Financial Analysis: Capital Joinery Ltd Unit 5 Management Accounting

VerifiedAdded on 2023/01/04

|17

|4751

|89

Report

AI Summary

This report delves into the realm of management accounting, focusing on its application within Capital Joinery Ltd. It begins by defining management accounting and its systems, including inventory management, cost management, price optimization, and job costing. The report then explores various management accounting reporting methods, such as inventory reports, accounts receivable aging reports, and budget reports, alongside the integration of management accounting systems and reporting within an organizational process. Furthermore, the report analyzes different management accounting techniques, including marginal costing, absorption costing, and cost-profit-volume analysis, with supporting financial statements. The report includes an interpretation of the comparison between absorption and marginal costing methods, and concludes with a discussion on variance analysis.

Unit 5 Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

SCENARIO 1..................................................................................................................................1

Understanding management accounting and its systems.............................................................1

Different methods for management accounting reporting...........................................................3

SCENARIO 2..................................................................................................................................4

Types of management accounting techniques.............................................................................4

Explaining the different planning tools used by the company for budgetary control.................8

Comparing how organisations are adapting the management accounting systems for

responding to the financial problems.........................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

SCENARIO 1..................................................................................................................................1

Understanding management accounting and its systems.............................................................1

Different methods for management accounting reporting...........................................................3

SCENARIO 2..................................................................................................................................4

Types of management accounting techniques.............................................................................4

Explaining the different planning tools used by the company for budgetary control.................8

Comparing how organisations are adapting the management accounting systems for

responding to the financial problems.........................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUTION

The management accounting (MA) refers to the process through which relevant reports

pertaining to the business operations is being prepared which assists the internal managerial team

for undertaking the business decisions. This information can be helpful in short term as well as

long term. This report is on the Capital Joinery Ltd and provides an information about the MA

and the different types MA systems and reporting which is being used in an organization.

Alongside, the application of MA techniques for carrying out the cost analysis and implication of

planning tools for establishing the budgetary control.It also covers the identifying the tools

through which financial problems business is facing can be determining and a comparative

analysis of the MA systems being utilized by the companies for overcoming its financial issues

and attain sustainable success.

SCENARIO 1

Understanding management accounting and its systems

According to the Institute of Management Accountants, which describes the management

accountant as the profession which incorporates the functions like planning, performance

management, offering expertise services and implementing the strategy for the assisting the

management in achieve its goals.

Principles of management accounting

Accuracy: This means that the financial information available should be accurate in order to take

informed and right decision by the CJL.

UpToDate: The data should be updated from time to time for increasing its relevance for

undertaking decisions by the user of these information of CL.

Reliability:Every information should be reliable and this can be proved by the source document

or evidence. This is very vital for CJL for ensuring reliability.

Truth worthy:the data should be obtained from the reliable and trusted sources in order to avoid

any error or inaccurate information which is important for an organization like CJL.

Future planning: The financial information provided is helpful in undertaking various business

decisions which is significant for CJL and also helps in taking decisions for future.

Types of management accounting system

Inventory management system

1

The management accounting (MA) refers to the process through which relevant reports

pertaining to the business operations is being prepared which assists the internal managerial team

for undertaking the business decisions. This information can be helpful in short term as well as

long term. This report is on the Capital Joinery Ltd and provides an information about the MA

and the different types MA systems and reporting which is being used in an organization.

Alongside, the application of MA techniques for carrying out the cost analysis and implication of

planning tools for establishing the budgetary control.It also covers the identifying the tools

through which financial problems business is facing can be determining and a comparative

analysis of the MA systems being utilized by the companies for overcoming its financial issues

and attain sustainable success.

SCENARIO 1

Understanding management accounting and its systems

According to the Institute of Management Accountants, which describes the management

accountant as the profession which incorporates the functions like planning, performance

management, offering expertise services and implementing the strategy for the assisting the

management in achieve its goals.

Principles of management accounting

Accuracy: This means that the financial information available should be accurate in order to take

informed and right decision by the CJL.

UpToDate: The data should be updated from time to time for increasing its relevance for

undertaking decisions by the user of these information of CL.

Reliability:Every information should be reliable and this can be proved by the source document

or evidence. This is very vital for CJL for ensuring reliability.

Truth worthy:the data should be obtained from the reliable and trusted sources in order to avoid

any error or inaccurate information which is important for an organization like CJL.

Future planning: The financial information provided is helpful in undertaking various business

decisions which is significant for CJL and also helps in taking decisions for future.

Types of management accounting system

Inventory management system

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This system is being used by the management for the purpose of managing the inventory

of the business. This system helps in keeping track of the movement of the inventory from one

process of production to another. The process continues till the good is delivered to the client on

the specified time and quantity (Atieh and et.al., 2016). This MA system is mostly crucial for

Capital Joinery Ltd which is having an extensive and complex supply chain which makes it

difficult for the company to handle it keep record of it on a manual basis. Thus, this system is

essential in order to efficiently handling the stock level of the products.

Benefits:

It helps in keeping track of the stocks and helps in reducing the error.

It additionally assists in determining the reorder point and quantity required to avoid the

situation of over and under stocking.

This system can be utilized in making estimation about the future demand and trends.

Application:

It is useful for all types of business entities and can be implemented by Capital Joinery

Ltd. for effectively managing its stock.

Cost management system

Under this MA system, the various types of costs are being monitored which can be

defined as the expected cost which will be incurred in order to produce the required quantity of

products (Kostyukova and et.al., 2018). It is useful for the business entity in identifying and

understanding the cost of various product which is important for setting the price of the

product.This is essential for Capital Joinery Ltd because it help in managing the cost in a better

way in order to maximise the profits.

Benefits:

This approach supports in computing the profit or loss associated with the product and

the productiveness of the production procedures being used.

It helps in exercising control over the product cost so that wastage and unnecessary

expense can be avoided.

Also, it provides information about the productive and non-productive activities.

Application:

Application of it will support Capital Joinery Ltd. in determining the cost of each product

which will help in fixing price of it.

2

of the business. This system helps in keeping track of the movement of the inventory from one

process of production to another. The process continues till the good is delivered to the client on

the specified time and quantity (Atieh and et.al., 2016). This MA system is mostly crucial for

Capital Joinery Ltd which is having an extensive and complex supply chain which makes it

difficult for the company to handle it keep record of it on a manual basis. Thus, this system is

essential in order to efficiently handling the stock level of the products.

Benefits:

It helps in keeping track of the stocks and helps in reducing the error.

It additionally assists in determining the reorder point and quantity required to avoid the

situation of over and under stocking.

This system can be utilized in making estimation about the future demand and trends.

Application:

It is useful for all types of business entities and can be implemented by Capital Joinery

Ltd. for effectively managing its stock.

Cost management system

Under this MA system, the various types of costs are being monitored which can be

defined as the expected cost which will be incurred in order to produce the required quantity of

products (Kostyukova and et.al., 2018). It is useful for the business entity in identifying and

understanding the cost of various product which is important for setting the price of the

product.This is essential for Capital Joinery Ltd because it help in managing the cost in a better

way in order to maximise the profits.

Benefits:

This approach supports in computing the profit or loss associated with the product and

the productiveness of the production procedures being used.

It helps in exercising control over the product cost so that wastage and unnecessary

expense can be avoided.

Also, it provides information about the productive and non-productive activities.

Application:

Application of it will support Capital Joinery Ltd. in determining the cost of each product

which will help in fixing price of it.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price optimization system

In this MA system, price is decided after considering the willingness of the consumers for

buying that product. This is based on the demand of the product in the market; thus, the price is

set in such a way that it helps the businesses in attaining the maximum profit (Wang and Wang,

2017).This system is essential for Capital Joinery Ltd in order to set the product price taking into

consideration important factors.

Benefits:

It is based on market demand and customer willingness.

Helps in attaining the maximum profitability.

Also, it reduces the manual errors and in optimization of the process.

Application:

It will help Capital Joinery Ltd. in effectively appropriately setting the price of its

product.

Job costing system

This system is useful when the goods are being produced as per the specification of the

clients. Through this system, an organization in easily identify or compute the cost which will be

incurred pertaining to the specific product (Ahmad, 2017). It is essential in case of the

companylike Capital Joinery Ltdis involved into production of multiple products where the cost

and profit associated with each such activity is required to be determined.

Benefits:

By determining the cost for each job helps in exercising cost control approaches.

It helps in easily determining the wastage or not so necessary activity.

Also, helps in knowing the profits under each job separately.

Application:

This will support the company in computing the cost and profits for each type of product

created by it.

Different methods for management accounting reporting

MA reporting helps the management in getting an insight into the business functioning

andthe performance and along with this, it provides assistance in identifying the weaker areas of

the business where it requires to put more focus. Some of the important MA reporting system is

explained below.

3

In this MA system, price is decided after considering the willingness of the consumers for

buying that product. This is based on the demand of the product in the market; thus, the price is

set in such a way that it helps the businesses in attaining the maximum profit (Wang and Wang,

2017).This system is essential for Capital Joinery Ltd in order to set the product price taking into

consideration important factors.

Benefits:

It is based on market demand and customer willingness.

Helps in attaining the maximum profitability.

Also, it reduces the manual errors and in optimization of the process.

Application:

It will help Capital Joinery Ltd. in effectively appropriately setting the price of its

product.

Job costing system

This system is useful when the goods are being produced as per the specification of the

clients. Through this system, an organization in easily identify or compute the cost which will be

incurred pertaining to the specific product (Ahmad, 2017). It is essential in case of the

companylike Capital Joinery Ltdis involved into production of multiple products where the cost

and profit associated with each such activity is required to be determined.

Benefits:

By determining the cost for each job helps in exercising cost control approaches.

It helps in easily determining the wastage or not so necessary activity.

Also, helps in knowing the profits under each job separately.

Application:

This will support the company in computing the cost and profits for each type of product

created by it.

Different methods for management accounting reporting

MA reporting helps the management in getting an insight into the business functioning

andthe performance and along with this, it provides assistance in identifying the weaker areas of

the business where it requires to put more focus. Some of the important MA reporting system is

explained below.

3

Inventory report

This report provides the information pertaining to the current inventory levelof the

Capital Joinery Ltd(Maas, Schaltegger and Crutzen, 2016). This supports the management in

undertaking decision in regard to how much stock should to reordered and at what time which

will assist in overcoming the circumstances of less or more stocking. Through this report, the

company can also make forecasting about the future requirements.

Account Receivable Aging report

This report is very important for the businesses which provides goods on credit to its

customers. It includes compete details about the customers like date and time of sales, credit

period provided and so forth. This helps the organization in determining the account details of

the customers which also leads to gathering information about the ability of the customer repays

back (Pylypenko and Tyvonchuk, 2020). Therefore, it results into making management of

Capital Joinery Ltdaware of the chances of default that may arise so that they can have

arrangement for the same. It can also help inmaking changes in the organization’s credit policy

in order to overcomethe situation.

Budget report

It refers to the formal statement which incorporates the expected income and expenses of

the business pertaining to the future period for which the report is prepared. Under this, the

actual outcome or the performance is compared with the budgeted one and in case, if there is any

major deviation in the outcome the remedial steps are being undertaken for reducing such

difference (Erokhin and et.al., 2019). Through this report, the management of Capital Joinery Ltd

can analyze the expenditure and income which will help them in gaining insight about the causes

of it so that they implement strategy in order to grab control over the unnecessary expenditure

along with the increase the income level.This report differs from one year to another and

organization to organization.

Integration of MA system and reporting in the organizational process

By integrating the MA system and reporting will provide support to the company in

achieving its desired goals and objectives in an effective way.Through this way, the management

will be able to effectively deal with its business activities and managing its performance with

easy availability of the requirement by the way of MA reporting system. it helps in identifying

4

This report provides the information pertaining to the current inventory levelof the

Capital Joinery Ltd(Maas, Schaltegger and Crutzen, 2016). This supports the management in

undertaking decision in regard to how much stock should to reordered and at what time which

will assist in overcoming the circumstances of less or more stocking. Through this report, the

company can also make forecasting about the future requirements.

Account Receivable Aging report

This report is very important for the businesses which provides goods on credit to its

customers. It includes compete details about the customers like date and time of sales, credit

period provided and so forth. This helps the organization in determining the account details of

the customers which also leads to gathering information about the ability of the customer repays

back (Pylypenko and Tyvonchuk, 2020). Therefore, it results into making management of

Capital Joinery Ltdaware of the chances of default that may arise so that they can have

arrangement for the same. It can also help inmaking changes in the organization’s credit policy

in order to overcomethe situation.

Budget report

It refers to the formal statement which incorporates the expected income and expenses of

the business pertaining to the future period for which the report is prepared. Under this, the

actual outcome or the performance is compared with the budgeted one and in case, if there is any

major deviation in the outcome the remedial steps are being undertaken for reducing such

difference (Erokhin and et.al., 2019). Through this report, the management of Capital Joinery Ltd

can analyze the expenditure and income which will help them in gaining insight about the causes

of it so that they implement strategy in order to grab control over the unnecessary expenditure

along with the increase the income level.This report differs from one year to another and

organization to organization.

Integration of MA system and reporting in the organizational process

By integrating the MA system and reporting will provide support to the company in

achieving its desired goals and objectives in an effective way.Through this way, the management

will be able to effectively deal with its business activities and managing its performance with

easy availability of the requirement by the way of MA reporting system. it helps in identifying

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the areas of improvement so that appropriate actions and decisions can be undertaken to

implementing the strategy.

SCENARIO 2

Types of management accounting techniques

The MA techniques are being used by the businesses for the purpose of analysing the cost

of the product and this analysis can be carrying out on the different techniques as per the

requirement of the business.

Marginal costing: This MA technique is very helpful to the management in which the

variable cost is being charges to the cost of product while the fixed cost is taken completely for

the period (Marginal Costing: Meaning and Features. 2020). This method helps in ascertaining

the marginal cost along with the impact on the profit in regard to the differentiating the cost into

fixed and variable.This is based upon the cost behavior and is useful in ascertaining the break-

even point as well.

Absorption costing: It is technique in which the cost is accumulated and allocated to the

individual products (Absorption Costing. 2020). Both the cost fixed and variable in

determination of the cost of product. This approach is also needed by the accounting standards

for the purpose of creating inventory valuation. This type of costing is useful in for the income

tax purpose also.

Cost profit volume analysis: This analysis is used for knowing the impact of change in

the costs along with the volume of sales which results into affecting the profits of the company

(Navaneetha and et.al., 2017).Through this, the company can get a better information about the

performance by determining how many units can be sold to attain the situation of break even or

the margin of safety.

Applying management accounting techniques and producing appropriate financial

reporting documents

Income statement as per Absorption Costing

Particulars May June

Sales Revenue (100*250)

2500

0 (75*250)

1875

0

Cost of Sales

Direct Materials (100*60) 6000 (80*60) 4800

Direct Labour (100*40) 4000 (80*40) 3200

5

implementing the strategy.

SCENARIO 2

Types of management accounting techniques

The MA techniques are being used by the businesses for the purpose of analysing the cost

of the product and this analysis can be carrying out on the different techniques as per the

requirement of the business.

Marginal costing: This MA technique is very helpful to the management in which the

variable cost is being charges to the cost of product while the fixed cost is taken completely for

the period (Marginal Costing: Meaning and Features. 2020). This method helps in ascertaining

the marginal cost along with the impact on the profit in regard to the differentiating the cost into

fixed and variable.This is based upon the cost behavior and is useful in ascertaining the break-

even point as well.

Absorption costing: It is technique in which the cost is accumulated and allocated to the

individual products (Absorption Costing. 2020). Both the cost fixed and variable in

determination of the cost of product. This approach is also needed by the accounting standards

for the purpose of creating inventory valuation. This type of costing is useful in for the income

tax purpose also.

Cost profit volume analysis: This analysis is used for knowing the impact of change in

the costs along with the volume of sales which results into affecting the profits of the company

(Navaneetha and et.al., 2017).Through this, the company can get a better information about the

performance by determining how many units can be sold to attain the situation of break even or

the margin of safety.

Applying management accounting techniques and producing appropriate financial

reporting documents

Income statement as per Absorption Costing

Particulars May June

Sales Revenue (100*250)

2500

0 (75*250)

1875

0

Cost of Sales

Direct Materials (100*60) 6000 (80*60) 4800

Direct Labour (100*40) 4000 (80*40) 3200

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variable Production Overheads (100*20) 2000 (80*20) 1600

Fixed production overheads (100*20) 2000 (80*20) 1600

1400

0

1120

0

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5*140) 700

(Under)/over absorbed Fixed prod o/h 0 (2000 - (80*20)) -400

1400

0

1090

0

Gross profit

1100

0 7850

Fixed selling 1000 1000

Fixed administration cost 3000 3000

Variable sales commission (25000*2%) 500 (18750*2%) 375

Net Income 6500 3475

Income statement as per Marginal Costing

Particulars May June

Sales Revenue (100*250) 25000 (75*250) 18750

Marginal Cost of Sales

Direct Materials (100*60) 6000 (80*60) 4800

Direct Labour (100*40) 4000 (80*40) 3200

Variable sales commission (25000*2%) 500 (18750*2%) 375

Variable Production Overheads (100*20) 2000 (80*20) 1600

12500 9975

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5*120) 600

12500 9375

Contribution 12500 9375

Fixed production overheads 2000 2000

Fixed selling cost 1000 1000

Fixed administration cost 3000 3000

6

Fixed production overheads (100*20) 2000 (80*20) 1600

1400

0

1120

0

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5*140) 700

(Under)/over absorbed Fixed prod o/h 0 (2000 - (80*20)) -400

1400

0

1090

0

Gross profit

1100

0 7850

Fixed selling 1000 1000

Fixed administration cost 3000 3000

Variable sales commission (25000*2%) 500 (18750*2%) 375

Net Income 6500 3475

Income statement as per Marginal Costing

Particulars May June

Sales Revenue (100*250) 25000 (75*250) 18750

Marginal Cost of Sales

Direct Materials (100*60) 6000 (80*60) 4800

Direct Labour (100*40) 4000 (80*40) 3200

Variable sales commission (25000*2%) 500 (18750*2%) 375

Variable Production Overheads (100*20) 2000 (80*20) 1600

12500 9975

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5*120) 600

12500 9375

Contribution 12500 9375

Fixed production overheads 2000 2000

Fixed selling cost 1000 1000

Fixed administration cost 3000 3000

6

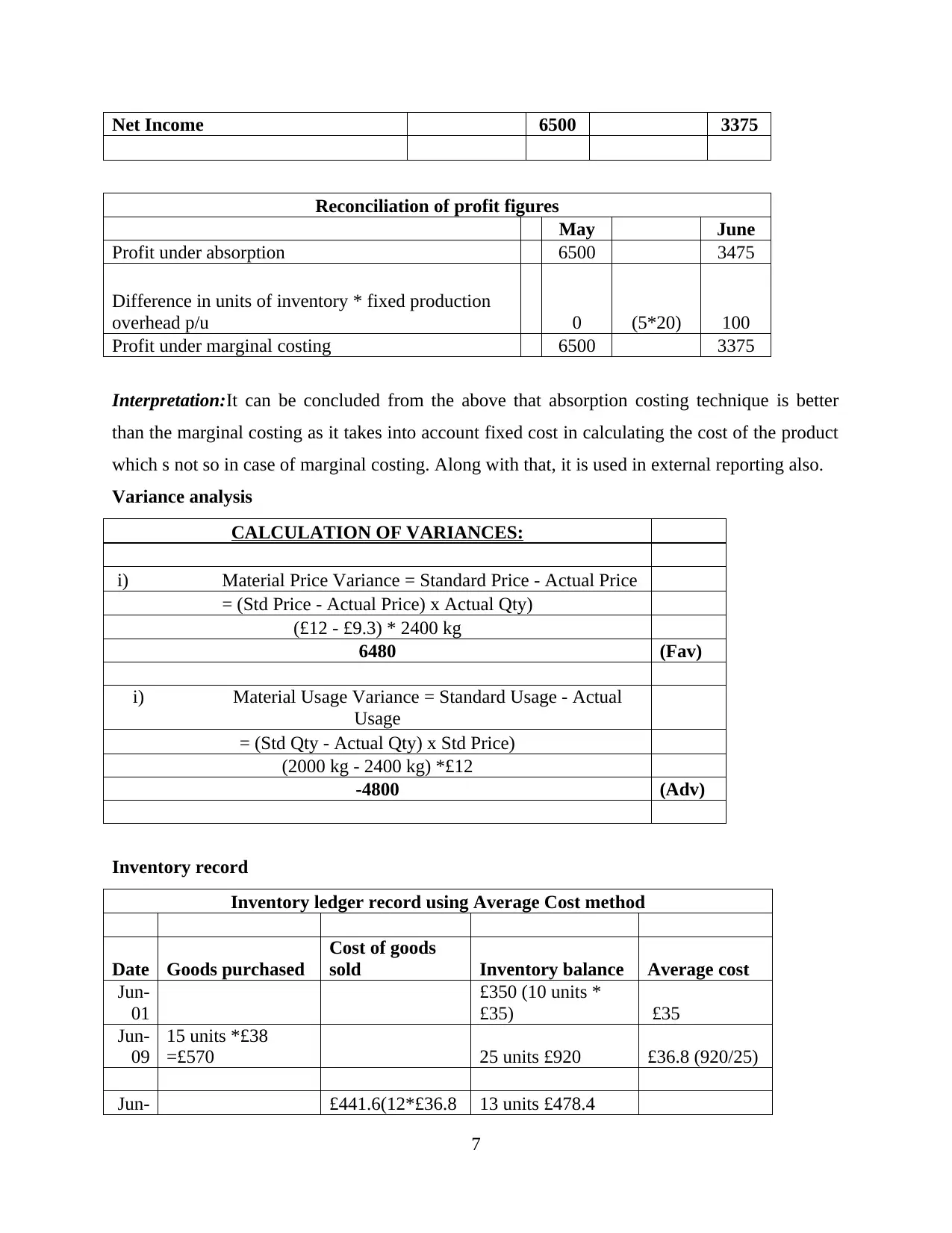

Net Income 6500 3375

Reconciliation of profit figures

May June

Profit under absorption 6500 3475

Difference in units of inventory * fixed production

overhead p/u 0 (5*20) 100

Profit under marginal costing 6500 3375

Interpretation:It can be concluded from the above that absorption costing technique is better

than the marginal costing as it takes into account fixed cost in calculating the cost of the product

which s not so in case of marginal costing. Along with that, it is used in external reporting also.

Variance analysis

CALCULATION OF VARIANCES:

i) Material Price Variance = Standard Price - Actual Price

= (Std Price - Actual Price) x Actual Qty)

(£12 - £9.3) * 2400 kg

6480 (Fav)

i) Material Usage Variance = Standard Usage - Actual

Usage

= (Std Qty - Actual Qty) x Std Price)

(2000 kg - 2400 kg) *£12

-4800 (Adv)

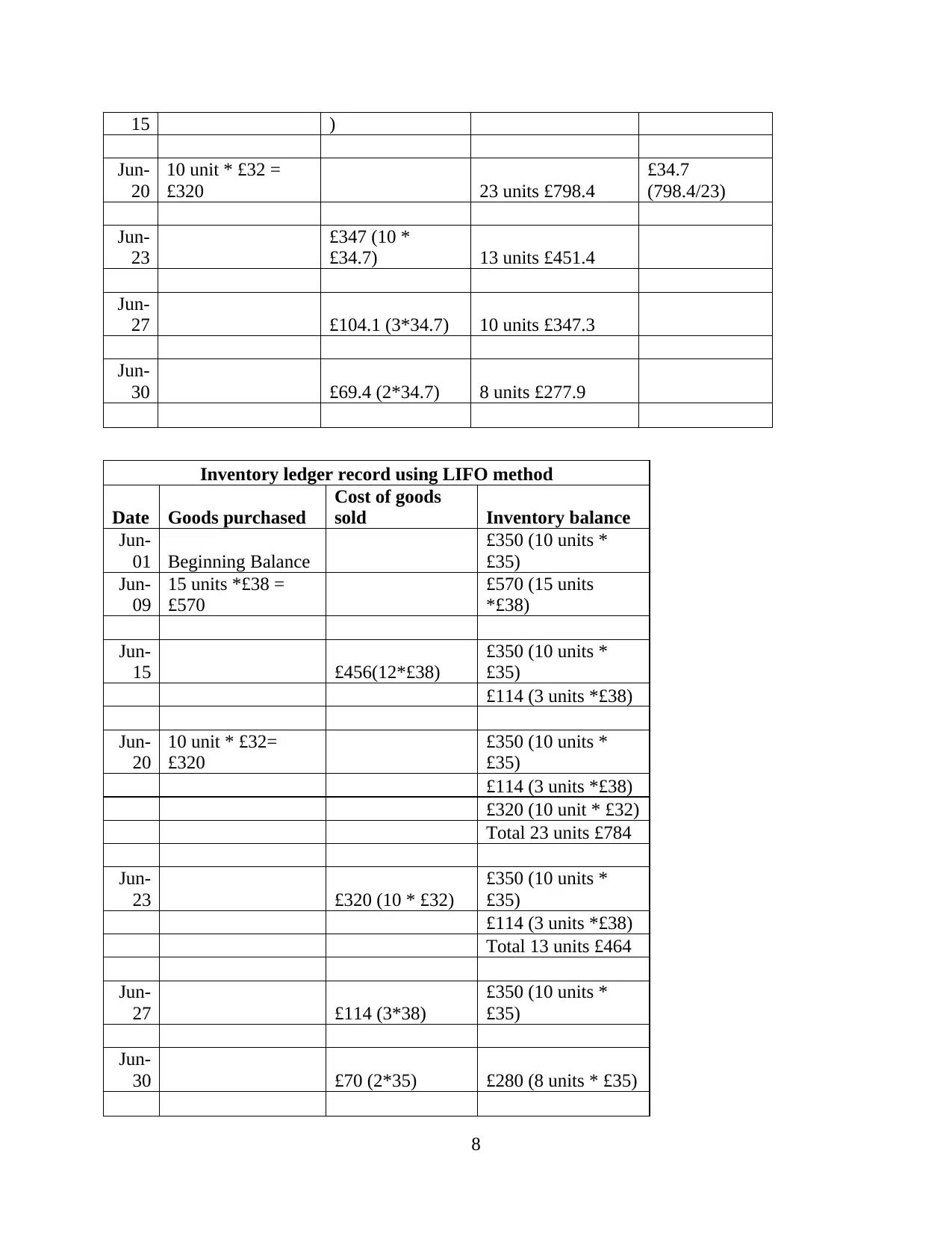

Inventory record

Inventory ledger record using Average Cost method

Date Goods purchased

Cost of goods

sold Inventory balance Average cost

Jun-

01

£350 (10 units *

£35) £35

Jun-

09

15 units *£38

=£570 25 units £920 £36.8 (920/25)

Jun- £441.6(12*£36.8 13 units £478.4

7

Reconciliation of profit figures

May June

Profit under absorption 6500 3475

Difference in units of inventory * fixed production

overhead p/u 0 (5*20) 100

Profit under marginal costing 6500 3375

Interpretation:It can be concluded from the above that absorption costing technique is better

than the marginal costing as it takes into account fixed cost in calculating the cost of the product

which s not so in case of marginal costing. Along with that, it is used in external reporting also.

Variance analysis

CALCULATION OF VARIANCES:

i) Material Price Variance = Standard Price - Actual Price

= (Std Price - Actual Price) x Actual Qty)

(£12 - £9.3) * 2400 kg

6480 (Fav)

i) Material Usage Variance = Standard Usage - Actual

Usage

= (Std Qty - Actual Qty) x Std Price)

(2000 kg - 2400 kg) *£12

-4800 (Adv)

Inventory record

Inventory ledger record using Average Cost method

Date Goods purchased

Cost of goods

sold Inventory balance Average cost

Jun-

01

£350 (10 units *

£35) £35

Jun-

09

15 units *£38

=£570 25 units £920 £36.8 (920/25)

Jun- £441.6(12*£36.8 13 units £478.4

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

15 )

Jun-

20

10 unit * £32 =

£320 23 units £798.4

£34.7

(798.4/23)

Jun-

23

£347 (10 *

£34.7) 13 units £451.4

Jun-

27 £104.1 (3*34.7) 10 units £347.3

Jun-

30 £69.4 (2*34.7) 8 units £277.9

Inventory ledger record using LIFO method

Date Goods purchased

Cost of goods

sold Inventory balance

Jun-

01 Beginning Balance

£350 (10 units *

£35)

Jun-

09

15 units *£38 =

£570

£570 (15 units

*£38)

Jun-

15 £456(12*£38)

£350 (10 units *

£35)

£114 (3 units *£38)

Jun-

20

10 unit * £32=

£320

£350 (10 units *

£35)

£114 (3 units *£38)

£320 (10 unit * £32)

Total 23 units £784

Jun-

23 £320 (10 * £32)

£350 (10 units *

£35)

£114 (3 units *£38)

Total 13 units £464

Jun-

27 £114 (3*38)

£350 (10 units *

£35)

Jun-

30 £70 (2*35) £280 (8 units * £35)

8

Jun-

20

10 unit * £32 =

£320 23 units £798.4

£34.7

(798.4/23)

Jun-

23

£347 (10 *

£34.7) 13 units £451.4

Jun-

27 £104.1 (3*34.7) 10 units £347.3

Jun-

30 £69.4 (2*34.7) 8 units £277.9

Inventory ledger record using LIFO method

Date Goods purchased

Cost of goods

sold Inventory balance

Jun-

01 Beginning Balance

£350 (10 units *

£35)

Jun-

09

15 units *£38 =

£570

£570 (15 units

*£38)

Jun-

15 £456(12*£38)

£350 (10 units *

£35)

£114 (3 units *£38)

Jun-

20

10 unit * £32=

£320

£350 (10 units *

£35)

£114 (3 units *£38)

£320 (10 unit * £32)

Total 23 units £784

Jun-

23 £320 (10 * £32)

£350 (10 units *

£35)

£114 (3 units *£38)

Total 13 units £464

Jun-

27 £114 (3*38)

£350 (10 units *

£35)

Jun-

30 £70 (2*35) £280 (8 units * £35)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation:It can be inferred that the value of stock at the end of the month in case of average

cost method is 8 units for £277.9, that is, per unit cost is £34.7 while in the LIFO method, the

inventory value is £280 (8 units * £35). This means that under LIFO method value is high.

Explaining the different planning tools used by the company for budgetary control

Budgeting refers to planning or creating a budget that is also called spending plan of the

organisation. It is prepared after considering factors that could influence the budget and

operations of business. It is an effective planning which is used for analysing the requirements of

business based on trends or previous budgets and making appropriate allocation of the resources

between different departments of company. It is aimed at balancing the expenditures of the

business so that adequate profits could be earned by the company. Budgetary control could be

described as process which is used for preparing budgets for future period and comparing the

budgets with actual performances of the company(Abdusalomova, 2019). The comparison with

actual output helps n identifying the variances or differences between the two. Based over these

differences management or organisation makes corrective measures to reduce these differences

and achieve greater level of efficiency and effectiveness. There are different budgeting tools

which are used as planning tool by the organisations and to achieve the organisational goals and

objectives.

Zero Based Budgeting

It is a budgeting approach for making budget from the scratch. ZBB do not involve

making budget using the previous budgets’ information or data. Every time the budget is

prepared detailed analysis of the different factors associated with the budget are assessed that

could influence the budget and operations of the departments. The budget requires the

management to justify each expense that is added to budget. Main motive of budget is of

reducing the spending of company by assessing every time where the costs could be reduced or

be controlled. Management could involve the employees in identifying the activities that are seen

to have maximum changes so that they could be assessed.

Advantages

It is prepared after analysing the business goals and objectives of the business. It is prepared

from the scratch every time that reduces the chances of discrepancies to be carried forward.

9

cost method is 8 units for £277.9, that is, per unit cost is £34.7 while in the LIFO method, the

inventory value is £280 (8 units * £35). This means that under LIFO method value is high.

Explaining the different planning tools used by the company for budgetary control

Budgeting refers to planning or creating a budget that is also called spending plan of the

organisation. It is prepared after considering factors that could influence the budget and

operations of business. It is an effective planning which is used for analysing the requirements of

business based on trends or previous budgets and making appropriate allocation of the resources

between different departments of company. It is aimed at balancing the expenditures of the

business so that adequate profits could be earned by the company. Budgetary control could be

described as process which is used for preparing budgets for future period and comparing the

budgets with actual performances of the company(Abdusalomova, 2019). The comparison with

actual output helps n identifying the variances or differences between the two. Based over these

differences management or organisation makes corrective measures to reduce these differences

and achieve greater level of efficiency and effectiveness. There are different budgeting tools

which are used as planning tool by the organisations and to achieve the organisational goals and

objectives.

Zero Based Budgeting

It is a budgeting approach for making budget from the scratch. ZBB do not involve

making budget using the previous budgets’ information or data. Every time the budget is

prepared detailed analysis of the different factors associated with the budget are assessed that

could influence the budget and operations of the departments. The budget requires the

management to justify each expense that is added to budget. Main motive of budget is of

reducing the spending of company by assessing every time where the costs could be reduced or

be controlled. Management could involve the employees in identifying the activities that are seen

to have maximum changes so that they could be assessed.

Advantages

It is prepared after analysing the business goals and objectives of the business. It is prepared

from the scratch every time that reduces the chances of discrepancies to be carried forward.

9

The budget requires justification for every new expense added in the budget. It is useful for

the business or activities where more changes are seen.

Disadvantages

The budget is very expensive and time consuming. It is not suitable for all the business due to

long process. The time of managers could not be productively applied elsewhere.

Activity Based Budgeting

The budget approach is used in the cost accounting. The budget is prepared based on the

activities to be performed in the process. It also involves recording, researching and analysing

the activities that incurs cost for the company. In this approach the managers assess and

scrutinises the potential ways of creating efficiencies. Management also analyses the past budget

and the spending propositions for preparing the budget for current year ((Burritt and et.al., 2019)

). Based on the information from previous budgets and research of activities the budgets

are prepared by the management. The budget has proved to be very useful for the business

organisation for making allocation of different users.

Advantages

The budget makes research over activities for preparing the budget unlike traditional method

of budgeting. The budget has been very useful for the organisation that has various activities

or processes. It helps in assessing the cost and expenses of every budget so that appropriate

allocation of the resources. It helps in increasing the profit levels by controlling the costs.

Disadvantages

The budget is time consuming and expensive as assessing every activity involves time. The

process required professional knowledge to carry out the processes. The budget is suitable

only for companies that have multiple processes or activities going at the same time or

simultaneously.

Incremental Budgeting

The budgeting refers to type of the budgeting process which are based over idea that new

budget could be prepared by doing some marginal changes to previous budgets. In incremental

budget the budget of current year is taken as the based to whom incremental assumptions after

10

the business or activities where more changes are seen.

Disadvantages

The budget is very expensive and time consuming. It is not suitable for all the business due to

long process. The time of managers could not be productively applied elsewhere.

Activity Based Budgeting

The budget approach is used in the cost accounting. The budget is prepared based on the

activities to be performed in the process. It also involves recording, researching and analysing

the activities that incurs cost for the company. In this approach the managers assess and

scrutinises the potential ways of creating efficiencies. Management also analyses the past budget

and the spending propositions for preparing the budget for current year ((Burritt and et.al., 2019)

). Based on the information from previous budgets and research of activities the budgets

are prepared by the management. The budget has proved to be very useful for the business

organisation for making allocation of different users.

Advantages

The budget makes research over activities for preparing the budget unlike traditional method

of budgeting. The budget has been very useful for the organisation that has various activities

or processes. It helps in assessing the cost and expenses of every budget so that appropriate

allocation of the resources. It helps in increasing the profit levels by controlling the costs.

Disadvantages

The budget is time consuming and expensive as assessing every activity involves time. The

process required professional knowledge to carry out the processes. The budget is suitable

only for companies that have multiple processes or activities going at the same time or

simultaneously.

Incremental Budgeting

The budgeting refers to type of the budgeting process which are based over idea that new

budget could be prepared by doing some marginal changes to previous budgets. In incremental

budget the budget of current year is taken as the based to whom incremental assumptions after

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.