Financial Accounting Report: ACC518 on Auditing and Standards

VerifiedAdded on 2023/06/05

|18

|3706

|456

Report

AI Summary

This report comprises two main sections: the first analyzes a news article discussing the role of major accounting firms in Australia and their impact on the global economy, linking the issues to concepts from ACC518, such as accounting policies, auditing practices, and the importance of IFRS. It highlights concerns about the shift of these firms towards consultancy services and the potential implications for financial statement accuracy and public interest. The second section examines comments from various business organizations (RSM, KPMG, IAS Plus, and Deloitte) on an upcoming accounting standard update (2018-13) regarding fair value measurement, focusing on disclosure framework changes and their implications. The report discusses the upcoming accounting standard and the key modifications and removals of disclosure requirements. It also emphasizes the importance of these standards for transparent financial reporting and its impact on various stakeholders.

AP 1

Running Head: ACCOUNTING

Accounting Paper

Running Head: ACCOUNTING

Accounting Paper

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AP 2

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................4

Relation to ACC518........................................................................................................................5

Conclusion.......................................................................................................................................7

Introduction......................................................................................................................................9

Upcoming accounting standard.......................................................................................................9

Comments of different Stakeholders on the Proposed Standards..................................................12

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................4

Relation to ACC518........................................................................................................................5

Conclusion.......................................................................................................................................7

Introduction......................................................................................................................................9

Upcoming accounting standard.......................................................................................................9

Comments of different Stakeholders on the Proposed Standards..................................................12

Conclusion.....................................................................................................................................16

References......................................................................................................................................17

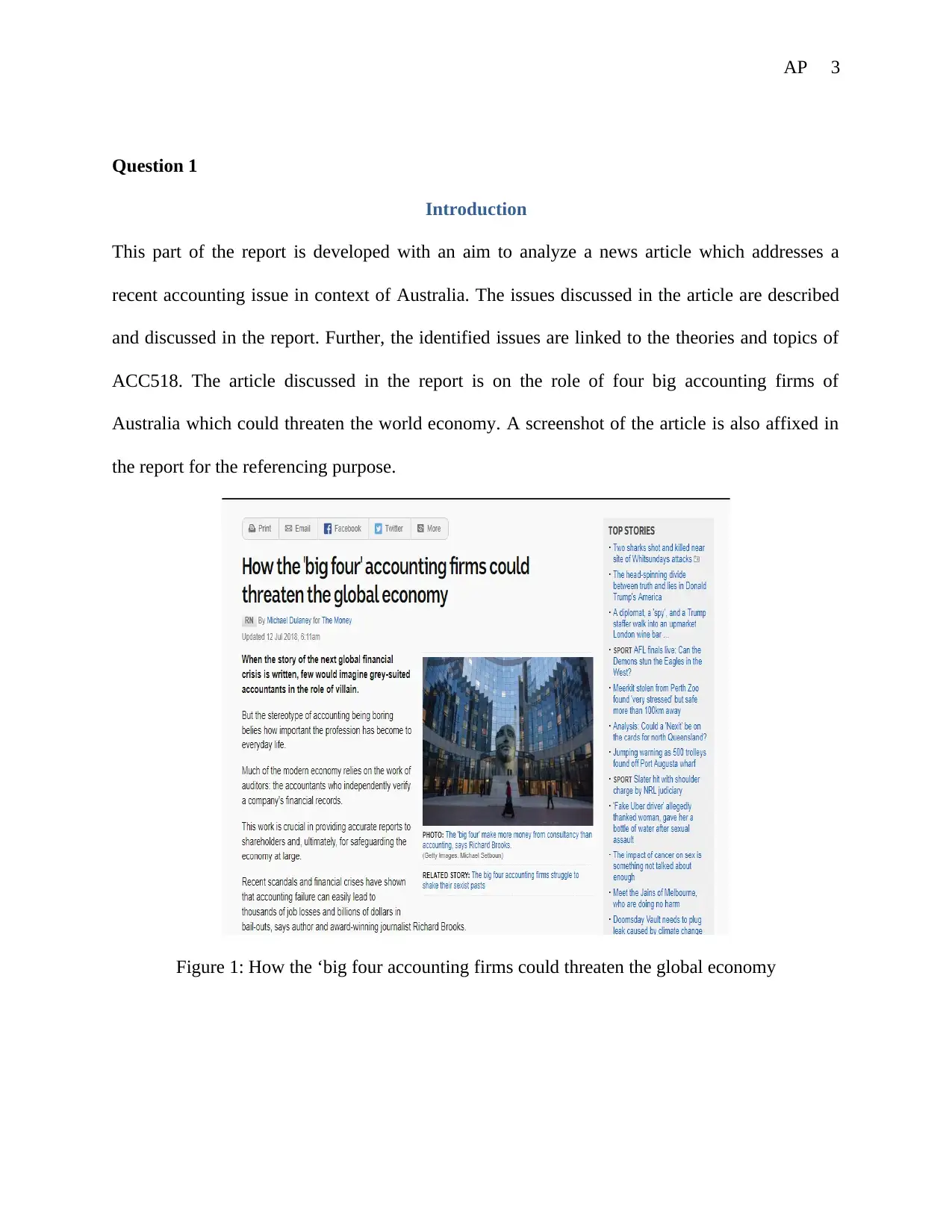

AP 3

Question 1

Introduction

This part of the report is developed with an aim to analyze a news article which addresses a

recent accounting issue in context of Australia. The issues discussed in the article are described

and discussed in the report. Further, the identified issues are linked to the theories and topics of

ACC518. The article discussed in the report is on the role of four big accounting firms of

Australia which could threaten the world economy. A screenshot of the article is also affixed in

the report for the referencing purpose.

Figure 1: How the ‘big four accounting firms could threaten the global economy

Question 1

Introduction

This part of the report is developed with an aim to analyze a news article which addresses a

recent accounting issue in context of Australia. The issues discussed in the article are described

and discussed in the report. Further, the identified issues are linked to the theories and topics of

ACC518. The article discussed in the report is on the role of four big accounting firms of

Australia which could threaten the world economy. A screenshot of the article is also affixed in

the report for the referencing purpose.

Figure 1: How the ‘big four accounting firms could threaten the global economy

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AP 4

Discussion

Even though the accounting seems to be boring but it is an important aspect of every business.

Almost every economy of the world relies on accountants for their auditing work for verifying

the financial records of the company. Auditing is crucial in determining the accuracy of the

report provided to the different stakeholders of the company and safeguards the economy on a

large scale (Abeysekara, 2013). But recent financial crises and scandals depicted that any failure

in the accounting may lead to losing jobs in thousands of numbers and billions of dollars as well.

The major issue identified in the newspaper article is related to the auditing practices of the big

accounting firms such as Deloitte, KPMG, Ernst and Young, and PwC. These companies are

well known for auditing the big multinational corporation according to their market shares. The

concern addressed in the article is about the losing insight of these companies in exercising their

core business which is auditing. Rather, these companies are giving more importance on

providing the consultancy services. Their reducing revenue from the work of auditing and

increasing revenue from the sale of consultancy services is evident to this fact. These top

accounting firms are no longer seems to be working for accounting profession. Earlier, the

auditing was in majority of their profession and in the current phase it has reduced to one third

and has turned into just one of a line of their business. Due to insufficiency in the auditing

practices provided by these four big accounting firms to the multinational corporation, their

businesses are getting affected in an adverse manner. All the decisions of the company are

dependent on their financial statements and auditing them is the only tool by which the accuracy

of financial statements can be tested (Ball, Jayaraman, and Shivkumar, 2012). But since the big

organizations have routed their interest to constancy service many of the multinational

Discussion

Even though the accounting seems to be boring but it is an important aspect of every business.

Almost every economy of the world relies on accountants for their auditing work for verifying

the financial records of the company. Auditing is crucial in determining the accuracy of the

report provided to the different stakeholders of the company and safeguards the economy on a

large scale (Abeysekara, 2013). But recent financial crises and scandals depicted that any failure

in the accounting may lead to losing jobs in thousands of numbers and billions of dollars as well.

The major issue identified in the newspaper article is related to the auditing practices of the big

accounting firms such as Deloitte, KPMG, Ernst and Young, and PwC. These companies are

well known for auditing the big multinational corporation according to their market shares. The

concern addressed in the article is about the losing insight of these companies in exercising their

core business which is auditing. Rather, these companies are giving more importance on

providing the consultancy services. Their reducing revenue from the work of auditing and

increasing revenue from the sale of consultancy services is evident to this fact. These top

accounting firms are no longer seems to be working for accounting profession. Earlier, the

auditing was in majority of their profession and in the current phase it has reduced to one third

and has turned into just one of a line of their business. Due to insufficiency in the auditing

practices provided by these four big accounting firms to the multinational corporation, their

businesses are getting affected in an adverse manner. All the decisions of the company are

dependent on their financial statements and auditing them is the only tool by which the accuracy

of financial statements can be tested (Ball, Jayaraman, and Shivkumar, 2012). But since the big

organizations have routed their interest to constancy service many of the multinational

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AP 5

corporations are facing with the accuracy of their financial statements. The incorrectly recorded

transactions are not being checked for accuracy and due to which the proper evaluation of the

company’s financial performance could not be done. The four accounting firms are selling

consultancy services to the politicians and bureaucrats to whom there were providing auditing

services before. This shows that the firms are becoming a consigliere to the government as the

politicians and bureaucrats are taking advantages of their services and are able to hide their real

financial positions. Apart from this, the investment related to major infrastructure, nuclear

policy, and transport policy are driven by the advice from these major accounting firms (Brown

and Zhou, 2013). It was also analyzed from the report that these major accounting firms are also

planning to split themselves into consulting and auditing arms of the firms. In this way they will

be changed from big four to big eight. In order to remove the profit motive form the accounting

services, auditing can be done from public funding. This will be a significant move in

differentiating the image if the auditing firms as an outsider.

Relation to ACC518

There are several theories and concepts of ACC518 which are in relatable in context to the above

information analyzed form the news article related to the issue of decreasing importance of

auditing and providing the consulting to the same clients by four big Australian companies. The

concepts of ACC518 identified for the news article is related to the accounting policies and

principles, procedures and rules which can be implemented in the preparation of financial

statement so that their accuracy can be assured. The detailed information is mentioned below:

Organizations use accounting policies in order to avoid the potential mistakes in developing

financial statements and making them more stable, fair and true in the eyes of different

stakeholders (Scherer, Palazz0, and Seidl, 2013). The use of accounting policies in simply not

corporations are facing with the accuracy of their financial statements. The incorrectly recorded

transactions are not being checked for accuracy and due to which the proper evaluation of the

company’s financial performance could not be done. The four accounting firms are selling

consultancy services to the politicians and bureaucrats to whom there were providing auditing

services before. This shows that the firms are becoming a consigliere to the government as the

politicians and bureaucrats are taking advantages of their services and are able to hide their real

financial positions. Apart from this, the investment related to major infrastructure, nuclear

policy, and transport policy are driven by the advice from these major accounting firms (Brown

and Zhou, 2013). It was also analyzed from the report that these major accounting firms are also

planning to split themselves into consulting and auditing arms of the firms. In this way they will

be changed from big four to big eight. In order to remove the profit motive form the accounting

services, auditing can be done from public funding. This will be a significant move in

differentiating the image if the auditing firms as an outsider.

Relation to ACC518

There are several theories and concepts of ACC518 which are in relatable in context to the above

information analyzed form the news article related to the issue of decreasing importance of

auditing and providing the consulting to the same clients by four big Australian companies. The

concepts of ACC518 identified for the news article is related to the accounting policies and

principles, procedures and rules which can be implemented in the preparation of financial

statement so that their accuracy can be assured. The detailed information is mentioned below:

Organizations use accounting policies in order to avoid the potential mistakes in developing

financial statements and making them more stable, fair and true in the eyes of different

stakeholders (Scherer, Palazz0, and Seidl, 2013). The use of accounting policies in simply not

AP 6

enough to see whether the information mentioned in them is totally correct or not. Often when

the financial statements such as balance sheet, income statements, and cash flow statements are

prepared by the accounting personnel of the company there are chances of error and omission of

figures and numbers. Due to these reasons the financial information becomes incorrect and an

incorrect picture of the financial performance of the company is formed. The company makes

decision on the basis of information contained in the financial statement but due incorrect

information all the decisions and strategies based on them becomes vague (Drnevich and Croson,

2013). Therefore, there is strong need for the organizations to undergo auditing to increase the

credibility and reliability of their financial statements.

Accounting standard

IFRS is developed by the IASB to develop global standards which will be used while preparing

the financial statement. While auditing the financial reports of the companies the four big firms

has to check whether their reports are in accordance with the IFRS. Since the four big accounting

firms have mould their interest to the consultancy business, the organizations which are required

to perform audit are also not focusing of conducting the audit in accordance with the IFRS.

Complex activities and corporate governance are included in the IFRS due to which the cost of

preparing the financial statement increases (Albu and Albu, 2012). Small firms invest money in

the preparation of financial statements and the big accounting firms have limited their auditing

services to multinational brands only. Due to this reason, the small forms are unable to check

whether their financial statements are materially correct or not. This negatively impacts the

operations of the small organization due to which many people have to lose their jobs. If more

companies will shutdown then the unemployment level will be increased and GDP of the

economy will decreased. This will lead to a global economic downturn if continued.

enough to see whether the information mentioned in them is totally correct or not. Often when

the financial statements such as balance sheet, income statements, and cash flow statements are

prepared by the accounting personnel of the company there are chances of error and omission of

figures and numbers. Due to these reasons the financial information becomes incorrect and an

incorrect picture of the financial performance of the company is formed. The company makes

decision on the basis of information contained in the financial statement but due incorrect

information all the decisions and strategies based on them becomes vague (Drnevich and Croson,

2013). Therefore, there is strong need for the organizations to undergo auditing to increase the

credibility and reliability of their financial statements.

Accounting standard

IFRS is developed by the IASB to develop global standards which will be used while preparing

the financial statement. While auditing the financial reports of the companies the four big firms

has to check whether their reports are in accordance with the IFRS. Since the four big accounting

firms have mould their interest to the consultancy business, the organizations which are required

to perform audit are also not focusing of conducting the audit in accordance with the IFRS.

Complex activities and corporate governance are included in the IFRS due to which the cost of

preparing the financial statement increases (Albu and Albu, 2012). Small firms invest money in

the preparation of financial statements and the big accounting firms have limited their auditing

services to multinational brands only. Due to this reason, the small forms are unable to check

whether their financial statements are materially correct or not. This negatively impacts the

operations of the small organization due to which many people have to lose their jobs. If more

companies will shutdown then the unemployment level will be increased and GDP of the

economy will decreased. This will lead to a global economic downturn if continued.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AP 7

Assumption behind the public interest

It is assumed that IFRS is required by 120 nations in the reporting jurisdiction in the listed and

domestic companies so that the financial statements can be prepared in a better manner. IFRS is

helpful for the organizations to comply with all the accounting system regulation so that they can

keep the interest of public at large. IFRS includes many elements which are at high level of

public interest. These elements include financial sustainability, continuous public enhancement,

transactions related to accounts in the preparation of financial statements and portrait of

economic reality (Nobes, 2014). All these aspects can be assured only if regular auditing is done

for the financial statements prepared under the consideration of IFRS. Therefore, the financial

statements shall be audited to that the firms can maintain the public interest at large.

Private concern

Since the prime focus of big four accounting firms have moved from auditing practices to

consultancy services the private companies can freely adopt the IFRS which could help them in

complying with the accounting standard and reduce the chances of errors while making the

financial statements. This will also enable them to build the confidence of the investors in the

financial reporting. When the financial statement will be materially correct then the interest of

the public as well as investors will be increased and people will not lose jobs (Levine, 2012).

This could also reduce the rate of unemployment and the save the world from economic

downturn.

Conclusion

It can be concluded from the above report that the accounting standards and auditing plays a vital

role in the creation of financial statements. Accounting standards are useful in making the

financial statements while auditing is useful in assuring that the financial statements are

Assumption behind the public interest

It is assumed that IFRS is required by 120 nations in the reporting jurisdiction in the listed and

domestic companies so that the financial statements can be prepared in a better manner. IFRS is

helpful for the organizations to comply with all the accounting system regulation so that they can

keep the interest of public at large. IFRS includes many elements which are at high level of

public interest. These elements include financial sustainability, continuous public enhancement,

transactions related to accounts in the preparation of financial statements and portrait of

economic reality (Nobes, 2014). All these aspects can be assured only if regular auditing is done

for the financial statements prepared under the consideration of IFRS. Therefore, the financial

statements shall be audited to that the firms can maintain the public interest at large.

Private concern

Since the prime focus of big four accounting firms have moved from auditing practices to

consultancy services the private companies can freely adopt the IFRS which could help them in

complying with the accounting standard and reduce the chances of errors while making the

financial statements. This will also enable them to build the confidence of the investors in the

financial reporting. When the financial statement will be materially correct then the interest of

the public as well as investors will be increased and people will not lose jobs (Levine, 2012).

This could also reduce the rate of unemployment and the save the world from economic

downturn.

Conclusion

It can be concluded from the above report that the accounting standards and auditing plays a vital

role in the creation of financial statements. Accounting standards are useful in making the

financial statements while auditing is useful in assuring that the financial statements are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AP 8

materially correct. Together the accounting standards and auditing can aid any organization in

increasing the credibility of their financial statements and increase the confidence of investors as

well as public. The private companies can easily opt for the IFRS to make their financial

statements reliable and shall not rely on the big firms for the executing the auditing practices.

materially correct. Together the accounting standards and auditing can aid any organization in

increasing the credibility of their financial statements and increase the confidence of investors as

well as public. The private companies can easily opt for the IFRS to make their financial

statements reliable and shall not rely on the big firms for the executing the auditing practices.

AP 9

Question 2

Introduction

This report is prepared for developing the understanding about comments provided by different

business organizations on an upcoming accounting standard in Australia. The upcoming

accounting standard that has been taken in this report for analysis is accounting standards update

no. 2018-13, fair value measurement (TOPIC 820): disclosure framework—changes to the

disclosure requirements for fair value measurement. At the same time, four comments have also

been included in this report for analysis purpose. The names of companies the comment letter of

which are included in this discussion are RSM, KPMG, IAS Plus and Deloitte.

Upcoming accounting standard

The proposed accounting standard Update: “Fair Value Measurement (Topic 820)”

Comments: August 28, 2018

Source: https://asc.fasb.org/imageRoot/81/118196181.pdf and

https://www.fasb.org/cs/ContentServer?

c=FASBContent_C&cid=1176171179766&d=&pagename=FASB%2FFASBContent_C

%2FCompletedProjectPage

Financial accounting standards board generally launches draft for the proposal to develop

exposure before implementation of the new accounting standards in Australia. The main purpose

of the organization is to search for the comments from the experts in the industry and for the

public to provide the views so that the shortcomings can be identified and the IFRS can be

improved for better accounting and disclosures. FASB draft report is associated to the Fair Value

Measurement (Topic 820).

Question 2

Introduction

This report is prepared for developing the understanding about comments provided by different

business organizations on an upcoming accounting standard in Australia. The upcoming

accounting standard that has been taken in this report for analysis is accounting standards update

no. 2018-13, fair value measurement (TOPIC 820): disclosure framework—changes to the

disclosure requirements for fair value measurement. At the same time, four comments have also

been included in this report for analysis purpose. The names of companies the comment letter of

which are included in this discussion are RSM, KPMG, IAS Plus and Deloitte.

Upcoming accounting standard

The proposed accounting standard Update: “Fair Value Measurement (Topic 820)”

Comments: August 28, 2018

Source: https://asc.fasb.org/imageRoot/81/118196181.pdf and

https://www.fasb.org/cs/ContentServer?

c=FASBContent_C&cid=1176171179766&d=&pagename=FASB%2FFASBContent_C

%2FCompletedProjectPage

Financial accounting standards board generally launches draft for the proposal to develop

exposure before implementation of the new accounting standards in Australia. The main purpose

of the organization is to search for the comments from the experts in the industry and for the

public to provide the views so that the shortcomings can be identified and the IFRS can be

improved for better accounting and disclosures. FASB draft report is associated to the Fair Value

Measurement (Topic 820).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AP 10

The major focus of the updating in the accounting policy is due to the need to improve

effectiveness of the disclosures while preparing the financial statements and providing notes to

the financial statements. It facilitates clear communication of the information needed as per the

generally accepted accounting principles. It includes a developmental framework to promote

consistent decisions towards requirement of the disclosures as required by board. The second

thing is the appropriate exercise of carefulness by reporting entities (FASB, 2018).

The part of the disclosure framework project and the amendments will lead to various changes in

the accounting standard. These changes have lead to affect the entities that are covered under

GAAP and have to follow disclosures towards recurring and non-recurring fair value

measurements. There are some changes that are not needed to be implemented and followed by

nonpublic entities (FASB, 2018). The main provisions are consideration of the costs and benefits

due to which there are several removals of the disclosure requirements takes place.

The amount of and the reasons for the transfers among stage 1 and stage 2 of the fair value chain

of command was removed. The next removed requirement is policy towards the transfer between

levels, valuation processes under level 3 while carrying fair value measurement. At last the

requirements that are removed for nonpublic entities includes the changes in the unrealized

losses and gains for the time included in the income for the recurring stage 3 fair value

measurements remained at the end of the period.

the modifications that were made under this amendment are in case of lieu of a roll forward at

stage 3 FVM it is needed that a nonpublic entity disclose transfer towards and outwards under

level 3 of the fair value chain. In addition to this the purchases or issues of assets and liabilities

are also needed to be treated same. Similarly, in case of the investments in certain entities, the

net asset value is needed to disclose at the time of liquidation for the assets of the investees as on

The major focus of the updating in the accounting policy is due to the need to improve

effectiveness of the disclosures while preparing the financial statements and providing notes to

the financial statements. It facilitates clear communication of the information needed as per the

generally accepted accounting principles. It includes a developmental framework to promote

consistent decisions towards requirement of the disclosures as required by board. The second

thing is the appropriate exercise of carefulness by reporting entities (FASB, 2018).

The part of the disclosure framework project and the amendments will lead to various changes in

the accounting standard. These changes have lead to affect the entities that are covered under

GAAP and have to follow disclosures towards recurring and non-recurring fair value

measurements. There are some changes that are not needed to be implemented and followed by

nonpublic entities (FASB, 2018). The main provisions are consideration of the costs and benefits

due to which there are several removals of the disclosure requirements takes place.

The amount of and the reasons for the transfers among stage 1 and stage 2 of the fair value chain

of command was removed. The next removed requirement is policy towards the transfer between

levels, valuation processes under level 3 while carrying fair value measurement. At last the

requirements that are removed for nonpublic entities includes the changes in the unrealized

losses and gains for the time included in the income for the recurring stage 3 fair value

measurements remained at the end of the period.

the modifications that were made under this amendment are in case of lieu of a roll forward at

stage 3 FVM it is needed that a nonpublic entity disclose transfer towards and outwards under

level 3 of the fair value chain. In addition to this the purchases or issues of assets and liabilities

are also needed to be treated same. Similarly, in case of the investments in certain entities, the

net asset value is needed to disclose at the time of liquidation for the assets of the investees as on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AP 11

the date when restriction from salvation might drop in case the investee communicate the

timing/announce publicly (Deloitte, 2018). The last modification in this standard is the

measurement of uncertainty disclosure to communicate the information regarding the uncertainty

in measurable form as of the reporting date.

There is an addition in the disclosure requirements which are not needed to be followed by

nonpublic entities. There are changes in the unrealized gains and losses that are include in

comprehensible income at level 3. The range and weighted average for the unobservable inputs

are also needed to be disclosed up to a certain extent (FASB, 2018). The amendment will be

effective for all the entities at the starting of the financial 2020. The valuation approach will be

applied under three categories such as market approach was valuation will be made as per the

quoted price in active market. The other approach will be income approach that will value the

future amounts such as cash flows and income streams to present value on the date measurement.

Under the last approach which is cost approach the valuation will be done on the amount that

will be needed to replace the service capacity of the asset (FASB, 2018). The main concept

behind the approach is an investor will not pay more for an asset then the cost to buy substitute

or construct.

the date when restriction from salvation might drop in case the investee communicate the

timing/announce publicly (Deloitte, 2018). The last modification in this standard is the

measurement of uncertainty disclosure to communicate the information regarding the uncertainty

in measurable form as of the reporting date.

There is an addition in the disclosure requirements which are not needed to be followed by

nonpublic entities. There are changes in the unrealized gains and losses that are include in

comprehensible income at level 3. The range and weighted average for the unobservable inputs

are also needed to be disclosed up to a certain extent (FASB, 2018). The amendment will be

effective for all the entities at the starting of the financial 2020. The valuation approach will be

applied under three categories such as market approach was valuation will be made as per the

quoted price in active market. The other approach will be income approach that will value the

future amounts such as cash flows and income streams to present value on the date measurement.

Under the last approach which is cost approach the valuation will be done on the amount that

will be needed to replace the service capacity of the asset (FASB, 2018). The main concept

behind the approach is an investor will not pay more for an asset then the cost to buy substitute

or construct.

AP 12

Comments of different Stakeholders on the Proposed Standards

Source of Comments for Deliotte:

https://www2.deloitte.com/us/en/pages/audit/articles/hu-fasb-issues-standard-to-amend-required-

fair-value-measurement-disclosures.html

Screen Shot:

Source of Comments for RSM:

https://rsmus.com/our-insights/newsletters/financial-reporting-insights/changes-to-fair-value-

measurement-disclosure-requirements.html

Screen Shot:

Comments of different Stakeholders on the Proposed Standards

Source of Comments for Deliotte:

https://www2.deloitte.com/us/en/pages/audit/articles/hu-fasb-issues-standard-to-amend-required-

fair-value-measurement-disclosures.html

Screen Shot:

Source of Comments for RSM:

https://rsmus.com/our-insights/newsletters/financial-reporting-insights/changes-to-fair-value-

measurement-disclosure-requirements.html

Screen Shot:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.