Financial Accounting Report: Final Accounts and Bank Reconciliation

VerifiedAdded on 2023/01/18

|12

|3295

|41

Report

AI Summary

This report on financial accounting delves into the preparation of final accounts for both sole proprietorships and limited companies, including income statements and balance sheets. It explores the differences between these statements and provides a hypothetical example of a bank reconciliation statement, detailing the process of reconciling bank and company records. Furthermore, the report examines the reconciliation of control and suspense accounts, crucial for maintaining accurate financial records. The content includes practical examples and explanations, aiming to provide a clear understanding of key accounting concepts and their application in financial analysis and reporting. The report also discusses the importance of these processes in ensuring the accuracy and reliability of financial data, essential for informed decision-making by stakeholders.

FINANCIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

FINAL ACCOUNTS OF GREG PALMER.........................................................................................3

FINAL ACCOUNTS OF KENNY PATON LTD.................................................................................4

DIFFERENCES BETWEEN AN INCOME STATEMENT AND STATEMENT OF FINANCIAL

POSITION............................................................................................................................................5

HYPOTHETICAL EXAMPLE OF A BANK RECONCILIATION STATEMENT ...........................7

RECONCILIATION OF CONTROL AND SUSPENSE ACCOUNTS...............................................9

CONCLUSION...................................................................................................................................11

REFERENCES...................................................................................................................................12

INTRODUCTION................................................................................................................................3

FINAL ACCOUNTS OF GREG PALMER.........................................................................................3

FINAL ACCOUNTS OF KENNY PATON LTD.................................................................................4

DIFFERENCES BETWEEN AN INCOME STATEMENT AND STATEMENT OF FINANCIAL

POSITION............................................................................................................................................5

HYPOTHETICAL EXAMPLE OF A BANK RECONCILIATION STATEMENT ...........................7

RECONCILIATION OF CONTROL AND SUSPENSE ACCOUNTS...............................................9

CONCLUSION...................................................................................................................................11

REFERENCES...................................................................................................................................12

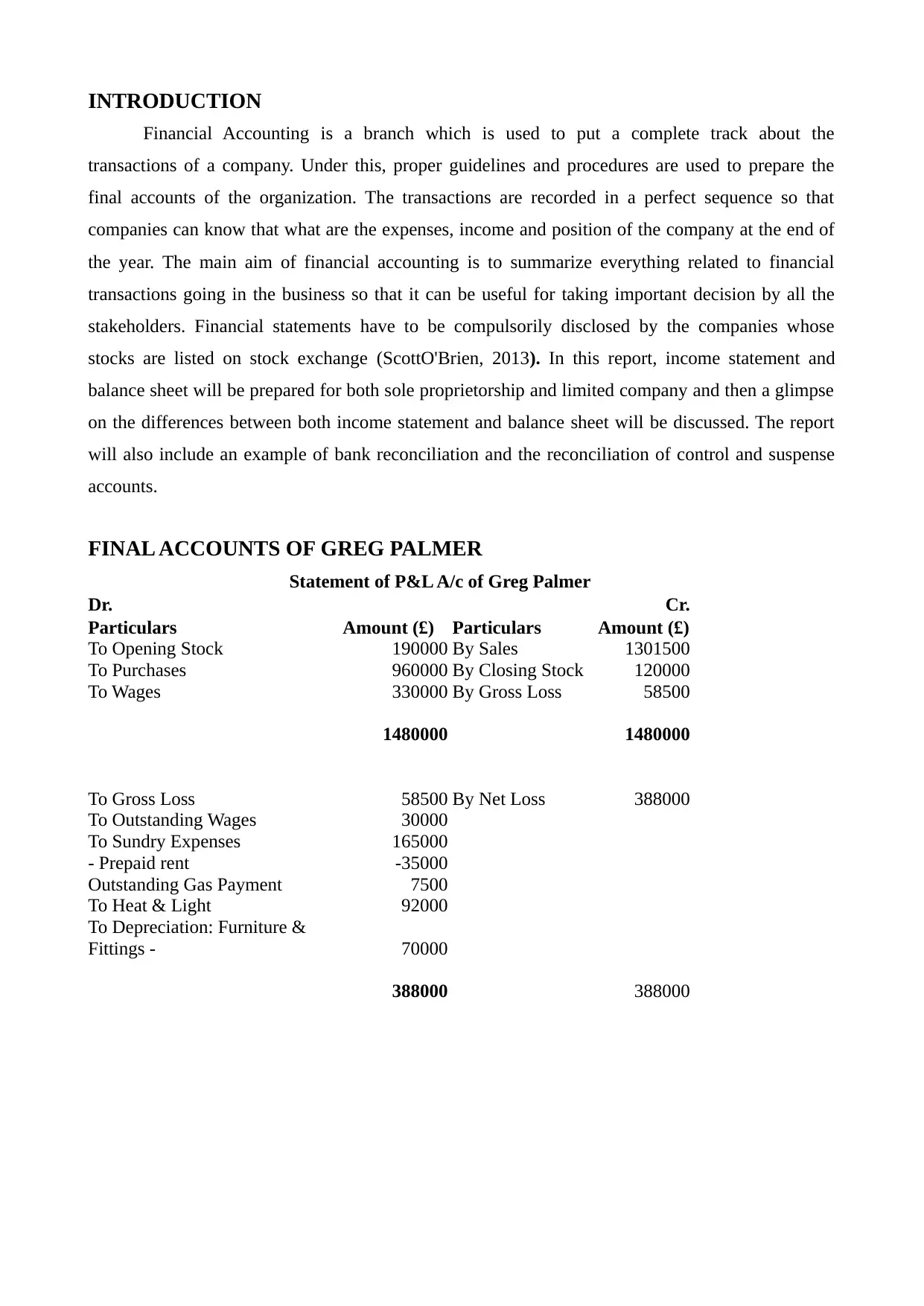

INTRODUCTION

Financial Accounting is a branch which is used to put a complete track about the

transactions of a company. Under this, proper guidelines and procedures are used to prepare the

final accounts of the organization. The transactions are recorded in a perfect sequence so that

companies can know that what are the expenses, income and position of the company at the end of

the year. The main aim of financial accounting is to summarize everything related to financial

transactions going in the business so that it can be useful for taking important decision by all the

stakeholders. Financial statements have to be compulsorily disclosed by the companies whose

stocks are listed on stock exchange (ScottO'Brien, 2013). In this report, income statement and

balance sheet will be prepared for both sole proprietorship and limited company and then a glimpse

on the differences between both income statement and balance sheet will be discussed. The report

will also include an example of bank reconciliation and the reconciliation of control and suspense

accounts.

FINAL ACCOUNTS OF GREG PALMER

Statement of P&L A/c of Greg Palmer

Dr. Cr.

Particulars Amount (£) Particulars Amount (£)

To Opening Stock 190000 By Sales 1301500

To Purchases 960000 By Closing Stock 120000

To Wages 330000 By Gross Loss 58500

1480000 1480000

To Gross Loss 58500 By Net Loss 388000

To Outstanding Wages 30000

To Sundry Expenses 165000

- Prepaid rent -35000

Outstanding Gas Payment 7500

To Heat & Light 92000

To Depreciation: Furniture &

Fittings - 70000

388000 388000

Financial Accounting is a branch which is used to put a complete track about the

transactions of a company. Under this, proper guidelines and procedures are used to prepare the

final accounts of the organization. The transactions are recorded in a perfect sequence so that

companies can know that what are the expenses, income and position of the company at the end of

the year. The main aim of financial accounting is to summarize everything related to financial

transactions going in the business so that it can be useful for taking important decision by all the

stakeholders. Financial statements have to be compulsorily disclosed by the companies whose

stocks are listed on stock exchange (ScottO'Brien, 2013). In this report, income statement and

balance sheet will be prepared for both sole proprietorship and limited company and then a glimpse

on the differences between both income statement and balance sheet will be discussed. The report

will also include an example of bank reconciliation and the reconciliation of control and suspense

accounts.

FINAL ACCOUNTS OF GREG PALMER

Statement of P&L A/c of Greg Palmer

Dr. Cr.

Particulars Amount (£) Particulars Amount (£)

To Opening Stock 190000 By Sales 1301500

To Purchases 960000 By Closing Stock 120000

To Wages 330000 By Gross Loss 58500

1480000 1480000

To Gross Loss 58500 By Net Loss 388000

To Outstanding Wages 30000

To Sundry Expenses 165000

- Prepaid rent -35000

Outstanding Gas Payment 7500

To Heat & Light 92000

To Depreciation: Furniture &

Fittings - 70000

388000 388000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Balance Sheet for Greg Palmer as on..

Liabilities Amount (£) Assets Amount (£)

Capital 960500

Account

Receivables 120000

- Net Loss -388000 Prepaid Rent 35000

- Drawings -105000 Closing Stock 120000

Bank Overdraft 50000

Fixtures and

fittings 350000

Outstanding Gas Payment 7500 - Depreciation -70000 280000

Outstanding Wages 30000

555000 555000

FINAL ACCOUNTS OF KENNY PATON LTD.

Statement of P&L A/c of Kenny Paton Ltd.

Dr. Cr.

Particulars Amount (£) Particulars

Amount

(£)

To Opening Stock 86000 By Sales 2068000

To Purchases 1054000 By Closing Stock 78000

To Gross Profit 1006000

2146000 2146000

To Distribution Costs 367000 By Gross Profit 1006000

To Administration Costs 287000

To Outstanding Interest 14274

To Outstanding Dividend 152000

To Depreciation:

On Plant & Machinery 119700

On Office Equipment 26400

To Outstanding

Corporation Tax 30000

To Net Profit 9626

1006000 1006000

Balance Sheet for Kenny Paton as on..

Liabilities Amount (£) Assets Amount (£)

£1 ordinary shares fully

paid 1520000 Account Receivables 619000

Net Profit 9626 Bank 45000

Dividend declared 152000 Closing Stock 78000

Bank Loan 549000 Premises 1345000

Outstanding Interest 14274 Plant & Equipment 798000

Trade Payables 640000 - Depreciation 119700 678300

Outstanding Corporation 30000 Office Equipment 176000

Liabilities Amount (£) Assets Amount (£)

Capital 960500

Account

Receivables 120000

- Net Loss -388000 Prepaid Rent 35000

- Drawings -105000 Closing Stock 120000

Bank Overdraft 50000

Fixtures and

fittings 350000

Outstanding Gas Payment 7500 - Depreciation -70000 280000

Outstanding Wages 30000

555000 555000

FINAL ACCOUNTS OF KENNY PATON LTD.

Statement of P&L A/c of Kenny Paton Ltd.

Dr. Cr.

Particulars Amount (£) Particulars

Amount

(£)

To Opening Stock 86000 By Sales 2068000

To Purchases 1054000 By Closing Stock 78000

To Gross Profit 1006000

2146000 2146000

To Distribution Costs 367000 By Gross Profit 1006000

To Administration Costs 287000

To Outstanding Interest 14274

To Outstanding Dividend 152000

To Depreciation:

On Plant & Machinery 119700

On Office Equipment 26400

To Outstanding

Corporation Tax 30000

To Net Profit 9626

1006000 1006000

Balance Sheet for Kenny Paton as on..

Liabilities Amount (£) Assets Amount (£)

£1 ordinary shares fully

paid 1520000 Account Receivables 619000

Net Profit 9626 Bank 45000

Dividend declared 152000 Closing Stock 78000

Bank Loan 549000 Premises 1345000

Outstanding Interest 14274 Plant & Equipment 798000

Trade Payables 640000 - Depreciation 119700 678300

Outstanding Corporation 30000 Office Equipment 176000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

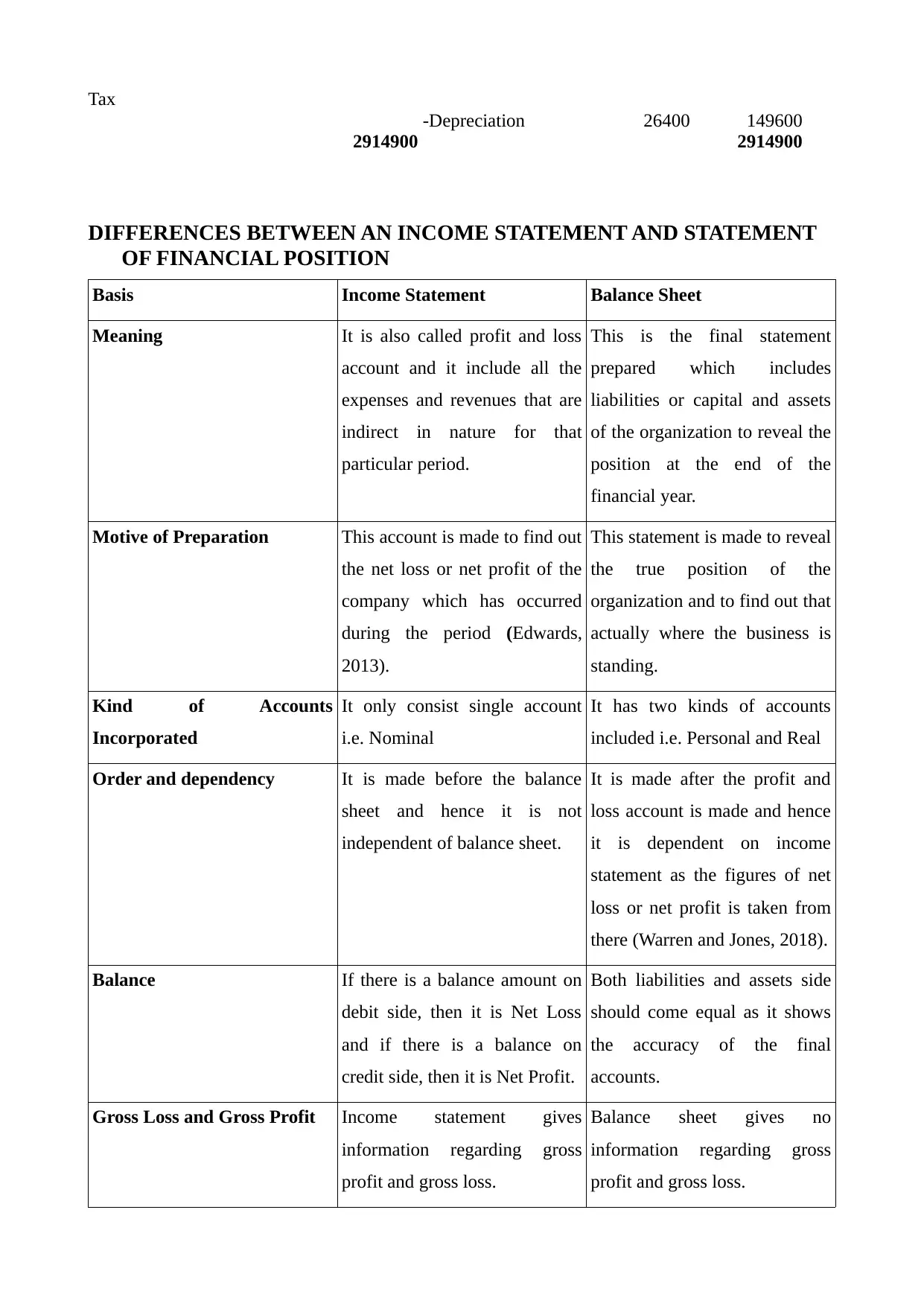

Tax

-Depreciation 26400 149600

2914900 2914900

DIFFERENCES BETWEEN AN INCOME STATEMENT AND STATEMENT

OF FINANCIAL POSITION

Basis Income Statement Balance Sheet

Meaning It is also called profit and loss

account and it include all the

expenses and revenues that are

indirect in nature for that

particular period.

This is the final statement

prepared which includes

liabilities or capital and assets

of the organization to reveal the

position at the end of the

financial year.

Motive of Preparation This account is made to find out

the net loss or net profit of the

company which has occurred

during the period (Edwards,

2013).

This statement is made to reveal

the true position of the

organization and to find out that

actually where the business is

standing.

Kind of Accounts

Incorporated

It only consist single account

i.e. Nominal

It has two kinds of accounts

included i.e. Personal and Real

Order and dependency It is made before the balance

sheet and hence it is not

independent of balance sheet.

It is made after the profit and

loss account is made and hence

it is dependent on income

statement as the figures of net

loss or net profit is taken from

there (Warren and Jones, 2018).

Balance If there is a balance amount on

debit side, then it is Net Loss

and if there is a balance on

credit side, then it is Net Profit.

Both liabilities and assets side

should come equal as it shows

the accuracy of the final

accounts.

Gross Loss and Gross Profit Income statement gives

information regarding gross

profit and gross loss.

Balance sheet gives no

information regarding gross

profit and gross loss.

-Depreciation 26400 149600

2914900 2914900

DIFFERENCES BETWEEN AN INCOME STATEMENT AND STATEMENT

OF FINANCIAL POSITION

Basis Income Statement Balance Sheet

Meaning It is also called profit and loss

account and it include all the

expenses and revenues that are

indirect in nature for that

particular period.

This is the final statement

prepared which includes

liabilities or capital and assets

of the organization to reveal the

position at the end of the

financial year.

Motive of Preparation This account is made to find out

the net loss or net profit of the

company which has occurred

during the period (Edwards,

2013).

This statement is made to reveal

the true position of the

organization and to find out that

actually where the business is

standing.

Kind of Accounts

Incorporated

It only consist single account

i.e. Nominal

It has two kinds of accounts

included i.e. Personal and Real

Order and dependency It is made before the balance

sheet and hence it is not

independent of balance sheet.

It is made after the profit and

loss account is made and hence

it is dependent on income

statement as the figures of net

loss or net profit is taken from

there (Warren and Jones, 2018).

Balance If there is a balance amount on

debit side, then it is Net Loss

and if there is a balance on

credit side, then it is Net Profit.

Both liabilities and assets side

should come equal as it shows

the accuracy of the final

accounts.

Gross Loss and Gross Profit Income statement gives

information regarding gross

profit and gross loss.

Balance sheet gives no

information regarding gross

profit and gross loss.

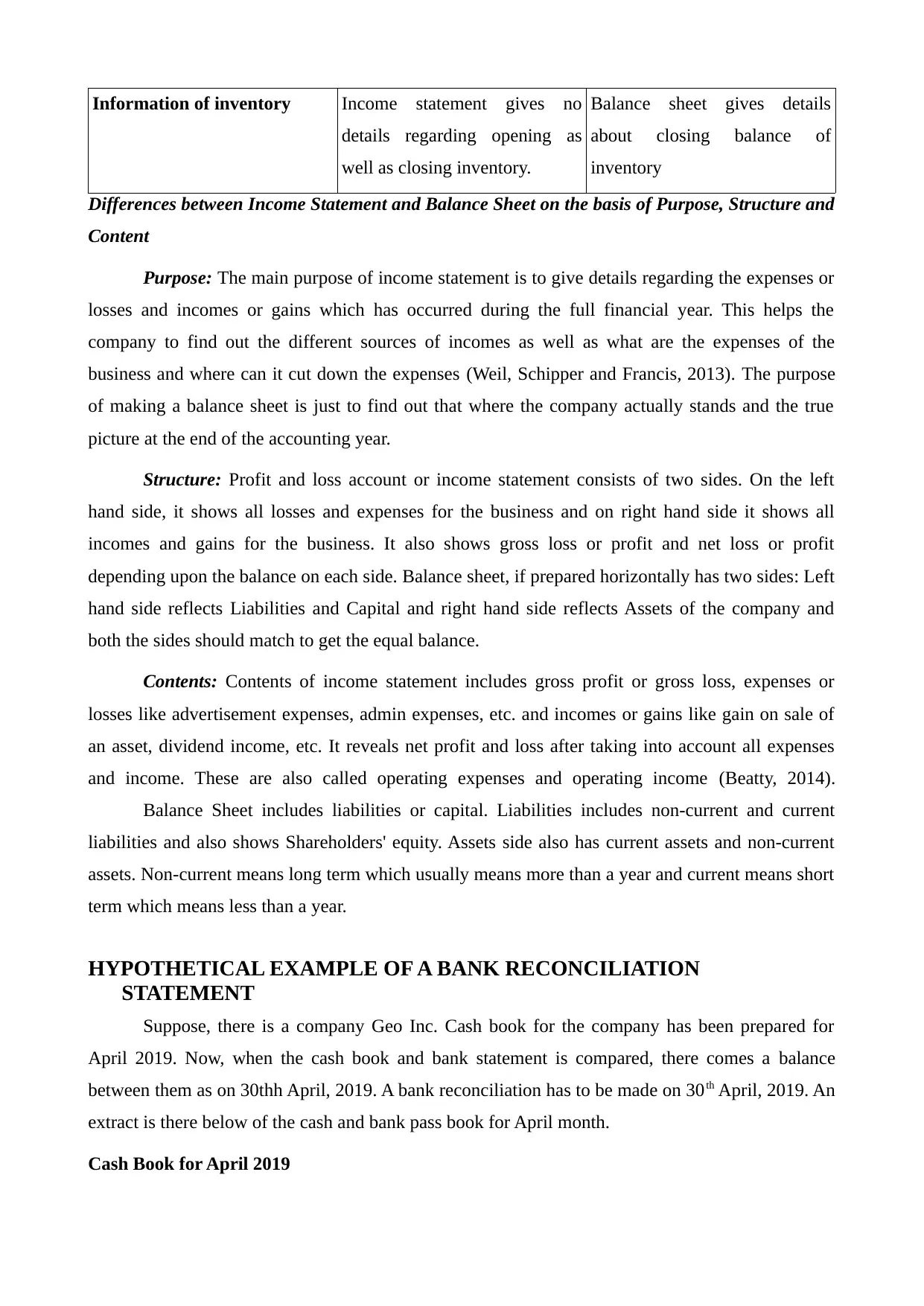

Information of inventory Income statement gives no

details regarding opening as

well as closing inventory.

Balance sheet gives details

about closing balance of

inventory

Differences between Income Statement and Balance Sheet on the basis of Purpose, Structure and

Content

Purpose: The main purpose of income statement is to give details regarding the expenses or

losses and incomes or gains which has occurred during the full financial year. This helps the

company to find out the different sources of incomes as well as what are the expenses of the

business and where can it cut down the expenses (Weil, Schipper and Francis, 2013). The purpose

of making a balance sheet is just to find out that where the company actually stands and the true

picture at the end of the accounting year.

Structure: Profit and loss account or income statement consists of two sides. On the left

hand side, it shows all losses and expenses for the business and on right hand side it shows all

incomes and gains for the business. It also shows gross loss or profit and net loss or profit

depending upon the balance on each side. Balance sheet, if prepared horizontally has two sides: Left

hand side reflects Liabilities and Capital and right hand side reflects Assets of the company and

both the sides should match to get the equal balance.

Contents: Contents of income statement includes gross profit or gross loss, expenses or

losses like advertisement expenses, admin expenses, etc. and incomes or gains like gain on sale of

an asset, dividend income, etc. It reveals net profit and loss after taking into account all expenses

and income. These are also called operating expenses and operating income (Beatty, 2014).

Balance Sheet includes liabilities or capital. Liabilities includes non-current and current

liabilities and also shows Shareholders' equity. Assets side also has current assets and non-current

assets. Non-current means long term which usually means more than a year and current means short

term which means less than a year.

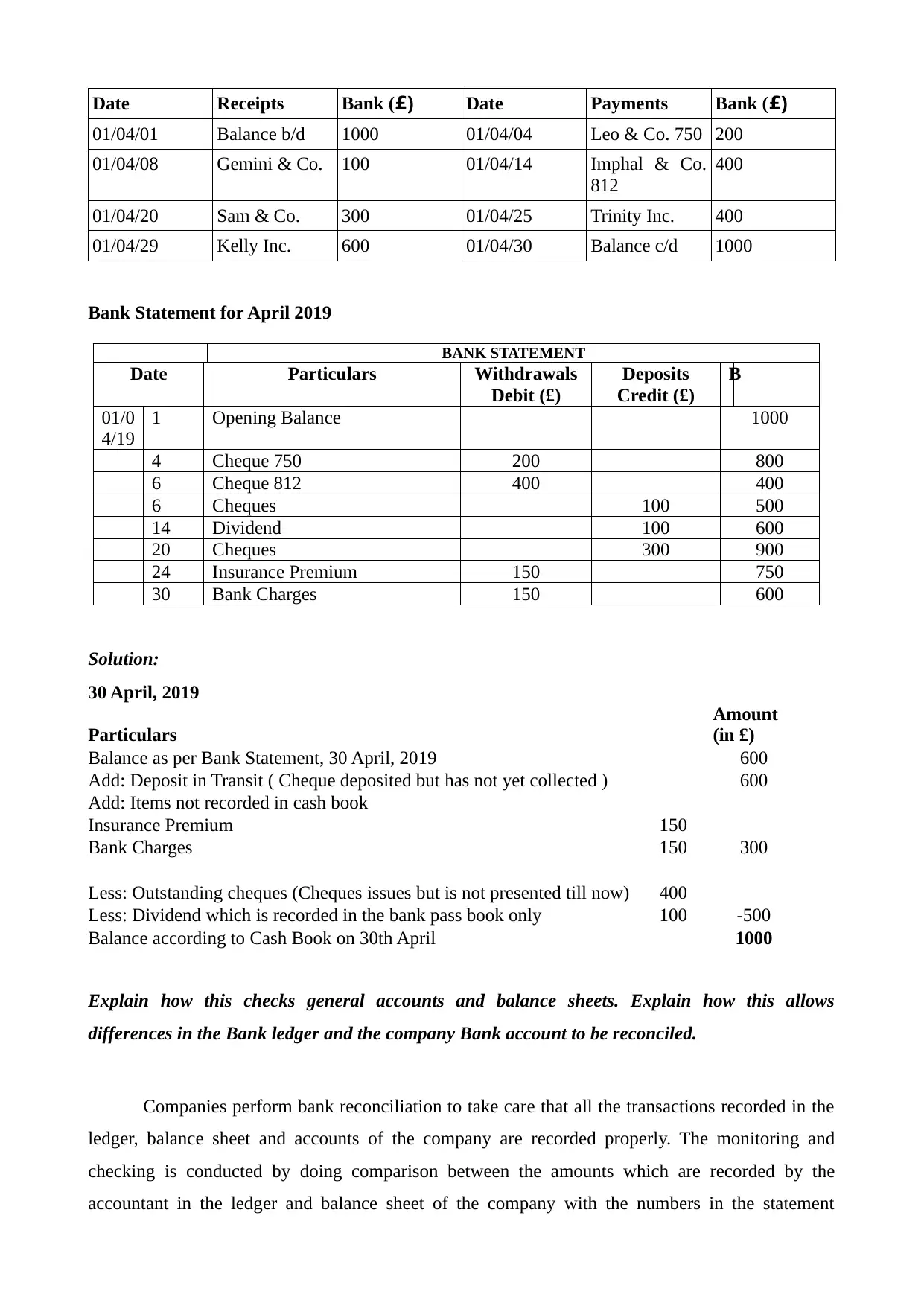

HYPOTHETICAL EXAMPLE OF A BANK RECONCILIATION

STATEMENT

Suppose, there is a company Geo Inc. Cash book for the company has been prepared for

April 2019. Now, when the cash book and bank statement is compared, there comes a balance

between them as on 30thh April, 2019. A bank reconciliation has to be made on 30th April, 2019. An

extract is there below of the cash and bank pass book for April month.

Cash Book for April 2019

details regarding opening as

well as closing inventory.

Balance sheet gives details

about closing balance of

inventory

Differences between Income Statement and Balance Sheet on the basis of Purpose, Structure and

Content

Purpose: The main purpose of income statement is to give details regarding the expenses or

losses and incomes or gains which has occurred during the full financial year. This helps the

company to find out the different sources of incomes as well as what are the expenses of the

business and where can it cut down the expenses (Weil, Schipper and Francis, 2013). The purpose

of making a balance sheet is just to find out that where the company actually stands and the true

picture at the end of the accounting year.

Structure: Profit and loss account or income statement consists of two sides. On the left

hand side, it shows all losses and expenses for the business and on right hand side it shows all

incomes and gains for the business. It also shows gross loss or profit and net loss or profit

depending upon the balance on each side. Balance sheet, if prepared horizontally has two sides: Left

hand side reflects Liabilities and Capital and right hand side reflects Assets of the company and

both the sides should match to get the equal balance.

Contents: Contents of income statement includes gross profit or gross loss, expenses or

losses like advertisement expenses, admin expenses, etc. and incomes or gains like gain on sale of

an asset, dividend income, etc. It reveals net profit and loss after taking into account all expenses

and income. These are also called operating expenses and operating income (Beatty, 2014).

Balance Sheet includes liabilities or capital. Liabilities includes non-current and current

liabilities and also shows Shareholders' equity. Assets side also has current assets and non-current

assets. Non-current means long term which usually means more than a year and current means short

term which means less than a year.

HYPOTHETICAL EXAMPLE OF A BANK RECONCILIATION

STATEMENT

Suppose, there is a company Geo Inc. Cash book for the company has been prepared for

April 2019. Now, when the cash book and bank statement is compared, there comes a balance

between them as on 30thh April, 2019. A bank reconciliation has to be made on 30th April, 2019. An

extract is there below of the cash and bank pass book for April month.

Cash Book for April 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Date Receipts Bank (£) Date Payments Bank (£)

01/04/01 Balance b/d 1000 01/04/04 Leo & Co. 750 200

01/04/08 Gemini & Co. 100 01/04/14 Imphal & Co.

812

400

01/04/20 Sam & Co. 300 01/04/25 Trinity Inc. 400

01/04/29 Kelly Inc. 600 01/04/30 Balance c/d 1000

Bank Statement for April 2019

BANK STATEMENT

Date Particulars Withdrawals

Debit (£)

Deposits

Credit (£)

B

01/0

4/19

1 Opening Balance 1000

4 Cheque 750 200 800

6 Cheque 812 400 400

6 Cheques 100 500

14 Dividend 100 600

20 Cheques 300 900

24 Insurance Premium 150 750

30 Bank Charges 150 600

Solution:

30 April, 2019

Particulars

Amount

(in £)

Balance as per Bank Statement, 30 April, 2019 600

Add: Deposit in Transit ( Cheque deposited but has not yet collected ) 600

Add: Items not recorded in cash book

Insurance Premium 150

Bank Charges 150 300

Less: Outstanding cheques (Cheques issues but is not presented till now) 400

Less: Dividend which is recorded in the bank pass book only 100 -500

Balance according to Cash Book on 30th April 1000

Explain how this checks general accounts and balance sheets. Explain how this allows

differences in the Bank ledger and the company Bank account to be reconciled.

Companies perform bank reconciliation to take care that all the transactions recorded in the

ledger, balance sheet and accounts of the company are recorded properly. The monitoring and

checking is conducted by doing comparison between the amounts which are recorded by the

accountant in the ledger and balance sheet of the company with the numbers in the statement

01/04/01 Balance b/d 1000 01/04/04 Leo & Co. 750 200

01/04/08 Gemini & Co. 100 01/04/14 Imphal & Co.

812

400

01/04/20 Sam & Co. 300 01/04/25 Trinity Inc. 400

01/04/29 Kelly Inc. 600 01/04/30 Balance c/d 1000

Bank Statement for April 2019

BANK STATEMENT

Date Particulars Withdrawals

Debit (£)

Deposits

Credit (£)

B

01/0

4/19

1 Opening Balance 1000

4 Cheque 750 200 800

6 Cheque 812 400 400

6 Cheques 100 500

14 Dividend 100 600

20 Cheques 300 900

24 Insurance Premium 150 750

30 Bank Charges 150 600

Solution:

30 April, 2019

Particulars

Amount

(in £)

Balance as per Bank Statement, 30 April, 2019 600

Add: Deposit in Transit ( Cheque deposited but has not yet collected ) 600

Add: Items not recorded in cash book

Insurance Premium 150

Bank Charges 150 300

Less: Outstanding cheques (Cheques issues but is not presented till now) 400

Less: Dividend which is recorded in the bank pass book only 100 -500

Balance according to Cash Book on 30th April 1000

Explain how this checks general accounts and balance sheets. Explain how this allows

differences in the Bank ledger and the company Bank account to be reconciled.

Companies perform bank reconciliation to take care that all the transactions recorded in the

ledger, balance sheet and accounts of the company are recorded properly. The monitoring and

checking is conducted by doing comparison between the amounts which are recorded by the

accountant in the ledger and balance sheet of the company with the numbers in the statement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

generated by the bank. If any differences occur, then proper justification has to be there and if there

are no differences then it can be concluded that the statement of bank is reconciled (Taipaleenmäki

and Ikäheimo, 2013).

Bank reconciliation is very crucial area of accounting and important to prepare for the

companies to understand and rectify if there are any kind of errors or mistakes between the bank

balance and the balance which comes from ledgers made by the businesses. Reconciliation helps

the company to search for the exact errors between the general accounts and the bank. With this the

company can find the cash balance in the end (Parson and et. al., 2015). The differences occurs due

to some cheques which are outstanding which means these cheques have been issued but still not

presented and also due to some deposits which are there in the transit, these are the kind of cheques

which are deposited but it has not yet taken by the company. While reconciling, the accountants

keep in mind to deduct these outstanding cheques and add back these deposited cheques. The ledger

balance and bank balance matches once this process is completed.

As per the size of the companies, there are many cheques which are outstanding and many

cheques which may have been deposited by the debtors but it is not yet processed in the bank. For

example: If the company has paid to its suppliers, this transaction has come into the ledgers of the

company but processing takes time from the bank side and it may take few weeks to process. So, till

that time it might not be included in the monthly statement of the company. These kind of

transactions have to be kept in mind to get the actual cash balance of the company and the

adjustments have to be made for the reconciliation purpose.

Errors in Reconciliation Process: Accountant must make adjustments in the ledger for the

following: Bank charges like charges for insufficient funds, interest charges, charges for

maintenance of the account. At last, when the complete reconciliation is done then figures of

statement generated by the bank and the balance in general ledger must match and if it does not

match then errors have to be checked. Errors can be generally in the determination of outstanding as

well as deposit cheques or there may be errors due to the incorrect numbers recorded or the

numbers are mixed and transposed. It should be kept in mind that all the cheques which are cleared

by the bank are recorded into the ledger.

RECONCILIATION OF CONTROL AND SUSPENSE ACCOUNTS

Control Account: Control account is a account which provides summary of accounts

receivables or debtors and accounts payables or creditors. As both debtors and creditors comprises

of huge transactions and have huge volume, so there comes the requirement of separating them

from the general ledger and make a subsidiary ledger. This makes the transactions easy to

are no differences then it can be concluded that the statement of bank is reconciled (Taipaleenmäki

and Ikäheimo, 2013).

Bank reconciliation is very crucial area of accounting and important to prepare for the

companies to understand and rectify if there are any kind of errors or mistakes between the bank

balance and the balance which comes from ledgers made by the businesses. Reconciliation helps

the company to search for the exact errors between the general accounts and the bank. With this the

company can find the cash balance in the end (Parson and et. al., 2015). The differences occurs due

to some cheques which are outstanding which means these cheques have been issued but still not

presented and also due to some deposits which are there in the transit, these are the kind of cheques

which are deposited but it has not yet taken by the company. While reconciling, the accountants

keep in mind to deduct these outstanding cheques and add back these deposited cheques. The ledger

balance and bank balance matches once this process is completed.

As per the size of the companies, there are many cheques which are outstanding and many

cheques which may have been deposited by the debtors but it is not yet processed in the bank. For

example: If the company has paid to its suppliers, this transaction has come into the ledgers of the

company but processing takes time from the bank side and it may take few weeks to process. So, till

that time it might not be included in the monthly statement of the company. These kind of

transactions have to be kept in mind to get the actual cash balance of the company and the

adjustments have to be made for the reconciliation purpose.

Errors in Reconciliation Process: Accountant must make adjustments in the ledger for the

following: Bank charges like charges for insufficient funds, interest charges, charges for

maintenance of the account. At last, when the complete reconciliation is done then figures of

statement generated by the bank and the balance in general ledger must match and if it does not

match then errors have to be checked. Errors can be generally in the determination of outstanding as

well as deposit cheques or there may be errors due to the incorrect numbers recorded or the

numbers are mixed and transposed. It should be kept in mind that all the cheques which are cleared

by the bank are recorded into the ledger.

RECONCILIATION OF CONTROL AND SUSPENSE ACCOUNTS

Control Account: Control account is a account which provides summary of accounts

receivables or debtors and accounts payables or creditors. As both debtors and creditors comprises

of huge transactions and have huge volume, so there comes the requirement of separating them

from the general ledger and make a subsidiary ledger. This makes the transactions easy to

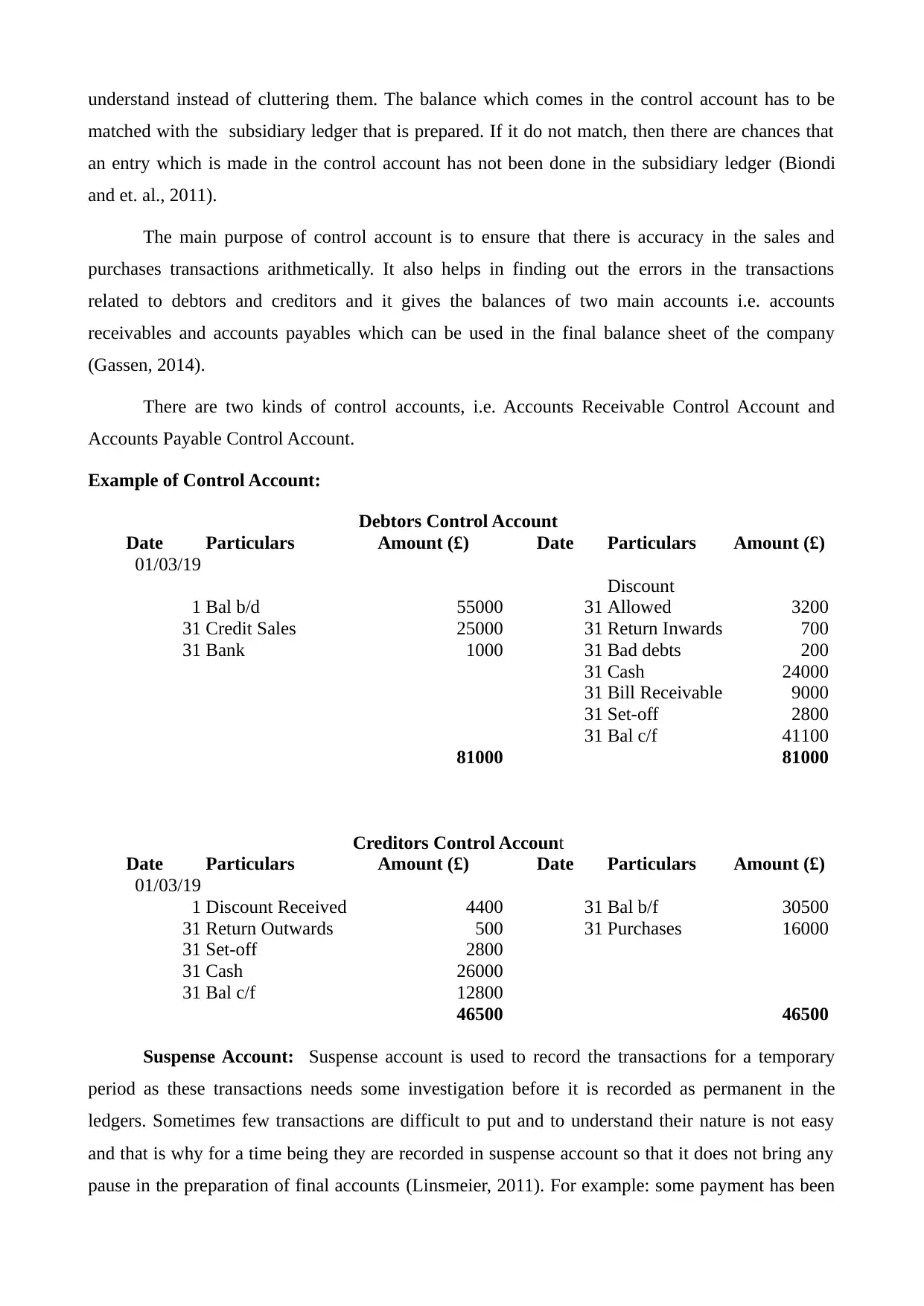

understand instead of cluttering them. The balance which comes in the control account has to be

matched with the subsidiary ledger that is prepared. If it do not match, then there are chances that

an entry which is made in the control account has not been done in the subsidiary ledger (Biondi

and et. al., 2011).

The main purpose of control account is to ensure that there is accuracy in the sales and

purchases transactions arithmetically. It also helps in finding out the errors in the transactions

related to debtors and creditors and it gives the balances of two main accounts i.e. accounts

receivables and accounts payables which can be used in the final balance sheet of the company

(Gassen, 2014).

There are two kinds of control accounts, i.e. Accounts Receivable Control Account and

Accounts Payable Control Account.

Example of Control Account:

Debtors Control Account

Date Particulars Amount (£) Date Particulars Amount (£)

01/03/19

1 Bal b/d 55000 31

Discount

Allowed 3200

31 Credit Sales 25000 31 Return Inwards 700

31 Bank 1000 31 Bad debts 200

31 Cash 24000

31 Bill Receivable 9000

31 Set-off 2800

31 Bal c/f 41100

81000 81000

Creditors Control Account

Date Particulars Amount (£) Date Particulars Amount (£)

01/03/19

1 Discount Received 4400 31 Bal b/f 30500

31 Return Outwards 500 31 Purchases 16000

31 Set-off 2800

31 Cash 26000

31 Bal c/f 12800

46500 46500

Suspense Account: Suspense account is used to record the transactions for a temporary

period as these transactions needs some investigation before it is recorded as permanent in the

ledgers. Sometimes few transactions are difficult to put and to understand their nature is not easy

and that is why for a time being they are recorded in suspense account so that it does not bring any

pause in the preparation of final accounts (Linsmeier, 2011). For example: some payment has been

matched with the subsidiary ledger that is prepared. If it do not match, then there are chances that

an entry which is made in the control account has not been done in the subsidiary ledger (Biondi

and et. al., 2011).

The main purpose of control account is to ensure that there is accuracy in the sales and

purchases transactions arithmetically. It also helps in finding out the errors in the transactions

related to debtors and creditors and it gives the balances of two main accounts i.e. accounts

receivables and accounts payables which can be used in the final balance sheet of the company

(Gassen, 2014).

There are two kinds of control accounts, i.e. Accounts Receivable Control Account and

Accounts Payable Control Account.

Example of Control Account:

Debtors Control Account

Date Particulars Amount (£) Date Particulars Amount (£)

01/03/19

1 Bal b/d 55000 31

Discount

Allowed 3200

31 Credit Sales 25000 31 Return Inwards 700

31 Bank 1000 31 Bad debts 200

31 Cash 24000

31 Bill Receivable 9000

31 Set-off 2800

31 Bal c/f 41100

81000 81000

Creditors Control Account

Date Particulars Amount (£) Date Particulars Amount (£)

01/03/19

1 Discount Received 4400 31 Bal b/f 30500

31 Return Outwards 500 31 Purchases 16000

31 Set-off 2800

31 Cash 26000

31 Bal c/f 12800

46500 46500

Suspense Account: Suspense account is used to record the transactions for a temporary

period as these transactions needs some investigation before it is recorded as permanent in the

ledgers. Sometimes few transactions are difficult to put and to understand their nature is not easy

and that is why for a time being they are recorded in suspense account so that it does not bring any

pause in the preparation of final accounts (Linsmeier, 2011). For example: some payment has been

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

credited with the wrong account details or the information is vague, amounts which are for legal

conflict, etc.

Suspense account is also reconciled on a timely basis so that there are no discrepancies in the end

and all transactions match with each other.

Example of Suspense Account:

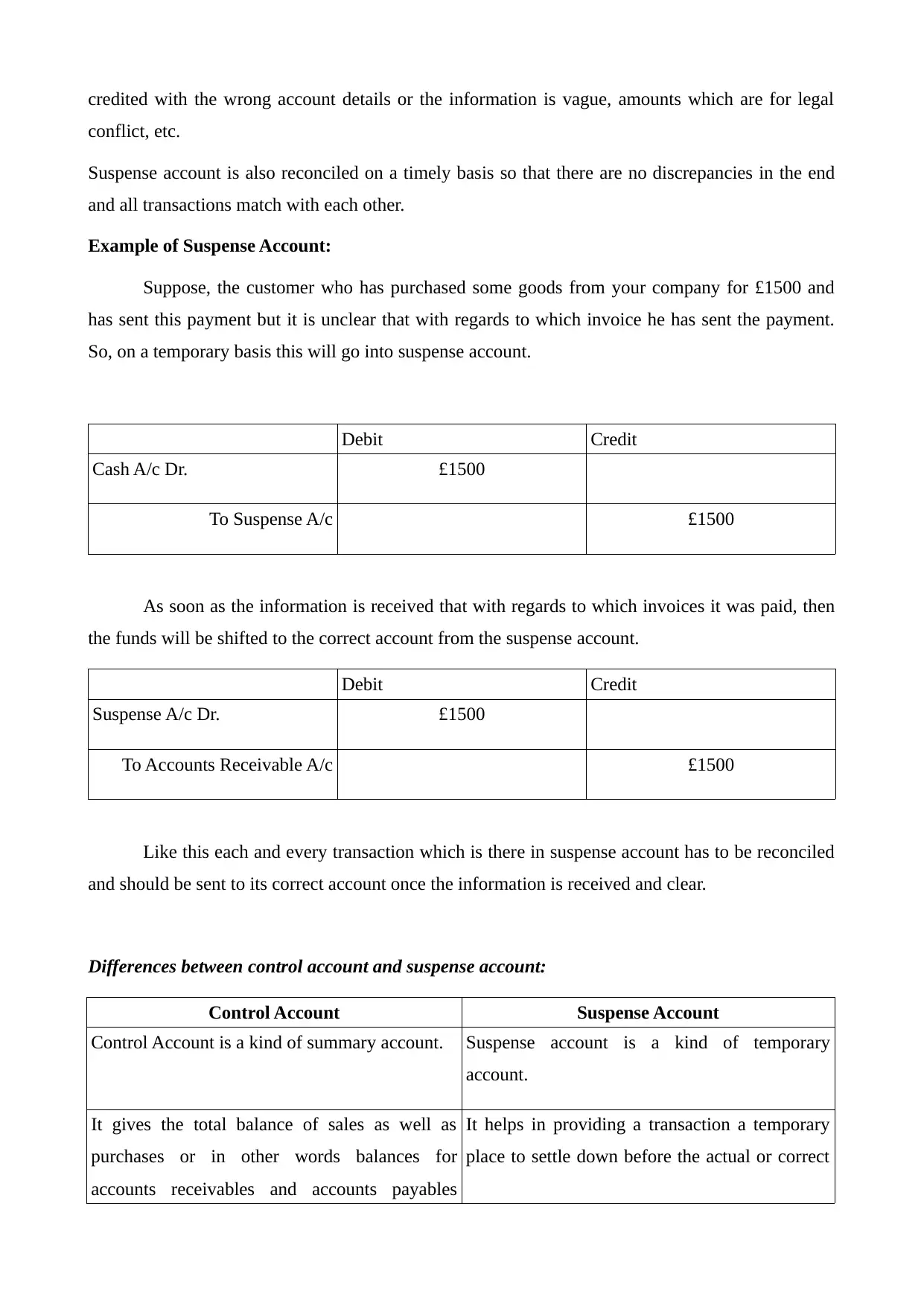

Suppose, the customer who has purchased some goods from your company for £1500 and

has sent this payment but it is unclear that with regards to which invoice he has sent the payment.

So, on a temporary basis this will go into suspense account.

Debit Credit

Cash A/c Dr. £1500

To Suspense A/c £1500

As soon as the information is received that with regards to which invoices it was paid, then

the funds will be shifted to the correct account from the suspense account.

Debit Credit

Suspense A/c Dr. £1500

To Accounts Receivable A/c £1500

Like this each and every transaction which is there in suspense account has to be reconciled

and should be sent to its correct account once the information is received and clear.

Differences between control account and suspense account:

Control Account Suspense Account

Control Account is a kind of summary account. Suspense account is a kind of temporary

account.

It gives the total balance of sales as well as

purchases or in other words balances for

accounts receivables and accounts payables

It helps in providing a transaction a temporary

place to settle down before the actual or correct

conflict, etc.

Suspense account is also reconciled on a timely basis so that there are no discrepancies in the end

and all transactions match with each other.

Example of Suspense Account:

Suppose, the customer who has purchased some goods from your company for £1500 and

has sent this payment but it is unclear that with regards to which invoice he has sent the payment.

So, on a temporary basis this will go into suspense account.

Debit Credit

Cash A/c Dr. £1500

To Suspense A/c £1500

As soon as the information is received that with regards to which invoices it was paid, then

the funds will be shifted to the correct account from the suspense account.

Debit Credit

Suspense A/c Dr. £1500

To Accounts Receivable A/c £1500

Like this each and every transaction which is there in suspense account has to be reconciled

and should be sent to its correct account once the information is received and clear.

Differences between control account and suspense account:

Control Account Suspense Account

Control Account is a kind of summary account. Suspense account is a kind of temporary

account.

It gives the total balance of sales as well as

purchases or in other words balances for

accounts receivables and accounts payables

It helps in providing a transaction a temporary

place to settle down before the actual or correct

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Glover, 2014). account is found for that.

It only deals with sales and purchases and no

other transactions can be put into this.

Suspense account can include anything for

which the information is not clear or the correct

account is difficult to find out.

CONCLUSION

To conclude, companies should do proper reporting of financial statements i.e. income

statement and balance sheet. It should be kept in mind that minimum errors are made so that when

reconciliation have to be done it will clearly match. Reconciliation is done so that errors can be

checked and final cash balance can be identified by the company. Management can take good

decisions if these accounts are maintained properly (De Waegenaere, Sansing and Wielhouwer,

2015).

REFERENCES

Books and Journals

Scott, W. R. and O'Brien, P. C., 2013. Financial accounting theory (Vol. 3). Toronto: Prentice Hall.

Edwards, J. R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Weil, R. L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to concepts,

methods and uses. Cengage Learning.

It only deals with sales and purchases and no

other transactions can be put into this.

Suspense account can include anything for

which the information is not clear or the correct

account is difficult to find out.

CONCLUSION

To conclude, companies should do proper reporting of financial statements i.e. income

statement and balance sheet. It should be kept in mind that minimum errors are made so that when

reconciliation have to be done it will clearly match. Reconciliation is done so that errors can be

checked and final cash balance can be identified by the company. Management can take good

decisions if these accounts are maintained properly (De Waegenaere, Sansing and Wielhouwer,

2015).

REFERENCES

Books and Journals

Scott, W. R. and O'Brien, P. C., 2013. Financial accounting theory (Vol. 3). Toronto: Prentice Hall.

Edwards, J. R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Weil, R. L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to concepts,

methods and uses. Cengage Learning.

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics. 58(2-3). pp.339-383.

Taipaleenmäki, J. and Ikäheimo, S., 2013. On the convergence of management accounting and

financial accounting–the role of information technology in accounting

change. International Journal of Accounting Information Systems. 14(4). pp.321-348.

Parson, R. and et. al., 2015. Methods and apparatus for analysing and/or pre-processing financial

accounting data. U.S. Patent 9.031.873.

Biondi, Y. and et. al., 2011. A perspective on the joint IASB/FASB exposure draft on accounting for

leases: American Accounting Association's Financial Accounting Standards Committee

(AAA FASC). Accounting Horizons. 25(4). pp.861-871.

Gassen, J., 2014. Causal inference in empirical archival financial accounting research. Accounting,

Organizations and Society. 39(7). pp. 535-544.

Linsmeier, T. J., 2011. Financial reporting and financial crises: The case for measuring financial

instruments at fair value in the financial statements. Accounting horizons. 25(2). pp.409-

417.

Glover, J., 2014. Have academic accountants and financial accounting standard setters traded

places?. Accounting, Economics and Law Account. Econ. Law. 4(1). pp.17-26.

De Waegenaere, A., Sansing, R. and Wielhouwer, J. L., 2015. Financial accounting effects of tax

aggressiveness: Contracting and measurement. Contemporary Accounting Research. 32(1).

pp.223-242.

Tugas, F. C., 2012. Exploring a new element of fraud: A study on selected financial accounting

fraud cases in the world. American International Journal of Contemporary Research. 2(6).

pp.112-121.

Ryan, S. G., 2012. Financial reporting for financial instruments. Foundations and Trends® in

Accounting. 6(3–4). pp.187-354.

empirical literature. Journal of Accounting and Economics. 58(2-3). pp.339-383.

Taipaleenmäki, J. and Ikäheimo, S., 2013. On the convergence of management accounting and

financial accounting–the role of information technology in accounting

change. International Journal of Accounting Information Systems. 14(4). pp.321-348.

Parson, R. and et. al., 2015. Methods and apparatus for analysing and/or pre-processing financial

accounting data. U.S. Patent 9.031.873.

Biondi, Y. and et. al., 2011. A perspective on the joint IASB/FASB exposure draft on accounting for

leases: American Accounting Association's Financial Accounting Standards Committee

(AAA FASC). Accounting Horizons. 25(4). pp.861-871.

Gassen, J., 2014. Causal inference in empirical archival financial accounting research. Accounting,

Organizations and Society. 39(7). pp. 535-544.

Linsmeier, T. J., 2011. Financial reporting and financial crises: The case for measuring financial

instruments at fair value in the financial statements. Accounting horizons. 25(2). pp.409-

417.

Glover, J., 2014. Have academic accountants and financial accounting standard setters traded

places?. Accounting, Economics and Law Account. Econ. Law. 4(1). pp.17-26.

De Waegenaere, A., Sansing, R. and Wielhouwer, J. L., 2015. Financial accounting effects of tax

aggressiveness: Contracting and measurement. Contemporary Accounting Research. 32(1).

pp.223-242.

Tugas, F. C., 2012. Exploring a new element of fraud: A study on selected financial accounting

fraud cases in the world. American International Journal of Contemporary Research. 2(6).

pp.112-121.

Ryan, S. G., 2012. Financial reporting for financial instruments. Foundations and Trends® in

Accounting. 6(3–4). pp.187-354.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.