Financial Accounting Report: Analysis of Financial Principles

VerifiedAdded on 2021/02/19

|24

|5821

|433

Report

AI Summary

This report delves into the core principles of financial accounting, examining its purpose and legal requirements, particularly within the context of a small accounting company named Brook City. It contrasts financial and management accounting, highlighting their differences in legal requirements, focus, and adherence to GAAP. The report identifies and differentiates between internal and external stakeholders, emphasizing the importance of financial information for their decision-making processes. Furthermore, the assignment provides practical examples, including double-entry bookkeeping with ledgers for various clients, demonstrating the application of accounting principles in real-world scenarios. The report covers the creation of essential financial statements such as balance sheets and trial balances, as per accounting rules and standards.

Financial Accounting

Principles

Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

Financial accounting and its purpose..........................................................................................1

Legal requirements......................................................................................................................2

TASK 2............................................................................................................................................5

Client 1. ......................................................................................................................................5

CLIENT 2..................................................................................................................................14

Client 3......................................................................................................................................16

Client 4......................................................................................................................................19

CLIENT 5..................................................................................................................................19

CONCLUSION .............................................................................................................................21

REFERENCES .............................................................................................................................22

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

Financial accounting and its purpose..........................................................................................1

Legal requirements......................................................................................................................2

TASK 2............................................................................................................................................5

Client 1. ......................................................................................................................................5

CLIENT 2..................................................................................................................................14

Client 3......................................................................................................................................16

Client 4......................................................................................................................................19

CLIENT 5..................................................................................................................................19

CONCLUSION .............................................................................................................................21

REFERENCES .............................................................................................................................22

INTRODUCTION

In accounting term, financial accounting relates to the accounting standards and methods

involved in preparing the firm's crucial financial statements like trading profit and loss accounts,

cash flow statements and statements of financial position (Edwards, 2013). In general words,

financial accounting is an accounting field that is consistent with the collection, analysis and

presentation of financial data so that financial position and strength of company can be

presented to external and internal stakeholder. In order to better understand the concept of small

accounting company have been selected named Brook City which has the main function to

provide essential accounting services to number of people at initial level in London.

In this project meaning and purpose of financial accounting, difference between Financial

and Management accounting is discussed. Report also defines about the external and internal

stakeholders and the important of financial information to them in decision making. This project

also discusses about formulation of assorted accounts like bank reconciliation statement, balance

sheet, trail balance as per principles and rules of accounting.

TASK 1

Financial accounting and its purpose.

In business word, the definition of accounting defines the process of recording, reporting,

analysing and summarising useful relevant financial data (Whittington, 2016). This is consider

to be the language of finance which transmits the company financial situation to interested

parties such as manager, shareholder and creditor, so that they can translate a firm's operations

into authentic and comparable accounts. The main role to be achieved by accounting is related

with recording of the various operations that are produced within the company.

Financial accounting is a methodology of collecting and processing an organization's

financial statements that demonstrates the business's economic stability used by business-related

stakeholders to create an intelligent decision. The financial accounting method starts with the

recording of overall business dealing within journal, that are further posted into ledger and then

to check the overall accountability trail balance is prepared at the end of specific accounting

year. Financial manager are truly responsible to record and report every business dealing that

shows the actual and real value of business. This stream of accounting is total different for

management accounting because it relates to the evaluation of professional expertise, methods

1

In accounting term, financial accounting relates to the accounting standards and methods

involved in preparing the firm's crucial financial statements like trading profit and loss accounts,

cash flow statements and statements of financial position (Edwards, 2013). In general words,

financial accounting is an accounting field that is consistent with the collection, analysis and

presentation of financial data so that financial position and strength of company can be

presented to external and internal stakeholder. In order to better understand the concept of small

accounting company have been selected named Brook City which has the main function to

provide essential accounting services to number of people at initial level in London.

In this project meaning and purpose of financial accounting, difference between Financial

and Management accounting is discussed. Report also defines about the external and internal

stakeholders and the important of financial information to them in decision making. This project

also discusses about formulation of assorted accounts like bank reconciliation statement, balance

sheet, trail balance as per principles and rules of accounting.

TASK 1

Financial accounting and its purpose.

In business word, the definition of accounting defines the process of recording, reporting,

analysing and summarising useful relevant financial data (Whittington, 2016). This is consider

to be the language of finance which transmits the company financial situation to interested

parties such as manager, shareholder and creditor, so that they can translate a firm's operations

into authentic and comparable accounts. The main role to be achieved by accounting is related

with recording of the various operations that are produced within the company.

Financial accounting is a methodology of collecting and processing an organization's

financial statements that demonstrates the business's economic stability used by business-related

stakeholders to create an intelligent decision. The financial accounting method starts with the

recording of overall business dealing within journal, that are further posted into ledger and then

to check the overall accountability trail balance is prepared at the end of specific accounting

year. Financial manager are truly responsible to record and report every business dealing that

shows the actual and real value of business. This stream of accounting is total different for

management accounting because it relates to the evaluation of professional expertise, methods

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

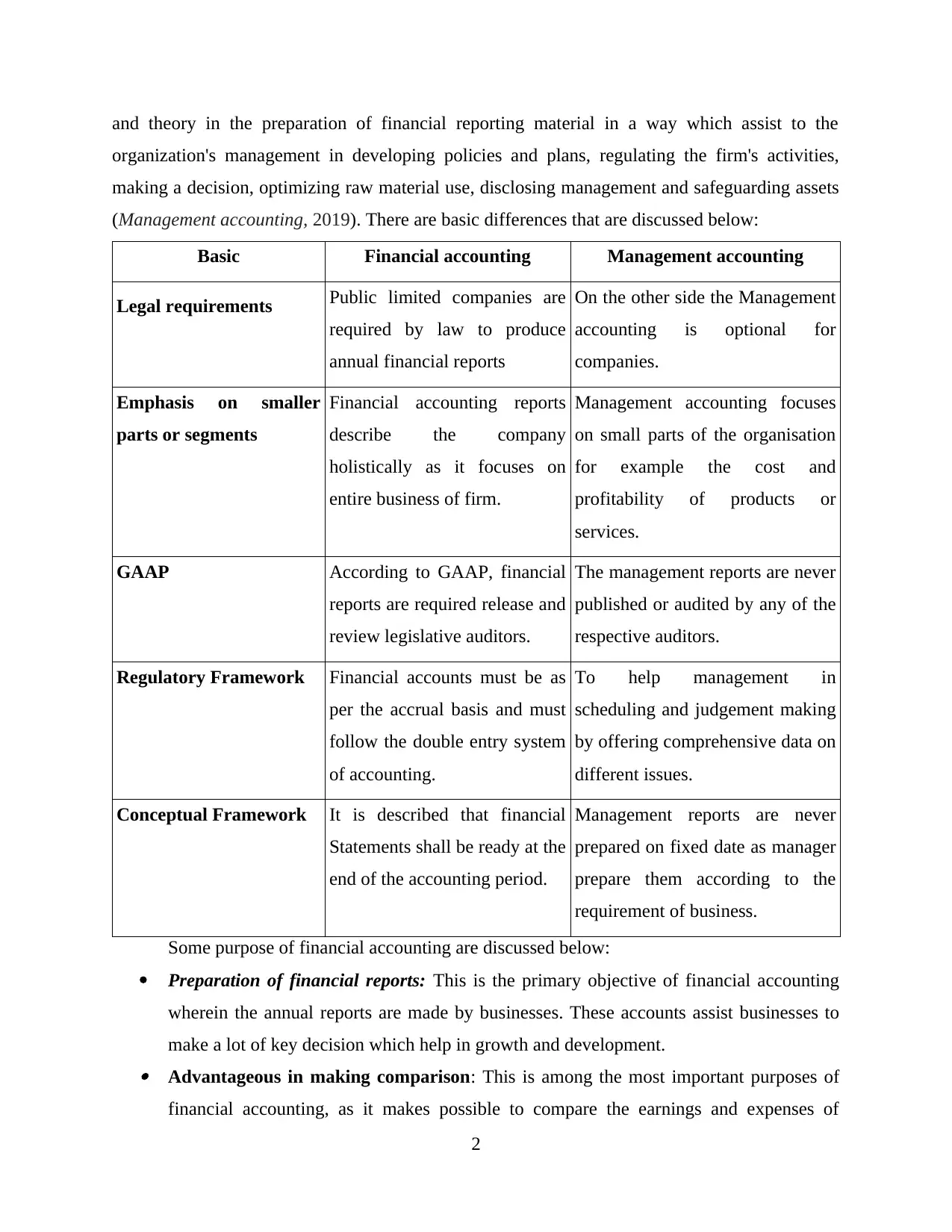

and theory in the preparation of financial reporting material in a way which assist to the

organization's management in developing policies and plans, regulating the firm's activities,

making a decision, optimizing raw material use, disclosing management and safeguarding assets

(Management accounting, 2019). There are basic differences that are discussed below:

Basic Financial accounting Management accounting

Legal requirements Public limited companies are

required by law to produce

annual financial reports

On the other side the Management

accounting is optional for

companies.

Emphasis on smaller

parts or segments

Financial accounting reports

describe the company

holistically as it focuses on

entire business of firm.

Management accounting focuses

on small parts of the organisation

for example the cost and

profitability of products or

services.

GAAP According to GAAP, financial

reports are required release and

review legislative auditors.

The management reports are never

published or audited by any of the

respective auditors.

Regulatory Framework Financial accounts must be as

per the accrual basis and must

follow the double entry system

of accounting.

To help management in

scheduling and judgement making

by offering comprehensive data on

different issues.

Conceptual Framework It is described that financial

Statements shall be ready at the

end of the accounting period.

Management reports are never

prepared on fixed date as manager

prepare them according to the

requirement of business.

Some purpose of financial accounting are discussed below:

Preparation of financial reports: This is the primary objective of financial accounting

wherein the annual reports are made by businesses. These accounts assist businesses to

make a lot of key decision which help in growth and development. Advantageous in making comparison: This is among the most important purposes of

financial accounting, as it makes possible to compare the earnings and expenses of

2

organization's management in developing policies and plans, regulating the firm's activities,

making a decision, optimizing raw material use, disclosing management and safeguarding assets

(Management accounting, 2019). There are basic differences that are discussed below:

Basic Financial accounting Management accounting

Legal requirements Public limited companies are

required by law to produce

annual financial reports

On the other side the Management

accounting is optional for

companies.

Emphasis on smaller

parts or segments

Financial accounting reports

describe the company

holistically as it focuses on

entire business of firm.

Management accounting focuses

on small parts of the organisation

for example the cost and

profitability of products or

services.

GAAP According to GAAP, financial

reports are required release and

review legislative auditors.

The management reports are never

published or audited by any of the

respective auditors.

Regulatory Framework Financial accounts must be as

per the accrual basis and must

follow the double entry system

of accounting.

To help management in

scheduling and judgement making

by offering comprehensive data on

different issues.

Conceptual Framework It is described that financial

Statements shall be ready at the

end of the accounting period.

Management reports are never

prepared on fixed date as manager

prepare them according to the

requirement of business.

Some purpose of financial accounting are discussed below:

Preparation of financial reports: This is the primary objective of financial accounting

wherein the annual reports are made by businesses. These accounts assist businesses to

make a lot of key decision which help in growth and development. Advantageous in making comparison: This is among the most important purposes of

financial accounting, as it makes possible to compare the earnings and expenses of

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company with their preceding year which further aid businesses to create corresponding

adjustments to plans and strategies (Fraser, Ormiston and Fraser, 2010). Benefit to build strategies: Financial reports provide the entire management of Brook

City with both quantitative and qualitative information which support them develop

future policies. The manager prepare and interpret the information into useful outputs

regarding the current target that are to be focused with the assist of financial data.

Support to stakeholders: The stakeholders should analyse profitability and possible

future situation with the help of company's financial statements. They may assess

whether to spend further or cancel their cash on the grounds of this data. It also helps the

authorities find out if the business is fluid or moving towards illness.

A stakeholder any person or entity who will take interest in the business activities and

focus on the operations that play role in failure and success of a business project. They can have

influence on decision in reference of operations and finances of a company. There are

categorised of stakeholder into two parts -

Internal stakeholders

External stakeholders

Both type of stakeholders aware for the other business function and take report in details.

There are defined both stakeholders in detail -

External stakeholder – These types of stakeholders are part of stakeholder who can not

take interest into daily routine activities of business but sometimes take interest. They have

different types of rights like other company members. There are consisting of various types of

stakeholders such as government, suppliers, creditors etc. All the external stakeholder wants to

earn more income from the company and on the basis of financial information invest money in

the company. Herein, below some types of external stakeholder are mentioned such as -

Investors – These stakeholders are involved in spending cash in company procedures

and events (Hiebl, 2014). The purpose of investors to earn more profit from their invested

money so fulfil the purpose they were taking interest into financial information. They are

taking meeting and right to provide suggestion regarding to company policy. On the basis

of financial report they take decisions about whether they should invest or not. In the lack

of reviewing the company's economic data, asset allocation can be hard for them

3

adjustments to plans and strategies (Fraser, Ormiston and Fraser, 2010). Benefit to build strategies: Financial reports provide the entire management of Brook

City with both quantitative and qualitative information which support them develop

future policies. The manager prepare and interpret the information into useful outputs

regarding the current target that are to be focused with the assist of financial data.

Support to stakeholders: The stakeholders should analyse profitability and possible

future situation with the help of company's financial statements. They may assess

whether to spend further or cancel their cash on the grounds of this data. It also helps the

authorities find out if the business is fluid or moving towards illness.

A stakeholder any person or entity who will take interest in the business activities and

focus on the operations that play role in failure and success of a business project. They can have

influence on decision in reference of operations and finances of a company. There are

categorised of stakeholder into two parts -

Internal stakeholders

External stakeholders

Both type of stakeholders aware for the other business function and take report in details.

There are defined both stakeholders in detail -

External stakeholder – These types of stakeholders are part of stakeholder who can not

take interest into daily routine activities of business but sometimes take interest. They have

different types of rights like other company members. There are consisting of various types of

stakeholders such as government, suppliers, creditors etc. All the external stakeholder wants to

earn more income from the company and on the basis of financial information invest money in

the company. Herein, below some types of external stakeholder are mentioned such as -

Investors – These stakeholders are involved in spending cash in company procedures

and events (Hiebl, 2014). The purpose of investors to earn more profit from their invested

money so fulfil the purpose they were taking interest into financial information. They are

taking meeting and right to provide suggestion regarding to company policy. On the basis

of financial report they take decisions about whether they should invest or not. In the lack

of reviewing the company's economic data, asset allocation can be hard for them

3

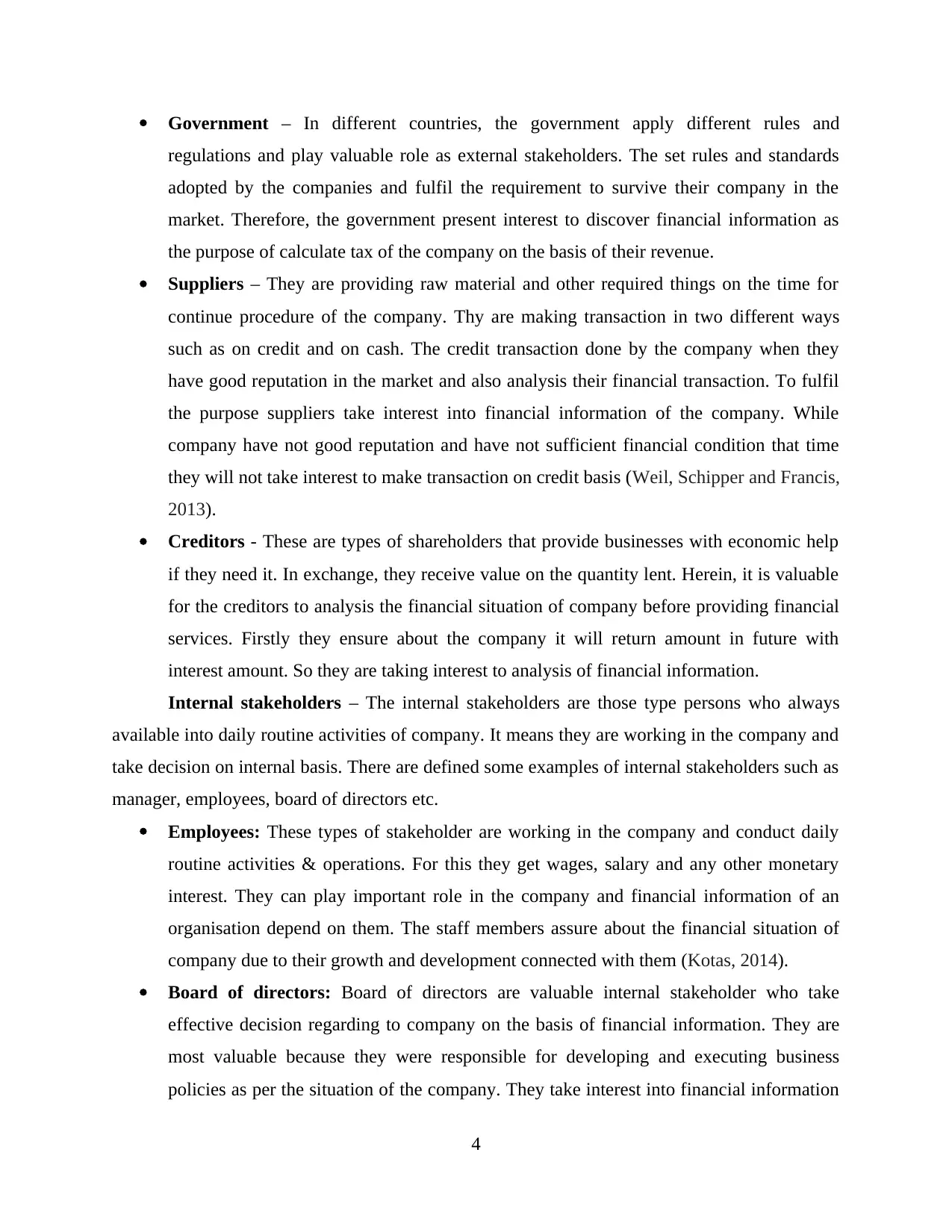

Government – In different countries, the government apply different rules and

regulations and play valuable role as external stakeholders. The set rules and standards

adopted by the companies and fulfil the requirement to survive their company in the

market. Therefore, the government present interest to discover financial information as

the purpose of calculate tax of the company on the basis of their revenue.

Suppliers – They are providing raw material and other required things on the time for

continue procedure of the company. Thy are making transaction in two different ways

such as on credit and on cash. The credit transaction done by the company when they

have good reputation in the market and also analysis their financial transaction. To fulfil

the purpose suppliers take interest into financial information of the company. While

company have not good reputation and have not sufficient financial condition that time

they will not take interest to make transaction on credit basis (Weil, Schipper and Francis,

2013).

Creditors - These are types of shareholders that provide businesses with economic help

if they need it. In exchange, they receive value on the quantity lent. Herein, it is valuable

for the creditors to analysis the financial situation of company before providing financial

services. Firstly they ensure about the company it will return amount in future with

interest amount. So they are taking interest to analysis of financial information.

Internal stakeholders – The internal stakeholders are those type persons who always

available into daily routine activities of company. It means they are working in the company and

take decision on internal basis. There are defined some examples of internal stakeholders such as

manager, employees, board of directors etc.

Employees: These types of stakeholder are working in the company and conduct daily

routine activities & operations. For this they get wages, salary and any other monetary

interest. They can play important role in the company and financial information of an

organisation depend on them. The staff members assure about the financial situation of

company due to their growth and development connected with them (Kotas, 2014).

Board of directors: Board of directors are valuable internal stakeholder who take

effective decision regarding to company on the basis of financial information. They are

most valuable because they were responsible for developing and executing business

policies as per the situation of the company. They take interest into financial information

4

regulations and play valuable role as external stakeholders. The set rules and standards

adopted by the companies and fulfil the requirement to survive their company in the

market. Therefore, the government present interest to discover financial information as

the purpose of calculate tax of the company on the basis of their revenue.

Suppliers – They are providing raw material and other required things on the time for

continue procedure of the company. Thy are making transaction in two different ways

such as on credit and on cash. The credit transaction done by the company when they

have good reputation in the market and also analysis their financial transaction. To fulfil

the purpose suppliers take interest into financial information of the company. While

company have not good reputation and have not sufficient financial condition that time

they will not take interest to make transaction on credit basis (Weil, Schipper and Francis,

2013).

Creditors - These are types of shareholders that provide businesses with economic help

if they need it. In exchange, they receive value on the quantity lent. Herein, it is valuable

for the creditors to analysis the financial situation of company before providing financial

services. Firstly they ensure about the company it will return amount in future with

interest amount. So they are taking interest to analysis of financial information.

Internal stakeholders – The internal stakeholders are those type persons who always

available into daily routine activities of company. It means they are working in the company and

take decision on internal basis. There are defined some examples of internal stakeholders such as

manager, employees, board of directors etc.

Employees: These types of stakeholder are working in the company and conduct daily

routine activities & operations. For this they get wages, salary and any other monetary

interest. They can play important role in the company and financial information of an

organisation depend on them. The staff members assure about the financial situation of

company due to their growth and development connected with them (Kotas, 2014).

Board of directors: Board of directors are valuable internal stakeholder who take

effective decision regarding to company on the basis of financial information. They are

most valuable because they were responsible for developing and executing business

policies as per the situation of the company. They take interest into financial information

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in an organisation to make future plans and think about further investments as per the

policies.

TASK 2

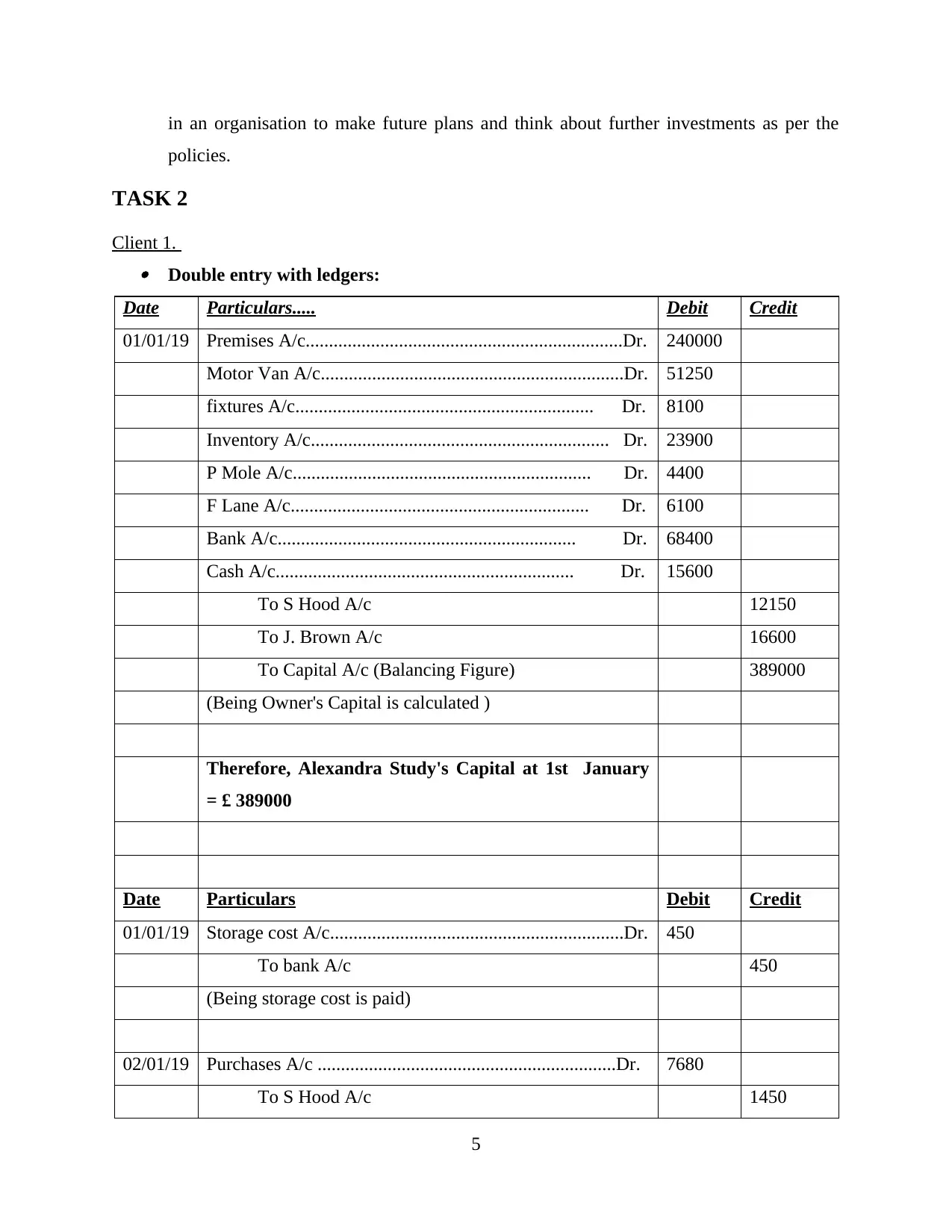

Client 1. Double entry with ledgers:

Date Particulars..... Debit Credit

01/01/19 Premises A/c....................................................................Dr. 240000

Motor Van A/c.................................................................Dr. 51250

fixtures A/c................................................................ Dr. 8100

Inventory A/c................................................................ Dr. 23900

P Mole A/c................................................................ Dr. 4400

F Lane A/c................................................................ Dr. 6100

Bank A/c................................................................ Dr. 68400

Cash A/c................................................................ Dr. 15600

To S Hood A/c 12150

To J. Brown A/c 16600

To Capital A/c (Balancing Figure) 389000

(Being Owner's Capital is calculated )

Therefore, Alexandra Study's Capital at 1st January

= £ 389000

Date Particulars Debit Credit

01/01/19 Storage cost A/c...............................................................Dr. 450

To bank A/c 450

(Being storage cost is paid)

02/01/19 Purchases A/c ................................................................Dr. 7680

To S Hood A/c 1450

5

policies.

TASK 2

Client 1. Double entry with ledgers:

Date Particulars..... Debit Credit

01/01/19 Premises A/c....................................................................Dr. 240000

Motor Van A/c.................................................................Dr. 51250

fixtures A/c................................................................ Dr. 8100

Inventory A/c................................................................ Dr. 23900

P Mole A/c................................................................ Dr. 4400

F Lane A/c................................................................ Dr. 6100

Bank A/c................................................................ Dr. 68400

Cash A/c................................................................ Dr. 15600

To S Hood A/c 12150

To J. Brown A/c 16600

To Capital A/c (Balancing Figure) 389000

(Being Owner's Capital is calculated )

Therefore, Alexandra Study's Capital at 1st January

= £ 389000

Date Particulars Debit Credit

01/01/19 Storage cost A/c...............................................................Dr. 450

To bank A/c 450

(Being storage cost is paid)

02/01/19 Purchases A/c ................................................................Dr. 7680

To S Hood A/c 1450

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

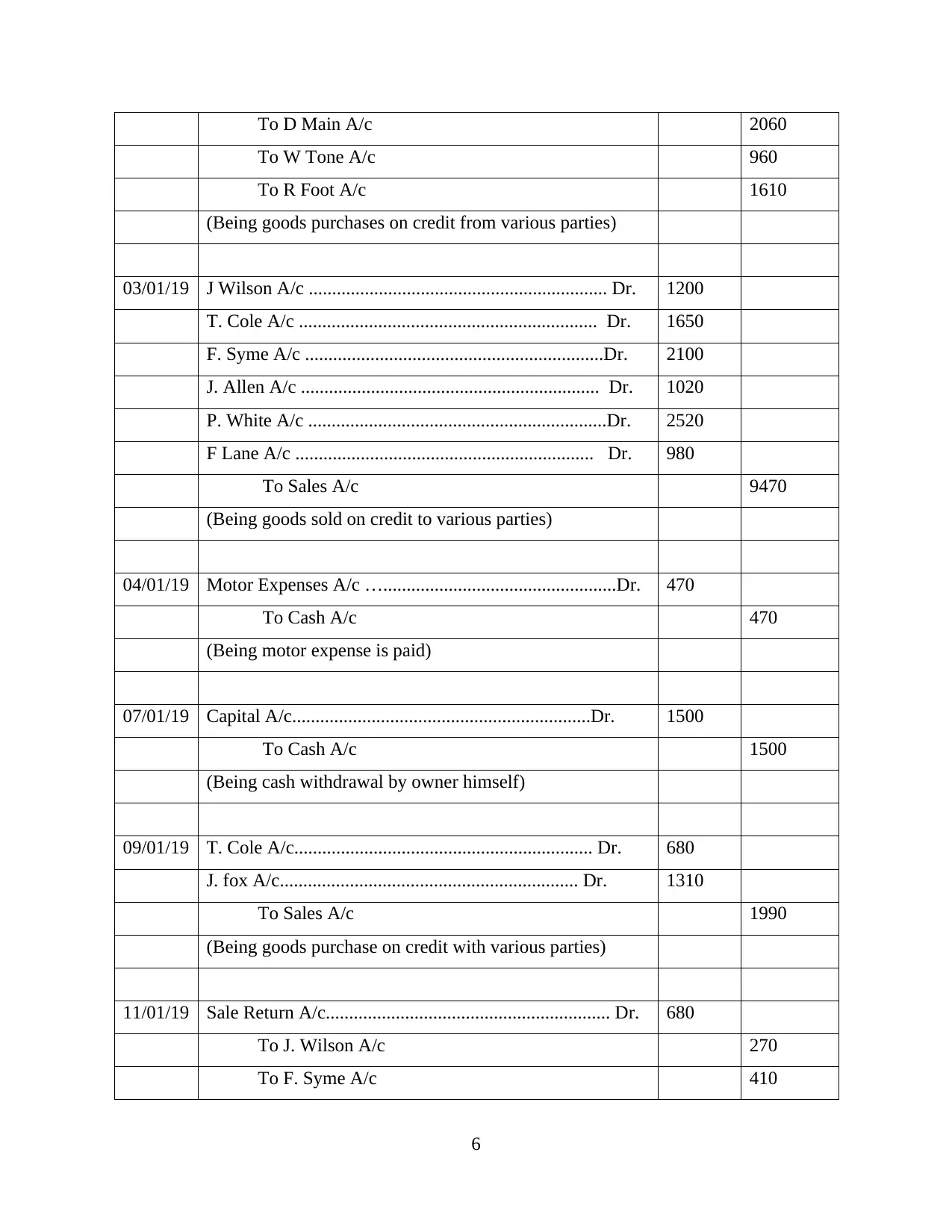

To D Main A/c 2060

To W Tone A/c 960

To R Foot A/c 1610

(Being goods purchases on credit from various parties)

03/01/19 J Wilson A/c ................................................................ Dr. 1200

T. Cole A/c ................................................................ Dr. 1650

F. Syme A/c ................................................................Dr. 2100

J. Allen A/c ................................................................ Dr. 1020

P. White A/c ................................................................Dr. 2520

F Lane A/c ................................................................ Dr. 980

To Sales A/c 9470

(Being goods sold on credit to various parties)

04/01/19 Motor Expenses A/c …..................................................Dr. 470

To Cash A/c 470

(Being motor expense is paid)

07/01/19 Capital A/c................................................................Dr. 1500

To Cash A/c 1500

(Being cash withdrawal by owner himself)

09/01/19 T. Cole A/c................................................................ Dr. 680

J. fox A/c................................................................ Dr. 1310

To Sales A/c 1990

(Being goods purchase on credit with various parties)

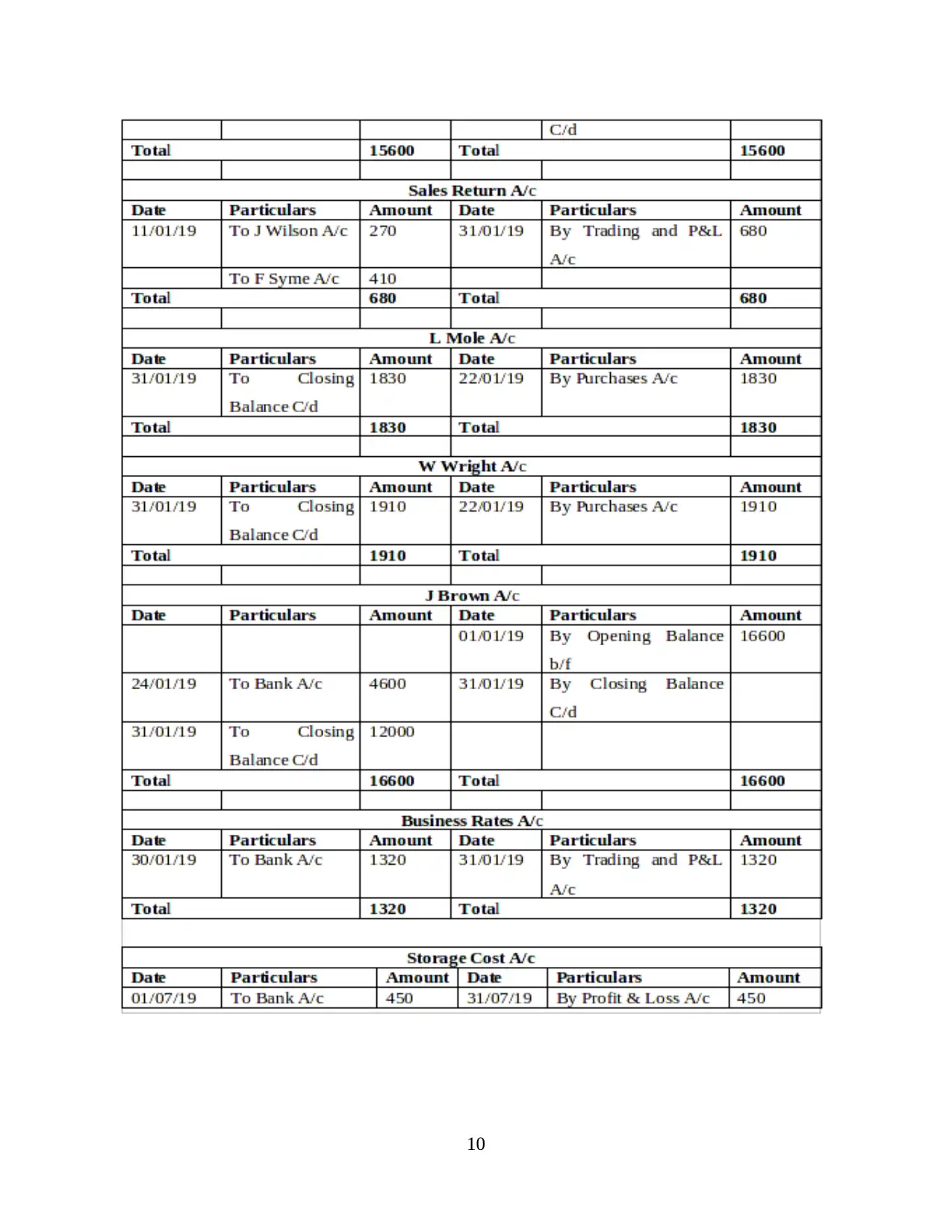

11/01/19 Sale Return A/c............................................................. Dr. 680

To J. Wilson A/c 270

To F. Syme A/c 410

6

To W Tone A/c 960

To R Foot A/c 1610

(Being goods purchases on credit from various parties)

03/01/19 J Wilson A/c ................................................................ Dr. 1200

T. Cole A/c ................................................................ Dr. 1650

F. Syme A/c ................................................................Dr. 2100

J. Allen A/c ................................................................ Dr. 1020

P. White A/c ................................................................Dr. 2520

F Lane A/c ................................................................ Dr. 980

To Sales A/c 9470

(Being goods sold on credit to various parties)

04/01/19 Motor Expenses A/c …..................................................Dr. 470

To Cash A/c 470

(Being motor expense is paid)

07/01/19 Capital A/c................................................................Dr. 1500

To Cash A/c 1500

(Being cash withdrawal by owner himself)

09/01/19 T. Cole A/c................................................................ Dr. 680

J. fox A/c................................................................ Dr. 1310

To Sales A/c 1990

(Being goods purchase on credit with various parties)

11/01/19 Sale Return A/c............................................................. Dr. 680

To J. Wilson A/c 270

To F. Syme A/c 410

6

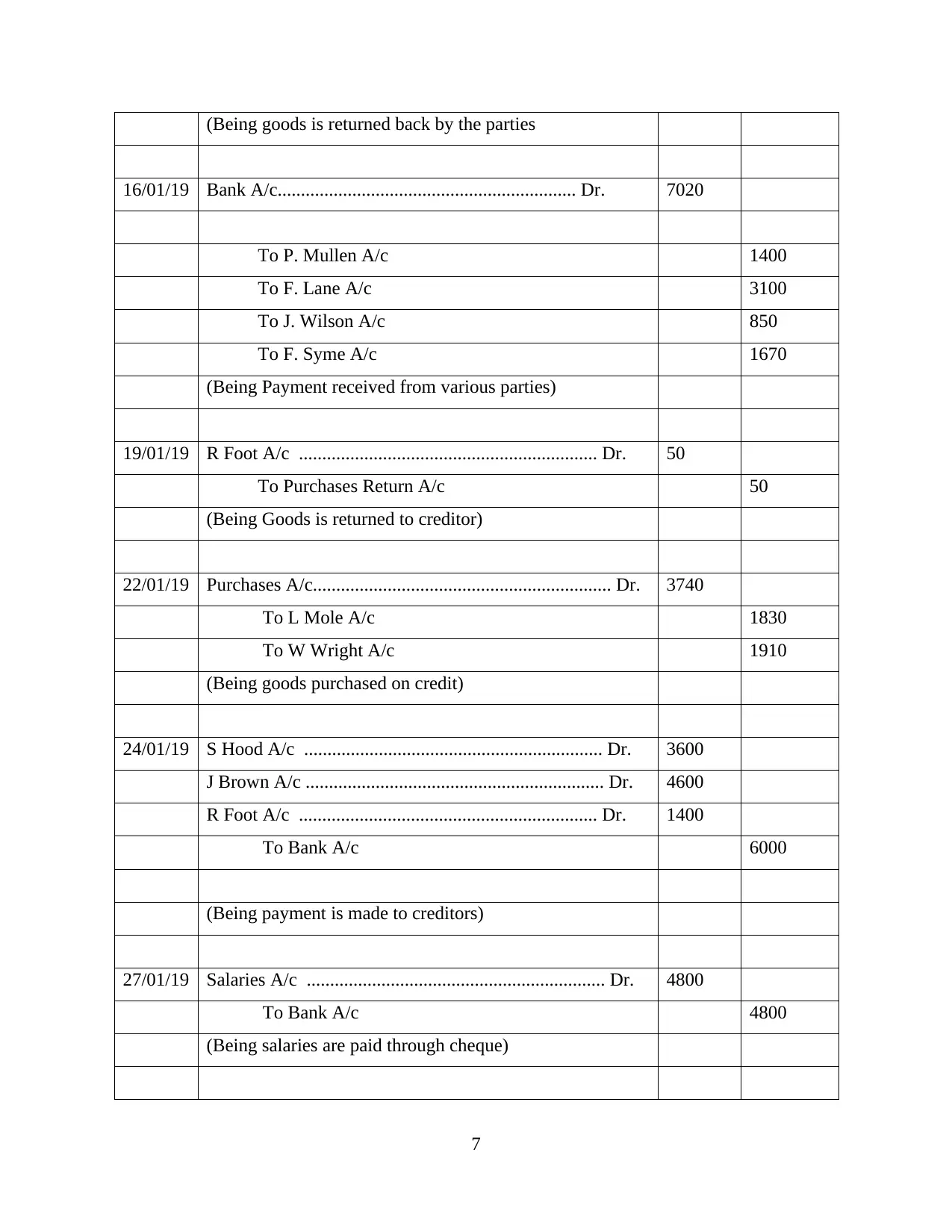

(Being goods is returned back by the parties

16/01/19 Bank A/c................................................................ Dr. 7020

To P. Mullen A/c 1400

To F. Lane A/c 3100

To J. Wilson A/c 850

To F. Syme A/c 1670

(Being Payment received from various parties)

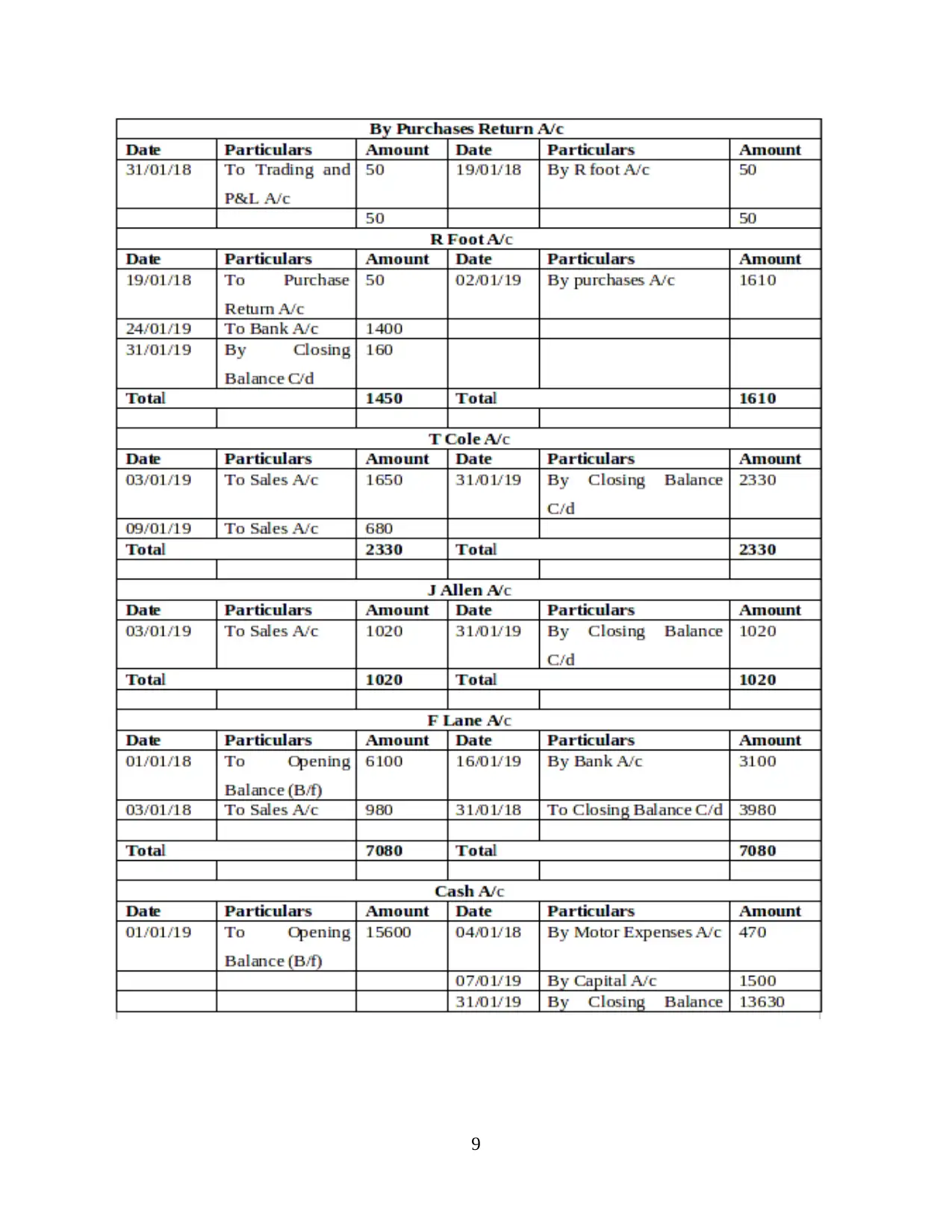

19/01/19 R Foot A/c ................................................................ Dr. 50

To Purchases Return A/c 50

(Being Goods is returned to creditor)

22/01/19 Purchases A/c................................................................ Dr. 3740

To L Mole A/c 1830

To W Wright A/c 1910

(Being goods purchased on credit)

24/01/19 S Hood A/c ................................................................ Dr. 3600

J Brown A/c ................................................................ Dr. 4600

R Foot A/c ................................................................ Dr. 1400

To Bank A/c 6000

(Being payment is made to creditors)

27/01/19 Salaries A/c ................................................................ Dr. 4800

To Bank A/c 4800

(Being salaries are paid through cheque)

7

16/01/19 Bank A/c................................................................ Dr. 7020

To P. Mullen A/c 1400

To F. Lane A/c 3100

To J. Wilson A/c 850

To F. Syme A/c 1670

(Being Payment received from various parties)

19/01/19 R Foot A/c ................................................................ Dr. 50

To Purchases Return A/c 50

(Being Goods is returned to creditor)

22/01/19 Purchases A/c................................................................ Dr. 3740

To L Mole A/c 1830

To W Wright A/c 1910

(Being goods purchased on credit)

24/01/19 S Hood A/c ................................................................ Dr. 3600

J Brown A/c ................................................................ Dr. 4600

R Foot A/c ................................................................ Dr. 1400

To Bank A/c 6000

(Being payment is made to creditors)

27/01/19 Salaries A/c ................................................................ Dr. 4800

To Bank A/c 4800

(Being salaries are paid through cheque)

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

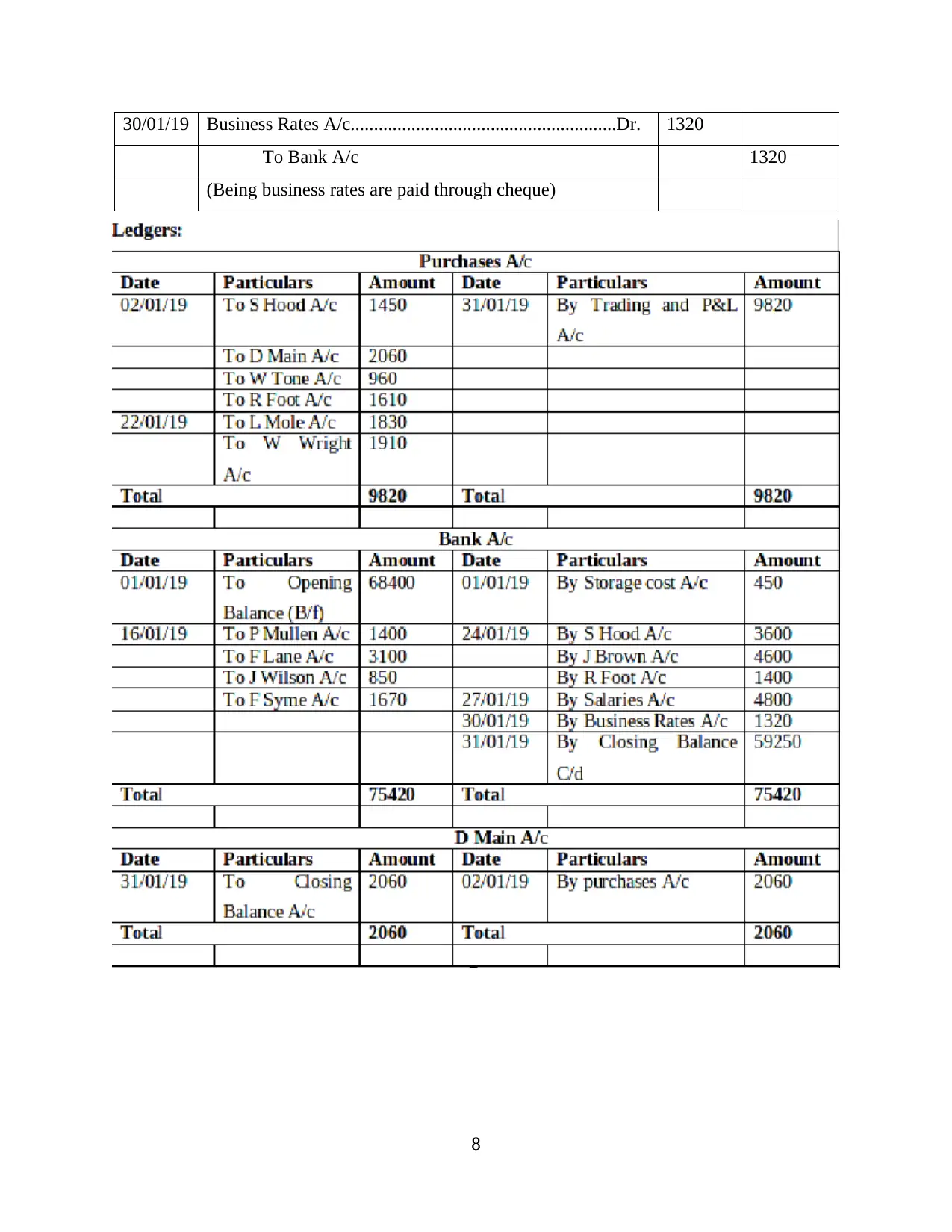

30/01/19 Business Rates A/c.........................................................Dr. 1320

To Bank A/c 1320

(Being business rates are paid through cheque)

8

To Bank A/c 1320

(Being business rates are paid through cheque)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.