Financial Accounting Report: Business Entities and Funding Sources

VerifiedAdded on 2021/04/24

|12

|2746

|379

Report

AI Summary

This report provides a comprehensive overview of business finance and financial accounting. It begins by examining different types of business entities, including sole proprietorships, partnerships, and corporations, outlining their respective merits and limitations. The report then delves into various sources of business finance, categorizing them based on time duration (medium and long term) and providing examples of each. It further differentiates between financial and management accounting, highlighting their objectives and key differences. Finally, the report offers a recommendation, from a financial consultant's perspective, advising clients on the optimal choice of business entity and financing sources, emphasizing the advantages of establishing a company for long-term benefits and access to capital.

RUNNING HEAD: FINANCIAL ACCOUNTING

BUSINESS ACCOUNTING

BUSINESS ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING 1

Contents

Introduction................................................................................................................................2

Task 1.........................................................................................................................................2

Task 2.........................................................................................................................................4

Task 3.........................................................................................................................................7

Recommendation........................................................................................................................9

Conclusion..................................................................................................................................9

References................................................................................................................................10

Contents

Introduction................................................................................................................................2

Task 1.........................................................................................................................................2

Task 2.........................................................................................................................................4

Task 3.........................................................................................................................................7

Recommendation........................................................................................................................9

Conclusion..................................................................................................................................9

References................................................................................................................................10

FINANCIAL ACCOUNTING 2

Introduction

This report contains detailed information about the type of business entities available along

with the merits and demerits of each type. It also explains the various sources of funds

available to a business owner. The main focus is on the long term and medium term sources

of finance and explained with the examples. The last part of the report explains and

differentiates the terms financial and management accounting, followed by a

recommendation provided to the client by a financial consultant working in a consultancy

firm, named IBM. The advice was about choosing the best type of entity and best source of

finance.

Task 1

An organization which produces goods and services with the help of available resources, in

order to meet the requirements of a consumer, is known as business organization. The

business organization can be funded by a single individual or a group of individuals who

owns and manage the business in the form of partnership or a company. Such arrangement of

ownership is called as forms of business organization. Following are the different forms of

business units:

Sole proprietorship

As the name suggest, it is the form in which business is managed and owned by one

individual. In the books of accounts, owner and business are considered as a separate entity

but for legal purposes both are taken as single entity. The profit or loss made in the business

solely belongs to the trader and he has the full control over the activities of the organization.

(Pride, Hughes & Kapoor, 2014).

Introduction

This report contains detailed information about the type of business entities available along

with the merits and demerits of each type. It also explains the various sources of funds

available to a business owner. The main focus is on the long term and medium term sources

of finance and explained with the examples. The last part of the report explains and

differentiates the terms financial and management accounting, followed by a

recommendation provided to the client by a financial consultant working in a consultancy

firm, named IBM. The advice was about choosing the best type of entity and best source of

finance.

Task 1

An organization which produces goods and services with the help of available resources, in

order to meet the requirements of a consumer, is known as business organization. The

business organization can be funded by a single individual or a group of individuals who

owns and manage the business in the form of partnership or a company. Such arrangement of

ownership is called as forms of business organization. Following are the different forms of

business units:

Sole proprietorship

As the name suggest, it is the form in which business is managed and owned by one

individual. In the books of accounts, owner and business are considered as a separate entity

but for legal purposes both are taken as single entity. The profit or loss made in the business

solely belongs to the trader and he has the full control over the activities of the organization.

(Pride, Hughes & Kapoor, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING 3

Benefits Limitations

It is very easy to form a sole proprietorship form

of business. Also it can be easily wind up as and

when the proprietor decides to do so.

The resources available are limited

because the proprietor has a limited

capacity for arranging funds from his

own sources.

No external interference is there, which results in

quick decision making (Mancuso, 2016).

Unlimited liability is there. Reason

being, owner and the entity are treated

as a single person in front of law.

It requires less legal formalities at time of

formation and the changes can be made in the

structure as and when required.

It is not suitable for performing large

scale operations because of limited

resources and capital (Scott, 2012).

Partnership

The firm owned by two or more people, who work as partners, is called a partnership firm. In

such form, a partnership deed is formed which states the distribution of profits and losses,

interest on capital and many more (Clough, Sears, Sears, Segner & Rounds, 2015).

Benefits Limitations

It is also very easy to form as it only requires a

simple agreement to be made.

The firm has limited capital because of

limited number of partners.

Partners have a right to participate in the

management of the firm and decisions are taken

from the consent of all the partners. This led to

better decision making.

The major drawback is that partners

have unlimited liability. This means

they are personally liable for any debt

or obligation.

Risk or losses are shared among all the partners

either equally or in a stated ratio (Kumar, 2008).

Conflict may arise due to differences in

the view point and interest of partners.

Company or Corporation

Benefits Limitations

It is very easy to form a sole proprietorship form

of business. Also it can be easily wind up as and

when the proprietor decides to do so.

The resources available are limited

because the proprietor has a limited

capacity for arranging funds from his

own sources.

No external interference is there, which results in

quick decision making (Mancuso, 2016).

Unlimited liability is there. Reason

being, owner and the entity are treated

as a single person in front of law.

It requires less legal formalities at time of

formation and the changes can be made in the

structure as and when required.

It is not suitable for performing large

scale operations because of limited

resources and capital (Scott, 2012).

Partnership

The firm owned by two or more people, who work as partners, is called a partnership firm. In

such form, a partnership deed is formed which states the distribution of profits and losses,

interest on capital and many more (Clough, Sears, Sears, Segner & Rounds, 2015).

Benefits Limitations

It is also very easy to form as it only requires a

simple agreement to be made.

The firm has limited capital because of

limited number of partners.

Partners have a right to participate in the

management of the firm and decisions are taken

from the consent of all the partners. This led to

better decision making.

The major drawback is that partners

have unlimited liability. This means

they are personally liable for any debt

or obligation.

Risk or losses are shared among all the partners

either equally or in a stated ratio (Kumar, 2008).

Conflict may arise due to differences in

the view point and interest of partners.

Company or Corporation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING 4

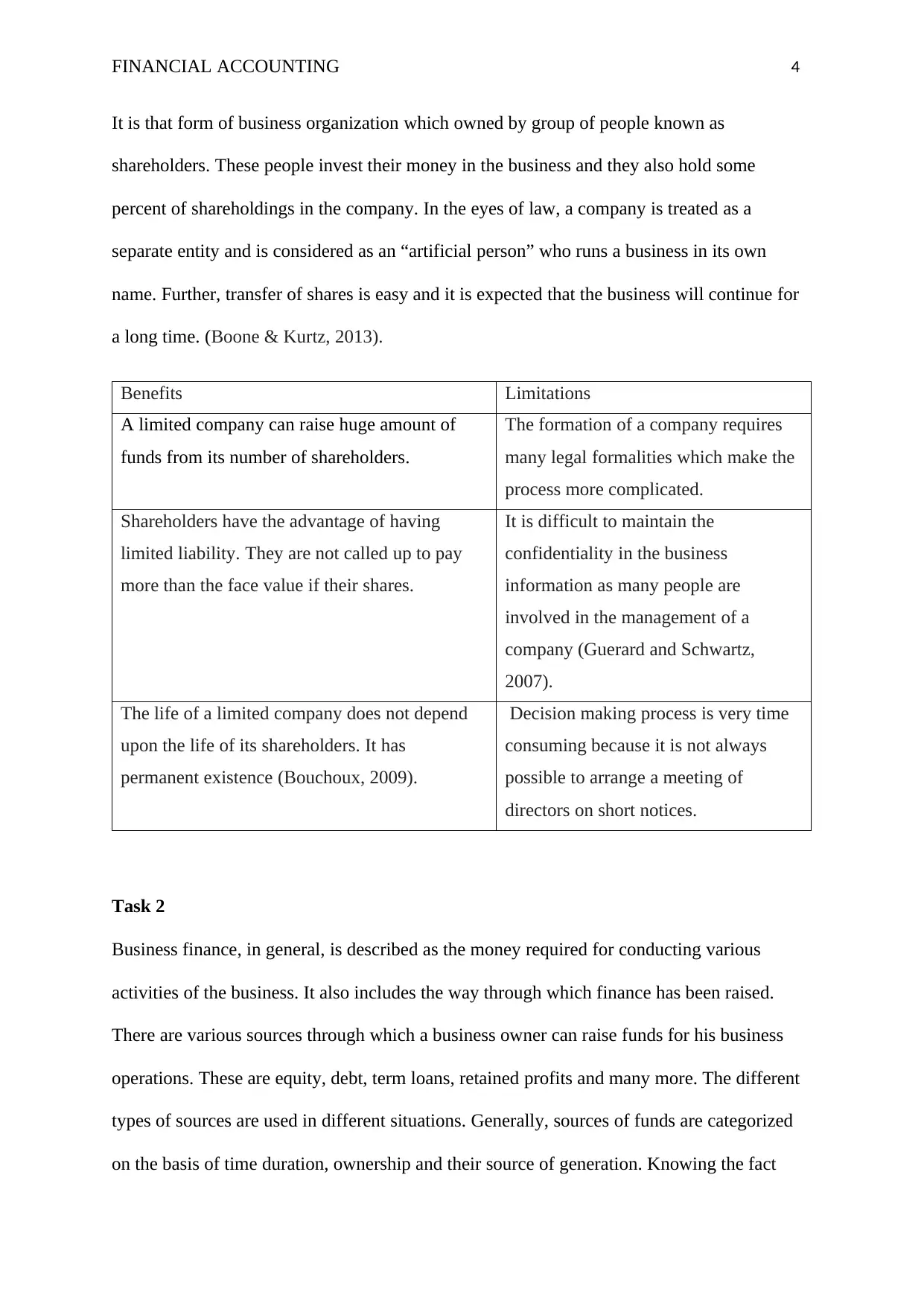

It is that form of business organization which owned by group of people known as

shareholders. These people invest their money in the business and they also hold some

percent of shareholdings in the company. In the eyes of law, a company is treated as a

separate entity and is considered as an “artificial person” who runs a business in its own

name. Further, transfer of shares is easy and it is expected that the business will continue for

a long time. (Boone & Kurtz, 2013).

Benefits Limitations

A limited company can raise huge amount of

funds from its number of shareholders.

The formation of a company requires

many legal formalities which make the

process more complicated.

Shareholders have the advantage of having

limited liability. They are not called up to pay

more than the face value if their shares.

It is difficult to maintain the

confidentiality in the business

information as many people are

involved in the management of a

company (Guerard and Schwartz,

2007).

The life of a limited company does not depend

upon the life of its shareholders. It has

permanent existence (Bouchoux, 2009).

Decision making process is very time

consuming because it is not always

possible to arrange a meeting of

directors on short notices.

Task 2

Business finance, in general, is described as the money required for conducting various

activities of the business. It also includes the way through which finance has been raised.

There are various sources through which a business owner can raise funds for his business

operations. These are equity, debt, term loans, retained profits and many more. The different

types of sources are used in different situations. Generally, sources of funds are categorized

on the basis of time duration, ownership and their source of generation. Knowing the fact

It is that form of business organization which owned by group of people known as

shareholders. These people invest their money in the business and they also hold some

percent of shareholdings in the company. In the eyes of law, a company is treated as a

separate entity and is considered as an “artificial person” who runs a business in its own

name. Further, transfer of shares is easy and it is expected that the business will continue for

a long time. (Boone & Kurtz, 2013).

Benefits Limitations

A limited company can raise huge amount of

funds from its number of shareholders.

The formation of a company requires

many legal formalities which make the

process more complicated.

Shareholders have the advantage of having

limited liability. They are not called up to pay

more than the face value if their shares.

It is difficult to maintain the

confidentiality in the business

information as many people are

involved in the management of a

company (Guerard and Schwartz,

2007).

The life of a limited company does not depend

upon the life of its shareholders. It has

permanent existence (Bouchoux, 2009).

Decision making process is very time

consuming because it is not always

possible to arrange a meeting of

directors on short notices.

Task 2

Business finance, in general, is described as the money required for conducting various

activities of the business. It also includes the way through which finance has been raised.

There are various sources through which a business owner can raise funds for his business

operations. These are equity, debt, term loans, retained profits and many more. The different

types of sources are used in different situations. Generally, sources of funds are categorized

on the basis of time duration, ownership and their source of generation. Knowing the fact

FINANCIAL ACCOUNTING 5

that, there are various financing sources available, company should choose the right source

and right mix of capital (Cinnamon and Helweg-Larsen, 2010).

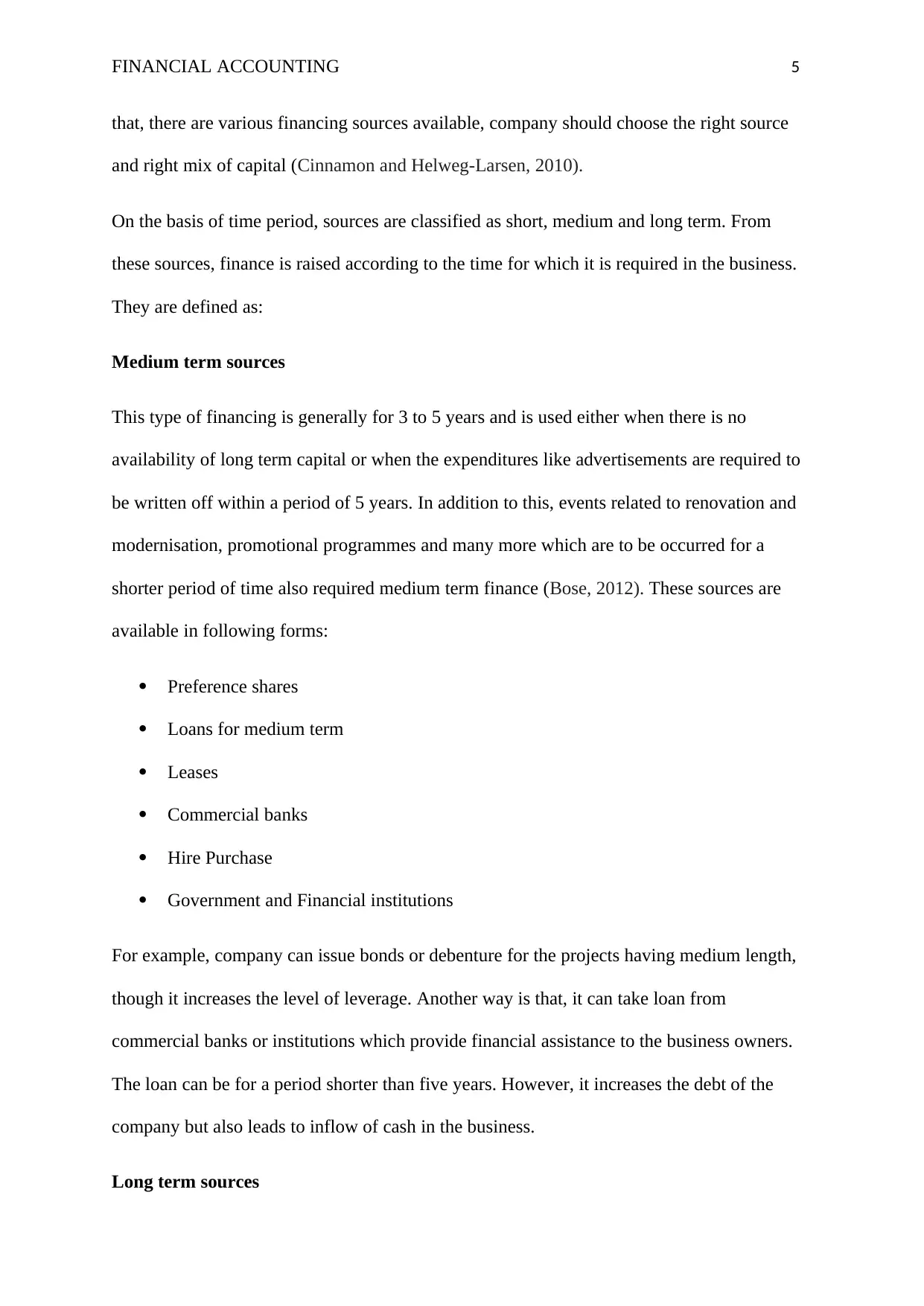

On the basis of time period, sources are classified as short, medium and long term. From

these sources, finance is raised according to the time for which it is required in the business.

They are defined as:

Medium term sources

This type of financing is generally for 3 to 5 years and is used either when there is no

availability of long term capital or when the expenditures like advertisements are required to

be written off within a period of 5 years. In addition to this, events related to renovation and

modernisation, promotional programmes and many more which are to be occurred for a

shorter period of time also required medium term finance (Bose, 2012). These sources are

available in following forms:

Preference shares

Loans for medium term

Leases

Commercial banks

Hire Purchase

Government and Financial institutions

For example, company can issue bonds or debenture for the projects having medium length,

though it increases the level of leverage. Another way is that, it can take loan from

commercial banks or institutions which provide financial assistance to the business owners.

The loan can be for a period shorter than five years. However, it increases the debt of the

company but also leads to inflow of cash in the business.

Long term sources

that, there are various financing sources available, company should choose the right source

and right mix of capital (Cinnamon and Helweg-Larsen, 2010).

On the basis of time period, sources are classified as short, medium and long term. From

these sources, finance is raised according to the time for which it is required in the business.

They are defined as:

Medium term sources

This type of financing is generally for 3 to 5 years and is used either when there is no

availability of long term capital or when the expenditures like advertisements are required to

be written off within a period of 5 years. In addition to this, events related to renovation and

modernisation, promotional programmes and many more which are to be occurred for a

shorter period of time also required medium term finance (Bose, 2012). These sources are

available in following forms:

Preference shares

Loans for medium term

Leases

Commercial banks

Hire Purchase

Government and Financial institutions

For example, company can issue bonds or debenture for the projects having medium length,

though it increases the level of leverage. Another way is that, it can take loan from

commercial banks or institutions which provide financial assistance to the business owners.

The loan can be for a period shorter than five years. However, it increases the debt of the

company but also leads to inflow of cash in the business.

Long term sources

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING 6

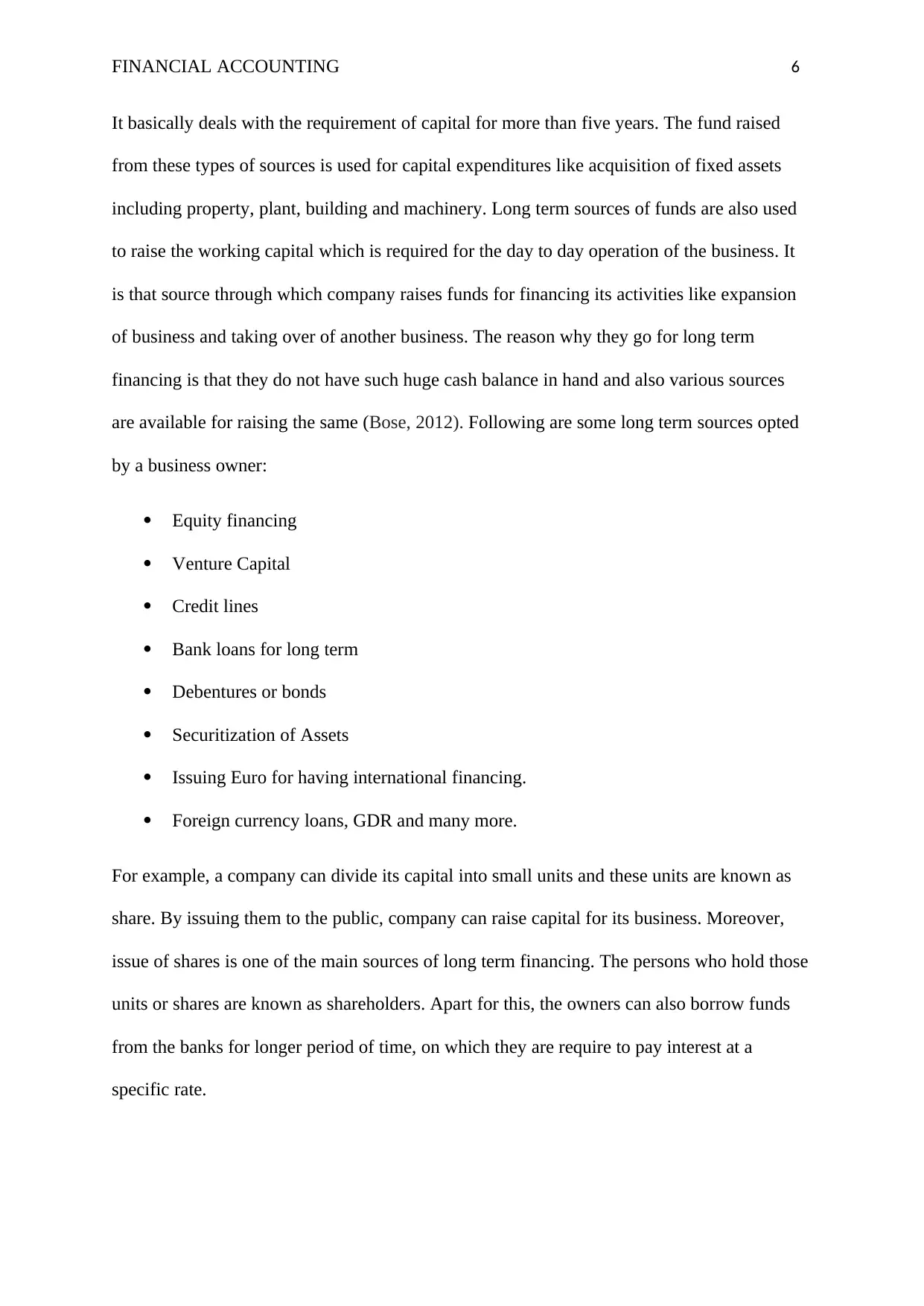

It basically deals with the requirement of capital for more than five years. The fund raised

from these types of sources is used for capital expenditures like acquisition of fixed assets

including property, plant, building and machinery. Long term sources of funds are also used

to raise the working capital which is required for the day to day operation of the business. It

is that source through which company raises funds for financing its activities like expansion

of business and taking over of another business. The reason why they go for long term

financing is that they do not have such huge cash balance in hand and also various sources

are available for raising the same (Bose, 2012). Following are some long term sources opted

by a business owner:

Equity financing

Venture Capital

Credit lines

Bank loans for long term

Debentures or bonds

Securitization of Assets

Issuing Euro for having international financing.

Foreign currency loans, GDR and many more.

For example, a company can divide its capital into small units and these units are known as

share. By issuing them to the public, company can raise capital for its business. Moreover,

issue of shares is one of the main sources of long term financing. The persons who hold those

units or shares are known as shareholders. Apart for this, the owners can also borrow funds

from the banks for longer period of time, on which they are require to pay interest at a

specific rate.

It basically deals with the requirement of capital for more than five years. The fund raised

from these types of sources is used for capital expenditures like acquisition of fixed assets

including property, plant, building and machinery. Long term sources of funds are also used

to raise the working capital which is required for the day to day operation of the business. It

is that source through which company raises funds for financing its activities like expansion

of business and taking over of another business. The reason why they go for long term

financing is that they do not have such huge cash balance in hand and also various sources

are available for raising the same (Bose, 2012). Following are some long term sources opted

by a business owner:

Equity financing

Venture Capital

Credit lines

Bank loans for long term

Debentures or bonds

Securitization of Assets

Issuing Euro for having international financing.

Foreign currency loans, GDR and many more.

For example, a company can divide its capital into small units and these units are known as

share. By issuing them to the public, company can raise capital for its business. Moreover,

issue of shares is one of the main sources of long term financing. The persons who hold those

units or shares are known as shareholders. Apart for this, the owners can also borrow funds

from the banks for longer period of time, on which they are require to pay interest at a

specific rate.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING 7

Apart from the above, there are also various sources of funds through which a company can

arrange or mange finance for its business activities or operations.

Task 3

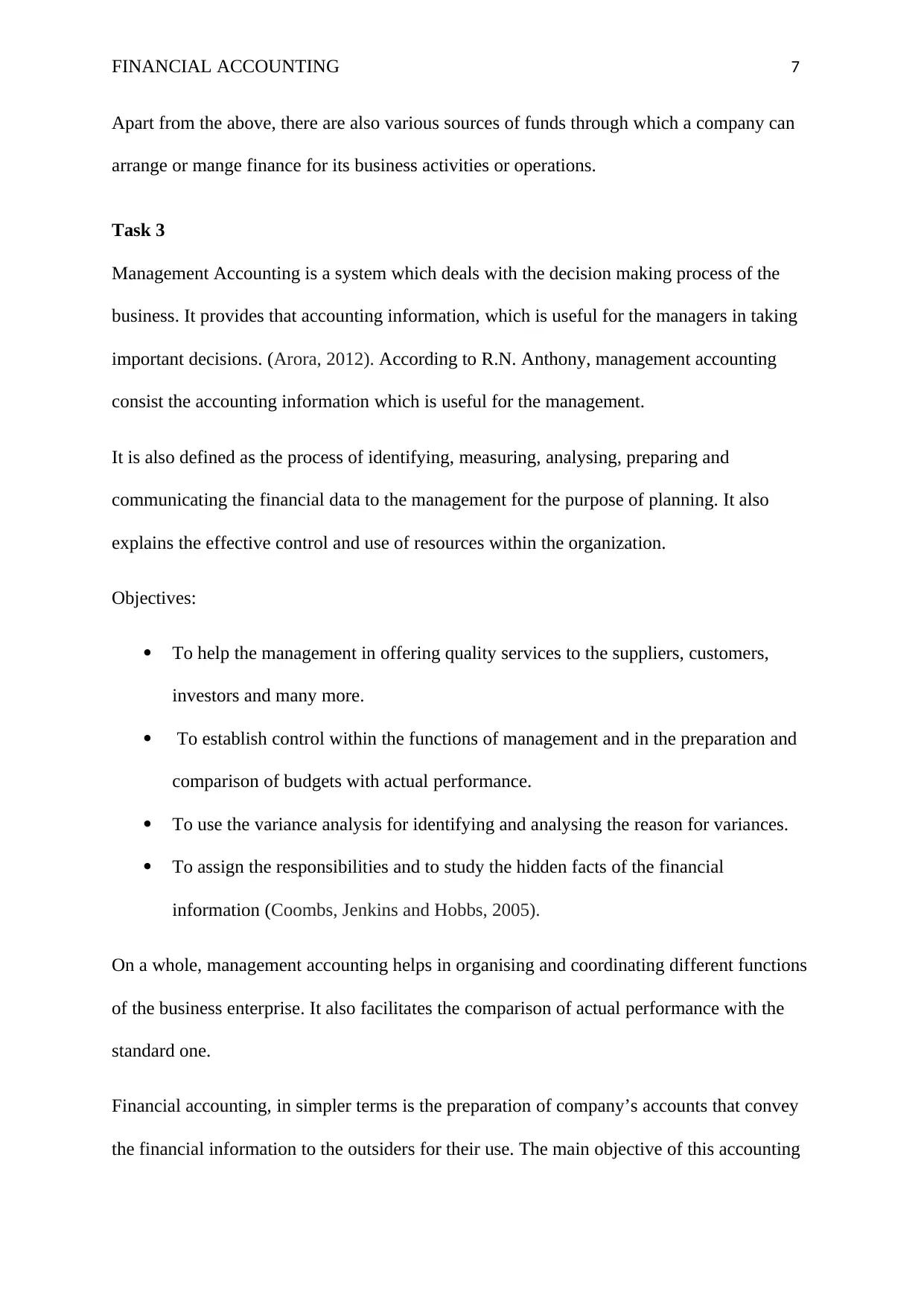

Management Accounting is a system which deals with the decision making process of the

business. It provides that accounting information, which is useful for the managers in taking

important decisions. (Arora, 2012). According to R.N. Anthony, management accounting

consist the accounting information which is useful for the management.

It is also defined as the process of identifying, measuring, analysing, preparing and

communicating the financial data to the management for the purpose of planning. It also

explains the effective control and use of resources within the organization.

Objectives:

To help the management in offering quality services to the suppliers, customers,

investors and many more.

To establish control within the functions of management and in the preparation and

comparison of budgets with actual performance.

To use the variance analysis for identifying and analysing the reason for variances.

To assign the responsibilities and to study the hidden facts of the financial

information (Coombs, Jenkins and Hobbs, 2005).

On a whole, management accounting helps in organising and coordinating different functions

of the business enterprise. It also facilitates the comparison of actual performance with the

standard one.

Financial accounting, in simpler terms is the preparation of company’s accounts that convey

the financial information to the outsiders for their use. The main objective of this accounting

Apart from the above, there are also various sources of funds through which a company can

arrange or mange finance for its business activities or operations.

Task 3

Management Accounting is a system which deals with the decision making process of the

business. It provides that accounting information, which is useful for the managers in taking

important decisions. (Arora, 2012). According to R.N. Anthony, management accounting

consist the accounting information which is useful for the management.

It is also defined as the process of identifying, measuring, analysing, preparing and

communicating the financial data to the management for the purpose of planning. It also

explains the effective control and use of resources within the organization.

Objectives:

To help the management in offering quality services to the suppliers, customers,

investors and many more.

To establish control within the functions of management and in the preparation and

comparison of budgets with actual performance.

To use the variance analysis for identifying and analysing the reason for variances.

To assign the responsibilities and to study the hidden facts of the financial

information (Coombs, Jenkins and Hobbs, 2005).

On a whole, management accounting helps in organising and coordinating different functions

of the business enterprise. It also facilitates the comparison of actual performance with the

standard one.

Financial accounting, in simpler terms is the preparation of company’s accounts that convey

the financial information to the outsiders for their use. The main objective of this accounting

FINANCIAL ACCOUNTING 8

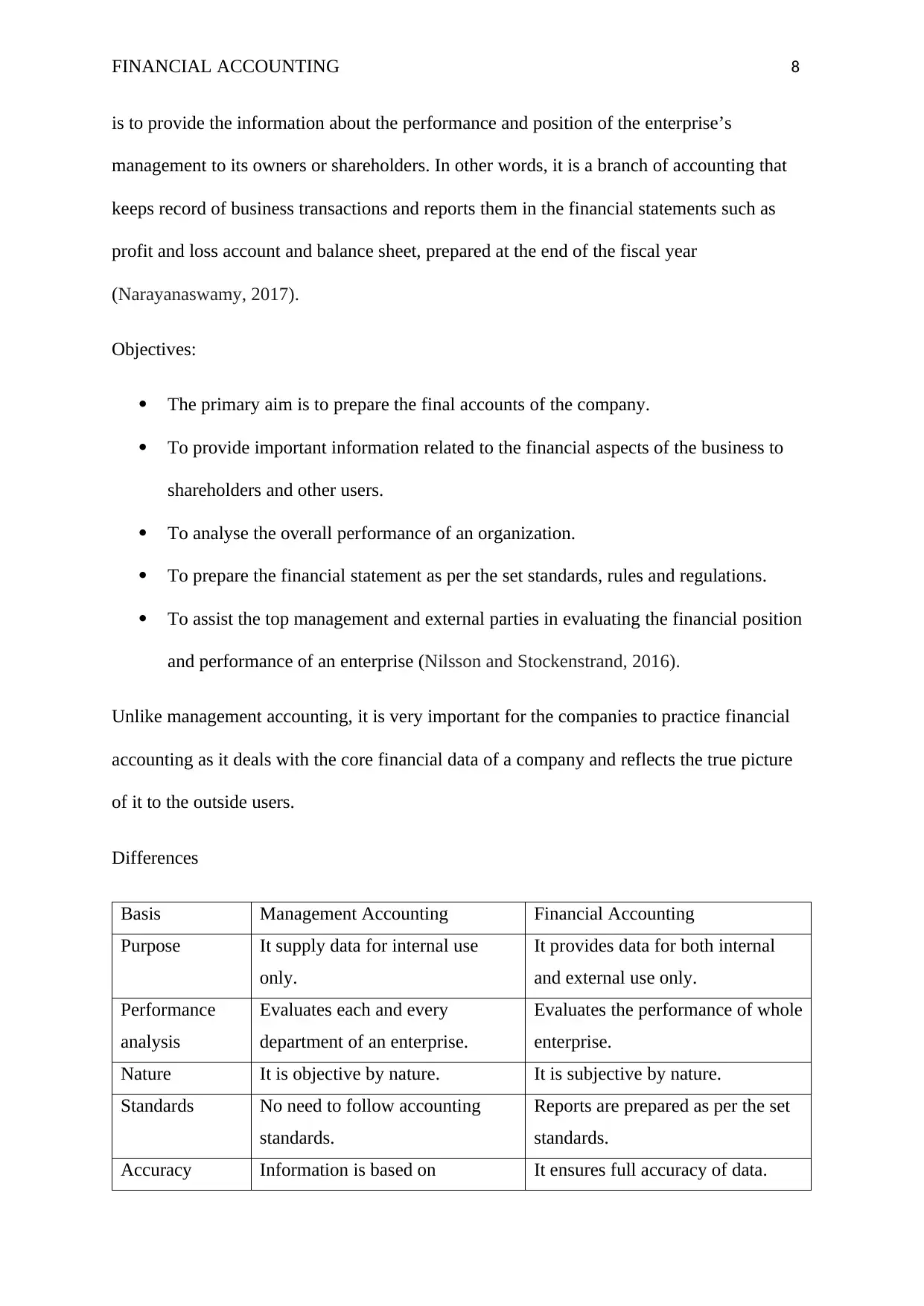

is to provide the information about the performance and position of the enterprise’s

management to its owners or shareholders. In other words, it is a branch of accounting that

keeps record of business transactions and reports them in the financial statements such as

profit and loss account and balance sheet, prepared at the end of the fiscal year

(Narayanaswamy, 2017).

Objectives:

The primary aim is to prepare the final accounts of the company.

To provide important information related to the financial aspects of the business to

shareholders and other users.

To analyse the overall performance of an organization.

To prepare the financial statement as per the set standards, rules and regulations.

To assist the top management and external parties in evaluating the financial position

and performance of an enterprise (Nilsson and Stockenstrand, 2016).

Unlike management accounting, it is very important for the companies to practice financial

accounting as it deals with the core financial data of a company and reflects the true picture

of it to the outside users.

Differences

Basis Management Accounting Financial Accounting

Purpose It supply data for internal use

only.

It provides data for both internal

and external use only.

Performance

analysis

Evaluates each and every

department of an enterprise.

Evaluates the performance of whole

enterprise.

Nature It is objective by nature. It is subjective by nature.

Standards No need to follow accounting

standards.

Reports are prepared as per the set

standards.

Accuracy Information is based on It ensures full accuracy of data.

is to provide the information about the performance and position of the enterprise’s

management to its owners or shareholders. In other words, it is a branch of accounting that

keeps record of business transactions and reports them in the financial statements such as

profit and loss account and balance sheet, prepared at the end of the fiscal year

(Narayanaswamy, 2017).

Objectives:

The primary aim is to prepare the final accounts of the company.

To provide important information related to the financial aspects of the business to

shareholders and other users.

To analyse the overall performance of an organization.

To prepare the financial statement as per the set standards, rules and regulations.

To assist the top management and external parties in evaluating the financial position

and performance of an enterprise (Nilsson and Stockenstrand, 2016).

Unlike management accounting, it is very important for the companies to practice financial

accounting as it deals with the core financial data of a company and reflects the true picture

of it to the outside users.

Differences

Basis Management Accounting Financial Accounting

Purpose It supply data for internal use

only.

It provides data for both internal

and external use only.

Performance

analysis

Evaluates each and every

department of an enterprise.

Evaluates the performance of whole

enterprise.

Nature It is objective by nature. It is subjective by nature.

Standards No need to follow accounting

standards.

Reports are prepared as per the set

standards.

Accuracy Information is based on It ensures full accuracy of data.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING 9

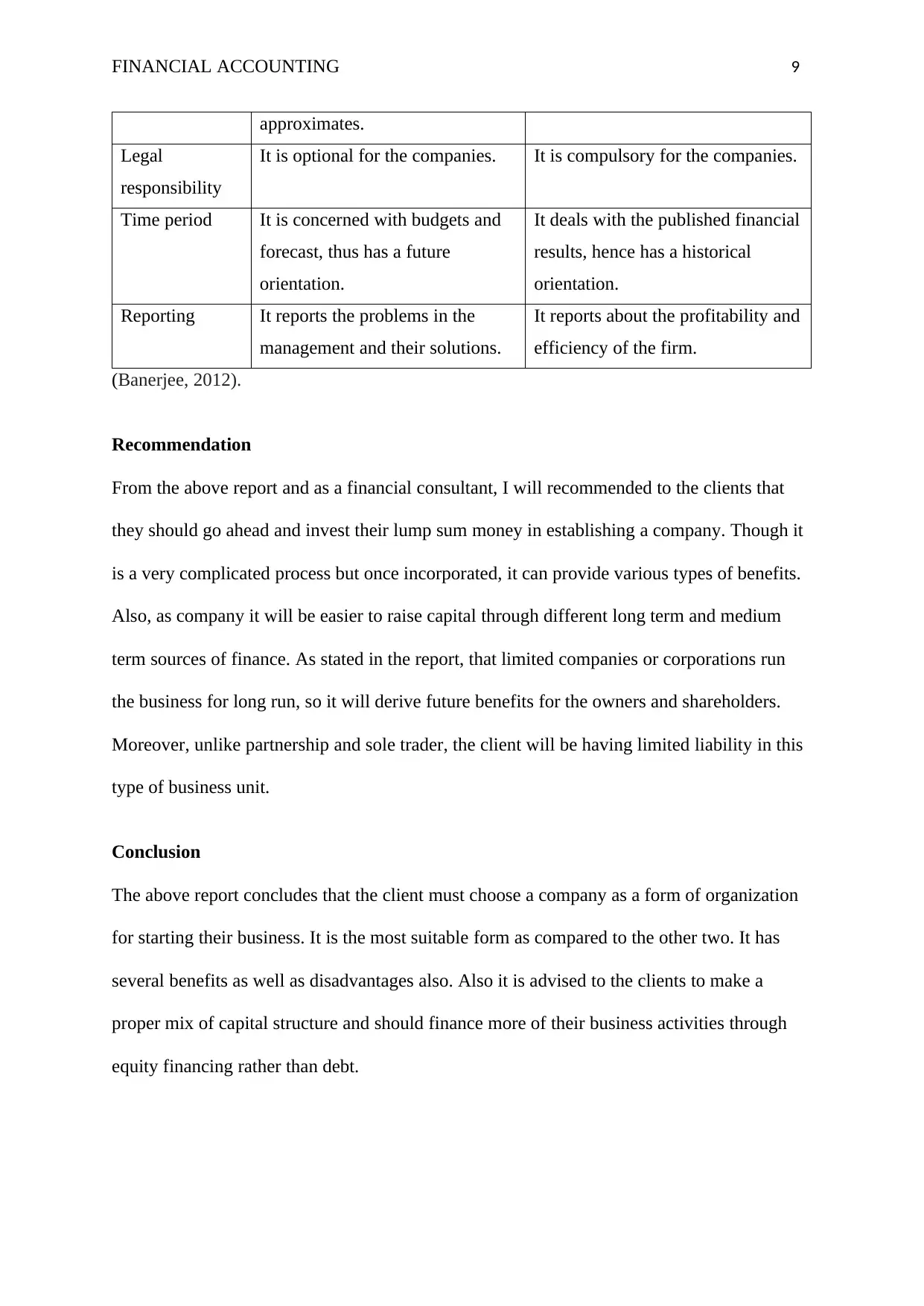

approximates.

Legal

responsibility

It is optional for the companies. It is compulsory for the companies.

Time period It is concerned with budgets and

forecast, thus has a future

orientation.

It deals with the published financial

results, hence has a historical

orientation.

Reporting It reports the problems in the

management and their solutions.

It reports about the profitability and

efficiency of the firm.

(Banerjee, 2012).

Recommendation

From the above report and as a financial consultant, I will recommended to the clients that

they should go ahead and invest their lump sum money in establishing a company. Though it

is a very complicated process but once incorporated, it can provide various types of benefits.

Also, as company it will be easier to raise capital through different long term and medium

term sources of finance. As stated in the report, that limited companies or corporations run

the business for long run, so it will derive future benefits for the owners and shareholders.

Moreover, unlike partnership and sole trader, the client will be having limited liability in this

type of business unit.

Conclusion

The above report concludes that the client must choose a company as a form of organization

for starting their business. It is the most suitable form as compared to the other two. It has

several benefits as well as disadvantages also. Also it is advised to the clients to make a

proper mix of capital structure and should finance more of their business activities through

equity financing rather than debt.

approximates.

Legal

responsibility

It is optional for the companies. It is compulsory for the companies.

Time period It is concerned with budgets and

forecast, thus has a future

orientation.

It deals with the published financial

results, hence has a historical

orientation.

Reporting It reports the problems in the

management and their solutions.

It reports about the profitability and

efficiency of the firm.

(Banerjee, 2012).

Recommendation

From the above report and as a financial consultant, I will recommended to the clients that

they should go ahead and invest their lump sum money in establishing a company. Though it

is a very complicated process but once incorporated, it can provide various types of benefits.

Also, as company it will be easier to raise capital through different long term and medium

term sources of finance. As stated in the report, that limited companies or corporations run

the business for long run, so it will derive future benefits for the owners and shareholders.

Moreover, unlike partnership and sole trader, the client will be having limited liability in this

type of business unit.

Conclusion

The above report concludes that the client must choose a company as a form of organization

for starting their business. It is the most suitable form as compared to the other two. It has

several benefits as well as disadvantages also. Also it is advised to the clients to make a

proper mix of capital structure and should finance more of their business activities through

equity financing rather than debt.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING 10

References

Arora, M.N., (2012). A textbook of cost and management accounting. 10th ed. New Delhi:

Vikas Publishing House.

Banerjee, B., (2012). Financial policy and management accounting. 7th ed. pp.7-8. New

Delhi: PHI Learning Pvt. Ltd.

Boone, L. E., & Kurtz, D. L. (2013). Essentials of Contemporary Business, Binder Ready

Version. (1st ed.). USA: John Wiley & Sons.

Bose, D.C., (2012). Principles of management and administration. 2nd ed. New Delhi: PHI

Learning Pvt. Ltd.

Bouchoux, D.E., (2009). Business organizations for paralegals. 3rd ed. New York: Aspen

Publishers.

Cinnamon, B. and Helweg-Larsen, B., (2010). How to understand business finance. 2nd ed.

United Kingdom: Kogan Page Publishers.

Clough, R. H., Sears, G. A., Sears, S. K., Segner, R. O., & Rounds, J. L. (2015). Construction

contracting: A practical guide to company management. (8th ed.). New Jersey: John Wiley &

Sons.

Coombs, H., Jenkins, E. and Hobbs, D., (2005). Management accounting: principles and

applications. London: Sage.

Guerard Jr, J.B. and Schwartz, E., (2007). Quantitative corporate finance. New York:

Springer Science & Business Media.

Kumar, S.A., (2008). Entrepreneurship development. New Delhi: New Age International.

References

Arora, M.N., (2012). A textbook of cost and management accounting. 10th ed. New Delhi:

Vikas Publishing House.

Banerjee, B., (2012). Financial policy and management accounting. 7th ed. pp.7-8. New

Delhi: PHI Learning Pvt. Ltd.

Boone, L. E., & Kurtz, D. L. (2013). Essentials of Contemporary Business, Binder Ready

Version. (1st ed.). USA: John Wiley & Sons.

Bose, D.C., (2012). Principles of management and administration. 2nd ed. New Delhi: PHI

Learning Pvt. Ltd.

Bouchoux, D.E., (2009). Business organizations for paralegals. 3rd ed. New York: Aspen

Publishers.

Cinnamon, B. and Helweg-Larsen, B., (2010). How to understand business finance. 2nd ed.

United Kingdom: Kogan Page Publishers.

Clough, R. H., Sears, G. A., Sears, S. K., Segner, R. O., & Rounds, J. L. (2015). Construction

contracting: A practical guide to company management. (8th ed.). New Jersey: John Wiley &

Sons.

Coombs, H., Jenkins, E. and Hobbs, D., (2005). Management accounting: principles and

applications. London: Sage.

Guerard Jr, J.B. and Schwartz, E., (2007). Quantitative corporate finance. New York:

Springer Science & Business Media.

Kumar, S.A., (2008). Entrepreneurship development. New Delhi: New Age International.

FINANCIAL ACCOUNTING 11

Mancuso, A., (2016). Llc Or Corporation?: Choose the Right Form for Your Business. 7th ed.

USA: Nolo.

Narayanaswamy, R., (2017). Financial accounting: a managerial perspective. 5th ed. New

Delhi: PHI Learning Pvt. Ltd.

Nilsson, F. and Stockenstrand, A.K., (2016). Financial Accounting and Management Control.

Springer International Publishing: Imprint: Switzerland: Springer

Pride, W. M., Hughes, R. J., & Kapoor, J. R. (2014). Foundations of business. (4th ed.).

USA: Cengage Learning.

Scott, P., (2012). Accounting for Business: An Integrated Print and Online Solution. United

Kingdom: Oxford University Press.

Mancuso, A., (2016). Llc Or Corporation?: Choose the Right Form for Your Business. 7th ed.

USA: Nolo.

Narayanaswamy, R., (2017). Financial accounting: a managerial perspective. 5th ed. New

Delhi: PHI Learning Pvt. Ltd.

Nilsson, F. and Stockenstrand, A.K., (2016). Financial Accounting and Management Control.

Springer International Publishing: Imprint: Switzerland: Springer

Pride, W. M., Hughes, R. J., & Kapoor, J. R. (2014). Foundations of business. (4th ed.).

USA: Cengage Learning.

Scott, P., (2012). Accounting for Business: An Integrated Print and Online Solution. United

Kingdom: Oxford University Press.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.