Financial Accounting Report

VerifiedAdded on 2020/02/03

|29

|4944

|27

Report

AI Summary

This report on financial accounting covers various aspects including journal entries, ledgers, trial balances, and financial statements for multiple clients. It emphasizes the importance of accurate accounting practices and provides detailed examples of profit and loss statements, balance sheets, and bank reconciliation statements. The report also discusses key accounting concepts such as depreciation and the significance of maintaining consistency in financial reporting.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................3

CLIENT 1...................................................................................................................................3

a. Doing Journal Entries in the books of Alex Study’s..........................................................3

b. Preparing ledgers account..................................................................................................5

c. Showing trial balance.........................................................................................................5

CLIENT 2...................................................................................................................................7

a. Preparing statement of profit and loss for Peter Piper........................................................7

b. Drafting statement of financial position for Peter Piper....................................................8

CLIENT 3...................................................................................................................................9

a. Showing profitability statement of Raintree Ltd..............................................................10

b. Preparing and presenting balance sheet of Raintree Ltd..................................................10

c. Defining the concept of consistency and prudent............................................................11

d. Stating the purpose of depreciation and illustrating two methods associated with it......12

CLIENT 4.................................................................................................................................13

a. Defining the purpose of bank reconciliation statement....................................................13

b. Presenting the reasons due to which balance of cash and pass book differs....................13

c. Preparing bank reconciliation statement..........................................................................13

CLIENT 5.................................................................................................................................14

a. Preparing purchase and sales ledger account for Henderson Ltd.....................................14

b. Defining the term of control account...............................................................................15

CLIENT 6.................................................................................................................................15

a. Presenting suspense account along with its main features...............................................15

b. Preparing trial balance by undertaking control a/c..........................................................15

c. Rectification of errors and journal entries based on it......................................................16

d. Stating the difference takes place between the suspense and clearing account...............17

INTRODUCTION......................................................................................................................3

CLIENT 1...................................................................................................................................3

a. Doing Journal Entries in the books of Alex Study’s..........................................................3

b. Preparing ledgers account..................................................................................................5

c. Showing trial balance.........................................................................................................5

CLIENT 2...................................................................................................................................7

a. Preparing statement of profit and loss for Peter Piper........................................................7

b. Drafting statement of financial position for Peter Piper....................................................8

CLIENT 3...................................................................................................................................9

a. Showing profitability statement of Raintree Ltd..............................................................10

b. Preparing and presenting balance sheet of Raintree Ltd..................................................10

c. Defining the concept of consistency and prudent............................................................11

d. Stating the purpose of depreciation and illustrating two methods associated with it......12

CLIENT 4.................................................................................................................................13

a. Defining the purpose of bank reconciliation statement....................................................13

b. Presenting the reasons due to which balance of cash and pass book differs....................13

c. Preparing bank reconciliation statement..........................................................................13

CLIENT 5.................................................................................................................................14

a. Preparing purchase and sales ledger account for Henderson Ltd.....................................14

b. Defining the term of control account...............................................................................15

CLIENT 6.................................................................................................................................15

a. Presenting suspense account along with its main features...............................................15

b. Preparing trial balance by undertaking control a/c..........................................................15

c. Rectification of errors and journal entries based on it......................................................16

d. Stating the difference takes place between the suspense and clearing account...............17

CONCUSION..........................................................................................................................17

REFERENCES.........................................................................................................................19

APPENDIX..............................................................................................................................21

Appendix 1: Ledger account................................................................................................21

REFERENCES.........................................................................................................................19

APPENDIX..............................................................................................................................21

Appendix 1: Ledger account................................................................................................21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is concerned with the preparation of highly appropriate

statement that furnishes information about the monetary position and performance.

Accounting tools and techniques are highly significant which in turn provides high level of

assistance to the business unit in preparing as well as presenting suitable view of monetary

performance. This report is drafted by addressing the different case situation which will shed

light on the manner through which adjusted profit& loss and balance sheet can be prepared.

Besides this, it will also develop understanding about the concepts of depreciation, suspense

and control account. Further, report will also highlight the way in which errors take place in

the accounting entries can be rectified. Thus, report will clearly present how trial balance

assists in preparing final accounts in an effectual way.

CLIENT 1

a. Doing Journal Entries in the books of Alex Study’s

Journal of Alex study for the month of May 2016

Particulars Debit Credit

1. Storage expenses a/c Dr.

To bank a/c

400

400

2. Purchase a/c Dr.

To S. Hood a/c

1450

1450

2. Purchase a/c Dr.

To D. Main a/c

2060

2060

2 Purchase a/c Dr.

To W. Tone a/c

960

960

2 Purchase a/c Dr.

To R. Foot a/c

1610

1610

3. J Wilson a/c Dr.

To sales a/c

1120

1120

3. T. Cole a/c Dr.

To sales a/c

1640

1640

Financial accounting is concerned with the preparation of highly appropriate

statement that furnishes information about the monetary position and performance.

Accounting tools and techniques are highly significant which in turn provides high level of

assistance to the business unit in preparing as well as presenting suitable view of monetary

performance. This report is drafted by addressing the different case situation which will shed

light on the manner through which adjusted profit& loss and balance sheet can be prepared.

Besides this, it will also develop understanding about the concepts of depreciation, suspense

and control account. Further, report will also highlight the way in which errors take place in

the accounting entries can be rectified. Thus, report will clearly present how trial balance

assists in preparing final accounts in an effectual way.

CLIENT 1

a. Doing Journal Entries in the books of Alex Study’s

Journal of Alex study for the month of May 2016

Particulars Debit Credit

1. Storage expenses a/c Dr.

To bank a/c

400

400

2. Purchase a/c Dr.

To S. Hood a/c

1450

1450

2. Purchase a/c Dr.

To D. Main a/c

2060

2060

2 Purchase a/c Dr.

To W. Tone a/c

960

960

2 Purchase a/c Dr.

To R. Foot a/c

1610

1610

3. J Wilson a/c Dr.

To sales a/c

1120

1120

3. T. Cole a/c Dr.

To sales a/c

1640

1640

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. F. Syme a/c Dr.

To sales a/c

2080

2080

3. J. Allen a/c Dr.

To sales a/c

910

910

3. P. White a/c Dr.

To sales a/c

2420

2420

3. F. Lane a/c Dr.

To sales a/c

770

770

4. Motor car expenses a/c Dr.

To cash a/c

470

470

7. Drawing a/c Dr.

To cash a/c

1500

1500

9. T. Cole a/c Dr.

J. Fox a/c Dr.

To sales a/c

680

1310

11. Sales return a/c Dr.

To J. Wilson

To F. Syme a/c

680

270

410

14 Van a/c Dr.

To Abel Motors Ltd

28500

28500

16 (a). Bank a/c Dr.

Discount allowed a/c Dr.

To P Mullen

(b)

Bank a/c Dr.

Discount allowed a/c Dr.

To F. Lane

(c)

Bank a/c Dr.

Discount allowed a/c Dr.

To J. Wilson

(d)

Bank a/c Dr.

Discount allowed a/c Dr.

To F. Syme

1330

70

2945

155

807.5

42.5

1586.5

83.5

1400

3100

850

1670

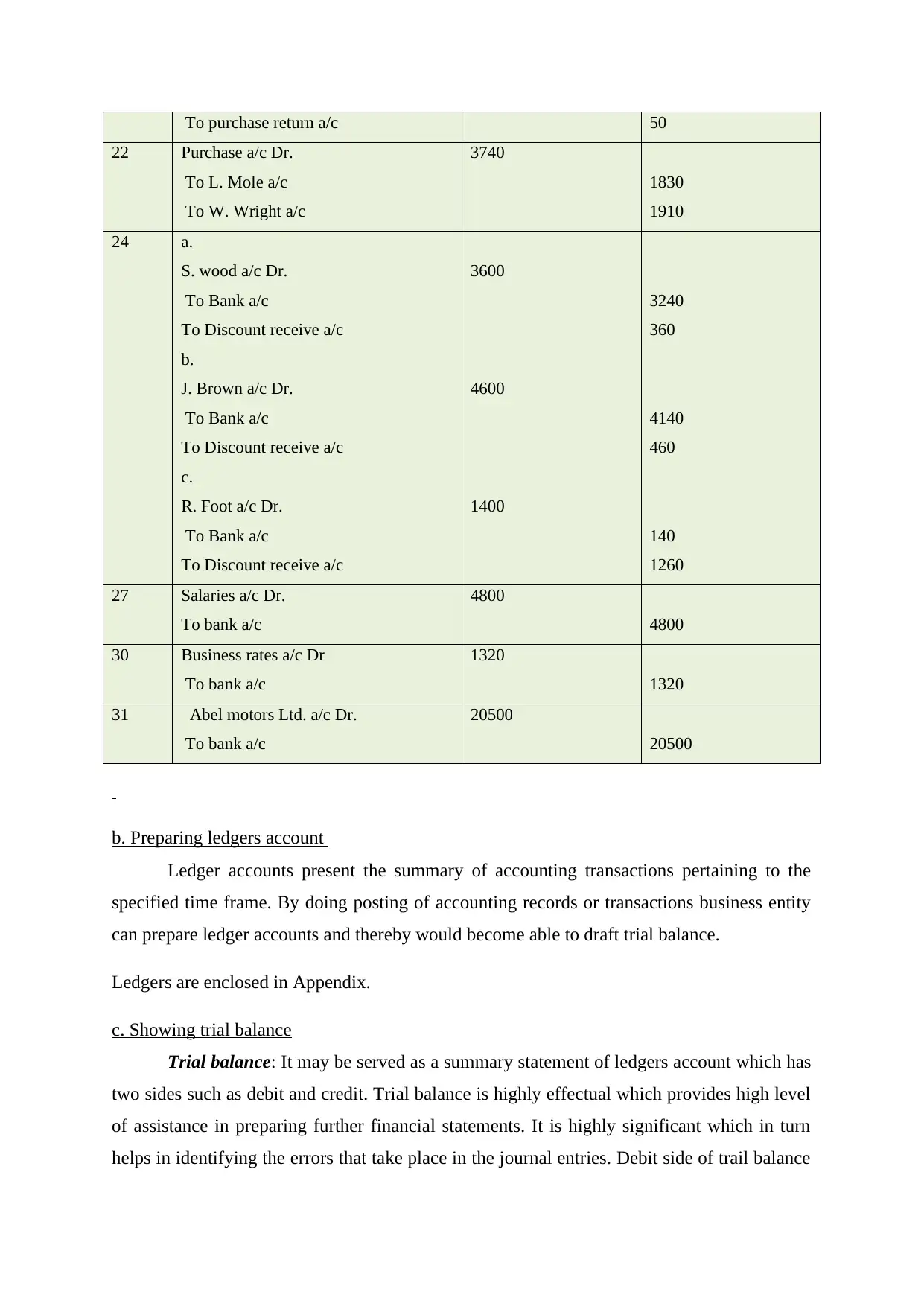

19 R. Foot a/c Dr. 50

To sales a/c

2080

2080

3. J. Allen a/c Dr.

To sales a/c

910

910

3. P. White a/c Dr.

To sales a/c

2420

2420

3. F. Lane a/c Dr.

To sales a/c

770

770

4. Motor car expenses a/c Dr.

To cash a/c

470

470

7. Drawing a/c Dr.

To cash a/c

1500

1500

9. T. Cole a/c Dr.

J. Fox a/c Dr.

To sales a/c

680

1310

11. Sales return a/c Dr.

To J. Wilson

To F. Syme a/c

680

270

410

14 Van a/c Dr.

To Abel Motors Ltd

28500

28500

16 (a). Bank a/c Dr.

Discount allowed a/c Dr.

To P Mullen

(b)

Bank a/c Dr.

Discount allowed a/c Dr.

To F. Lane

(c)

Bank a/c Dr.

Discount allowed a/c Dr.

To J. Wilson

(d)

Bank a/c Dr.

Discount allowed a/c Dr.

To F. Syme

1330

70

2945

155

807.5

42.5

1586.5

83.5

1400

3100

850

1670

19 R. Foot a/c Dr. 50

To purchase return a/c 50

22 Purchase a/c Dr.

To L. Mole a/c

To W. Wright a/c

3740

1830

1910

24 a.

S. wood a/c Dr.

To Bank a/c

To Discount receive a/c

b.

J. Brown a/c Dr.

To Bank a/c

To Discount receive a/c

c.

R. Foot a/c Dr.

To Bank a/c

To Discount receive a/c

3600

4600

1400

3240

360

4140

460

140

1260

27 Salaries a/c Dr.

To bank a/c

4800

4800

30 Business rates a/c Dr

To bank a/c

1320

1320

31 Abel motors Ltd. a/c Dr.

To bank a/c

20500

20500

b. Preparing ledgers account

Ledger accounts present the summary of accounting transactions pertaining to the

specified time frame. By doing posting of accounting records or transactions business entity

can prepare ledger accounts and thereby would become able to draft trial balance.

Ledgers are enclosed in Appendix.

c. Showing trial balance

Trial balance: It may be served as a summary statement of ledgers account which has

two sides such as debit and credit. Trial balance is highly effectual which provides high level

of assistance in preparing further financial statements. It is highly significant which in turn

helps in identifying the errors that take place in the journal entries. Debit side of trail balance

22 Purchase a/c Dr.

To L. Mole a/c

To W. Wright a/c

3740

1830

1910

24 a.

S. wood a/c Dr.

To Bank a/c

To Discount receive a/c

b.

J. Brown a/c Dr.

To Bank a/c

To Discount receive a/c

c.

R. Foot a/c Dr.

To Bank a/c

To Discount receive a/c

3600

4600

1400

3240

360

4140

460

140

1260

27 Salaries a/c Dr.

To bank a/c

4800

4800

30 Business rates a/c Dr

To bank a/c

1320

1320

31 Abel motors Ltd. a/c Dr.

To bank a/c

20500

20500

b. Preparing ledgers account

Ledger accounts present the summary of accounting transactions pertaining to the

specified time frame. By doing posting of accounting records or transactions business entity

can prepare ledger accounts and thereby would become able to draft trial balance.

Ledgers are enclosed in Appendix.

c. Showing trial balance

Trial balance: It may be served as a summary statement of ledgers account which has

two sides such as debit and credit. Trial balance is highly effectual which provides high level

of assistance in preparing further financial statements. It is highly significant which in turn

helps in identifying the errors that take place in the journal entries. Debit side of trail balance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

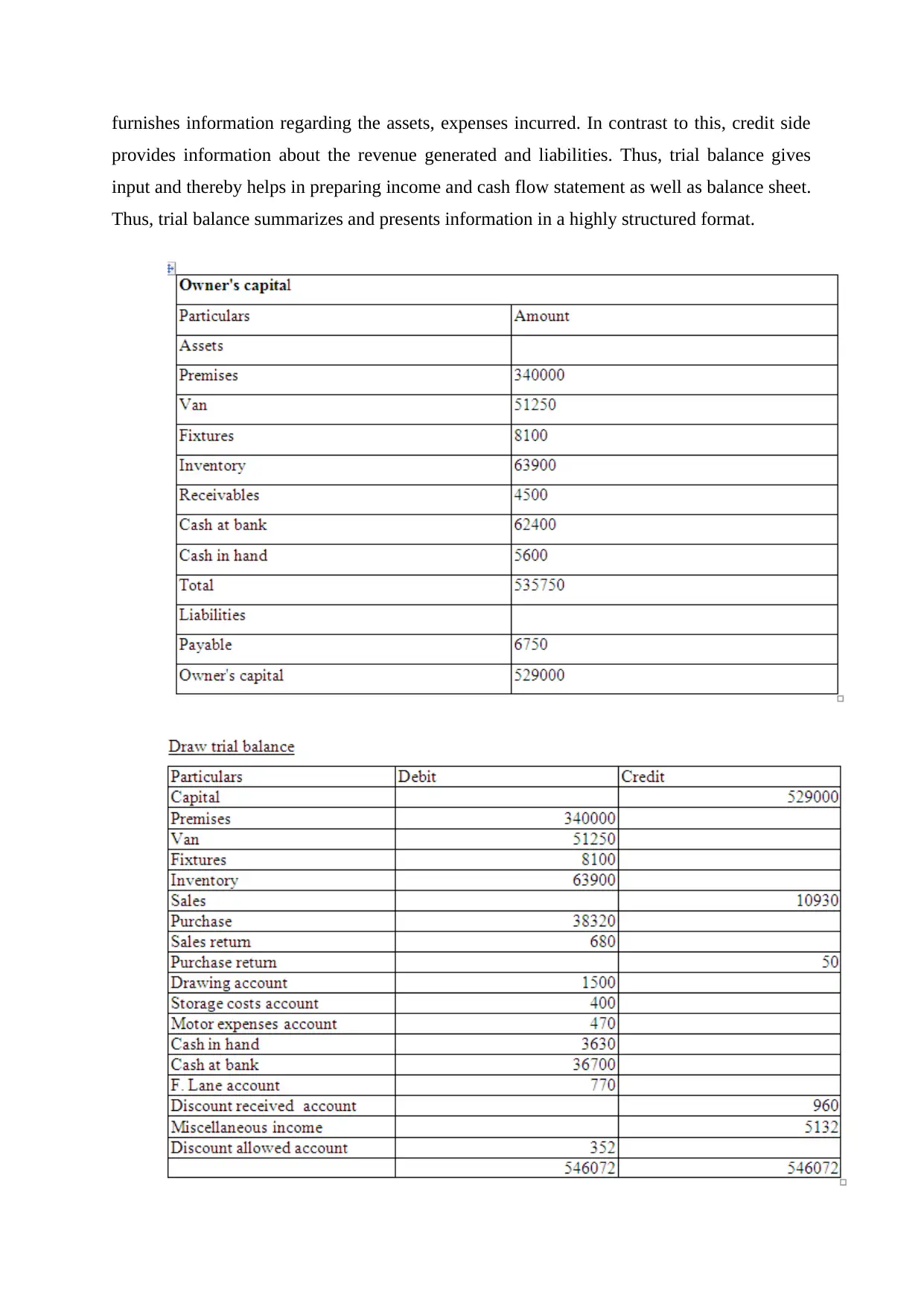

furnishes information regarding the assets, expenses incurred. In contrast to this, credit side

provides information about the revenue generated and liabilities. Thus, trial balance gives

input and thereby helps in preparing income and cash flow statement as well as balance sheet.

Thus, trial balance summarizes and presents information in a highly structured format.

provides information about the revenue generated and liabilities. Thus, trial balance gives

input and thereby helps in preparing income and cash flow statement as well as balance sheet.

Thus, trial balance summarizes and presents information in a highly structured format.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CLIENT 2

On the basis of cited case situation, Peter Piper is sole trader which in turn lays high

level of emphasis on preparing income statement. Moreover, doing assessment of return over

the expenses is one of the main objectives of sole trader. In the sole proprietor firm, business

entity is highly concerned towards the sales revenue and profit margin generated in against to

the expenses. Along with this, sole trader also prepares balance sheet with the motive to get

information regarding the liabilities and assets (Kwinto and Voss, 2016). Both such

statements are highly significant which in turn provides assistance to the sole trader namely

Peter Piper in making evaluation of financial health and performance (Iatridis, 2016). This in

turn assists sole trader in developing highly effectual and competent financial framework for

the upcoming time period.

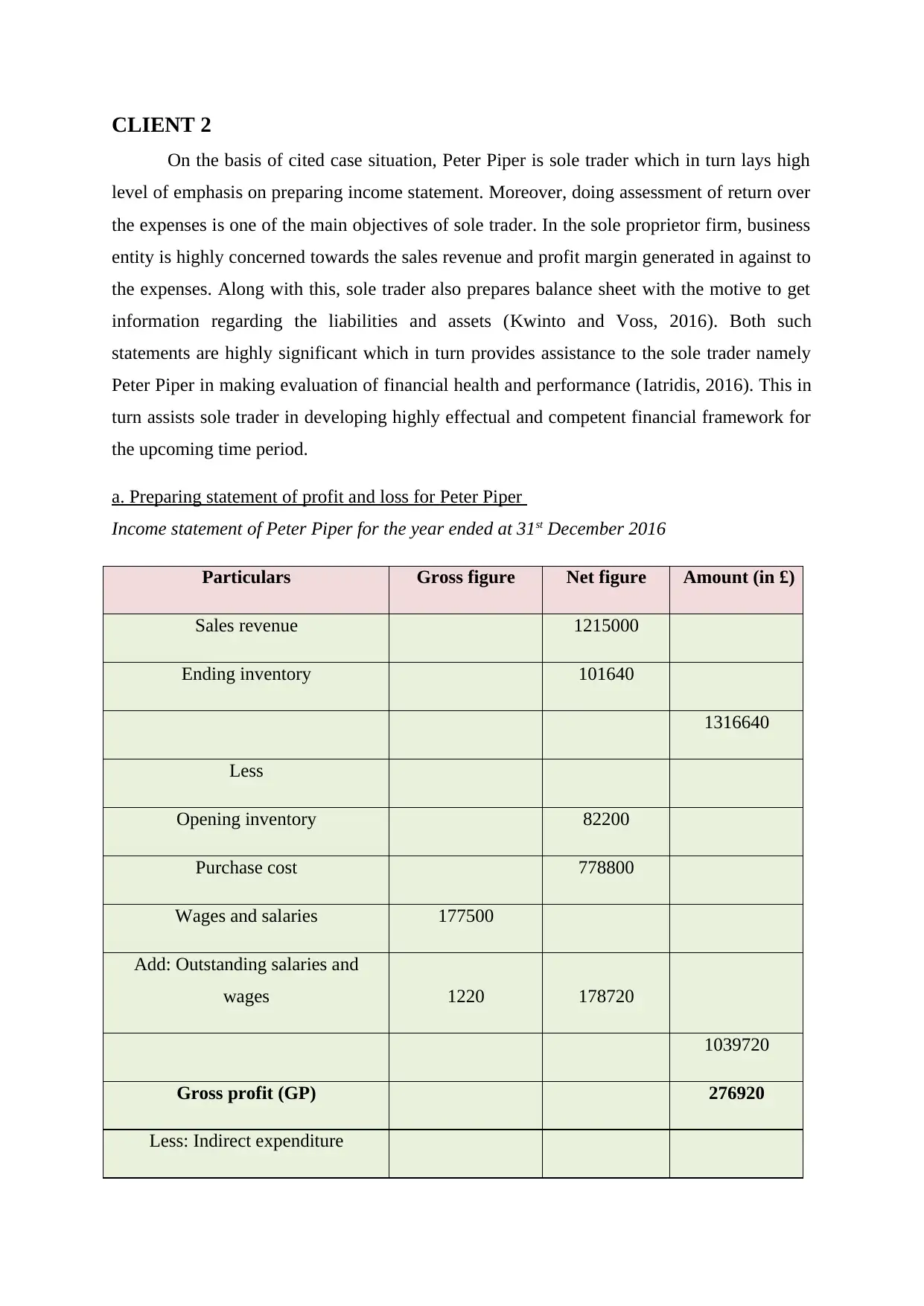

a. Preparing statement of profit and loss for Peter Piper

Income statement of Peter Piper for the year ended at 31st December 2016

Particulars Gross figure Net figure Amount (in £)

Sales revenue 1215000

Ending inventory 101640

1316640

Less

Opening inventory 82200

Purchase cost 778800

Wages and salaries 177500

Add: Outstanding salaries and

wages 1220 178720

1039720

Gross profit (GP) 276920

Less: Indirect expenditure

On the basis of cited case situation, Peter Piper is sole trader which in turn lays high

level of emphasis on preparing income statement. Moreover, doing assessment of return over

the expenses is one of the main objectives of sole trader. In the sole proprietor firm, business

entity is highly concerned towards the sales revenue and profit margin generated in against to

the expenses. Along with this, sole trader also prepares balance sheet with the motive to get

information regarding the liabilities and assets (Kwinto and Voss, 2016). Both such

statements are highly significant which in turn provides assistance to the sole trader namely

Peter Piper in making evaluation of financial health and performance (Iatridis, 2016). This in

turn assists sole trader in developing highly effectual and competent financial framework for

the upcoming time period.

a. Preparing statement of profit and loss for Peter Piper

Income statement of Peter Piper for the year ended at 31st December 2016

Particulars Gross figure Net figure Amount (in £)

Sales revenue 1215000

Ending inventory 101640

1316640

Less

Opening inventory 82200

Purchase cost 778800

Wages and salaries 177500

Add: Outstanding salaries and

wages 1220 178720

1039720

Gross profit (GP) 276920

Less: Indirect expenditure

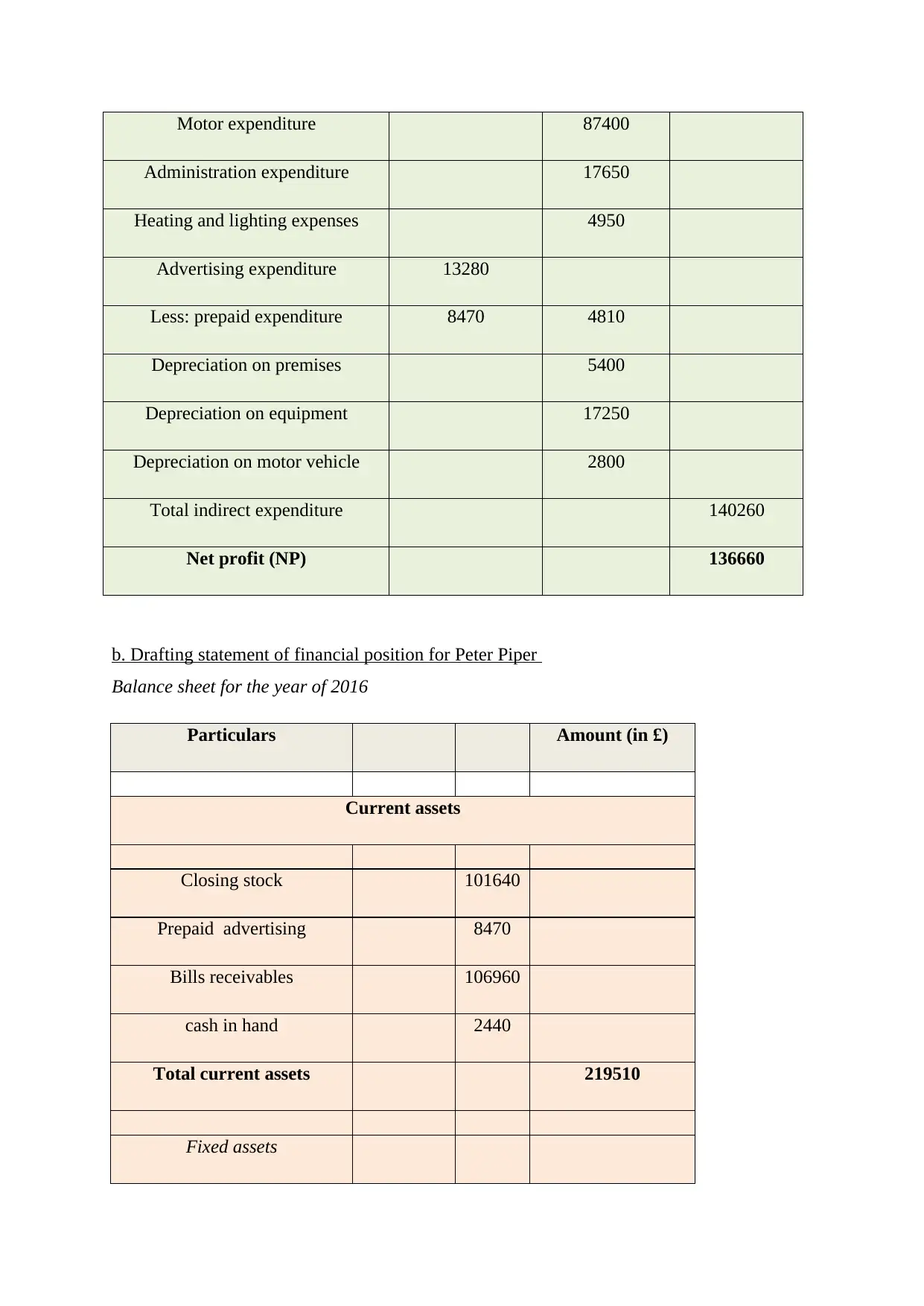

Motor expenditure 87400

Administration expenditure 17650

Heating and lighting expenses 4950

Advertising expenditure 13280

Less: prepaid expenditure 8470 4810

Depreciation on premises 5400

Depreciation on equipment 17250

Depreciation on motor vehicle 2800

Total indirect expenditure 140260

Net profit (NP) 136660

b. Drafting statement of financial position for Peter Piper

Balance sheet for the year of 2016

Particulars Amount (in £)

Current assets

Closing stock 101640

Prepaid advertising 8470

Bills receivables 106960

cash in hand 2440

Total current assets 219510

Fixed assets

Administration expenditure 17650

Heating and lighting expenses 4950

Advertising expenditure 13280

Less: prepaid expenditure 8470 4810

Depreciation on premises 5400

Depreciation on equipment 17250

Depreciation on motor vehicle 2800

Total indirect expenditure 140260

Net profit (NP) 136660

b. Drafting statement of financial position for Peter Piper

Balance sheet for the year of 2016

Particulars Amount (in £)

Current assets

Closing stock 101640

Prepaid advertising 8470

Bills receivables 106960

cash in hand 2440

Total current assets 219510

Fixed assets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

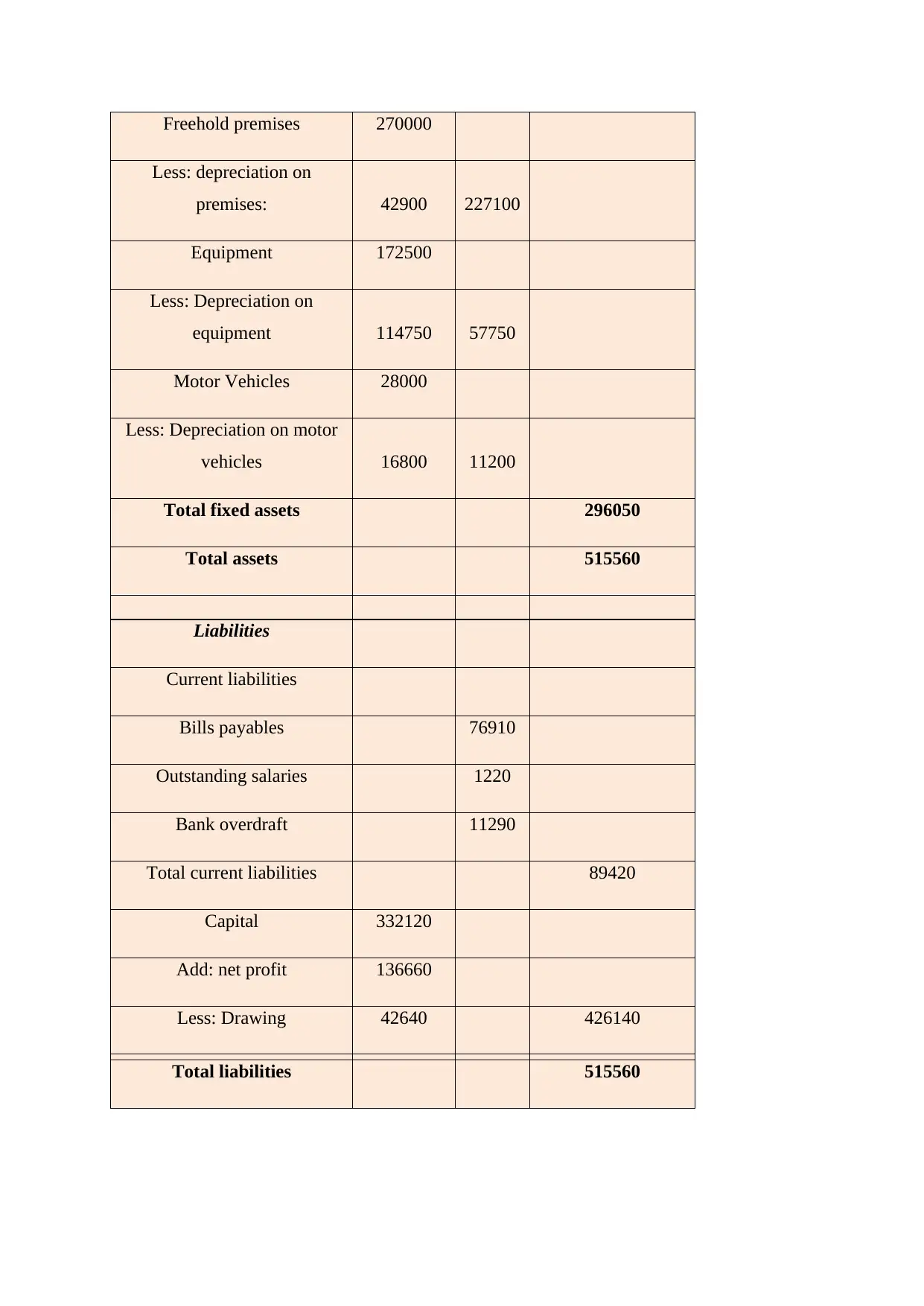

Freehold premises 270000

Less: depreciation on

premises: 42900 227100

Equipment 172500

Less: Depreciation on

equipment 114750 57750

Motor Vehicles 28000

Less: Depreciation on motor

vehicles 16800 11200

Total fixed assets 296050

Total assets 515560

Liabilities

Current liabilities

Bills payables 76910

Outstanding salaries 1220

Bank overdraft 11290

Total current liabilities 89420

Capital 332120

Add: net profit 136660

Less: Drawing 42640 426140

Total liabilities 515560

Less: depreciation on

premises: 42900 227100

Equipment 172500

Less: Depreciation on

equipment 114750 57750

Motor Vehicles 28000

Less: Depreciation on motor

vehicles 16800 11200

Total fixed assets 296050

Total assets 515560

Liabilities

Current liabilities

Bills payables 76910

Outstanding salaries 1220

Bank overdraft 11290

Total current liabilities 89420

Capital 332120

Add: net profit 136660

Less: Drawing 42640 426140

Total liabilities 515560

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CLIENT 3

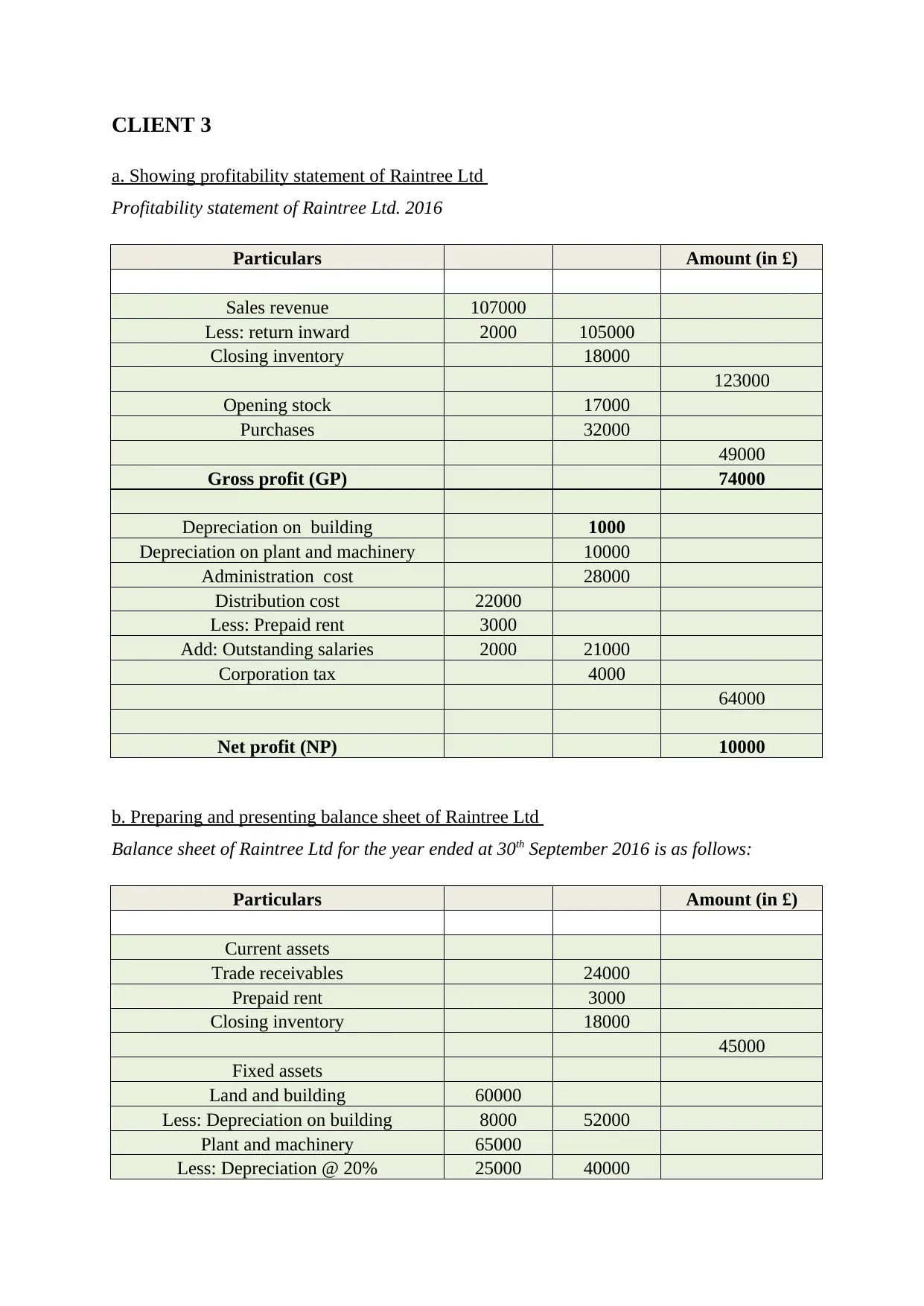

a. Showing profitability statement of Raintree Ltd

Profitability statement of Raintree Ltd. 2016

Particulars Amount (in £)

Sales revenue 107000

Less: return inward 2000 105000

Closing inventory 18000

123000

Opening stock 17000

Purchases 32000

49000

Gross profit (GP) 74000

Depreciation on building 1000

Depreciation on plant and machinery 10000

Administration cost 28000

Distribution cost 22000

Less: Prepaid rent 3000

Add: Outstanding salaries 2000 21000

Corporation tax 4000

64000

Net profit (NP) 10000

b. Preparing and presenting balance sheet of Raintree Ltd

Balance sheet of Raintree Ltd for the year ended at 30th September 2016 is as follows:

Particulars Amount (in £)

Current assets

Trade receivables 24000

Prepaid rent 3000

Closing inventory 18000

45000

Fixed assets

Land and building 60000

Less: Depreciation on building 8000 52000

Plant and machinery 65000

Less: Depreciation @ 20% 25000 40000

a. Showing profitability statement of Raintree Ltd

Profitability statement of Raintree Ltd. 2016

Particulars Amount (in £)

Sales revenue 107000

Less: return inward 2000 105000

Closing inventory 18000

123000

Opening stock 17000

Purchases 32000

49000

Gross profit (GP) 74000

Depreciation on building 1000

Depreciation on plant and machinery 10000

Administration cost 28000

Distribution cost 22000

Less: Prepaid rent 3000

Add: Outstanding salaries 2000 21000

Corporation tax 4000

64000

Net profit (NP) 10000

b. Preparing and presenting balance sheet of Raintree Ltd

Balance sheet of Raintree Ltd for the year ended at 30th September 2016 is as follows:

Particulars Amount (in £)

Current assets

Trade receivables 24000

Prepaid rent 3000

Closing inventory 18000

45000

Fixed assets

Land and building 60000

Less: Depreciation on building 8000 52000

Plant and machinery 65000

Less: Depreciation @ 20% 25000 40000

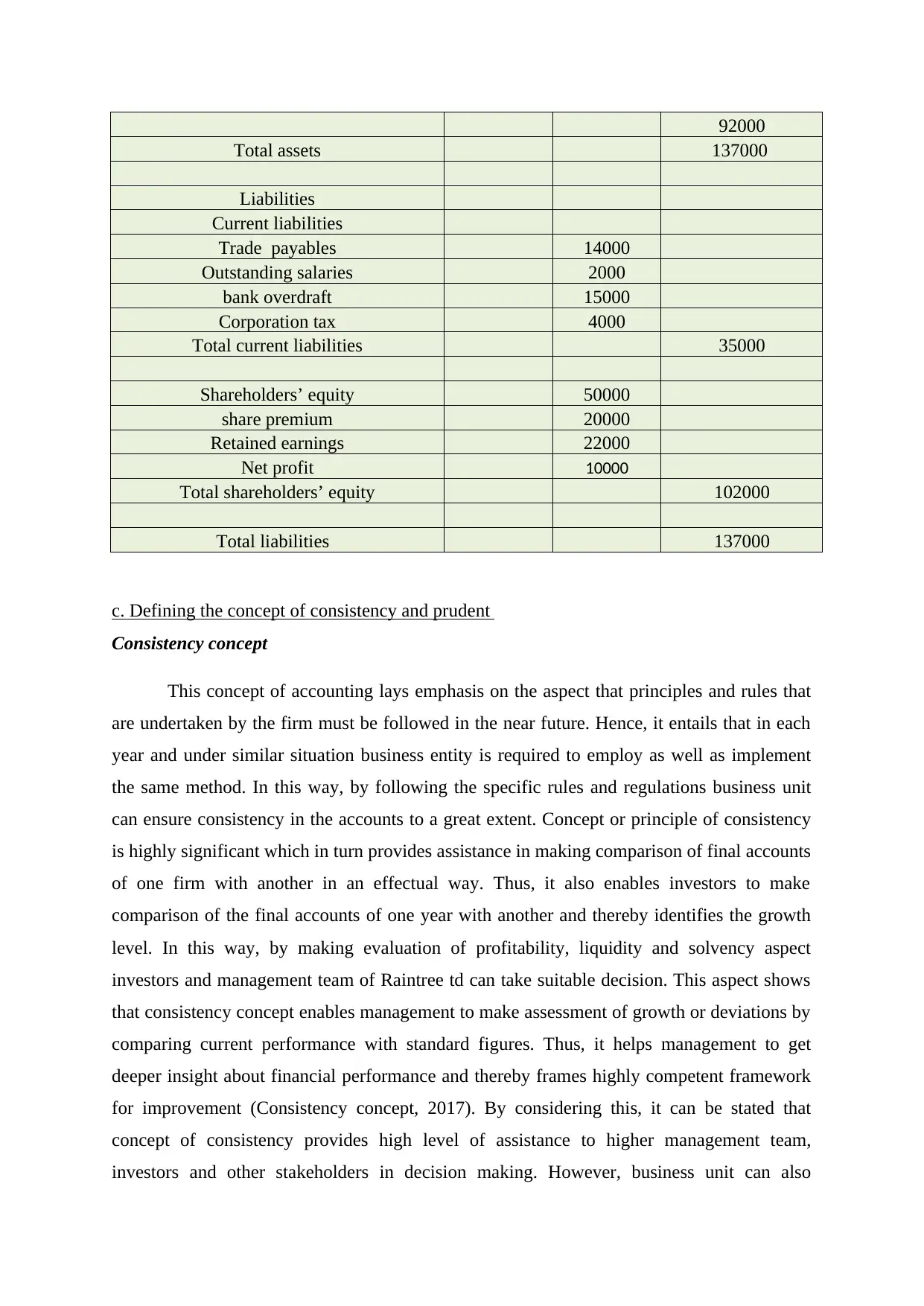

92000

Total assets 137000

Liabilities

Current liabilities

Trade payables 14000

Outstanding salaries 2000

bank overdraft 15000

Corporation tax 4000

Total current liabilities 35000

Shareholders’ equity 50000

share premium 20000

Retained earnings 22000

Net profit 10000

Total shareholders’ equity 102000

Total liabilities 137000

c. Defining the concept of consistency and prudent

Consistency concept

This concept of accounting lays emphasis on the aspect that principles and rules that

are undertaken by the firm must be followed in the near future. Hence, it entails that in each

year and under similar situation business entity is required to employ as well as implement

the same method. In this way, by following the specific rules and regulations business unit

can ensure consistency in the accounts to a great extent. Concept or principle of consistency

is highly significant which in turn provides assistance in making comparison of final accounts

of one firm with another in an effectual way. Thus, it also enables investors to make

comparison of the final accounts of one year with another and thereby identifies the growth

level. In this way, by making evaluation of profitability, liquidity and solvency aspect

investors and management team of Raintree td can take suitable decision. This aspect shows

that consistency concept enables management to make assessment of growth or deviations by

comparing current performance with standard figures. Thus, it helps management to get

deeper insight about financial performance and thereby frames highly competent framework

for improvement (Consistency concept, 2017). By considering this, it can be stated that

concept of consistency provides high level of assistance to higher management team,

investors and other stakeholders in decision making. However, business unit can also

Total assets 137000

Liabilities

Current liabilities

Trade payables 14000

Outstanding salaries 2000

bank overdraft 15000

Corporation tax 4000

Total current liabilities 35000

Shareholders’ equity 50000

share premium 20000

Retained earnings 22000

Net profit 10000

Total shareholders’ equity 102000

Total liabilities 137000

c. Defining the concept of consistency and prudent

Consistency concept

This concept of accounting lays emphasis on the aspect that principles and rules that

are undertaken by the firm must be followed in the near future. Hence, it entails that in each

year and under similar situation business entity is required to employ as well as implement

the same method. In this way, by following the specific rules and regulations business unit

can ensure consistency in the accounts to a great extent. Concept or principle of consistency

is highly significant which in turn provides assistance in making comparison of final accounts

of one firm with another in an effectual way. Thus, it also enables investors to make

comparison of the final accounts of one year with another and thereby identifies the growth

level. In this way, by making evaluation of profitability, liquidity and solvency aspect

investors and management team of Raintree td can take suitable decision. This aspect shows

that consistency concept enables management to make assessment of growth or deviations by

comparing current performance with standard figures. Thus, it helps management to get

deeper insight about financial performance and thereby frames highly competent framework

for improvement (Consistency concept, 2017). By considering this, it can be stated that

concept of consistency provides high level of assistance to higher management team,

investors and other stakeholders in decision making. However, business unit can also

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.