Comprehensive Financial Accounting Report: Concepts and Calculations

VerifiedAdded on 2022/11/28

|28

|4619

|66

Report

AI Summary

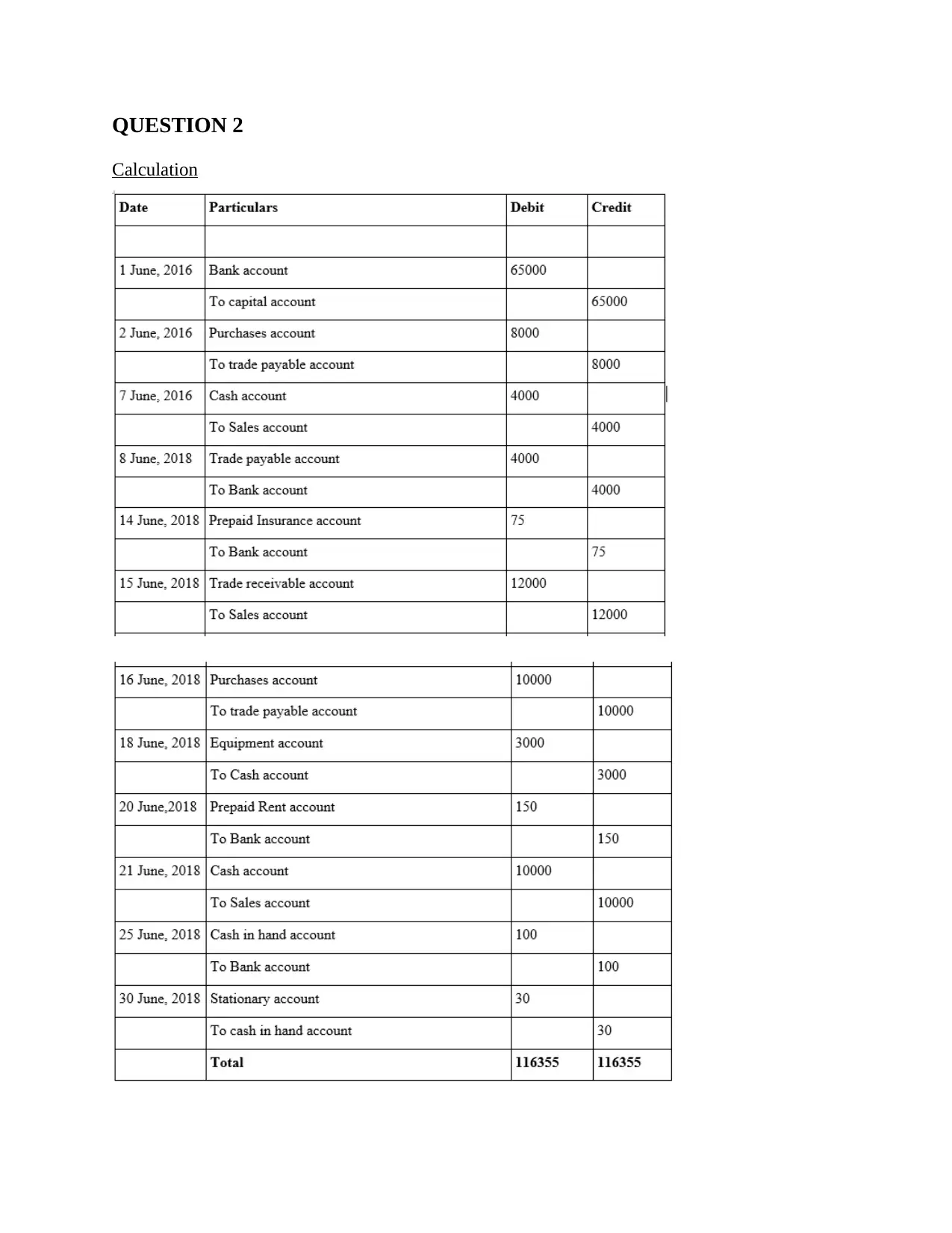

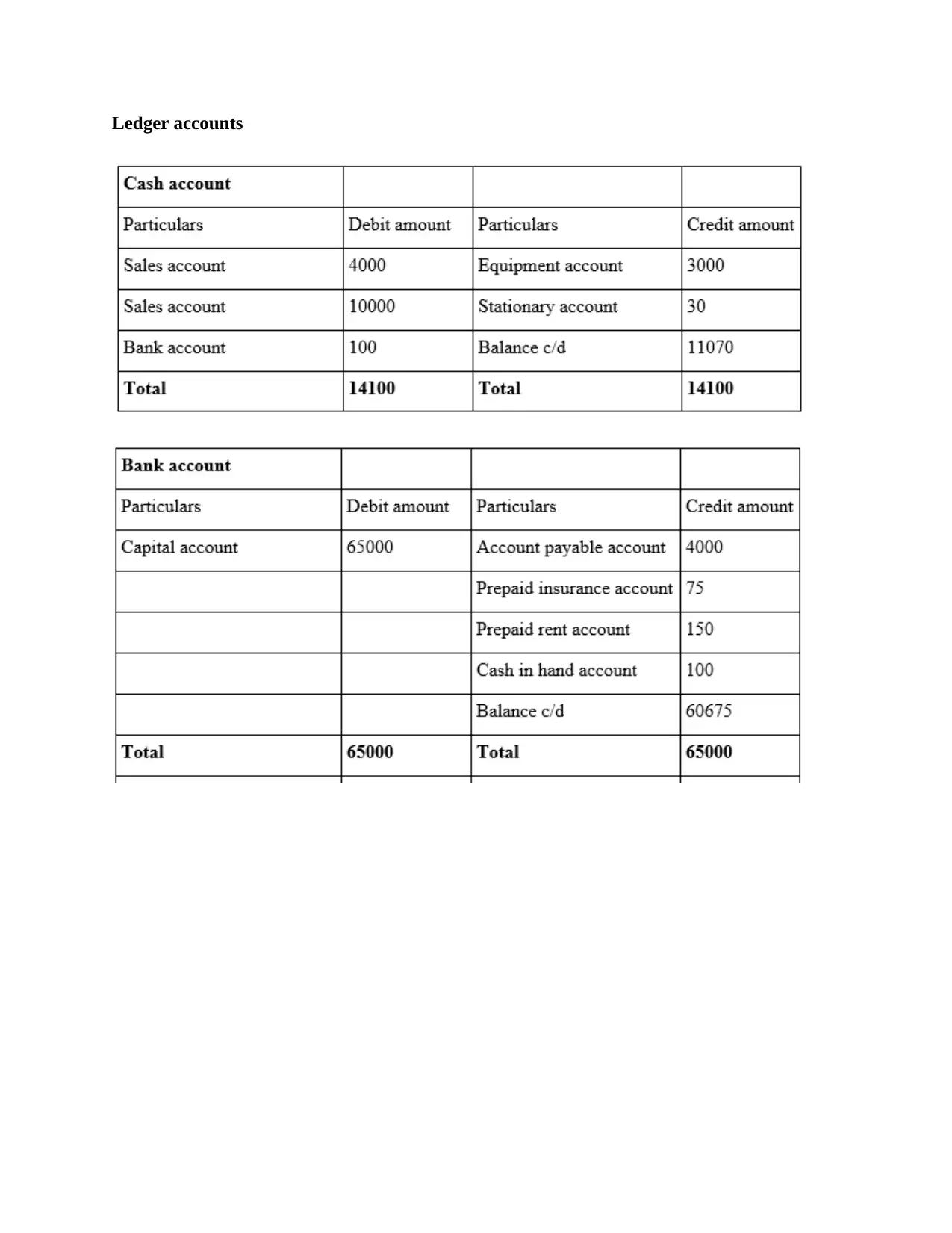

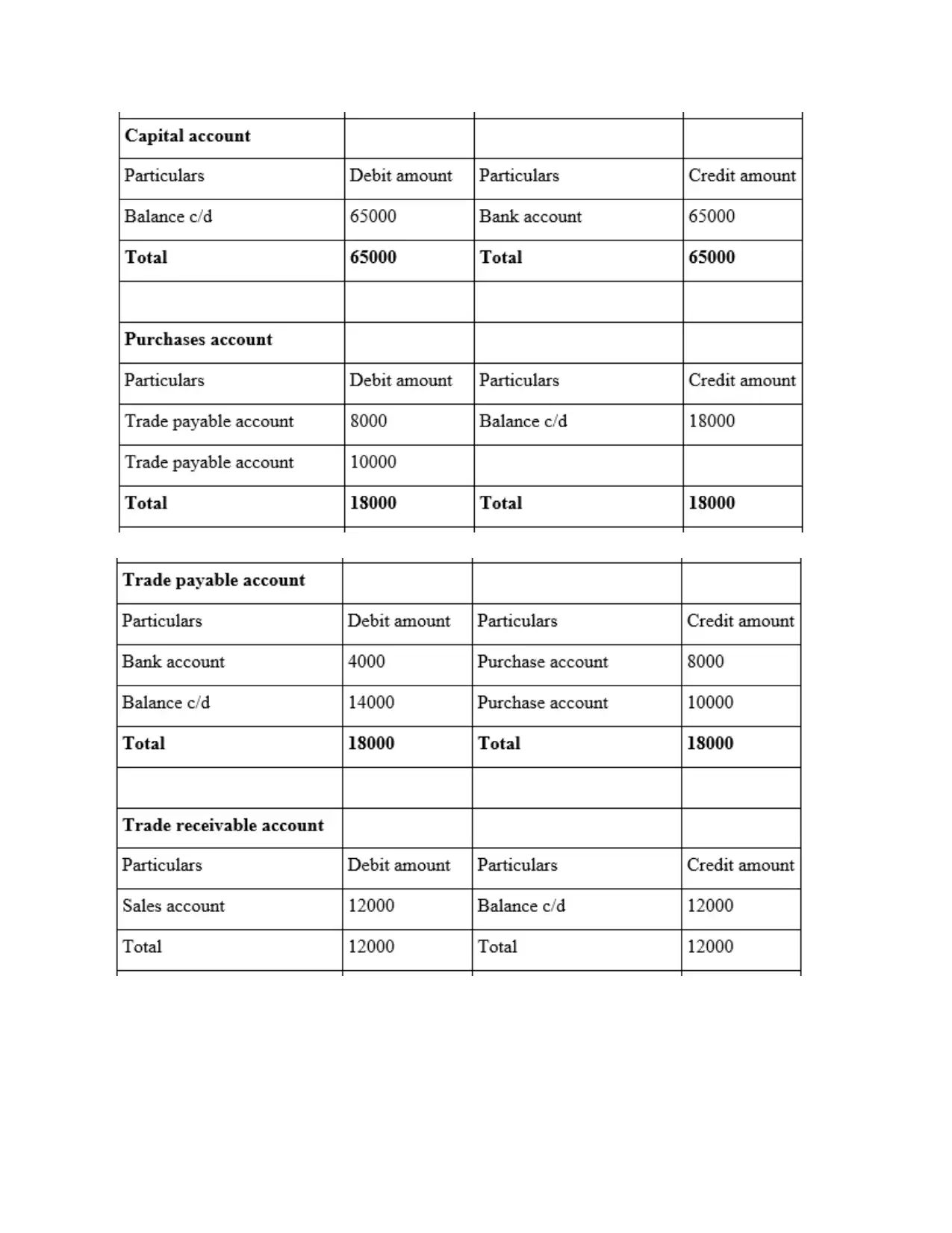

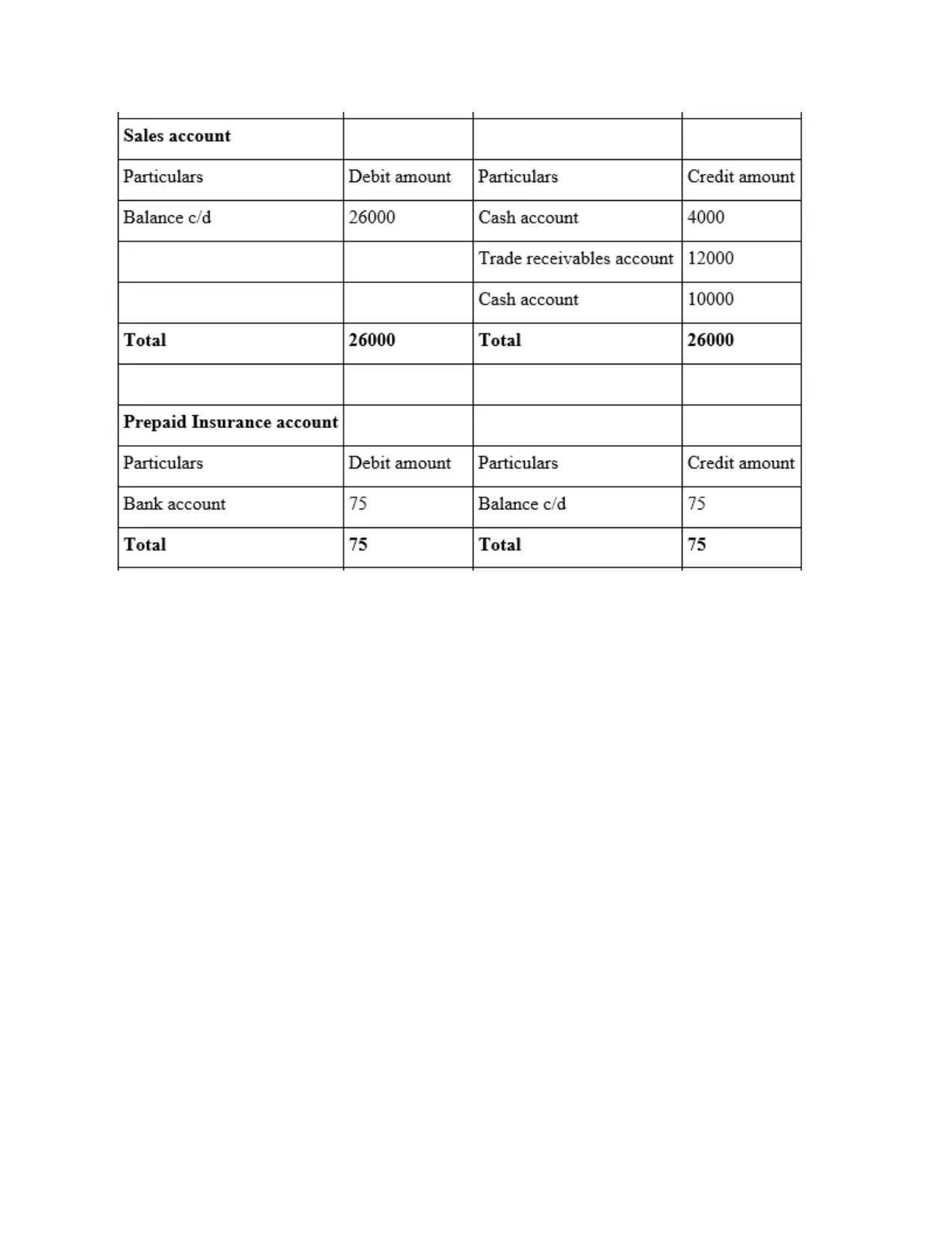

This report delves into the core principles of financial accounting, beginning with an introduction to the accounting process and its importance in evaluating a company's financial health. It explores different types of business transactions within single and double-entry bookkeeping systems, elucidating the roles of sales, purchases, and receipts. The report also covers the creation of trial balances and their significance in accounting. It then distinguishes between financial statements and financial reports, detailing the components of income statements, balance sheets, and cash flow statements. The report includes calculations and examples to illustrate key concepts. It further examines accounting principles, such as full disclosure, materiality, consistency, monetary unit, and going concern. The report extends to scenarios involving bank reconciliations, control accounts, and suspense accounts, complete with journal entries and updated cash books, providing a holistic view of financial accounting practices.

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.