Financial Accounting Report: Analysis of Different Firms' Accounting

VerifiedAdded on 2020/01/21

|43

|7291

|197

Report

AI Summary

This report provides a comprehensive overview of financial accounting, beginning with an introduction to financial accounting terms, regulations, and fundamental accounting principles. It delves into the conventions of consistency and material disclosure, crucial for accurate financial reporting. The report then explores accounting practices for various firms through detailed case studies, including double-entry recording, ledger entries, and the preparation of profit and loss accounts and balance sheets. It includes illustrations of journal entries, ledger accounts, and bank reconciliations for several clients, such as Alex Study, Peter Piper, Raintree Ltd, and Kendal Ltd, providing practical examples of financial statement preparation and analysis. The report also covers trail balances and the application of accounting principles to diverse business scenarios, concluding with a synthesis of the key concepts discussed.

Financial Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

a) FINANCIAL ACCOUNTING AND ITS DIFFERENT TERMS...............................................4

1) Financial accounting................................................................................................................4

2) Regulations regarding financial accounting............................................................................5

3) Accounting rules and principles..............................................................................................6

4) Conventions and concepts related to consistency and material disclosure.............................7

B) ACCOUNTING FOR DIFFERENT FIRMS..............................................................................8

Client 1(Alex Study)....................................................................................................................8

Client 2 (Peter Piper case)..........................................................................................................25

Client 3 (Raintree Ltd)...............................................................................................................30

Client 4 (Kendal ltd and bank statement)..................................................................................35

Client 5 (Henderson)..................................................................................................................38

Client 6 (Suspense account concept).........................................................................................42

CONCLUSION..............................................................................................................................45

REFERENCE.................................................................................................................................46

2

INTRODUCTION...........................................................................................................................4

a) FINANCIAL ACCOUNTING AND ITS DIFFERENT TERMS...............................................4

1) Financial accounting................................................................................................................4

2) Regulations regarding financial accounting............................................................................5

3) Accounting rules and principles..............................................................................................6

4) Conventions and concepts related to consistency and material disclosure.............................7

B) ACCOUNTING FOR DIFFERENT FIRMS..............................................................................8

Client 1(Alex Study)....................................................................................................................8

Client 2 (Peter Piper case)..........................................................................................................25

Client 3 (Raintree Ltd)...............................................................................................................30

Client 4 (Kendal ltd and bank statement)..................................................................................35

Client 5 (Henderson)..................................................................................................................38

Client 6 (Suspense account concept).........................................................................................42

CONCLUSION..............................................................................................................................45

REFERENCE.................................................................................................................................46

2

Illustration Index

Illustration 1: Data entry at primary level........................................................................................8

Illustration 2: Double Entry recording within relevant Journal.....................................................11

Illustration 3: Purchase Journal Account.......................................................................................12

Illustration 4: Receipt Account......................................................................................................13

Illustration 5: Payment and discount received account..................................................................14

Illustration 6: Discount allowed account.......................................................................................15

Illustration 7: R. Foot, J. Wilson and T. Cole account...................................................................16

Illustration 8: F. Syme, J. Allen and P. white account...................................................................17

Illustration 9: F. lane, S. Hood and J. Brown account...................................................................18

Illustration 10: J. Fox, P. Mullen, L. Mole and W. Wright account..............................................19

Illustration 11: D. Main, W. Tone and Abel motors account........................................................20

Illustration 12: Bank account.........................................................................................................20

Illustration 13: Van and Storage costs account..............................................................................21

Illustration 14: Profit and loss account for Peter and Piper...........................................................23

Illustration 15: Balance sheet for Peter and Piper..........................................................................24

Illustration 16: Profit and loss account for Raintree Ltd................................................................26

Illustration 17: Balance sheet for Rain tree Ltd.............................................................................28

Illustration 18: Statement of bank reconciliation for 1st December 2016.....................................32

Illustration 19: Kendal Ltd's updated cash book for December 2016...........................................33

Illustration 20: Statement of bank reconciliation for 1st December 2016.....................................33

Illustration 21: Statement reconciliation as 21st December..........................................................34

Illustration 22: sales ledger account ..............................................................................................35

Illustration 23: Purchase ledger account........................................................................................36

Illustration 24: Statement of bank reconciliation for 1st December 2016.....................................36

Illustration 25: Statement of bank reconciliation for 1st December 2016.....................................37

Illustration 26: Trail balance..........................................................................................................39

Illustration 27: Statement of bank reconciliation for 1st December 2016.....................................40

3

Illustration 1: Data entry at primary level........................................................................................8

Illustration 2: Double Entry recording within relevant Journal.....................................................11

Illustration 3: Purchase Journal Account.......................................................................................12

Illustration 4: Receipt Account......................................................................................................13

Illustration 5: Payment and discount received account..................................................................14

Illustration 6: Discount allowed account.......................................................................................15

Illustration 7: R. Foot, J. Wilson and T. Cole account...................................................................16

Illustration 8: F. Syme, J. Allen and P. white account...................................................................17

Illustration 9: F. lane, S. Hood and J. Brown account...................................................................18

Illustration 10: J. Fox, P. Mullen, L. Mole and W. Wright account..............................................19

Illustration 11: D. Main, W. Tone and Abel motors account........................................................20

Illustration 12: Bank account.........................................................................................................20

Illustration 13: Van and Storage costs account..............................................................................21

Illustration 14: Profit and loss account for Peter and Piper...........................................................23

Illustration 15: Balance sheet for Peter and Piper..........................................................................24

Illustration 16: Profit and loss account for Raintree Ltd................................................................26

Illustration 17: Balance sheet for Rain tree Ltd.............................................................................28

Illustration 18: Statement of bank reconciliation for 1st December 2016.....................................32

Illustration 19: Kendal Ltd's updated cash book for December 2016...........................................33

Illustration 20: Statement of bank reconciliation for 1st December 2016.....................................33

Illustration 21: Statement reconciliation as 21st December..........................................................34

Illustration 22: sales ledger account ..............................................................................................35

Illustration 23: Purchase ledger account........................................................................................36

Illustration 24: Statement of bank reconciliation for 1st December 2016.....................................36

Illustration 25: Statement of bank reconciliation for 1st December 2016.....................................37

Illustration 26: Trail balance..........................................................................................................39

Illustration 27: Statement of bank reconciliation for 1st December 2016.....................................40

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is an accountancy component for analyzing economic position of

organization by using its tools and making decisions for further years' business operations. In this

regard, summary of all business activities is presented that plays crucial role improving

efficiencies of company. In the present report, several aspects of financial accounting including

tools and methods for decision making are to be introduced. Likewise, rules and regulations for

preparing financial statements and notes can be expressed. Including this, through this

assignment, conventions for consistency and material Closure can be presented that affects

financial accountancy. However, different calculations regarding double entry recording for

preparing ledger and maintaining accounts are to be explained. Besides this, preparing profit and

loss account for Peter Piper and Raintree Ltd for the period ended 31st December 2016 and year

ended 30th September respectively can be illustrated that shows monetary performance of

organizations. Along with this, usefulness of preparing bank statements for Kendal Ltd can be

described here. Similarly, preparation of balance sheet for Henderson Ltd is to be presented that

affects business operations. Thus, it is significant to study the present report that aims to

understand financial accounting terms for different entities.

A) FINANCIAL ACCOUNTING AND ITS DIFFERENT TERMS

1) Financial accounting

Financial accounting is an approach for summarizing, reporting and presenting monetary

performance of any organization. It is considered as key component for measuring economic

structure as well applying different tools for improving efficiencies of business organization.

However, several kinds of financial statements are prepared and recorded by entity just as; profit

and loss account, balance sheet, income statement and so on (Abdul and et.al., 2016). On the

basis of analyzing these statements, further ideas are created to be implement in future time to

achieve effectiveness of organization and enhancing its quality services. Including this, balance

between incurred expenses and gained revenue is presented that shows profitability and profit

earning capacity of company to operate business activities. In this process, different financial

transactions with collaborative are identified emerges varieties of tools for increasing quality

services and managing all financial resources efficiently. However, by analyzing liabilities,

4

Financial accounting is an accountancy component for analyzing economic position of

organization by using its tools and making decisions for further years' business operations. In this

regard, summary of all business activities is presented that plays crucial role improving

efficiencies of company. In the present report, several aspects of financial accounting including

tools and methods for decision making are to be introduced. Likewise, rules and regulations for

preparing financial statements and notes can be expressed. Including this, through this

assignment, conventions for consistency and material Closure can be presented that affects

financial accountancy. However, different calculations regarding double entry recording for

preparing ledger and maintaining accounts are to be explained. Besides this, preparing profit and

loss account for Peter Piper and Raintree Ltd for the period ended 31st December 2016 and year

ended 30th September respectively can be illustrated that shows monetary performance of

organizations. Along with this, usefulness of preparing bank statements for Kendal Ltd can be

described here. Similarly, preparation of balance sheet for Henderson Ltd is to be presented that

affects business operations. Thus, it is significant to study the present report that aims to

understand financial accounting terms for different entities.

A) FINANCIAL ACCOUNTING AND ITS DIFFERENT TERMS

1) Financial accounting

Financial accounting is an approach for summarizing, reporting and presenting monetary

performance of any organization. It is considered as key component for measuring economic

structure as well applying different tools for improving efficiencies of business organization.

However, several kinds of financial statements are prepared and recorded by entity just as; profit

and loss account, balance sheet, income statement and so on (Abdul and et.al., 2016). On the

basis of analyzing these statements, further ideas are created to be implement in future time to

achieve effectiveness of organization and enhancing its quality services. Including this, balance

between incurred expenses and gained revenue is presented that shows profitability and profit

earning capacity of company to operate business activities. In this process, different financial

transactions with collaborative are identified emerges varieties of tools for increasing quality

services and managing all financial resources efficiently. However, by analyzing liabilities,

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

assets, revenue and expenditures for producing and supplementing goods are presented through

these financial records and reports that are effective for proper financial management and

making strong monetary position of entity for future time periodicity.

Thus, financial accounting is composition of various tools and reports that indicates

actual economic position and also generates several ideas for better quality services. There are

some specific rules and regulations followed for preparing and maintaining financial statements

to present organization's economic performance and further making decisions on the basis of its

identification (Aizenman, Chinn and Ito, 2016). However, through financial accounting, different

tools are applied for presenting monetary position to create to prepare and implement strategies

for future implementation and making strong financial performance of entity for long time

period.

2) Regulations regarding financial accounting

Financial accounting is comprised of different tools for identifying monetary position and

following on all provisions for financial accountancy. There are several kinds of rules and

obligations defined for financial accounting to prepare notes and statements. In this regard,

various provisions are determined for accountancy regarding journal, ledger, balance sheet, profit

and loss etc (Anderson, 2016). In this process, various regulatory boards are made that provides

guidelines and provisions for preparing financial statements for recording as well reporting

financial transactions related to business operations. Some regulatory boards are like;

International Financial reporting Council (IFRC), International Accounting Standard Board

(IASB), Accounting Standard Board (ASB), Financial reporting Standard (FRC) and so on. In

such way, these regulations can be understood as below:-

Accounting Standard Board (ASB):- This accounting standard board aims to formulate

accounting standard for preparing and presenting financial statements. However, there are

different provisions and guidance are available for financial records. In this regard,

various accounting functions are also carried out to following on provisions provided

regarding laws, costumes for regulating on financial accountancy. Moreover, by

following on different rules and obligations for financial data related to statements and

taking guidance for reporting more efficiently. In this regard, various tools and

5

these financial records and reports that are effective for proper financial management and

making strong monetary position of entity for future time periodicity.

Thus, financial accounting is composition of various tools and reports that indicates

actual economic position and also generates several ideas for better quality services. There are

some specific rules and regulations followed for preparing and maintaining financial statements

to present organization's economic performance and further making decisions on the basis of its

identification (Aizenman, Chinn and Ito, 2016). However, through financial accounting, different

tools are applied for presenting monetary position to create to prepare and implement strategies

for future implementation and making strong financial performance of entity for long time

period.

2) Regulations regarding financial accounting

Financial accounting is comprised of different tools for identifying monetary position and

following on all provisions for financial accountancy. There are several kinds of rules and

obligations defined for financial accounting to prepare notes and statements. In this regard,

various provisions are determined for accountancy regarding journal, ledger, balance sheet, profit

and loss etc (Anderson, 2016). In this process, various regulatory boards are made that provides

guidelines and provisions for preparing financial statements for recording as well reporting

financial transactions related to business operations. Some regulatory boards are like;

International Financial reporting Council (IFRC), International Accounting Standard Board

(IASB), Accounting Standard Board (ASB), Financial reporting Standard (FRC) and so on. In

such way, these regulations can be understood as below:-

Accounting Standard Board (ASB):- This accounting standard board aims to formulate

accounting standard for preparing and presenting financial statements. However, there are

different provisions and guidance are available for financial records. In this regard,

various accounting functions are also carried out to following on provisions provided

regarding laws, costumes for regulating on financial accountancy. Moreover, by

following on different rules and obligations for financial data related to statements and

taking guidance for reporting more efficiently. In this regard, various tools and

5

applications are applied for following on accounting standard effectively (Barron, Chung

and Yong, 2016).

International Financial reporting Council (IFRC):- It is accounting standard regulator

of UK for promoting effective quality of corporate governance and also relates to foster

investment. Including this, it provides corporate reporting, monitoring, oversight and

managing all accounting standards effectively (Beatty and Liao, 2014). However, IFRC is

comprised of different codes and standard committee, Executives Committee, Conduct

Committee. Moreover, various regulations are provided to be followed on related to

financial statements' preparation and applying disciplinary functions to recognize income

and expenditures for operating business activities.

3) Accounting rules and principles

There are some accounting principles and rules given by GAPP and Financial accounting

Standard Board (FASB) that companies must followed for preparation of there financial

statements or running there organization through legal procedure.(GAPP) improve the clarity of

the communication of financial information and reduce due to loss from financial activity

(Edwards, 2016).

Some basic accounting principles and guidelines:- The GAPP is founded on the basis

accounting principles and rules. They are followed by many organization. Explanation of each

Profitable Entity Assumption:- The accountant of the organization keep all the business

transaction of a sole proprietorship separate from the company's owners. For legal

purpose of the organization and Assumption of probability of the company.

Cost Principle:- from the accountant's point of view, the cost refers to the money invest

on cash or cash equipment. When the product purchase by the company (Evans, 2015).

For this reasons the amount shown on financial statements are referred to as past cost of

purchase of product by organization.

Going concern principle:- this system of rules anticipate that a company to exist long

carry out the vision and objective for increase the profit and company's productivity in

the predictable future (Kapan and Minoiu, 2016).

6

and Yong, 2016).

International Financial reporting Council (IFRC):- It is accounting standard regulator

of UK for promoting effective quality of corporate governance and also relates to foster

investment. Including this, it provides corporate reporting, monitoring, oversight and

managing all accounting standards effectively (Beatty and Liao, 2014). However, IFRC is

comprised of different codes and standard committee, Executives Committee, Conduct

Committee. Moreover, various regulations are provided to be followed on related to

financial statements' preparation and applying disciplinary functions to recognize income

and expenditures for operating business activities.

3) Accounting rules and principles

There are some accounting principles and rules given by GAPP and Financial accounting

Standard Board (FASB) that companies must followed for preparation of there financial

statements or running there organization through legal procedure.(GAPP) improve the clarity of

the communication of financial information and reduce due to loss from financial activity

(Edwards, 2016).

Some basic accounting principles and guidelines:- The GAPP is founded on the basis

accounting principles and rules. They are followed by many organization. Explanation of each

Profitable Entity Assumption:- The accountant of the organization keep all the business

transaction of a sole proprietorship separate from the company's owners. For legal

purpose of the organization and Assumption of probability of the company.

Cost Principle:- from the accountant's point of view, the cost refers to the money invest

on cash or cash equipment. When the product purchase by the company (Evans, 2015).

For this reasons the amount shown on financial statements are referred to as past cost of

purchase of product by organization.

Going concern principle:- this system of rules anticipate that a company to exist long

carry out the vision and objective for increase the profit and company's productivity in

the predictable future (Kapan and Minoiu, 2016).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conservatism:- the basic accounting principles of conservatism leads controller to

evaluate or disclose fiscal loss, but it does not allow a similar action for gains. Controller

are anticipated to be unbiased and objective.

Full Disclosure principles:- If the certain information is important to capitalist or

contributor using the financial statement (Kim, Shi and Zhou, 2014). That message

should be disclosed within the fiscal statement of company or in the notes documents to

the statement.

4) Conventions and concepts related to consistency and material disclosure

Convention of disclosure:-the disclosure of all important information is one of the

important accounting conventions. It is express that accounts should be prepared in such

a manner that all material message is clear disclosed to the reader. The term disclosure

does not express that all the information that anyone could tendency is to include in

accountancy statement (Koo, 2014). the disclosure within the body of financial statement

in meeting of board of directors.

Convention of consistency:- this convention means that accounting process and pattern

should proceed uncharged from one period to another. Consistency does not mean

inflexibility. In other words consistency means is principle that the same administration

accountancy principles should be used for preparing financial statement for various of

time period. It is different accounting process or procedures are used for preparation of

financial statement for organization of different years.

Convention of Materiality:- it is refers to the relative importance of items or even.

According to this convention only some or this component or outcome should recorded.

the materialist concepts is an constituted accountancy convention recognize

comprehensive. Such other convention is the past cost by which organization record

business transaction at the price prevalent at the book of the possession at original cost

(Ledger, 2014). There is not a formula in component a discrimination between material

and immaterial events. Similarly, whole items material in one year may not Be material

in the next year of the financial statement for the organization.

7

evaluate or disclose fiscal loss, but it does not allow a similar action for gains. Controller

are anticipated to be unbiased and objective.

Full Disclosure principles:- If the certain information is important to capitalist or

contributor using the financial statement (Kim, Shi and Zhou, 2014). That message

should be disclosed within the fiscal statement of company or in the notes documents to

the statement.

4) Conventions and concepts related to consistency and material disclosure

Convention of disclosure:-the disclosure of all important information is one of the

important accounting conventions. It is express that accounts should be prepared in such

a manner that all material message is clear disclosed to the reader. The term disclosure

does not express that all the information that anyone could tendency is to include in

accountancy statement (Koo, 2014). the disclosure within the body of financial statement

in meeting of board of directors.

Convention of consistency:- this convention means that accounting process and pattern

should proceed uncharged from one period to another. Consistency does not mean

inflexibility. In other words consistency means is principle that the same administration

accountancy principles should be used for preparing financial statement for various of

time period. It is different accounting process or procedures are used for preparation of

financial statement for organization of different years.

Convention of Materiality:- it is refers to the relative importance of items or even.

According to this convention only some or this component or outcome should recorded.

the materialist concepts is an constituted accountancy convention recognize

comprehensive. Such other convention is the past cost by which organization record

business transaction at the price prevalent at the book of the possession at original cost

(Ledger, 2014). There is not a formula in component a discrimination between material

and immaterial events. Similarly, whole items material in one year may not Be material

in the next year of the financial statement for the organization.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

B) ACCOUNTING FOR DIFFERENT FIRMS

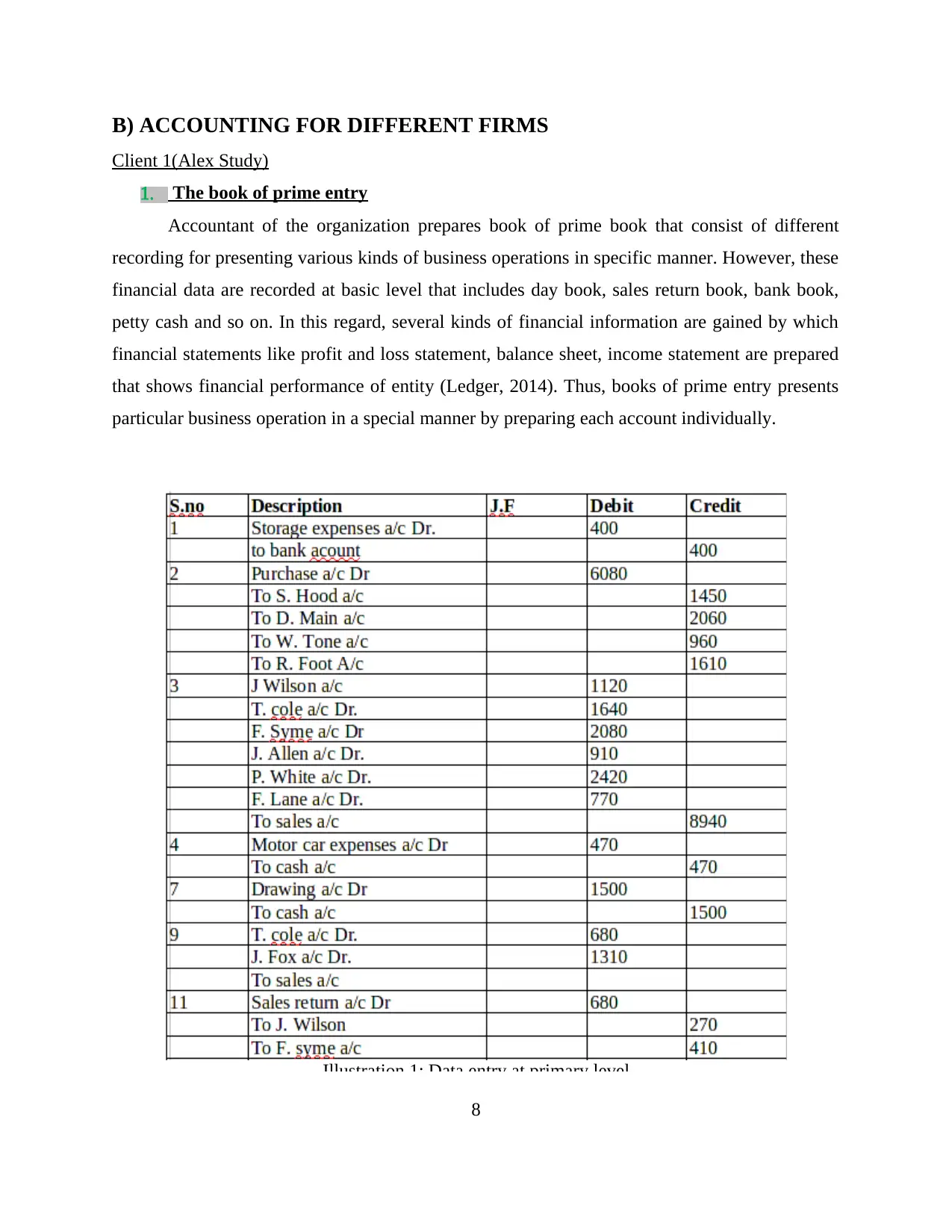

Client 1(Alex Study)

1. The book of prime entry

Accountant of the organization prepares book of prime book that consist of different

recording for presenting various kinds of business operations in specific manner. However, these

financial data are recorded at basic level that includes day book, sales return book, bank book,

petty cash and so on. In this regard, several kinds of financial information are gained by which

financial statements like profit and loss statement, balance sheet, income statement are prepared

that shows financial performance of entity (Ledger, 2014). Thus, books of prime entry presents

particular business operation in a special manner by preparing each account individually.

8

Illustration 1: Data entry at primary level

Client 1(Alex Study)

1. The book of prime entry

Accountant of the organization prepares book of prime book that consist of different

recording for presenting various kinds of business operations in specific manner. However, these

financial data are recorded at basic level that includes day book, sales return book, bank book,

petty cash and so on. In this regard, several kinds of financial information are gained by which

financial statements like profit and loss statement, balance sheet, income statement are prepared

that shows financial performance of entity (Ledger, 2014). Thus, books of prime entry presents

particular business operation in a special manner by preparing each account individually.

8

Illustration 1: Data entry at primary level

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

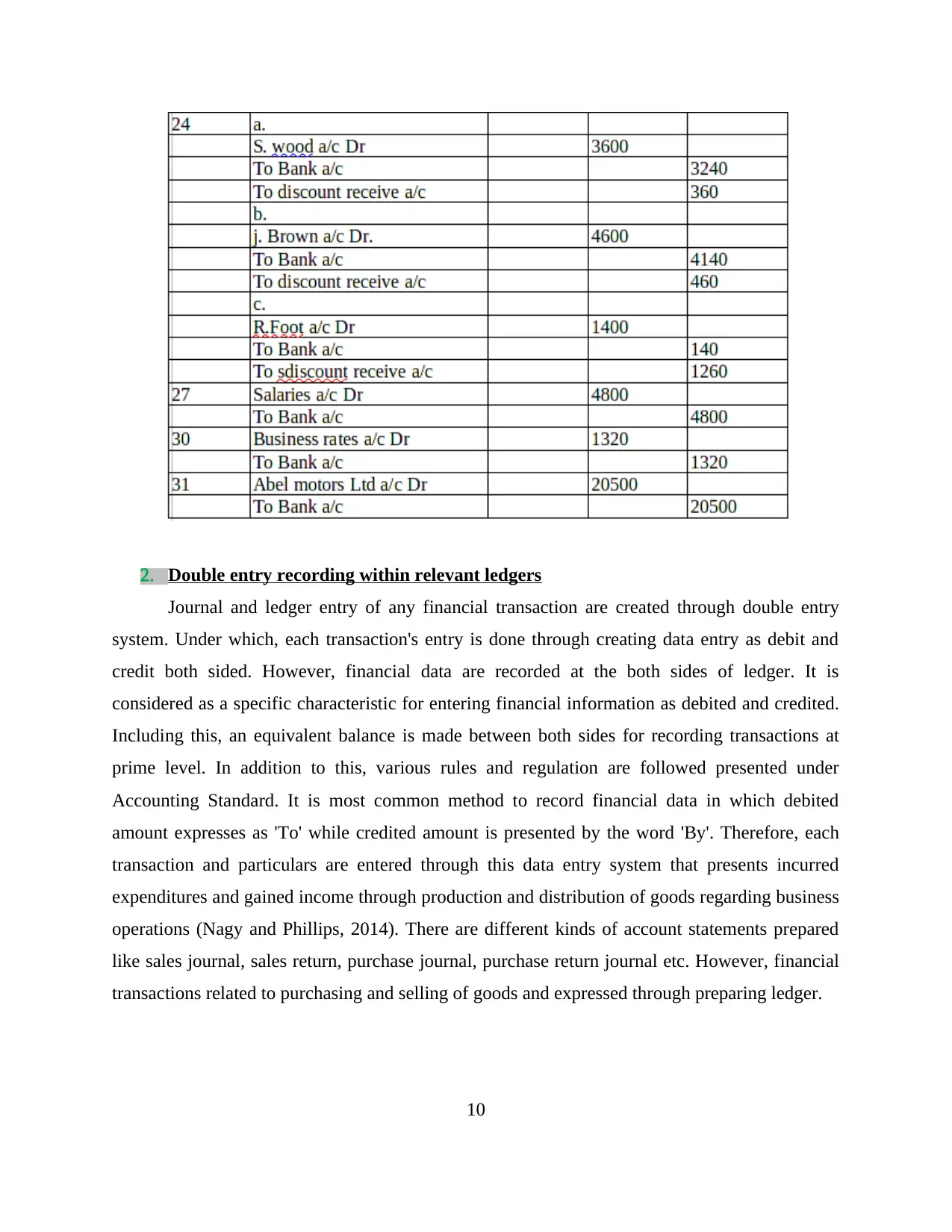

2. Double entry recording within relevant ledgers

Journal and ledger entry of any financial transaction are created through double entry

system. Under which, each transaction's entry is done through creating data entry as debit and

credit both sided. However, financial data are recorded at the both sides of ledger. It is

considered as a specific characteristic for entering financial information as debited and credited.

Including this, an equivalent balance is made between both sides for recording transactions at

prime level. In addition to this, various rules and regulation are followed presented under

Accounting Standard. It is most common method to record financial data in which debited

amount expresses as 'To' while credited amount is presented by the word 'By'. Therefore, each

transaction and particulars are entered through this data entry system that presents incurred

expenditures and gained income through production and distribution of goods regarding business

operations (Nagy and Phillips, 2014). There are different kinds of account statements prepared

like sales journal, sales return, purchase journal, purchase return journal etc. However, financial

transactions related to purchasing and selling of goods and expressed through preparing ledger.

10

Journal and ledger entry of any financial transaction are created through double entry

system. Under which, each transaction's entry is done through creating data entry as debit and

credit both sided. However, financial data are recorded at the both sides of ledger. It is

considered as a specific characteristic for entering financial information as debited and credited.

Including this, an equivalent balance is made between both sides for recording transactions at

prime level. In addition to this, various rules and regulation are followed presented under

Accounting Standard. It is most common method to record financial data in which debited

amount expresses as 'To' while credited amount is presented by the word 'By'. Therefore, each

transaction and particulars are entered through this data entry system that presents incurred

expenditures and gained income through production and distribution of goods regarding business

operations (Nagy and Phillips, 2014). There are different kinds of account statements prepared

like sales journal, sales return, purchase journal, purchase return journal etc. However, financial

transactions related to purchasing and selling of goods and expressed through preparing ledger.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

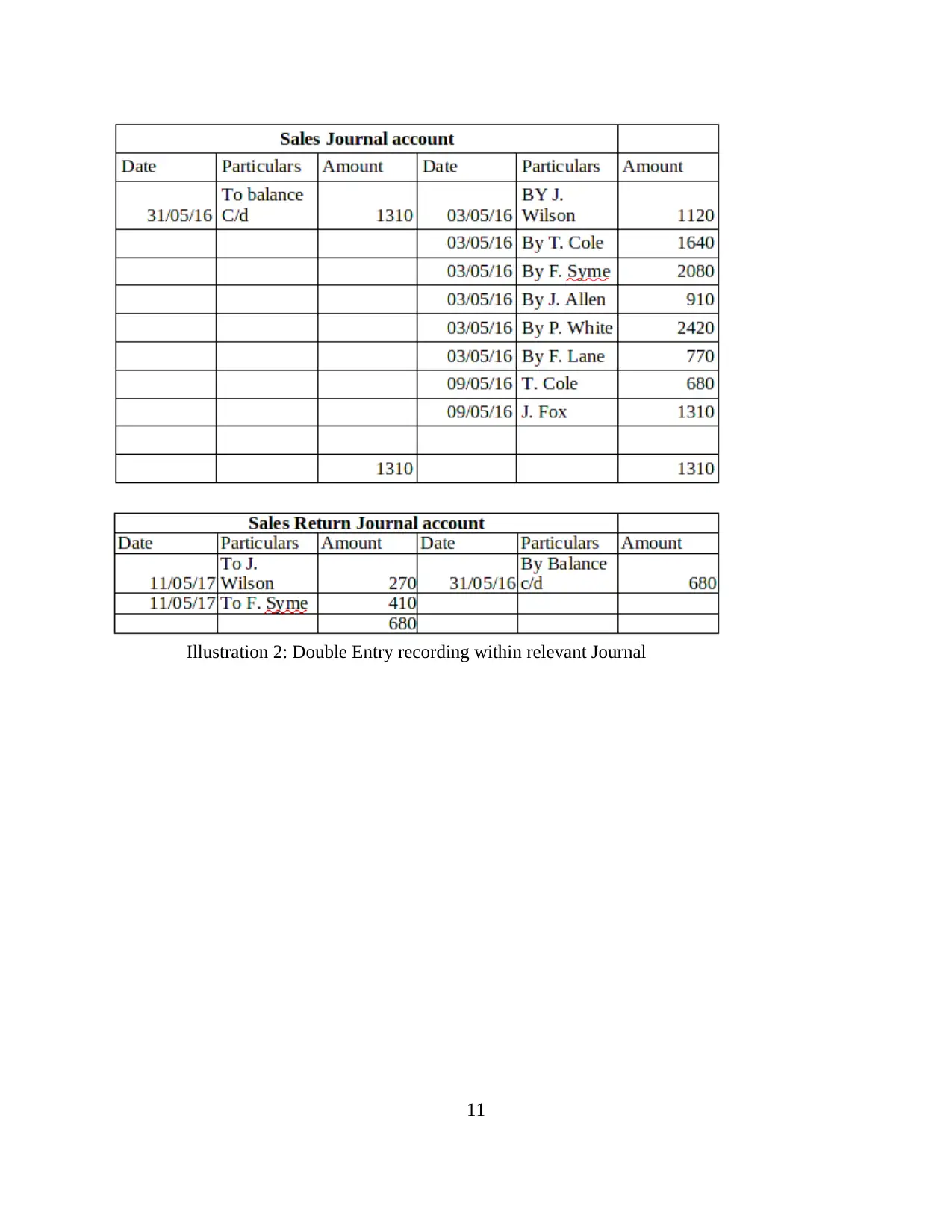

Illustration 2: Double Entry recording within relevant Journal

11

11

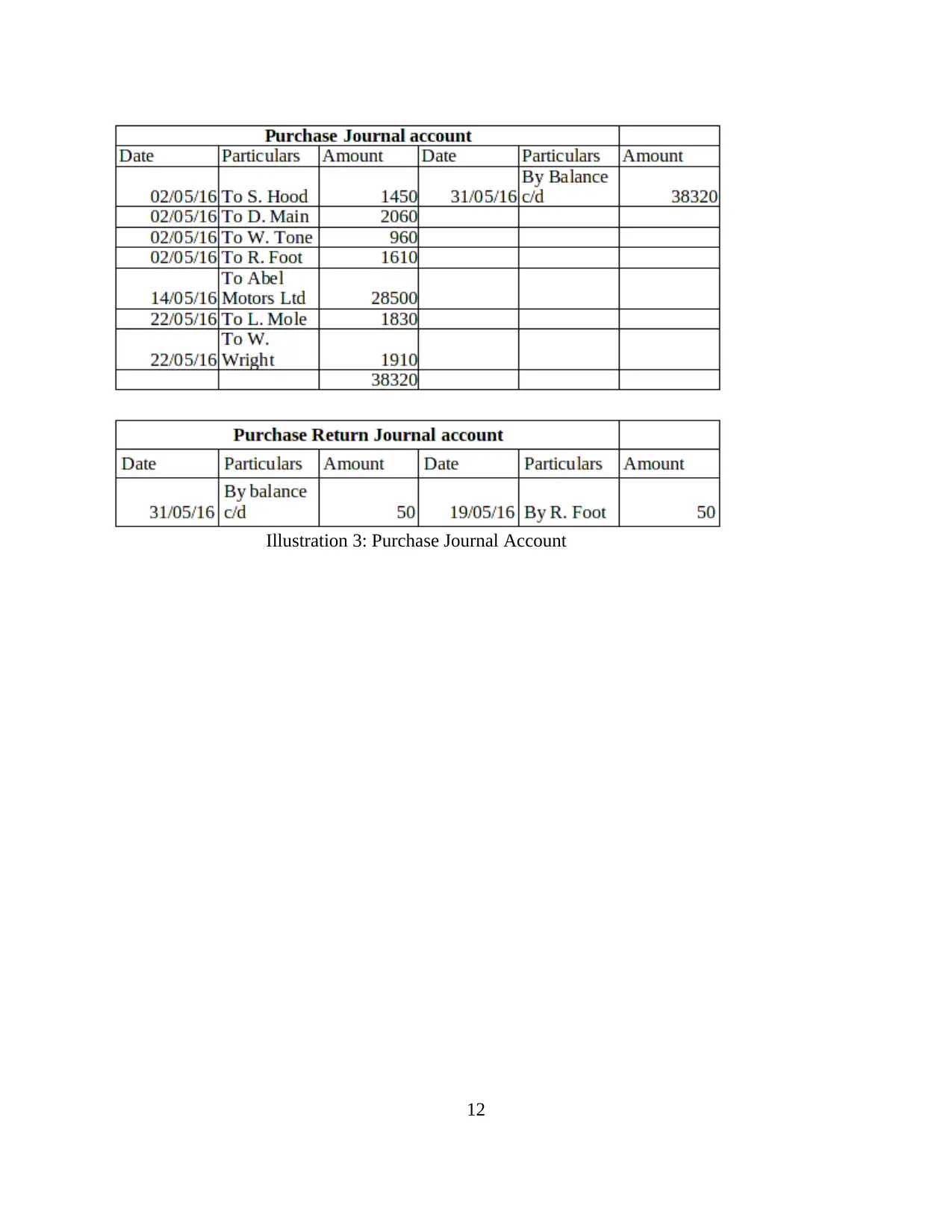

Illustration 3: Purchase Journal Account

12

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 43

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.