Financial Accounting Report: Heritage and Biological Assets Analysis

VerifiedAdded on 2023/01/16

|8

|1653

|58

Report

AI Summary

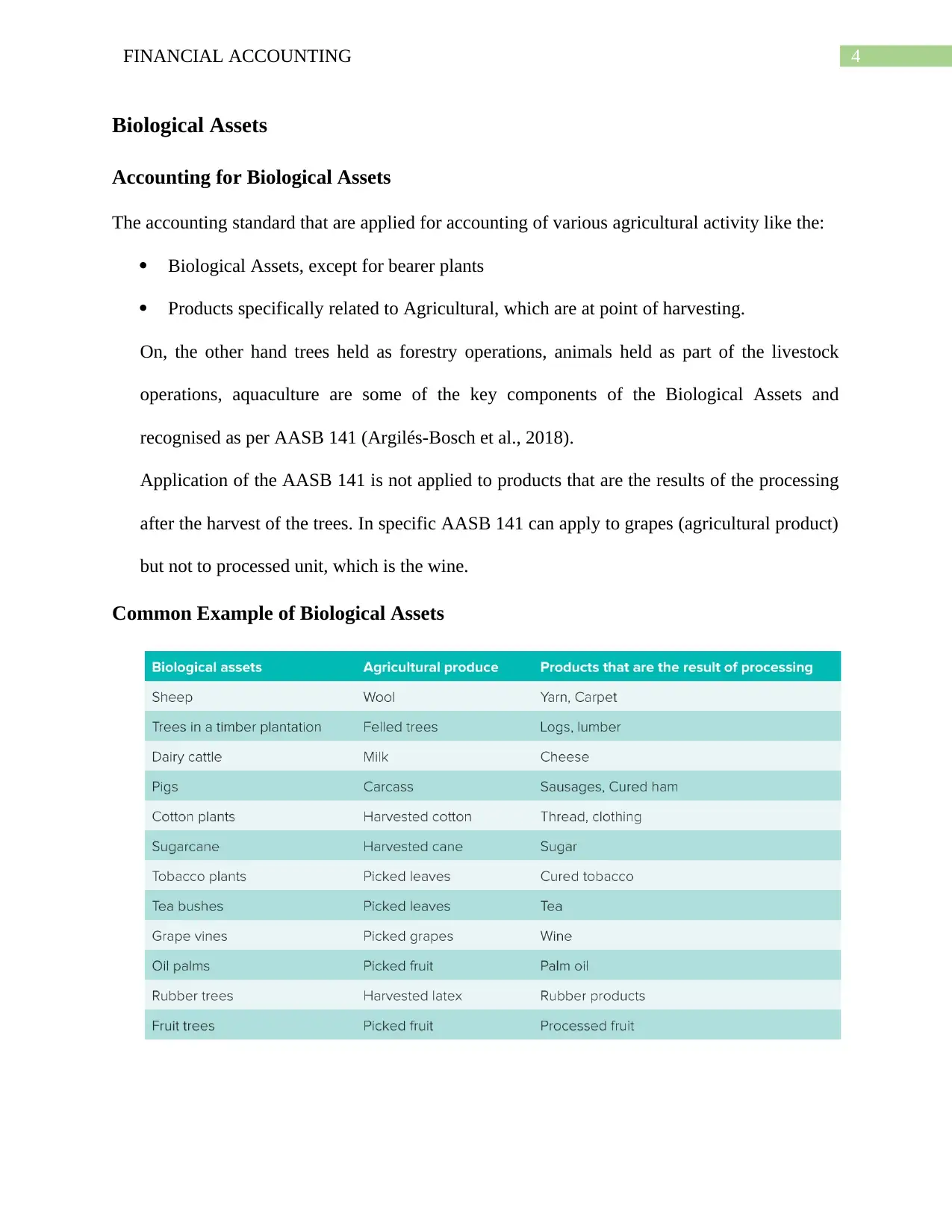

This report delves into the intricacies of financial accounting, specifically focusing on heritage and biological assets. It examines the accounting standards, namely AASB 116 for heritage assets and AASB 141 for biological assets, and their practical applications. The report discusses the definition, recognition, measurement, and classification of heritage assets, including their valuation methods like contingent valuation, travel cost, and market-based valuation. It also covers the accounting for biological assets, such as agricultural products, and the application of fair value measurement. The report differentiates between heritage assets and assets typically held by private-sector entities, highlighting the unique characteristics and challenges associated with each type. Furthermore, the report addresses the classification and reporting of these assets in financial statements, including the challenges in measurement and the importance of fair value assessment for biological assets. The report concludes by summarizing the key aspects of accounting for both asset types, offering valuable insights into their financial reporting. The report also includes references to the accounting standards and related literature.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.