University Financial Accounting and Reporting Assignment

VerifiedAdded on 2022/10/16

|11

|2087

|263

Report

AI Summary

This report examines financial accounting policies and estimates concerning property, plant, and equipment, focusing on the application of professional judgment by accountants. It begins with an overview of the criteria for selecting and changing accounting policies according to AASB 108. The report then analyzes the accounting policies and estimates of Commonwealth Bank, specifically regarding property, plant, and equipment, and evaluates the appropriateness of the professional judgments made. It identifies areas for improvement in accounting estimates and policies, offering recommendations based on industry standards and accounting principles. The report emphasizes the importance of accurate financial reporting and the role of accountants in providing a clear and reliable financial picture for stakeholders.

Running head: FINANCIAL ACCOUNTING AND REPORTING

Financial Accounting and Reporting

Name of the Student

Name of the University

Author’s note

Financial Accounting and Reporting

Name of the Student

Name of the University

Author’s note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2FINANCIAL ACCOUNTING AND REPORTING

Table of Contents

Executive Summary...................................................................................................................3

Introduction................................................................................................................................4

Body...........................................................................................................................................4

Summary of the criteria for selecting and changing accounting policies according to AASB

108..............................................................................................................................................4

Explanation of the accounting policies and estimates used by the company.............................5

Critical evaluation of the appropriateness of the professional judgement.................................6

Recommendation for the improvement of the accounting estimates and policies of property,

plant and equipment...................................................................................................................7

Conclusion..................................................................................................................................7

References..................................................................................................................................8

Appendix....................................................................................................................................9

Table of Contents

Executive Summary...................................................................................................................3

Introduction................................................................................................................................4

Body...........................................................................................................................................4

Summary of the criteria for selecting and changing accounting policies according to AASB

108..............................................................................................................................................4

Explanation of the accounting policies and estimates used by the company.............................5

Critical evaluation of the appropriateness of the professional judgement.................................6

Recommendation for the improvement of the accounting estimates and policies of property,

plant and equipment...................................................................................................................7

Conclusion..................................................................................................................................7

References..................................................................................................................................8

Appendix....................................................................................................................................9

3FINANCIAL ACCOUNTING AND REPORTING

Executive Summary

The report intends to highlight the importance of accountants for applying the professional

judgements that would be significant for constructing the accounting policies of the financial

statements. Keeping this aspect into focus, the report centralises on the discussion of the

principles and regulations that are related to the construction of these accounting policies by

different organisations of Australia. The report begins with a general discussion of the criteria

that is laid down by AASB 108 for the selection and change of accounting policies of the

organisations. At the next section the topic gets narrowed down to a specific company of

Australia, that is Commonwealth Bank. The accounting policies and the estimates that are

used by the company are detailed in the report focussing on the plant, equipment and

property. Next, the report talks about the evaluation of the professional judgements given to

the accounting policies. At the end section the report suggests suitable recommendations for

the highlighted issues that have been detected in the policies of accounting of the company.

Executive Summary

The report intends to highlight the importance of accountants for applying the professional

judgements that would be significant for constructing the accounting policies of the financial

statements. Keeping this aspect into focus, the report centralises on the discussion of the

principles and regulations that are related to the construction of these accounting policies by

different organisations of Australia. The report begins with a general discussion of the criteria

that is laid down by AASB 108 for the selection and change of accounting policies of the

organisations. At the next section the topic gets narrowed down to a specific company of

Australia, that is Commonwealth Bank. The accounting policies and the estimates that are

used by the company are detailed in the report focussing on the plant, equipment and

property. Next, the report talks about the evaluation of the professional judgements given to

the accounting policies. At the end section the report suggests suitable recommendations for

the highlighted issues that have been detected in the policies of accounting of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4FINANCIAL ACCOUNTING AND REPORTING

Introduction

The objective of this report is to bring about a discussion regarding the professional

judgements provided by the accountants while explaining the accounting policies related to

property, equipment and plant. In this context, a general description of the changes

highlighted in the accounting policies are detected and noted down. The regulations are

described following the principles laid by Australian Securities Exchange Board (AASB). A

company is selected which is listed in the securities exchange and the accounting policies and

estimates are thoroughly studied. Any misrepresentation detected in the financial statements

regarding the professional judgement is noted down and appropriate recommendations are

given in addressing these issues.

Body

Summary of the criteria for selecting and changing accounting policies according to

AASB 108

An Australian Accounting Standard is specifically applied to a transaction in such a

condition that all the other events or the accounting policies related to the transaction are

determined through this accounting standard (Aasb.gov.au 2019). The Australian Accounting

Standards normally come with a guidance description that is required to be followed by the

organisations for carrying out their requirements (Carey, Potter and Tanewski 2014). Due to

absence of any Australian Accounting Standard for any particular transaction, the

management is free to use its own professional judgements in developing the accounting

policies of its organisation (Aasb.gov.au 2019). However, the information should be relevant

as well as reliable. There are certain other conditions imposed on the management for

providing the judgement regarding the accounting policies. The management should consider

the application of the requirements which are stated in the Australian Accounting Standard

and also take into account the definitions, criteria for recognition and the measurement

concepts that are related to assets, liabilities, expenses and incomes.

The Australian Accounting Standard also sets out rules regarding the changes in the

accounting policies of the different entities (Carey, Potter and Tanewski 2014). According to

the principles of the standard an entity can change its accounting policies only under certain

conditions. It should be ensured by the entities that the implemented change is required by

one of the Australian Accounting standards (Nobes 2014). It should also be ensured by the

Introduction

The objective of this report is to bring about a discussion regarding the professional

judgements provided by the accountants while explaining the accounting policies related to

property, equipment and plant. In this context, a general description of the changes

highlighted in the accounting policies are detected and noted down. The regulations are

described following the principles laid by Australian Securities Exchange Board (AASB). A

company is selected which is listed in the securities exchange and the accounting policies and

estimates are thoroughly studied. Any misrepresentation detected in the financial statements

regarding the professional judgement is noted down and appropriate recommendations are

given in addressing these issues.

Body

Summary of the criteria for selecting and changing accounting policies according to

AASB 108

An Australian Accounting Standard is specifically applied to a transaction in such a

condition that all the other events or the accounting policies related to the transaction are

determined through this accounting standard (Aasb.gov.au 2019). The Australian Accounting

Standards normally come with a guidance description that is required to be followed by the

organisations for carrying out their requirements (Carey, Potter and Tanewski 2014). Due to

absence of any Australian Accounting Standard for any particular transaction, the

management is free to use its own professional judgements in developing the accounting

policies of its organisation (Aasb.gov.au 2019). However, the information should be relevant

as well as reliable. There are certain other conditions imposed on the management for

providing the judgement regarding the accounting policies. The management should consider

the application of the requirements which are stated in the Australian Accounting Standard

and also take into account the definitions, criteria for recognition and the measurement

concepts that are related to assets, liabilities, expenses and incomes.

The Australian Accounting Standard also sets out rules regarding the changes in the

accounting policies of the different entities (Carey, Potter and Tanewski 2014). According to

the principles of the standard an entity can change its accounting policies only under certain

conditions. It should be ensured by the entities that the implemented change is required by

one of the Australian Accounting standards (Nobes 2014). It should also be ensured by the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5FINANCIAL ACCOUNTING AND REPORTING

entities that the change results in the construction of a reliable financial statement. Such

financial statement should possess relevant information about the effects that are reflected

through performed transactions all over the financial year. The information should also

discuss in details about the events and conditions that determine the current financial position

of the entity. The changes policy should also explain the cash flows of the entity over the

financial year which would automatically signal its financial performance.

Explanation of the accounting policies and estimates used by the company

The company chosen for the purpose of analysing the accounting policies and

estimates of the financial statements is Commonwealth Bank (Commbank.com.au 2019). The

company is an ASX listed company. The annual report of the company for the ending year is

properly analysed and evaluated for carrying out the explanation of accounting policies and

estimates regarding property, plant and equipment.

The different accounting policies and estimates that have been suitably found out from

the financial statements consist of the following points.

1) The net gain or the net loss that is generated from the disposal of the property,

plant or equipment is estimated to be the difference between the proceeds which

are received and the carrying value of these items.

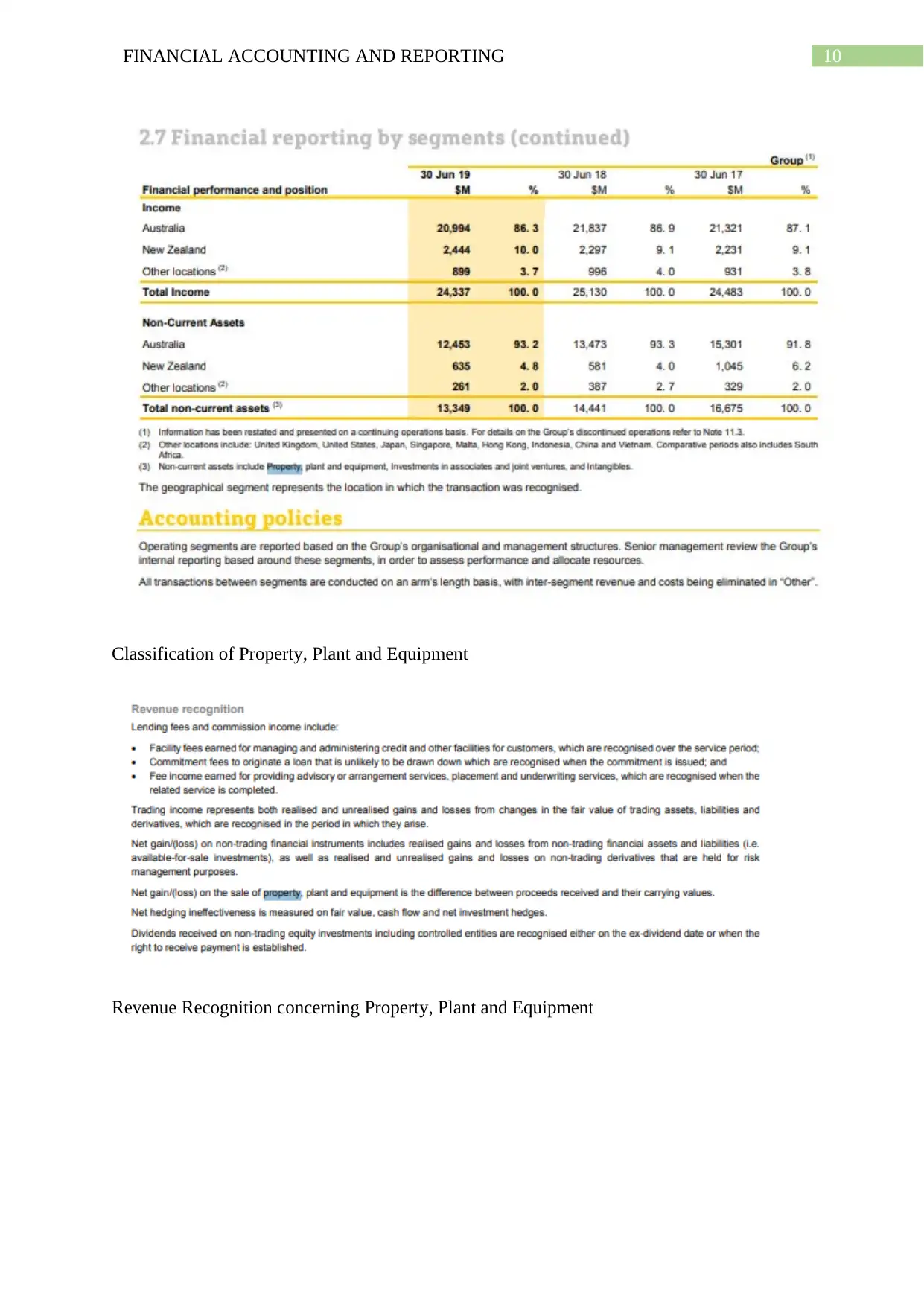

2) The plant, property and the equipment are classified under non-current assets by

the company. These assets have been held by the company to be used for later

years and for leasing through the asset finance businesses (Commbank.com.au

2019). These assets are regarded in the column of “other assets” which are not

prone to risk exposure.

3) Considering the revenue recognition of the company, the net gain or loss that is

obtained or incurred by the company through the sale of plant, equipment and

property is also measured (Commbank.com.au 2019). The measurement is done

through the difference among the received proceeds with the carrying value of

these assets.

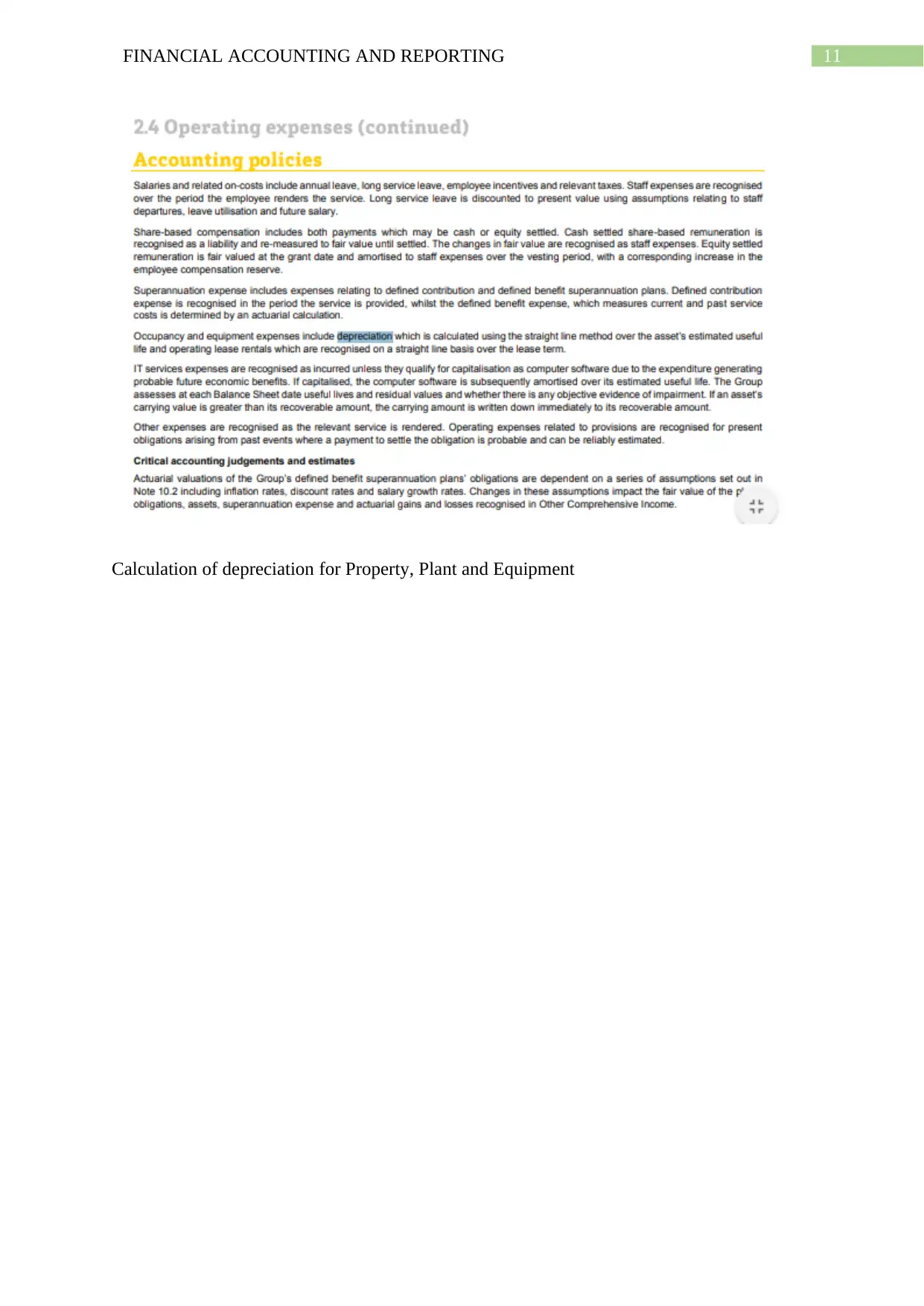

4) Depreciation of these assets is calculated through the straight line method. The

calculation is done over the useful life of the assets and also at the rentals from the

operating lease. The estimated values are recognised based on a straight line over

the entire term of the lease.

entities that the change results in the construction of a reliable financial statement. Such

financial statement should possess relevant information about the effects that are reflected

through performed transactions all over the financial year. The information should also

discuss in details about the events and conditions that determine the current financial position

of the entity. The changes policy should also explain the cash flows of the entity over the

financial year which would automatically signal its financial performance.

Explanation of the accounting policies and estimates used by the company

The company chosen for the purpose of analysing the accounting policies and

estimates of the financial statements is Commonwealth Bank (Commbank.com.au 2019). The

company is an ASX listed company. The annual report of the company for the ending year is

properly analysed and evaluated for carrying out the explanation of accounting policies and

estimates regarding property, plant and equipment.

The different accounting policies and estimates that have been suitably found out from

the financial statements consist of the following points.

1) The net gain or the net loss that is generated from the disposal of the property,

plant or equipment is estimated to be the difference between the proceeds which

are received and the carrying value of these items.

2) The plant, property and the equipment are classified under non-current assets by

the company. These assets have been held by the company to be used for later

years and for leasing through the asset finance businesses (Commbank.com.au

2019). These assets are regarded in the column of “other assets” which are not

prone to risk exposure.

3) Considering the revenue recognition of the company, the net gain or loss that is

obtained or incurred by the company through the sale of plant, equipment and

property is also measured (Commbank.com.au 2019). The measurement is done

through the difference among the received proceeds with the carrying value of

these assets.

4) Depreciation of these assets is calculated through the straight line method. The

calculation is done over the useful life of the assets and also at the rentals from the

operating lease. The estimated values are recognised based on a straight line over

the entire term of the lease.

6FINANCIAL ACCOUNTING AND REPORTING

Critical evaluation of the appropriateness of the professional judgement

According to the professional judgement provided by the accounting policies of the

organisation, there has been no trace of the model that has been used by the company

(Worthington 2016). According to AASB 116 standard, the accounting policy of the entity in

the application of property, equipment and plant should be chosen either through the cost

model or through the revaluation model.

It can be assumed through the criteria of estimation, that the company tends to use the

revaluation model for properly accounting the property, plant and the equipment. The criteria

used for estimation also do not talk about exclusion of the accumulated depreciation and the

accumulated losses of impairment (Del Giudice, Manganelli and De Paola 2016). The

industry standard states that the accumulated depreciation and the losses of impairment

should be excluded from the fair value in order to revaluate the assets.

The classification of the property, plant and the equipment is done correctly and the

entire class has been classified under non-current assets (Lourenço et al. 2015). The disposal

of the item belonging to property, land and equipment is done correctly through the entry into

a financial lease. The net gain or loss of the plant property and equipment is also done

correctly. The industry structure states that the derecognition of the items belonging to

property, plant and equipment should be determined according to the difference between the

process of the net disposal as well as the carrying amount of the item.

Considering the depreciation of the property, plant and the equipment, the

depreciation charge has not been specifically mentioned in the accounting policies.

According to AASB, the charge of the depreciation should be determined as a profit or a loss

(Trifan and Anton 2014). However, the method of depreciation that is used by the company is

straight-line depreciation. This is a standard method that has been stated in the industry

standards. This method is a convenient method for allocating the depreciable amount of an

asset systematically over its entire useful life.

Recommendation for the improvement of the accounting estimates and policies of

property, plant and equipment

The accounting policies and estimates that have been stated in the financial statement

of the company should be more elaborate considering the perspective of property, plant and

equipment (Carnegie and O’Connell 2014). Some of the policies that are estimated and

Critical evaluation of the appropriateness of the professional judgement

According to the professional judgement provided by the accounting policies of the

organisation, there has been no trace of the model that has been used by the company

(Worthington 2016). According to AASB 116 standard, the accounting policy of the entity in

the application of property, equipment and plant should be chosen either through the cost

model or through the revaluation model.

It can be assumed through the criteria of estimation, that the company tends to use the

revaluation model for properly accounting the property, plant and the equipment. The criteria

used for estimation also do not talk about exclusion of the accumulated depreciation and the

accumulated losses of impairment (Del Giudice, Manganelli and De Paola 2016). The

industry standard states that the accumulated depreciation and the losses of impairment

should be excluded from the fair value in order to revaluate the assets.

The classification of the property, plant and the equipment is done correctly and the

entire class has been classified under non-current assets (Lourenço et al. 2015). The disposal

of the item belonging to property, land and equipment is done correctly through the entry into

a financial lease. The net gain or loss of the plant property and equipment is also done

correctly. The industry structure states that the derecognition of the items belonging to

property, plant and equipment should be determined according to the difference between the

process of the net disposal as well as the carrying amount of the item.

Considering the depreciation of the property, plant and the equipment, the

depreciation charge has not been specifically mentioned in the accounting policies.

According to AASB, the charge of the depreciation should be determined as a profit or a loss

(Trifan and Anton 2014). However, the method of depreciation that is used by the company is

straight-line depreciation. This is a standard method that has been stated in the industry

standards. This method is a convenient method for allocating the depreciable amount of an

asset systematically over its entire useful life.

Recommendation for the improvement of the accounting estimates and policies of

property, plant and equipment

The accounting policies and estimates that have been stated in the financial statement

of the company should be more elaborate considering the perspective of property, plant and

equipment (Carnegie and O’Connell 2014). Some of the policies that are estimated and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7FINANCIAL ACCOUNTING AND REPORTING

judged are correct to a certain extent. However, there are other criteria as mentioned in the

industry standards which should be incorporated into the accounting policies of the

organisation. The different models that have been used for estimation should be stated. Out of

the two convenient models, that is, cost model and revaluation model, the policy should

highlight at least one (Yao, Percy and Hu 2015). Certain other small modifications should be

done in order to properly the judge the recognition and derecognition of the plant, property

and equipment. Some of them could be charge of the depreciation and accounting for the

accumulated depreciation and impairment losses.

Conclusion

From the above report, a conclusion can be made regarding the accounting policies

related to the property, plant and the equipment. These assets should be properly presented

and well-judged by the professional accountants in order to present a healthy financial picture

of the company in front of the stakeholders. In this context, criteria for selection and change

in the accounting policy is extracted from AASB. Accounting policy of Commonwealth Bank

is analysed for getting a more detailed view of the criteria and suitable recommendations are

provided regarding any loophole that is detected.

judged are correct to a certain extent. However, there are other criteria as mentioned in the

industry standards which should be incorporated into the accounting policies of the

organisation. The different models that have been used for estimation should be stated. Out of

the two convenient models, that is, cost model and revaluation model, the policy should

highlight at least one (Yao, Percy and Hu 2015). Certain other small modifications should be

done in order to properly the judge the recognition and derecognition of the plant, property

and equipment. Some of them could be charge of the depreciation and accounting for the

accumulated depreciation and impairment losses.

Conclusion

From the above report, a conclusion can be made regarding the accounting policies

related to the property, plant and the equipment. These assets should be properly presented

and well-judged by the professional accountants in order to present a healthy financial picture

of the company in front of the stakeholders. In this context, criteria for selection and change

in the accounting policy is extracted from AASB. Accounting policy of Commonwealth Bank

is analysed for getting a more detailed view of the criteria and suitable recommendations are

provided regarding any loophole that is detected.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8FINANCIAL ACCOUNTING AND REPORTING

References

Aasb.gov.au (2019). [online] Available at:

aasb.gov.au/admin/file/content105/c9/AASB108_08-15.pdf [Accessed 24 Sep. 2019].

Carey, P., Potter, B. and Tanewski, G., 2014. AASB Research Report No.

Carnegie, G.D. and O’Connell, B.T., 2014. A longitudinal study of the interplay of corporate

collapse, accounting failure and governance change in Australia: Early 1890s to early

2000s. Critical Perspectives on Accounting, 25(6), pp.446-468.

Commbank.com.au (2019). [online] Available at:

commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/annual-reports/CBA-

2019-Annual-Report.pdf [Accessed 24 Sep. 2019].

Del Giudice, V., Manganelli, B. and De Paola, P., 2016, July. Depreciation methods for

firm’s assets. In International Conference on Computational Science and Its Applications(pp.

214-227). Springer, Cham.

Lourenço, I.C., Sarquis, R., Branco, M.C. and Pais, C., 2015. Extending the classification of

European Countries by their IFRS practices: A research note. Accounting in Europe, 12(2),

pp.223-232.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Trifan, A. and Anton, C., 2014. ACCOUNTING TREATMENT FOR PROPERTY, PLANT

AND EQUIPMENT REVALUATIONS. Management & Marketing, 9(2).

Worthington, A.C., 2016. Financial literacy and financial literacy programmes in Australia.

In Financial Literacy and the Limits of Financial Decision-Making (pp. 281-301). Palgrave

Macmillan, Cham.

Yao, D.F.T., Percy, M. and Hu, F., 2015. Fair value accounting for non-current assets and

audit fees: Evidence from Australian companies. Journal of Contemporary Accounting &

Economics, 11(1), pp.31-45.

References

Aasb.gov.au (2019). [online] Available at:

aasb.gov.au/admin/file/content105/c9/AASB108_08-15.pdf [Accessed 24 Sep. 2019].

Carey, P., Potter, B. and Tanewski, G., 2014. AASB Research Report No.

Carnegie, G.D. and O’Connell, B.T., 2014. A longitudinal study of the interplay of corporate

collapse, accounting failure and governance change in Australia: Early 1890s to early

2000s. Critical Perspectives on Accounting, 25(6), pp.446-468.

Commbank.com.au (2019). [online] Available at:

commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/annual-reports/CBA-

2019-Annual-Report.pdf [Accessed 24 Sep. 2019].

Del Giudice, V., Manganelli, B. and De Paola, P., 2016, July. Depreciation methods for

firm’s assets. In International Conference on Computational Science and Its Applications(pp.

214-227). Springer, Cham.

Lourenço, I.C., Sarquis, R., Branco, M.C. and Pais, C., 2015. Extending the classification of

European Countries by their IFRS practices: A research note. Accounting in Europe, 12(2),

pp.223-232.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Trifan, A. and Anton, C., 2014. ACCOUNTING TREATMENT FOR PROPERTY, PLANT

AND EQUIPMENT REVALUATIONS. Management & Marketing, 9(2).

Worthington, A.C., 2016. Financial literacy and financial literacy programmes in Australia.

In Financial Literacy and the Limits of Financial Decision-Making (pp. 281-301). Palgrave

Macmillan, Cham.

Yao, D.F.T., Percy, M. and Hu, F., 2015. Fair value accounting for non-current assets and

audit fees: Evidence from Australian companies. Journal of Contemporary Accounting &

Economics, 11(1), pp.31-45.

9FINANCIAL ACCOUNTING AND REPORTING

Appendix

Accounting Policies for Property, Plant and Equipment for the calculation of net gain or loss

Appendix

Accounting Policies for Property, Plant and Equipment for the calculation of net gain or loss

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10FINANCIAL ACCOUNTING AND REPORTING

Classification of Property, Plant and Equipment

Revenue Recognition concerning Property, Plant and Equipment

Classification of Property, Plant and Equipment

Revenue Recognition concerning Property, Plant and Equipment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11FINANCIAL ACCOUNTING AND REPORTING

Calculation of depreciation for Property, Plant and Equipment

Calculation of depreciation for Property, Plant and Equipment

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.