Financial Accounting: Principles, Statements, and Analysis Report

VerifiedAdded on 2020/11/23

|28

|2966

|79

Report

AI Summary

This financial accounting report provides a comprehensive overview of financial accounting principles and their practical applications. It begins with an introduction to financial accounting, its purpose, and its importance to internal and external stakeholders. The report then delves into various aspects of accounting, including journal entries, ledgers, trial balances, and the preparation of financial statements such as the statement of profit and loss and balance sheets. It explores key concepts like consistency, prudence, and depreciation methods. Furthermore, the report covers bank reconciliation statements, control accounts, and suspense accounts, along with a discussion on the differences between financial statements prepared by sole traders and limited companies. The report uses examples from different clients to illustrate accounting practices, making it a valuable resource for students and professionals seeking to understand and apply financial accounting principles. It concludes with a summary of the key takeaways and a list of references.

FINANCIAL

ACCOUNTING

PRINCIPAL

ACCOUNTING

PRINCIPAL

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENT

INTRODUCTION...........................................................................................................................4

Report...............................................................................................................................................4

Financial accounting and its purpose..........................................................................................4

Importance of financial information to internal and external stakeholders................................5

CLIENT 1........................................................................................................................................8

a. Journal entries and books of accounts.....................................................................................8

b. Ledger...................................................................................................................................11

........................................................................................................................................................14

c. Trial balance..........................................................................................................................21

...................................................................................................................................................21

CLIENT 2......................................................................................................................................22

a. Statement of profit and loss...................................................................................................22

b. Balance sheet of firm............................................................................................................23

c. Consistency and prudence concept........................................................................................24

d. Purpose of depreciation and its methods...............................................................................24

e. Difference between financial statement prepared by sole trader and limited company........24

CLIENT 3......................................................................................................................................25

a. Purpose of bank reconciliation statement .............................................................................25

b. Areas which may cause record vary from bank statement....................................................25

c. Term 'imprest' in petty cash book..........................................................................................25

d. Bank reconcilliation statement ............................................................................................25

CLIENT 4......................................................................................................................................26

a. Sales ledger account and purchase ledger account................................................................26

b. Need of control account .......................................................................................................27

CLIENT 5......................................................................................................................................28

a. Suspense account and its features.........................................................................................28

b. Suspense account calculation................................................................................................28

CONCLUSION..............................................................................................................................28

REFERENCES..............................................................................................................................30

INTRODUCTION...........................................................................................................................4

Report...............................................................................................................................................4

Financial accounting and its purpose..........................................................................................4

Importance of financial information to internal and external stakeholders................................5

CLIENT 1........................................................................................................................................8

a. Journal entries and books of accounts.....................................................................................8

b. Ledger...................................................................................................................................11

........................................................................................................................................................14

c. Trial balance..........................................................................................................................21

...................................................................................................................................................21

CLIENT 2......................................................................................................................................22

a. Statement of profit and loss...................................................................................................22

b. Balance sheet of firm............................................................................................................23

c. Consistency and prudence concept........................................................................................24

d. Purpose of depreciation and its methods...............................................................................24

e. Difference between financial statement prepared by sole trader and limited company........24

CLIENT 3......................................................................................................................................25

a. Purpose of bank reconciliation statement .............................................................................25

b. Areas which may cause record vary from bank statement....................................................25

c. Term 'imprest' in petty cash book..........................................................................................25

d. Bank reconcilliation statement ............................................................................................25

CLIENT 4......................................................................................................................................26

a. Sales ledger account and purchase ledger account................................................................26

b. Need of control account .......................................................................................................27

CLIENT 5......................................................................................................................................28

a. Suspense account and its features.........................................................................................28

b. Suspense account calculation................................................................................................28

CONCLUSION..............................................................................................................................28

REFERENCES..............................................................................................................................30

INTRODUCTION

Financial accounting is a part of accounting that deals with financial transactions of

the company. Its purpose is to provide financial information to external users of the company.

Financial accounting has some generally accepted principles which allow financial manger to

work based on these rules. The report consists of purpose of financial accounting and its users.

It includes business transactions, final accounts for various types of traders along with bank

reconciliation statement and control accounts along with suspense account.

Report

Financial accounting and its purpose

It is the branch of accounting which records revenue of organisation, receipts, and also

expense of the company and measure them and prepare a report in the form of balance sheet

or income statement. Financial accounting helps in providing information to external as well

as internal users which includes owner, creditors, government, investors and other agencies. It

is known as the language of the business.

The basic structure of preparing financial accounts is identifying financial transactions

then measuring them in terms of money, recording them according the date of transactions,

classifying them in ledger and summarising them in balance sheet, cash flow or income

statement and then analysing them for interpretation and finally communicating them to the

users who wants information (Warren, 2018).

This also allows owner of business to analyses the financial condition of the company

and helps to allocate resources efficiently. Most companies uses GAAP for creating financial

statements but it is not a compulsion for private companies. Companies issues these

statements on regular basis so that external users can be aware about the position of the

company.

Financial accounting system is based on accrual basis as well as double entry system

of accounting. Double entry reflects that each transaction of the company have effect on two

accounts at least. Its advantage is that to have equal balance on both the sides of assets and

liabilities and balance is maintained at any point of time which lead to smooth operations of

the company.

Financial accounting is a part of accounting that deals with financial transactions of

the company. Its purpose is to provide financial information to external users of the company.

Financial accounting has some generally accepted principles which allow financial manger to

work based on these rules. The report consists of purpose of financial accounting and its users.

It includes business transactions, final accounts for various types of traders along with bank

reconciliation statement and control accounts along with suspense account.

Report

Financial accounting and its purpose

It is the branch of accounting which records revenue of organisation, receipts, and also

expense of the company and measure them and prepare a report in the form of balance sheet

or income statement. Financial accounting helps in providing information to external as well

as internal users which includes owner, creditors, government, investors and other agencies. It

is known as the language of the business.

The basic structure of preparing financial accounts is identifying financial transactions

then measuring them in terms of money, recording them according the date of transactions,

classifying them in ledger and summarising them in balance sheet, cash flow or income

statement and then analysing them for interpretation and finally communicating them to the

users who wants information (Warren, 2018).

This also allows owner of business to analyses the financial condition of the company

and helps to allocate resources efficiently. Most companies uses GAAP for creating financial

statements but it is not a compulsion for private companies. Companies issues these

statements on regular basis so that external users can be aware about the position of the

company.

Financial accounting system is based on accrual basis as well as double entry system

of accounting. Double entry reflects that each transaction of the company have effect on two

accounts at least. Its advantage is that to have equal balance on both the sides of assets and

liabilities and balance is maintained at any point of time which lead to smooth operations of

the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The other trait is accrual basis which reflects the idea of considering revenue when

they are actually earned by the company and not when money is received, and consider

expenses when they actually occur and not when they are paid (Hermanson, 2016). This helps

company to keep check on its profitability and assets and liabilities held by the company.

Purpose of financial accounting

The purpose of financial accounting is to provide information and statistics to internal

and external users about financial position of the company, cash inflow and outflow of the

company, and operational results of the company. The information helps the company to

allocate its resources efficiently where they are required ad help outsiders to decide whether to

invest in the company or not.

It helps investors to find out future perspective and prospectus of business. It also

helps employees to know that whether they are associated with profitable company or not and

help customers to know the condition of business. Financial reports help business to take

sound decisions that can lead to efficient working operations.

The financial statement is consists of 3 statements which offers different purposes. The

income statement of the company allow investors and others to know about the capability of

company to generate profits and it reveals sales turnover of the company as well as help in

analysing the trend of the company. The other statement is balance sheet which discloses the

financial position of the company and helps in estimating assets, liabilities and liquidity

position of the company to its users and company itself (Basioudis, 2019). At last comes the

statement of cash flows which helps in analysing nature of cash in the company by estimating

cash inflows and outflows.

The other purposes of financial accounting is to help company in taking credit

decisions, decisions related to investment and taxation decisions.

Importance of financial information to internal and external stakeholders

Financial accounting provides financial data to various individual and agencies. Each

of them is interested in different type of financial information. These are divided into internal

and external users of information which are creditors, investors, management, owner,

employees etc.

Internal users – These are individuals who are responsible to runs, operates and

manages day to day operations and activities of the company internally. It helps them to

they are actually earned by the company and not when money is received, and consider

expenses when they actually occur and not when they are paid (Hermanson, 2016). This helps

company to keep check on its profitability and assets and liabilities held by the company.

Purpose of financial accounting

The purpose of financial accounting is to provide information and statistics to internal

and external users about financial position of the company, cash inflow and outflow of the

company, and operational results of the company. The information helps the company to

allocate its resources efficiently where they are required ad help outsiders to decide whether to

invest in the company or not.

It helps investors to find out future perspective and prospectus of business. It also

helps employees to know that whether they are associated with profitable company or not and

help customers to know the condition of business. Financial reports help business to take

sound decisions that can lead to efficient working operations.

The financial statement is consists of 3 statements which offers different purposes. The

income statement of the company allow investors and others to know about the capability of

company to generate profits and it reveals sales turnover of the company as well as help in

analysing the trend of the company. The other statement is balance sheet which discloses the

financial position of the company and helps in estimating assets, liabilities and liquidity

position of the company to its users and company itself (Basioudis, 2019). At last comes the

statement of cash flows which helps in analysing nature of cash in the company by estimating

cash inflows and outflows.

The other purposes of financial accounting is to help company in taking credit

decisions, decisions related to investment and taxation decisions.

Importance of financial information to internal and external stakeholders

Financial accounting provides financial data to various individual and agencies. Each

of them is interested in different type of financial information. These are divided into internal

and external users of information which are creditors, investors, management, owner,

employees etc.

Internal users – These are individuals who are responsible to runs, operates and

manages day to day operations and activities of the company internally. It helps them to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

analyse profitability of company's products and operational units. It helps company and

management to decide need of cash flows to support and increase the efficient working of

operations.

It helps management to decide buy or sell a particular business segment and it helps

organisation to decide to expand new product line or to build new production facilities. The

user of international information are -

Management of the company – The most important user of information is the

management of the company because unless and until the management is not aware of

company's financial position decisions to improve the position cannot be made. Management

need accounting information to plan, implement and assess business decision. It helps

management to allocate its human as well as financial resources through creating specific

budgetary plans.

It helps in comparing past performance of the company with current performance and

analyse the competitive advantage and disadvantage and benchmarks of industry. It helps

management to take decisions regarding investment, pricing and financing. To have a better

understanding of financial information cash flows, balance sheets, income statements needs to

be updated and analyse by the management on regular basis.

Employees – Employees are the core part of organisation and each and every

employee needs information related to financial performance of the company. Firstly

employees engage in finance department needs to know the information for preparing various

reports as it is the part of their job (Brown, 2017.). Rest of the employees want to know the

financial position of the company because they work their and that can directly impact on

their income, salary, bonus and job security.

The other reason for employees to know the financial information is to have a better

understanding of the company's business that is it profitable or not. In addition to all this there

are also employees who are seeking to join the business needs information about the company

that it is worth joining or not.

External users – These are the users of information who presents outside the

organisation. These users can be investors, creditors, suppliers, government etc. The external

users need information to buy and sell shares of the company in case of profit and loss, to

provide loan to the entity in case of it have good financial position, To impose taxes on profits

management to decide need of cash flows to support and increase the efficient working of

operations.

It helps management to decide buy or sell a particular business segment and it helps

organisation to decide to expand new product line or to build new production facilities. The

user of international information are -

Management of the company – The most important user of information is the

management of the company because unless and until the management is not aware of

company's financial position decisions to improve the position cannot be made. Management

need accounting information to plan, implement and assess business decision. It helps

management to allocate its human as well as financial resources through creating specific

budgetary plans.

It helps in comparing past performance of the company with current performance and

analyse the competitive advantage and disadvantage and benchmarks of industry. It helps

management to take decisions regarding investment, pricing and financing. To have a better

understanding of financial information cash flows, balance sheets, income statements needs to

be updated and analyse by the management on regular basis.

Employees – Employees are the core part of organisation and each and every

employee needs information related to financial performance of the company. Firstly

employees engage in finance department needs to know the information for preparing various

reports as it is the part of their job (Brown, 2017.). Rest of the employees want to know the

financial position of the company because they work their and that can directly impact on

their income, salary, bonus and job security.

The other reason for employees to know the financial information is to have a better

understanding of the company's business that is it profitable or not. In addition to all this there

are also employees who are seeking to join the business needs information about the company

that it is worth joining or not.

External users – These are the users of information who presents outside the

organisation. These users can be investors, creditors, suppliers, government etc. The external

users need information to buy and sell shares of the company in case of profit and loss, to

provide loan to the entity in case of it have good financial position, To impose taxes on profits

by government and at last to have sales and purchase transactions with the company. The

external users are -

Government - Government needs financial information in order to see that company

has discloses its accounting information according to the accounting standards set by the

government in order to protect shareholders interest. It needs information to see that company

is working legally on fair basis and not conducting misdeeds. At last government needs to

know financial position of the company to impose tax on the net profit of the company.

Lenders – They need information to see credit worthiness of the company and ability

to pay back the loan. Lenders are important to business as they provide loan and financial

support to the company but after getting information on financial position of the company

(Narayanaswamy, 2017).

When company has high profitability, ability to pay liability and secured assets any

lender would give financial support to the company. On the contrary when company has poor

liquidity, lack of assets and no ability to pay back the liability it shows poor financial health of

the company.

Investors - The other most important user of external information are investors that

want to invest in the company or has already invested. They want to know how much return

they are getting on their investment and how well the company is performing. To know all the

details about their investment, to assess profitability, risk and return investors needs

information about financial statements.

It also helps existing investors to take decision on increase or decrease their investment based

on the performance of the company (Libby, 2017). It helps new investors to take a decision on

buying shares of the company based on its income statement and balance sheet.

Investment analysts – They require detail information on company's finances

especially those who are trading on stock exchange. They need information to analyse

performance of the competitors in the same business. They also gather information from

company's key person interviews and briefings. They help investors to compare the

investment and returns of different companies and projects their past trends and future trends

to show which company would more likely to generates high returns.

external users are -

Government - Government needs financial information in order to see that company

has discloses its accounting information according to the accounting standards set by the

government in order to protect shareholders interest. It needs information to see that company

is working legally on fair basis and not conducting misdeeds. At last government needs to

know financial position of the company to impose tax on the net profit of the company.

Lenders – They need information to see credit worthiness of the company and ability

to pay back the loan. Lenders are important to business as they provide loan and financial

support to the company but after getting information on financial position of the company

(Narayanaswamy, 2017).

When company has high profitability, ability to pay liability and secured assets any

lender would give financial support to the company. On the contrary when company has poor

liquidity, lack of assets and no ability to pay back the liability it shows poor financial health of

the company.

Investors - The other most important user of external information are investors that

want to invest in the company or has already invested. They want to know how much return

they are getting on their investment and how well the company is performing. To know all the

details about their investment, to assess profitability, risk and return investors needs

information about financial statements.

It also helps existing investors to take decision on increase or decrease their investment based

on the performance of the company (Libby, 2017). It helps new investors to take a decision on

buying shares of the company based on its income statement and balance sheet.

Investment analysts – They require detail information on company's finances

especially those who are trading on stock exchange. They need information to analyse

performance of the competitors in the same business. They also gather information from

company's key person interviews and briefings. They help investors to compare the

investment and returns of different companies and projects their past trends and future trends

to show which company would more likely to generates high returns.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

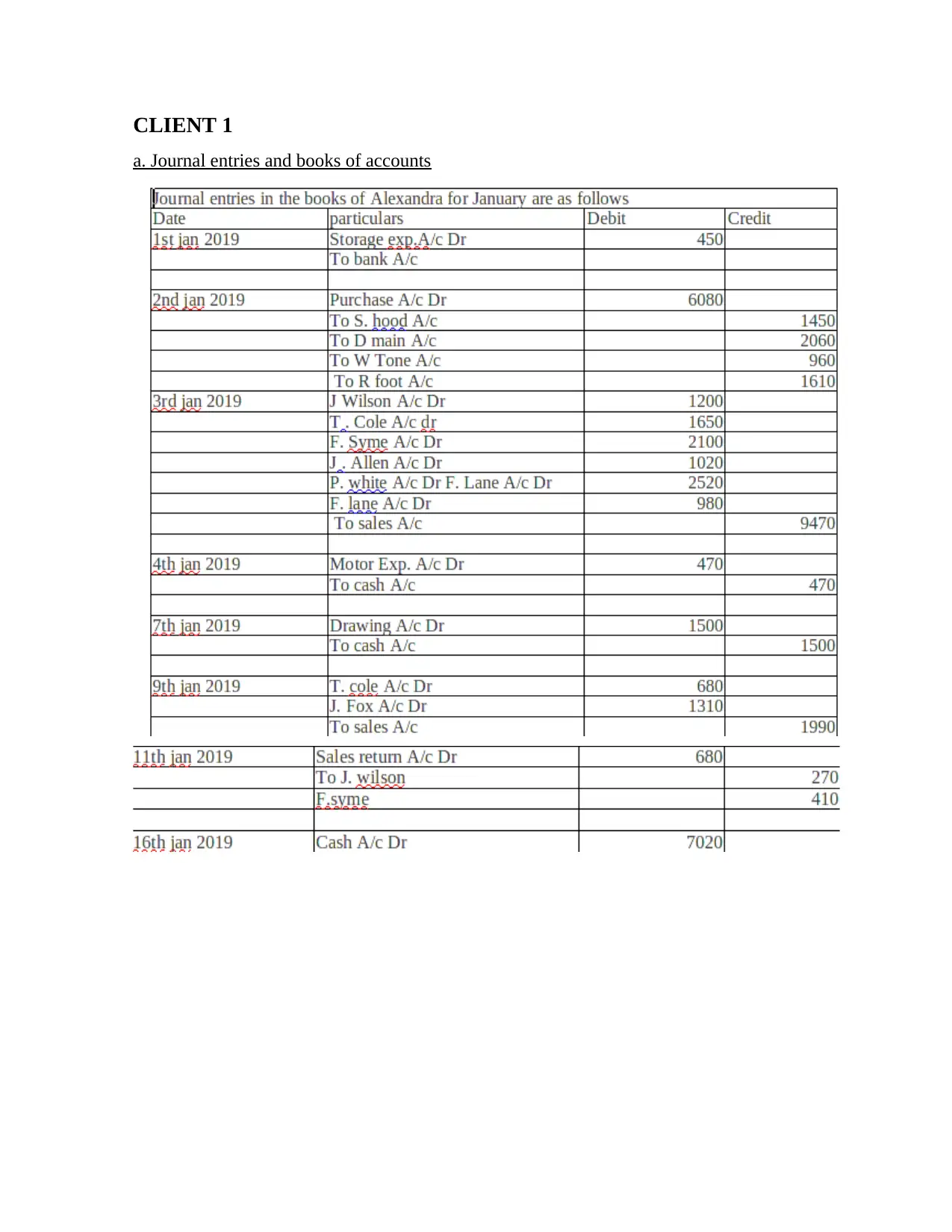

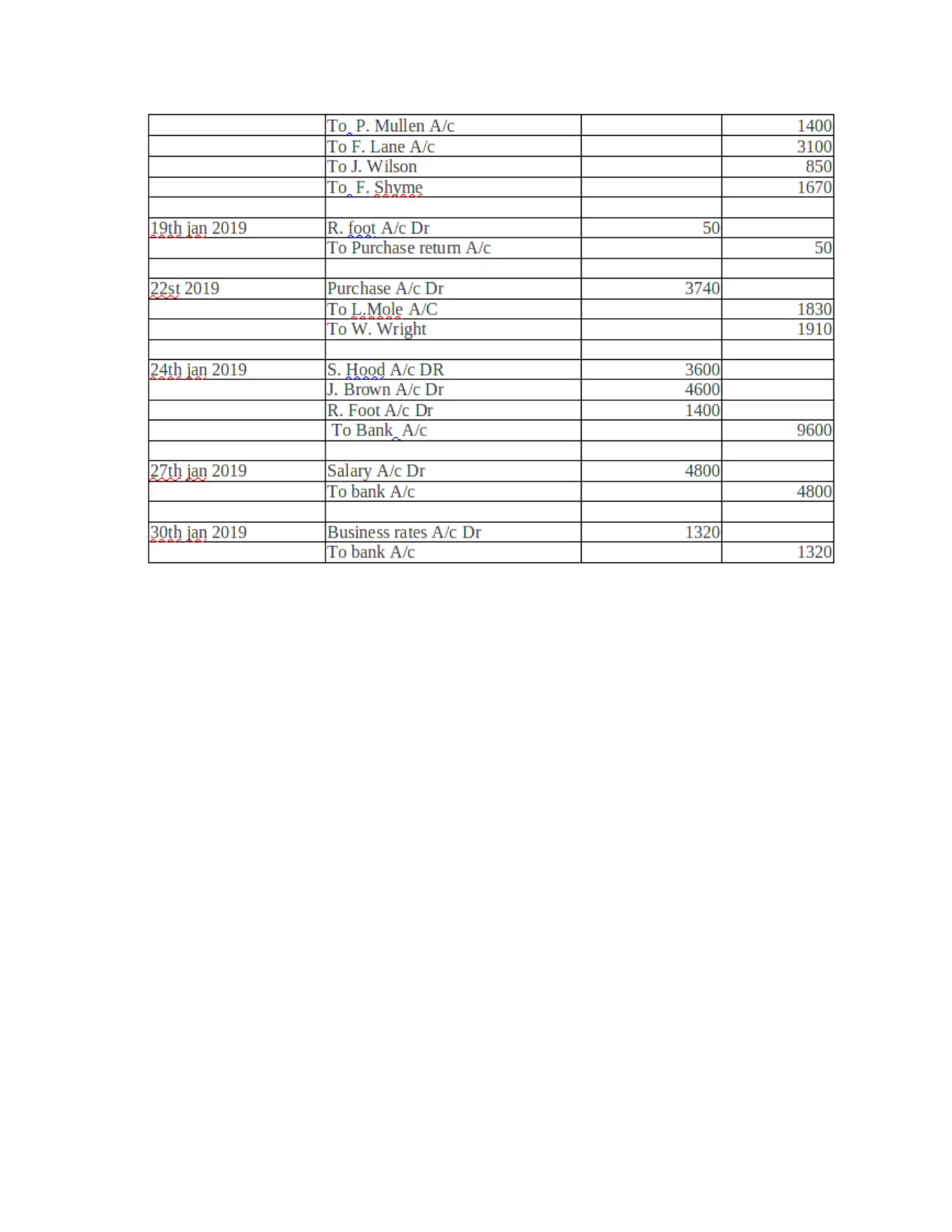

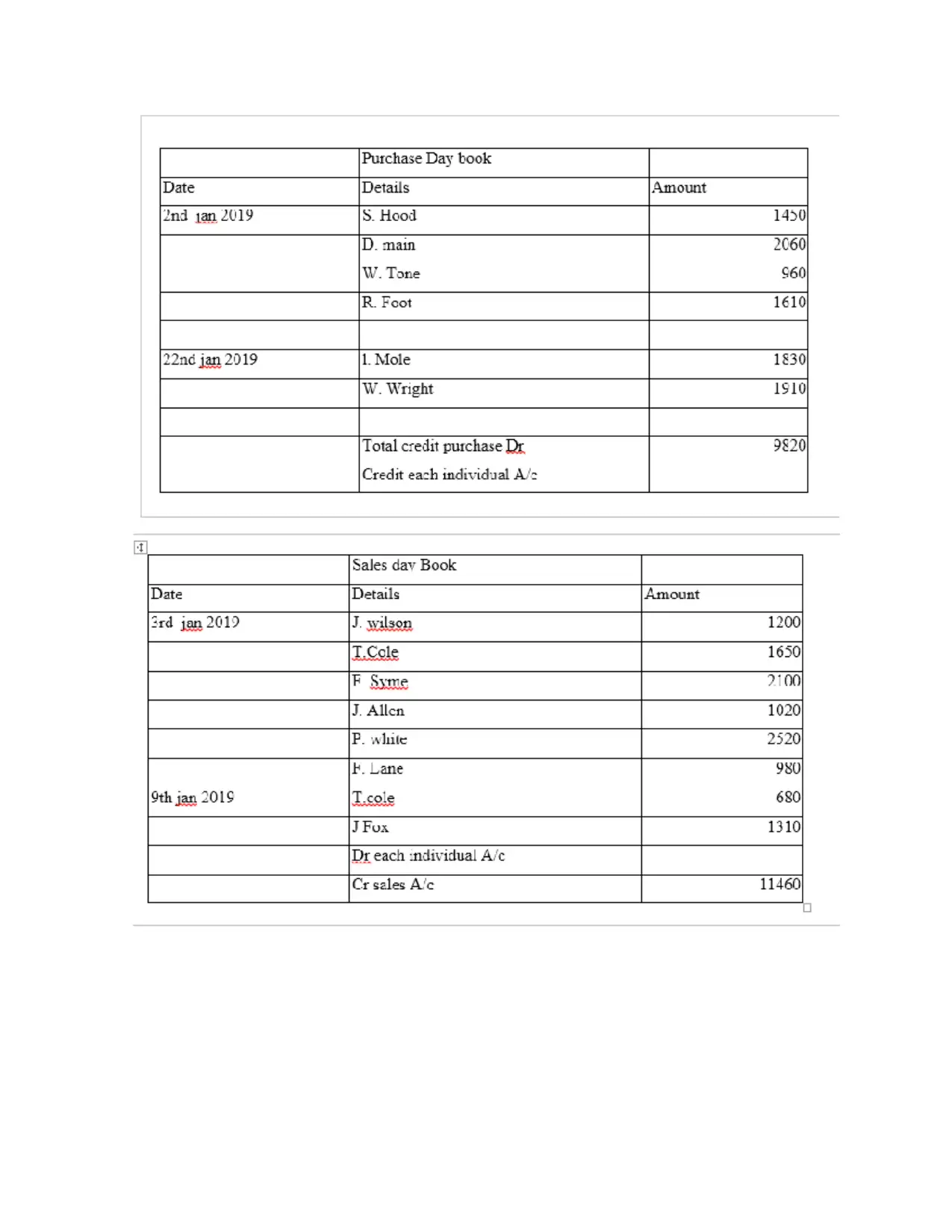

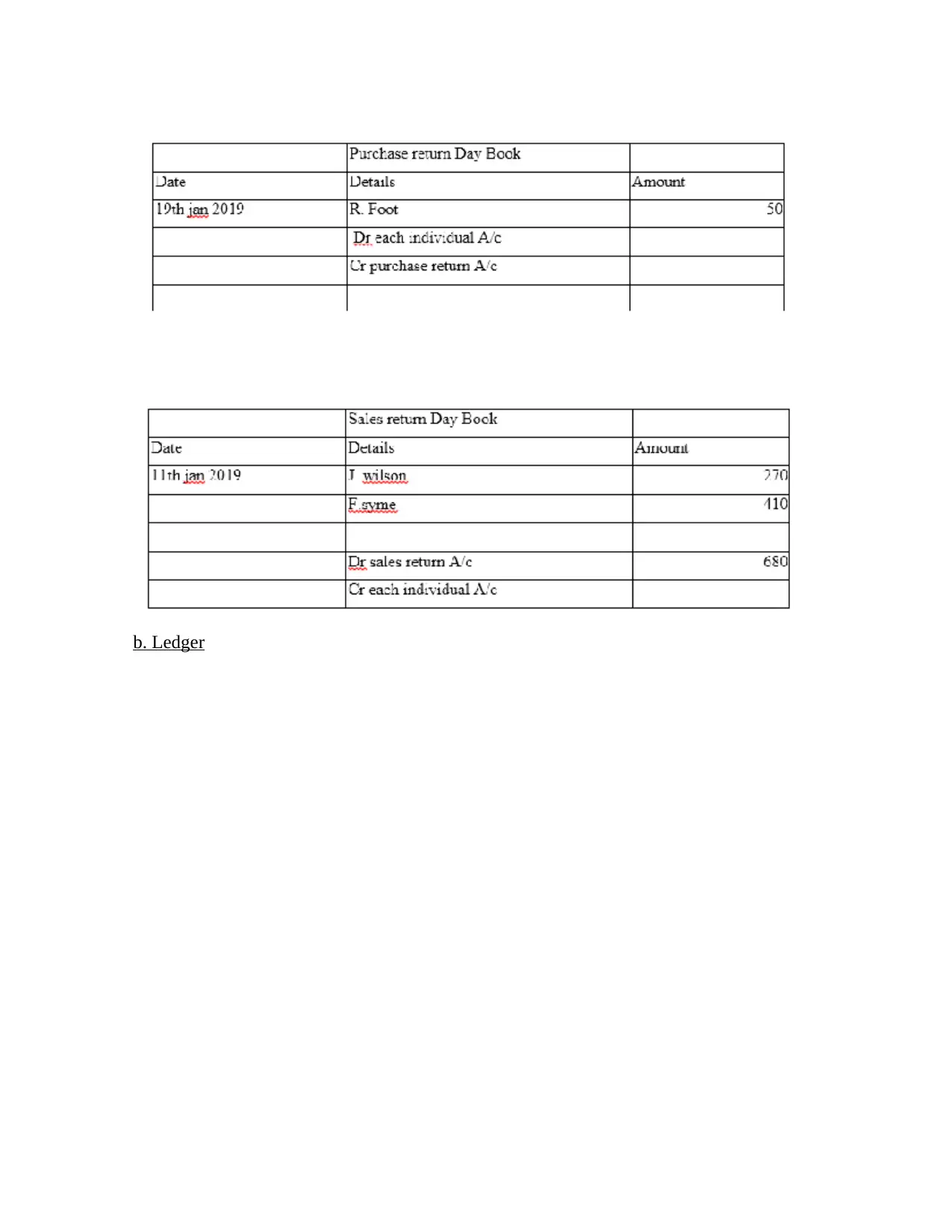

CLIENT 1

a. Journal entries and books of accounts

a. Journal entries and books of accounts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

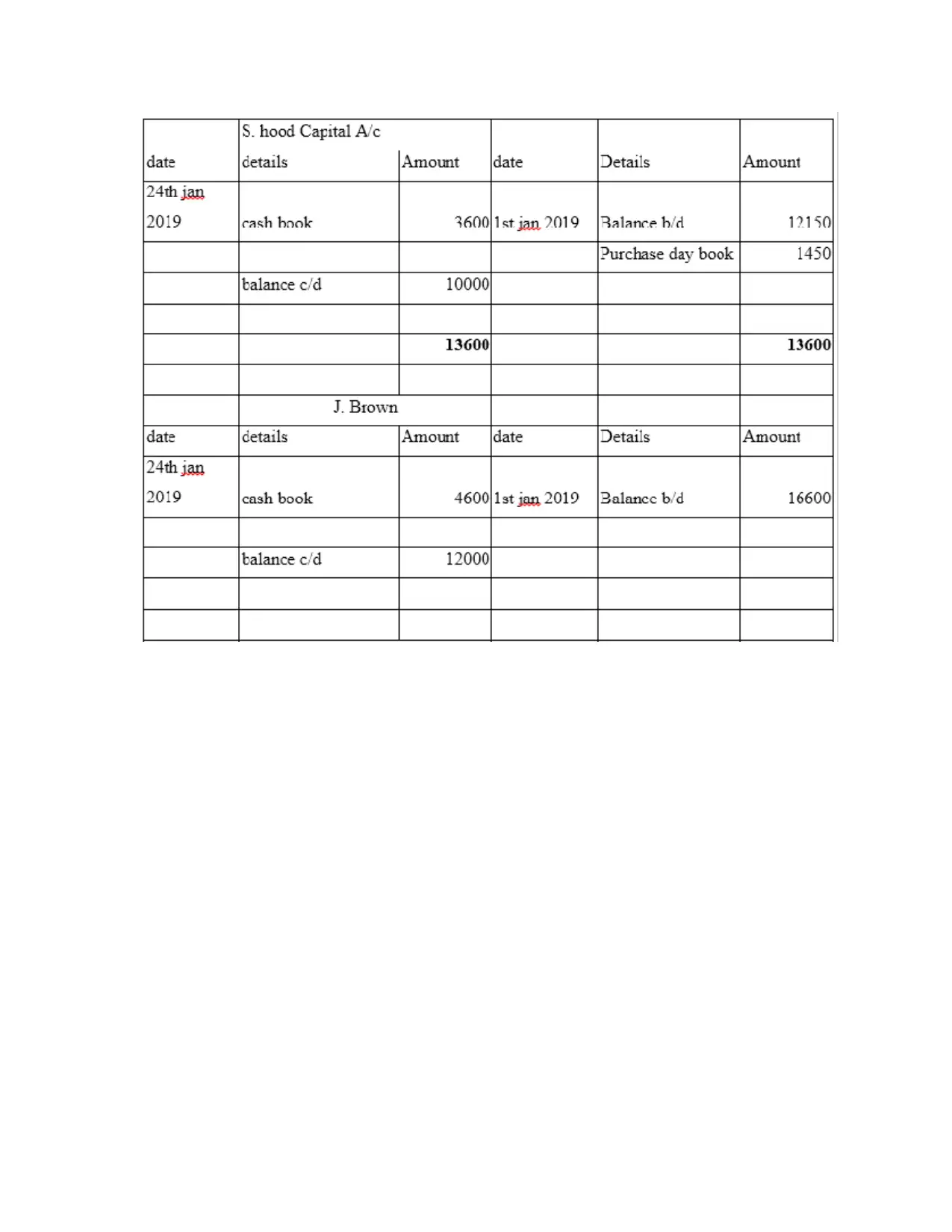

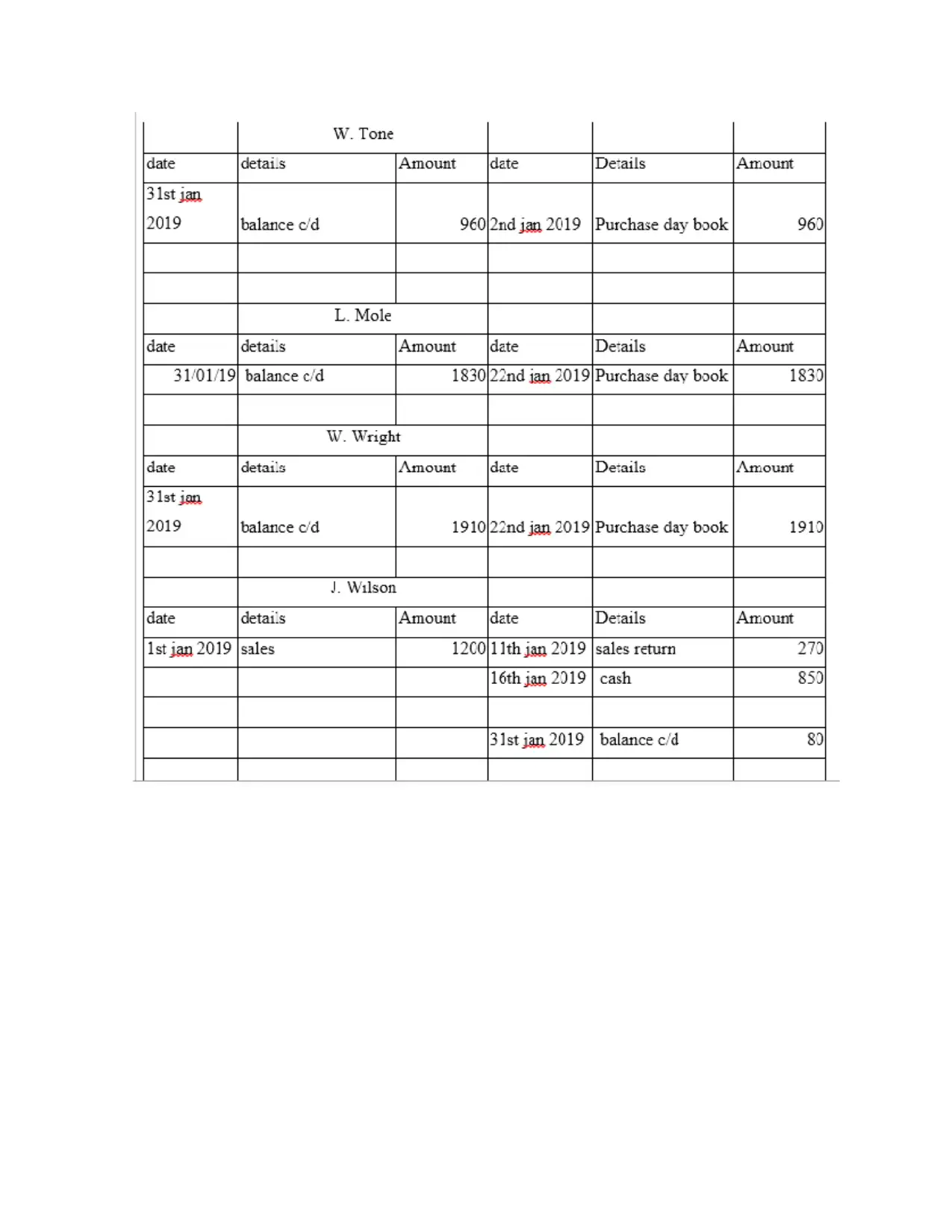

b. Ledger

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.