Financial Accounting Report: FA, Stakeholders, and Statements

VerifiedAdded on 2021/02/21

|29

|3959

|25

Report

AI Summary

This report provides a comprehensive analysis of financial accounting (FA) principles, focusing on the operations of Taj Accountants. It begins with an introduction to FA, its purpose in recording, summarizing, and presenting financial transactions, and its importance for stakeholders. The report then delves into the roles and interests of both internal and external stakeholders, including managers, employees, creditors, investors, and government entities. It covers key accounting concepts such as consistency and prudence, along with depreciation methods like Straight-Line Method (SLM) and Written Down Value (WDV). Furthermore, the report contrasts financial accounting with management accounting and discusses the regulatory framework, including GAAP, IFRS, and the role of the Financial Reporting Council (FRC). The report also presents journal entries, trial balance, income statements and balance sheets for two clients, and it concludes with a comparison of financial statements for sole proprietors and limited companies.

Date assignment marked:__________________________

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION

Financial accounting (FA) is a procedure which is useful in tracking the financial

transaction of company for particular fiscal year. It is an effective tool which helps in recording,

summarizing and presenting the financial records in a systematic and efficient manner.

1

Financial accounting (FA) is a procedure which is useful in tracking the financial

transaction of company for particular fiscal year. It is an effective tool which helps in recording,

summarizing and presenting the financial records in a systematic and efficient manner.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This study will highlight, the purpose of FA, and also examine why stakeholders of the

organization are interested in financial records. This study will record financial transactions

using double entry book keeping. It will also prepare final accounts in compliance with proper

principles, standards and conventions. Furthermore, this study prepare bank reconciliation

statement and also reconcile control systems.

Taj Accountants is a small business accounting firm based in London. They provide

effective accounting services such as payroll, taxation services, advice, business planning, book

keeping, etc.

Part A

1. FA and purpose.

Financial accounting (FA) is a process which is useful in tracking the financial

transaction of the Taj Accountants for particular fiscal year. It is an impelling tool which helps in

recording, summarizing and presenting the financial records in a systematic and standard

manner. This information is presented in financial reports like statement of financial position,

stockholder's equity, income statement and statement for cash flow (Lawrence, 2019). Financial

accounting is done by keeping in mind all the financial reporting standards, conventions and

principles such as (Generally accepted accounting principle) GAAP. FA is useful in critically

analysing the fiscal reports of company and also allocating the resources. It helps in determining

the growth in the Taj Accountants by comparing it with the previous statements. Financial

accounting helps in presenting the financial information in the structured manner for better

understanding and effective decision making for future success and development of the business.

There various users of financial information which mainly includes internal and external

stakeholders and it helps in better decision making. It is useful because it aid in evaluating the

current financial state of the company in a snapshot. This helps in better understanding and

formulation of plans and strategies. FA plays a crucial role in determining the liabilities and asset

of organization. It also helps in comparing the financial position with its competitors in order to

attain desired goals and objectives.

Purpose of FA

FA helps in providing in- depth information of the organization fiscal state and it also

helps in sound decision making in an accurate and efficient manner. The aim of FA is to provide

2

organization are interested in financial records. This study will record financial transactions

using double entry book keeping. It will also prepare final accounts in compliance with proper

principles, standards and conventions. Furthermore, this study prepare bank reconciliation

statement and also reconcile control systems.

Taj Accountants is a small business accounting firm based in London. They provide

effective accounting services such as payroll, taxation services, advice, business planning, book

keeping, etc.

Part A

1. FA and purpose.

Financial accounting (FA) is a process which is useful in tracking the financial

transaction of the Taj Accountants for particular fiscal year. It is an impelling tool which helps in

recording, summarizing and presenting the financial records in a systematic and standard

manner. This information is presented in financial reports like statement of financial position,

stockholder's equity, income statement and statement for cash flow (Lawrence, 2019). Financial

accounting is done by keeping in mind all the financial reporting standards, conventions and

principles such as (Generally accepted accounting principle) GAAP. FA is useful in critically

analysing the fiscal reports of company and also allocating the resources. It helps in determining

the growth in the Taj Accountants by comparing it with the previous statements. Financial

accounting helps in presenting the financial information in the structured manner for better

understanding and effective decision making for future success and development of the business.

There various users of financial information which mainly includes internal and external

stakeholders and it helps in better decision making. It is useful because it aid in evaluating the

current financial state of the company in a snapshot. This helps in better understanding and

formulation of plans and strategies. FA plays a crucial role in determining the liabilities and asset

of organization. It also helps in comparing the financial position with its competitors in order to

attain desired goals and objectives.

Purpose of FA

FA helps in providing in- depth information of the organization fiscal state and it also

helps in sound decision making in an accurate and efficient manner. The aim of FA is to provide

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

necessary data to stakeholders of the Taj Accountancy. It is beneficial in determining the

financial strengths of the organization. It is very useful in communicating the information to the

stakeholders by formulating various financial statements on a timely manner with utmost

accuracy. This provides the snapshot of the financial health of the Taj Accountants in order to

attain greater heights. The main reason of FA is that it helps in determining the best performing

sector of the organization in order to achieve desired objectives and leads to further growth and

success (Lawrence, 2019). It gives relevant and reliable information to the stakeholders which

helps in strategic decision making. It is useful in distinguishing the results with the past historic

statements to evaluate the profitability of the organization over the particular span of period

period. It helps in controlling the cost and increasing the overall productivity of the Taj

Accountants. FA is useful in determining the flaws and take necessary action to resolve the issue

in an accurate and systematic manner. It helps in ascertaining the areas which generates higher

profit and also focuses on evaluating the factors which leads to higher manufacturing cost. It is

very crucial because it helps in forecasting the needs of the future which leads to higher

operational standards and efficiency.

FA vs MA

Financial accounting is a process which is useful in examining the financial position of

the organization to achieve desired goals and objectives. It is very crucial for external

shareholders of the organization to determine the financial position and take strategic decision in

an efficient and timely manner. Financial accounting has to prepared while complying with

various standards such as GAAP, IFRS, etc. It has to be prepared every financial year ending to

determine the position of the company for a particular accounting year.

Management accounting (MA) helps internal stakeholders of the organization to take

appropriate decision. Management accounting helps in providing statistical information which

helps in short term decision making. It is not mandatory to prepare management reports and

statements. But can be prepared anytime during a particular financial year.

Regulatory framework

Regulatory framework is the authority given to the regulators which helps in aligning

various accounting standards in the accounting practice in order to generate accurate and reliable

manner. Their focus is to ensure that the company focuses on maintaining consistency in the

3

financial strengths of the organization. It is very useful in communicating the information to the

stakeholders by formulating various financial statements on a timely manner with utmost

accuracy. This provides the snapshot of the financial health of the Taj Accountants in order to

attain greater heights. The main reason of FA is that it helps in determining the best performing

sector of the organization in order to achieve desired objectives and leads to further growth and

success (Lawrence, 2019). It gives relevant and reliable information to the stakeholders which

helps in strategic decision making. It is useful in distinguishing the results with the past historic

statements to evaluate the profitability of the organization over the particular span of period

period. It helps in controlling the cost and increasing the overall productivity of the Taj

Accountants. FA is useful in determining the flaws and take necessary action to resolve the issue

in an accurate and systematic manner. It helps in ascertaining the areas which generates higher

profit and also focuses on evaluating the factors which leads to higher manufacturing cost. It is

very crucial because it helps in forecasting the needs of the future which leads to higher

operational standards and efficiency.

FA vs MA

Financial accounting is a process which is useful in examining the financial position of

the organization to achieve desired goals and objectives. It is very crucial for external

shareholders of the organization to determine the financial position and take strategic decision in

an efficient and timely manner. Financial accounting has to prepared while complying with

various standards such as GAAP, IFRS, etc. It has to be prepared every financial year ending to

determine the position of the company for a particular accounting year.

Management accounting (MA) helps internal stakeholders of the organization to take

appropriate decision. Management accounting helps in providing statistical information which

helps in short term decision making. It is not mandatory to prepare management reports and

statements. But can be prepared anytime during a particular financial year.

Regulatory framework

Regulatory framework is the authority given to the regulators which helps in aligning

various accounting standards in the accounting practice in order to generate accurate and reliable

manner. Their focus is to ensure that the company focuses on maintaining consistency in the

3

approaches during a specific accounting period (Bennett, 2017). It mainly includes GAAP, IFRS,

IAS. Financial reporting council (FRC) set standards for motoring, reporting and enforcing

accounting standards.

Conceptual framework

Conceptual framework is a set of rules, regulations and standards which are developed by

the IASB (International accounting standard board) to make sure that the uniformity is

maintained in various accounting methods. It helps in setting concepts for guidance and

disclosures.

Going concern concept: This is a fundamental framework which states that the company should

be existing for the foreseeable future period to attain long term organizational goals and

objectives.

Accrual concept: This principle helps in recording of all the revenues earned when the cash is

received by the company in a particular financial year. It helps in determining the expenses and

revenues which has not been received and paid.

2. External and Internal stakeholders.

Internal stakeholders of the organisation are entities within the organization which mainly

includes employees, BOD, managers, owners, etc. they have financial interest in the company

and it mainly focuses on vesting interest on working of the organisation to take strategic decision

(Yarahmadi and Bohloli, 2015). It is useful for internal stakeholders which helps in downsizing

and expansion of the business and take necessary decision to structure the business effectively

for attainment of long run goals and objectives.

Managers: A manager is person who takes strategic decision to control the functioning

of the business concern. Financial accounting information helps managers in taking strategic

decision in relation with the operation of the company. It helps manager in assessing the

profitability and liquidity state of organisation. Financial information helps mangers in analysing

the most profitable units and prioritize the work to attain higher profits and economies of scale. It

is also useful in optimally utilizing the resources by controlling the activities and reducing

wastage.

Employees: employees are internal stakeholders of the business, and they are interested

in the financial reports of the organisation in order to determine the overall performance of the

4

IAS. Financial reporting council (FRC) set standards for motoring, reporting and enforcing

accounting standards.

Conceptual framework

Conceptual framework is a set of rules, regulations and standards which are developed by

the IASB (International accounting standard board) to make sure that the uniformity is

maintained in various accounting methods. It helps in setting concepts for guidance and

disclosures.

Going concern concept: This is a fundamental framework which states that the company should

be existing for the foreseeable future period to attain long term organizational goals and

objectives.

Accrual concept: This principle helps in recording of all the revenues earned when the cash is

received by the company in a particular financial year. It helps in determining the expenses and

revenues which has not been received and paid.

2. External and Internal stakeholders.

Internal stakeholders of the organisation are entities within the organization which mainly

includes employees, BOD, managers, owners, etc. they have financial interest in the company

and it mainly focuses on vesting interest on working of the organisation to take strategic decision

(Yarahmadi and Bohloli, 2015). It is useful for internal stakeholders which helps in downsizing

and expansion of the business and take necessary decision to structure the business effectively

for attainment of long run goals and objectives.

Managers: A manager is person who takes strategic decision to control the functioning

of the business concern. Financial accounting information helps managers in taking strategic

decision in relation with the operation of the company. It helps manager in assessing the

profitability and liquidity state of organisation. Financial information helps mangers in analysing

the most profitable units and prioritize the work to attain higher profits and economies of scale. It

is also useful in optimally utilizing the resources by controlling the activities and reducing

wastage.

Employees: employees are internal stakeholders of the business, and they are interested

in the financial reports of the organisation in order to determine the overall performance of the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company and it also helps in analysing the company's ability to provide additional benefit and

salaries to the employees. It aids employees in evaluating the company's stability position to

access the expansion possibilities and future career growth opportunities to the employees (Users

of Accounting Information, 2019). It is useful to them to evaluate the compensation benefits and

also accurately determine the job security and future remuneration.

External shareholders of organization are entities outside of organization which mainly

includes investors, suppliers, competitors, government, creditors, customers, local community,

etc. every stakeholders have different interest in the fiscal interest of the business.

Creditors: Fiscal data helps company in evaluating the credibility and liquidity state of

the organization. It is useful in determining whether the company will be able to repay the

amount within the stipulated duration of time or not. In case the company is having good

credibility position then the creditors will lend money to the company that results in smooth

working of company. The creditors are interested in financial statement because they are curious

in determining the fiscal liquidity state of the organisation to meet their short term obligations.

Investors: They focus on ascertaining the viability and financial position. The fiscal data

is useful for investors in predicting the dividends of the company based on the profits earned in

the particular financial year (Cascino and et.al., 2017). For example, if the company is generating

higher profit, then the company will give higher dividends to the shareholders. On the contrary,

if the profits are fluctuating this indicates higher risk to the investor and helps them, in taking

strategic decision. FA information helps investor in taking investment decision accurately.

Government: They are external stakeholders and are interested in financial statements to

determine validity of the tax declared in financial reports of the organization. It is useful in

evaluating the tax returns. Financial statements of the organization helps government in tracking

the economic progress by thoroughly analysing the varied sectors of economy. They are

interested in the financial information of the company for regulatory purpose. It helps

government in determining the tax due and tax paid thereon.

Customers: They are concerned in financial reports of the organization as it is useful in

analysing the stability position of the organization (Cascino and et.al., 2017). It is also essential

in determining whether the resources of the organization are effectively utilized in order to attain

desired goals and objectives.

5

salaries to the employees. It aids employees in evaluating the company's stability position to

access the expansion possibilities and future career growth opportunities to the employees (Users

of Accounting Information, 2019). It is useful to them to evaluate the compensation benefits and

also accurately determine the job security and future remuneration.

External shareholders of organization are entities outside of organization which mainly

includes investors, suppliers, competitors, government, creditors, customers, local community,

etc. every stakeholders have different interest in the fiscal interest of the business.

Creditors: Fiscal data helps company in evaluating the credibility and liquidity state of

the organization. It is useful in determining whether the company will be able to repay the

amount within the stipulated duration of time or not. In case the company is having good

credibility position then the creditors will lend money to the company that results in smooth

working of company. The creditors are interested in financial statement because they are curious

in determining the fiscal liquidity state of the organisation to meet their short term obligations.

Investors: They focus on ascertaining the viability and financial position. The fiscal data

is useful for investors in predicting the dividends of the company based on the profits earned in

the particular financial year (Cascino and et.al., 2017). For example, if the company is generating

higher profit, then the company will give higher dividends to the shareholders. On the contrary,

if the profits are fluctuating this indicates higher risk to the investor and helps them, in taking

strategic decision. FA information helps investor in taking investment decision accurately.

Government: They are external stakeholders and are interested in financial statements to

determine validity of the tax declared in financial reports of the organization. It is useful in

evaluating the tax returns. Financial statements of the organization helps government in tracking

the economic progress by thoroughly analysing the varied sectors of economy. They are

interested in the financial information of the company for regulatory purpose. It helps

government in determining the tax due and tax paid thereon.

Customers: They are concerned in financial reports of the organization as it is useful in

analysing the stability position of the organization (Cascino and et.al., 2017). It is also essential

in determining whether the resources of the organization are effectively utilized in order to attain

desired goals and objectives.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

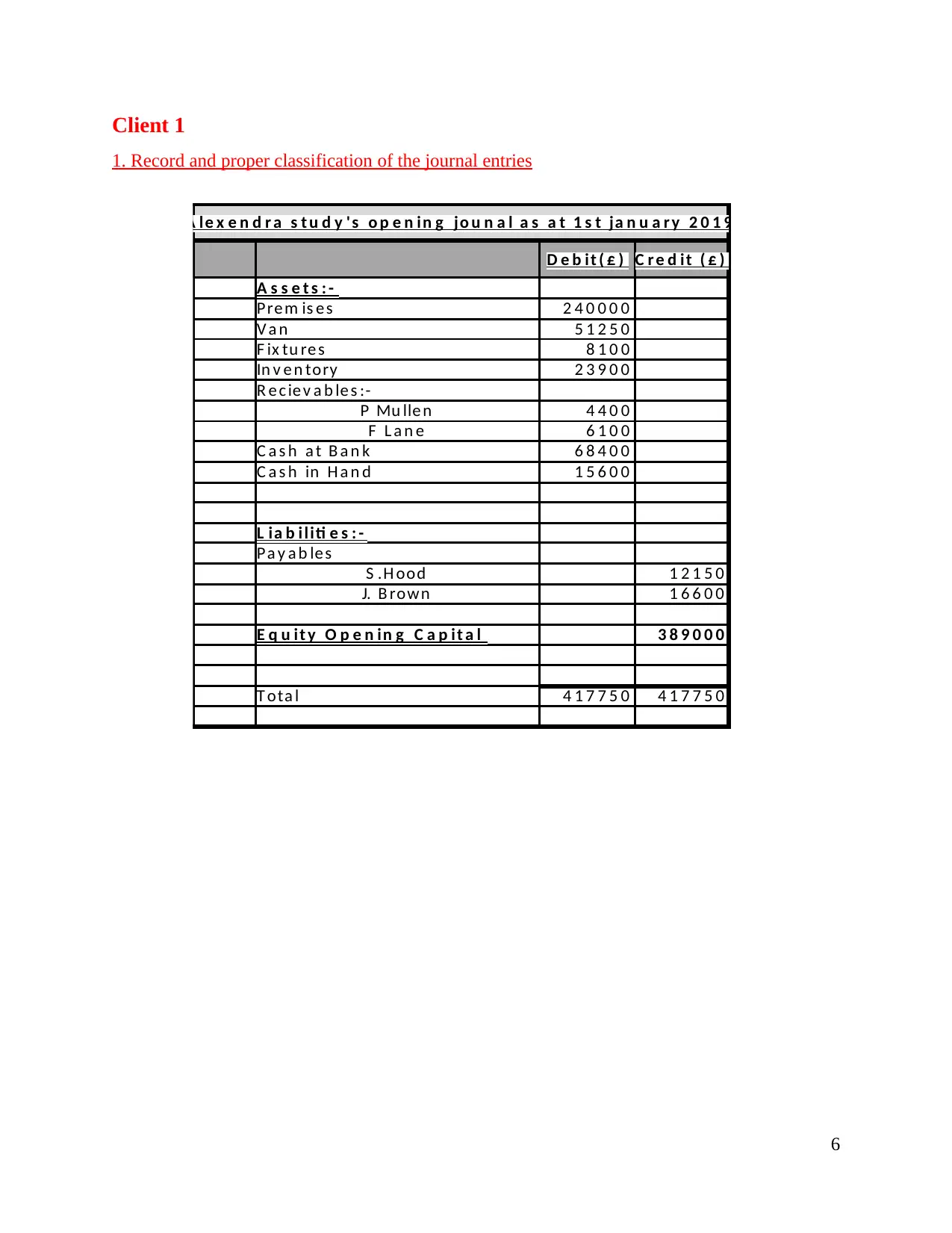

Client 1

1. Record and proper classification of the journal entries

6

A le x e n d r a s t u d y ' s o p e n in g jo u n a l a s a t 1 s t ja n u a r y 2 0 1 9

D e b it ( £ ) C r e d it ( £ )

A s s e t s : -

Pre m is e s 2 4 0 0 0 0

V a n 5 1 2 5 0

F ix tu re s 8 1 0 0

In v e n tory 2 3 9 0 0

R e c ie v a b le s :-

P Mu lle n 4 4 0 0

F L a n e 6 1 0 0

C a s h a t B a n k 6 8 4 0 0

C a s h in H a n d 1 5 6 0 0

L ia b i liti e s : -

Pa y a b le s

S .H ood 1 2 1 5 0

J. B row n 1 6 6 0 0

E q u it y O p e n in g C a p it a l 3 8 9 0 0 0

T ota l 4 1 7 7 5 0 4 1 7 7 5 0

1. Record and proper classification of the journal entries

6

A le x e n d r a s t u d y ' s o p e n in g jo u n a l a s a t 1 s t ja n u a r y 2 0 1 9

D e b it ( £ ) C r e d it ( £ )

A s s e t s : -

Pre m is e s 2 4 0 0 0 0

V a n 5 1 2 5 0

F ix tu re s 8 1 0 0

In v e n tory 2 3 9 0 0

R e c ie v a b le s :-

P Mu lle n 4 4 0 0

F L a n e 6 1 0 0

C a s h a t B a n k 6 8 4 0 0

C a s h in H a n d 1 5 6 0 0

L ia b i liti e s : -

Pa y a b le s

S .H ood 1 2 1 5 0

J. B row n 1 6 6 0 0

E q u it y O p e n in g C a p it a l 3 8 9 0 0 0

T ota l 4 1 7 7 5 0 4 1 7 7 5 0

7

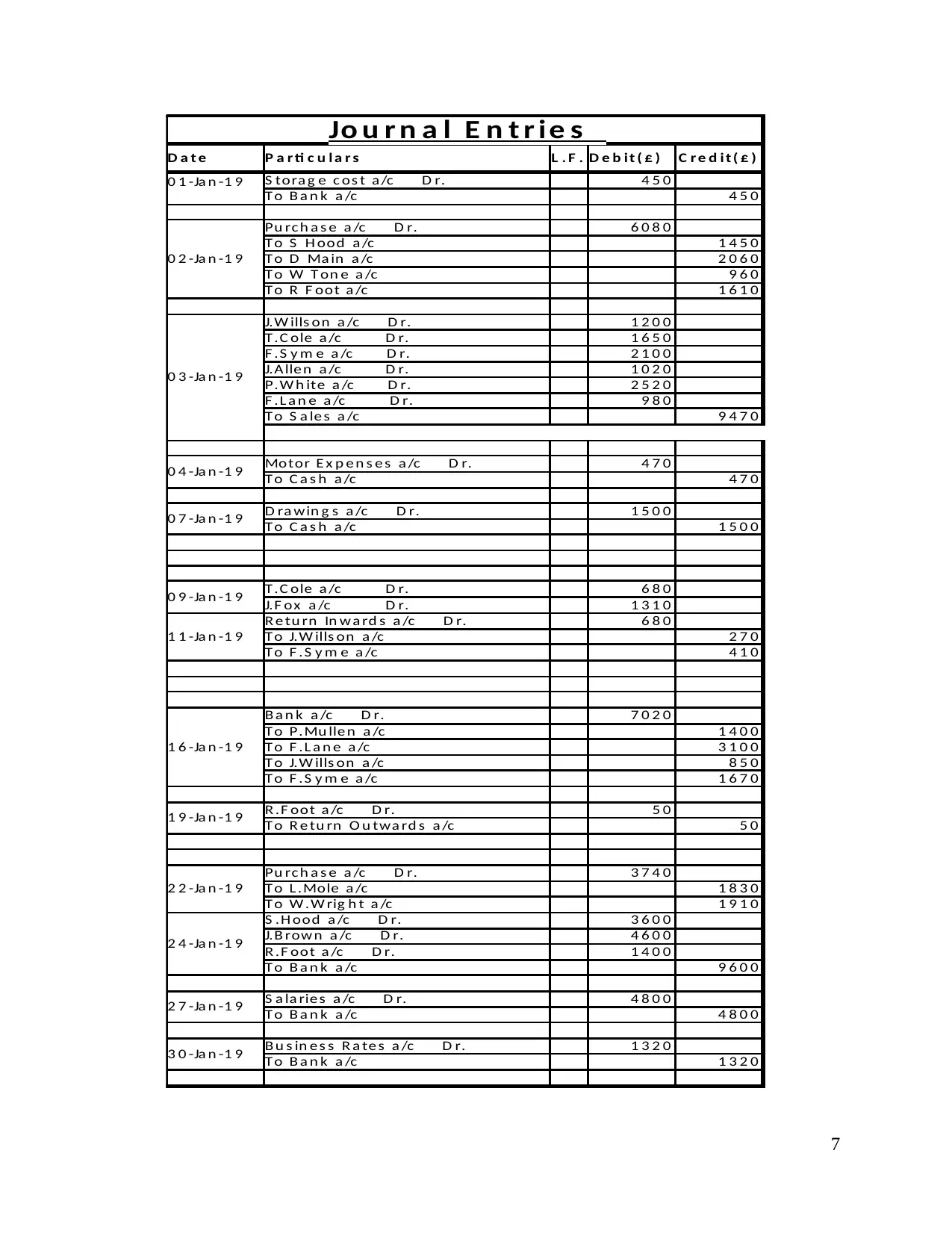

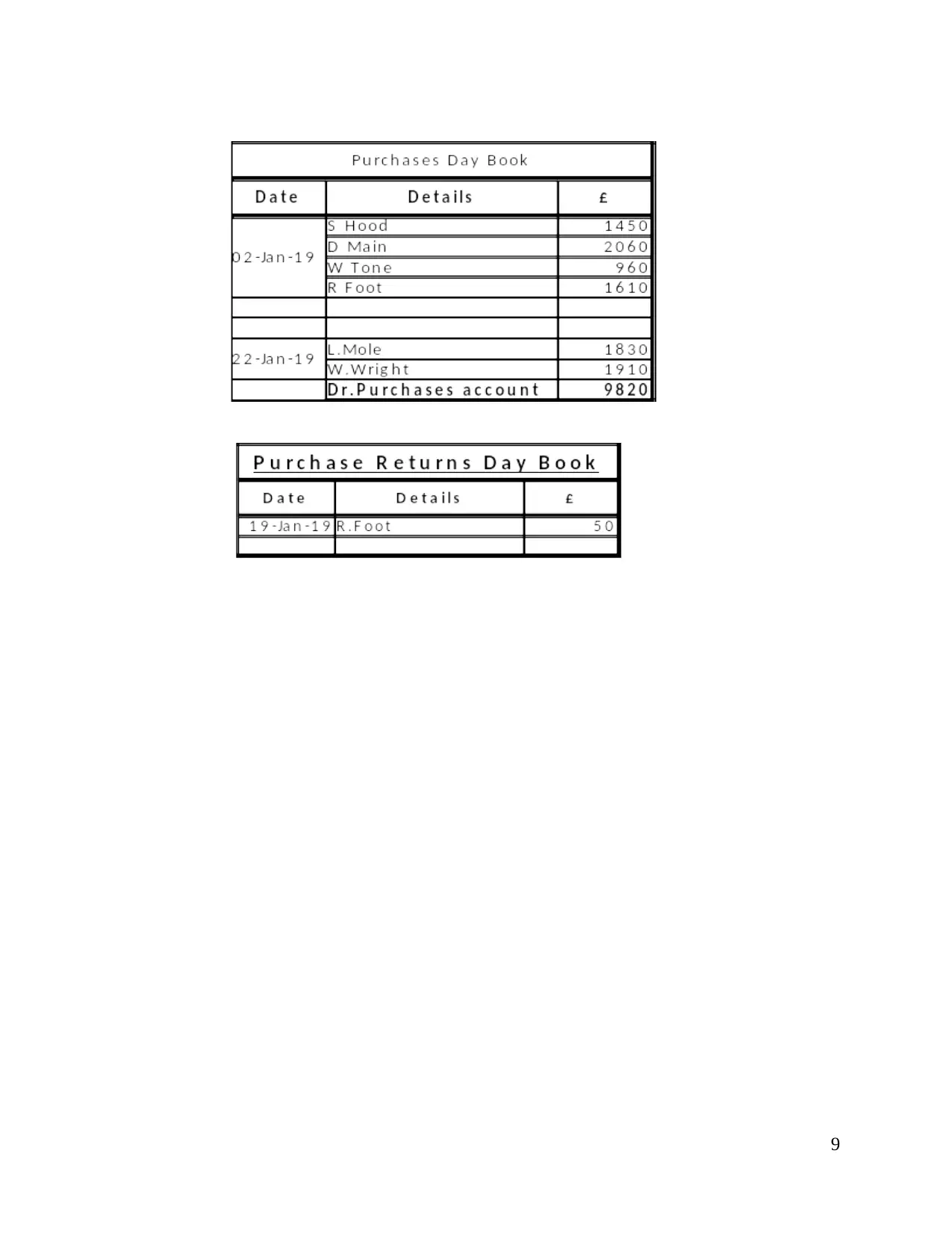

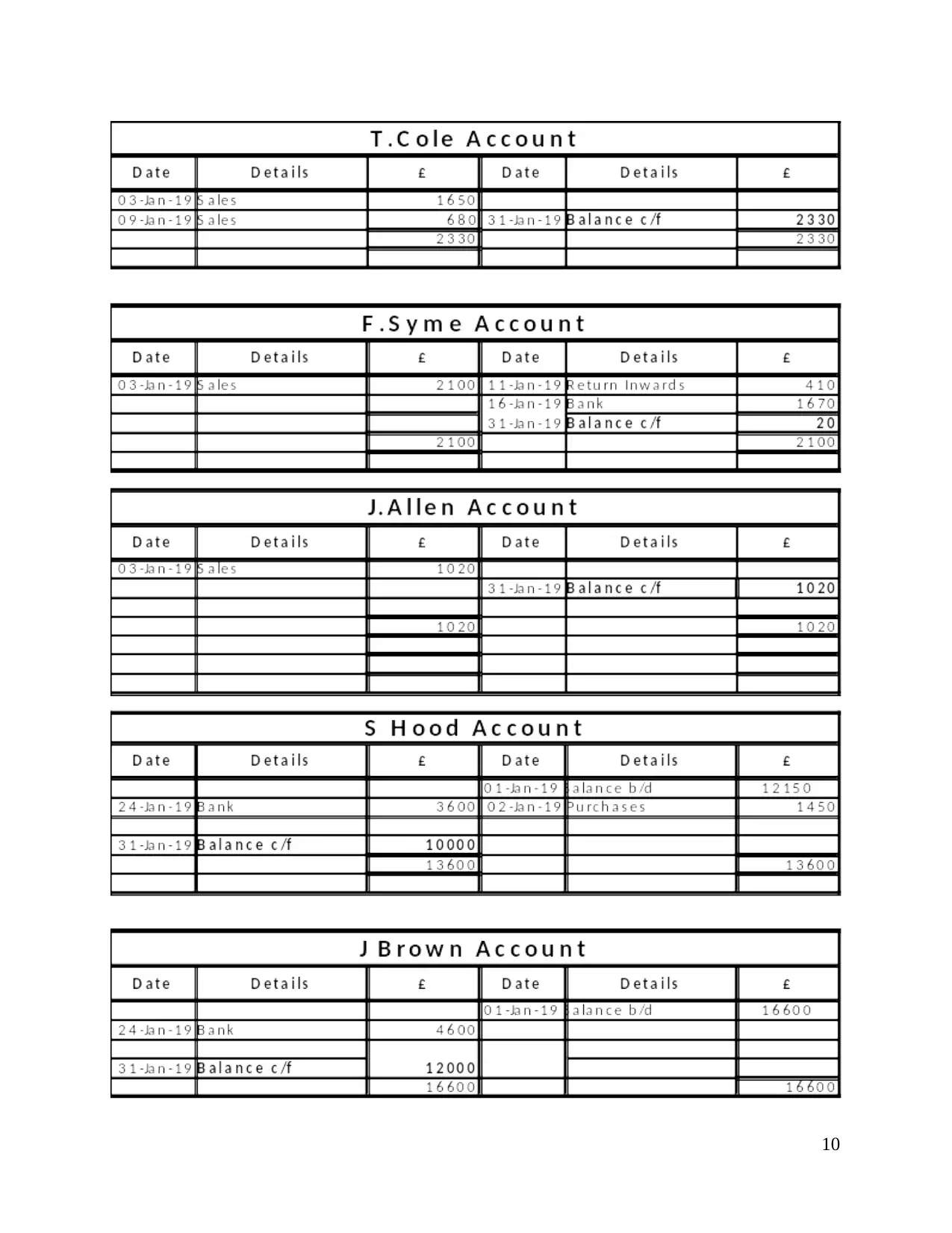

Jo u r n a l E n t r ie s

D a t e P a r ti c u l a r s L . F . D e b it ( £ ) C r e d i t ( £ )

0 1 -Ja n -1 9 S tora g e c os t a /c D r. 4 5 0

T o B a n k a /c 4 5 0

0 2 -Ja n -1 9

Pu rc h a s e a /c D r. 6 0 8 0

T o S H ood a /c 1 4 5 0

T o D Ma in a /c 2 0 6 0

T o W T on e a /c 9 6 0

T o R F oot a /c 1 6 1 0

0 3 -Ja n -1 9

J.W ills on a /c D r. 1 2 0 0

T .C ole a /c D r. 1 6 5 0

F .S y m e a /c D r. 2 1 0 0

J.A lle n a /c D r. 1 0 2 0

P.W h ite a /c D r. 2 5 2 0

F .L a n e a /c D r. 9 8 0

T o S a le s a /c 9 4 7 0

0 4 -Ja n -1 9 Motor E x p e n s e s a /c D r. 4 7 0

T o C a s h a /c 4 7 0

0 7 -Ja n -1 9 D ra win g s a /c D r. 1 5 0 0

T o C a s h a /c 1 5 0 0

0 9 -Ja n -1 9 T .C ole a /c D r. 6 8 0

J.F ox a /c D r. 1 3 1 0

1 1 -Ja n -1 9

R e tu rn In w a rd s a /c D r. 6 8 0

T o J.W ills on a /c 2 7 0

T o F .S y m e a /c 4 1 0

1 6 -Ja n -1 9

B a n k a /c D r. 7 0 2 0

T o P.Mu lle n a /c 1 4 0 0

T o F .L a n e a /c 3 1 0 0

T o J.W ills on a /c 8 5 0

T o F .S y m e a /c 1 6 7 0

1 9 -Ja n -1 9 R .F oot a /c D r. 5 0

T o R e tu rn O u twa rd s a /c 5 0

2 2 -Ja n -1 9

Pu rc h a s e a /c D r. 3 7 4 0

T o L .Mole a /c 1 8 3 0

T o W .W rig h t a /c 1 9 1 0

2 4 -Ja n -1 9

S .H ood a /c D r. 3 6 0 0

J.B row n a /c D r. 4 6 0 0

R .F oot a /c D r. 1 4 0 0

T o B a n k a /c 9 6 0 0

2 7 -Ja n -1 9 S a la ries a /c D r. 4 8 0 0

T o B a n k a /c 4 8 0 0

3 0 -Ja n -1 9 B u s in es s R a te s a /c D r. 1 3 2 0

T o B a n k a /c 1 3 2 0

Jo u r n a l E n t r ie s

D a t e P a r ti c u l a r s L . F . D e b it ( £ ) C r e d i t ( £ )

0 1 -Ja n -1 9 S tora g e c os t a /c D r. 4 5 0

T o B a n k a /c 4 5 0

0 2 -Ja n -1 9

Pu rc h a s e a /c D r. 6 0 8 0

T o S H ood a /c 1 4 5 0

T o D Ma in a /c 2 0 6 0

T o W T on e a /c 9 6 0

T o R F oot a /c 1 6 1 0

0 3 -Ja n -1 9

J.W ills on a /c D r. 1 2 0 0

T .C ole a /c D r. 1 6 5 0

F .S y m e a /c D r. 2 1 0 0

J.A lle n a /c D r. 1 0 2 0

P.W h ite a /c D r. 2 5 2 0

F .L a n e a /c D r. 9 8 0

T o S a le s a /c 9 4 7 0

0 4 -Ja n -1 9 Motor E x p e n s e s a /c D r. 4 7 0

T o C a s h a /c 4 7 0

0 7 -Ja n -1 9 D ra win g s a /c D r. 1 5 0 0

T o C a s h a /c 1 5 0 0

0 9 -Ja n -1 9 T .C ole a /c D r. 6 8 0

J.F ox a /c D r. 1 3 1 0

1 1 -Ja n -1 9

R e tu rn In w a rd s a /c D r. 6 8 0

T o J.W ills on a /c 2 7 0

T o F .S y m e a /c 4 1 0

1 6 -Ja n -1 9

B a n k a /c D r. 7 0 2 0

T o P.Mu lle n a /c 1 4 0 0

T o F .L a n e a /c 3 1 0 0

T o J.W ills on a /c 8 5 0

T o F .S y m e a /c 1 6 7 0

1 9 -Ja n -1 9 R .F oot a /c D r. 5 0

T o R e tu rn O u twa rd s a /c 5 0

2 2 -Ja n -1 9

Pu rc h a s e a /c D r. 3 7 4 0

T o L .Mole a /c 1 8 3 0

T o W .W rig h t a /c 1 9 1 0

2 4 -Ja n -1 9

S .H ood a /c D r. 3 6 0 0

J.B row n a /c D r. 4 6 0 0

R .F oot a /c D r. 1 4 0 0

T o B a n k a /c 9 6 0 0

2 7 -Ja n -1 9 S a la ries a /c D r. 4 8 0 0

T o B a n k a /c 4 8 0 0

3 0 -Ja n -1 9 B u s in es s R a te s a /c D r. 1 3 2 0

T o B a n k a /c 1 3 2 0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

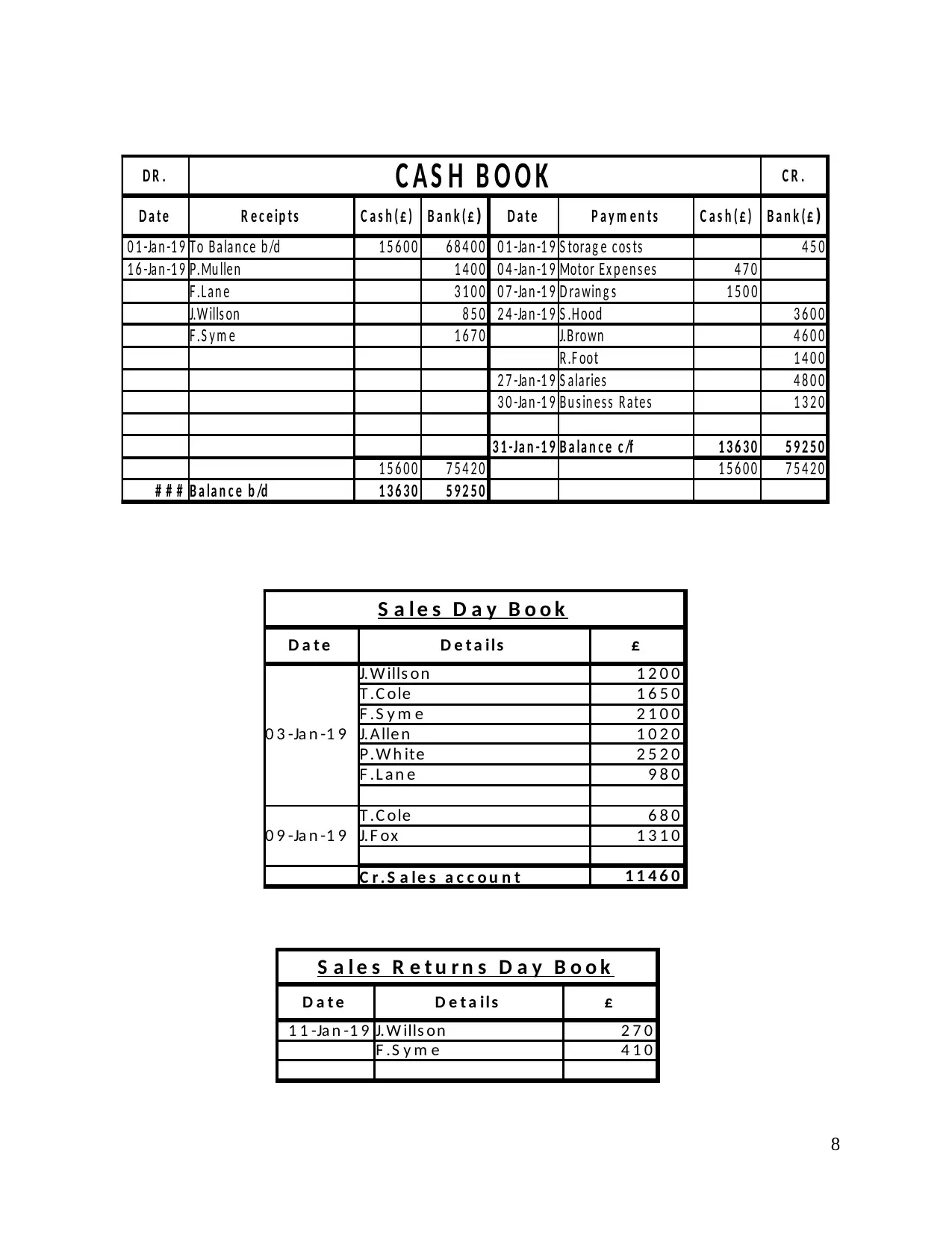

D R . C A S H B O O K C R .

D a t e R e c e ip t s C a s h ( £ ) D a t e P a y m e n t s C a s h ( £ )

0 1 -Ja n -1 9 T o B a la n c e b /d 1 5 6 0 0 6 8 4 0 0 0 1 -Ja n -1 9 S tora g e c os ts 4 5 0

1 6 -Ja n -1 9 P.Mu lle n 1 4 0 0 0 4 -Ja n -1 9 Motor E x p e n s e s 4 7 0

F .L a n e 3 1 0 0 0 7 -Ja n -1 9 D ra win g s 1 5 0 0

J.W ills on 8 5 0 2 4 -Ja n -1 9 S .H ood 3 6 0 0

F .S y m e 1 6 7 0 J.B rown 4 6 0 0

R .F oot 1 4 0 0

2 7 -Ja n -1 9 S a la rie s 4 8 0 0

3 0 -Ja n -1 9 B u s in e s s R a te s 1 3 2 0

3 1 -Ja n - 1 9 B a la n c e c /f 1 3 6 3 0 5 9 2 5 0

1 5 6 0 0 7 5 4 2 0 1 5 6 0 0 7 5 4 2 0

# # # B a la n c e b /d 1 3 6 3 0 5 9 2 5 0

B a n k ( £ ) B a n k ( £ )

S a l e s D a y B o o k

D a t e D e t a ils £

0 3 -Ja n -1 9

J.W ills on 1 2 0 0

T .C ole 1 6 5 0

F .S y m e 2 1 0 0

J.Alle n 1 0 2 0

P.W h ite 2 5 2 0

F .L a n e 9 8 0

0 9 -Ja n -1 9

T .C ole 6 8 0

J.F ox 1 3 1 0

C r . S a le s a c c o u n t 1 1 4 6 0

S a l e s R e t u r n s D a y B o o k

D a t e D e t a ils £

1 1 -Ja n -1 9 J.W ills on 2 7 0

F .S y m e 4 1 0

D R . C A S H B O O K C R .

D a t e R e c e ip t s C a s h ( £ ) D a t e P a y m e n t s C a s h ( £ )

0 1 -Ja n -1 9 T o B a la n c e b /d 1 5 6 0 0 6 8 4 0 0 0 1 -Ja n -1 9 S tora g e c os ts 4 5 0

1 6 -Ja n -1 9 P.Mu lle n 1 4 0 0 0 4 -Ja n -1 9 Motor E x p e n s e s 4 7 0

F .L a n e 3 1 0 0 0 7 -Ja n -1 9 D ra win g s 1 5 0 0

J.W ills on 8 5 0 2 4 -Ja n -1 9 S .H ood 3 6 0 0

F .S y m e 1 6 7 0 J.B rown 4 6 0 0

R .F oot 1 4 0 0

2 7 -Ja n -1 9 S a la rie s 4 8 0 0

3 0 -Ja n -1 9 B u s in e s s R a te s 1 3 2 0

3 1 -Ja n - 1 9 B a la n c e c /f 1 3 6 3 0 5 9 2 5 0

1 5 6 0 0 7 5 4 2 0 1 5 6 0 0 7 5 4 2 0

# # # B a la n c e b /d 1 3 6 3 0 5 9 2 5 0

B a n k ( £ ) B a n k ( £ )

S a l e s D a y B o o k

D a t e D e t a ils £

0 3 -Ja n -1 9

J.W ills on 1 2 0 0

T .C ole 1 6 5 0

F .S y m e 2 1 0 0

J.Alle n 1 0 2 0

P.W h ite 2 5 2 0

F .L a n e 9 8 0

0 9 -Ja n -1 9

T .C ole 6 8 0

J.F ox 1 3 1 0

C r . S a le s a c c o u n t 1 1 4 6 0

S a l e s R e t u r n s D a y B o o k

D a t e D e t a ils £

1 1 -Ja n -1 9 J.W ills on 2 7 0

F .S y m e 4 1 0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.