Financial Accounting Report: Financial Statements and Ratio Analysis

VerifiedAdded on 2023/01/12

|31

|3193

|29

Report

AI Summary

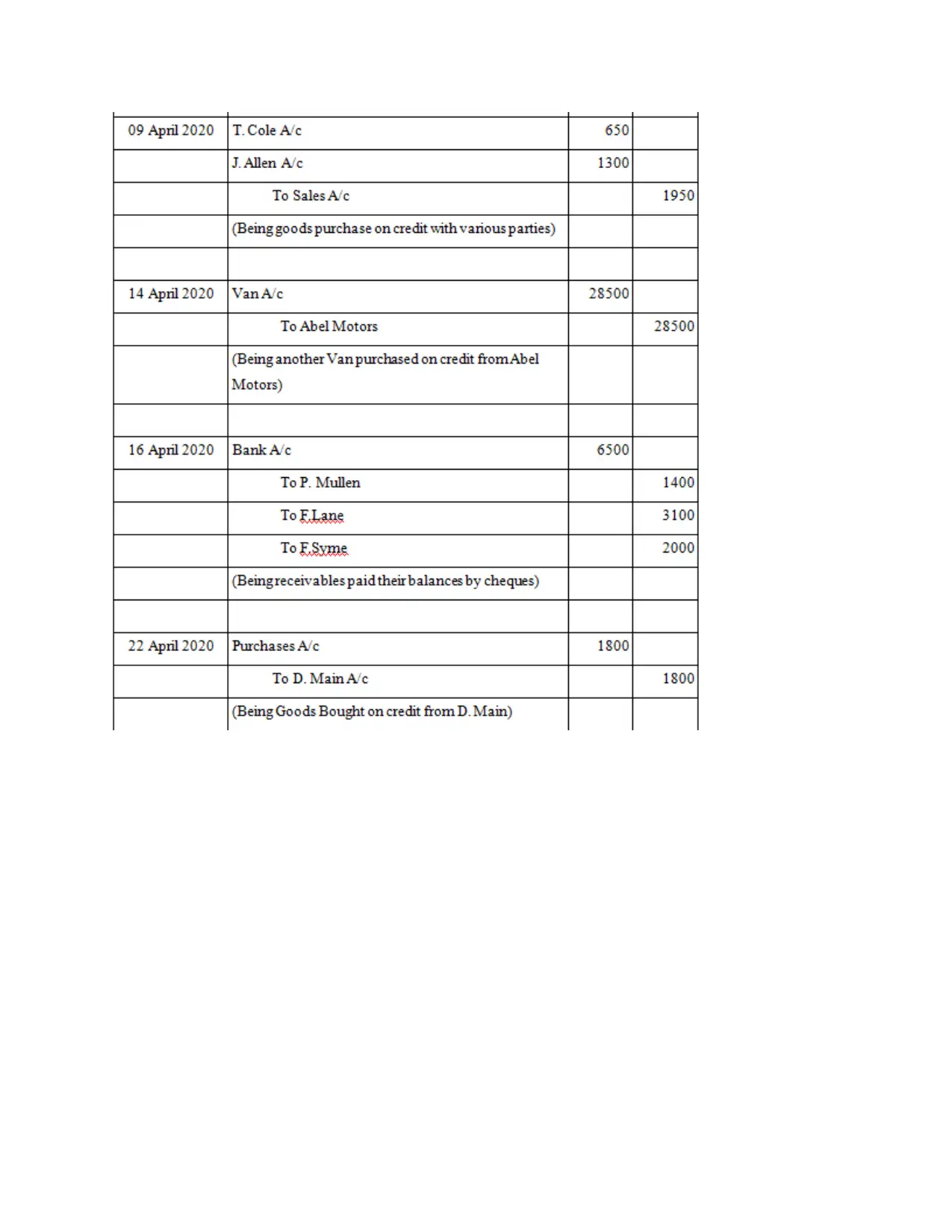

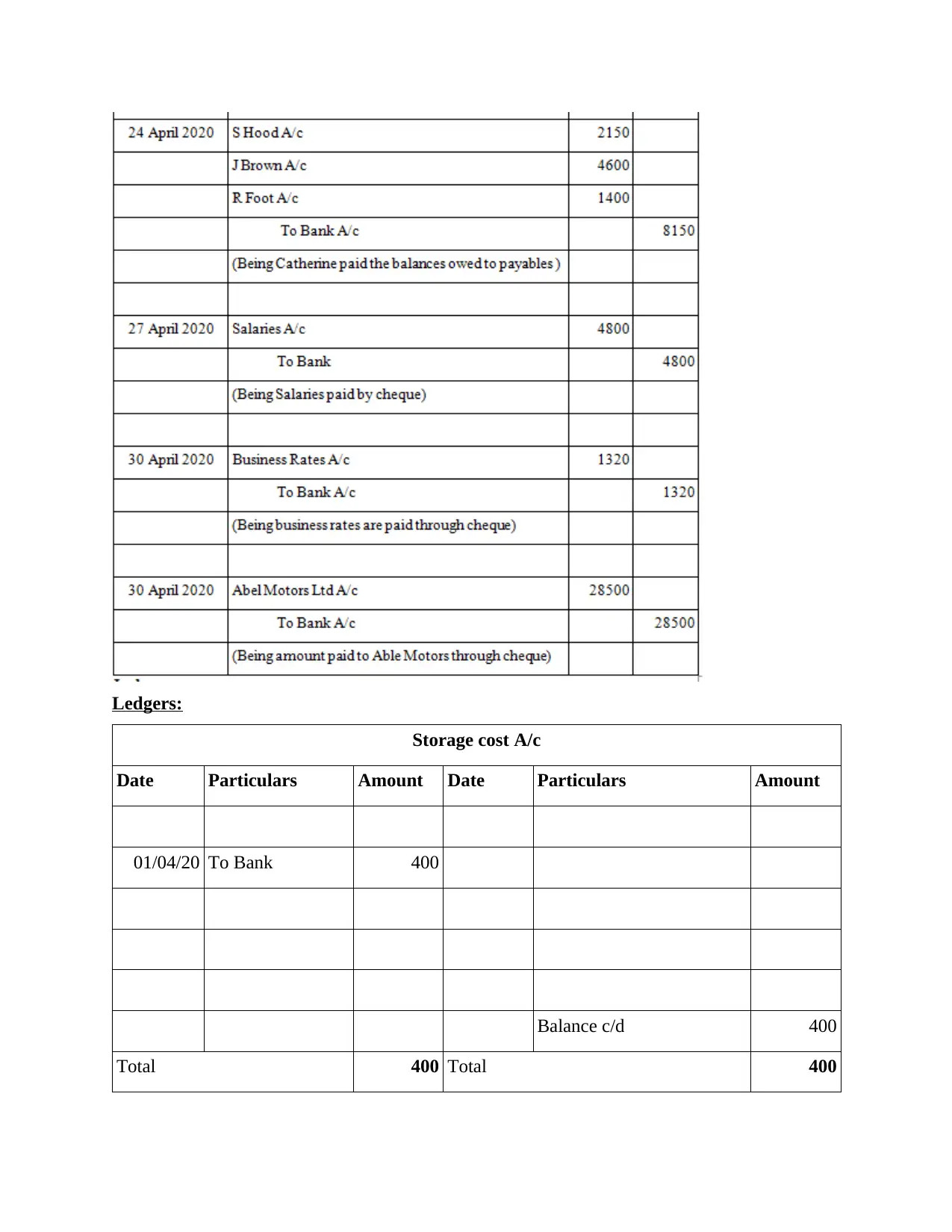

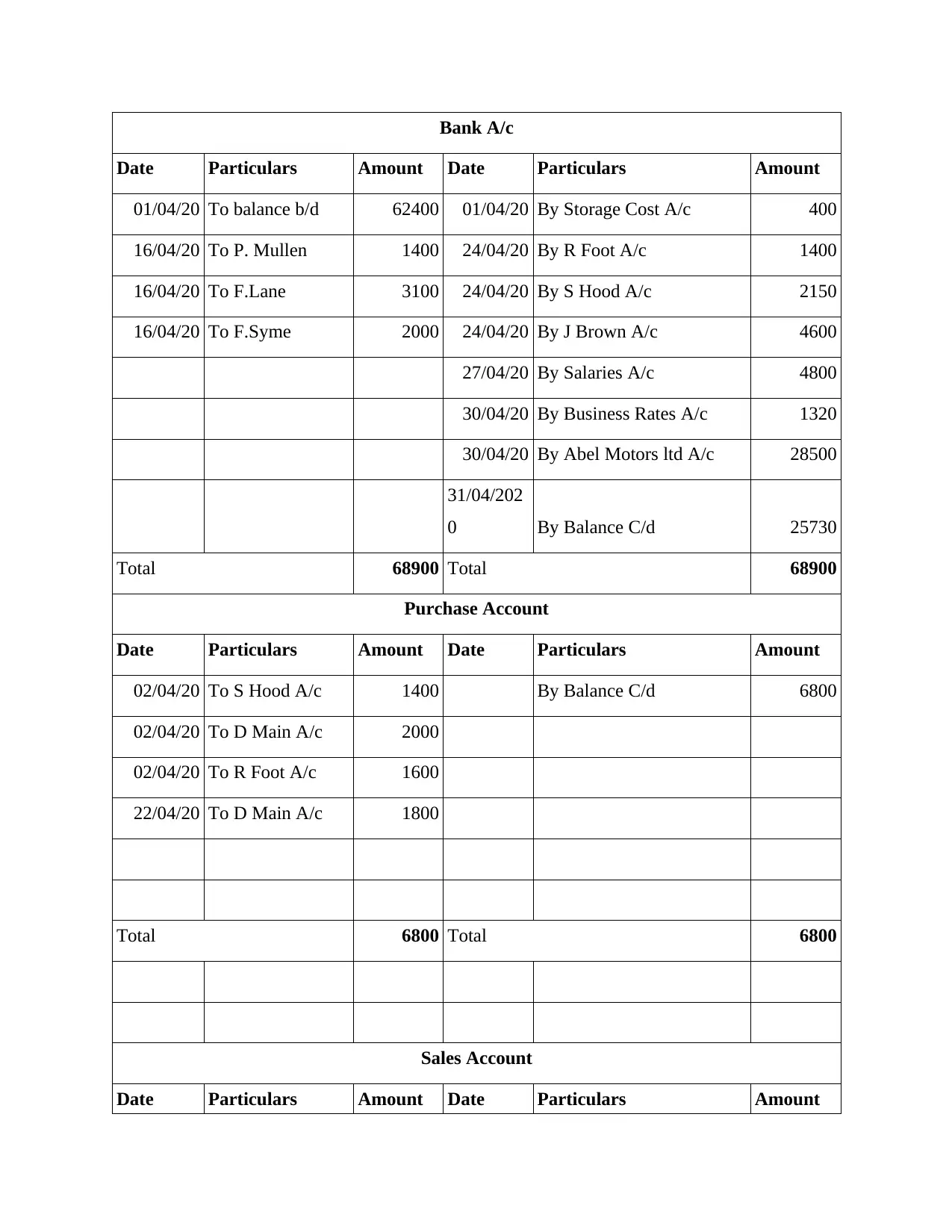

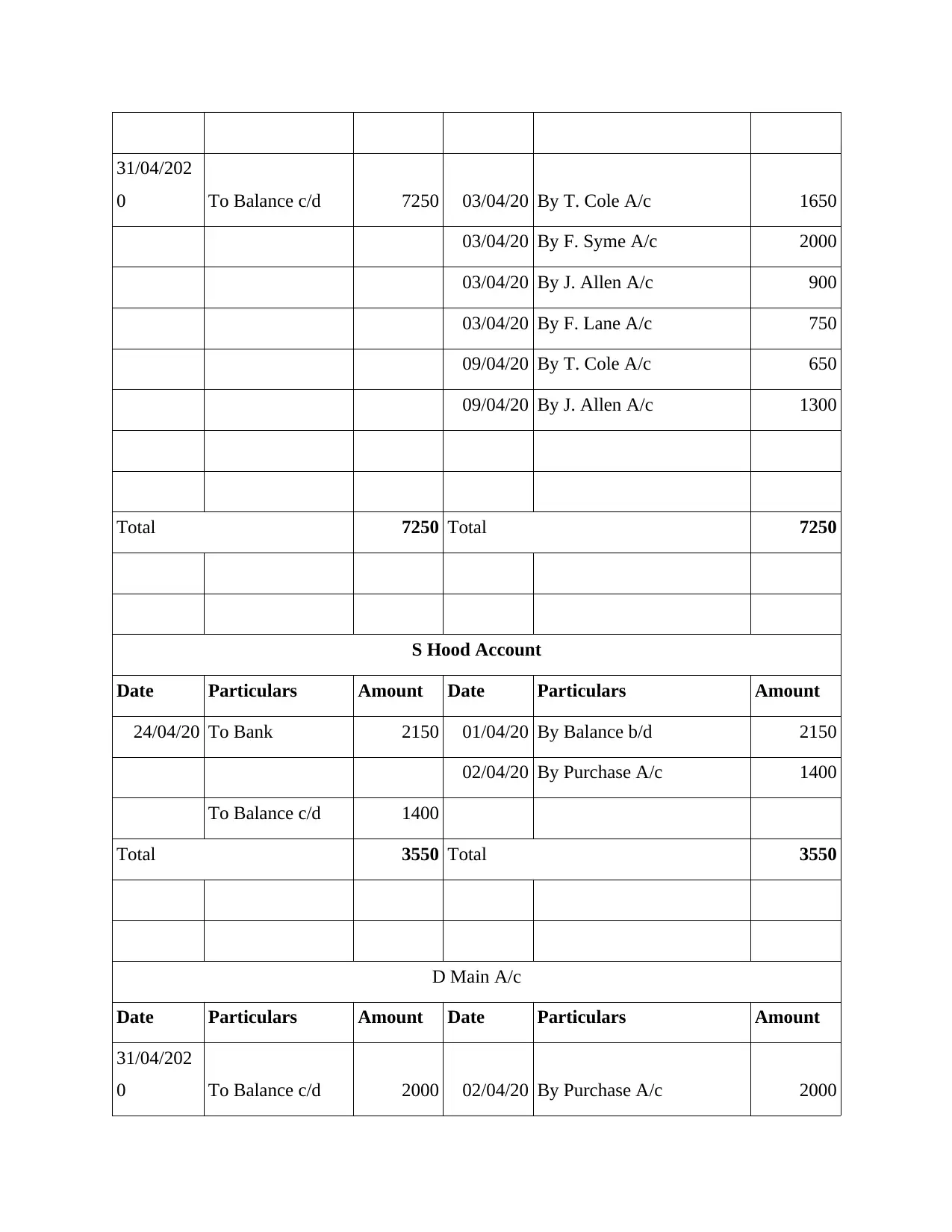

This financial accounting report delves into the core principles of financial accounting, beginning with an introduction to the process of recording, summarizing, analyzing, and presenting financial statements. The report covers the recording of business transactions using double-entry bookkeeping, including sales, purchases, receipts, and payments, while adhering to GAAP and IFRS regulations. It also covers the preparation of trial balances, including identifying and rectifying errors. The report then proceeds to the preparation of final accounts for sole traders, partnership firms, and limited corporations, including journal entries, ledgers, the profit and loss account, and the balance sheet. Furthermore, the report includes ratio analysis, such as return on capital employed, gross profit margin, and net profit margin to evaluate the financial performance of a company. The report also provides a statement of profit or loss and a statement of financial position in accordance with International Accounting Standards (IAS). The report concludes with the calculation and analysis of key financial ratios to assess the financial health of a company.

1 out of 31

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.