Financial Accounting Report: Regulations, Clients and Analysis

VerifiedAdded on 2020/10/22

|47

|5713

|177

Report

AI Summary

This report provides a detailed overview of financial accounting, starting with an introduction to its importance in business and the preparation of financial statements. It includes a discussion of accounting regulations, principles, and concepts, emphasizing their role in producing reliable financial information. The report analyzes various client scenarios, presenting journal entries, ledger accounts, trial balances, income statements, and balance sheets. It also covers bank reconciliation statements, suspense accounts, and control accounts. Furthermore, the report outlines key accounting principles such as GAAP, economic assumptions, the principle of full disclosure, going concern principle, materiality principle, and monetary unit assumption. The report also includes the concepts of consistency and material disclosure. The report concludes by emphasizing the crucial role of accounting in providing clarity regarding business transactions and overall financial health.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A. Produce a report to Line Manager for discussing accounting regulations........................1

Material disclosure and consistency concepts........................................................................4

CLIENT 1........................................................................................................................................5

A. Journal entries for the sole trader......................................................................................5

B. Producing ledger accounts for business...........................................................................10

C. Preparing trial balance for firm........................................................................................18

M1. Compiling trial balance by taking purchase and sale transactions...............................19

M2. Trial balance by considering accounting rules and regulations....................................20

CLIENT 2......................................................................................................................................20

A. Income statement for the sole trader................................................................................20

B. Balance sheet for firm......................................................................................................21

CLIENT 3......................................................................................................................................22

A. Profit and Loss account for organisation.........................................................................22

B. Balance sheet for Raintree Ltd.........................................................................................23

..............................................................................................................................................25

..............................................................................................................................................26

..............................................................................................................................................27

..............................................................................................................................................28

..............................................................................................................................................28

C. Outlining principles and concepts of accounting.............................................................28

D. Importance of measuring and presenting depreciation in financials...............................29

M2. Assessing P&L, balance sheet and cash flow statements.............................................29

D2. Accurate calculations in accounting for producing financial statements......................29

CLIENT 4......................................................................................................................................30

A. Preparation of bank reconciliation statement..................................................................30

B. Causes of recording transaction in bank reconciliation statement...................................30

C. Producing cash books......................................................................................................30

..............................................................................................................................................31

INTRODUCTION...........................................................................................................................1

A. Produce a report to Line Manager for discussing accounting regulations........................1

Material disclosure and consistency concepts........................................................................4

CLIENT 1........................................................................................................................................5

A. Journal entries for the sole trader......................................................................................5

B. Producing ledger accounts for business...........................................................................10

C. Preparing trial balance for firm........................................................................................18

M1. Compiling trial balance by taking purchase and sale transactions...............................19

M2. Trial balance by considering accounting rules and regulations....................................20

CLIENT 2......................................................................................................................................20

A. Income statement for the sole trader................................................................................20

B. Balance sheet for firm......................................................................................................21

CLIENT 3......................................................................................................................................22

A. Profit and Loss account for organisation.........................................................................22

B. Balance sheet for Raintree Ltd.........................................................................................23

..............................................................................................................................................25

..............................................................................................................................................26

..............................................................................................................................................27

..............................................................................................................................................28

..............................................................................................................................................28

C. Outlining principles and concepts of accounting.............................................................28

D. Importance of measuring and presenting depreciation in financials...............................29

M2. Assessing P&L, balance sheet and cash flow statements.............................................29

D2. Accurate calculations in accounting for producing financial statements......................29

CLIENT 4......................................................................................................................................30

A. Preparation of bank reconciliation statement..................................................................30

B. Causes of recording transaction in bank reconciliation statement...................................30

C. Producing cash books......................................................................................................30

..............................................................................................................................................31

..............................................................................................................................................31

M3. Reconciliation process and related accounting terms...................................................31

D3. Producing bank reconciliation statement.......................................................................32

CLIENT 5......................................................................................................................................32

A. Producing sales and purchase ledger account for the company......................................32

B. Explaining control account..............................................................................................33

CLIENT 6......................................................................................................................................33

A. Discussing suspense account and main features of suspense account.............................33

B. Preparation of trial balance..............................................................................................33

C. Producing journal entries.................................................................................................34

D. Distinguishing clearing and suspense account................................................................35

M4. Exploring types of accounts..........................................................................................35

D4. Providing accounting methods for organisation............................................................35

CONCLUSION..............................................................................................................................36

REFERENCES..............................................................................................................................37

M3. Reconciliation process and related accounting terms...................................................31

D3. Producing bank reconciliation statement.......................................................................32

CLIENT 5......................................................................................................................................32

A. Producing sales and purchase ledger account for the company......................................32

B. Explaining control account..............................................................................................33

CLIENT 6......................................................................................................................................33

A. Discussing suspense account and main features of suspense account.............................33

B. Preparation of trial balance..............................................................................................33

C. Producing journal entries.................................................................................................34

D. Distinguishing clearing and suspense account................................................................35

M4. Exploring types of accounts..........................................................................................35

D4. Providing accounting methods for organisation............................................................35

CONCLUSION..............................................................................................................................36

REFERENCES..............................................................................................................................37

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is crucial branch of accounting which is required for preparation of

financial statements in effective way. Present report deals with importance of accounting in the

business in order to record various transactions that occurs on day-to-day basis. The solutions for

various clients are provided by seeking information given and as a result, financials are prepared.

In accordance to this, journal entries are made, then entries are posted to general ledger accounts

in effective manner. From this, trial balance is formulated to check on errors if any that might

creep in posting entries into ledger. Finally, balance sheet and income statements are drawn.

Apart from this, bank reconciliation statement is prepared to rectify balances of bank and that

with records maintained by firm. Suspense account and control account is explained.

Furthermore, accounting regulations, principles and concepts are discussed which are provided

by various professional bodies. Thus, it can be said that accounting plays crucial role in the

business as it provides clarity regarding the transaction occurred in and classified into their

respective nature of accounts.

A. Produce a report to Line Manager for discussing accounting regulations

To: Line Manager

From: Junior Accountant

Subject: Accounting terms, regulations to be taken into account by organisation

Respected Sir,

Accounting is one of the important functions in the business so that day-to-day

transactions may be effectively recorded (Damodaran, 2016). It is essentially required because

without taking into account various transactions into account, financial statements cannot be

prepared in effectual manner. In carrying out this task, accounting principles and regulations

play a crucial role in preparing financials in the best possible manner. The financials such as

cash flow statement, balance sheet, income statement are important pillars of accounting which

is used to carry out proper financial health of the concern in effective way.

The balance sheet shows assets and liabilities of organisation for a particular period

usually one year. On the other side, cash flow statement effectively shows cash position

whether surplus or deficit exists. While, Profit and Loss account clarifies expenditures incurred

1

Financial accounting is crucial branch of accounting which is required for preparation of

financial statements in effective way. Present report deals with importance of accounting in the

business in order to record various transactions that occurs on day-to-day basis. The solutions for

various clients are provided by seeking information given and as a result, financials are prepared.

In accordance to this, journal entries are made, then entries are posted to general ledger accounts

in effective manner. From this, trial balance is formulated to check on errors if any that might

creep in posting entries into ledger. Finally, balance sheet and income statements are drawn.

Apart from this, bank reconciliation statement is prepared to rectify balances of bank and that

with records maintained by firm. Suspense account and control account is explained.

Furthermore, accounting regulations, principles and concepts are discussed which are provided

by various professional bodies. Thus, it can be said that accounting plays crucial role in the

business as it provides clarity regarding the transaction occurred in and classified into their

respective nature of accounts.

A. Produce a report to Line Manager for discussing accounting regulations

To: Line Manager

From: Junior Accountant

Subject: Accounting terms, regulations to be taken into account by organisation

Respected Sir,

Accounting is one of the important functions in the business so that day-to-day

transactions may be effectively recorded (Damodaran, 2016). It is essentially required because

without taking into account various transactions into account, financial statements cannot be

prepared in effectual manner. In carrying out this task, accounting principles and regulations

play a crucial role in preparing financials in the best possible manner. The financials such as

cash flow statement, balance sheet, income statement are important pillars of accounting which

is used to carry out proper financial health of the concern in effective way.

The balance sheet shows assets and liabilities of organisation for a particular period

usually one year. On the other side, cash flow statement effectively shows cash position

whether surplus or deficit exists. While, Profit and Loss account clarifies expenditures incurred

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and income earned in particular financial year. Hence, all these statements are prepared by

relying on proper accounting practices by accountant so that clear position can be highlighted

regarding health in effective manner.

Accounting principles and regulations governed by the accounting professional bodies

are important because financials cannot be formulated in effective way without abiding by rules

and principles of accounting (Nash, 2018). This helps to effectively prepare proper financials

which highlights true and fair view of financials in the best possible manner. On the other hand,

if regulations are not properly followed, then organisation is not able to produce financials in

effective way. This affects fairness of accounts and as such, it is required that such regulations

and principles should be followed for producing financials with ease. The accounting

information derived through financials is quite useful for the organisation as it imparts to the

external users of financial information for taking enhanced decisions. Creditors' are benefited as

they seek financials and attain clarity about the solvency position of company. On the other

side, investors' are benefited as they analyse profitability aspect of organisation. Moreover,

other users also seek such information and then take decisions. Hence, accounting regulations

are important part in carrying out accounting as firm is benefited by following various requisites

and thus, authentic financials are formulated in effective way.

Financial Accounting

Financial Accounting is useful as past data is used to draw effective financials. In simple

words, monetary transactions which occur on daily basis are taken into account and thus,

financials are prepared with ease. It is required so that proper statements may be formulated and

it may impart necessary information to external users quite effectually (Busco and Quattrone,

2018). This is essentially required because external users rely on financials which serves them

the required information by which they are able to take enhanced decisions.

Apart from external parties, internal management is also benefited by seeking financial

statements because they make strategies and initiates improvement for strengthening internal

operations. It is required to strengthen organisation internally so that output may be produced

more and customers' satisfaction level is enhanced in a better way.

Creditors and investors are able to take better decisions and thus, financial accounting is

2

relying on proper accounting practices by accountant so that clear position can be highlighted

regarding health in effective manner.

Accounting principles and regulations governed by the accounting professional bodies

are important because financials cannot be formulated in effective way without abiding by rules

and principles of accounting (Nash, 2018). This helps to effectively prepare proper financials

which highlights true and fair view of financials in the best possible manner. On the other hand,

if regulations are not properly followed, then organisation is not able to produce financials in

effective way. This affects fairness of accounts and as such, it is required that such regulations

and principles should be followed for producing financials with ease. The accounting

information derived through financials is quite useful for the organisation as it imparts to the

external users of financial information for taking enhanced decisions. Creditors' are benefited as

they seek financials and attain clarity about the solvency position of company. On the other

side, investors' are benefited as they analyse profitability aspect of organisation. Moreover,

other users also seek such information and then take decisions. Hence, accounting regulations

are important part in carrying out accounting as firm is benefited by following various requisites

and thus, authentic financials are formulated in effective way.

Financial Accounting

Financial Accounting is useful as past data is used to draw effective financials. In simple

words, monetary transactions which occur on daily basis are taken into account and thus,

financials are prepared with ease. It is required so that proper statements may be formulated and

it may impart necessary information to external users quite effectually (Busco and Quattrone,

2018). This is essentially required because external users rely on financials which serves them

the required information by which they are able to take enhanced decisions.

Apart from external parties, internal management is also benefited by seeking financial

statements because they make strategies and initiates improvement for strengthening internal

operations. It is required to strengthen organisation internally so that output may be produced

more and customers' satisfaction level is enhanced in a better way.

Creditors and investors are able to take better decisions and thus, financial accounting is

2

the main element in producing authenticated financials of organisation highlighting health in

terms of financial performance. Moreover, profitability, efficiency, solvency and liquidity

aspects of firm are effectively attained which is possible by preparing financial statements by

information provided by such accounting. In relation to this, monetary transactions such

recording in books of prime entry and posting them into ledger and then constructing trial

balance are bases for effectively producing balance sheet, income and cash flow statements

(Constable and Kuasirikun, 2018). In addressing this, taxation authorities are benefited by

seeking financials as it serves them to effectively ascertain tax liability of organisation in the

best possible manner. Thus, it can be said that financial accounting gives clarity regarding

overall position of firm quite effectually.

Regulations of Financial Accounting

The financials are produced in order to gain useful insight with regards to overall

position of company in effective manner. In relation to this, for preparing adequate and

authenticated statements, it is required that accounting regulations must be properly followed by

the organisation so that reliability and transparency may not get diminished. This helps to

produce effective and better statements by relying on various accounting regulations imparted

by professional bodies entrusted to provide guidelines to accountants so that reliable financials

may be prepared in effective way.

In addressing this, financial statements may be manipulated by company which affects

reliability and as such, imparts wrong information to users. It adversely affects them as when

they rely on manipulated statements, decision-making is hampered badly. False information is

provided to them impacting on external parties up to a high extent (Heitzman and Huang,

2018). This should be alleviated in order to produce reliable financials and thus, financial

regulator of UK has given FRC guidelines which have to be effectively followed by

organisation and government also for preparing authenticated financials. The legal frameworks

are listed under-

FRC (Financial Reporting Council)- The body is entitled to foster development in the nation

and regulates organisations and government units as well. Hence, accounting practices are

adopted by accountants quite effectually.

3

terms of financial performance. Moreover, profitability, efficiency, solvency and liquidity

aspects of firm are effectively attained which is possible by preparing financial statements by

information provided by such accounting. In relation to this, monetary transactions such

recording in books of prime entry and posting them into ledger and then constructing trial

balance are bases for effectively producing balance sheet, income and cash flow statements

(Constable and Kuasirikun, 2018). In addressing this, taxation authorities are benefited by

seeking financials as it serves them to effectively ascertain tax liability of organisation in the

best possible manner. Thus, it can be said that financial accounting gives clarity regarding

overall position of firm quite effectually.

Regulations of Financial Accounting

The financials are produced in order to gain useful insight with regards to overall

position of company in effective manner. In relation to this, for preparing adequate and

authenticated statements, it is required that accounting regulations must be properly followed by

the organisation so that reliability and transparency may not get diminished. This helps to

produce effective and better statements by relying on various accounting regulations imparted

by professional bodies entrusted to provide guidelines to accountants so that reliable financials

may be prepared in effective way.

In addressing this, financial statements may be manipulated by company which affects

reliability and as such, imparts wrong information to users. It adversely affects them as when

they rely on manipulated statements, decision-making is hampered badly. False information is

provided to them impacting on external parties up to a high extent (Heitzman and Huang,

2018). This should be alleviated in order to produce reliable financials and thus, financial

regulator of UK has given FRC guidelines which have to be effectively followed by

organisation and government also for preparing authenticated financials. The legal frameworks

are listed under-

FRC (Financial Reporting Council)- The body is entitled to foster development in the nation

and regulates organisations and government units as well. Hence, accounting practices are

adopted by accountants quite effectually.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

IASB (International Accounting Standards Board)- This body is entrusted to provide

guidelines to the company's accountant by which reliable and fair financials may be prepared.

This helps to effectively prepare statements and no false information is indulged in.

IFRS (International Financial Reporting Standards)- The accounting body also imparts

guidelines to the accountants in order to abide by legal framework so that adequate financials

may be formulated in the best possible manner.

Rules for accounting

GAAP (Generally Accepted Accounting Principles) which is another important body

has imparted guidelines for preparing financials in effective manner. The several principles and

rules are described below-

Economic assumption- This accounting rule postulates that organisation analyses economic

environment and as such, assumptions are made accordingly (Libby, 2017). In additional to

this, assumptions are made to estimate how economic environment will impact upon sales and

forthcoming project.

Principle of full disclosure- It states that firm should prepare financials by taking into account

all the monetary transactions. In simple words, to produce reliability, it is needed to compile

financials in single statements so that more transparency may be imparted in a better way.

Going concern principle- The accounting principle states that financial statements are produced

by taking into consideration this principle. It means that firm carries on business for long run

and will not shut down immediately. Observing this, financials are prepared.

Materiality principle- This principle postulates that only material information should be taken

into account which do not affect decision-making by external users. Hence, immaterial items

must be ignored. This is required so that material items are taken into account for producing

financials (Nitzl, 2018).

Monetary unit assumption- The principle is related to monetary value of currencies. The US

Dollar is universally applicable and accepted currency which can be used by organisation in

order to made business transactions in effective manner.

Material disclosure and consistency concepts

4

guidelines to the company's accountant by which reliable and fair financials may be prepared.

This helps to effectively prepare statements and no false information is indulged in.

IFRS (International Financial Reporting Standards)- The accounting body also imparts

guidelines to the accountants in order to abide by legal framework so that adequate financials

may be formulated in the best possible manner.

Rules for accounting

GAAP (Generally Accepted Accounting Principles) which is another important body

has imparted guidelines for preparing financials in effective manner. The several principles and

rules are described below-

Economic assumption- This accounting rule postulates that organisation analyses economic

environment and as such, assumptions are made accordingly (Libby, 2017). In additional to

this, assumptions are made to estimate how economic environment will impact upon sales and

forthcoming project.

Principle of full disclosure- It states that firm should prepare financials by taking into account

all the monetary transactions. In simple words, to produce reliability, it is needed to compile

financials in single statements so that more transparency may be imparted in a better way.

Going concern principle- The accounting principle states that financial statements are produced

by taking into consideration this principle. It means that firm carries on business for long run

and will not shut down immediately. Observing this, financials are prepared.

Materiality principle- This principle postulates that only material information should be taken

into account which do not affect decision-making by external users. Hence, immaterial items

must be ignored. This is required so that material items are taken into account for producing

financials (Nitzl, 2018).

Monetary unit assumption- The principle is related to monetary value of currencies. The US

Dollar is universally applicable and accepted currency which can be used by organisation in

order to made business transactions in effective manner.

Material disclosure and consistency concepts

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Concept of consistency- The accounting concept states that firm should take into account only

that accounting policies which it has used in previous year. In simple words, consistent methods

should be followed in order to produce reliability in the best possible manner. It can be said that

if consistent accounting methods are not taken into then transparency and reliability of

organisation is hampered. Hence, it is required to follow same policies. For instance, if straight

line method is followed by the organisation, then should be followed in forthcoming years in

order to produce reliable information.

Material disclosure- The concept states that material information should be taken into account

which affects financial statements up to a high extent. In other words, immaterial items or

information should be ignored which do not have impact on users of accounting information

and thus, reliability can be ascertained in a better way. The books of accounts should disclose

only material items which is effectively evaluated by external stakeholders and they are able to

take decisions in the best possible manner.

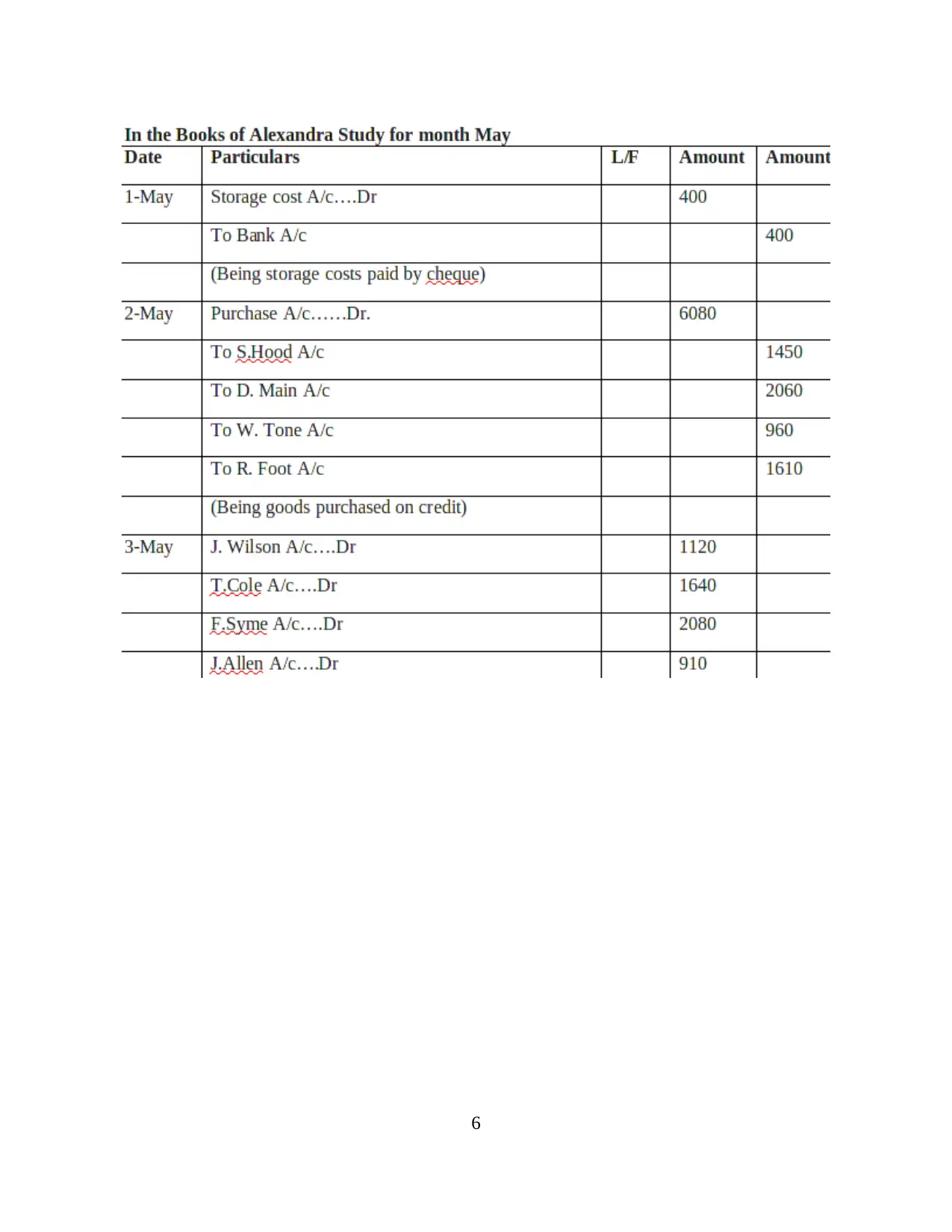

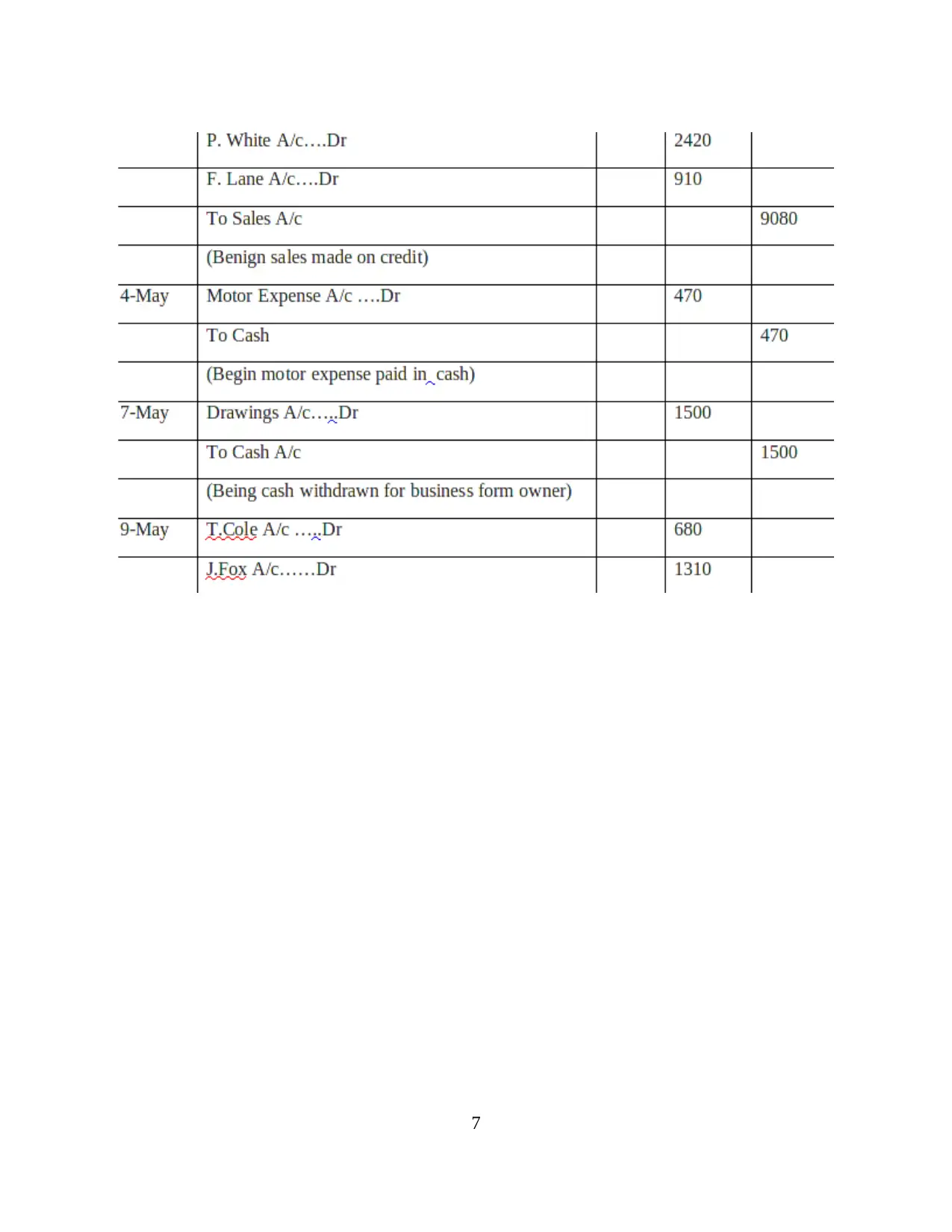

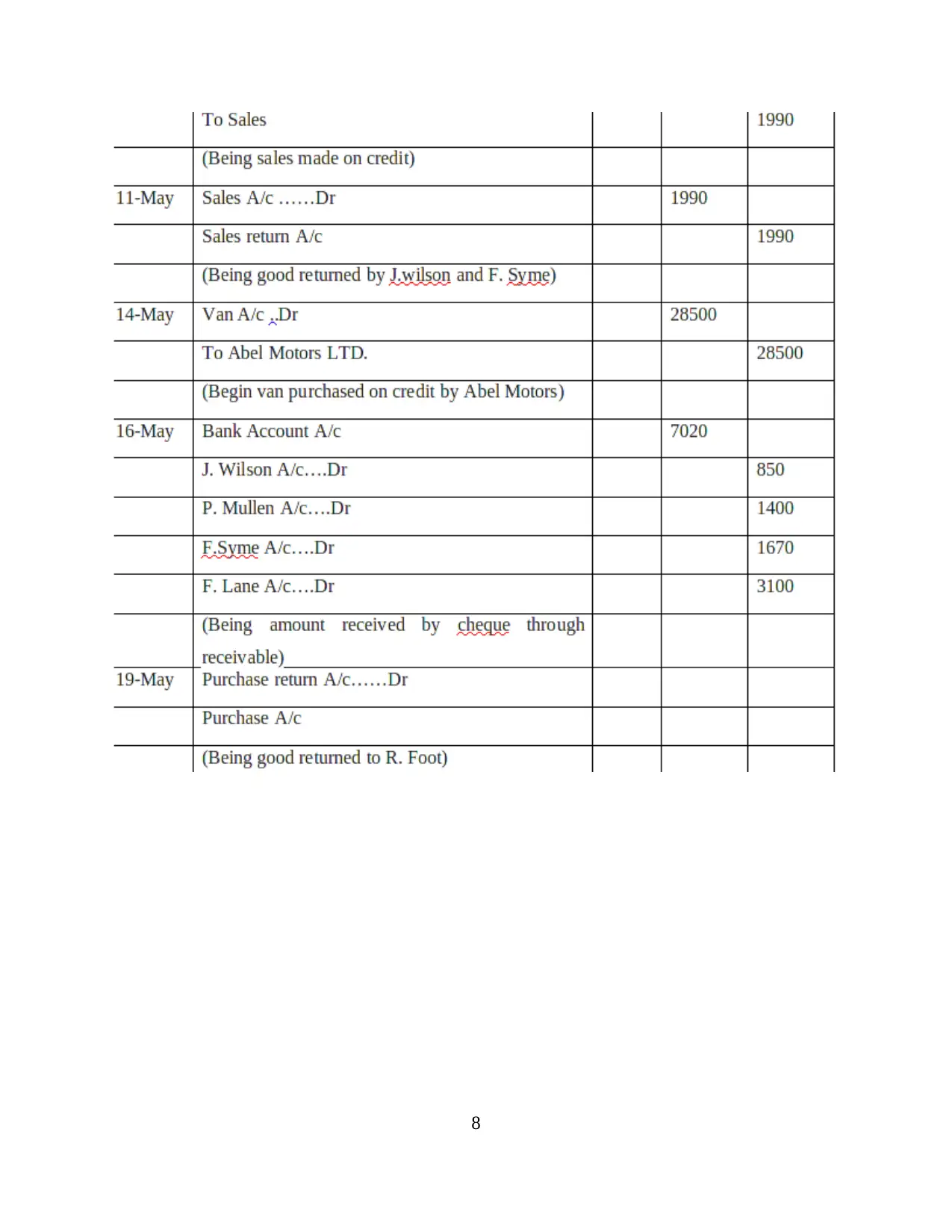

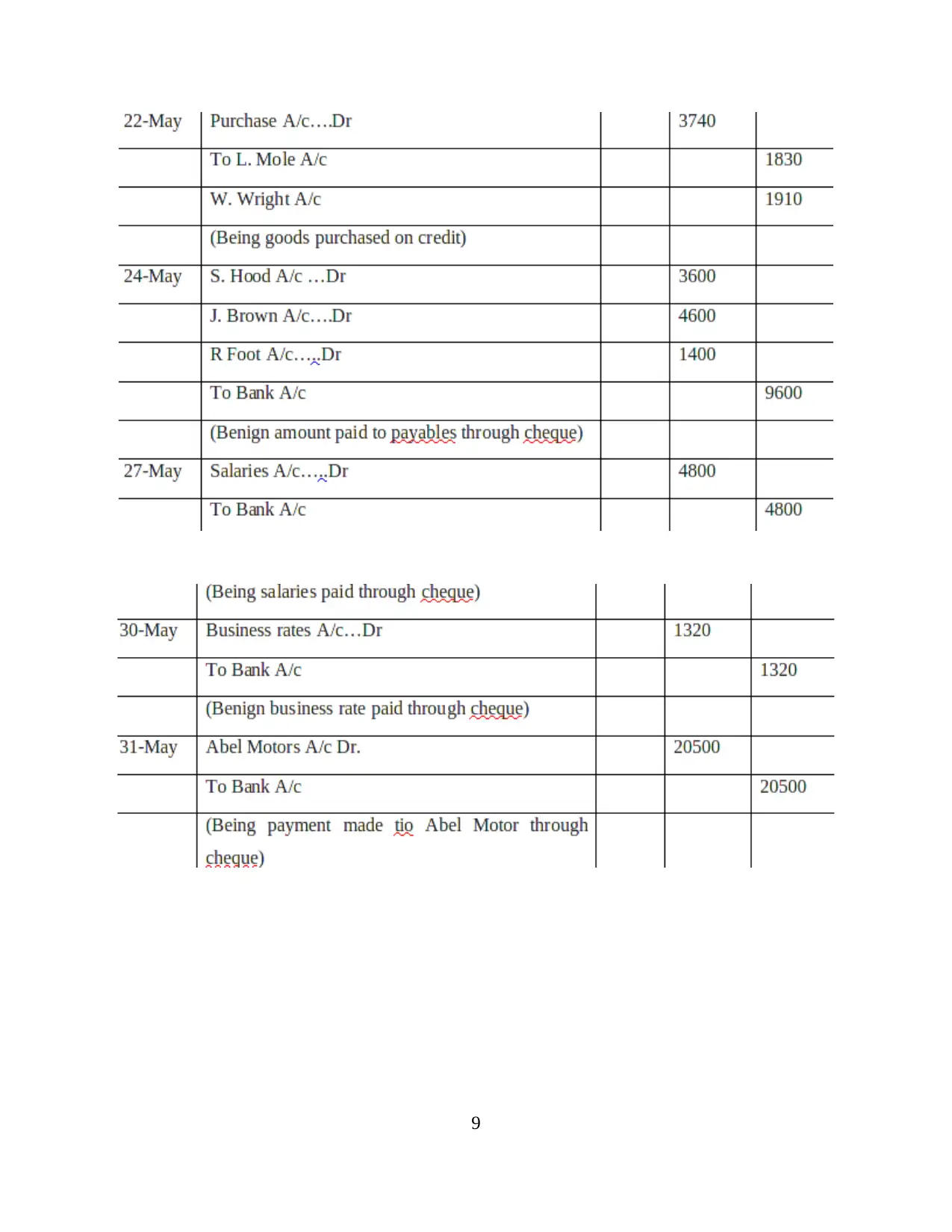

CLIENT 1

A. Journal entries for the sole trader

The transactions are to be recorded in a better way so that receipts and withdrawals may

be effectively ascertained (Schneider, 2018). For recording transactions, books of prime entry

also known as journal is made in the best possible manner. It can be said that for producing

financials, journal entries is the first step which is done by recording business transaction in

chronological order. This is made in chronological order so that every transaction occurred on a

particular date should be recorded on that date only for the purpose of reliability. Hence, entries

are posted in journal so that each and every transaction may be recorded and accounted for quite

effectually. The journal entries are produced for Alexandra firm below-

5

that accounting policies which it has used in previous year. In simple words, consistent methods

should be followed in order to produce reliability in the best possible manner. It can be said that

if consistent accounting methods are not taken into then transparency and reliability of

organisation is hampered. Hence, it is required to follow same policies. For instance, if straight

line method is followed by the organisation, then should be followed in forthcoming years in

order to produce reliable information.

Material disclosure- The concept states that material information should be taken into account

which affects financial statements up to a high extent. In other words, immaterial items or

information should be ignored which do not have impact on users of accounting information

and thus, reliability can be ascertained in a better way. The books of accounts should disclose

only material items which is effectively evaluated by external stakeholders and they are able to

take decisions in the best possible manner.

CLIENT 1

A. Journal entries for the sole trader

The transactions are to be recorded in a better way so that receipts and withdrawals may

be effectively ascertained (Schneider, 2018). For recording transactions, books of prime entry

also known as journal is made in the best possible manner. It can be said that for producing

financials, journal entries is the first step which is done by recording business transaction in

chronological order. This is made in chronological order so that every transaction occurred on a

particular date should be recorded on that date only for the purpose of reliability. Hence, entries

are posted in journal so that each and every transaction may be recorded and accounted for quite

effectually. The journal entries are produced for Alexandra firm below-

5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 47

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.