Financial Report: Innocent Drinks UK - Management Accounting Analysis

VerifiedAdded on 2022/10/12

|25

|5377

|39

Report

AI Summary

This report provides a detailed exploration of management accounting principles and their practical applications. Part 1 defines management and financial accounting, comparing their systems and outlining various types of management accounting systems such as cost accounting, inventory management, and job-costing systems. It also covers different reporting methods including job cost reports, performance reports, and variance analysis. Part 2 focuses on a case study of Innocent Drinks UK, applying absorption and marginal costing methods to prepare income statements. It includes calculations for full production costs, inventory valuation, and profit reconciliation. Furthermore, the report delves into break-even analysis, margin of safety calculations, and graphical representations. It also discusses budgetary control tools, including zero-based, activity-based, and incremental budgeting, alongside adaptations of management accounting systems like the Balanced Scorecard and benchmarking. The report concludes by assessing the significance of management accounting in modern organizations, emphasizing its advantages in strategic decision-making and performance improvement.

Contents

Page

Introduction 3

Part 1:

Management Accounting 4

Financial Accounting 4

A comparison between management and financial accounting systems 4

Types of management accounting systems 5

Cost Accounting 5

Benefits of cost accounting: 5

Inventory Management System 5

Benefits of Inventory System 5

Job-costing systems 5

Issues with Job-costing systems 6

Price-optimizing systems 6

Benefits of price-optimizing systems 6

Different Methods used for Management Accounting Reporting 6

Job Cost Reports 6

Inventory Management Reports 7

Performance Reports 7

Variance Report 7

A Profit and Loss Report (P&L) 7

The Cash Flow Statement 8

Customer Survey Reports 8

Part 2:

Innocent Drinks UK -

Prepare an Income Statement using Marginal and Absorption Costing 9

1.1

Absorption Costing 9

W1 Calculation of full production cost 9

W2 Calculation of value of inventory and production (valued at £8 per unit) 9

W3 Under/over absorbed fixed production overhead 10

Absorption costing profit statement 10

Net Profit 10

Marginal Costing 11

W1 Variable production cost 11

W2 Value of Inventory and production 11

Marginal costing profit statement 11

Net Profit 12

Reconciliation of profit figures 13

1.2 INNOCENT DRINKS UK - DAIRY FREE RANGE OF DRINKS

a). Break-Even Point for the next year 14

b). Margin of Safety for next year – Expressed in Quantity and Sales Value 15

c). Break Even Point using Graphical Method 16

0

Page

Introduction 3

Part 1:

Management Accounting 4

Financial Accounting 4

A comparison between management and financial accounting systems 4

Types of management accounting systems 5

Cost Accounting 5

Benefits of cost accounting: 5

Inventory Management System 5

Benefits of Inventory System 5

Job-costing systems 5

Issues with Job-costing systems 6

Price-optimizing systems 6

Benefits of price-optimizing systems 6

Different Methods used for Management Accounting Reporting 6

Job Cost Reports 6

Inventory Management Reports 7

Performance Reports 7

Variance Report 7

A Profit and Loss Report (P&L) 7

The Cash Flow Statement 8

Customer Survey Reports 8

Part 2:

Innocent Drinks UK -

Prepare an Income Statement using Marginal and Absorption Costing 9

1.1

Absorption Costing 9

W1 Calculation of full production cost 9

W2 Calculation of value of inventory and production (valued at £8 per unit) 9

W3 Under/over absorbed fixed production overhead 10

Absorption costing profit statement 10

Net Profit 10

Marginal Costing 11

W1 Variable production cost 11

W2 Value of Inventory and production 11

Marginal costing profit statement 11

Net Profit 12

Reconciliation of profit figures 13

1.2 INNOCENT DRINKS UK - DAIRY FREE RANGE OF DRINKS

a). Break-Even Point for the next year 14

b). Margin of Safety for next year – Expressed in Quantity and Sales Value 15

c). Break Even Point using Graphical Method 16

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The advantages and disadvantages of different types of planning tools used for budgetary

control 17

Zero based budgeting system 17

Activity based budgeting (ABB) 17

Incremental Budgeting 17

How organizations adapting to management accounting systems 17

Balanced Scorecard 18

Benchmarking 19

Key Performance Indicator (KPIs) 20

Budgetary control and variance analysis 20

Compare how organizations are adapting management accounting systems 21

Conclusion 23

Bibliography 24

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

1

control 17

Zero based budgeting system 17

Activity based budgeting (ABB) 17

Incremental Budgeting 17

How organizations adapting to management accounting systems 17

Balanced Scorecard 18

Benchmarking 19

Key Performance Indicator (KPIs) 20

Budgetary control and variance analysis 20

Compare how organizations are adapting management accounting systems 21

Conclusion 23

Bibliography 24

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

1

Introduction

This report consists of two parts in which the first part is an explanation of the management accounting

system and how it is beneficial in organisations future planning and decision making. This section also

discusses how important the management accounting to be integrated into the organisation processes.

The second part the of the report consists of a financial report where range of management techniques are

used to the accounting figures provided by Innocent Drinks UK to produce a Financial Report with

working to determine the profit and loss status. It also explains the advantages and disadvantages of

different types of planning tools and budgetary control in details.

A discussion on management accounting and financial accounting has been included to cover the types of

management accounting system.

Calculation of absorption costing and marginal costing have been carried out for the Innocent Drinks UK

company for its Super Smoothies with the reconciliation statement and the profit figures too are included.

Under the section 1.2 Income statement using Marginal and Absorption costs have been shown. The

financial report together with breakeven points including graphical method have been included.

The comparisons of Unilever and Tesco’s management accounting reporting have been discussed in the

report. The balance scored card method used by Unilever as a part of its management accounting and how

Tesco is benefitted using an advance just-in-time inventory management system haven also been discussed.

The concluding section assesses the importance of management accounting in a critical context with its

advantages in the modern-day organisations.

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

2

This report consists of two parts in which the first part is an explanation of the management accounting

system and how it is beneficial in organisations future planning and decision making. This section also

discusses how important the management accounting to be integrated into the organisation processes.

The second part the of the report consists of a financial report where range of management techniques are

used to the accounting figures provided by Innocent Drinks UK to produce a Financial Report with

working to determine the profit and loss status. It also explains the advantages and disadvantages of

different types of planning tools and budgetary control in details.

A discussion on management accounting and financial accounting has been included to cover the types of

management accounting system.

Calculation of absorption costing and marginal costing have been carried out for the Innocent Drinks UK

company for its Super Smoothies with the reconciliation statement and the profit figures too are included.

Under the section 1.2 Income statement using Marginal and Absorption costs have been shown. The

financial report together with breakeven points including graphical method have been included.

The comparisons of Unilever and Tesco’s management accounting reporting have been discussed in the

report. The balance scored card method used by Unilever as a part of its management accounting and how

Tesco is benefitted using an advance just-in-time inventory management system haven also been discussed.

The concluding section assesses the importance of management accounting in a critical context with its

advantages in the modern-day organisations.

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part 1:

Management Accounting:

Management accounting is defined as a process of identification, analysis, preparation, communication

and interpretation of both qualitative and quantitative data provided to managers within the organization so

that they could take strategical decisions as well as control day to day operations. (Burns, et.al.2013).

The management accounting information helps the internal managers of the organization, its employees

and senior executives in decision making and to improve performance. The future success of an

organization depends on information provided in the management accounting reports. Also, these

management accounting reports enhance both customer and shareholder value (researchgate,2018).

Financial Accounting :

This is a branch of accounting in which financial statements are produced of the transactions made to

show its financial position to the people outside the company. These people may include investors,

suppliers, creditors and customers. Producing financial account statements is also a regulatory requirement

that all companies and organizations must adhered to. There are several main functions of financial

accounting and these include, budget preparation, planning, cost control and prevention of fraud.

(Financial accounting and reporting, 2019)

A comparison between management and financial accounting systems.

.

Management Accounting Financial Accounting

Detailed information relating to department,

product, customer and employees are needed.

Only the summarized data is required.

Not mandatory. Mandatory as external customers could be waiting

for it.

Need to follow the accepted accounting rules. Need to follow the accepted accounting rules.

Information is bound by the time period. Precision past performance information is

required.

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

3

Management Accounting:

Management accounting is defined as a process of identification, analysis, preparation, communication

and interpretation of both qualitative and quantitative data provided to managers within the organization so

that they could take strategical decisions as well as control day to day operations. (Burns, et.al.2013).

The management accounting information helps the internal managers of the organization, its employees

and senior executives in decision making and to improve performance. The future success of an

organization depends on information provided in the management accounting reports. Also, these

management accounting reports enhance both customer and shareholder value (researchgate,2018).

Financial Accounting :

This is a branch of accounting in which financial statements are produced of the transactions made to

show its financial position to the people outside the company. These people may include investors,

suppliers, creditors and customers. Producing financial account statements is also a regulatory requirement

that all companies and organizations must adhered to. There are several main functions of financial

accounting and these include, budget preparation, planning, cost control and prevention of fraud.

(Financial accounting and reporting, 2019)

A comparison between management and financial accounting systems.

.

Management Accounting Financial Accounting

Detailed information relating to department,

product, customer and employees are needed.

Only the summarized data is required.

Not mandatory. Mandatory as external customers could be waiting

for it.

Need to follow the accepted accounting rules. Need to follow the accepted accounting rules.

Information is bound by the time period. Precision past performance information is

required.

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Types of management accounting systems:

Cost Accounting:

Cost accounting deals with calculating cost of goods and services provided and also in terms of

organizational units such as departments.

The details of various costs that are needed to control the existing operation are provided to the

management using cost accounting. There are large manufacturing organisations like Ford and General

Motors who uses cost accounting and from retailers Tesco and ASDA are known examples.

Benefits of cost accounting:

Cost accounting could determine precise cost of a product which is important in taking marketing decision.

It also helps to decide on the selling price of a product, calculating profitability and also to meet

competition.

Inventory Management System:

The inventory management system is a stock control system to determine the stock levels and how much

should be maintained and when it should be replenished. The inventory may include raw materials

supplied by the vendors but not yet used or added any labour, finished goods that are still in the factory or

possession of the firm and also work in progress items which are partially complete.

Benefits of Inventory systems:

It gives assurance against knowing the exact status of the stock level so that uncertainty can be avoided.

Also, it helps to avoid any shortages of materials and to address any shortages of demand. In addition, it

would support strategic plan and be able to take advantage of economies of scale.

Job-costing systems:

It is a system to accumulate costs of material, labour and overhead for a specific job or task. This system

of costing is ideal for ‘one off’ custom jobs which are different from customer to customer.

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

4

Cost Accounting:

Cost accounting deals with calculating cost of goods and services provided and also in terms of

organizational units such as departments.

The details of various costs that are needed to control the existing operation are provided to the

management using cost accounting. There are large manufacturing organisations like Ford and General

Motors who uses cost accounting and from retailers Tesco and ASDA are known examples.

Benefits of cost accounting:

Cost accounting could determine precise cost of a product which is important in taking marketing decision.

It also helps to decide on the selling price of a product, calculating profitability and also to meet

competition.

Inventory Management System:

The inventory management system is a stock control system to determine the stock levels and how much

should be maintained and when it should be replenished. The inventory may include raw materials

supplied by the vendors but not yet used or added any labour, finished goods that are still in the factory or

possession of the firm and also work in progress items which are partially complete.

Benefits of Inventory systems:

It gives assurance against knowing the exact status of the stock level so that uncertainty can be avoided.

Also, it helps to avoid any shortages of materials and to address any shortages of demand. In addition, it

would support strategic plan and be able to take advantage of economies of scale.

Job-costing systems:

It is a system to accumulate costs of material, labour and overhead for a specific job or task. This system

of costing is ideal for ‘one off’ custom jobs which are different from customer to customer.

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

4

Issues with job-costing:

It is difficult to set price for a job and to include the expected profit. Also, there is an issue of finding the

actual spent for the job. There is a possibility that profits could be negatively impacted due to the

differences in actual and expected costs.

Price-optimising systems:

By using price optimising system an organisation would be able to find how sensitive the existing clients to

price changes of the products and arrive at various profitability levels. The method is useful in setting

prices for different customer segments based on how they respond to changes in different pricing scenarios.

Benefits of price-optimising systems:

If an organisation’s main task is to keep the customer retention at current level and increase the profits,

then the optimal pricing is useful. It is used to understand how sensitive the customers to changing prices

of the product or services and obtain targeted profitability levels.

Different Methods used for Management Accounting Reporting:

The purpose of management accounting reports is to help the management of an organisation to take

informed decisions. These reports contain not only financial information but also non-financial data that

could facilitate decision making.

Presentation of Management account reporting could be:

1. Using visual aids, charts and tables.

2. Printed Reports.

3. Verbal presentation (may include use of above).

Job Cost Reports

Job cost reports show the ongoing costs of a project (e.g. construction). These reports are usually

compared against the estimates of revenue so that the company could have an idea of the profitability.

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

5

It is difficult to set price for a job and to include the expected profit. Also, there is an issue of finding the

actual spent for the job. There is a possibility that profits could be negatively impacted due to the

differences in actual and expected costs.

Price-optimising systems:

By using price optimising system an organisation would be able to find how sensitive the existing clients to

price changes of the products and arrive at various profitability levels. The method is useful in setting

prices for different customer segments based on how they respond to changes in different pricing scenarios.

Benefits of price-optimising systems:

If an organisation’s main task is to keep the customer retention at current level and increase the profits,

then the optimal pricing is useful. It is used to understand how sensitive the customers to changing prices

of the product or services and obtain targeted profitability levels.

Different Methods used for Management Accounting Reporting:

The purpose of management accounting reports is to help the management of an organisation to take

informed decisions. These reports contain not only financial information but also non-financial data that

could facilitate decision making.

Presentation of Management account reporting could be:

1. Using visual aids, charts and tables.

2. Printed Reports.

3. Verbal presentation (may include use of above).

Job Cost Reports

Job cost reports show the ongoing costs of a project (e.g. construction). These reports are usually

compared against the estimates of revenue so that the company could have an idea of the profitability.

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

These reports could be used to identify the higher earning areas so that the company could focus on those

leaving the lesser profitable areas.

Inventory Management Reports:

Inventory management reports are useful as it gives an account of how much stock is available at a given

time. It can also use to determine what level of stock should be maintained and how much stick should be

replenished. Further these reports will have data such as inventory waste, overheads and hourly labour

costs.

Management can use the above information to determine the best performing departments and the areas

that need attention to. (Inventory Management, 2019)

Performance Reports:

Performance reports are vital for the management as they give information relating to individual product

and service by departments or for each market segment relating to the business. By taking advantage of

these reports, companies can analyse the segments together with product lines for profitability analysis.

Any corrective measures could be taken to bring about cost saving and efficiency in its operations.

The report is used to compare the actual outcome against the budget or standard to determine any variances

of the two figures so that any action could be taken. (Seal, W, 2014).

Variance Report:

It is a report to identify any differences (variance) in the planned financial allocation with the actual

financial outcome. The variance reports would show any difference between the actual and budgeted

performance. If the report shown any permanent variances, then it may indicate that the budget report is in

correct and or they may be due to timing differences due to any costs taking place prior to or later than

expected.

A Profit and Loss Report (P&L):

This report shows the total income and the total expenditure during a specific period of time. It is a useful

financial tool as it clearly indicates the net profit or loss based on the income and expenditure. If the

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

6

leaving the lesser profitable areas.

Inventory Management Reports:

Inventory management reports are useful as it gives an account of how much stock is available at a given

time. It can also use to determine what level of stock should be maintained and how much stick should be

replenished. Further these reports will have data such as inventory waste, overheads and hourly labour

costs.

Management can use the above information to determine the best performing departments and the areas

that need attention to. (Inventory Management, 2019)

Performance Reports:

Performance reports are vital for the management as they give information relating to individual product

and service by departments or for each market segment relating to the business. By taking advantage of

these reports, companies can analyse the segments together with product lines for profitability analysis.

Any corrective measures could be taken to bring about cost saving and efficiency in its operations.

The report is used to compare the actual outcome against the budget or standard to determine any variances

of the two figures so that any action could be taken. (Seal, W, 2014).

Variance Report:

It is a report to identify any differences (variance) in the planned financial allocation with the actual

financial outcome. The variance reports would show any difference between the actual and budgeted

performance. If the report shown any permanent variances, then it may indicate that the budget report is in

correct and or they may be due to timing differences due to any costs taking place prior to or later than

expected.

A Profit and Loss Report (P&L):

This report shows the total income and the total expenditure during a specific period of time. It is a useful

financial tool as it clearly indicates the net profit or loss based on the income and expenditure. If the

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expenditure is high any cost cutting measure can be applied. The profit and loss (P&L) is sometimes

known as ‘Income Statement” or “Statement of Operations” or simply as “Income and Expenses

Statement”.

The Cash Flow Statement:

It is a financial statement summarizing the amount of cash or equivalent entering or leaving the company.

The Cash Flow Statement (CFS) of a company shows how well a company generate cash and whether it is

in a position to pay off its debt as well as to fund its operating expenses. Having a cash flow statement is

mandatory for a company and it complements balance sheet and income statement.

Customer Survey Reports:

These reports measure customer satisfaction with regard to company’s services or products. Managers

could also use these reports to take any informed decisions with regard to their services or for new product

development. Customer satisfaction surveys provide very valuable insight into one’s organization and

ensure that they stay relevant to the customer needs and wants. It’s a tool used widely to improve customer

satisfaction and loyalty so that existing customers would still retain in the company.

The information from customer satisfaction surveys help valuable insight to one’s organization to stay

relevant and to know the customer needs and wants. Customer satisfaction surveys are important tools for

updating business requirements and ensuring the customers remain with you

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

7

known as ‘Income Statement” or “Statement of Operations” or simply as “Income and Expenses

Statement”.

The Cash Flow Statement:

It is a financial statement summarizing the amount of cash or equivalent entering or leaving the company.

The Cash Flow Statement (CFS) of a company shows how well a company generate cash and whether it is

in a position to pay off its debt as well as to fund its operating expenses. Having a cash flow statement is

mandatory for a company and it complements balance sheet and income statement.

Customer Survey Reports:

These reports measure customer satisfaction with regard to company’s services or products. Managers

could also use these reports to take any informed decisions with regard to their services or for new product

development. Customer satisfaction surveys provide very valuable insight into one’s organization and

ensure that they stay relevant to the customer needs and wants. It’s a tool used widely to improve customer

satisfaction and loyalty so that existing customers would still retain in the company.

The information from customer satisfaction surveys help valuable insight to one’s organization to stay

relevant and to know the customer needs and wants. Customer satisfaction surveys are important tools for

updating business requirements and ensuring the customers remain with you

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

7

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

8

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part 2:

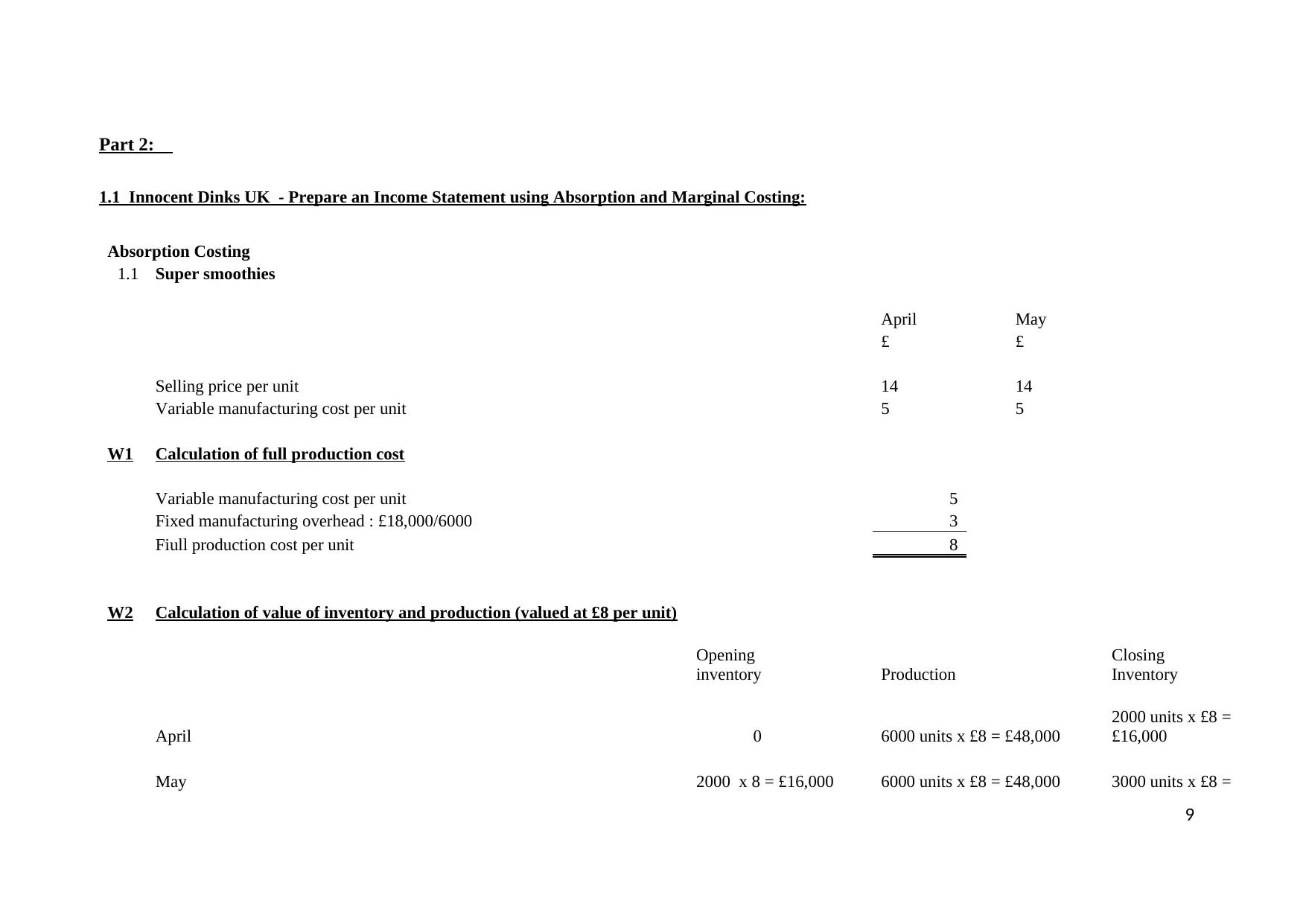

1.1 Innocent Dinks UK - Prepare an Income Statement using Absorption and Marginal Costing:

Absorption Costing

1.1 Super smoothies

April May

£ £

Selling price per unit 14 14

Variable manufacturing cost per unit 5 5

W1 Calculation of full production cost

Variable manufacturing cost per unit 5

Fixed manufacturing overhead : £18,000/6000 3

Fiull production cost per unit 8

W2 Calculation of value of inventory and production (valued at £8 per unit)

Opening

inventory Production

Closing

Inventory

April 0 6000 units x £8 = £48,000

2000 units x £8 =

£16,000

May 2000 x 8 = £16,000 6000 units x £8 = £48,000 3000 units x £8 =

9

1.1 Innocent Dinks UK - Prepare an Income Statement using Absorption and Marginal Costing:

Absorption Costing

1.1 Super smoothies

April May

£ £

Selling price per unit 14 14

Variable manufacturing cost per unit 5 5

W1 Calculation of full production cost

Variable manufacturing cost per unit 5

Fixed manufacturing overhead : £18,000/6000 3

Fiull production cost per unit 8

W2 Calculation of value of inventory and production (valued at £8 per unit)

Opening

inventory Production

Closing

Inventory

April 0 6000 units x £8 = £48,000

2000 units x £8 =

£16,000

May 2000 x 8 = £16,000 6000 units x £8 = £48,000 3000 units x £8 =

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

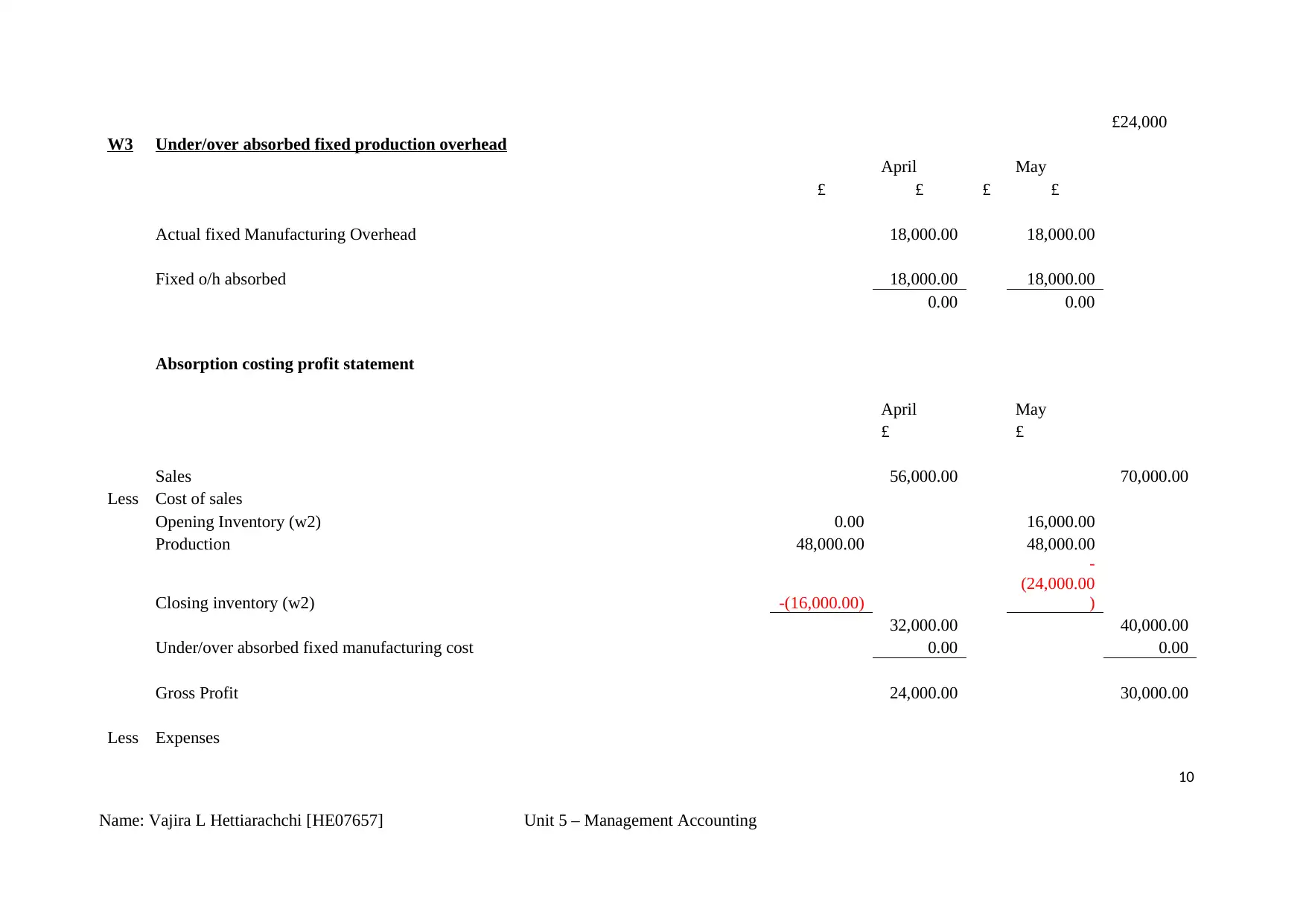

£24,000

W3 Under/over absorbed fixed production overhead

April May

£ £ £ £

Actual fixed Manufacturing Overhead 18,000.00 18,000.00

Fixed o/h absorbed 18,000.00 18,000.00

0.00 0.00

Absorption costing profit statement

April May

£ £

Sales 56,000.00 70,000.00

Less Cost of sales

Opening Inventory (w2) 0.00 16,000.00

Production 48,000.00 48,000.00

Closing inventory (w2) -(16,000.00)

-

(24,000.00

)

32,000.00 40,000.00

Under/over absorbed fixed manufacturing cost 0.00 0.00

Gross Profit 24,000.00 30,000.00

Less Expenses

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

10

W3 Under/over absorbed fixed production overhead

April May

£ £ £ £

Actual fixed Manufacturing Overhead 18,000.00 18,000.00

Fixed o/h absorbed 18,000.00 18,000.00

0.00 0.00

Absorption costing profit statement

April May

£ £

Sales 56,000.00 70,000.00

Less Cost of sales

Opening Inventory (w2) 0.00 16,000.00

Production 48,000.00 48,000.00

Closing inventory (w2) -(16,000.00)

-

(24,000.00

)

32,000.00 40,000.00

Under/over absorbed fixed manufacturing cost 0.00 0.00

Gross Profit 24,000.00 30,000.00

Less Expenses

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

10

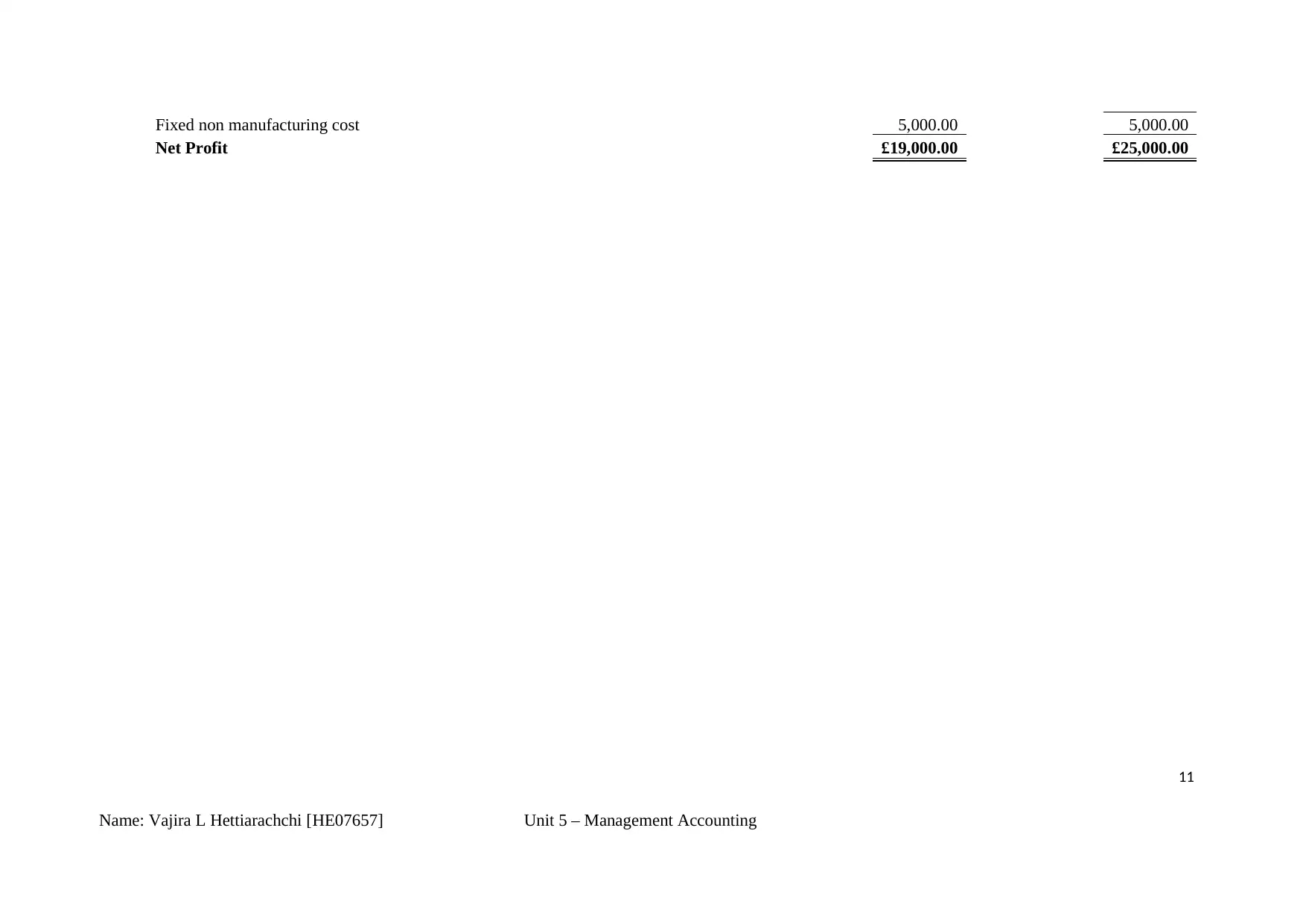

Fixed non manufacturing cost 5,000.00 5,000.00

Net Profit £19,000.00 £25,000.00

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

11

Net Profit £19,000.00 £25,000.00

Name: Vajira L Hettiarachchi [HE07657] Unit 5 – Management Accounting

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.