ACCM4200 Financial Accounting and Reporting: Technical Issue Report

VerifiedAdded on 2022/10/03

|7

|664

|75

Report

AI Summary

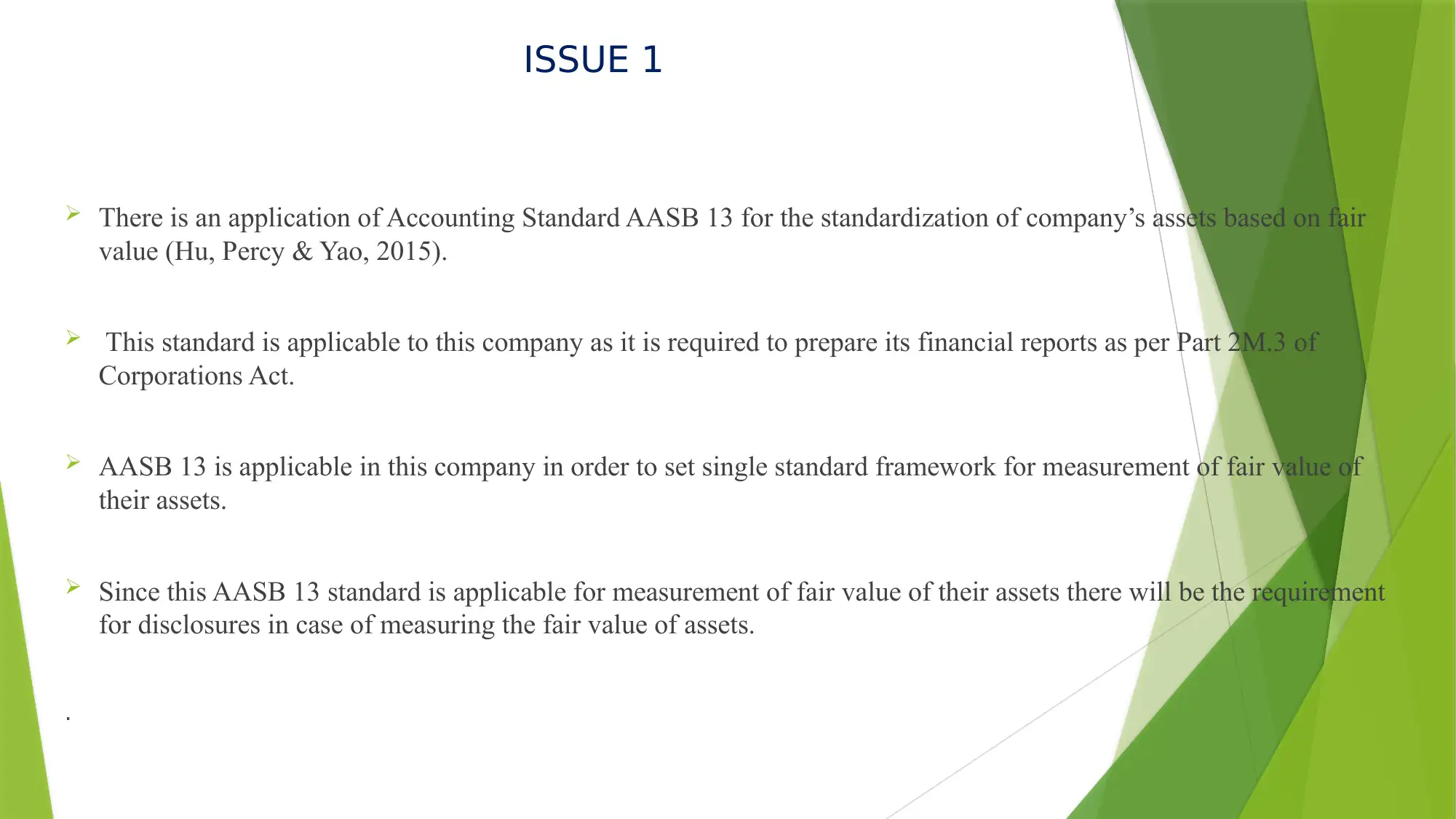

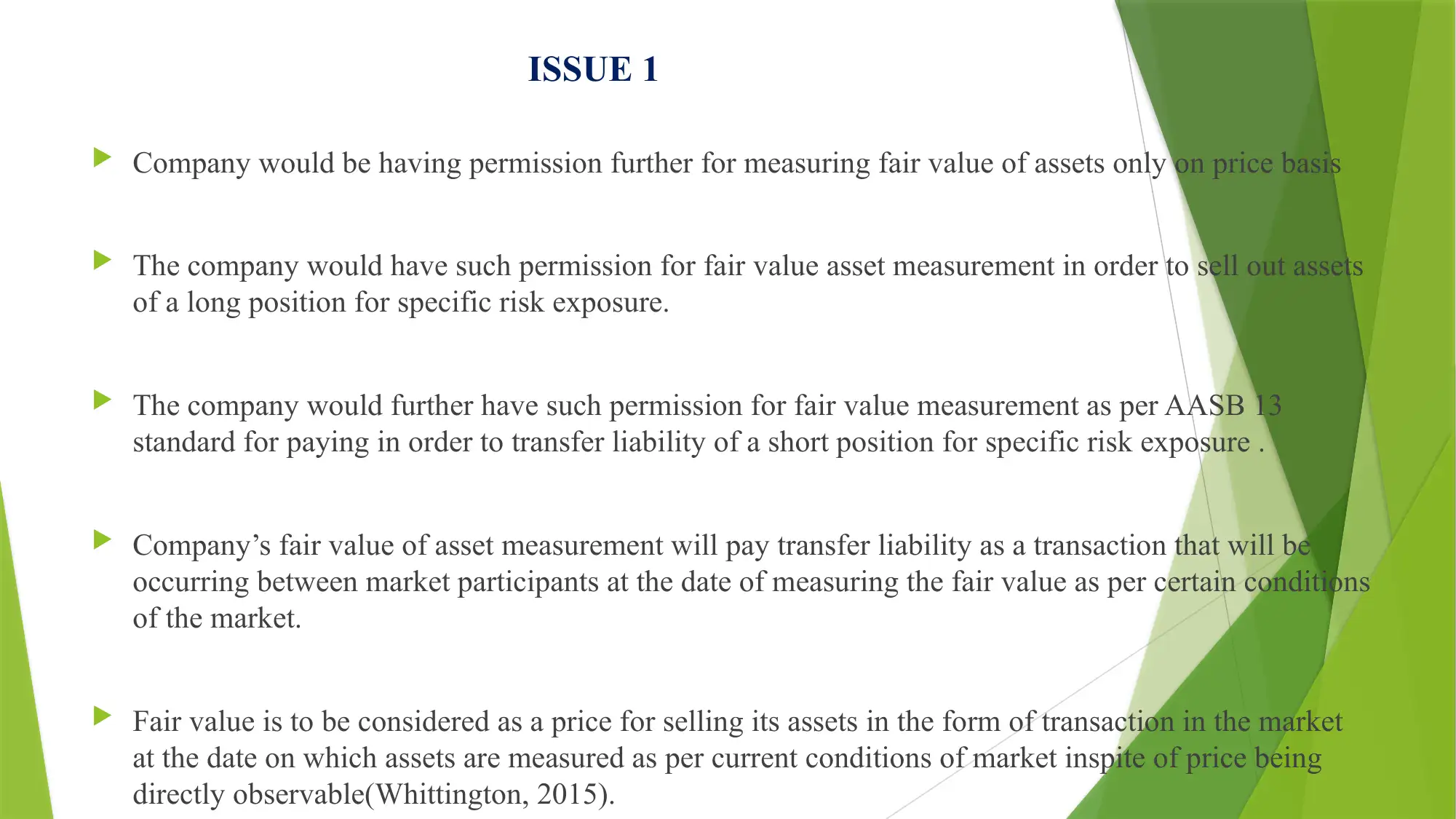

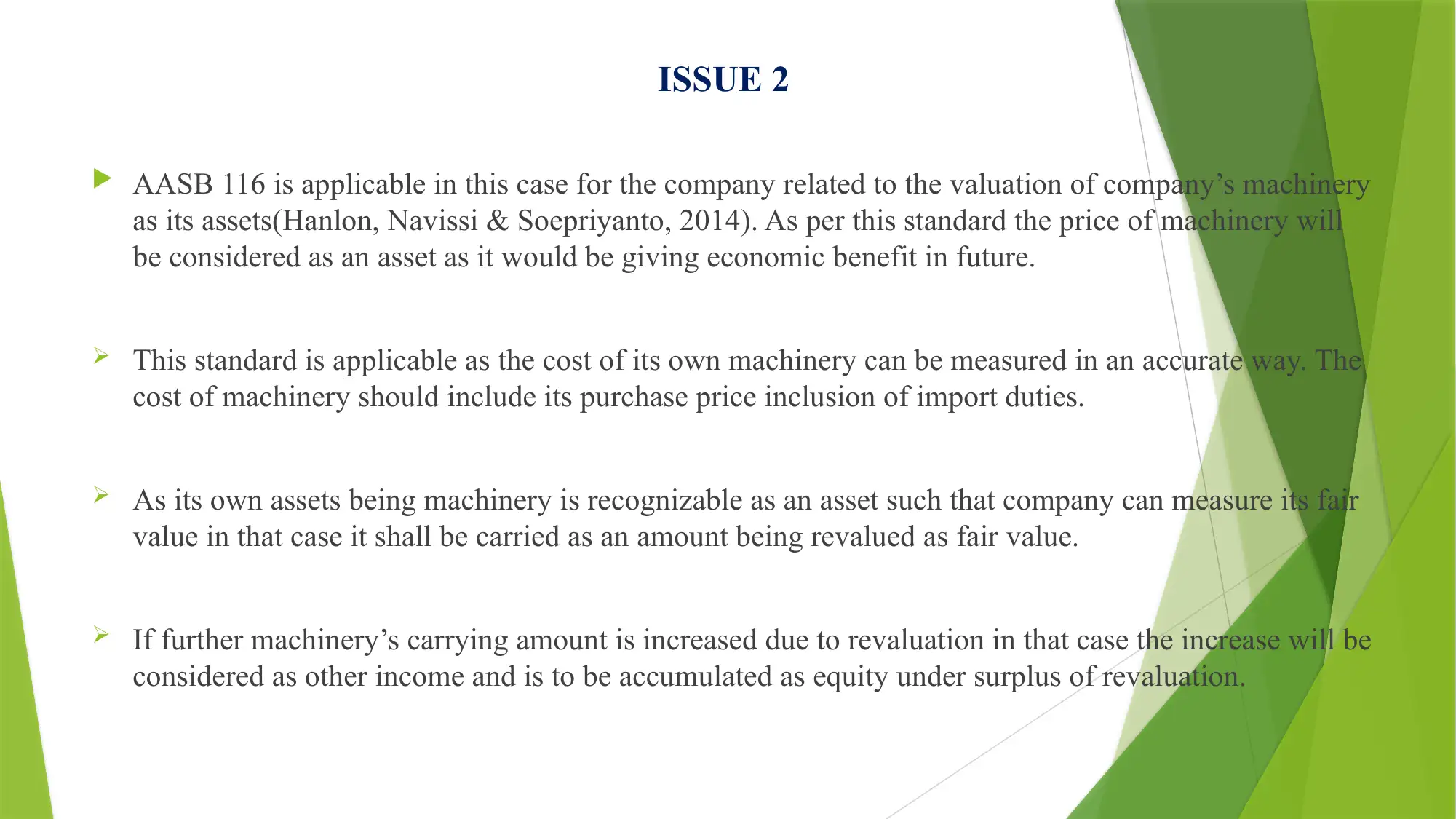

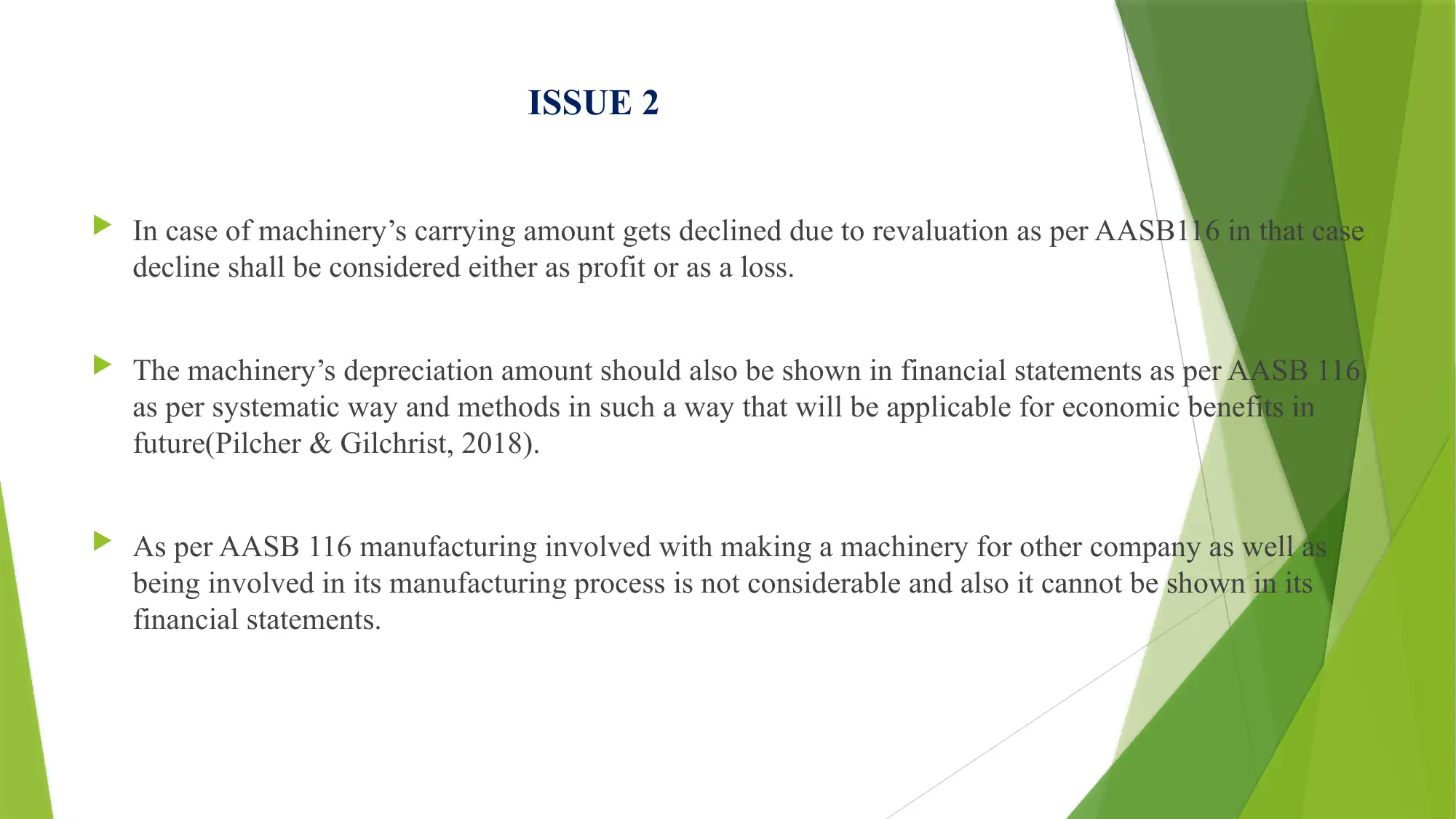

This report analyzes two key accounting issues faced by Pewter Ltd, addressing them in the context of Financial Accounting and Reporting. The first issue revolves around the application of AASB 13 for the fair value measurement of assets, discussing the conditions under which fair value can be applied and the required disclosures. The second issue focuses on the valuation of machinery under AASB 116, detailing how the cost of machinery should be determined, including import duties, and how revaluation increases or decreases should be accounted for in the financial statements. The report also covers the depreciation of machinery and clarifies the scope of AASB 116 regarding the manufacturing of machinery for other companies. The analysis is based on the provided assignment brief, which requires the creation of a business letter responding to a client's concerns and providing technical advice, supported by relevant accounting standards and references.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.