University Accounting Report: Financial Analysis and Planning

VerifiedAdded on 2021/04/21

|18

|2930

|422

Report

AI Summary

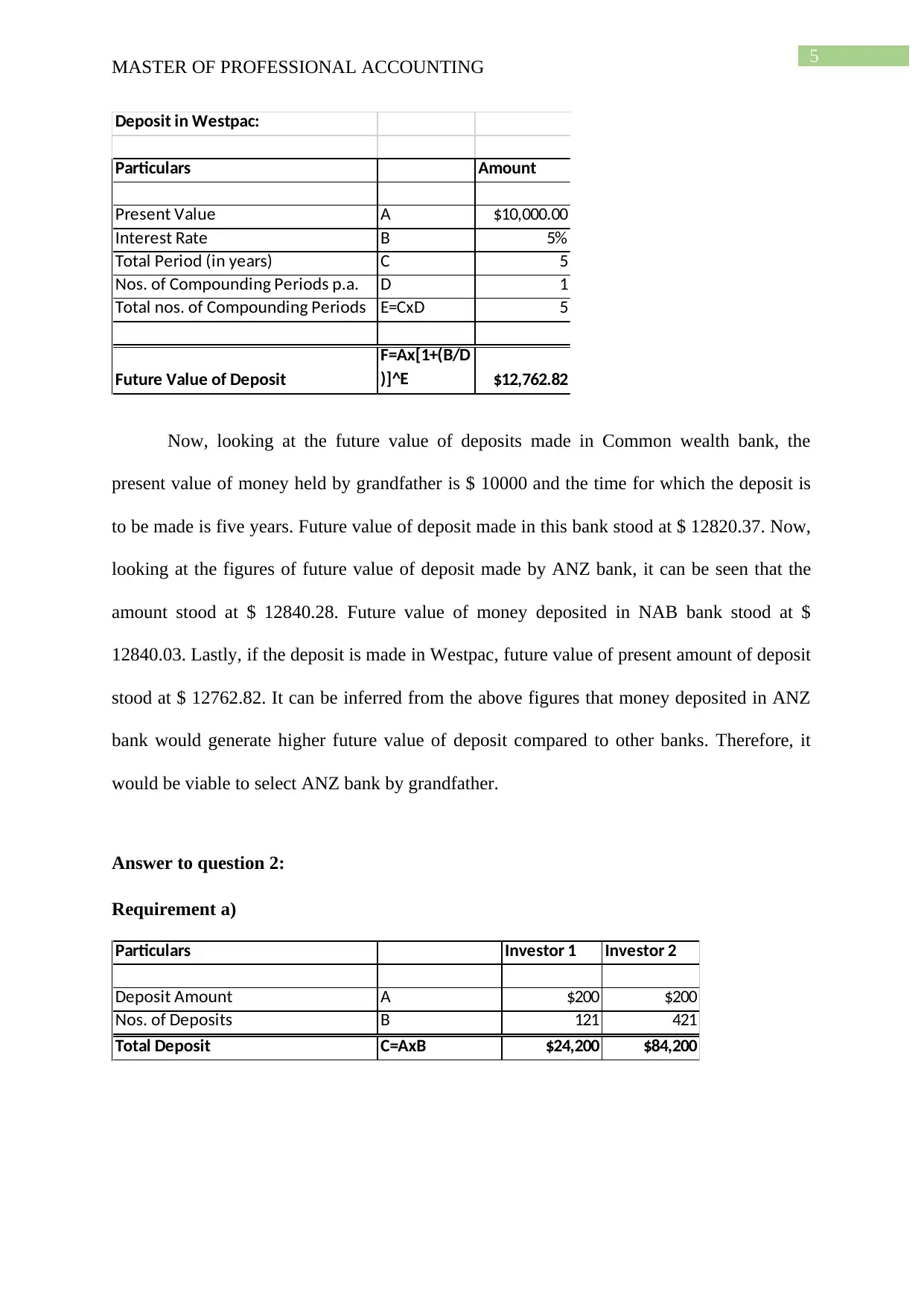

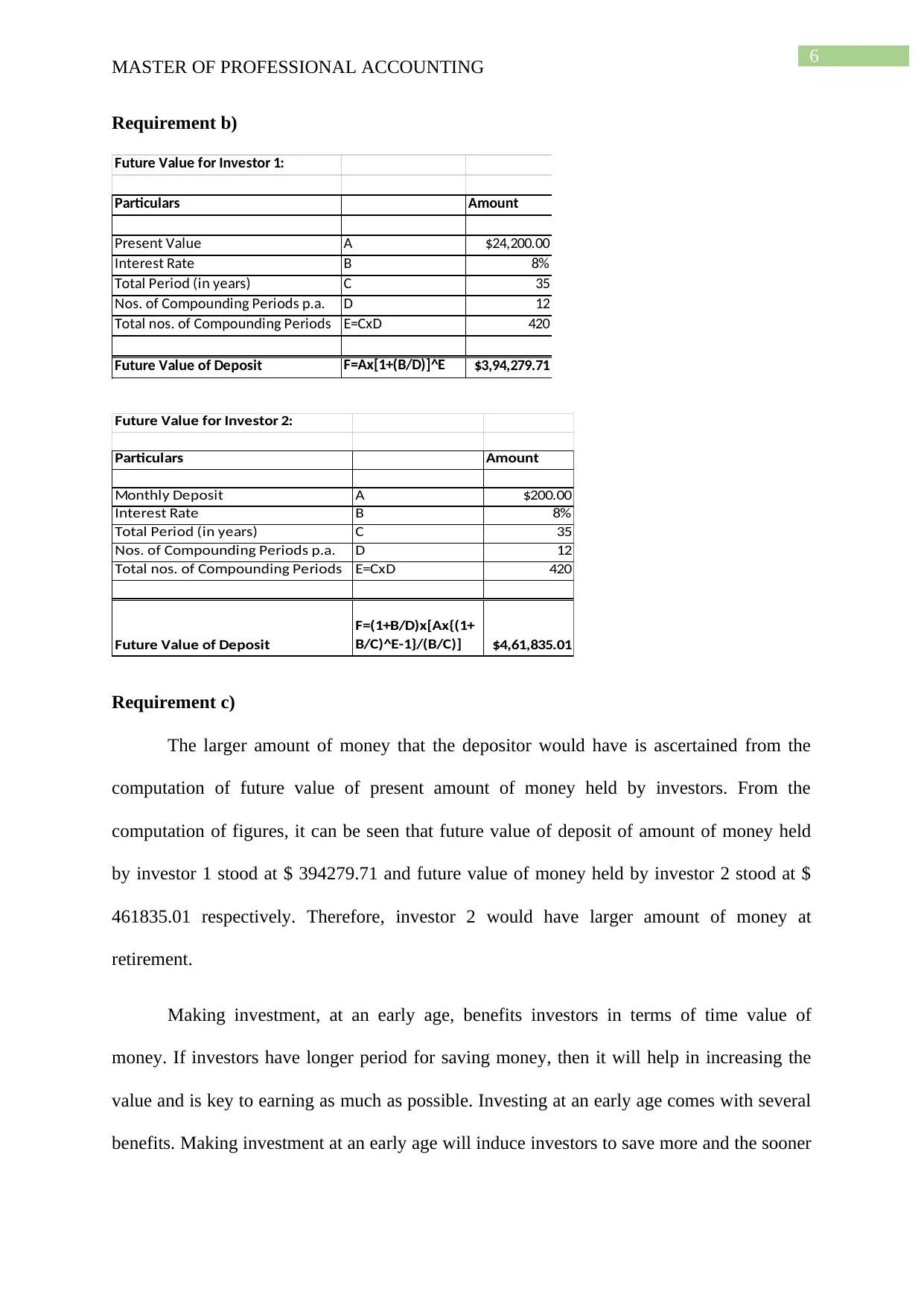

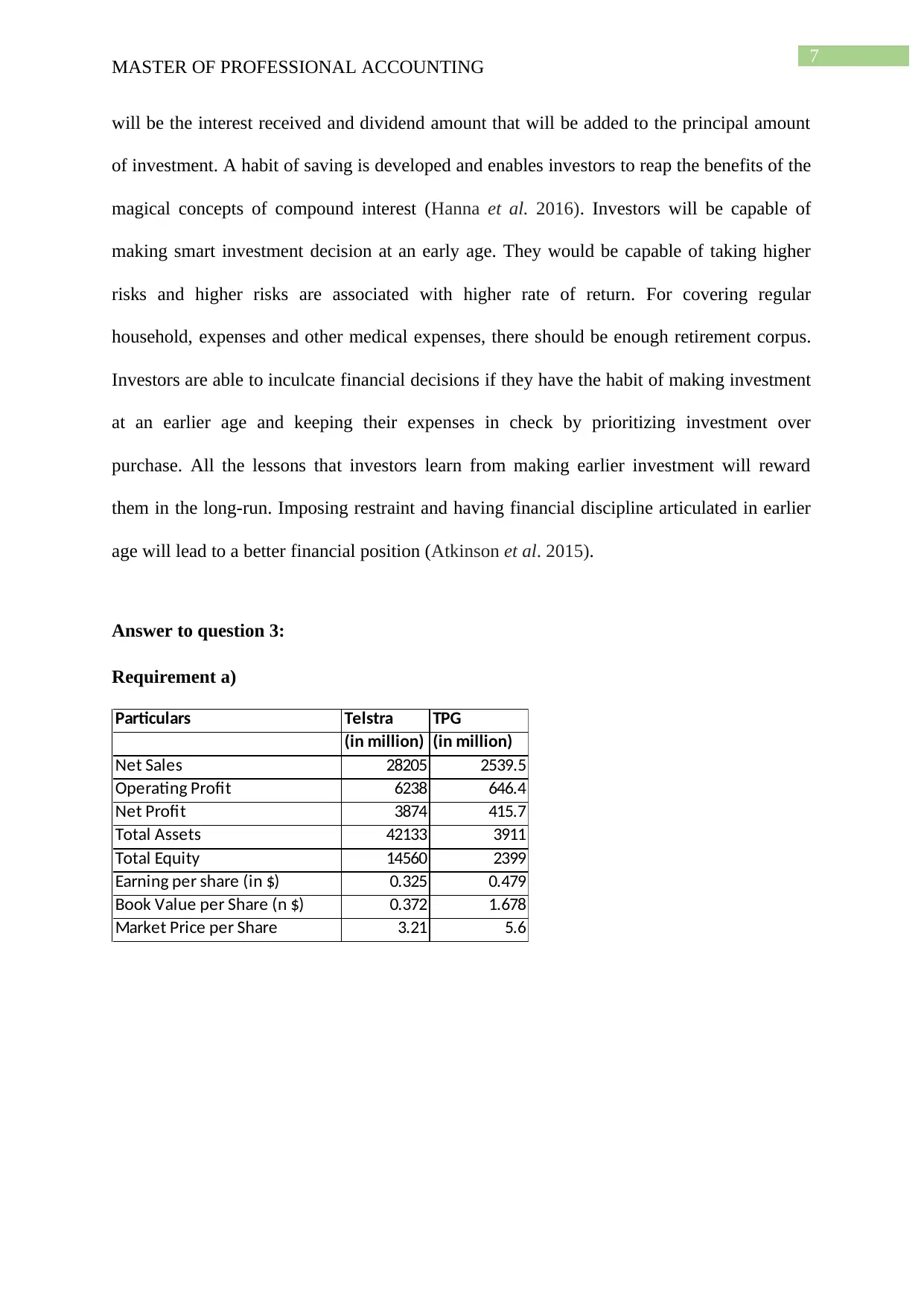

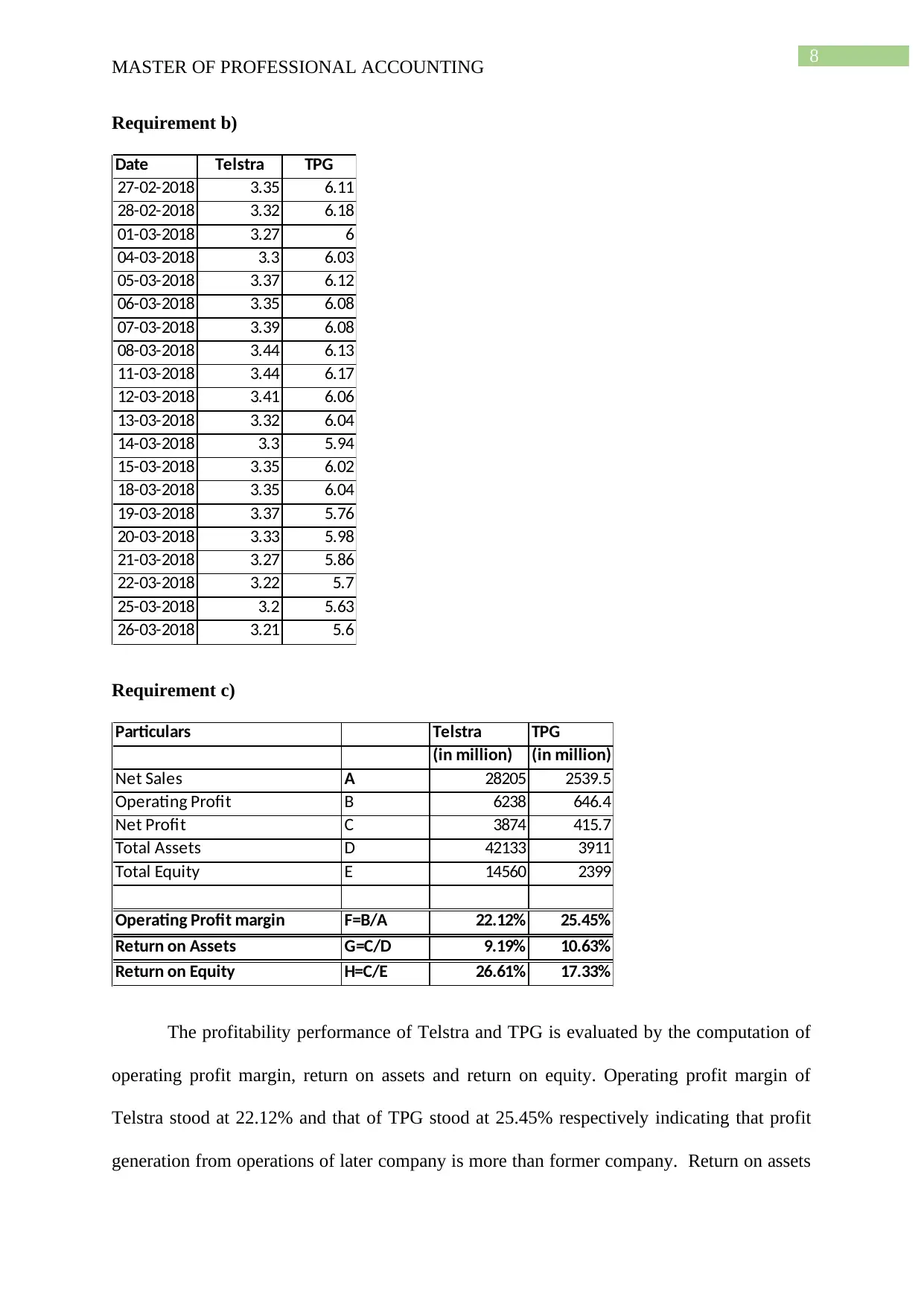

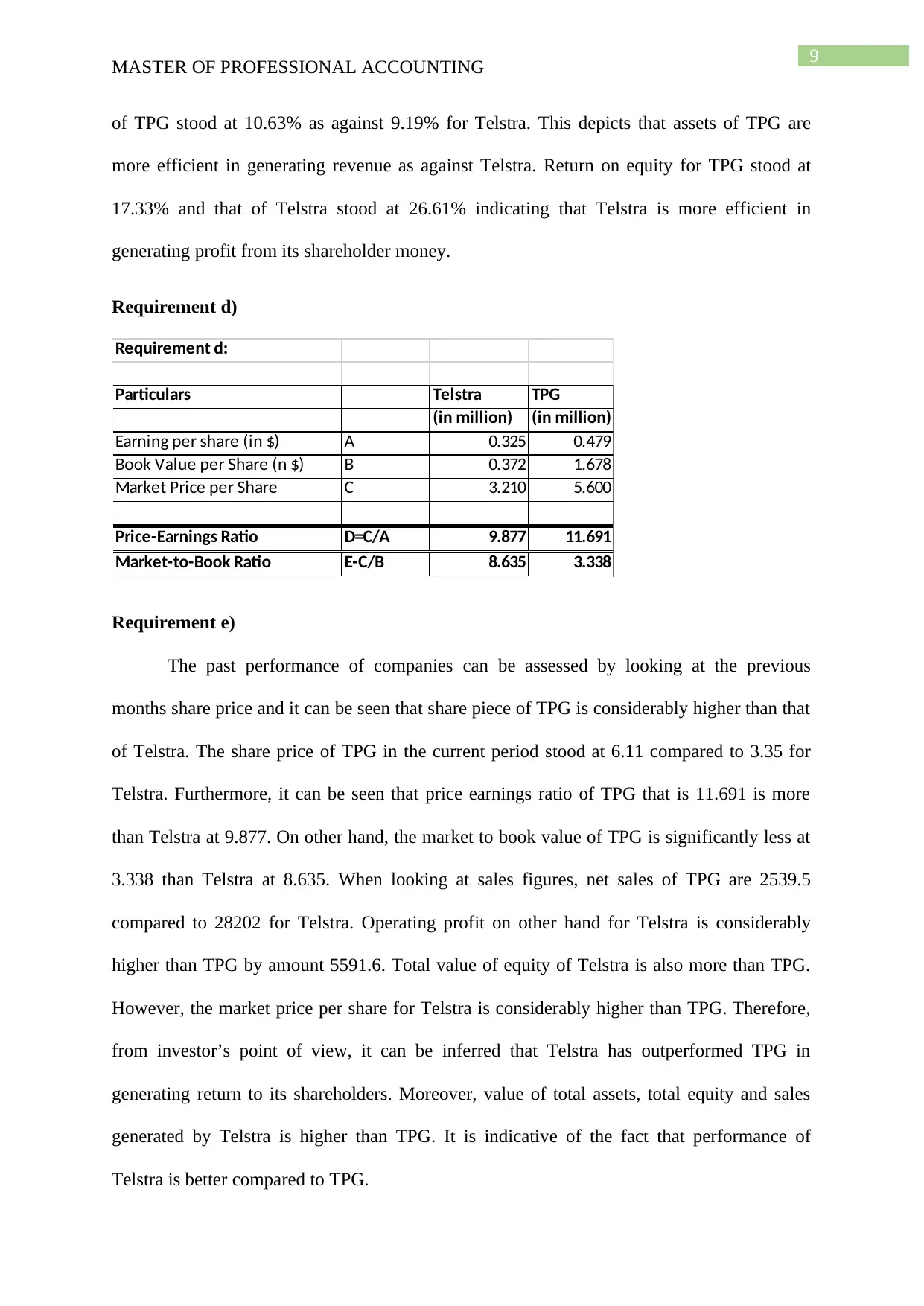

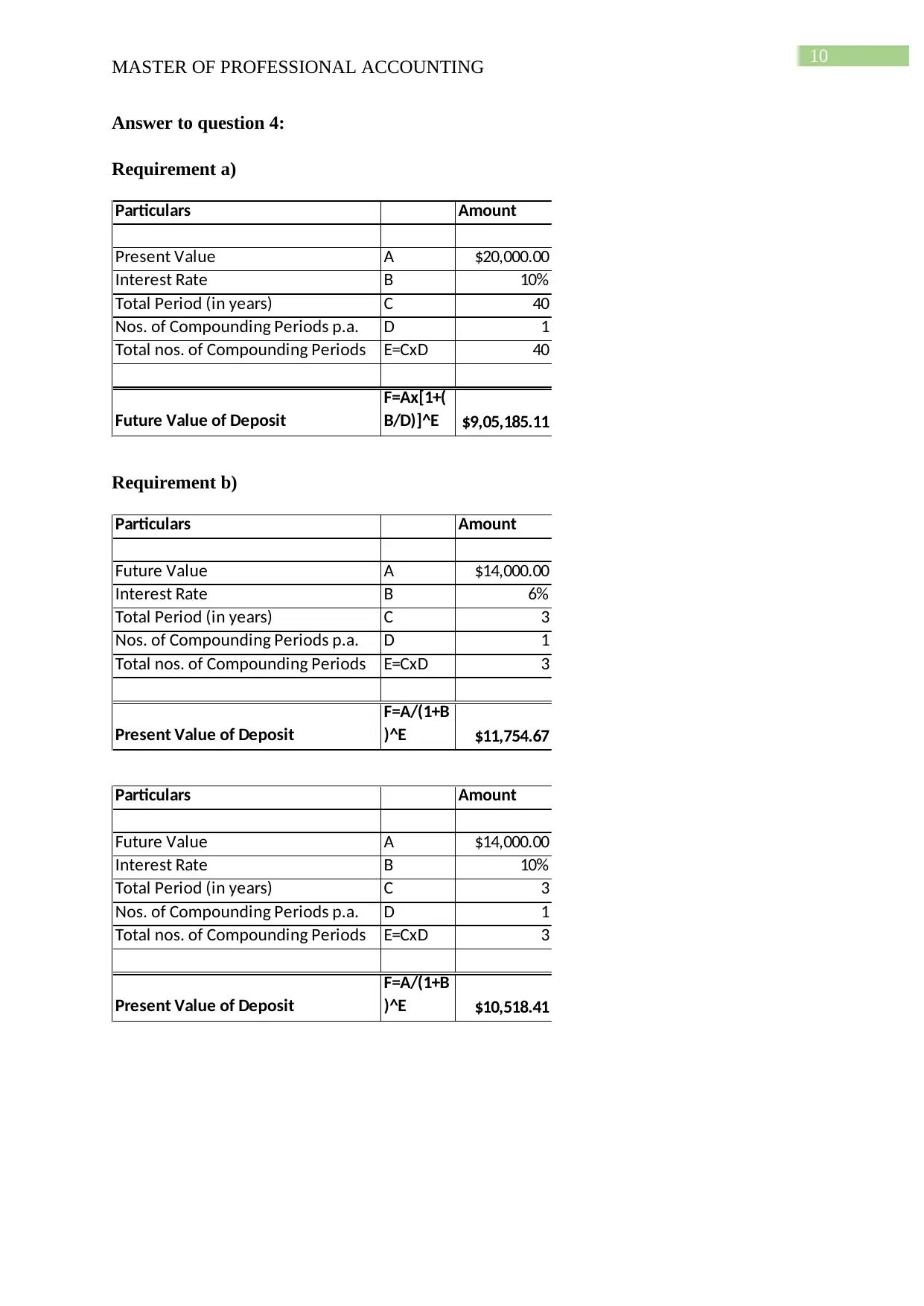

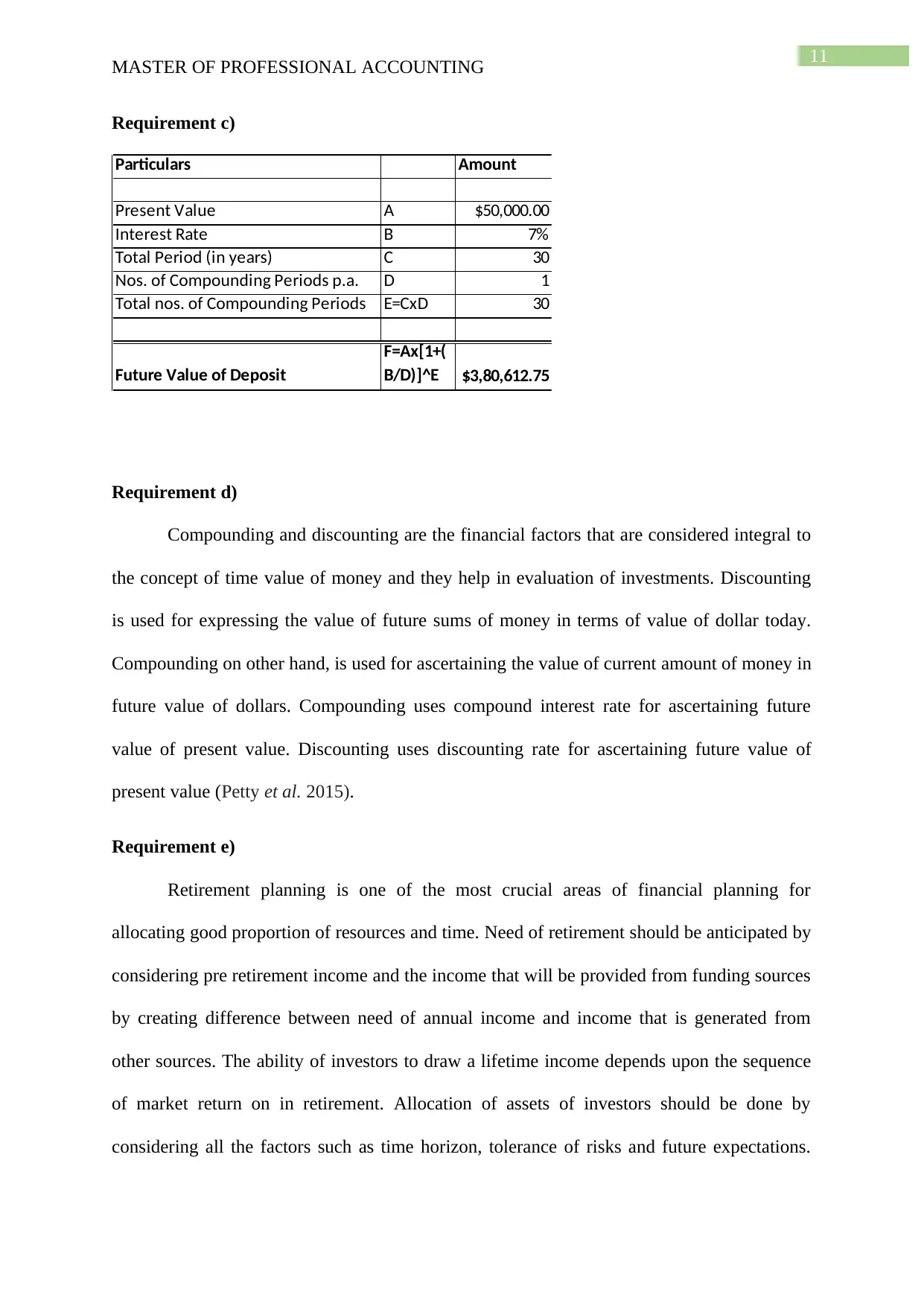

This comprehensive report, prepared for a Master of Professional Accounting program, delves into various financial accounting concepts and their practical applications. It begins by calculating the annual deposit amount required for university expenses, considering interest rates and the number of years. The report then evaluates different banks for investment, comparing future values and recommending the most viable option. It further explores the time value of money, analyzing the impact of early investments on retirement savings and comparing the financial outcomes of different investment strategies. The report also assesses the profitability and performance of Telstra and TPG, comparing key financial metrics like operating profit margin, return on assets, and return on equity, along with stock prices and sales figures to determine the better-performing company. Additionally, the report discusses compounding and discounting, crucial financial factors for investment evaluation, and emphasizes the importance of retirement planning, including asset allocation and the impact of interest rates. Finally, the report investigates the effects of cash rates on the Australian tourism sector, analyzing historical data and the reasons behind changes in cash rates, to understand the impact of monetary policy on the industry. The report concludes with a discussion on the implications of cash rate changes and their impact on economic indicators.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.