Financial Reporting: Accounting Principles, Case Study, and Project

VerifiedAdded on 2023/06/03

|17

|3214

|446

Report

AI Summary

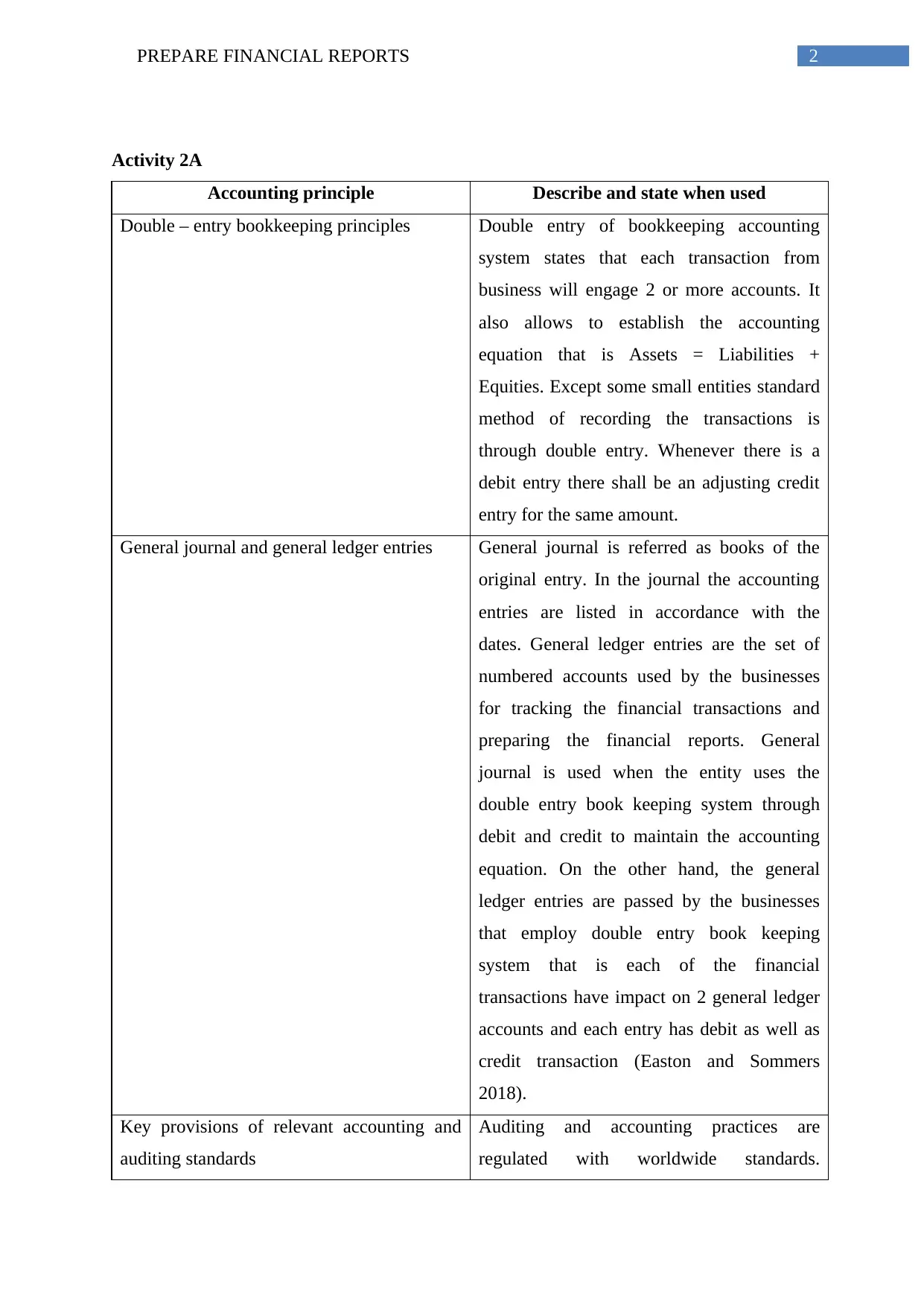

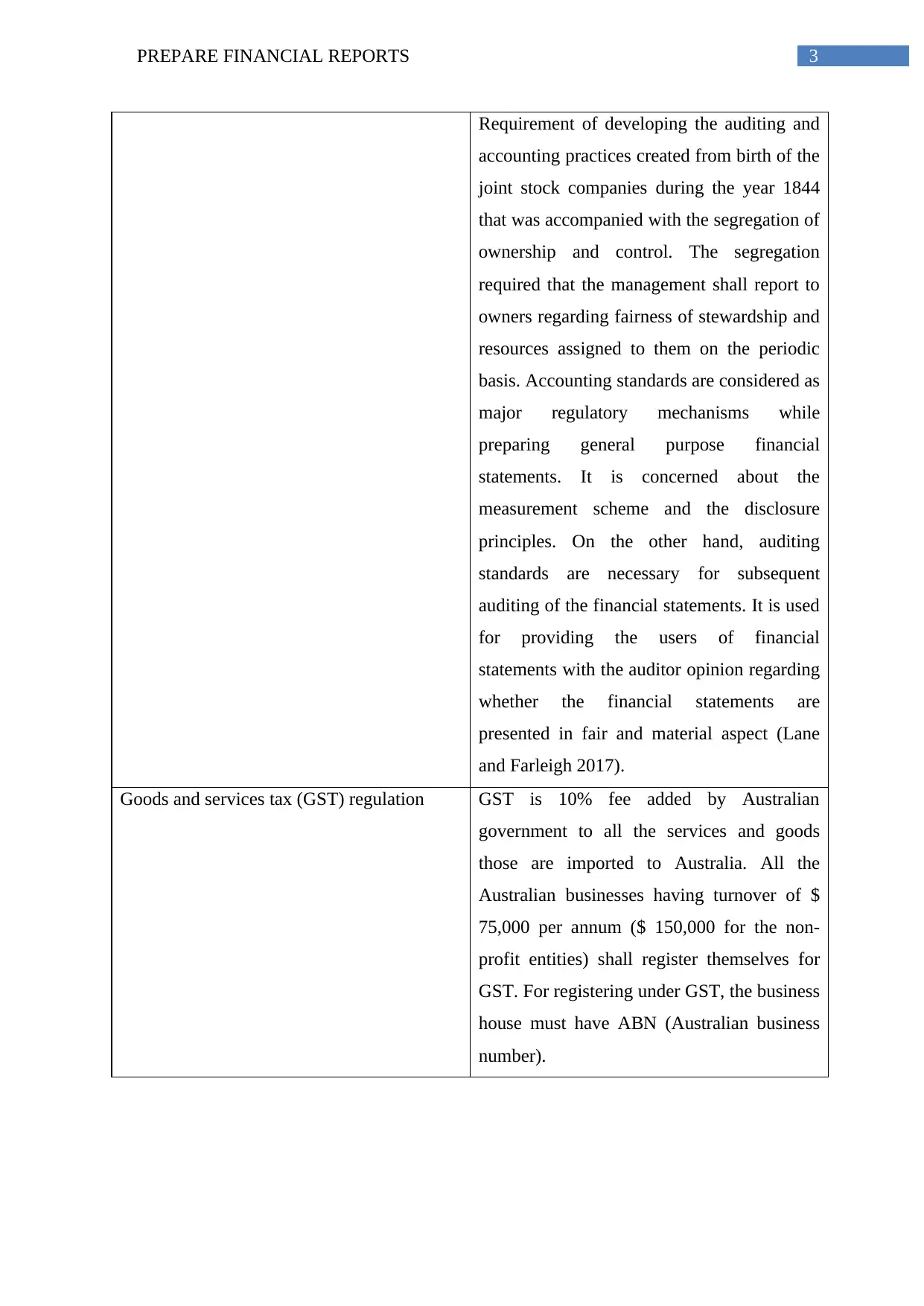

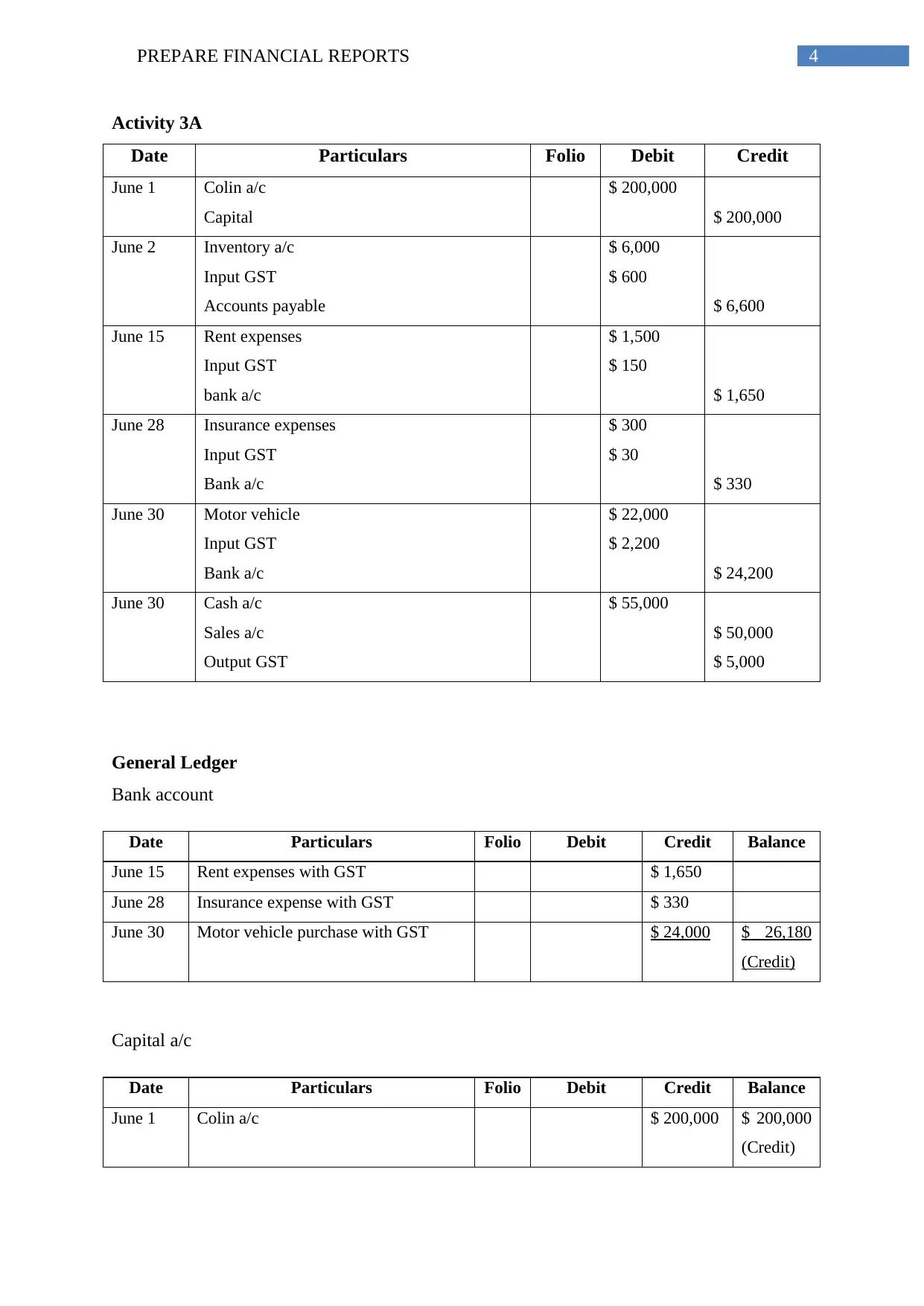

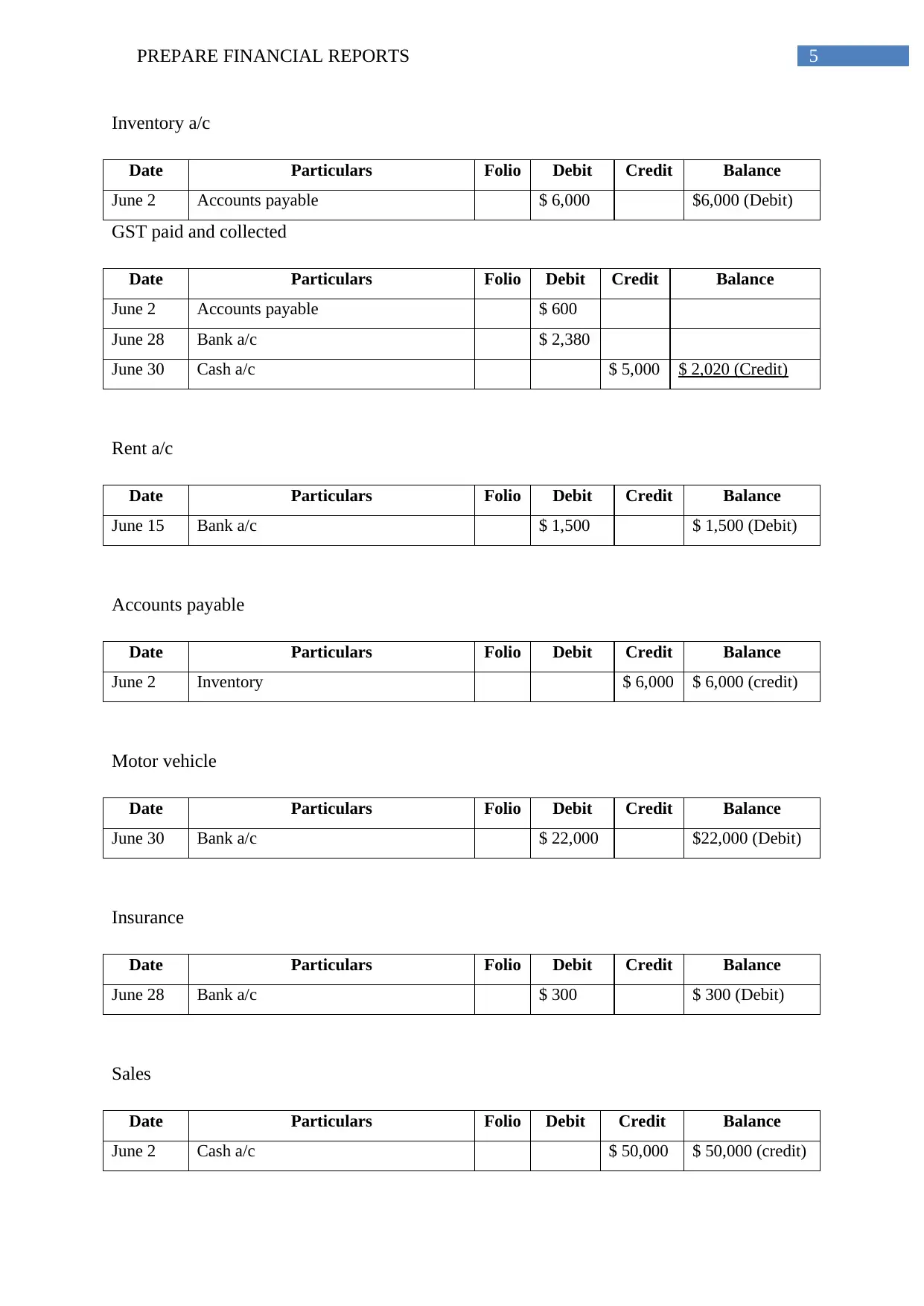

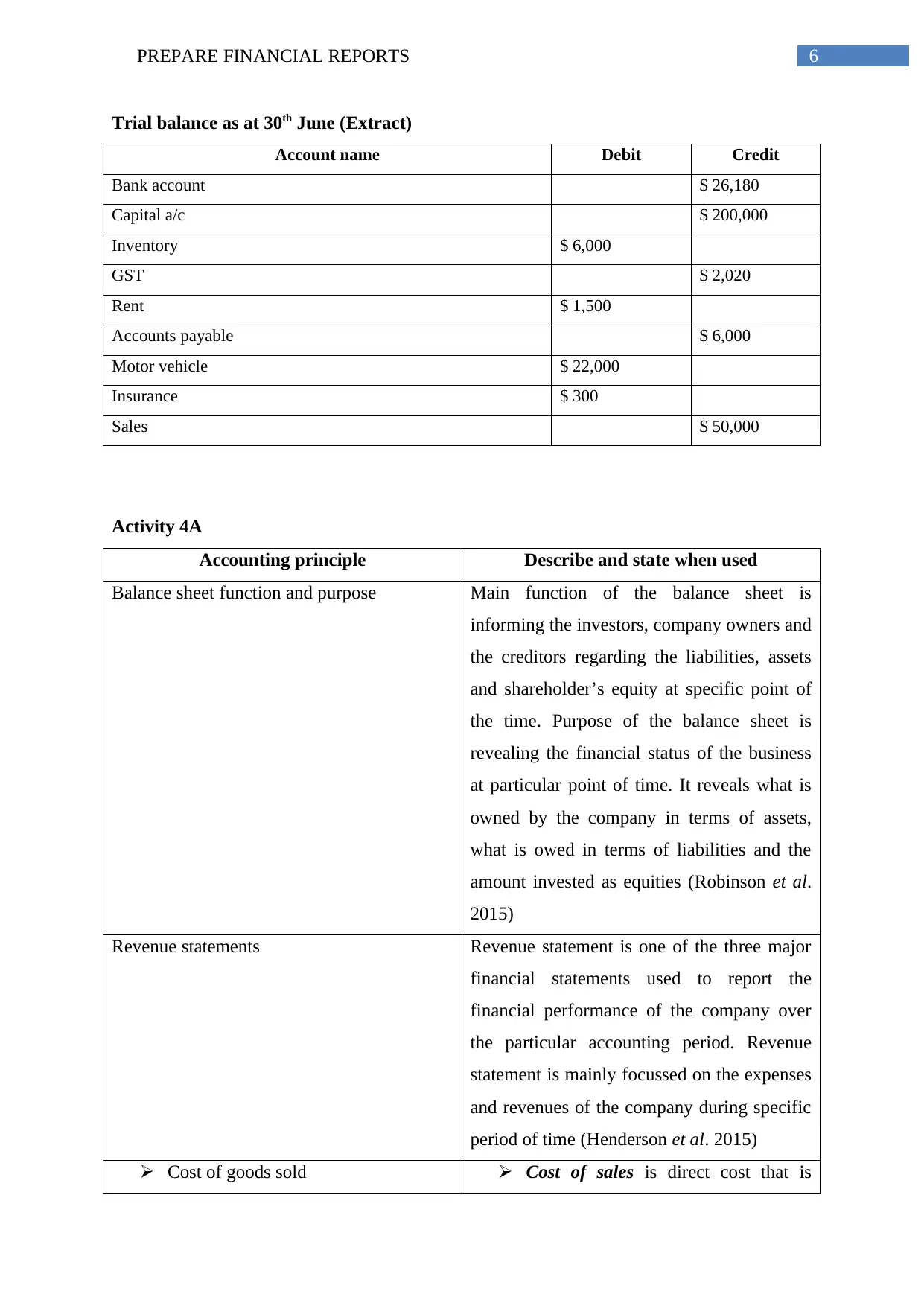

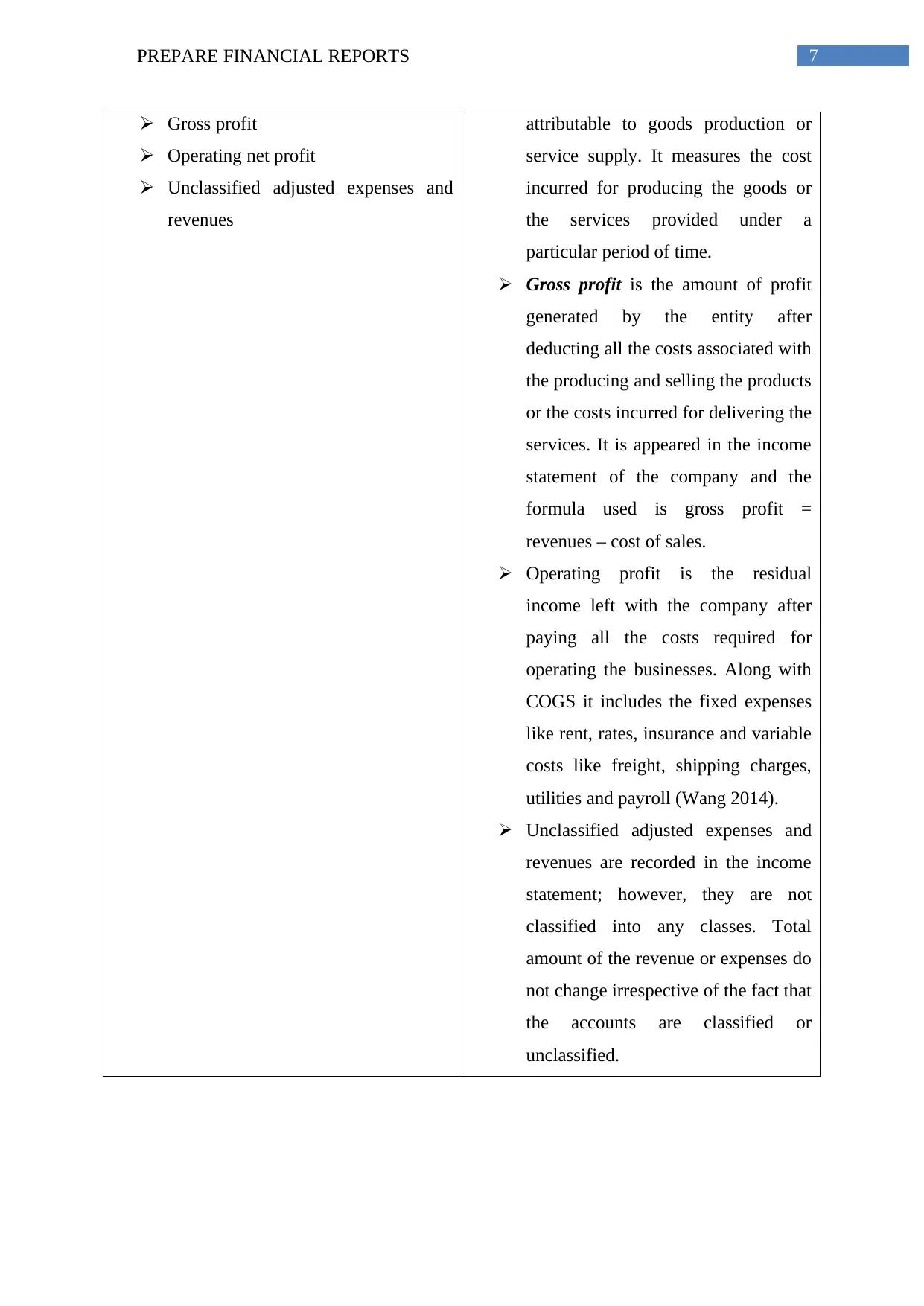

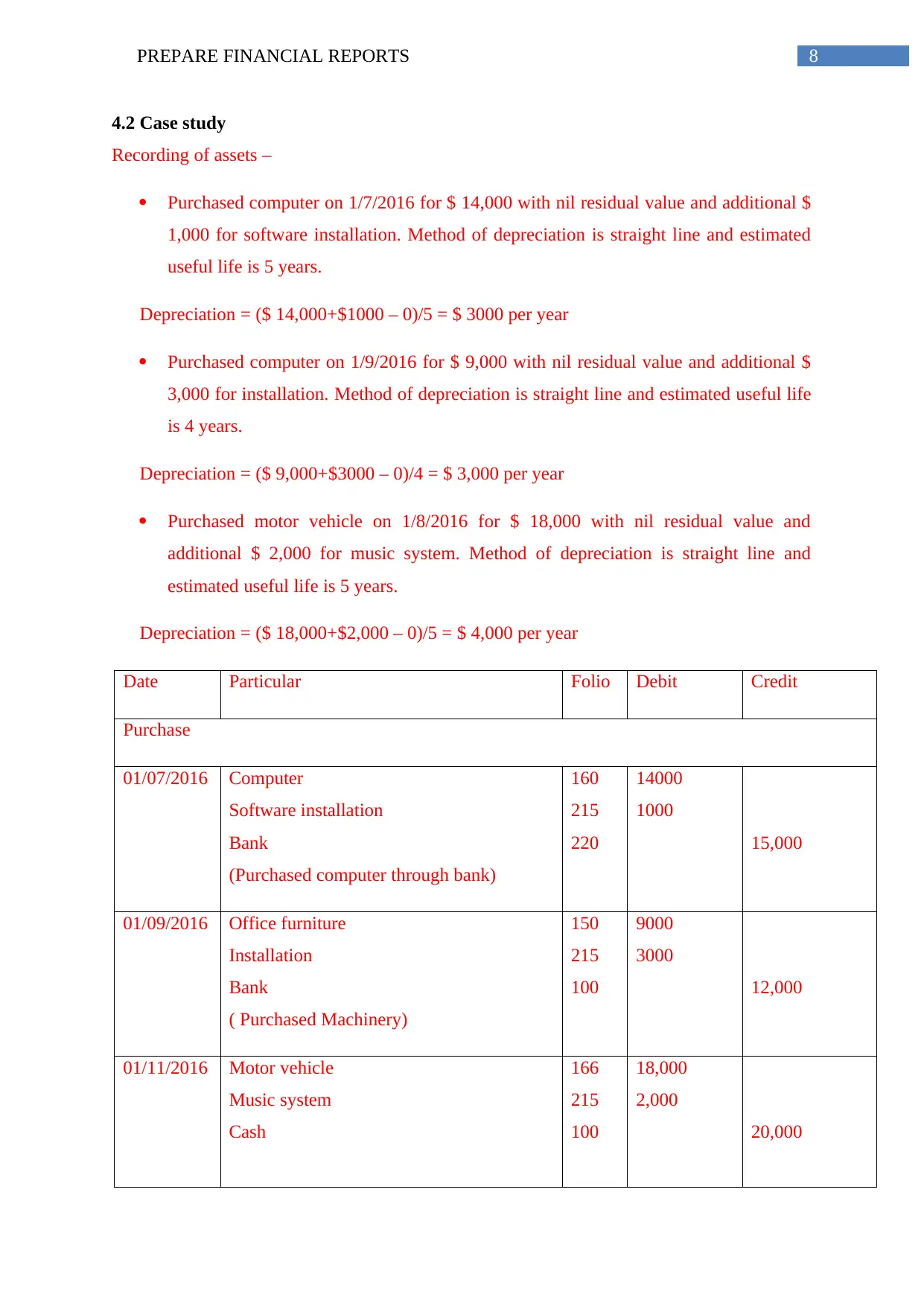

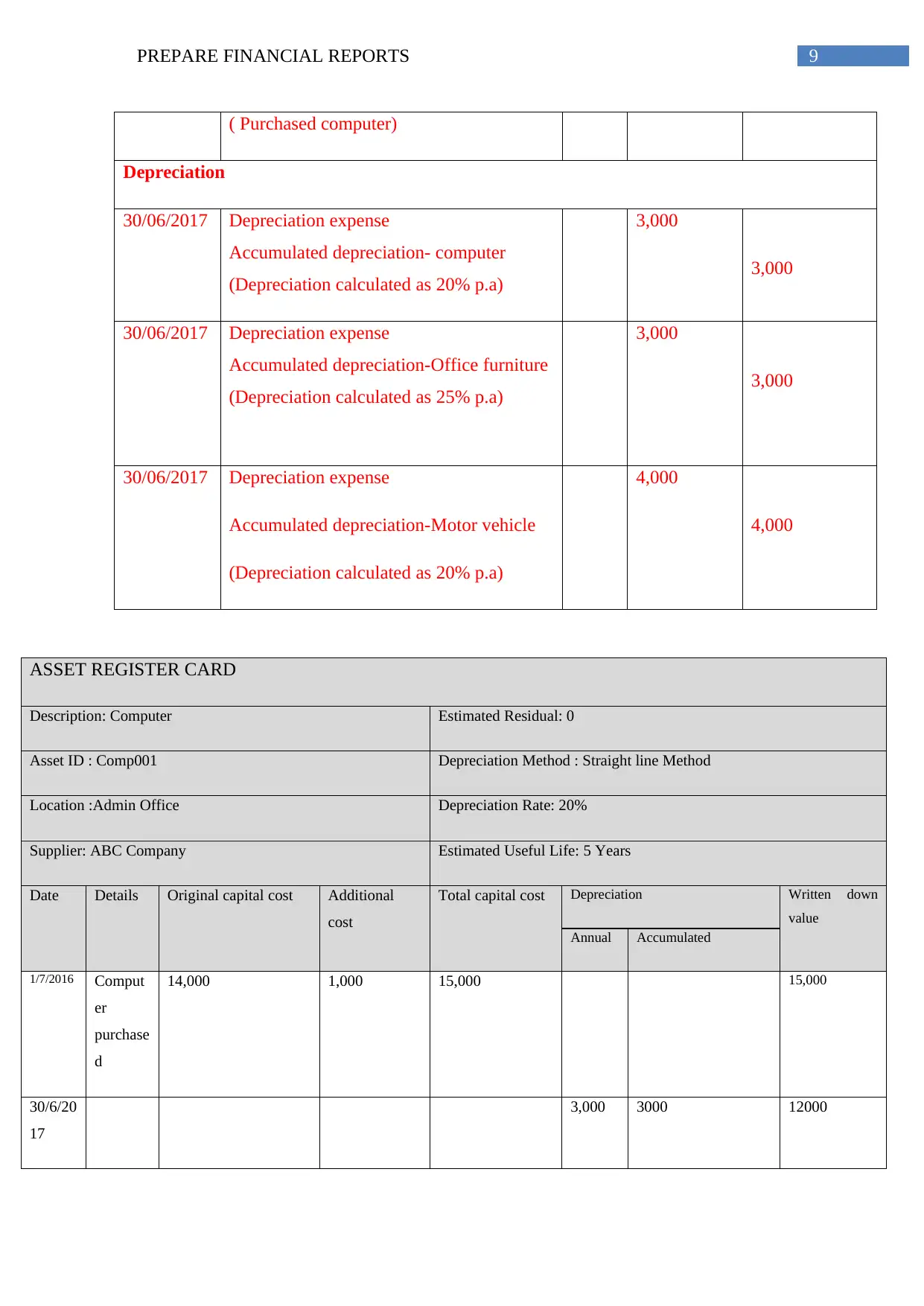

This report delves into the intricacies of financial reporting, commencing with an exploration of fundamental accounting principles such as double-entry bookkeeping and the use of general journals and ledgers. It then examines Goods and Services Tax (GST) regulations in Australia and presents detailed examples of journal entries and general ledger postings, culminating in a trial balance. The report further analyzes the balance sheet and revenue statements, including cost of goods sold, gross profit, and operating profit. A case study is presented, demonstrating the recording and depreciation of assets using the straight-line method, supported by asset register cards. Finally, the report incorporates project work, addressing the fixed asset register, depreciation methods, and the computation of depreciation, providing a comprehensive overview of financial reporting practices.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.