Corporate and Financial Reporting 1: Equity Analysis and Reporting

VerifiedAdded on 2023/06/05

|32

|4175

|314

Report

AI Summary

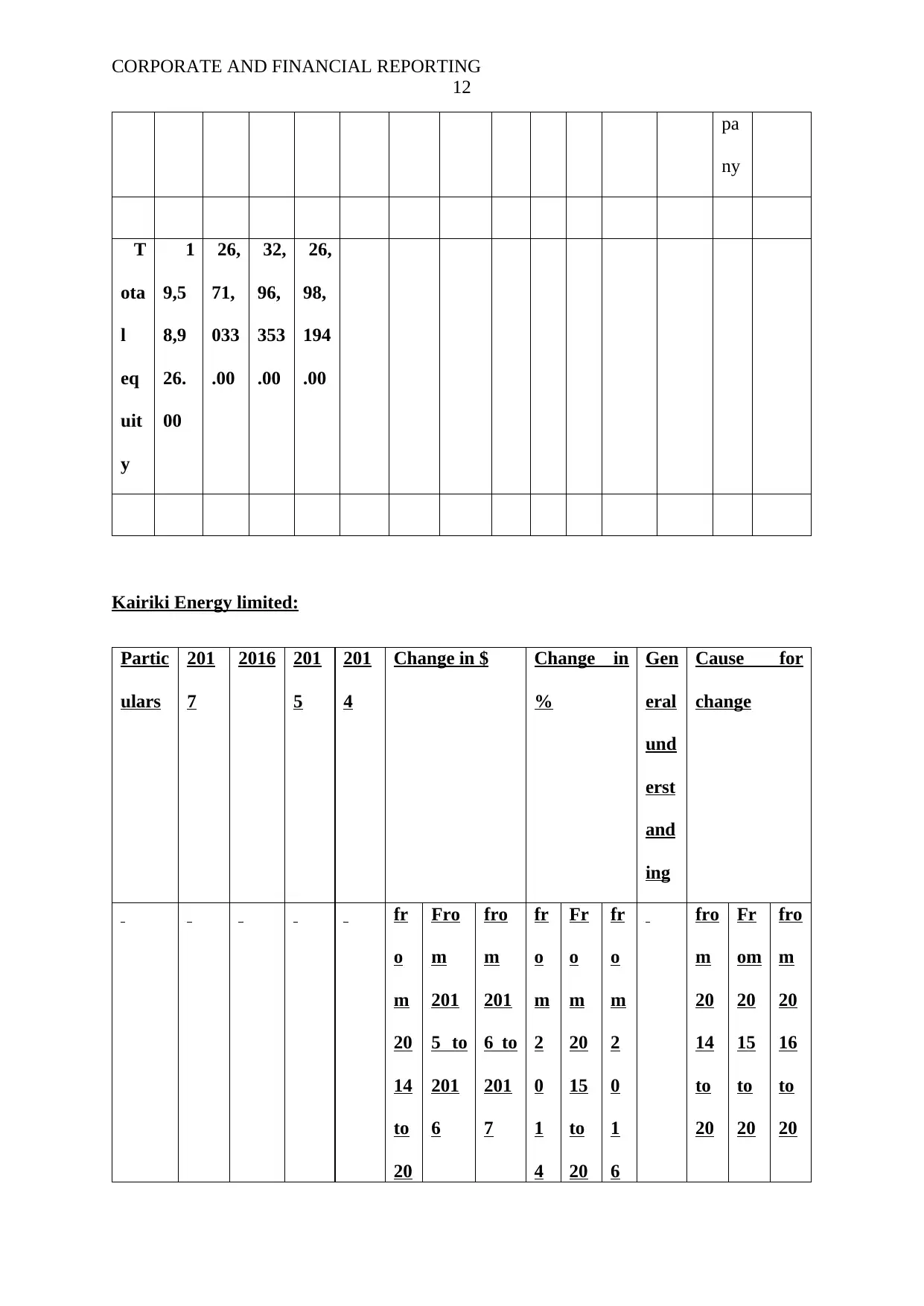

This report provides an in-depth analysis of financial accounting and reporting practices, focusing on the significance of financial transactions and the preparation of financial statements for external stakeholders like investors and creditors. It explores the roles of the AASB and IASB in setting accounting standards, highlighting the differences in their scope and influence. The report then delves into the concept of owner's equity, analyzing its components and changes over time for four selected companies. The analysis includes the examination of share capital, reserves, and accumulated losses, providing insights into the causes of equity fluctuations. The report also includes a discussion on the debt-to-equity ratios of the selected companies. The report concludes with a discussion on the importance of accurate financial reporting and its impact on decision-making, both internally and externally.

1 out of 32

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.