Financial Accounting Analysis of ChiHerbal Ltd - ACCT6003

VerifiedAdded on 2023/06/10

|11

|509

|463

Report

AI Summary

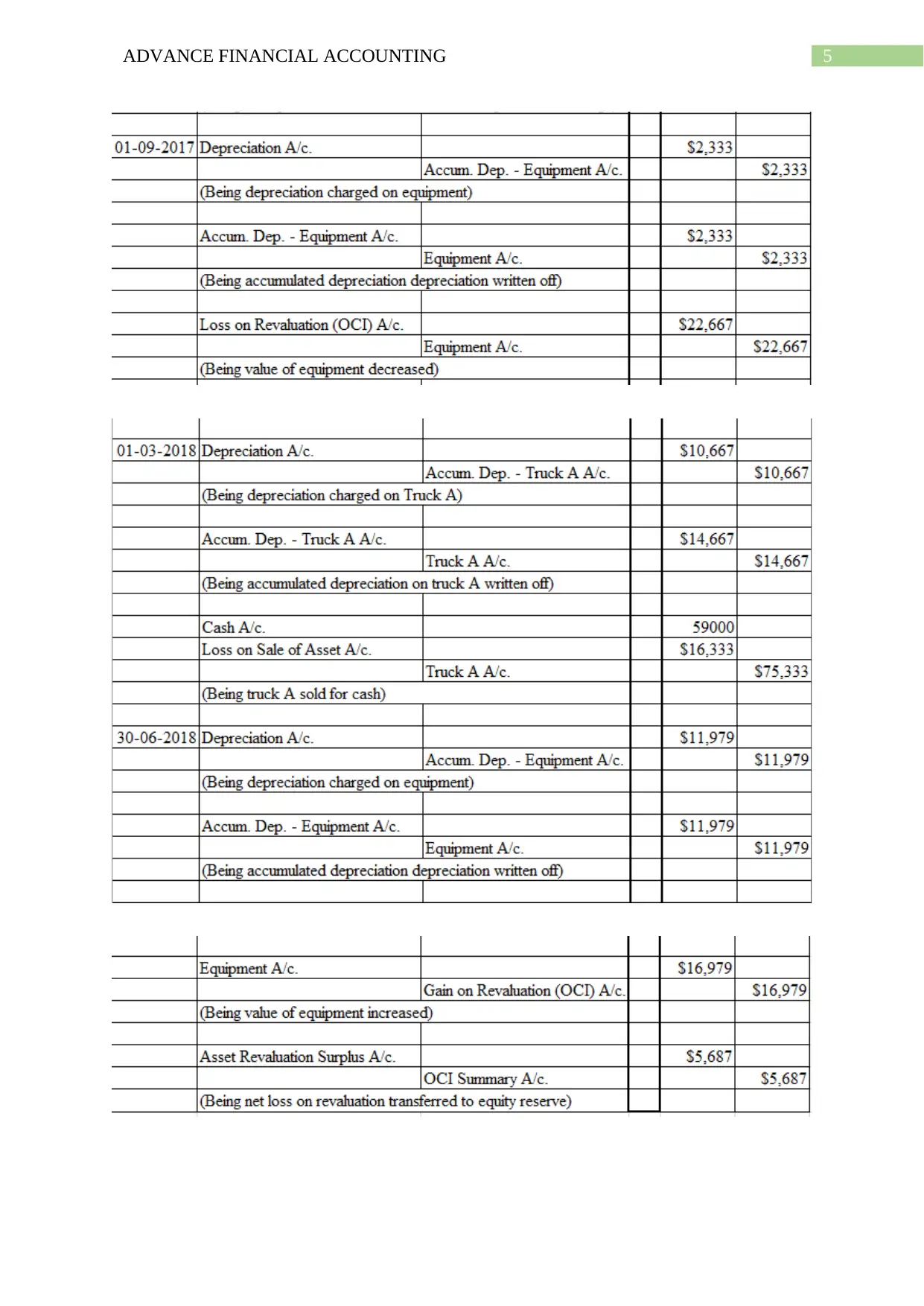

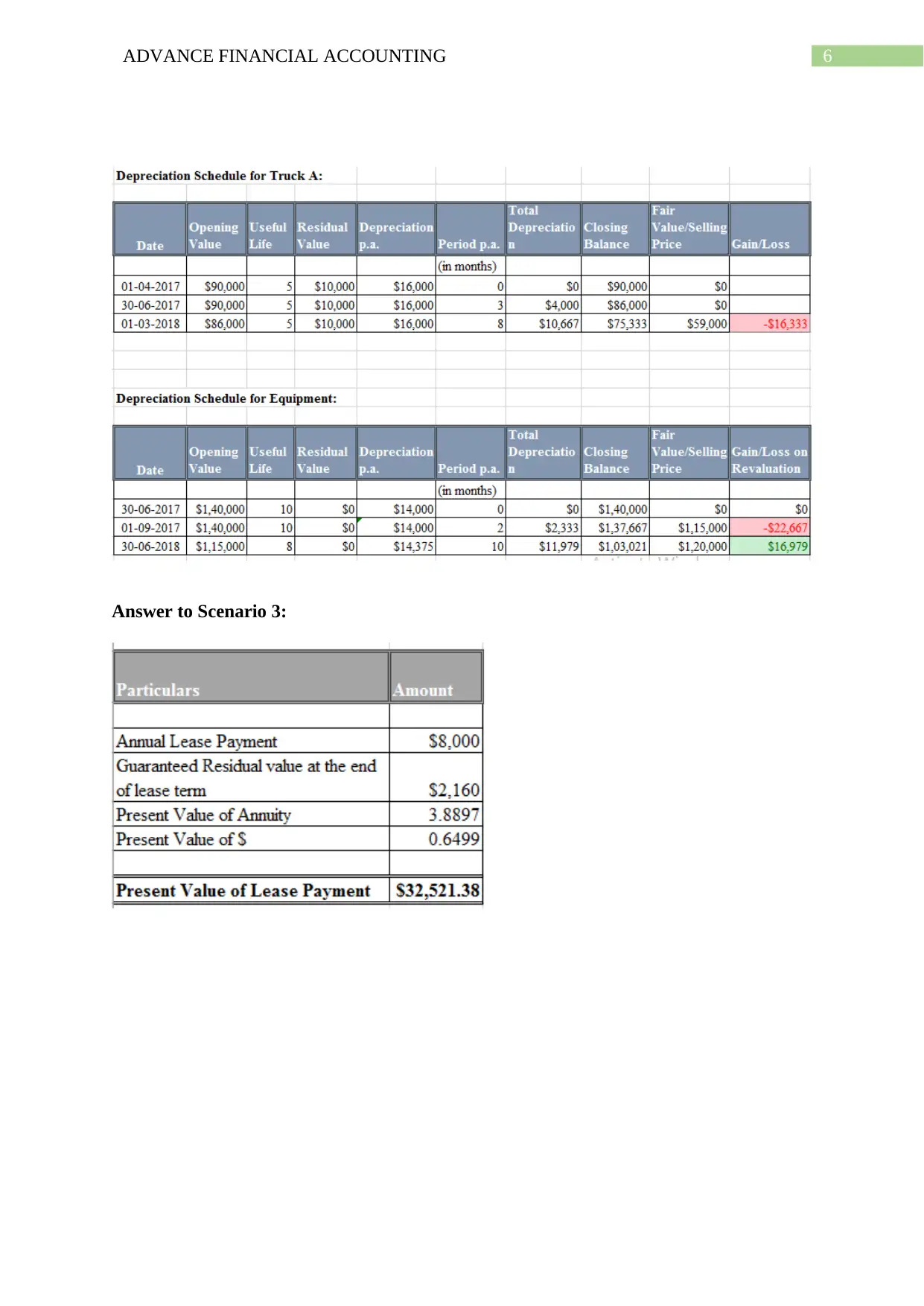

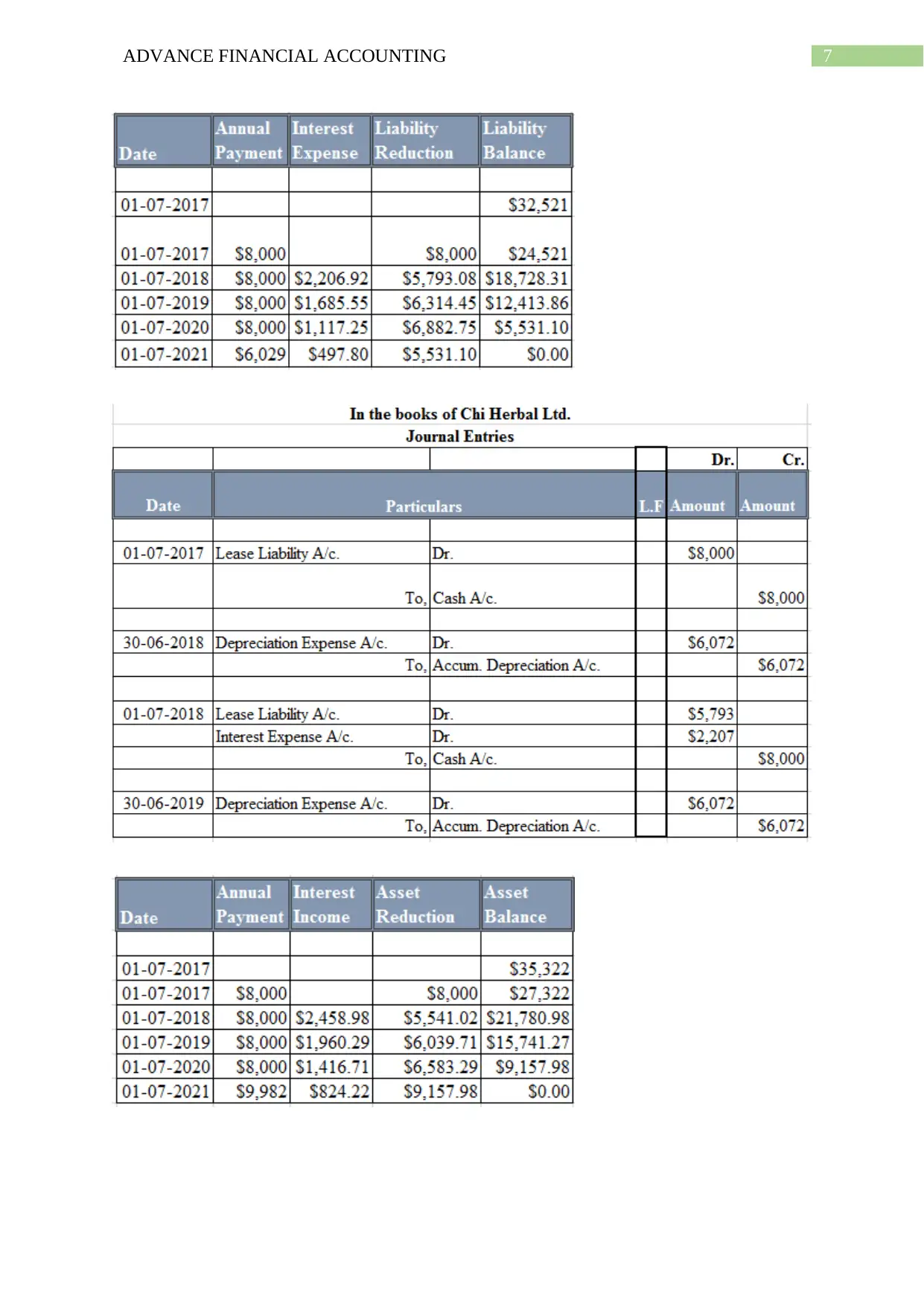

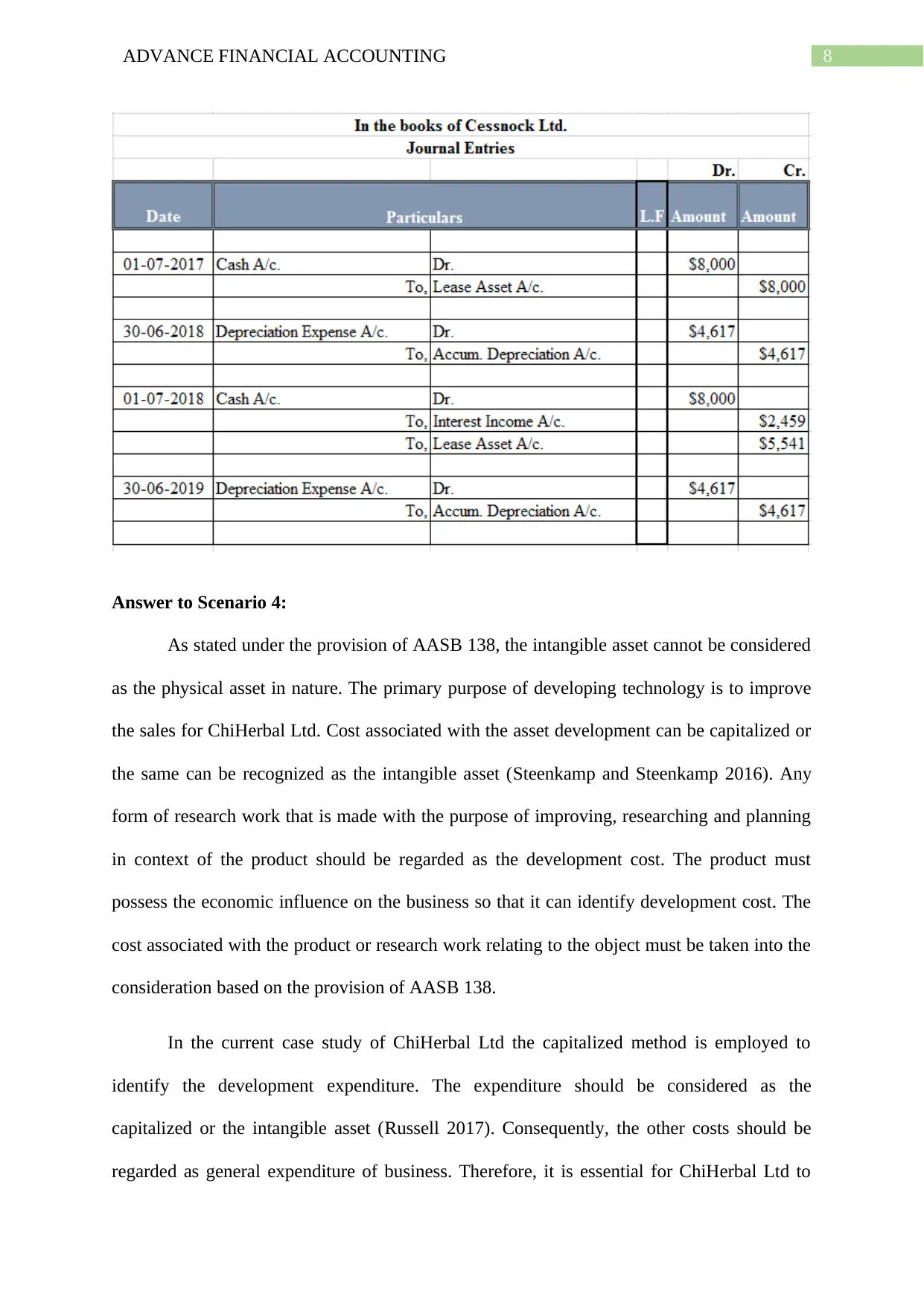

This report analyzes the financial accounting practices of ChiHerbal Ltd, a company that transitioned from a partnership to a private and then a public company structure. The report addresses various scenarios, including the application of AASB 138 to intangible assets, specifically focusing on research and development expenditures. It examines the capitalization of costs, differentiating between research and development phases, and considers the economic impact of these decisions. The analysis includes considerations for the recognition of intangible assets, differentiating between capitalized costs and general business expenditures, and the importance of accurate financial statement disclosures. The report also references relevant accounting standards and provides insights into the management of financial reporting, emphasizing the importance of proper accounting for intangible assets.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.