Financial Analysis and Management Accounting Report: Unit 5

VerifiedAdded on 2020/09/17

|18

|5254

|106

Report

AI Summary

This report provides a comprehensive analysis of management accounting, focusing on its crucial role in decision-making for Vectair Holdings Ltd, a manufacturing company. It delves into the essential requirements of various types of management accounting, including cost accounting, price optimization, job costing, and inventory management, highlighting their benefits in strengthening internal control and fostering growth. The report enumerates various methods for management accounting reporting, such as segmental reports, performance reports, inventory management reports, accounts receivables ageing reports, job cost reports, and operational budget reports. Furthermore, the report includes a practical application of marginal and absorption costing through income statements and provides insights into planning tools and management accounting systems to respond to financial problems. The report emphasizes the significance of management accounting in achieving organizational goals and responding effectively to financial challenges. It is a detailed exploration of management accounting principles and their practical application in a business context.

UNIT 5 MAN ACC

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirement of various kinds of management

accounting...............................................................................................................................1

P2 Enumerating various methods for management accounting reporting..............................3

TASK 2............................................................................................................................................6

P 3 Computation of marginal and absorption costing............................................................6

TASK 3............................................................................................................................................9

P4 Discuss kinds of planning tools.........................................................................................9

P 5 Management accounting system to respond to financial problems................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirement of various kinds of management

accounting...............................................................................................................................1

P2 Enumerating various methods for management accounting reporting..............................3

TASK 2............................................................................................................................................6

P 3 Computation of marginal and absorption costing............................................................6

TASK 3............................................................................................................................................9

P4 Discuss kinds of planning tools.........................................................................................9

P 5 Management accounting system to respond to financial problems................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is crucial branch of accounting helping management to take

better and effective decisions for strengthening organisation internally. The present report deals

with Vectair Holdings Ltd which is engaged in the manufacturing sector. The report highlights

importance of management accounting information which are used by the management to arrive

at concrete results. Moreover, various types of such accounting is discussed and managerial

reports are discussed as well. Various planning tools are discussed which help company to make

decision whether to invest in new project or not and helpful to check its viability. In relation to

this, marginal and absorption costing is also enumerated in the report. Furthermore, management

accounting system help in responding to financial problems and thus, it plays significant role in

the company to achieve common targets in the best possible way.

TASK 1

P1 Management accounting and essential requirement of various kinds of management

accounting

Management accounting is an effective decision making tool which helps management to

take enhanced decisions for the betterment of the company. It is quite useful tool which adds

value to organisation. The management takes this information for making effective internal

decisions for the betterment of the firm. The management accounting information is provided to

managers only and as such, it is not imparted to various stakeholders'. By analysing information,

management comes to know the progress of the company and as a result, if any deviations exist

then in consideration of the same, decisions are taken so that overall productivity may be

enhanced quite effectively. Vectair Holdings also uses management accounting information for

strengthening internal control and initiating healthy growth of the company (Chenhall and

Moers, 2015).

Management accounting is also termed as cost accounting as it controls various expenses

which help to achieve production in the best possible way. Timely reports are prepared and

which is handover to the management to analyse situation and then take decision thereon. The

main essence of management accounting information is that it blends or combines financial

information with non-financial one and then produce picture of the company. This helps Vectair

Holdings to take effective decisions for the betterment of it. Thus, it can be said that management

1

Management accounting is crucial branch of accounting helping management to take

better and effective decisions for strengthening organisation internally. The present report deals

with Vectair Holdings Ltd which is engaged in the manufacturing sector. The report highlights

importance of management accounting information which are used by the management to arrive

at concrete results. Moreover, various types of such accounting is discussed and managerial

reports are discussed as well. Various planning tools are discussed which help company to make

decision whether to invest in new project or not and helpful to check its viability. In relation to

this, marginal and absorption costing is also enumerated in the report. Furthermore, management

accounting system help in responding to financial problems and thus, it plays significant role in

the company to achieve common targets in the best possible way.

TASK 1

P1 Management accounting and essential requirement of various kinds of management

accounting

Management accounting is an effective decision making tool which helps management to

take enhanced decisions for the betterment of the company. It is quite useful tool which adds

value to organisation. The management takes this information for making effective internal

decisions for the betterment of the firm. The management accounting information is provided to

managers only and as such, it is not imparted to various stakeholders'. By analysing information,

management comes to know the progress of the company and as a result, if any deviations exist

then in consideration of the same, decisions are taken so that overall productivity may be

enhanced quite effectively. Vectair Holdings also uses management accounting information for

strengthening internal control and initiating healthy growth of the company (Chenhall and

Moers, 2015).

Management accounting is also termed as cost accounting as it controls various expenses

which help to achieve production in the best possible way. Timely reports are prepared and

which is handover to the management to analyse situation and then take decision thereon. The

main essence of management accounting information is that it blends or combines financial

information with non-financial one and then produce picture of the company. This helps Vectair

Holdings to take effective decisions for the betterment of it. Thus, it can be said that management

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accounting is required in the organisation to take enhanced decisions with much ease. In addition

to this, various types of management accounting and essential requirements of them are

described below-

Cost accounting:

Cost accounting is the main type of management accounting as it imparts effective

information to the manager for better decisions. Vectair Holdings Company is quite enhanced by

implementing cost accounting system to control costs in effectual way (Renz and Herman,

2016). As the name suggests, cost accounting helps to reduce and control various expenses in the

organisation so that production can be achieved with much ease. Various costs such as direct,

indirect, fixed and variable costs are analysed and consecutively reduced so that expenditures

may not exceed profit in any way. Thus, this branch of management accounting is essentially

required in the organisation so that costs can be effectively controlled in the best possible

manner.

Price optimisation:

Customer's behaviour should be analysed by the company so that prices can be easily set

by the organisation. To overcome this problem, management accounting type i.e. price

optimisation is used to generate effective results. This technique is a termed as a mathematical

analysis which is carried out to determine how consumer reacts to price quoted by the company.

In simple words, management analyses how customers respond to price set by the organisation

of a particular product. This helps Vectair Holdings Ltd to take effective decisions regarding

price of the product and thus, it quotes that price on which consumers are ready to purchase it

without any hesitation. It is quite essentially required in the company so that decisions regarding

prices of the products can be easily achieved with much ease (Otley, 2016).

Job costing:

Job costing is effective tool basically for small organisation. As such, it is quite useful for

Vectair Holdings to control costs on various jobs performed in the production site. Job costing is

quite helpful in firm so that expenses incurred on various jobs can be easily controlled and

reduced to get results in terms of more profits. It is combination of various costs such as

materials, labour and overhead which are incurred on a particular job. Thus, job costing is

2

to this, various types of management accounting and essential requirements of them are

described below-

Cost accounting:

Cost accounting is the main type of management accounting as it imparts effective

information to the manager for better decisions. Vectair Holdings Company is quite enhanced by

implementing cost accounting system to control costs in effectual way (Renz and Herman,

2016). As the name suggests, cost accounting helps to reduce and control various expenses in the

organisation so that production can be achieved with much ease. Various costs such as direct,

indirect, fixed and variable costs are analysed and consecutively reduced so that expenditures

may not exceed profit in any way. Thus, this branch of management accounting is essentially

required in the organisation so that costs can be effectively controlled in the best possible

manner.

Price optimisation:

Customer's behaviour should be analysed by the company so that prices can be easily set

by the organisation. To overcome this problem, management accounting type i.e. price

optimisation is used to generate effective results. This technique is a termed as a mathematical

analysis which is carried out to determine how consumer reacts to price quoted by the company.

In simple words, management analyses how customers respond to price set by the organisation

of a particular product. This helps Vectair Holdings Ltd to take effective decisions regarding

price of the product and thus, it quotes that price on which consumers are ready to purchase it

without any hesitation. It is quite essentially required in the company so that decisions regarding

prices of the products can be easily achieved with much ease (Otley, 2016).

Job costing:

Job costing is effective tool basically for small organisation. As such, it is quite useful for

Vectair Holdings to control costs on various jobs performed in the production site. Job costing is

quite helpful in firm so that expenses incurred on various jobs can be easily controlled and

reduced to get results in terms of more profits. It is combination of various costs such as

materials, labour and overhead which are incurred on a particular job. Thus, job costing is

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

essentially required in small organisation and large one as well so that effective results can be

drawn and expenditures on jobs can be reduced with much ease. Cost accountant manages and

keeps track of each costs and as such, it is provided to management for better and effectual

decisions in the best possible way.

Inventory management:

Inventory management is quite effective technique so that stock can be effectually

managed in the organisation. Stocks are required for the production purpose and as such,

adequate quantity is required to be maintained so that overall production may be met with much

ease. As such, inventory management helps to control inventory in respect to placing order,

storage of the same, holding costs (Cooper, Ezzamel and Qu, 2017). These aspects are important

in managing inventory so that goods can be easily produced and as such, company can meet

demand of customers in the best possible way. Managing inventory is required so that adequate

quantity can be purchased and provided to customers. If more quantity is ordered then it leads to

unnecessary spoilage of the inventory which should not be done by the company as it results into

incurring of additional cost for handling such inventory. As such, Vectair Holdings should

effectively manage inventory so that orders can be easily fulfilled and costs can be reduced as

well.

Providing benefits of management accounting system in the company

The management accounting system is quite useful for the top management to take

effective and better decisions which are suitable for strengthening internal control in the

organisation. The managerial reports also provide effective information to the management and

as such, management accounting is quite beneficial to firm. Costs are controlled in a better way

and as such, revenue is generated by the company. Moreover, efficient handling of inventory is

also observed and as a result, proper control is initiated quite effectually. Thus, it can be said that

management accounting system is crucial tool for organisation (Tappura and et.al, 2015).

P2 Enumerating various methods for management accounting reporting

1. Segmental report:

Segmental reporting is quite essential tool in the organisation as it provides information

related to operational segments of the company. As such, it is presented with the financial

3

drawn and expenditures on jobs can be reduced with much ease. Cost accountant manages and

keeps track of each costs and as such, it is provided to management for better and effectual

decisions in the best possible way.

Inventory management:

Inventory management is quite effective technique so that stock can be effectually

managed in the organisation. Stocks are required for the production purpose and as such,

adequate quantity is required to be maintained so that overall production may be met with much

ease. As such, inventory management helps to control inventory in respect to placing order,

storage of the same, holding costs (Cooper, Ezzamel and Qu, 2017). These aspects are important

in managing inventory so that goods can be easily produced and as such, company can meet

demand of customers in the best possible way. Managing inventory is required so that adequate

quantity can be purchased and provided to customers. If more quantity is ordered then it leads to

unnecessary spoilage of the inventory which should not be done by the company as it results into

incurring of additional cost for handling such inventory. As such, Vectair Holdings should

effectively manage inventory so that orders can be easily fulfilled and costs can be reduced as

well.

Providing benefits of management accounting system in the company

The management accounting system is quite useful for the top management to take

effective and better decisions which are suitable for strengthening internal control in the

organisation. The managerial reports also provide effective information to the management and

as such, management accounting is quite beneficial to firm. Costs are controlled in a better way

and as such, revenue is generated by the company. Moreover, efficient handling of inventory is

also observed and as a result, proper control is initiated quite effectually. Thus, it can be said that

management accounting system is crucial tool for organisation (Tappura and et.al, 2015).

P2 Enumerating various methods for management accounting reporting

1. Segmental report:

Segmental reporting is quite essential tool in the organisation as it provides information

related to operational segments of the company. As such, it is presented with the financial

3

statements of the business entity. Segmental reports are also prepared by Vectair Holdings as it

helps to provide effective information to various stakeholders' to take enhanced decisions with

much ease. This is quite useful piece of information which is provided to creditors and investors

to take effective information with regards to imparting funds to organisation. Thus, they may be

able to assess solvency and profitability of organisation and as such, decisions may be made

whether to provide funds to firm or not. Thus, segmental reports are quite effective method of

management accountant reporting and are available to public companies and not to private firms

(Chiarini and Vagnoni, 2015).

2. Performance report:

Performance report is prepared for measuring performance of something. Mainly report is

prepared to determine performance of employees so that there productivity can be easily

checked. The main essence of this report is that workers' performance is analysed and as such,

decisions are taken by the management if performance is not adequate and how it can be

enhanced so that overall productivity can be enhanced in the best possible way. This is an

effectual method to assess performance and productivity of employees can be attained by taking

effective steps to overcome weaknesses if any. Thus, performance report helps to attain desired

level of production by Vectair Holdings so that profits may be achieved with much ease.

3. Inventory management report:

Inventory management report is another effective tool for purchasing adequate quantity

of stocks in the best possible way. This report help to management about the quantum of

inventory required by the production department so that goods may be easily produced. Vectair

Holdings manages various orders which are received from customers on daily basis and as such,

inventory is required for achieving production with much ease (Hopper and Bui, 2016). Thus,

management is imparted with inventory management report which lists down amount of

inventory held by the production department and how much more is needed to accomplish

production as well. This helps management to analyse report and thus, places order for meeting

demand of the production department. This helps to reduce wastage of the stocks as management

place orders only which is required by the department. This eventually helps to minimise

inventory and as such, production is achieved with much ease.

4

helps to provide effective information to various stakeholders' to take enhanced decisions with

much ease. This is quite useful piece of information which is provided to creditors and investors

to take effective information with regards to imparting funds to organisation. Thus, they may be

able to assess solvency and profitability of organisation and as such, decisions may be made

whether to provide funds to firm or not. Thus, segmental reports are quite effective method of

management accountant reporting and are available to public companies and not to private firms

(Chiarini and Vagnoni, 2015).

2. Performance report:

Performance report is prepared for measuring performance of something. Mainly report is

prepared to determine performance of employees so that there productivity can be easily

checked. The main essence of this report is that workers' performance is analysed and as such,

decisions are taken by the management if performance is not adequate and how it can be

enhanced so that overall productivity can be enhanced in the best possible way. This is an

effectual method to assess performance and productivity of employees can be attained by taking

effective steps to overcome weaknesses if any. Thus, performance report helps to attain desired

level of production by Vectair Holdings so that profits may be achieved with much ease.

3. Inventory management report:

Inventory management report is another effective tool for purchasing adequate quantity

of stocks in the best possible way. This report help to management about the quantum of

inventory required by the production department so that goods may be easily produced. Vectair

Holdings manages various orders which are received from customers on daily basis and as such,

inventory is required for achieving production with much ease (Hopper and Bui, 2016). Thus,

management is imparted with inventory management report which lists down amount of

inventory held by the production department and how much more is needed to accomplish

production as well. This helps management to analyse report and thus, places order for meeting

demand of the production department. This helps to reduce wastage of the stocks as management

place orders only which is required by the department. This eventually helps to minimise

inventory and as such, production is achieved with much ease.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Accounts receivables ageing report:

This report is quite useful tool for organisation as it helps to recover outstanding dues

from the credit customers. Vectair Holdings should effectively utilise accounts receivables

ageing report so that it may analyse outstanding amount from customers who have purchased

goods on credit basis. This report is quite useful so that customers can be contacted for paying

out amount (Wouters and Kirchberger, 2015). Usually, this report is provided to the management

to analyse unpaid customers invoices and as such, management takes steps so that overdue

payment can be made by them. If more credit is outstanding, then management should formulate

strict credit policies so that consumers may pay amount within stipulated time frame.

5. Job cost report:

Job costing report is effective method of management accounting reports which is helps

in controlling costs which are incurred on various jobs. This report is mainly useful in the

manufacturing sector as it involves various costs such as material, labour and overhead which is

assigned to specific job. This helps company to analyse and assess expenditures incurred on

various jobs and as such, effective steps are being taken for controlling costs in the best possible

way. Thus, expenditures are effectively controlled and organisation can achieve desired

production with much ease (Vigorito, 2016). As such, output is achieved and costs are cut down

up to high extent. This helps company to accomplish production by reducing expenditures and

achieving more production with much ease.

6. Operational budget report:

This report is quite effective tool for analysing how money is spent on various

operational activities in the organisation. Thus, operational budget report is the accumulation of

various costs and expenditures, future costs and forecasting of income as well. This is quite

important report as operational activities are analysed and then decisions are taken so that

organisation can easily achieve profits quite effectually. Operational budget report is prepared in

advance and provided to the management so that prediction of expenditures and revenues may be

easily completed. Thus, management is able to analyse revenue and expenses and then take

suitable action so that operational tasks can be carried without any difficulty.

5

This report is quite useful tool for organisation as it helps to recover outstanding dues

from the credit customers. Vectair Holdings should effectively utilise accounts receivables

ageing report so that it may analyse outstanding amount from customers who have purchased

goods on credit basis. This report is quite useful so that customers can be contacted for paying

out amount (Wouters and Kirchberger, 2015). Usually, this report is provided to the management

to analyse unpaid customers invoices and as such, management takes steps so that overdue

payment can be made by them. If more credit is outstanding, then management should formulate

strict credit policies so that consumers may pay amount within stipulated time frame.

5. Job cost report:

Job costing report is effective method of management accounting reports which is helps

in controlling costs which are incurred on various jobs. This report is mainly useful in the

manufacturing sector as it involves various costs such as material, labour and overhead which is

assigned to specific job. This helps company to analyse and assess expenditures incurred on

various jobs and as such, effective steps are being taken for controlling costs in the best possible

way. Thus, expenditures are effectively controlled and organisation can achieve desired

production with much ease (Vigorito, 2016). As such, output is achieved and costs are cut down

up to high extent. This helps company to accomplish production by reducing expenditures and

achieving more production with much ease.

6. Operational budget report:

This report is quite effective tool for analysing how money is spent on various

operational activities in the organisation. Thus, operational budget report is the accumulation of

various costs and expenditures, future costs and forecasting of income as well. This is quite

important report as operational activities are analysed and then decisions are taken so that

organisation can easily achieve profits quite effectually. Operational budget report is prepared in

advance and provided to the management so that prediction of expenditures and revenues may be

easily completed. Thus, management is able to analyse revenue and expenses and then take

suitable action so that operational tasks can be carried without any difficulty.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

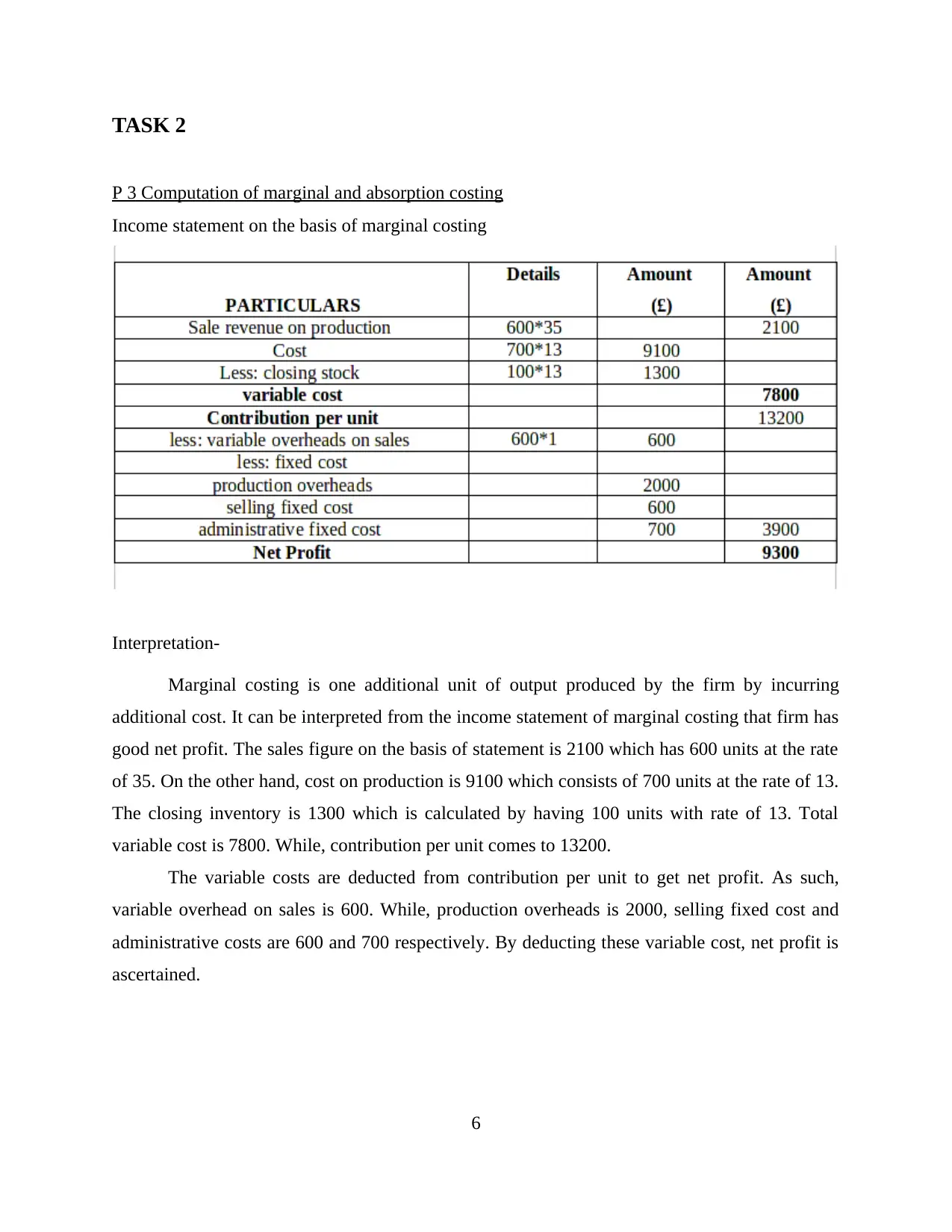

P 3 Computation of marginal and absorption costing

Income statement on the basis of marginal costing

Interpretation-

Marginal costing is one additional unit of output produced by the firm by incurring

additional cost. It can be interpreted from the income statement of marginal costing that firm has

good net profit. The sales figure on the basis of statement is 2100 which has 600 units at the rate

of 35. On the other hand, cost on production is 9100 which consists of 700 units at the rate of 13.

The closing inventory is 1300 which is calculated by having 100 units with rate of 13. Total

variable cost is 7800. While, contribution per unit comes to 13200.

The variable costs are deducted from contribution per unit to get net profit. As such,

variable overhead on sales is 600. While, production overheads is 2000, selling fixed cost and

administrative costs are 600 and 700 respectively. By deducting these variable cost, net profit is

ascertained.

6

P 3 Computation of marginal and absorption costing

Income statement on the basis of marginal costing

Interpretation-

Marginal costing is one additional unit of output produced by the firm by incurring

additional cost. It can be interpreted from the income statement of marginal costing that firm has

good net profit. The sales figure on the basis of statement is 2100 which has 600 units at the rate

of 35. On the other hand, cost on production is 9100 which consists of 700 units at the rate of 13.

The closing inventory is 1300 which is calculated by having 100 units with rate of 13. Total

variable cost is 7800. While, contribution per unit comes to 13200.

The variable costs are deducted from contribution per unit to get net profit. As such,

variable overhead on sales is 600. While, production overheads is 2000, selling fixed cost and

administrative costs are 600 and 700 respectively. By deducting these variable cost, net profit is

ascertained.

6

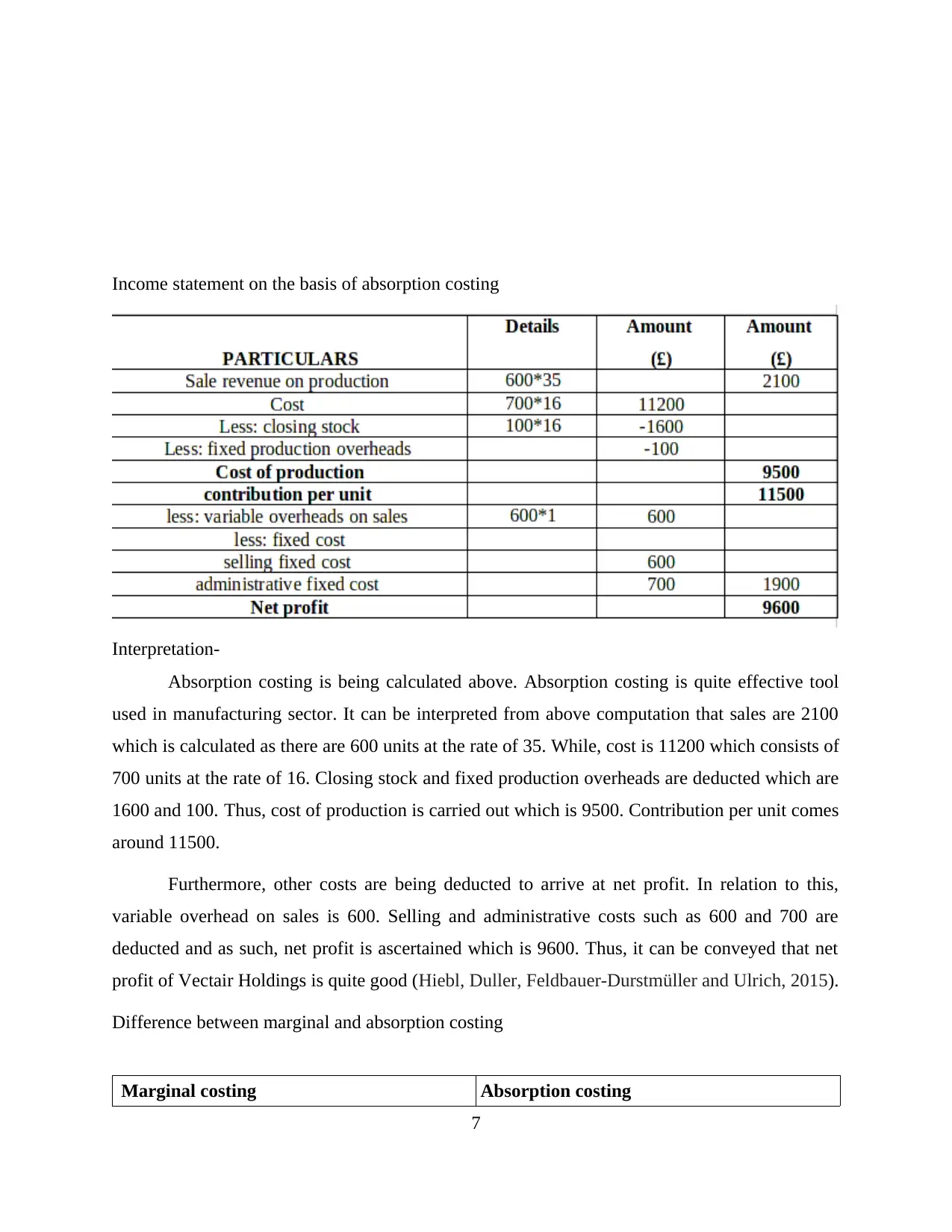

Income statement on the basis of absorption costing

Interpretation-

Absorption costing is being calculated above. Absorption costing is quite effective tool

used in manufacturing sector. It can be interpreted from above computation that sales are 2100

which is calculated as there are 600 units at the rate of 35. While, cost is 11200 which consists of

700 units at the rate of 16. Closing stock and fixed production overheads are deducted which are

1600 and 100. Thus, cost of production is carried out which is 9500. Contribution per unit comes

around 11500.

Furthermore, other costs are being deducted to arrive at net profit. In relation to this,

variable overhead on sales is 600. Selling and administrative costs such as 600 and 700 are

deducted and as such, net profit is ascertained which is 9600. Thus, it can be conveyed that net

profit of Vectair Holdings is quite good (Hiebl, Duller, Feldbauer-Durstmüller and Ulrich, 2015).

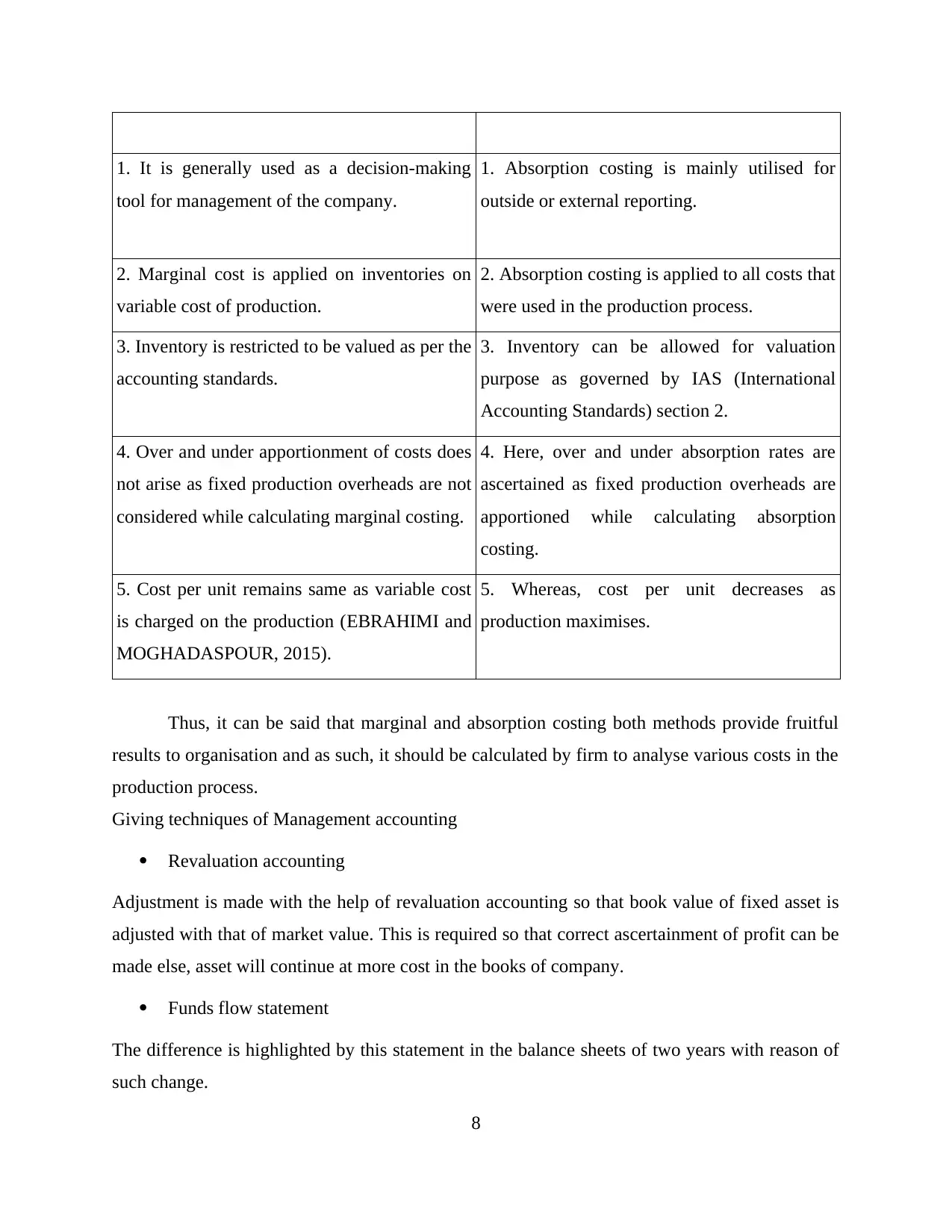

Difference between marginal and absorption costing

Marginal costing Absorption costing

7

Interpretation-

Absorption costing is being calculated above. Absorption costing is quite effective tool

used in manufacturing sector. It can be interpreted from above computation that sales are 2100

which is calculated as there are 600 units at the rate of 35. While, cost is 11200 which consists of

700 units at the rate of 16. Closing stock and fixed production overheads are deducted which are

1600 and 100. Thus, cost of production is carried out which is 9500. Contribution per unit comes

around 11500.

Furthermore, other costs are being deducted to arrive at net profit. In relation to this,

variable overhead on sales is 600. Selling and administrative costs such as 600 and 700 are

deducted and as such, net profit is ascertained which is 9600. Thus, it can be conveyed that net

profit of Vectair Holdings is quite good (Hiebl, Duller, Feldbauer-Durstmüller and Ulrich, 2015).

Difference between marginal and absorption costing

Marginal costing Absorption costing

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. It is generally used as a decision-making

tool for management of the company.

1. Absorption costing is mainly utilised for

outside or external reporting.

2. Marginal cost is applied on inventories on

variable cost of production.

2. Absorption costing is applied to all costs that

were used in the production process.

3. Inventory is restricted to be valued as per the

accounting standards.

3. Inventory can be allowed for valuation

purpose as governed by IAS (International

Accounting Standards) section 2.

4. Over and under apportionment of costs does

not arise as fixed production overheads are not

considered while calculating marginal costing.

4. Here, over and under absorption rates are

ascertained as fixed production overheads are

apportioned while calculating absorption

costing.

5. Cost per unit remains same as variable cost

is charged on the production (EBRAHIMI and

MOGHADASPOUR, 2015).

5. Whereas, cost per unit decreases as

production maximises.

Thus, it can be said that marginal and absorption costing both methods provide fruitful

results to organisation and as such, it should be calculated by firm to analyse various costs in the

production process.

Giving techniques of Management accounting

Revaluation accounting

Adjustment is made with the help of revaluation accounting so that book value of fixed asset is

adjusted with that of market value. This is required so that correct ascertainment of profit can be

made else, asset will continue at more cost in the books of company.

Funds flow statement

The difference is highlighted by this statement in the balance sheets of two years with reason of

such change.

8

tool for management of the company.

1. Absorption costing is mainly utilised for

outside or external reporting.

2. Marginal cost is applied on inventories on

variable cost of production.

2. Absorption costing is applied to all costs that

were used in the production process.

3. Inventory is restricted to be valued as per the

accounting standards.

3. Inventory can be allowed for valuation

purpose as governed by IAS (International

Accounting Standards) section 2.

4. Over and under apportionment of costs does

not arise as fixed production overheads are not

considered while calculating marginal costing.

4. Here, over and under absorption rates are

ascertained as fixed production overheads are

apportioned while calculating absorption

costing.

5. Cost per unit remains same as variable cost

is charged on the production (EBRAHIMI and

MOGHADASPOUR, 2015).

5. Whereas, cost per unit decreases as

production maximises.

Thus, it can be said that marginal and absorption costing both methods provide fruitful

results to organisation and as such, it should be calculated by firm to analyse various costs in the

production process.

Giving techniques of Management accounting

Revaluation accounting

Adjustment is made with the help of revaluation accounting so that book value of fixed asset is

adjusted with that of market value. This is required so that correct ascertainment of profit can be

made else, asset will continue at more cost in the books of company.

Funds flow statement

The difference is highlighted by this statement in the balance sheets of two years with reason of

such change.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Historical costing

It is the acquired cost of asset in the books of the business. Thus, it has the disadvantage that it

has to be revalued so that proper ascertainment of profit can be accomplished (Quattrone, 2016).

TASK 3

P4 Discuss kinds of planning tools

The various kinds of planning tools which are required by Vectair Holdings are as

follows-

Zero based budgeting

Zero based budgeting is the method which prepares budget from the scratch base and as

such, new budget cycle is prepared every year. In simple words, it is does not take previous year

base for formulating budget (Coad, Jack and Kholeif, 2015).

Advantages

1. The main advantage of this budget is that efficiency is obtained as no historical figures are

taken as a base for preparation of new budget.

2. Funds are allocated according to the current requirement of departments and as such, budget

inflation is not done. This is effective planning tool and proper allocation of funds are achieved

and as a result, it is easier method to inculcate better results.

Disadvantages

1. Main limitation of this method is that it does not take into account previous figures and as

such, more manpower is required to prepare budget from completely scratch base.

2. This method is time consuming as whole budget is prepared from zero base. Instead of this,

incremental budgeting should be used so that time can be saved just by increasing figures from

the previous budget (Helden and Uddin, 2016).

NPV

NPV (Net Present Value) method is effective planning tool which is helpful for Vectair

Holdings in the event of investing in any new project. NPV provides useful information

9

It is the acquired cost of asset in the books of the business. Thus, it has the disadvantage that it

has to be revalued so that proper ascertainment of profit can be accomplished (Quattrone, 2016).

TASK 3

P4 Discuss kinds of planning tools

The various kinds of planning tools which are required by Vectair Holdings are as

follows-

Zero based budgeting

Zero based budgeting is the method which prepares budget from the scratch base and as

such, new budget cycle is prepared every year. In simple words, it is does not take previous year

base for formulating budget (Coad, Jack and Kholeif, 2015).

Advantages

1. The main advantage of this budget is that efficiency is obtained as no historical figures are

taken as a base for preparation of new budget.

2. Funds are allocated according to the current requirement of departments and as such, budget

inflation is not done. This is effective planning tool and proper allocation of funds are achieved

and as a result, it is easier method to inculcate better results.

Disadvantages

1. Main limitation of this method is that it does not take into account previous figures and as

such, more manpower is required to prepare budget from completely scratch base.

2. This method is time consuming as whole budget is prepared from zero base. Instead of this,

incremental budgeting should be used so that time can be saved just by increasing figures from

the previous budget (Helden and Uddin, 2016).

NPV

NPV (Net Present Value) method is effective planning tool which is helpful for Vectair

Holdings in the event of investing in any new project. NPV provides useful information

9

regarding the profitability aspect of the project and as such, it is quite effective method to

analyse profitability of the project. Higher the NPV, better for firm to invest in the project.

Advantages

1. The main advantage of using NPV as a planning tool is that it considers time value of money

while evaluating project's profitability. Thus, it helps to maximise value of firm quite effectively.

2. Cost of capital is being considered and risks associated with new project is also made

available to the management so that they may take decision whether to invest in the project or

drop the plan (Tucker and Schaltegger, 2016).

Disadvantages

1. Disadvantage of NPV is that it uses discounting rate to predict profitability of the project and

as such, dependency on discounting rate may not provide reliable results. It is also difficult to

calculate such rate.

2. NPV provides results on the basis of forecasting and as such, wrongful interpretations may be

provided as it does not give concrete information regarding profitability aspect of the project.

IRR

IRR (Internal Rate of Return) is used as a planning tool because effective results are

provided by it. This method measures rate of return on project in that way so that effectiveness of

it may be carried out without any difficulty. It uses projected cash flows and imparts useful

information to business whether to invest in the same or not.

Advantages

1. It is effectual tool for making enhanced decision as it considers time value of money quite

effectively while assessing usefulness of investing in the new project. Moreover, it does involve

complex calculations and is easier to obtain results (Pavlatos and Kostakis, 2015).

2. It is good method for desired results as it equally considers cash flows and this helps to

measure present value of cash flow with that of outflow.

Disadvantages

10

analyse profitability of the project. Higher the NPV, better for firm to invest in the project.

Advantages

1. The main advantage of using NPV as a planning tool is that it considers time value of money

while evaluating project's profitability. Thus, it helps to maximise value of firm quite effectively.

2. Cost of capital is being considered and risks associated with new project is also made

available to the management so that they may take decision whether to invest in the project or

drop the plan (Tucker and Schaltegger, 2016).

Disadvantages

1. Disadvantage of NPV is that it uses discounting rate to predict profitability of the project and

as such, dependency on discounting rate may not provide reliable results. It is also difficult to

calculate such rate.

2. NPV provides results on the basis of forecasting and as such, wrongful interpretations may be

provided as it does not give concrete information regarding profitability aspect of the project.

IRR

IRR (Internal Rate of Return) is used as a planning tool because effective results are

provided by it. This method measures rate of return on project in that way so that effectiveness of

it may be carried out without any difficulty. It uses projected cash flows and imparts useful

information to business whether to invest in the same or not.

Advantages

1. It is effectual tool for making enhanced decision as it considers time value of money quite

effectively while assessing usefulness of investing in the new project. Moreover, it does involve

complex calculations and is easier to obtain results (Pavlatos and Kostakis, 2015).

2. It is good method for desired results as it equally considers cash flows and this helps to

measure present value of cash flow with that of outflow.

Disadvantages

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.