Financial Accounting Report: Recent Changes, Appliance Ltd Analysis

VerifiedAdded on 2020/11/12

|10

|2343

|170

Report

AI Summary

This financial accounting report begins with an introduction to financial reporting and its importance. It then delves into recent changes and developments in financial reporting, discussing the roles of various accounting boards like ASIC, AASB, IASB, and IFRS, and their impact on financial disclosure. The report also examines the Australian Stock Exchange (ASX) and its rules and guidelines. The core of the report involves a practical application of accounting principles through the preparation of journal entries, an income statement, a balance sheet, and a statement of changes in equity for Appliance Ltd. The report calculates depreciation, prepares financial statements, and analyzes the financial performance and position of the company, concluding with a summary of the findings and referencing relevant literature.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Drafting financial reports which ascertains changes, development and news relevant with

financial reporting in a period................................................................................................1

QUESTION 2...................................................................................................................................3

Preparing the Journal entries..................................................................................................3

Income statement....................................................................................................................4

Balance sheet..........................................................................................................................5

Statement of changes in equity...............................................................................................6

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Drafting financial reports which ascertains changes, development and news relevant with

financial reporting in a period................................................................................................1

QUESTION 2...................................................................................................................................3

Preparing the Journal entries..................................................................................................3

Income statement....................................................................................................................4

Balance sheet..........................................................................................................................5

Statement of changes in equity...............................................................................................6

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

INTRODUCTION

There is always an influence of financial accounting that presents the financial disclosure of

the accounts for an adequate necessary as per making effective changes and determination of all

operations. Financial Reporting consists of various accounts and statements which are needed to

express the financial stability of an organisation, especially among the users of such accounts.

In the present report, there will be a discussion based on recent changes and development

made in the financial reporting style. It will be based on demonstrating current news, which will

be based on guidelines issued by ASIC, AASB and IASB with respect to better records of the

accounts. Along with this, there has been a preparation of various final accounts such as journal

entries income statement, balance sheet and statement of changes in equity for Appliance Ltd.

QUESTION 1

Drafting financial reports to ascertains changes, development and news

An Influence of various accounting and reporting techniques, which will be adequate in

making suggestive changes as well as reporting of all assets. Financial reports and accounts will

be adequate in making the qualitative changes in the operations as well as the management of all

transactional activities. Implicating the techniques, rules and regulations were based on preparing

an adequate financial report that will be helpful for proper recording and disclosure of all

accounts (Joubert, Garvie & Parle, 2017). Provision and policies have been set by various

accounting boards with respect to making suggestive changes in the operational practices and

management of it in the due period.

There are various boards, which are currently operating as per bringing suggestive

guidelines to the accounting professionals and auditors in an entity as per making effective

records in the statements. However, there are various financial reporting issues which have been

resolved by these organisations and boards with the motive of bringing a transparent financial

disclosure (Dunbar & Laing, 2017). In relation with this aspect, ASX listed various rules and

principles on which the framework and structure are needed to be followed by the firm which

makes the financial disclosure as well as operations in the capital markets.

1

There is always an influence of financial accounting that presents the financial disclosure of

the accounts for an adequate necessary as per making effective changes and determination of all

operations. Financial Reporting consists of various accounts and statements which are needed to

express the financial stability of an organisation, especially among the users of such accounts.

In the present report, there will be a discussion based on recent changes and development

made in the financial reporting style. It will be based on demonstrating current news, which will

be based on guidelines issued by ASIC, AASB and IASB with respect to better records of the

accounts. Along with this, there has been a preparation of various final accounts such as journal

entries income statement, balance sheet and statement of changes in equity for Appliance Ltd.

QUESTION 1

Drafting financial reports to ascertains changes, development and news

An Influence of various accounting and reporting techniques, which will be adequate in

making suggestive changes as well as reporting of all assets. Financial reports and accounts will

be adequate in making the qualitative changes in the operations as well as the management of all

transactional activities. Implicating the techniques, rules and regulations were based on preparing

an adequate financial report that will be helpful for proper recording and disclosure of all

accounts (Joubert, Garvie & Parle, 2017). Provision and policies have been set by various

accounting boards with respect to making suggestive changes in the operational practices and

management of it in the due period.

There are various boards, which are currently operating as per bringing suggestive

guidelines to the accounting professionals and auditors in an entity as per making effective

records in the statements. However, there are various financial reporting issues which have been

resolved by these organisations and boards with the motive of bringing a transparent financial

disclosure (Dunbar & Laing, 2017). In relation with this aspect, ASX listed various rules and

principles on which the framework and structure are needed to be followed by the firm which

makes the financial disclosure as well as operations in the capital markets.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Australian Accounting Standard Board

This is a personal accounting board in Australia which is comprised for presenting the

fruitful disclosure of all accounts on which determination of actual financial status of an

organisation. It is concerned with the facts that states as this board is aimed at preserving an

adequate framework and structure of preparing the accounts or recoding data set.

However, there has been a list of various standards which will be helpful to the business

in analysing the actual amendments (Morris, 2017). It can be analysed such as First-time

adoption of Australian Accounting standards, share-based payments, business combinations,

insurance contracts etc.

International Accounting Standard Board

This board is created for making an adequate disclosure of the accounts which will be

based on presenting the appropriate framework and operational benefits for better recording of

all transactions. Governance and the execution of entire accounting process in an organisation

will be based on preparing reporting of statements. It is necessary that the accounting

professionals and auditors in an organisation must follow the instructions and make the fruitful

operational rise in the activities (Šehović & et.al., 2018). This board is comprised on delivering

information relevant with the procedures to be followed in preparing final accounts.

There has been an influence of various techniques and methods on which preparing the

statements like income statement, balance sheet and statement of change in equity. These are the

principles which is universally accepted and acknowledged by all countries in the world. It

brings fruitfulness to MNC’s in relation with getting the international investors (Nadeem, Zaman

& Saleem, 2017). Thus, it will positivity affect capital structure of the firm.

Australian Stock Exchange:

As per analysing the framework of ASX in capital market there have been various rule,

norms and amendments which were needed to be followed by accounting professionals. To bring

an organisation in the capital market as per making trade practices for buying and selling

securities in market (Babones, 2017).

There have been various rules, guidelines and amendments which have been set by this

authority such as:

1

This is a personal accounting board in Australia which is comprised for presenting the

fruitful disclosure of all accounts on which determination of actual financial status of an

organisation. It is concerned with the facts that states as this board is aimed at preserving an

adequate framework and structure of preparing the accounts or recoding data set.

However, there has been a list of various standards which will be helpful to the business

in analysing the actual amendments (Morris, 2017). It can be analysed such as First-time

adoption of Australian Accounting standards, share-based payments, business combinations,

insurance contracts etc.

International Accounting Standard Board

This board is created for making an adequate disclosure of the accounts which will be

based on presenting the appropriate framework and operational benefits for better recording of

all transactions. Governance and the execution of entire accounting process in an organisation

will be based on preparing reporting of statements. It is necessary that the accounting

professionals and auditors in an organisation must follow the instructions and make the fruitful

operational rise in the activities (Šehović & et.al., 2018). This board is comprised on delivering

information relevant with the procedures to be followed in preparing final accounts.

There has been an influence of various techniques and methods on which preparing the

statements like income statement, balance sheet and statement of change in equity. These are the

principles which is universally accepted and acknowledged by all countries in the world. It

brings fruitfulness to MNC’s in relation with getting the international investors (Nadeem, Zaman

& Saleem, 2017). Thus, it will positivity affect capital structure of the firm.

Australian Stock Exchange:

As per analysing the framework of ASX in capital market there have been various rule,

norms and amendments which were needed to be followed by accounting professionals. To bring

an organisation in the capital market as per making trade practices for buying and selling

securities in market (Babones, 2017).

There have been various rules, guidelines and amendments which have been set by this

authority such as:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

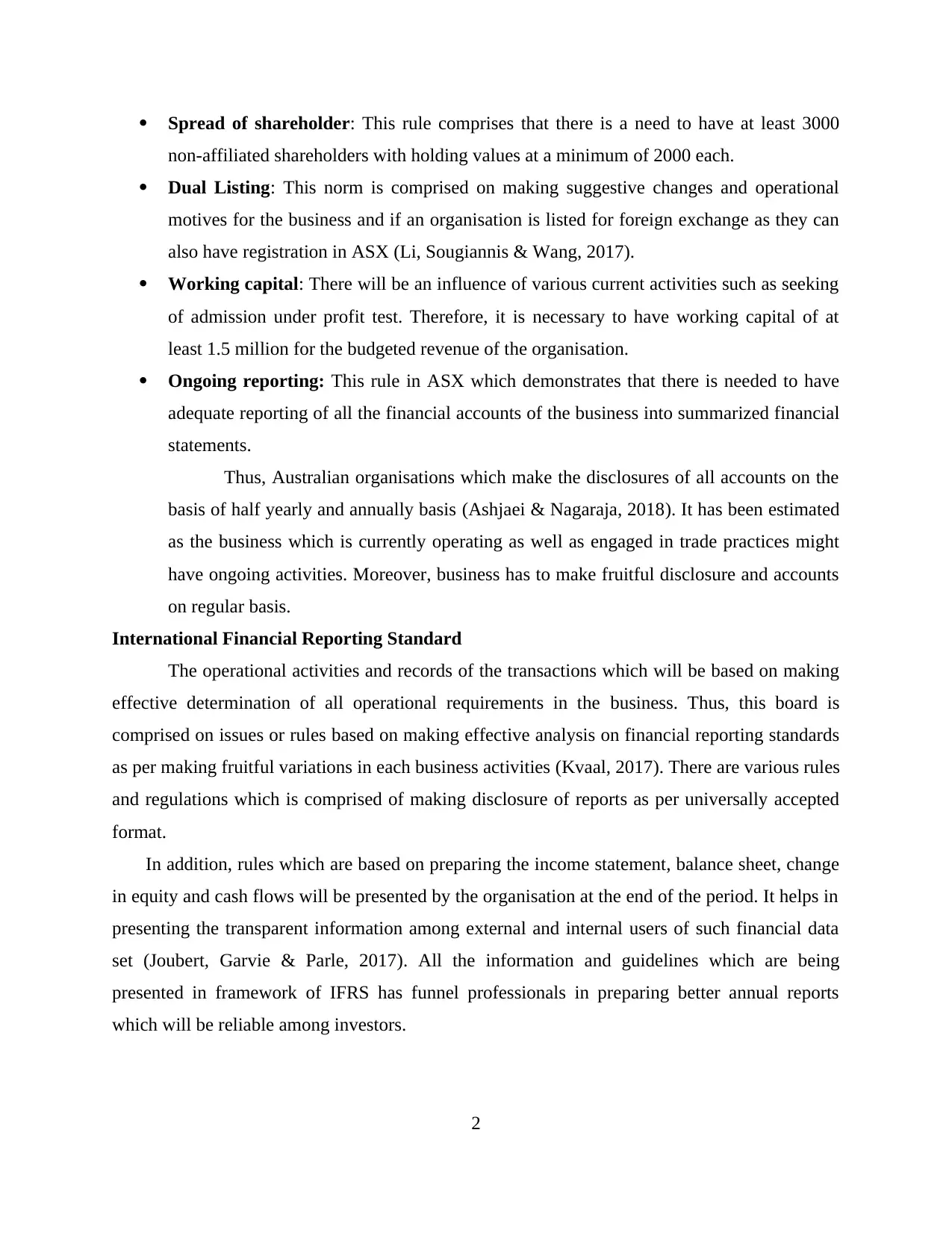

Spread of shareholder: This rule comprises that there is a need to have at least 3000

non-affiliated shareholders with holding values at a minimum of 2000 each.

Dual Listing: This norm is comprised on making suggestive changes and operational

motives for the business and if an organisation is listed for foreign exchange as they can

also have registration in ASX (Li, Sougiannis & Wang, 2017).

Working capital: There will be an influence of various current activities such as seeking

of admission under profit test. Therefore, it is necessary to have working capital of at

least 1.5 million for the budgeted revenue of the organisation.

Ongoing reporting: This rule in ASX which demonstrates that there is needed to have

adequate reporting of all the financial accounts of the business into summarized financial

statements.

Thus, Australian organisations which make the disclosures of all accounts on the

basis of half yearly and annually basis (Ashjaei & Nagaraja, 2018). It has been estimated

as the business which is currently operating as well as engaged in trade practices might

have ongoing activities. Moreover, business has to make fruitful disclosure and accounts

on regular basis.

International Financial Reporting Standard

The operational activities and records of the transactions which will be based on making

effective determination of all operational requirements in the business. Thus, this board is

comprised on issues or rules based on making effective analysis on financial reporting standards

as per making fruitful variations in each business activities (Kvaal, 2017). There are various rules

and regulations which is comprised of making disclosure of reports as per universally accepted

format.

In addition, rules which are based on preparing the income statement, balance sheet, change

in equity and cash flows will be presented by the organisation at the end of the period. It helps in

presenting the transparent information among external and internal users of such financial data

set (Joubert, Garvie & Parle, 2017). All the information and guidelines which are being

presented in framework of IFRS has funnel professionals in preparing better annual reports

which will be reliable among investors.

2

non-affiliated shareholders with holding values at a minimum of 2000 each.

Dual Listing: This norm is comprised on making suggestive changes and operational

motives for the business and if an organisation is listed for foreign exchange as they can

also have registration in ASX (Li, Sougiannis & Wang, 2017).

Working capital: There will be an influence of various current activities such as seeking

of admission under profit test. Therefore, it is necessary to have working capital of at

least 1.5 million for the budgeted revenue of the organisation.

Ongoing reporting: This rule in ASX which demonstrates that there is needed to have

adequate reporting of all the financial accounts of the business into summarized financial

statements.

Thus, Australian organisations which make the disclosures of all accounts on the

basis of half yearly and annually basis (Ashjaei & Nagaraja, 2018). It has been estimated

as the business which is currently operating as well as engaged in trade practices might

have ongoing activities. Moreover, business has to make fruitful disclosure and accounts

on regular basis.

International Financial Reporting Standard

The operational activities and records of the transactions which will be based on making

effective determination of all operational requirements in the business. Thus, this board is

comprised on issues or rules based on making effective analysis on financial reporting standards

as per making fruitful variations in each business activities (Kvaal, 2017). There are various rules

and regulations which is comprised of making disclosure of reports as per universally accepted

format.

In addition, rules which are based on preparing the income statement, balance sheet, change

in equity and cash flows will be presented by the organisation at the end of the period. It helps in

presenting the transparent information among external and internal users of such financial data

set (Joubert, Garvie & Parle, 2017). All the information and guidelines which are being

presented in framework of IFRS has funnel professionals in preparing better annual reports

which will be reliable among investors.

2

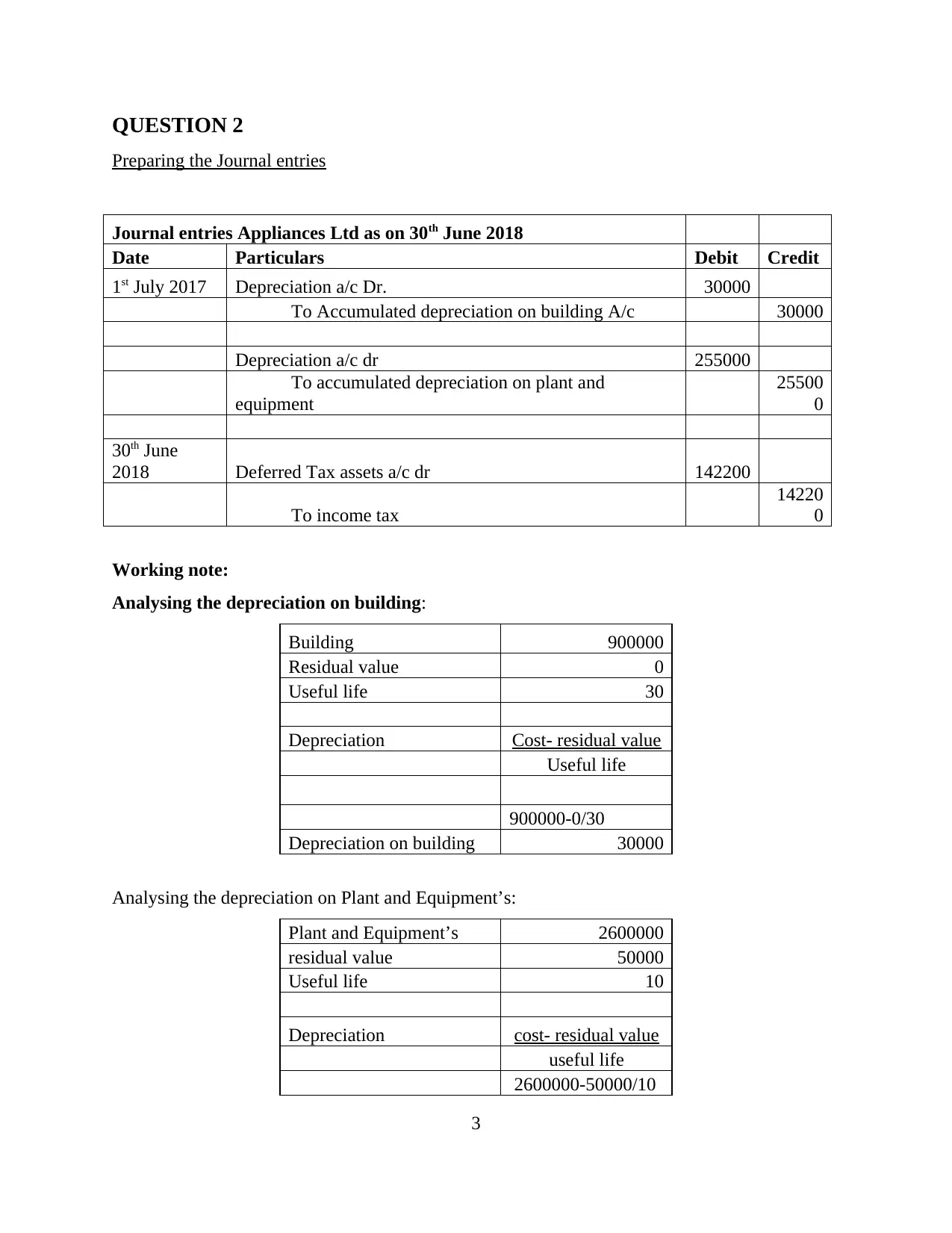

QUESTION 2

Preparing the Journal entries

Journal entries Appliances Ltd as on 30th June 2018

Date Particulars Debit Credit

1st July 2017 Depreciation a/c Dr. 30000

To Accumulated depreciation on building A/c 30000

Depreciation a/c dr 255000

To accumulated depreciation on plant and

equipment

25500

0

30th June

2018 Deferred Tax assets a/c dr 142200

To income tax

14220

0

Working note:

Analysing the depreciation on building:

Building 900000

Residual value 0

Useful life 30

Depreciation Cost- residual value

Useful life

900000-0/30

Depreciation on building 30000

Analysing the depreciation on Plant and Equipment’s:

Plant and Equipment’s 2600000

residual value 50000

Useful life 10

Depreciation cost- residual value

useful life

2600000-50000/10

3

Preparing the Journal entries

Journal entries Appliances Ltd as on 30th June 2018

Date Particulars Debit Credit

1st July 2017 Depreciation a/c Dr. 30000

To Accumulated depreciation on building A/c 30000

Depreciation a/c dr 255000

To accumulated depreciation on plant and

equipment

25500

0

30th June

2018 Deferred Tax assets a/c dr 142200

To income tax

14220

0

Working note:

Analysing the depreciation on building:

Building 900000

Residual value 0

Useful life 30

Depreciation Cost- residual value

Useful life

900000-0/30

Depreciation on building 30000

Analysing the depreciation on Plant and Equipment’s:

Plant and Equipment’s 2600000

residual value 50000

Useful life 10

Depreciation cost- residual value

useful life

2600000-50000/10

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

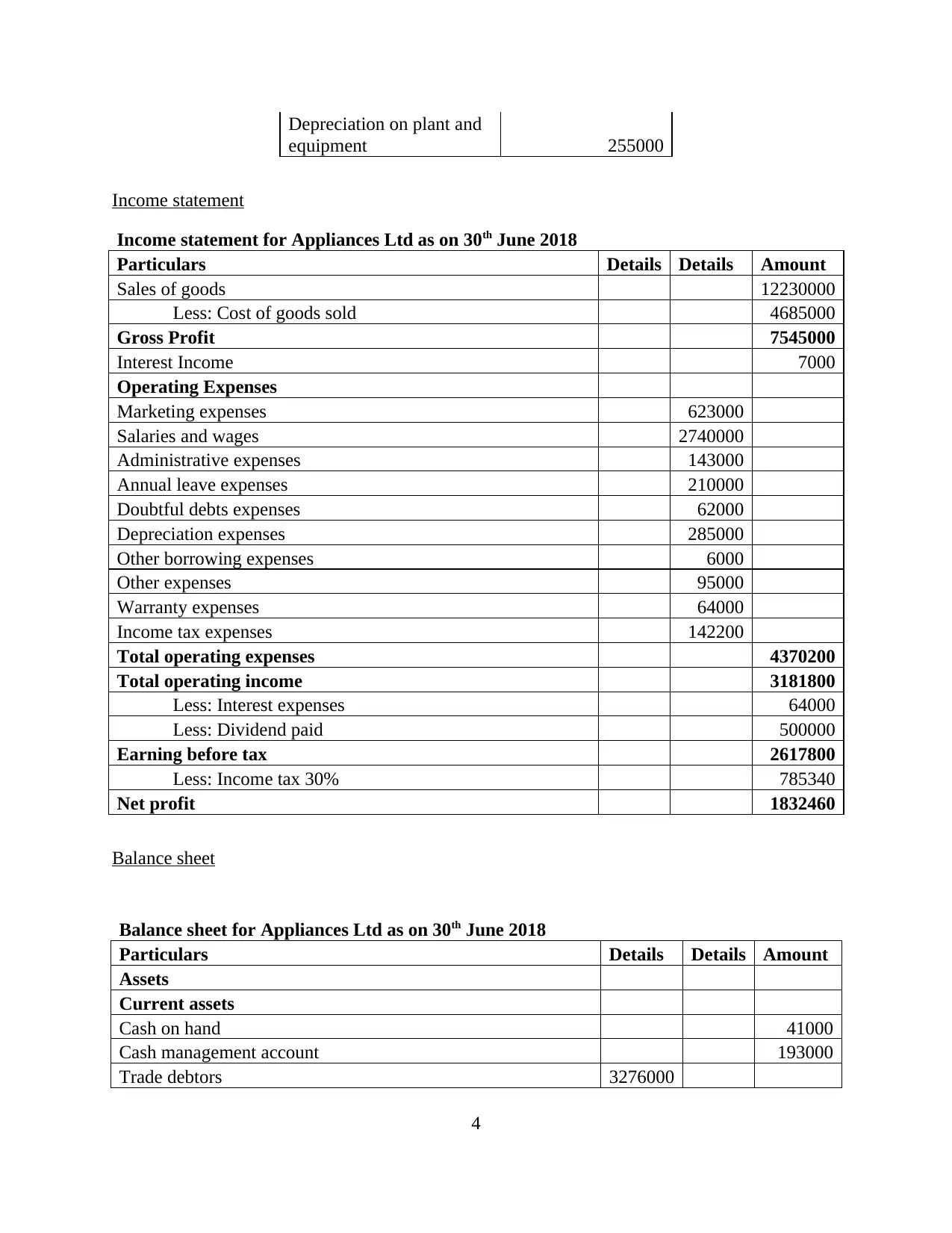

Depreciation on plant and

equipment 255000

Income statement

Income statement for Appliances Ltd as on 30th June 2018

Particulars Details Details Amount

Sales of goods 12230000

Less: Cost of goods sold 4685000

Gross Profit 7545000

Interest Income 7000

Operating Expenses

Marketing expenses 623000

Salaries and wages 2740000

Administrative expenses 143000

Annual leave expenses 210000

Doubtful debts expenses 62000

Depreciation expenses 285000

Other borrowing expenses 6000

Other expenses 95000

Warranty expenses 64000

Income tax expenses 142200

Total operating expenses 4370200

Total operating income 3181800

Less: Interest expenses 64000

Less: Dividend paid 500000

Earning before tax 2617800

Less: Income tax 30% 785340

Net profit 1832460

Balance sheet

Balance sheet for Appliances Ltd as on 30th June 2018

Particulars Details Details Amount

Assets

Current assets

Cash on hand 41000

Cash management account 193000

Trade debtors 3276000

4

equipment 255000

Income statement

Income statement for Appliances Ltd as on 30th June 2018

Particulars Details Details Amount

Sales of goods 12230000

Less: Cost of goods sold 4685000

Gross Profit 7545000

Interest Income 7000

Operating Expenses

Marketing expenses 623000

Salaries and wages 2740000

Administrative expenses 143000

Annual leave expenses 210000

Doubtful debts expenses 62000

Depreciation expenses 285000

Other borrowing expenses 6000

Other expenses 95000

Warranty expenses 64000

Income tax expenses 142200

Total operating expenses 4370200

Total operating income 3181800

Less: Interest expenses 64000

Less: Dividend paid 500000

Earning before tax 2617800

Less: Income tax 30% 785340

Net profit 1832460

Balance sheet

Balance sheet for Appliances Ltd as on 30th June 2018

Particulars Details Details Amount

Assets

Current assets

Cash on hand 41000

Cash management account 193000

Trade debtors 3276000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

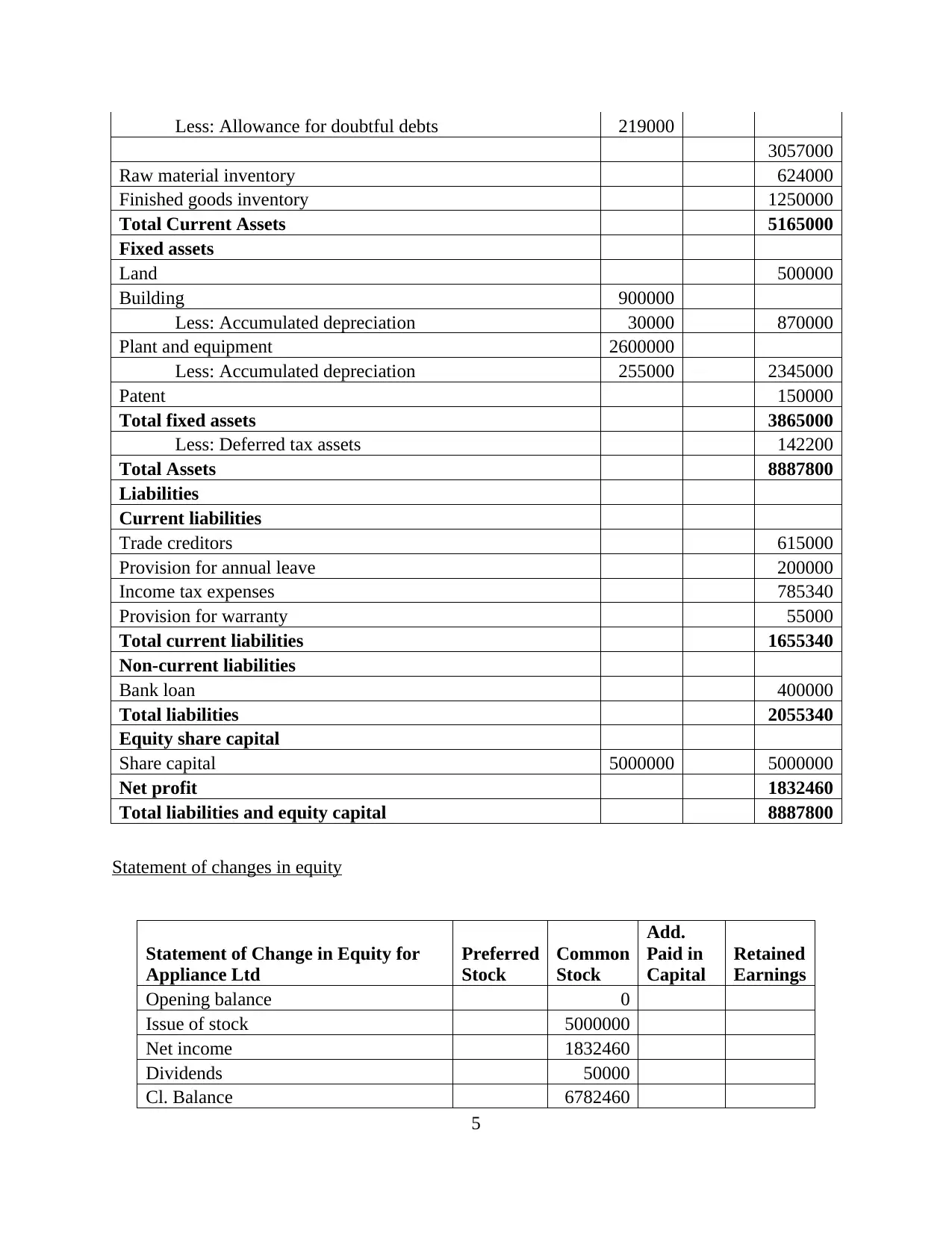

Less: Allowance for doubtful debts 219000

3057000

Raw material inventory 624000

Finished goods inventory 1250000

Total Current Assets 5165000

Fixed assets

Land 500000

Building 900000

Less: Accumulated depreciation 30000 870000

Plant and equipment 2600000

Less: Accumulated depreciation 255000 2345000

Patent 150000

Total fixed assets 3865000

Less: Deferred tax assets 142200

Total Assets 8887800

Liabilities

Current liabilities

Trade creditors 615000

Provision for annual leave 200000

Income tax expenses 785340

Provision for warranty 55000

Total current liabilities 1655340

Non-current liabilities

Bank loan 400000

Total liabilities 2055340

Equity share capital

Share capital 5000000 5000000

Net profit 1832460

Total liabilities and equity capital 8887800

Statement of changes in equity

Statement of Change in Equity for

Appliance Ltd

Preferred

Stock

Common

Stock

Add.

Paid in

Capital

Retained

Earnings

Opening balance 0

Issue of stock 5000000

Net income 1832460

Dividends 50000

Cl. Balance 6782460

5

3057000

Raw material inventory 624000

Finished goods inventory 1250000

Total Current Assets 5165000

Fixed assets

Land 500000

Building 900000

Less: Accumulated depreciation 30000 870000

Plant and equipment 2600000

Less: Accumulated depreciation 255000 2345000

Patent 150000

Total fixed assets 3865000

Less: Deferred tax assets 142200

Total Assets 8887800

Liabilities

Current liabilities

Trade creditors 615000

Provision for annual leave 200000

Income tax expenses 785340

Provision for warranty 55000

Total current liabilities 1655340

Non-current liabilities

Bank loan 400000

Total liabilities 2055340

Equity share capital

Share capital 5000000 5000000

Net profit 1832460

Total liabilities and equity capital 8887800

Statement of changes in equity

Statement of Change in Equity for

Appliance Ltd

Preferred

Stock

Common

Stock

Add.

Paid in

Capital

Retained

Earnings

Opening balance 0

Issue of stock 5000000

Net income 1832460

Dividends 50000

Cl. Balance 6782460

5

CONCLUSION

On the basis of the above report, it can be concluded that the impacts of financial standards

or boards in preparing of the financial accounts in any business has a positive influence. There

had been discussions that were made over various institutions and boards that presented

guidelines to the professionals as per making an effective operational determination of all the

accounts. It involves boards such as IASB, ASIC, ASSB and IFRS. Further, there had been a

preparation for various final accounts such as income statement, balance sheet and statement of

change in equity for Appliance Ltd.

6

On the basis of the above report, it can be concluded that the impacts of financial standards

or boards in preparing of the financial accounts in any business has a positive influence. There

had been discussions that were made over various institutions and boards that presented

guidelines to the professionals as per making an effective operational determination of all the

accounts. It involves boards such as IASB, ASIC, ASSB and IFRS. Further, there had been a

preparation for various final accounts such as income statement, balance sheet and statement of

change in equity for Appliance Ltd.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Ashjaei, N. P., & Nagaraja, N. (2018). Effect of IFRS Adoption on Income Smoothing in Indian

Companies. Asian Journal of Research in Banking and Finance. 8(4). 48-60.

Babones, S. (2017). The Australian Securities Exchange endorses the distributed ledger—but

don’t call it blockchain.

Dunbar, K., & Laing, G. K. (2017). Deconstructing the Accounting Standard AASB 13 Fair

Value: Exit vs Entry Price for Assets. Journal of New Business Ideas & Trends. 15(2).

Joubert, M., Garvie, L., & Parle, G. (2017). Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance

Sheet. Journal of New Business Ideas & Trends. 15(2).

Kvaal, E. (2017). The role and current status of IFRS in the completion of national accounting

rules–Evidence from Norway. Accounting in Europe. 14(1-2). 150-157.

Li, S., Sougiannis, T., & Wang, I. (2017). Mandatory IFRS Adoption and the Usefulness of

Accounting Information in Predicting Future Earnings and Cash Flows.

Morris, R. D. (2017). Discussion of: The Phoenix Rises: The Australian Accounting Standards

Board and IFRS Adoption. Journal of International Accounting Research. 16(2). 155-

157.

Nadeem, M., Zaman, R., & Saleem, I. (2017). Boardroom gender diversity and corporate

sustainability practices: Evidence from Australian Securities Exchange listed

firms. Journal of Cleaner Production. 149. 874-885.

Šehović, E., & et.al., (2018). Network Analysis on the in Silico Assigned Y Chromosome

Haplogroups in Western Balkan Populations. Genetics & Applications. 1(2). 36-43.

7

Books and Journals

Ashjaei, N. P., & Nagaraja, N. (2018). Effect of IFRS Adoption on Income Smoothing in Indian

Companies. Asian Journal of Research in Banking and Finance. 8(4). 48-60.

Babones, S. (2017). The Australian Securities Exchange endorses the distributed ledger—but

don’t call it blockchain.

Dunbar, K., & Laing, G. K. (2017). Deconstructing the Accounting Standard AASB 13 Fair

Value: Exit vs Entry Price for Assets. Journal of New Business Ideas & Trends. 15(2).

Joubert, M., Garvie, L., & Parle, G. (2017). Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance

Sheet. Journal of New Business Ideas & Trends. 15(2).

Kvaal, E. (2017). The role and current status of IFRS in the completion of national accounting

rules–Evidence from Norway. Accounting in Europe. 14(1-2). 150-157.

Li, S., Sougiannis, T., & Wang, I. (2017). Mandatory IFRS Adoption and the Usefulness of

Accounting Information in Predicting Future Earnings and Cash Flows.

Morris, R. D. (2017). Discussion of: The Phoenix Rises: The Australian Accounting Standards

Board and IFRS Adoption. Journal of International Accounting Research. 16(2). 155-

157.

Nadeem, M., Zaman, R., & Saleem, I. (2017). Boardroom gender diversity and corporate

sustainability practices: Evidence from Australian Securities Exchange listed

firms. Journal of Cleaner Production. 149. 874-885.

Šehović, E., & et.al., (2018). Network Analysis on the in Silico Assigned Y Chromosome

Haplogroups in Western Balkan Populations. Genetics & Applications. 1(2). 36-43.

7

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.