Financial Accounting Report: HNBS 310 - Semester 1, 2019-20

VerifiedAdded on 2023/01/10

|24

|3969

|87

Report

AI Summary

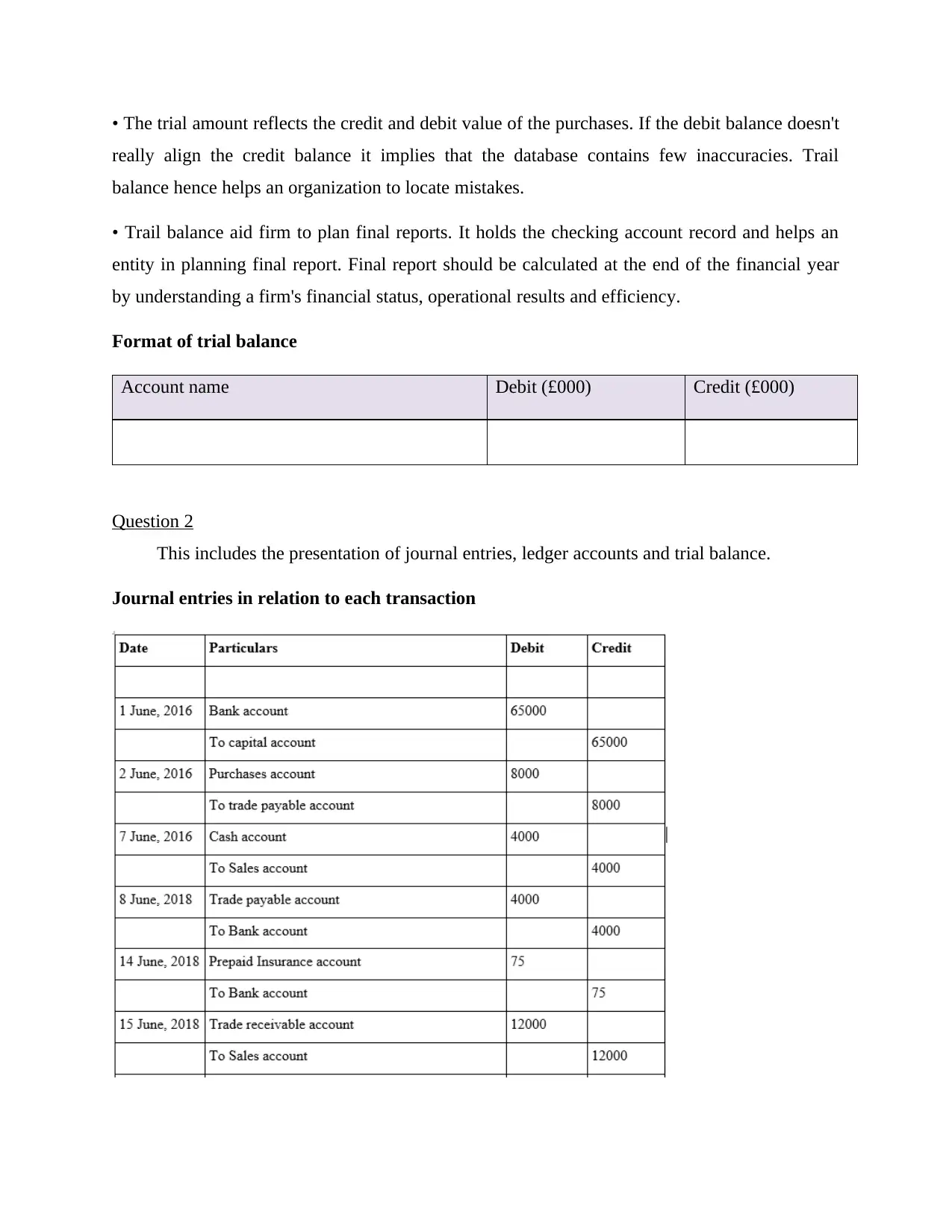

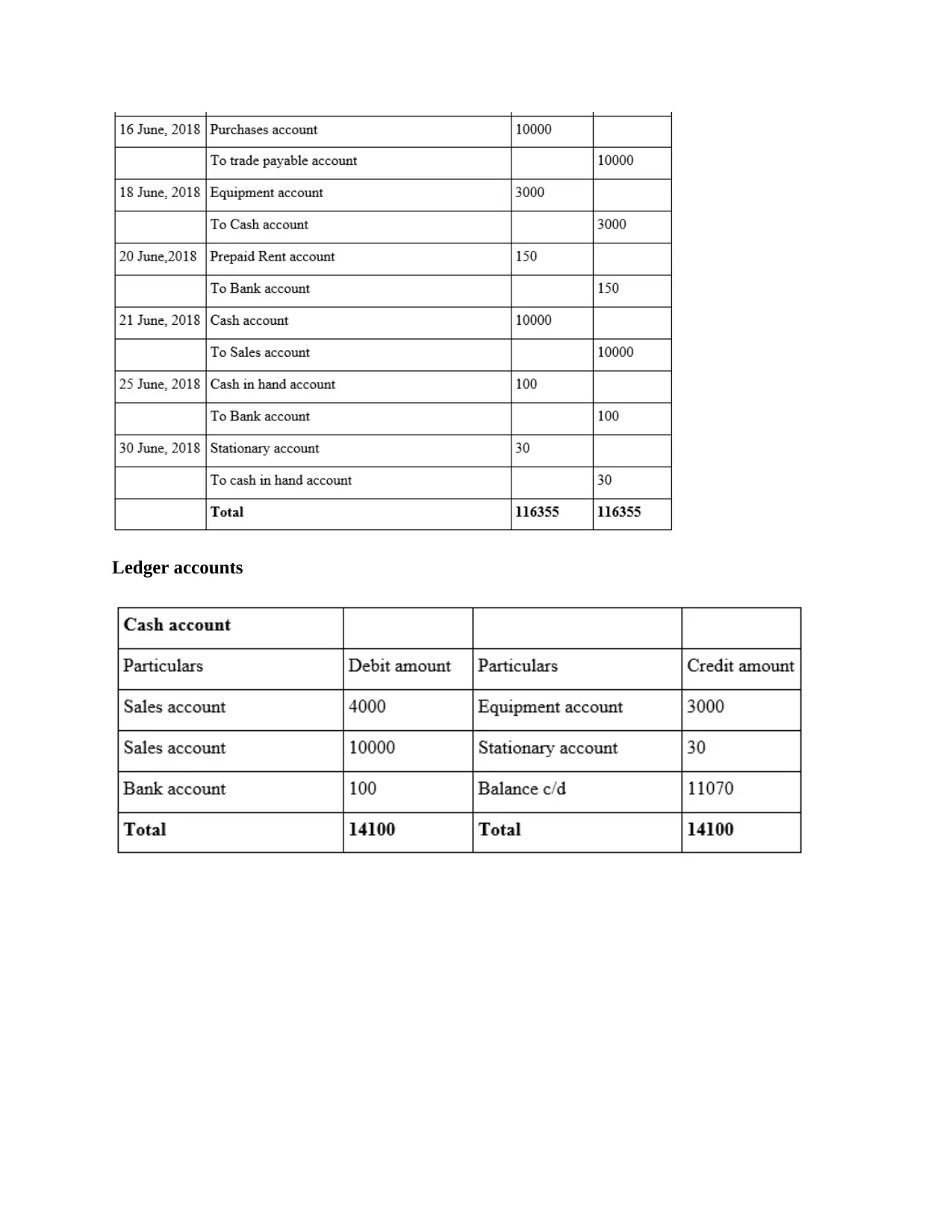

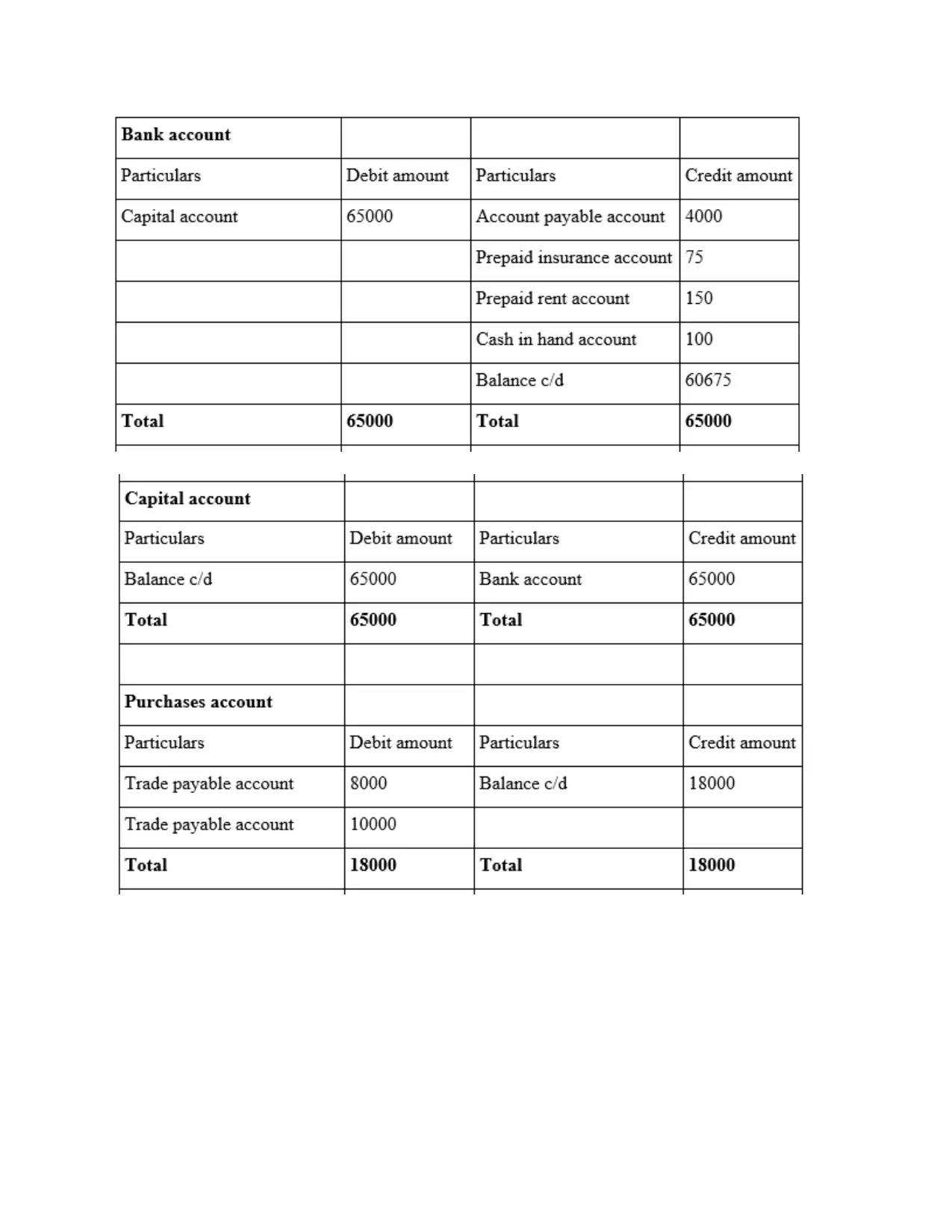

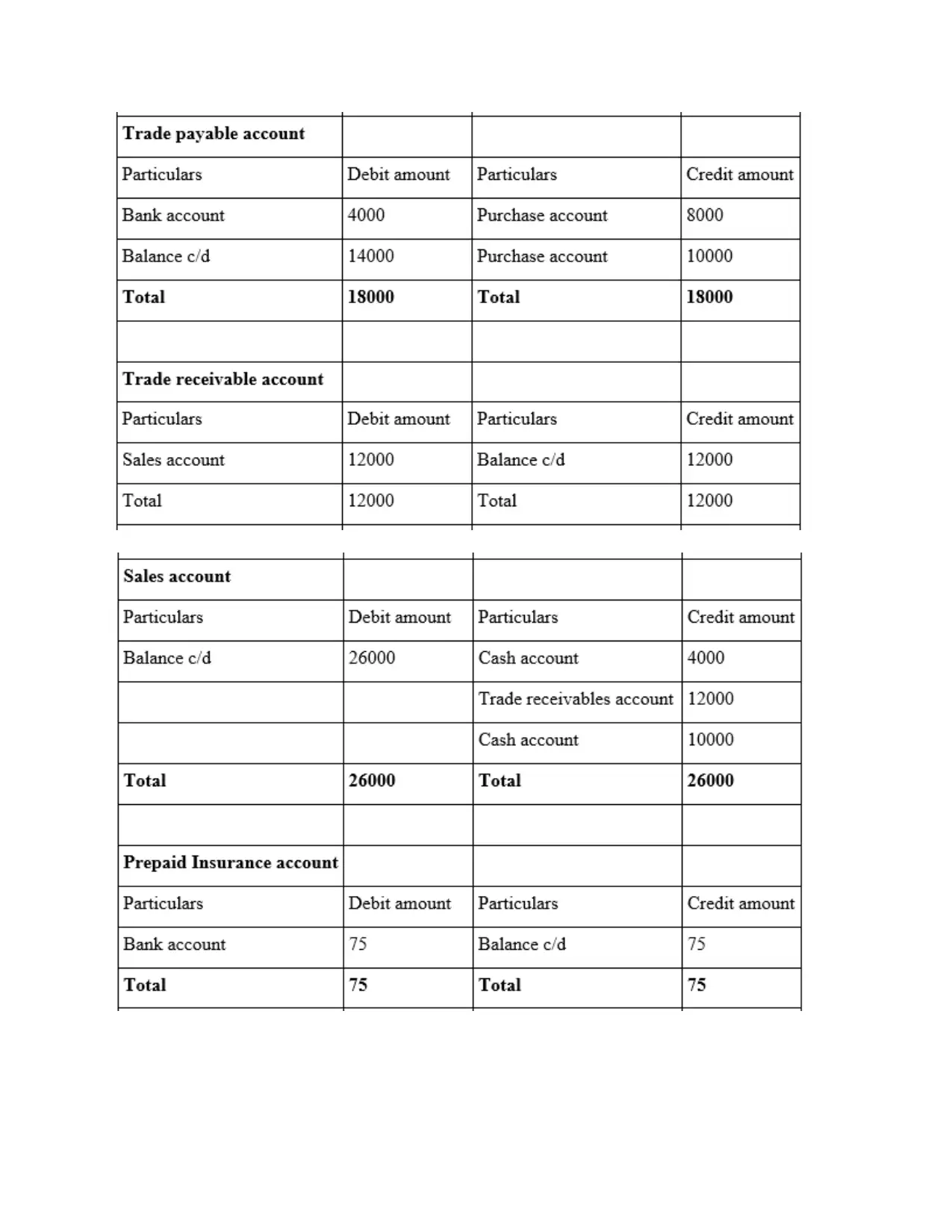

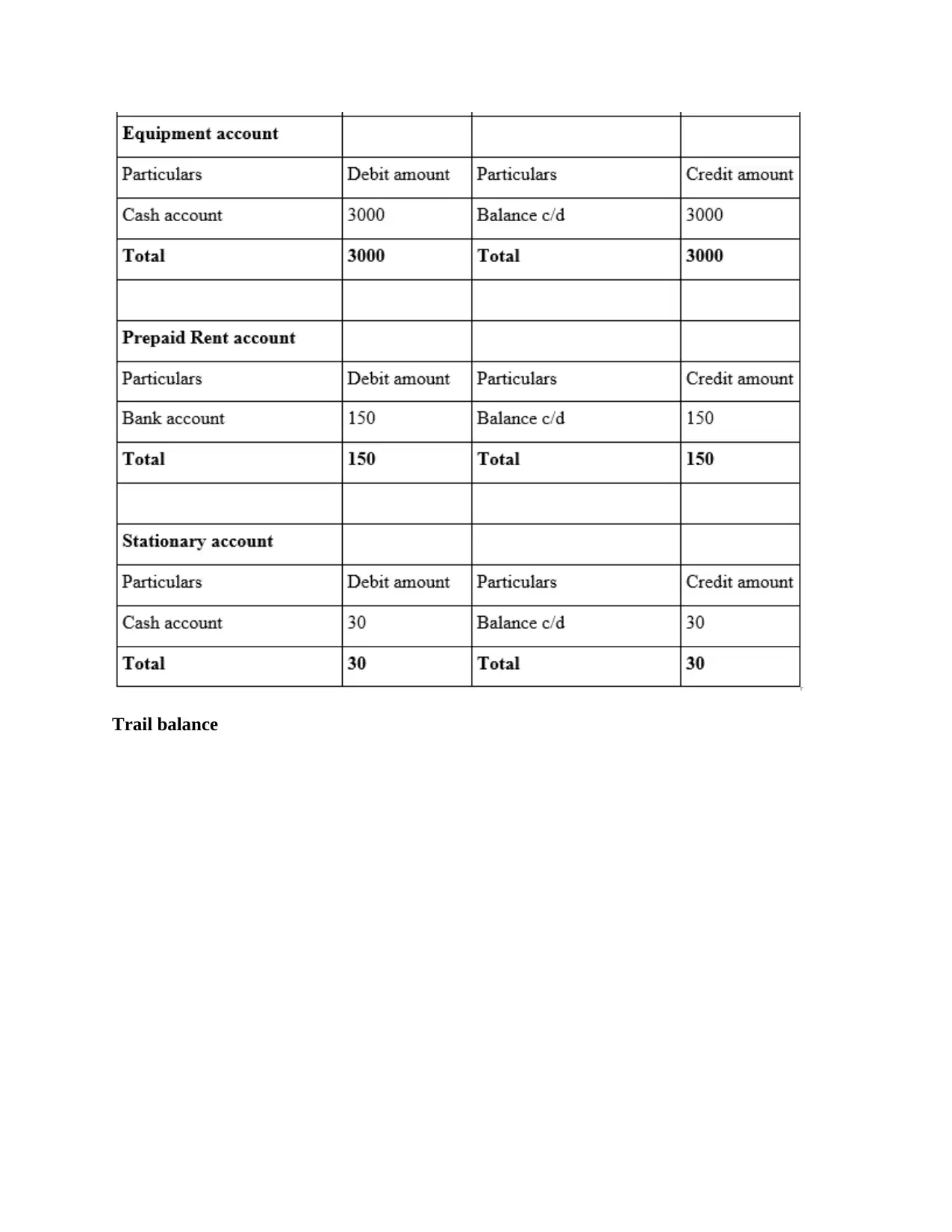

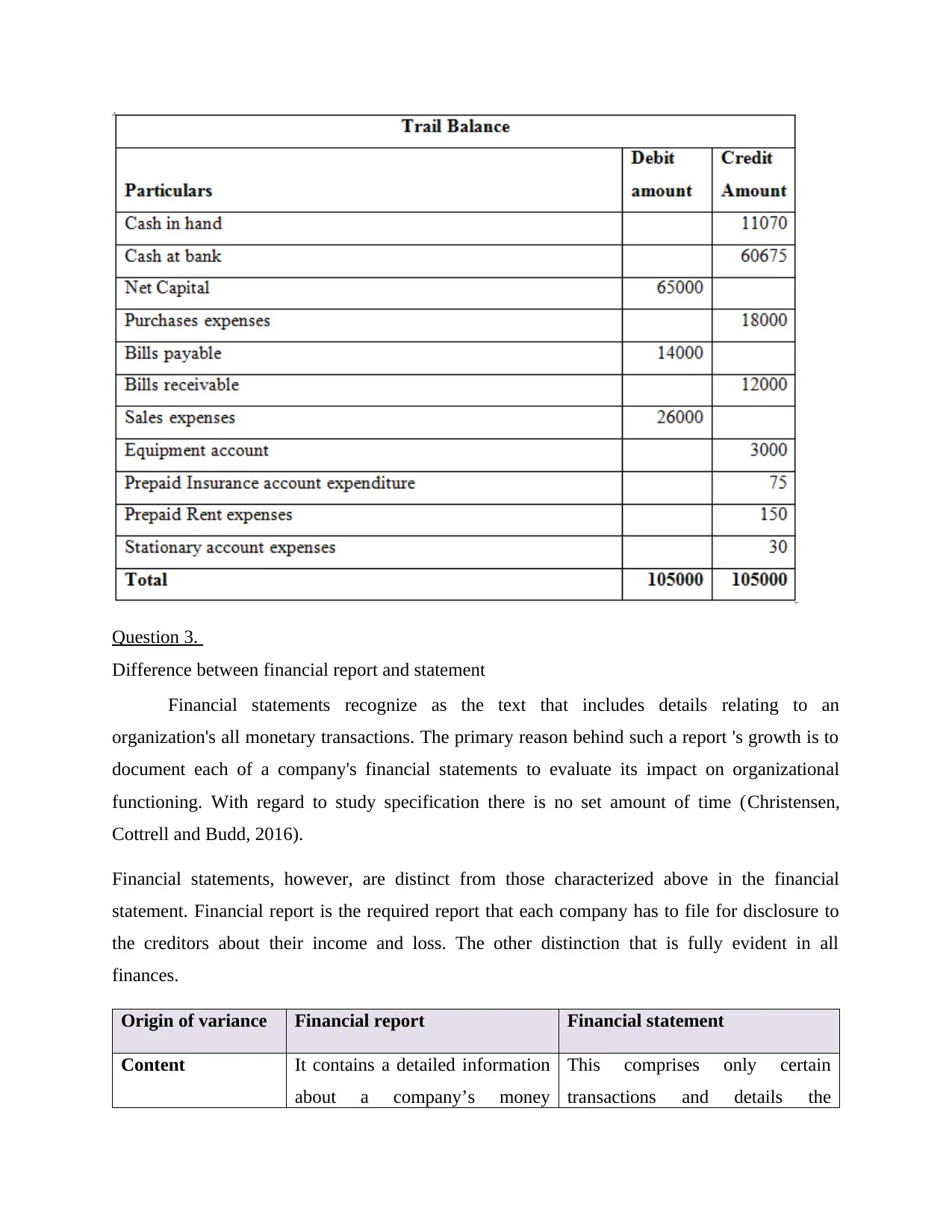

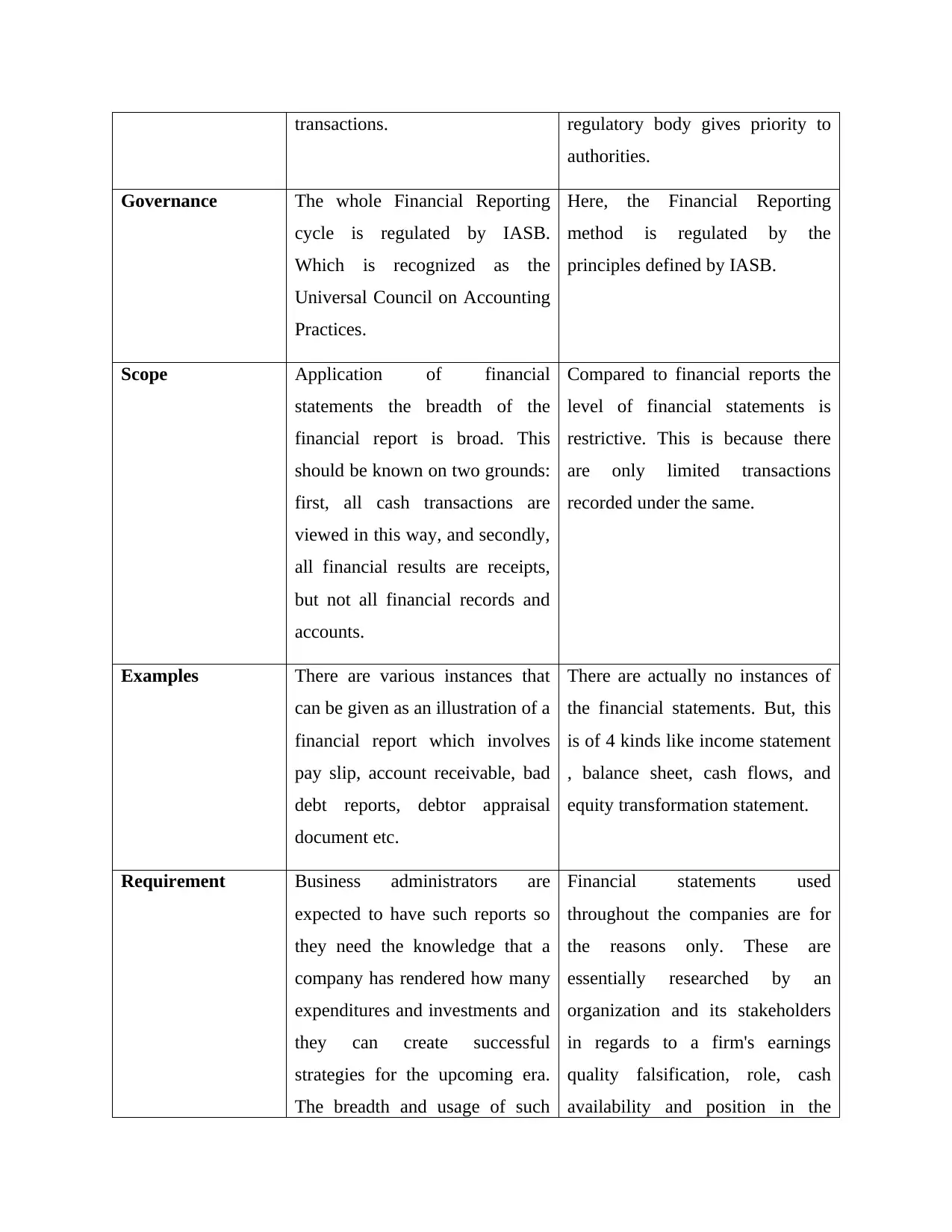

This report presents a comprehensive analysis of financial accounting principles and practices. It begins with an introduction to financial accounting and its importance, followed by an exploration of different types of business transactions, including internal and external transactions. The report then delves into the mechanics of double-entry bookkeeping, journal entries, ledger accounts, and trial balances. It differentiates between financial reports and financial statements, outlining their respective scopes, governance, and uses. The report also examines fundamental accounting principles such as the monetary unit assumption, going concern, and the matching principle. Furthermore, it provides examples of profit and loss accounts and balance sheets. The second scenario covers bank reconciliations, explaining the process and the reasons for discrepancies. The report also describes outstanding checks, NSF, and transit cash deposits. Finally, the report concludes with a discussion of the importance of bank reconciliation and suspense accounts. This report provides a detailed overview of the core concepts and practical applications in financial accounting.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.