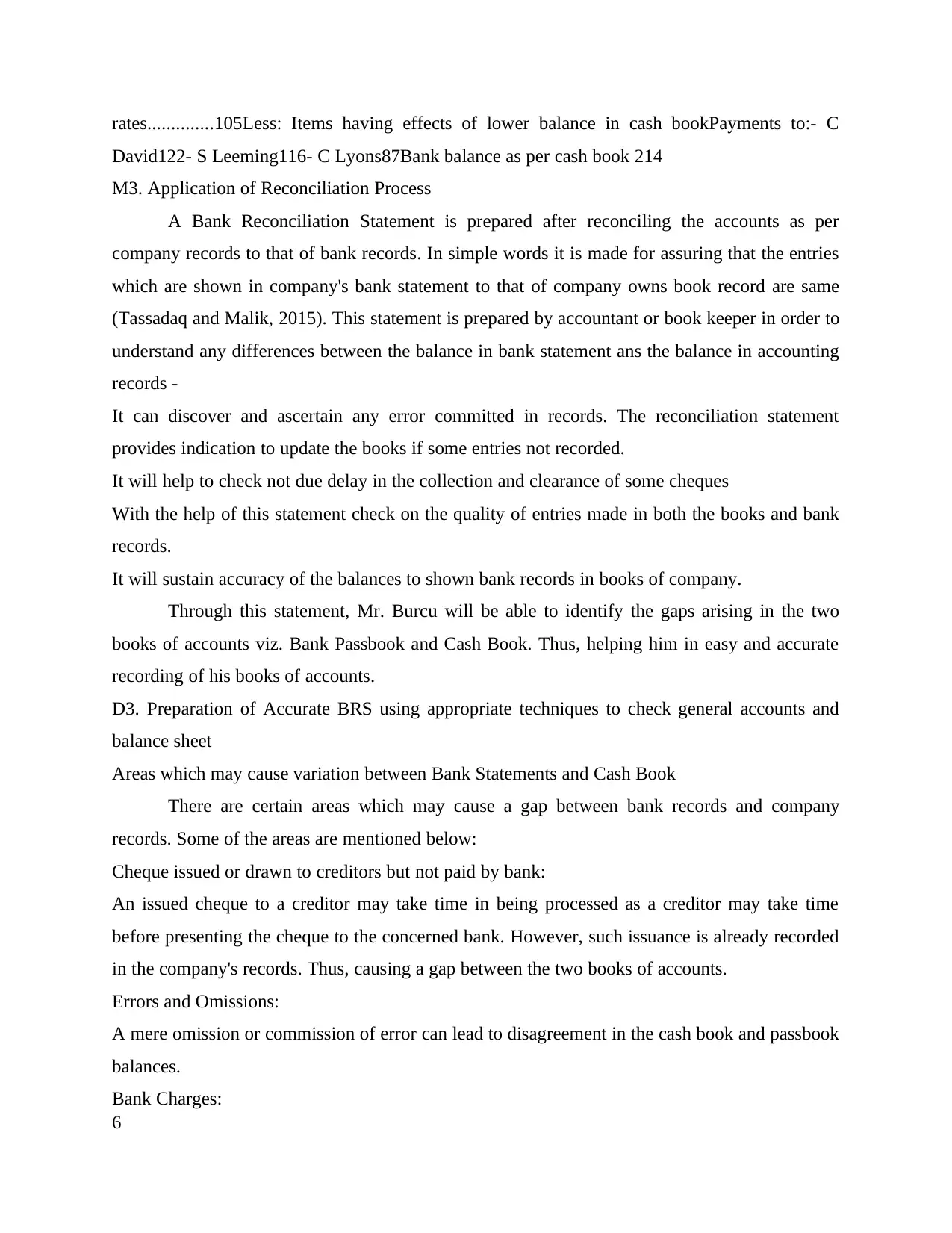

VerifiedAdded on 2023/02/02

|12

|3345

|87

Report

AI Summary

This financial accounting report begins with an introduction to financial accounting, defining its purpose and importance for both internal and external stakeholders, using Barclays as a case study. Part A presents a business report analyzing Barclays' financial accounting practices, including the roles of employees, management, vendors, financial institutions, customers, and investors. Part B delves into practical applications, covering double-entry bookkeeping, trial balance preparation, and the creation of final accounts like the balance sheet and income statement. The report also addresses depreciation methods and the application of bank reconciliation statements. The report includes practical examples, such as trial balances and profit and loss statements, and explores the reconciliation process, including the analysis of potential discrepancies between bank statements and company records, like errors, omissions, and bank charges. Finally, the report explores the process of reconciling control accounts and clearing suspense accounts and concludes with a discussion of different types of accounts, and the preparation of accurate reconciled accounts.

FINANCIAL ACCOUNTING

Table of Contents

μINTRODUCTION 1

PART A 1

Business Report 1

(a) Financial Accounting and it's Purpose 1

(b) Internal and External Stakeholders 2

PART B 4

P1 Application of Double-entry Book-keeping System to record sales and purchase transactions

4

P2. Preparation of Trial Balance 13

M1. Analysing transactions showing progression from previous to current trial balance 13

D1. Application of trial balance figures showing their position in statement of final accounts

14

P3. Prepare final accounts from trial balance 15

P4. Produce final accounts 16

M2. Adjusted Balances of Sum of Accounts before preparation of final accounts 20

D2. Comparing essential features of each financial account statement 20

P5. Apply the Bank Reconciliation Statement 20

M3. Application of Reconciliation Process 21

D3. Preparation of Accurate BRS using appropriate techniques to check general accounts and

balance sheet 22

P6. The process taken to reconcile control accounts and clear suspense accounts 23

M4. Understanding of different type of accounts 24

D4. Accurate Reconciled Accounts through application of appropriate techniques 24

CONCLUSION 25

Table of Contents

μINTRODUCTION 1

PART A 1

Business Report 1

(a) Financial Accounting and it's Purpose 1

(b) Internal and External Stakeholders 2

PART B 4

P1 Application of Double-entry Book-keeping System to record sales and purchase transactions

4

P2. Preparation of Trial Balance 13

M1. Analysing transactions showing progression from previous to current trial balance 13

D1. Application of trial balance figures showing their position in statement of final accounts

14

P3. Prepare final accounts from trial balance 15

P4. Produce final accounts 16

M2. Adjusted Balances of Sum of Accounts before preparation of final accounts 20

D2. Comparing essential features of each financial account statement 20

P5. Apply the Bank Reconciliation Statement 20

M3. Application of Reconciliation Process 21

D3. Preparation of Accurate BRS using appropriate techniques to check general accounts and

balance sheet 22

P6. The process taken to reconcile control accounts and clear suspense accounts 23

M4. Understanding of different type of accounts 24

D4. Accurate Reconciled Accounts through application of appropriate techniques 24

CONCLUSION 25

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES 26

INTRODUCTION

Financial accounting can be defined as the study of recording, journalising, summarizing

and reporting of financial transactions (Iatridis and Dimitras, 2013). Such reports are useful both

internal ans external shareholders who have different interest in regards to the financial

information presented. This report is divided into two parts A & B. In the part A, a business

report has been prepared in regards to Barclays. In the part B, various financial transactions of

sole trading, partnership and companies have been recorded to prepare final accounts such as

balance sheet, income statement and trial balance.

PART A

Business Report

(a) Financial Accounting and it's Purpose

Financial accounting is an accounting field that deals with company's financial

transactions. It mainly concerned with recording, classifying, summarizing and analysing day to

day proceedings in the books of accounts. These statement can be used for multi purpose. It

helps in determining the fiscal position of business (Edwards, Schwab and Shevlin, 2015).

Stockholders, customers are public the external elements they wants to gather information

regarding organization performance before investing in it therefore these statements are used by

them. Barclays an investment banking company uses such systems effectively to asses the

economical condition of organisation.

Let's discuss in details about the purpose of preparing such statements

Recording- The first and foremost purpose of accounting is to maintained and keeping the track

of all the transactions in systematic manner. Data related to organisation dealing with creditors

and debtors can be evaluated at any point of time. Barclays make sure that it records all the

contents in journal and ledger books.

Planning- It is prepared by management to analyse information and planning in advance about

the materials, resources required for future purpose. It ensured company does is braced to handle

issues whenever they occurs (Kim and Zhang, 2016). Barclays plans budgets and ensures

maintenance of necessary requirements.

Decision Making- Managers take effective decision after studying financial status of firm. These

statements provides them details about various alternatives available and potential of them so

1

Financial accounting can be defined as the study of recording, journalising, summarizing

and reporting of financial transactions (Iatridis and Dimitras, 2013). Such reports are useful both

internal ans external shareholders who have different interest in regards to the financial

information presented. This report is divided into two parts A & B. In the part A, a business

report has been prepared in regards to Barclays. In the part B, various financial transactions of

sole trading, partnership and companies have been recorded to prepare final accounts such as

balance sheet, income statement and trial balance.

PART A

Business Report

(a) Financial Accounting and it's Purpose

Financial accounting is an accounting field that deals with company's financial

transactions. It mainly concerned with recording, classifying, summarizing and analysing day to

day proceedings in the books of accounts. These statement can be used for multi purpose. It

helps in determining the fiscal position of business (Edwards, Schwab and Shevlin, 2015).

Stockholders, customers are public the external elements they wants to gather information

regarding organization performance before investing in it therefore these statements are used by

them. Barclays an investment banking company uses such systems effectively to asses the

economical condition of organisation.

Let's discuss in details about the purpose of preparing such statements

Recording- The first and foremost purpose of accounting is to maintained and keeping the track

of all the transactions in systematic manner. Data related to organisation dealing with creditors

and debtors can be evaluated at any point of time. Barclays make sure that it records all the

contents in journal and ledger books.

Planning- It is prepared by management to analyse information and planning in advance about

the materials, resources required for future purpose. It ensured company does is braced to handle

issues whenever they occurs (Kim and Zhang, 2016). Barclays plans budgets and ensures

maintenance of necessary requirements.

Decision Making- Managers take effective decision after studying financial status of firm. These

statements provides them details about various alternatives available and potential of them so

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that company can avail profits by using them. Barclays has to take decisions about prospective

monetary sources and how much investment is required.

Performance- Acquiring info about company's performance based on how much sales, profits

and revenue has been earned within an accounting period. Barclays builds itself from crises after

detecting the areas where it is lacking.

Liquidity- It is an important factor to analyse business state. Maintaining cash availability can be

assured with the help of such statements. Barclays manage working capital requirements after

the issues that it has faced in past.

(b) Internal and External Stakeholders

Internal Stakeholders:

Internal Stakeholders are those which are directly or indirectly related to the operational

process carried out in a business (Abernathy and et.al, 2014). The two main internal stakeholders

of Barclays that are likely to be impacted as well as would be interested in the financial

information of the organisation are:

Employees: Since a business is created by its employees, any business decision made by the

enterprise directly affects their economic well-being. Employees are interested in financial

information of Barclays as their livelihood depends on the level of performance exhibited by the

company in a given financial period.

Management: The top management of the business includes owners, board of directors as well as

the investors of Barclays. They are especially interested in such financial information as they

want to know whether their investments and efforts are being positively rewarded through profit

maximization.

External Stakeholders:

External Stakeholders are those individuals or groups that are external to an organisation

but have the power to affect or be affected by the operations of the business. The two main

external stakeholders of Barclays that would be interested in the financial information of the

organisation are:

Vendors: A Creditor includes any supplier or other parties from whom business is conducted on

a credit basis. Thus, Creditors of Barclays would be interested in their financial information so

as to sustain their business relationships by ascertaining the liquidity of the company. This is

2

monetary sources and how much investment is required.

Performance- Acquiring info about company's performance based on how much sales, profits

and revenue has been earned within an accounting period. Barclays builds itself from crises after

detecting the areas where it is lacking.

Liquidity- It is an important factor to analyse business state. Maintaining cash availability can be

assured with the help of such statements. Barclays manage working capital requirements after

the issues that it has faced in past.

(b) Internal and External Stakeholders

Internal Stakeholders:

Internal Stakeholders are those which are directly or indirectly related to the operational

process carried out in a business (Abernathy and et.al, 2014). The two main internal stakeholders

of Barclays that are likely to be impacted as well as would be interested in the financial

information of the organisation are:

Employees: Since a business is created by its employees, any business decision made by the

enterprise directly affects their economic well-being. Employees are interested in financial

information of Barclays as their livelihood depends on the level of performance exhibited by the

company in a given financial period.

Management: The top management of the business includes owners, board of directors as well as

the investors of Barclays. They are especially interested in such financial information as they

want to know whether their investments and efforts are being positively rewarded through profit

maximization.

External Stakeholders:

External Stakeholders are those individuals or groups that are external to an organisation

but have the power to affect or be affected by the operations of the business. The two main

external stakeholders of Barclays that would be interested in the financial information of the

organisation are:

Vendors: A Creditor includes any supplier or other parties from whom business is conducted on

a credit basis. Thus, Creditors of Barclays would be interested in their financial information so

as to sustain their business relationships by ascertaining the liquidity of the company. This is

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

important to them as liquidity would determine whether Barclays would be able to repay their

outstanding payments or not.

Financial Institutions: Since a business cannot invest the required working capital from its own

pockets, it may tend to take funding from institutions such as Banks. Therefore, these parties are

interested to know whether the business would be able to repay its loans or credit facilities on

time so as to avoid defaults.

Customers: Customers are the lifeblood of any organisation. A customer is interested to know

whether the business has been able to ascertain how socially responsive the company towards

them (Gupta, 2016).

Investors: Existing as well as Prospective Investors will be interested in knowing the financial

information of Barclays as it would indicate its financial performance, growth and returns that

company is capable of giving to them in the form of dividends.

Such requirements of internal as well as external stakeholders make them interested in

the financial information of any organisation including Barclays.

PART B

P1 Application of Double-entry Book-keeping System to record sales and purchase transactions

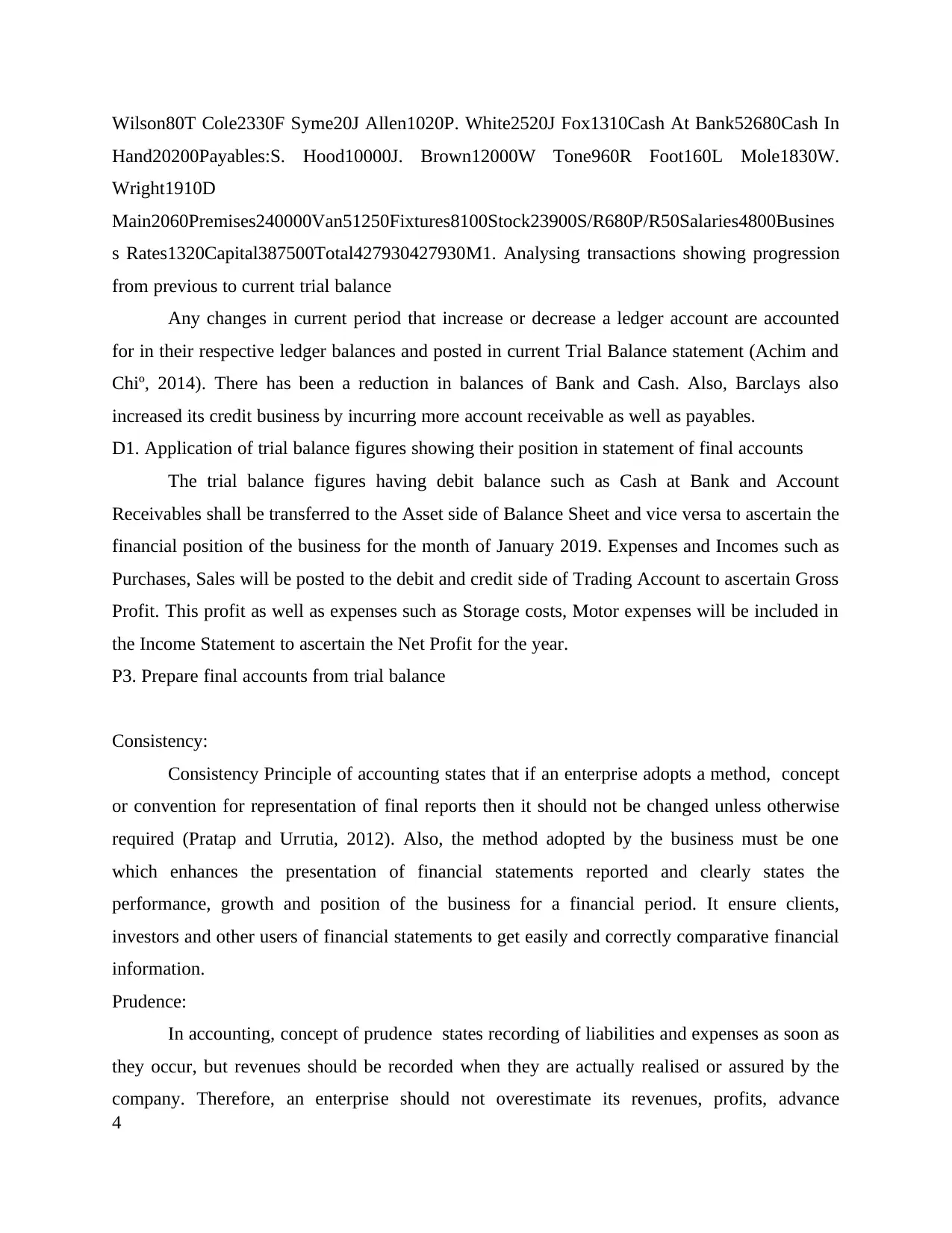

P2. Preparation of Trial Balance

Trial Balance for the month of 31st January 2019ParticularsDebitCreditStorage

Cost450Purchase9820Sales11460Motor Expenses470Receivables:P Mullen3000F Lane3980J

3

outstanding payments or not.

Financial Institutions: Since a business cannot invest the required working capital from its own

pockets, it may tend to take funding from institutions such as Banks. Therefore, these parties are

interested to know whether the business would be able to repay its loans or credit facilities on

time so as to avoid defaults.

Customers: Customers are the lifeblood of any organisation. A customer is interested to know

whether the business has been able to ascertain how socially responsive the company towards

them (Gupta, 2016).

Investors: Existing as well as Prospective Investors will be interested in knowing the financial

information of Barclays as it would indicate its financial performance, growth and returns that

company is capable of giving to them in the form of dividends.

Such requirements of internal as well as external stakeholders make them interested in

the financial information of any organisation including Barclays.

PART B

P1 Application of Double-entry Book-keeping System to record sales and purchase transactions

P2. Preparation of Trial Balance

Trial Balance for the month of 31st January 2019ParticularsDebitCreditStorage

Cost450Purchase9820Sales11460Motor Expenses470Receivables:P Mullen3000F Lane3980J

3

Wilson80T Cole2330F Syme20J Allen1020P. White2520J Fox1310Cash At Bank52680Cash In

Hand20200Payables:S. Hood10000J. Brown12000W Tone960R Foot160L Mole1830W.

Wright1910D

Main2060Premises240000Van51250Fixtures8100Stock23900S/R680P/R50Salaries4800Busines

s Rates1320Capital387500Total427930427930M1. Analysing transactions showing progression

from previous to current trial balance

Any changes in current period that increase or decrease a ledger account are accounted

for in their respective ledger balances and posted in current Trial Balance statement (Achim and

Chiº, 2014). There has been a reduction in balances of Bank and Cash. Also, Barclays also

increased its credit business by incurring more account receivable as well as payables.

D1. Application of trial balance figures showing their position in statement of final accounts

The trial balance figures having debit balance such as Cash at Bank and Account

Receivables shall be transferred to the Asset side of Balance Sheet and vice versa to ascertain the

financial position of the business for the month of January 2019. Expenses and Incomes such as

Purchases, Sales will be posted to the debit and credit side of Trading Account to ascertain Gross

Profit. This profit as well as expenses such as Storage costs, Motor expenses will be included in

the Income Statement to ascertain the Net Profit for the year.

P3. Prepare final accounts from trial balance

Consistency:

Consistency Principle of accounting states that if an enterprise adopts a method, concept

or convention for representation of final reports then it should not be changed unless otherwise

required (Pratap and Urrutia, 2012). Also, the method adopted by the business must be one

which enhances the presentation of financial statements reported and clearly states the

performance, growth and position of the business for a financial period. It ensure clients,

investors and other users of financial statements to get easily and correctly comparative financial

information.

Prudence:

In accounting, concept of prudence states recording of liabilities and expenses as soon as

they occur, but revenues should be recorded when they are actually realised or assured by the

company. Therefore, an enterprise should not overestimate its revenues, profits, advance

4

Hand20200Payables:S. Hood10000J. Brown12000W Tone960R Foot160L Mole1830W.

Wright1910D

Main2060Premises240000Van51250Fixtures8100Stock23900S/R680P/R50Salaries4800Busines

s Rates1320Capital387500Total427930427930M1. Analysing transactions showing progression

from previous to current trial balance

Any changes in current period that increase or decrease a ledger account are accounted

for in their respective ledger balances and posted in current Trial Balance statement (Achim and

Chiº, 2014). There has been a reduction in balances of Bank and Cash. Also, Barclays also

increased its credit business by incurring more account receivable as well as payables.

D1. Application of trial balance figures showing their position in statement of final accounts

The trial balance figures having debit balance such as Cash at Bank and Account

Receivables shall be transferred to the Asset side of Balance Sheet and vice versa to ascertain the

financial position of the business for the month of January 2019. Expenses and Incomes such as

Purchases, Sales will be posted to the debit and credit side of Trading Account to ascertain Gross

Profit. This profit as well as expenses such as Storage costs, Motor expenses will be included in

the Income Statement to ascertain the Net Profit for the year.

P3. Prepare final accounts from trial balance

Consistency:

Consistency Principle of accounting states that if an enterprise adopts a method, concept

or convention for representation of final reports then it should not be changed unless otherwise

required (Pratap and Urrutia, 2012). Also, the method adopted by the business must be one

which enhances the presentation of financial statements reported and clearly states the

performance, growth and position of the business for a financial period. It ensure clients,

investors and other users of financial statements to get easily and correctly comparative financial

information.

Prudence:

In accounting, concept of prudence states recording of liabilities and expenses as soon as

they occur, but revenues should be recorded when they are actually realised or assured by the

company. Therefore, an enterprise should not overestimate its revenues, profits, advance

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

incomes and assets and underestimate its expenses, losses and liabilities. This concept gives rise

to creation of Provisions and Reserves Account in the organisation (Velte and Freidank, 2015).

P4. Produce final accounts

Profit and loss statement for the sole trader Ebay

Balance sheet of sole trader of Ebay

Income statement of partnership company

Balance sheet

M2. Adjusted Balances of Sum of Accounts before preparation of final accounts

Depreciation refers to the decline in the cost of assets due to wear and tear, obsolescence,

etc. Its purpose is to match costs of a capital assets to the revenues earned from it. The two most

widely used methods are Written-Down Value (WDV) and Straight Line Method (SLM). The

WDV method is used when assets require negligible repairs and maintenance such as leases and

vice versa (Amiram, 2012).

D2. Comparing essential features of each financial account statement

P5. Apply the Bank Reconciliation Statement

Debit Corrected Cash Book (Bank) Credit££31-DecBalance

b/d19,973 Overstated

amount1Overstated

amount9 Bank charges47 Standing order137 310923 (Direct D)297 Balance

c/f19,500 19,982 19,982Balance b/d19,500

ParticularsAmount- Bank Balance as per pass book398Add: Items having effects of higher

balance in cash book- Bank charges not recorded in cash book...36- Adjustment for direct debit

5

to creation of Provisions and Reserves Account in the organisation (Velte and Freidank, 2015).

P4. Produce final accounts

Profit and loss statement for the sole trader Ebay

Balance sheet of sole trader of Ebay

Income statement of partnership company

Balance sheet

M2. Adjusted Balances of Sum of Accounts before preparation of final accounts

Depreciation refers to the decline in the cost of assets due to wear and tear, obsolescence,

etc. Its purpose is to match costs of a capital assets to the revenues earned from it. The two most

widely used methods are Written-Down Value (WDV) and Straight Line Method (SLM). The

WDV method is used when assets require negligible repairs and maintenance such as leases and

vice versa (Amiram, 2012).

D2. Comparing essential features of each financial account statement

P5. Apply the Bank Reconciliation Statement

Debit Corrected Cash Book (Bank) Credit££31-DecBalance

b/d19,973 Overstated

amount1Overstated

amount9 Bank charges47 Standing order137 310923 (Direct D)297 Balance

c/f19,500 19,982 19,982Balance b/d19,500

ParticularsAmount- Bank Balance as per pass book398Add: Items having effects of higher

balance in cash book- Bank charges not recorded in cash book...36- Adjustment for direct debit

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

rates..............105Less: Items having effects of lower balance in cash bookPayments to:- C

David122- S Leeming116- C Lyons87Bank balance as per cash book 214

M3. Application of Reconciliation Process

A Bank Reconciliation Statement is prepared after reconciling the accounts as per

company records to that of bank records. In simple words it is made for assuring that the entries

which are shown in company's bank statement to that of company owns book record are same

(Tassadaq and Malik, 2015). This statement is prepared by accountant or book keeper in order to

understand any differences between the balance in bank statement ans the balance in accounting

records -

It can discover and ascertain any error committed in records. The reconciliation statement

provides indication to update the books if some entries not recorded.

It will help to check not due delay in the collection and clearance of some cheques

With the help of this statement check on the quality of entries made in both the books and bank

records.

It will sustain accuracy of the balances to shown bank records in books of company.

Through this statement, Mr. Burcu will be able to identify the gaps arising in the two

books of accounts viz. Bank Passbook and Cash Book. Thus, helping him in easy and accurate

recording of his books of accounts.

D3. Preparation of Accurate BRS using appropriate techniques to check general accounts and

balance sheet

Areas which may cause variation between Bank Statements and Cash Book

There are certain areas which may cause a gap between bank records and company

records. Some of the areas are mentioned below:

Cheque issued or drawn to creditors but not paid by bank:

An issued cheque to a creditor may take time in being processed as a creditor may take time

before presenting the cheque to the concerned bank. However, such issuance is already recorded

in the company's records. Thus, causing a gap between the two books of accounts.

Errors and Omissions:

A mere omission or commission of error can lead to disagreement in the cash book and passbook

balances.

Bank Charges:

6

David122- S Leeming116- C Lyons87Bank balance as per cash book 214

M3. Application of Reconciliation Process

A Bank Reconciliation Statement is prepared after reconciling the accounts as per

company records to that of bank records. In simple words it is made for assuring that the entries

which are shown in company's bank statement to that of company owns book record are same

(Tassadaq and Malik, 2015). This statement is prepared by accountant or book keeper in order to

understand any differences between the balance in bank statement ans the balance in accounting

records -

It can discover and ascertain any error committed in records. The reconciliation statement

provides indication to update the books if some entries not recorded.

It will help to check not due delay in the collection and clearance of some cheques

With the help of this statement check on the quality of entries made in both the books and bank

records.

It will sustain accuracy of the balances to shown bank records in books of company.

Through this statement, Mr. Burcu will be able to identify the gaps arising in the two

books of accounts viz. Bank Passbook and Cash Book. Thus, helping him in easy and accurate

recording of his books of accounts.

D3. Preparation of Accurate BRS using appropriate techniques to check general accounts and

balance sheet

Areas which may cause variation between Bank Statements and Cash Book

There are certain areas which may cause a gap between bank records and company

records. Some of the areas are mentioned below:

Cheque issued or drawn to creditors but not paid by bank:

An issued cheque to a creditor may take time in being processed as a creditor may take time

before presenting the cheque to the concerned bank. However, such issuance is already recorded

in the company's records. Thus, causing a gap between the two books of accounts.

Errors and Omissions:

A mere omission or commission of error can lead to disagreement in the cash book and passbook

balances.

Bank Charges:

6

Bank charges a certain amount for the facilities provided to the account-holders such as

overdraft. This leads to a decrease in company's passbook balance. However, until notified, such

charges remain absent from company records leading to disagreement between the two.

Interest on Deposits:

A bank collects and credits accounts of its users with interest earned by them on their accounts.

This leads to a change in credit balance of the account-holders. However, the cash records

remain unchanged leading to a variation between two books of records.

Collection of Income by Bank:

A bank collects and credits accounts of its users with incomes such as dividend on shares and

interest earned on government securities directly. This leads to an incremental effect on the

Bank's account whereas the cash records remain unaffected until the information is retrieved in

the form of passbook from Banks.

Direct Payment of Expenses by Bank:

Expenses such as Insurance Premium, Factory Rent, trade subscriptions, etc. may be paid by the

Bank directly on behalf of the company. Such payments would reduce the company's bank

records with an equivalent amount leading to a variation between passbook and cash-book until

such changes are intimated to the company.

Direct Deposits made by Debtors into the Bank:

Sometimes a debtor may directly deposit the payment owed by them in the company's bank

account. This would result in an increase in the credit balance of organisation's bank account.

However, such a change will be recorded only after the bank statement is retrieved, resulting in a

gap between the two.

Imprest System

The imprest system is an accounting system which is used to track and document how

cash is being spent (Moser, 2012). For this system, most common example is that of petty cash

system, under which the general ledger account Petty Cash remains dormant or unchanged and

will be known as 'Imprest balance'.

P6. The process taken to reconcile control accounts and clear suspense accounts

Control account is that branch of ledger accounting that concerned with recording of

accounting receivable. It keeps a track of overall collections from customers. Subsidiary ledger

7

overdraft. This leads to a decrease in company's passbook balance. However, until notified, such

charges remain absent from company records leading to disagreement between the two.

Interest on Deposits:

A bank collects and credits accounts of its users with interest earned by them on their accounts.

This leads to a change in credit balance of the account-holders. However, the cash records

remain unchanged leading to a variation between two books of records.

Collection of Income by Bank:

A bank collects and credits accounts of its users with incomes such as dividend on shares and

interest earned on government securities directly. This leads to an incremental effect on the

Bank's account whereas the cash records remain unaffected until the information is retrieved in

the form of passbook from Banks.

Direct Payment of Expenses by Bank:

Expenses such as Insurance Premium, Factory Rent, trade subscriptions, etc. may be paid by the

Bank directly on behalf of the company. Such payments would reduce the company's bank

records with an equivalent amount leading to a variation between passbook and cash-book until

such changes are intimated to the company.

Direct Deposits made by Debtors into the Bank:

Sometimes a debtor may directly deposit the payment owed by them in the company's bank

account. This would result in an increase in the credit balance of organisation's bank account.

However, such a change will be recorded only after the bank statement is retrieved, resulting in a

gap between the two.

Imprest System

The imprest system is an accounting system which is used to track and document how

cash is being spent (Moser, 2012). For this system, most common example is that of petty cash

system, under which the general ledger account Petty Cash remains dormant or unchanged and

will be known as 'Imprest balance'.

P6. The process taken to reconcile control accounts and clear suspense accounts

Control account is that branch of ledger accounting that concerned with recording of

accounting receivable. It keeps a track of overall collections from customers. Subsidiary ledger

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

derive transactions from this account which helps in maintaining equilibrium in trial in trial

balance. These accounts can be divided into two main accounts:

Purchase ledger control account- This account is prepared to keep record of all credit purchase

related transactions.

Sales ledger control account- This account is prepared to keep record of all credit purchase

related transactions.

In order to reconcile these control accounts, the business needs to verify that the entries

made in sales and purchase ledgers match the balances produced in the above mentioned

accounts. To clear suspense accounts, verification of such accounts is made with the General

Ledger entries. If there's any discrepancy arising, they are relocated and corrected in both

accounts to ensure accuracy.

M4. Understanding of different type of accounts

Purchase ledger control account- This account is prepared when client buys goods on credit

basis. It keeps record and manage transactions of suppliers who has not made payment in cash. It

shows complete information of the amount owed by them. Nowadays it is prepared on software

systems which makes more accurate and reliable (Nikolaou, I. and Evangelinos, 2012).

Sales ledger control account- It maintained records of sales in the form of sales invoice, sales

credit and payments received in cash. It is also prepared in general ledger. Purpose of this

account is to evaluates how much money does the organisation owned.

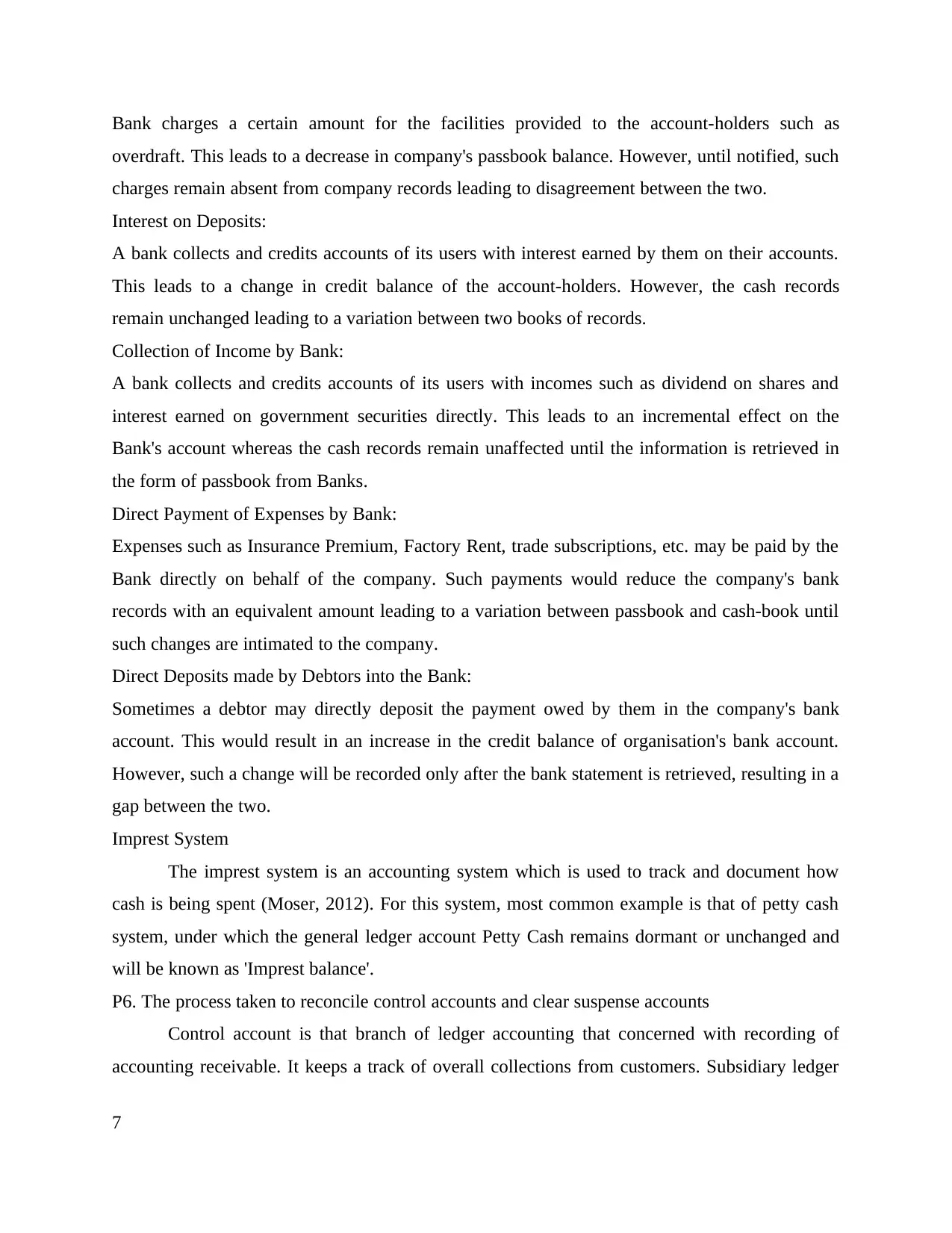

D4. Accurate Reconciled Accounts through application of appropriate techniques

Sales Ledger Control AccountParticularsAmount (£)ParticularsAmount (£)Balance

b/d12600S/R4320Cr. Sales152350Bad Debts1600Discount Allowed1060Bank/ Cash (Receipt

from credit customers)120610Set-off (Transfer to purchase ledger).640Balance

c/d.................36720Total 164950Total 164950Balance b/d36720

Purchase Ledger Control A/cParticularsAmount (£)ParticularsAmount (£)Discount

Received...850Balance b/d11360P/R3110Credit Purchase126500Bank/ Cash (Payment to

suppliers)91010Bank (Refund from supplier)500Set-off (Transfer from sales ledger)640Balance

c/d42750Total138360Total138360Balance b/d42750CONCLUSION

As per the above discussion it has been concluded that financial accounting is essential

part of any organisation which is shows actual performance of a company and help in decision

8

balance. These accounts can be divided into two main accounts:

Purchase ledger control account- This account is prepared to keep record of all credit purchase

related transactions.

Sales ledger control account- This account is prepared to keep record of all credit purchase

related transactions.

In order to reconcile these control accounts, the business needs to verify that the entries

made in sales and purchase ledgers match the balances produced in the above mentioned

accounts. To clear suspense accounts, verification of such accounts is made with the General

Ledger entries. If there's any discrepancy arising, they are relocated and corrected in both

accounts to ensure accuracy.

M4. Understanding of different type of accounts

Purchase ledger control account- This account is prepared when client buys goods on credit

basis. It keeps record and manage transactions of suppliers who has not made payment in cash. It

shows complete information of the amount owed by them. Nowadays it is prepared on software

systems which makes more accurate and reliable (Nikolaou, I. and Evangelinos, 2012).

Sales ledger control account- It maintained records of sales in the form of sales invoice, sales

credit and payments received in cash. It is also prepared in general ledger. Purpose of this

account is to evaluates how much money does the organisation owned.

D4. Accurate Reconciled Accounts through application of appropriate techniques

Sales Ledger Control AccountParticularsAmount (£)ParticularsAmount (£)Balance

b/d12600S/R4320Cr. Sales152350Bad Debts1600Discount Allowed1060Bank/ Cash (Receipt

from credit customers)120610Set-off (Transfer to purchase ledger).640Balance

c/d.................36720Total 164950Total 164950Balance b/d36720

Purchase Ledger Control A/cParticularsAmount (£)ParticularsAmount (£)Discount

Received...850Balance b/d11360P/R3110Credit Purchase126500Bank/ Cash (Payment to

suppliers)91010Bank (Refund from supplier)500Set-off (Transfer from sales ledger)640Balance

c/d42750Total138360Total138360Balance b/d42750CONCLUSION

As per the above discussion it has been concluded that financial accounting is essential

part of any organisation which is shows actual performance of a company and help in decision

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

making process. With the help of accounting prepare different types of financial statement which

is presented in front of internal and external stakeholders. There is produce balance, ledger

accounts and trial balance to show position of a company and reconcile of bank statement.

REFERENCES

Books and Journals

Iatridis, G. and Dimitras, A. I., 2013. Financial crisis and accounting quality: evidence from five

European countries. Advances in Accounting, 29(1), pp.154-160.

Edwards, A., Schwab, C. and Shevlin, T., 2015. Financial constraints and cash tax savings. The

Accounting Review. 91(3). pp.859-881.

Kim, J. B. and Zhang, L., 2016. Accounting conservatism and stock price crash risk: Firm-level

evidence. Contemporary Accounting Research. 33(1). pp.412-441.

Abernathy, J. L. And et.al, 2014. The association between characteristics of audit committee

accounting experts, audit committee chairs, and financial reporting timeliness. Advances in

Accounting. 30(2). pp.283-297.

Gupta, A., 2016. Financial Accounting for Management. Pearson Education India.

Achim, A. M. and Chiº, A. O., 2014. FINANCIAL ACCOUNTING QUALITY AND ITS

DEFINING CHARACTERISTICS. SEA: Practical Application of Science. 2(3).

Pratap, S. and Urrutia, C., 2012. Financial frictions and total factor productivity: Accounting for

the real effects of financial crises. Review of Economic Dynamics. 15(3). pp.336-358.

Velte, P. and Freidank, C. C., 2015. The link between in-and external rotation of the auditor and

the quality of financial accounting and external audit. European journal of law and economics.

40(2). pp.225-246.

Amiram, D., 2012. Financial information globalization and foreign investment decisions. Journal

of International Accounting Research. 11(2). pp.57-81.

Tassadaq, F. and Malik, Q. A., 2015. Creative Accounting & Financial Reporting: Model

Development & Empirical Testing. International Journal of Economics and Financial Issues.

5(2). pp.544-551.

Moser, D. V., 2012. Is accounting research stagnant?. Accounting Horizons. 26(4). pp.845-850.

Nikolaou, I. and Evangelinos, K., 2012. Financial and non-financial environmental information:

significant factors for corporate environmental performance measuring. International Journal of

Managerial and Financial Accounting. 4(1). pp.61-77.

9

is presented in front of internal and external stakeholders. There is produce balance, ledger

accounts and trial balance to show position of a company and reconcile of bank statement.

REFERENCES

Books and Journals

Iatridis, G. and Dimitras, A. I., 2013. Financial crisis and accounting quality: evidence from five

European countries. Advances in Accounting, 29(1), pp.154-160.

Edwards, A., Schwab, C. and Shevlin, T., 2015. Financial constraints and cash tax savings. The

Accounting Review. 91(3). pp.859-881.

Kim, J. B. and Zhang, L., 2016. Accounting conservatism and stock price crash risk: Firm-level

evidence. Contemporary Accounting Research. 33(1). pp.412-441.

Abernathy, J. L. And et.al, 2014. The association between characteristics of audit committee

accounting experts, audit committee chairs, and financial reporting timeliness. Advances in

Accounting. 30(2). pp.283-297.

Gupta, A., 2016. Financial Accounting for Management. Pearson Education India.

Achim, A. M. and Chiº, A. O., 2014. FINANCIAL ACCOUNTING QUALITY AND ITS

DEFINING CHARACTERISTICS. SEA: Practical Application of Science. 2(3).

Pratap, S. and Urrutia, C., 2012. Financial frictions and total factor productivity: Accounting for

the real effects of financial crises. Review of Economic Dynamics. 15(3). pp.336-358.

Velte, P. and Freidank, C. C., 2015. The link between in-and external rotation of the auditor and

the quality of financial accounting and external audit. European journal of law and economics.

40(2). pp.225-246.

Amiram, D., 2012. Financial information globalization and foreign investment decisions. Journal

of International Accounting Research. 11(2). pp.57-81.

Tassadaq, F. and Malik, Q. A., 2015. Creative Accounting & Financial Reporting: Model

Development & Empirical Testing. International Journal of Economics and Financial Issues.

5(2). pp.544-551.

Moser, D. V., 2012. Is accounting research stagnant?. Accounting Horizons. 26(4). pp.845-850.

Nikolaou, I. and Evangelinos, K., 2012. Financial and non-financial environmental information:

significant factors for corporate environmental performance measuring. International Journal of

Managerial and Financial Accounting. 4(1). pp.61-77.

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.