ACCM4200 Financial Accounting and Reporting Business Letter Report

VerifiedAdded on 2022/11/24

|10

|1993

|377

Report

AI Summary

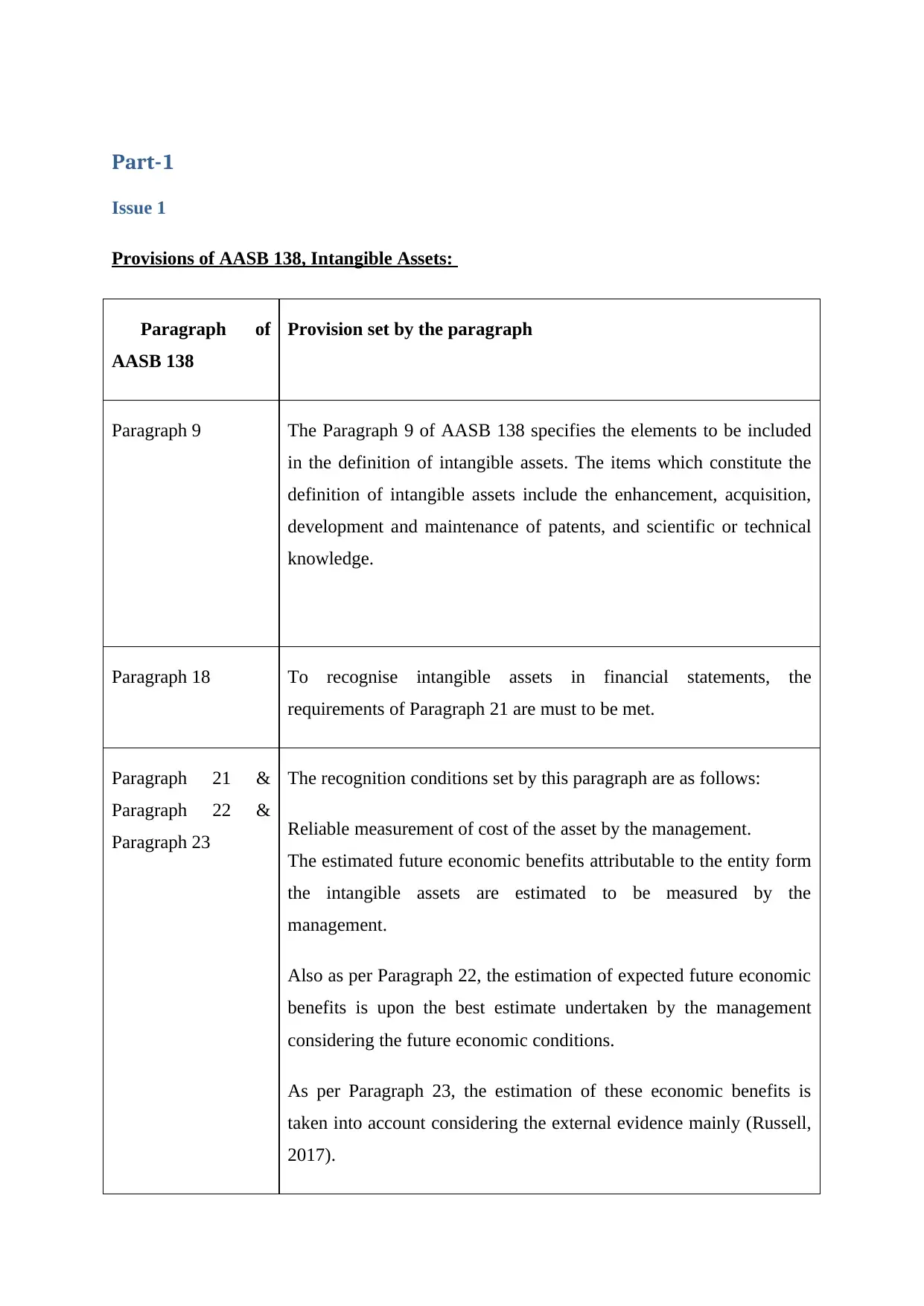

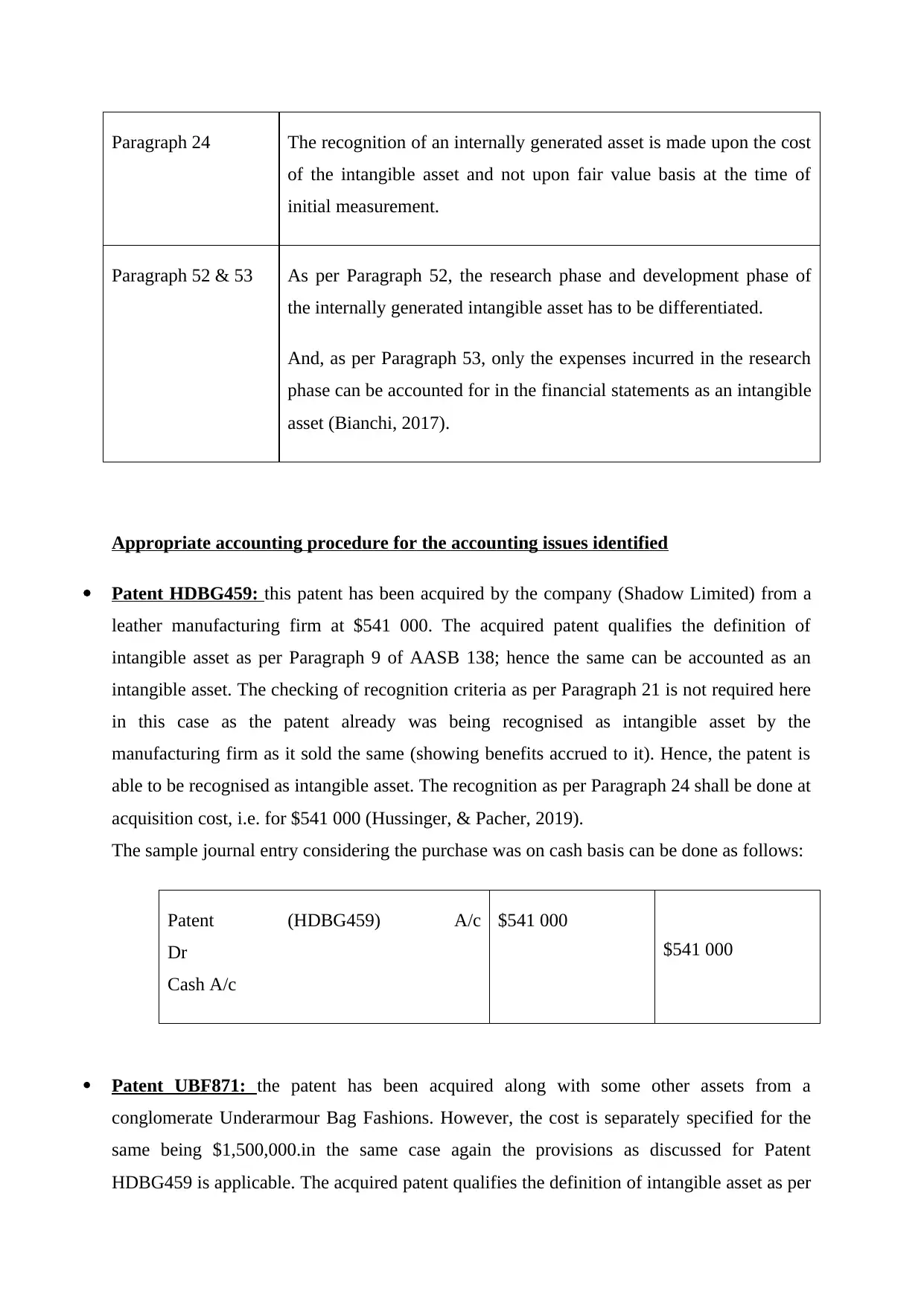

This assignment, prepared for the Financial Accounting and Reporting module (ACCM4200), analyzes two key accounting issues faced by Shadow Limited, a company dealing with intangible assets and equipment depreciation. The first issue concerns the accounting treatment of acquired and internally generated patents, referencing AASB 138 on Intangible Assets, and includes journal entries. The second issue addresses the rapid obsolescence of factory machines and explores the appropriateness of adjusting depreciation rates, considering AASB 116 on Property, Plant & Equipment, AASB 1041 on Revaluation of Non-current Assets, and AASB 136 on Impairment of Assets. The assignment culminates in a business letter from Miley Jaspen, a financial professional, to the Managing Director of Shadow Limited, providing recommendations and advice on the accounting treatments, while considering the implications of the Corporations Act 2001. The letter provides a practical application of the standards and frameworks to resolve the identified accounting issues.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.