Financial Accounting: Principles, Stakeholders, and Statements

VerifiedAdded on 2020/11/23

|28

|4250

|210

Report

AI Summary

This report delves into the core principles of financial accounting, presenting a detailed exploration of its purpose and application. The report begins by defining financial accounting and its significance, followed by an examination of both internal and external stakeholders within a large business organization, highlighting their specific interests in financial information. The main body of the report includes practical examples of double-entry bookkeeping, trial balance, statement of profit and loss, and statement of financial position. It further elaborates on key accounting concepts such as consistency and prudence, along with a discussion on depreciation methods and their role in accounting. The report also addresses bank reconciliation statements, including their purpose and the factors that may cause discrepancies between bank and company records. Furthermore, it covers sales and purchase ledger control accounts, suspense accounts, and journal entries. Overall, the report provides a comprehensive analysis of financial accounting, supported by practical examples and real-world scenarios.

FINANCIAL ACCOUNTING

PRINCIPLES

PRINCIPLES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Defining financial accounting and its purpose........................................................................1

2. Naming two internal and four external stakeholders of large business organisation and

reason behind their interest in financial information of entity....................................................3

CLIENT 1........................................................................................................................................5

1. Completing double entry recording within the relevant ledger..............................................5

2. Trail balance at 31st January 2019........................................................................................13

CLIENT 2......................................................................................................................................14

(A.) Statement of profit and loss of Munteanu Ltd...................................................................14

(B.) Statement of financial position of Munteanu Ltd..............................................................14

(C.) Explaining the following accounting concepts..................................................................15

(D.) Describing the purpose of depreciation in formulating accounting concept with its two

widely used methods.................................................................................................................16

(E.) Critically evaluating difference between financial statements prepared by sole trader and

the limited companies...............................................................................................................17

CLIENT 3......................................................................................................................................17

(a.) Explaining the purpose of bank reconciliation statement with reason of performing

statements on monthly basis......................................................................................................17

(b.) Listing some areas which may cause record vary from the bank records..........................18

(c.) Explaining the term 'imprest' which used in petty cash system..........................................18

(d.) Bank reconciliation statement as at 30 September 2018....................................................18

CLIENT 4......................................................................................................................................20

(a.) preparation of sales and purchase ledger control account..................................................20

(b.) Explaining need for preparing control account and the term control account....................20

CLIENT 5......................................................................................................................................21

(a.) Describing the term suspense account with its main features............................................21

(b.) Trial balance from the figures............................................................................................22

(c.) Preparation of journal entries with suspense account.........................................................22

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Defining financial accounting and its purpose........................................................................1

2. Naming two internal and four external stakeholders of large business organisation and

reason behind their interest in financial information of entity....................................................3

CLIENT 1........................................................................................................................................5

1. Completing double entry recording within the relevant ledger..............................................5

2. Trail balance at 31st January 2019........................................................................................13

CLIENT 2......................................................................................................................................14

(A.) Statement of profit and loss of Munteanu Ltd...................................................................14

(B.) Statement of financial position of Munteanu Ltd..............................................................14

(C.) Explaining the following accounting concepts..................................................................15

(D.) Describing the purpose of depreciation in formulating accounting concept with its two

widely used methods.................................................................................................................16

(E.) Critically evaluating difference between financial statements prepared by sole trader and

the limited companies...............................................................................................................17

CLIENT 3......................................................................................................................................17

(a.) Explaining the purpose of bank reconciliation statement with reason of performing

statements on monthly basis......................................................................................................17

(b.) Listing some areas which may cause record vary from the bank records..........................18

(c.) Explaining the term 'imprest' which used in petty cash system..........................................18

(d.) Bank reconciliation statement as at 30 September 2018....................................................18

CLIENT 4......................................................................................................................................20

(a.) preparation of sales and purchase ledger control account..................................................20

(b.) Explaining need for preparing control account and the term control account....................20

CLIENT 5......................................................................................................................................21

(a.) Describing the term suspense account with its main features............................................21

(b.) Trial balance from the figures............................................................................................22

(c.) Preparation of journal entries with suspense account.........................................................22

CONCLUSION..............................................................................................................................23

REFERENCES.............................................................................................................................24

REFERENCES.............................................................................................................................24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting principles are the rules and guidelines which must be followed by

entity while reporting financial data in entities books of accounts. It is the specialised branch of

accounting which generally keeps track on financial transactions of the entity (Peterson,

Schmardebeck and Wilks, 2015). For the present report, selected small accountancy firm is

Howlader & Co. which is a group of chartered accountants that provides services as both tax

advisers and CA. In this report, explanation will be provided on financial accounting and its

purpose with two internal and four external stakeholders of organisation. Further, study will be

discussed on the interest of each stakeholder’s in the financial information of the entity.

Moreover, this report will also provide explanation related to methods of depreciation and need

of bank reconciliation statements.

MAIN BODY

To,

The Line manager

Howlader & Co,

Date: 16 march 2019

This is to inform you that for smooth running of business, here are some accounting rules and

regulations which our company is aware about it.

1. Defining financial accounting and its purpose

Financial accounting is a special branch of accounting which mainly helps entity to keep

track of accounting transactions of the entity. It is the field of accounting which mainly

concerned with the summary, analysis and reporting of financial transactions. This is an area of

accounting which focuses on providing information related to internal and external business

affairs to its users, stakeholders and creditors. Financial statements are issued by entity on their

routine schedule and such statements are given to people outside the company so that they are

able to take decision regarding investing their money on capital of the firm.

In other words, financial accounting is also known as field of accounting which treat money as

a means of measuring entity's economic performance rather than measuring as the factor of

production. It is also considered as process under which complete monitoring and control of

money takes place in order to analyse the amount of money which flow in and out from

1

Financial accounting principles are the rules and guidelines which must be followed by

entity while reporting financial data in entities books of accounts. It is the specialised branch of

accounting which generally keeps track on financial transactions of the entity (Peterson,

Schmardebeck and Wilks, 2015). For the present report, selected small accountancy firm is

Howlader & Co. which is a group of chartered accountants that provides services as both tax

advisers and CA. In this report, explanation will be provided on financial accounting and its

purpose with two internal and four external stakeholders of organisation. Further, study will be

discussed on the interest of each stakeholder’s in the financial information of the entity.

Moreover, this report will also provide explanation related to methods of depreciation and need

of bank reconciliation statements.

MAIN BODY

To,

The Line manager

Howlader & Co,

Date: 16 march 2019

This is to inform you that for smooth running of business, here are some accounting rules and

regulations which our company is aware about it.

1. Defining financial accounting and its purpose

Financial accounting is a special branch of accounting which mainly helps entity to keep

track of accounting transactions of the entity. It is the field of accounting which mainly

concerned with the summary, analysis and reporting of financial transactions. This is an area of

accounting which focuses on providing information related to internal and external business

affairs to its users, stakeholders and creditors. Financial statements are issued by entity on their

routine schedule and such statements are given to people outside the company so that they are

able to take decision regarding investing their money on capital of the firm.

In other words, financial accounting is also known as field of accounting which treat money as

a means of measuring entity's economic performance rather than measuring as the factor of

production. It is also considered as process under which complete monitoring and control of

money takes place in order to analyse the amount of money which flow in and out from

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organisation in the context of assets and liabilities. Thus, it can be said that financial accounting

is the process which keeps on track the cash flow of entity in order to run business with the long

term perspective.

However, it is a fact that financial accounting is mainly termed as the language of business

which main function is to serve communication. Thus, in order to protect the interest of the

shareholders, financial accounting is governed by both local and international accounting

standards. Through such accounting, Howlader & Co. will able to disclose its financial

capabilities and its performance in business market to the general public and to its stakeholders.

Its main purpose are as follows-

Main purpose of financial accounting is to provide the information which is important in

terms of decision making process of the entity. It is important to analyse that purpose of

financial accounting is not to report the business transaction. Rather, its goal is to provide

enough information to users and customers so that they will able to assess the value and

capability of company for themselves.

Its role is to prepare effective financial reports which will provide information regarding

the performance of the firms to its internal and external stakeholders such as investors,

creditors, manager and customer as well. It is a process through which company's revenue,

receivables, incomes and expenses are generally collected, measured and reported in the books

of accounts. Thus, it can be said that its purpose is to collect information regarding business

results, its financial capabilities and cash flow of organisation.

The other additional purpose of the financial accounting is as follows-

Credit decision: financial statements used by the lender for analysing entire set of

business information in order to determine whether the money which they have invested in

company will need to be extended or to be restricted. Thus, through this information, entities

will able to attract more support from the creditors.

Investment decision: financial statements are provided to investor so that they will use

such information in order to decide whether to invest on entity's business capital or at price per

share (The purpose of financial statements, 2018). Such information will analyse by them to

decide capability of the firm to provide adequate return.

Taxation decision: purpose of financial accounting is to serve the financial statements to

government or tax authorities so that they will able to charge tax on business by analysing

2

is the process which keeps on track the cash flow of entity in order to run business with the long

term perspective.

However, it is a fact that financial accounting is mainly termed as the language of business

which main function is to serve communication. Thus, in order to protect the interest of the

shareholders, financial accounting is governed by both local and international accounting

standards. Through such accounting, Howlader & Co. will able to disclose its financial

capabilities and its performance in business market to the general public and to its stakeholders.

Its main purpose are as follows-

Main purpose of financial accounting is to provide the information which is important in

terms of decision making process of the entity. It is important to analyse that purpose of

financial accounting is not to report the business transaction. Rather, its goal is to provide

enough information to users and customers so that they will able to assess the value and

capability of company for themselves.

Its role is to prepare effective financial reports which will provide information regarding

the performance of the firms to its internal and external stakeholders such as investors,

creditors, manager and customer as well. It is a process through which company's revenue,

receivables, incomes and expenses are generally collected, measured and reported in the books

of accounts. Thus, it can be said that its purpose is to collect information regarding business

results, its financial capabilities and cash flow of organisation.

The other additional purpose of the financial accounting is as follows-

Credit decision: financial statements used by the lender for analysing entire set of

business information in order to determine whether the money which they have invested in

company will need to be extended or to be restricted. Thus, through this information, entities

will able to attract more support from the creditors.

Investment decision: financial statements are provided to investor so that they will use

such information in order to decide whether to invest on entity's business capital or at price per

share (The purpose of financial statements, 2018). Such information will analyse by them to

decide capability of the firm to provide adequate return.

Taxation decision: purpose of financial accounting is to serve the financial statements to

government or tax authorities so that they will able to charge tax on business by analysing

2

company's assets and income.

Union bargaining decision: other purpose of financial accounting is to serve

information of business transaction to unions on which they can base their bargaining position

by analysing ability of the company to pay benefits to employees.

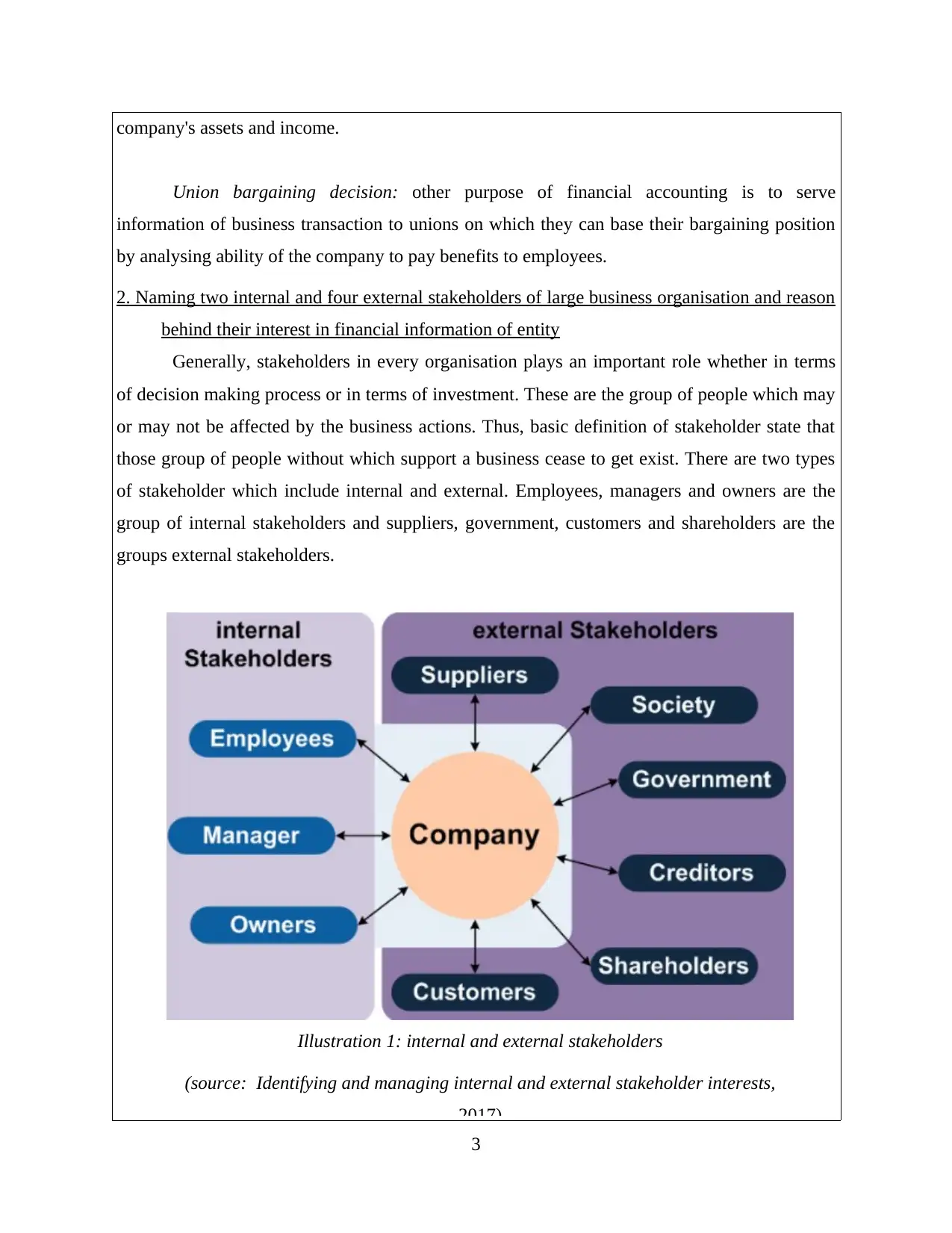

2. Naming two internal and four external stakeholders of large business organisation and reason

behind their interest in financial information of entity

Generally, stakeholders in every organisation plays an important role whether in terms

of decision making process or in terms of investment. These are the group of people which may

or may not be affected by the business actions. Thus, basic definition of stakeholder state that

those group of people without which support a business cease to get exist. There are two types

of stakeholder which include internal and external. Employees, managers and owners are the

group of internal stakeholders and suppliers, government, customers and shareholders are the

groups external stakeholders.

3

Illustration 1: internal and external stakeholders

(source: Identifying and managing internal and external stakeholder interests,

2017)

Union bargaining decision: other purpose of financial accounting is to serve

information of business transaction to unions on which they can base their bargaining position

by analysing ability of the company to pay benefits to employees.

2. Naming two internal and four external stakeholders of large business organisation and reason

behind their interest in financial information of entity

Generally, stakeholders in every organisation plays an important role whether in terms

of decision making process or in terms of investment. These are the group of people which may

or may not be affected by the business actions. Thus, basic definition of stakeholder state that

those group of people without which support a business cease to get exist. There are two types

of stakeholder which include internal and external. Employees, managers and owners are the

group of internal stakeholders and suppliers, government, customers and shareholders are the

groups external stakeholders.

3

Illustration 1: internal and external stakeholders

(source: Identifying and managing internal and external stakeholder interests,

2017)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The interest of each stakeholder behind the financial information of the entity is as follows-

Customers: These are the major important group of stakeholders for any type of

organisation whether it is small or large. In fact, it is said that business exist only to serve its

customers. Customers are known to be an actual stakeholder for enterprise and mainly impacted

by the service quality and its value. They are interested in company's financial information in

order to analyse the financial capability of the firm to serve them for the long term perspective.

They are generally interested in knowing the financial strength of the entity.

Employees: These are the group of stakeholders which has direct interest in entity's

financial information. Reason behind such interest is that they earn to provide support to

themselves and other too. They are interested towards profitability and stability in order to

analyse the ability of the company for paying their salaries and benefits (Interested parties of

financial statements, 2019). They are also interested to analyse their career development

opportunity in such enterprise.

Management: these are the group of stakeholders which has the deep interest in entities

financial as well in performance information. For small businesses are known as owners and are

hired professional to whom all the responsibility of the business operations are given.

Therefore, their interest in financial information of entity is for analysing the amount of

supplies which company purchased, cash inflows and outflow in the entity and profit which

earn last year so that sound economic decision will get developed for further business

operations of the entity.

Suppliers: they are the group of stakeholder which generally sells goods and services to

business and mainly rely only for the revenue generation with current business operations of

entity. They are the group which directly involved in companies’ operations (Mio, 2016). They

are interested in financial information in order to analyse the ability to pay obligation when it

becomes due. In simple terms, they are interested in liquidity position of the company and its

ability for paying short term obligations.

Government: they are also considered as major stakeholder group of business as

government collect taxes from both company and from its employees. This group is generally

interested in company's financial information for the purpose of taxations and regulatory

purpose. Government charge tax on the basis in entity's business operations result so that tax

will get charged on them. They are also interested in analysing amount of money which paid by

4

Customers: These are the major important group of stakeholders for any type of

organisation whether it is small or large. In fact, it is said that business exist only to serve its

customers. Customers are known to be an actual stakeholder for enterprise and mainly impacted

by the service quality and its value. They are interested in company's financial information in

order to analyse the financial capability of the firm to serve them for the long term perspective.

They are generally interested in knowing the financial strength of the entity.

Employees: These are the group of stakeholders which has direct interest in entity's

financial information. Reason behind such interest is that they earn to provide support to

themselves and other too. They are interested towards profitability and stability in order to

analyse the ability of the company for paying their salaries and benefits (Interested parties of

financial statements, 2019). They are also interested to analyse their career development

opportunity in such enterprise.

Management: these are the group of stakeholders which has the deep interest in entities

financial as well in performance information. For small businesses are known as owners and are

hired professional to whom all the responsibility of the business operations are given.

Therefore, their interest in financial information of entity is for analysing the amount of

supplies which company purchased, cash inflows and outflow in the entity and profit which

earn last year so that sound economic decision will get developed for further business

operations of the entity.

Suppliers: they are the group of stakeholder which generally sells goods and services to

business and mainly rely only for the revenue generation with current business operations of

entity. They are the group which directly involved in companies’ operations (Mio, 2016). They

are interested in financial information in order to analyse the ability to pay obligation when it

becomes due. In simple terms, they are interested in liquidity position of the company and its

ability for paying short term obligations.

Government: they are also considered as major stakeholder group of business as

government collect taxes from both company and from its employees. This group is generally

interested in company's financial information for the purpose of taxations and regulatory

purpose. Government charge tax on the basis in entity's business operations result so that tax

will get charged on them. They are also interested in analysing amount of money which paid by

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

taxpayer is correct or not.

Shareholders: These are the group of stakeholders which owns share in business with

the motive of getting return on capital. In general sense they are the real owners and has deep

interest in financial information of the entity. They want financial information in order to

analyse the way entity is utilizing their money which invested and ascertaining the profitability

and capability of the enterprise.

Thus, these are the two internal and four external stakeholders of the large business and

their interest towards financial information of the company. In simple terms, all these group are

interested in order to analyse the capability and strength of firm in business market.

From-

Junior Accountant

CLIENT 1

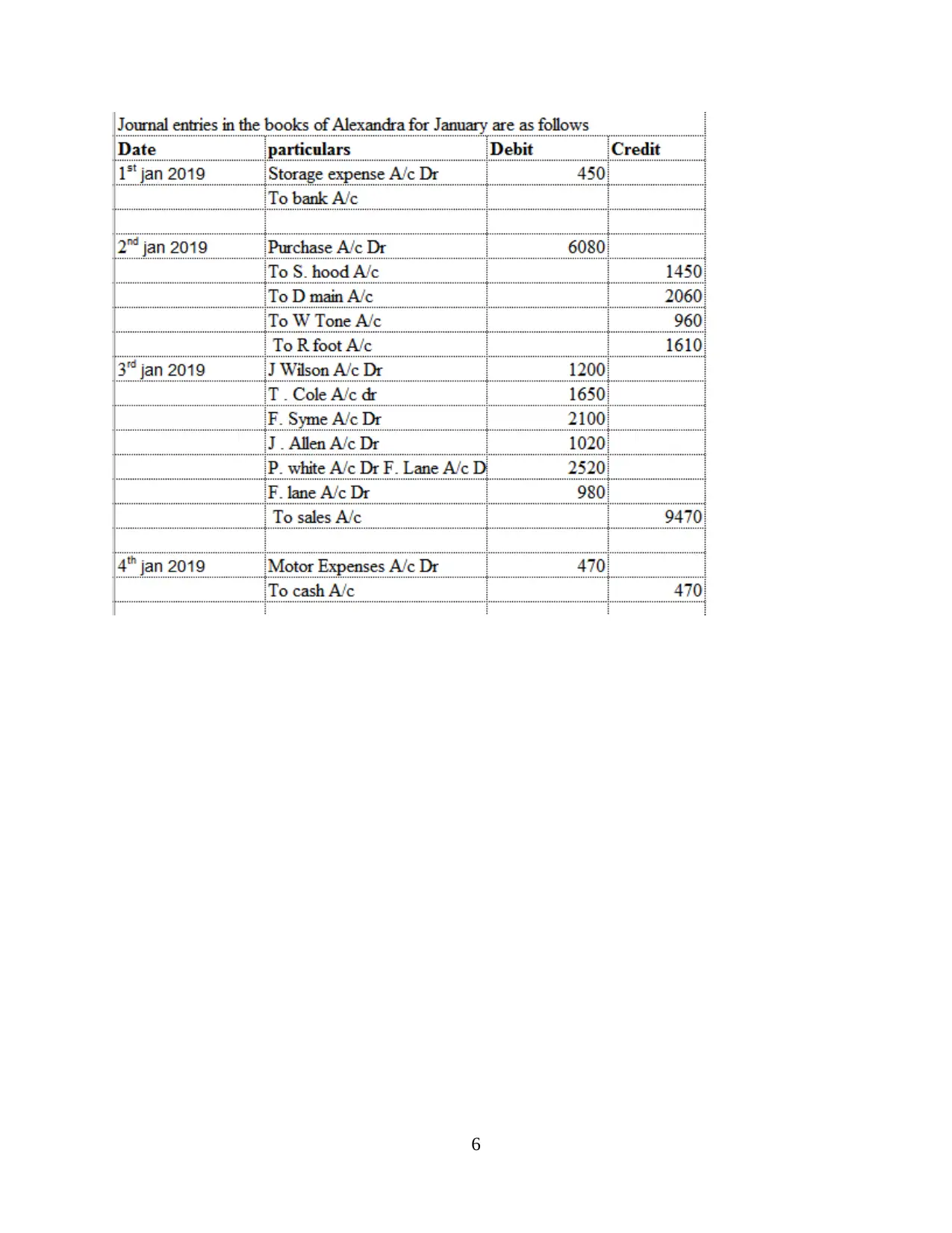

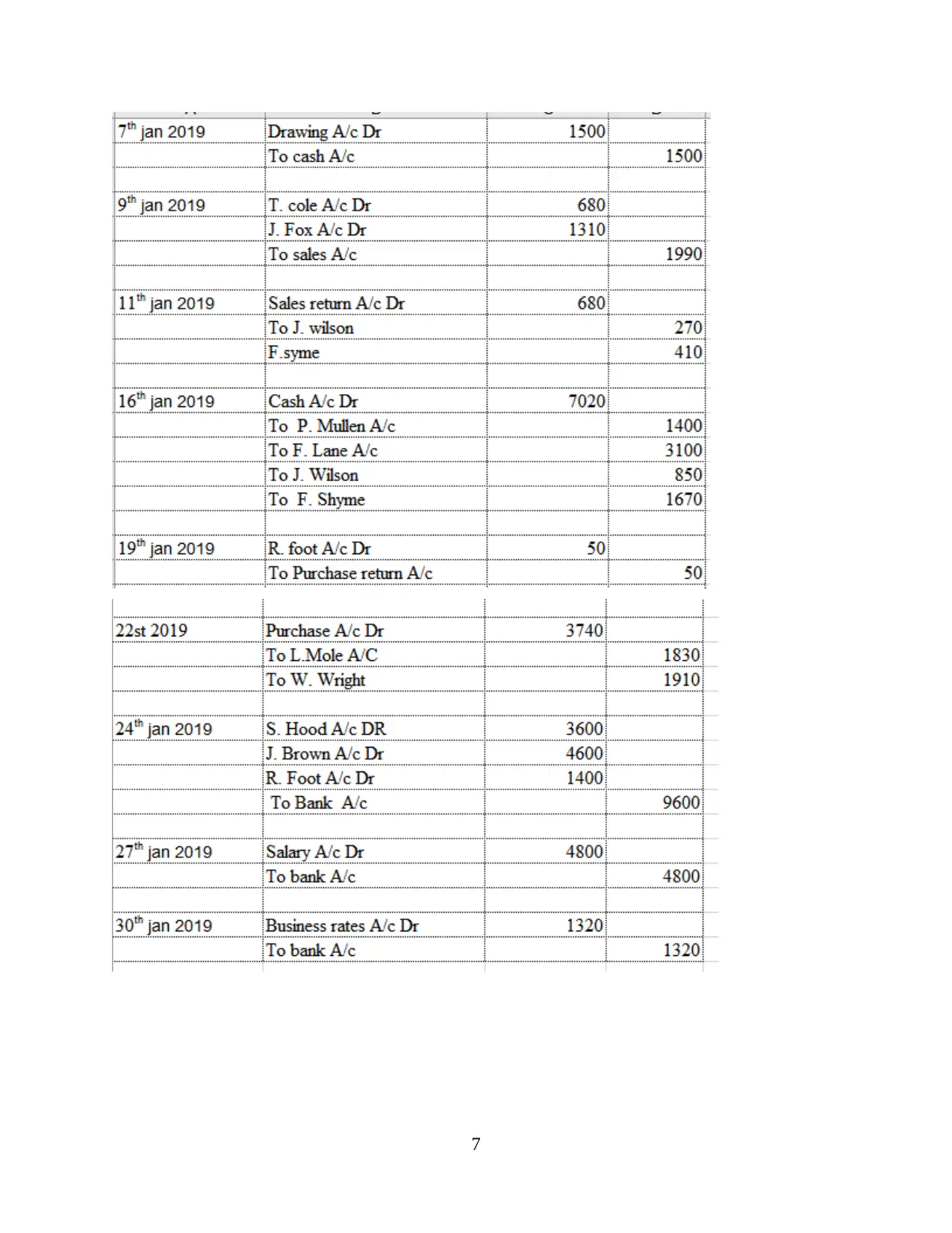

1. Completing double entry recording within the relevant ledger

5

Shareholders: These are the group of stakeholders which owns share in business with

the motive of getting return on capital. In general sense they are the real owners and has deep

interest in financial information of the entity. They want financial information in order to

analyse the way entity is utilizing their money which invested and ascertaining the profitability

and capability of the enterprise.

Thus, these are the two internal and four external stakeholders of the large business and

their interest towards financial information of the company. In simple terms, all these group are

interested in order to analyse the capability and strength of firm in business market.

From-

Junior Accountant

CLIENT 1

1. Completing double entry recording within the relevant ledger

5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

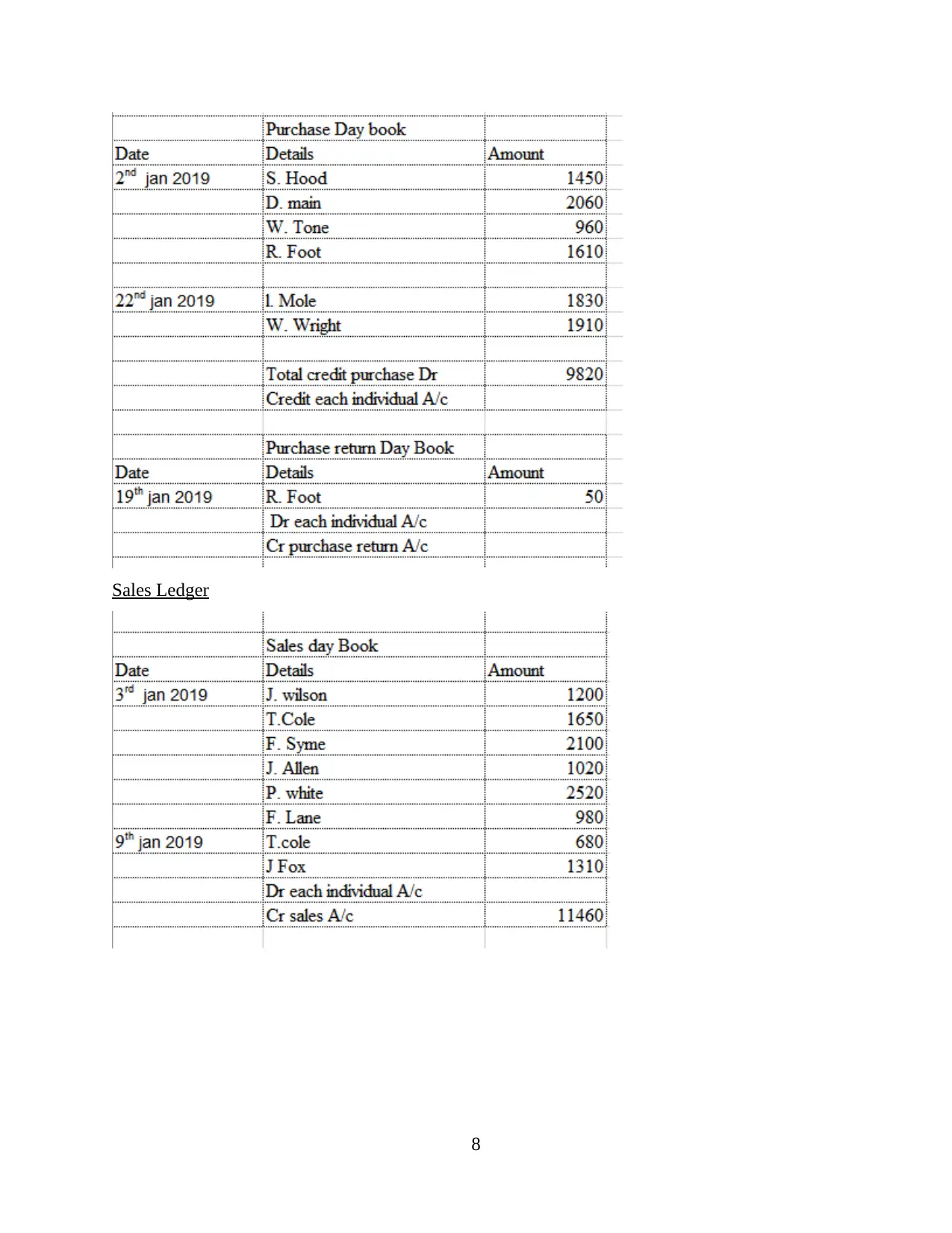

Sales Ledger

8

8

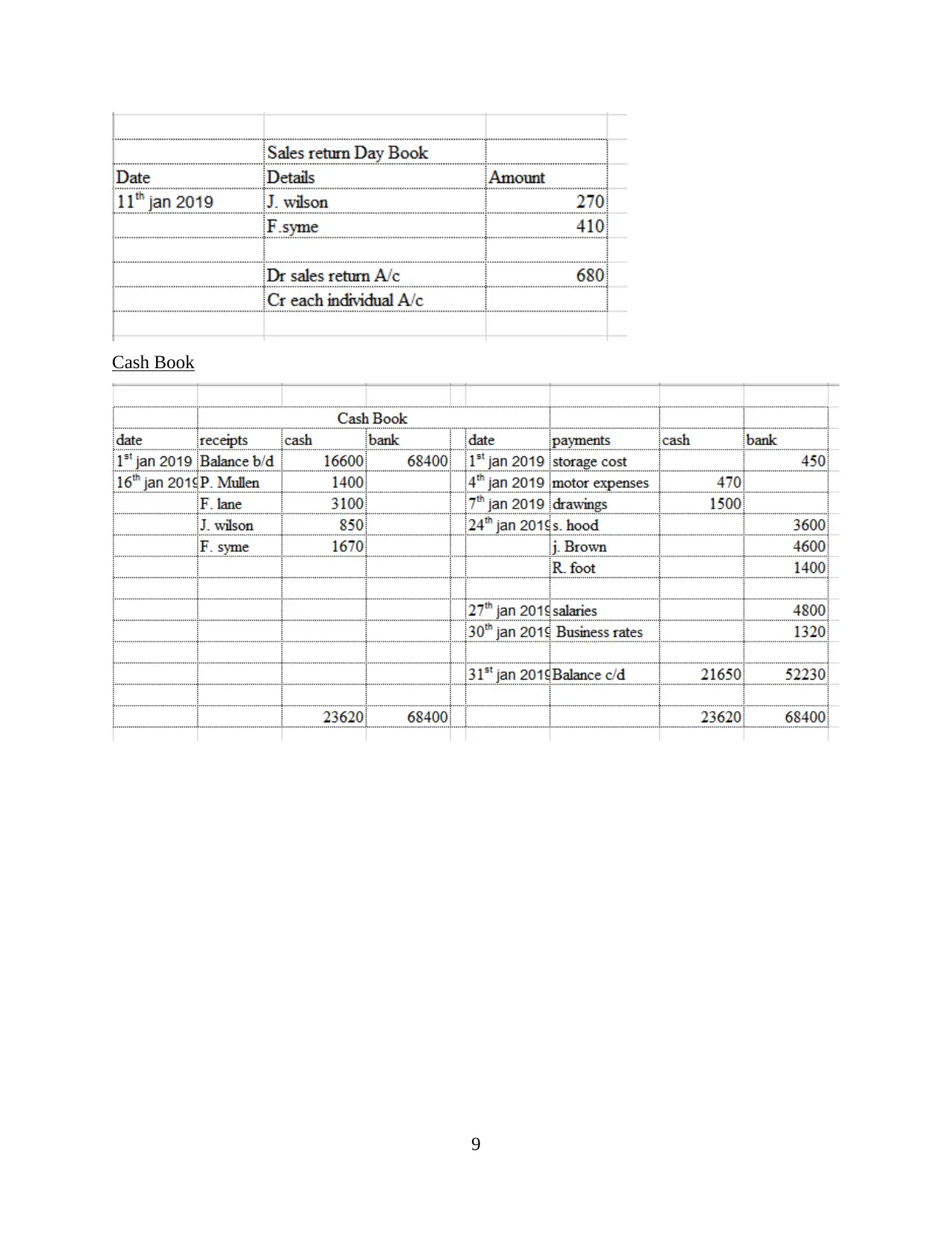

Cash Book

9

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.