Financial Accounting Report: Financial Analysis for Decision Making

VerifiedAdded on 2023/01/13

|9

|1848

|91

Report

AI Summary

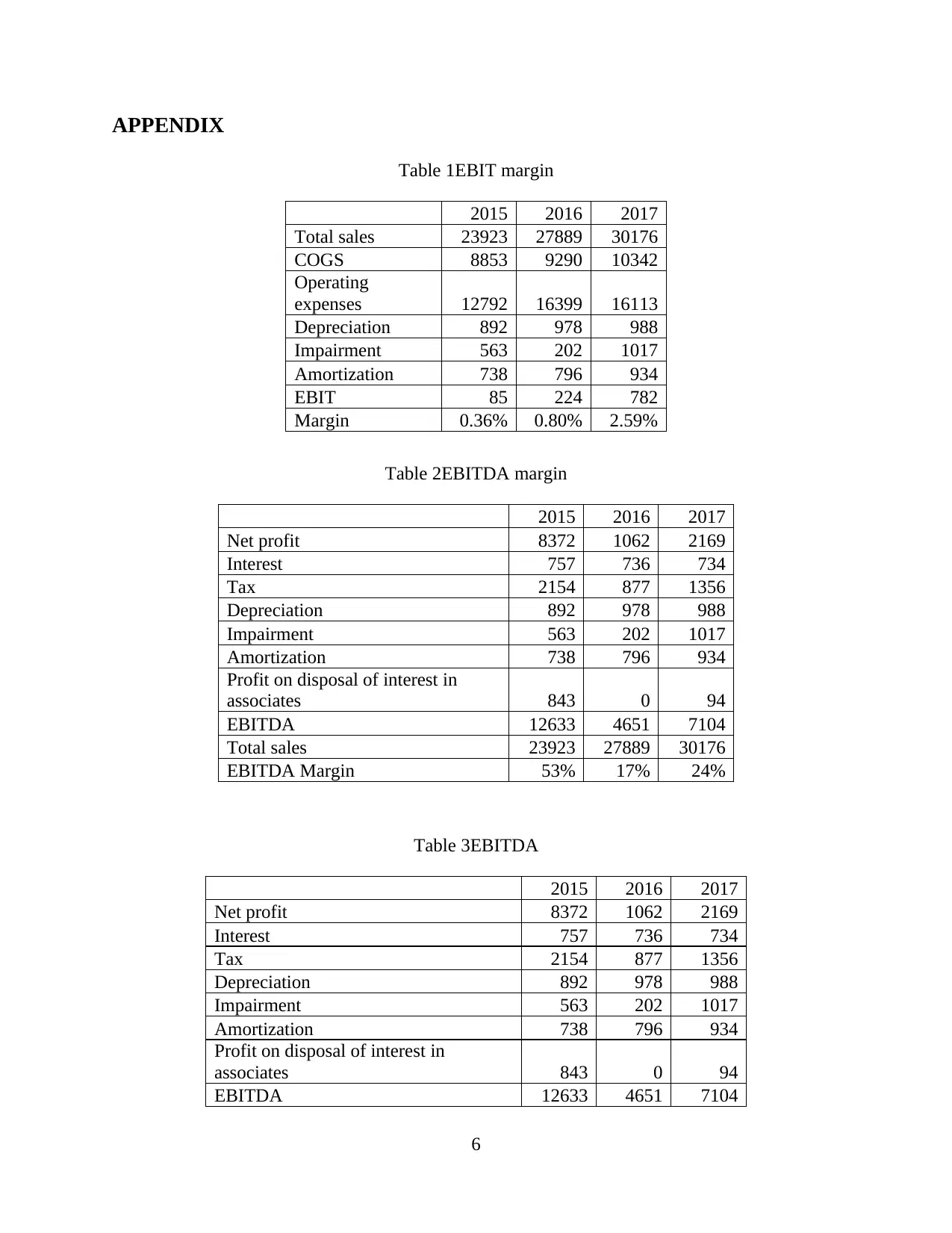

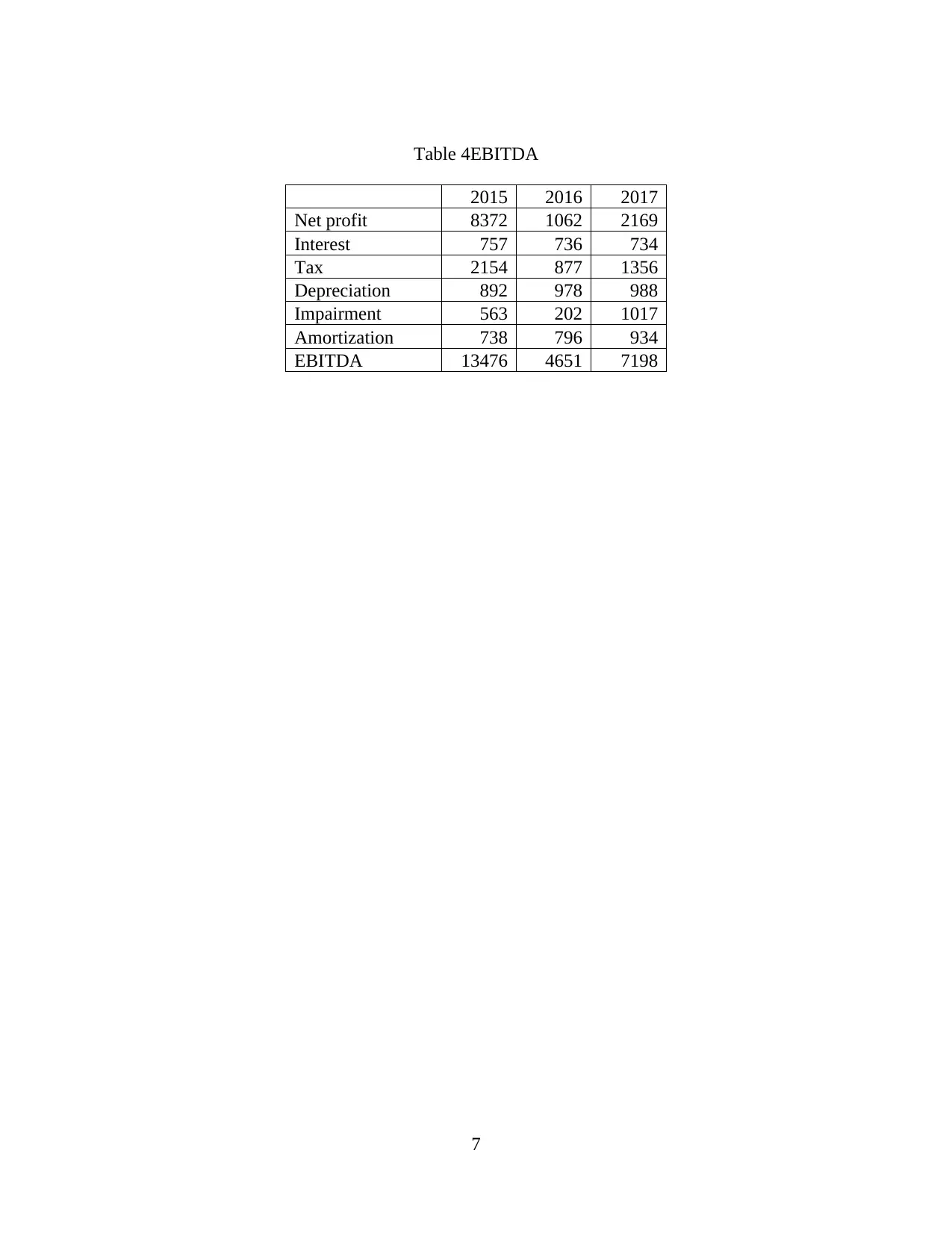

This report, prepared as part of a financial accounting assignment, analyzes the financial statements of Glaxo Smithkline PLC (GSK PLC) to assess its financial performance. The report focuses on the calculation and interpretation of Earnings Before Interest and Taxes (EBIT) and Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) margins, highlighting their usefulness in financial analysis and decision-making. The analysis includes a comparison of EBIT and EBITDA figures over multiple years, offering insights into the company's operating earnings and investment returns. Furthermore, the report explores the criteria for revenue recognition, referencing International Financial Reporting Standard 15, and the systematic application of depreciation in asset valuation. The conclusion emphasizes the importance of EBIT and EBITDA as key metrics for investors, providing a more accurate view of a company's production performance. The report is designed for a business analyst role, aiding in investment evaluations.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.