Financial Accounting: Stakeholders, Transactions, and Statements

VerifiedAdded on 2020/10/04

|26

|3644

|144

Report

AI Summary

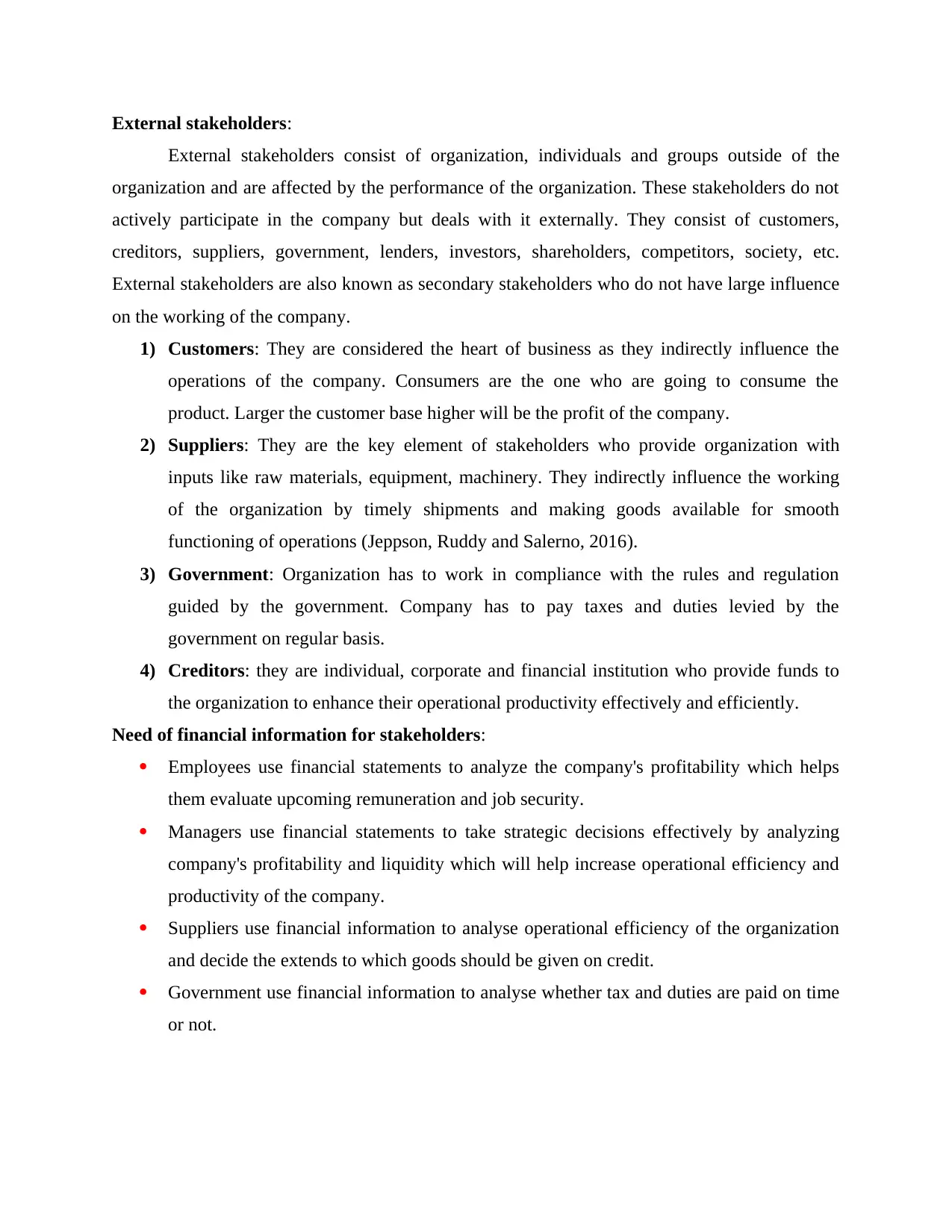

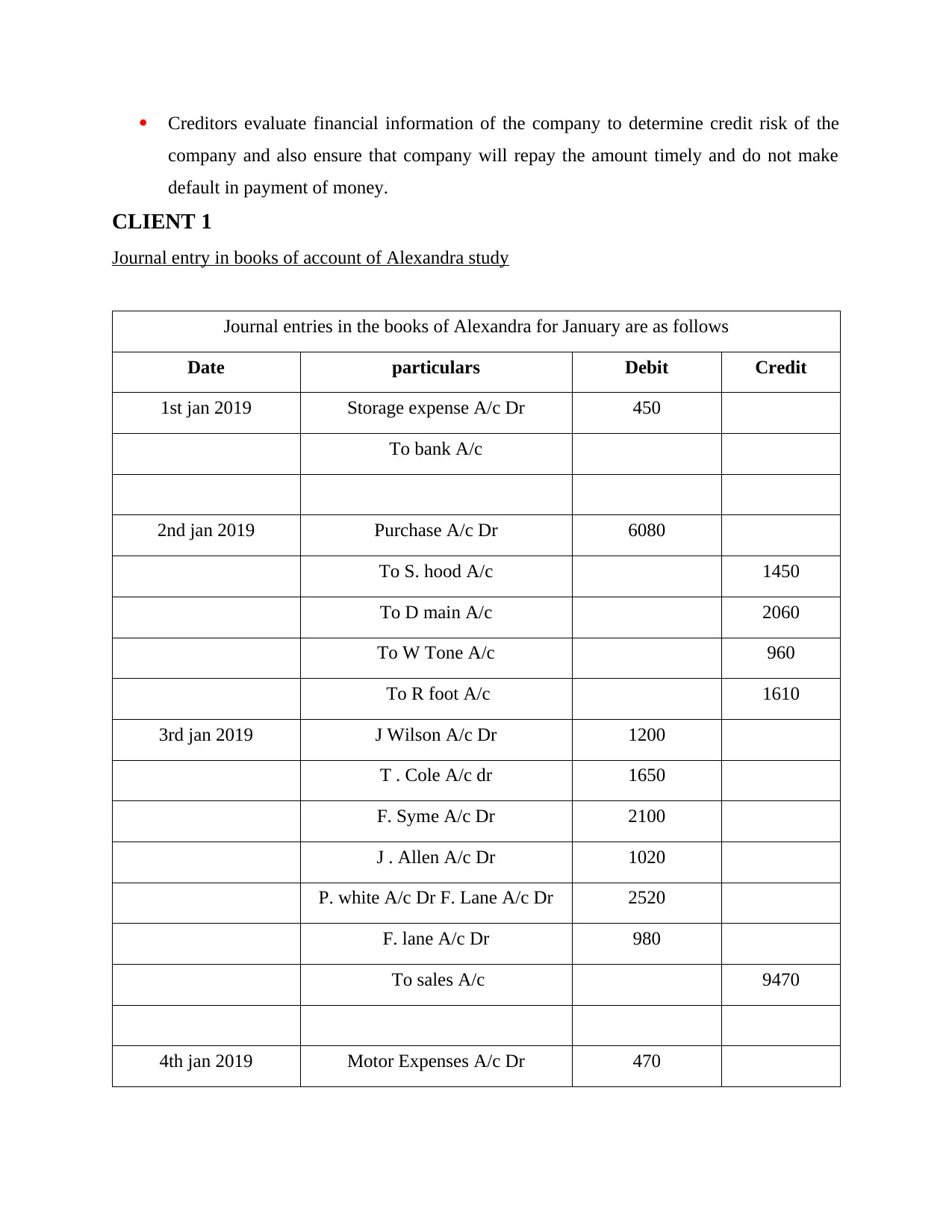

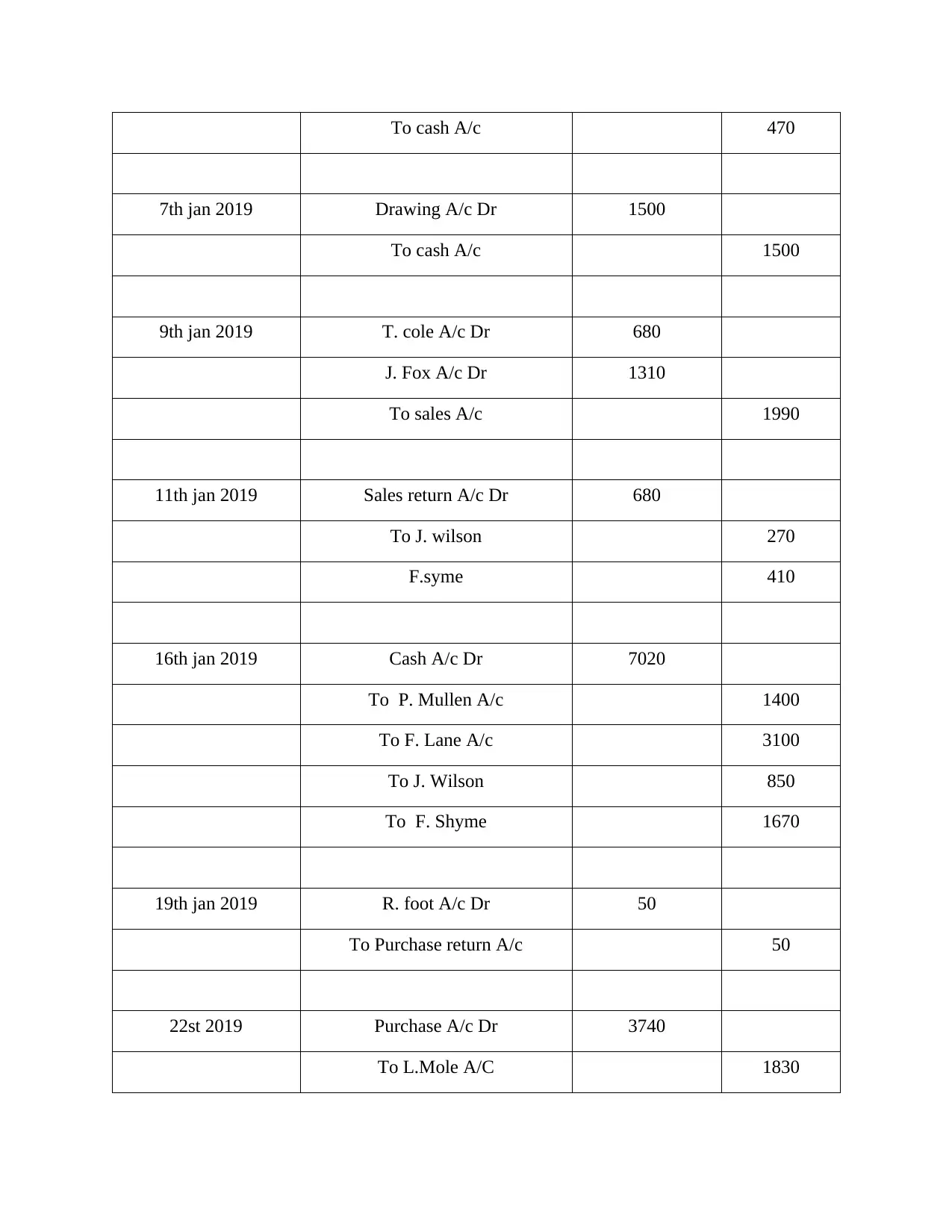

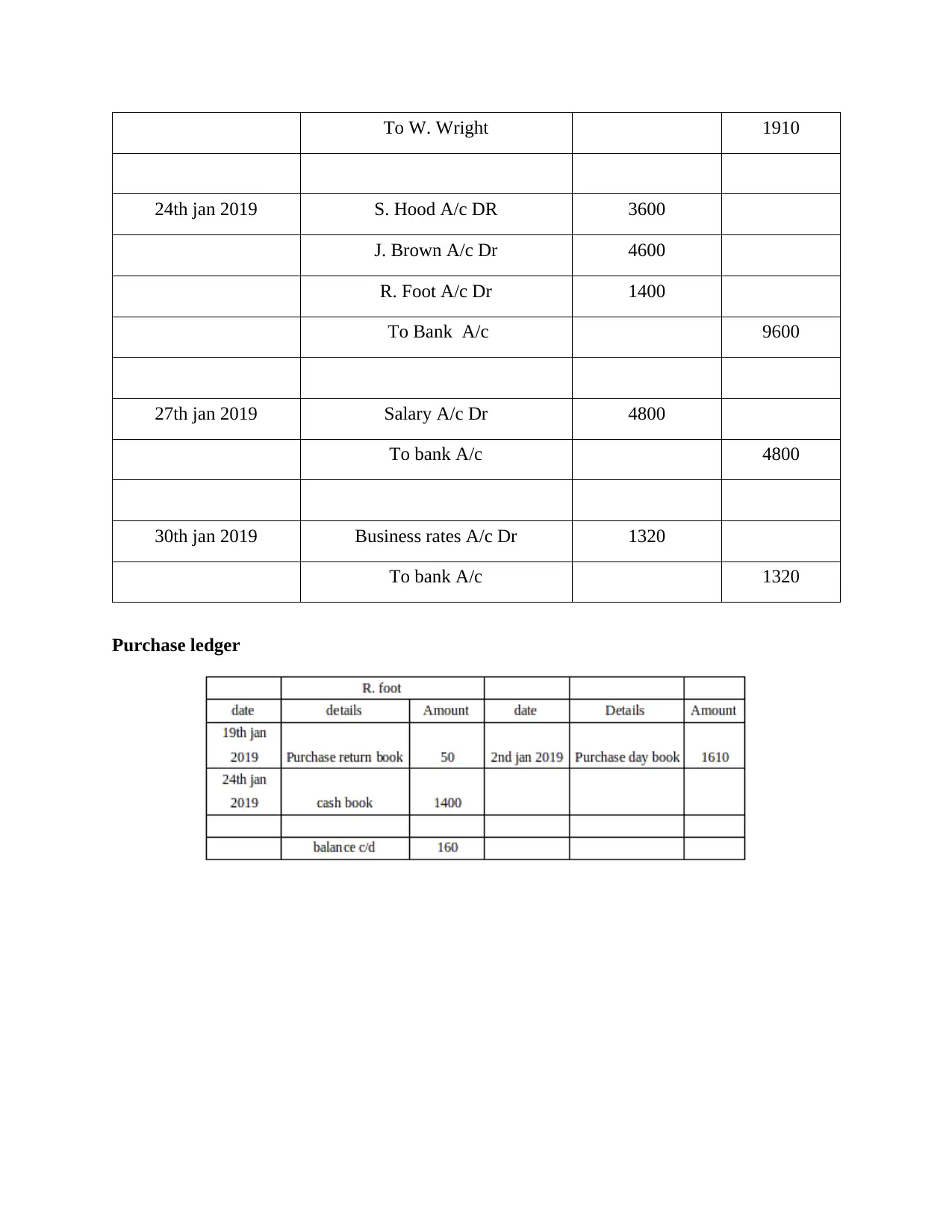

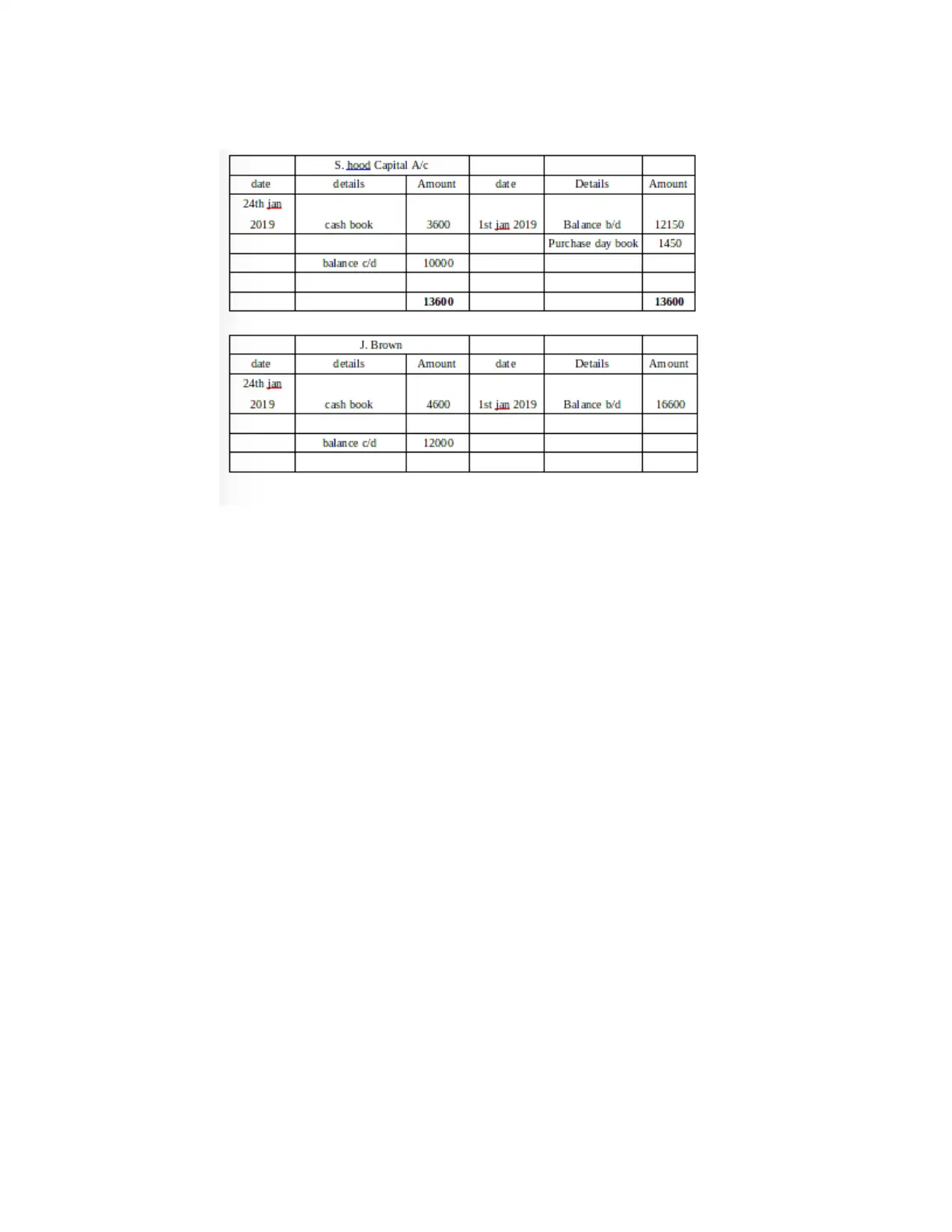

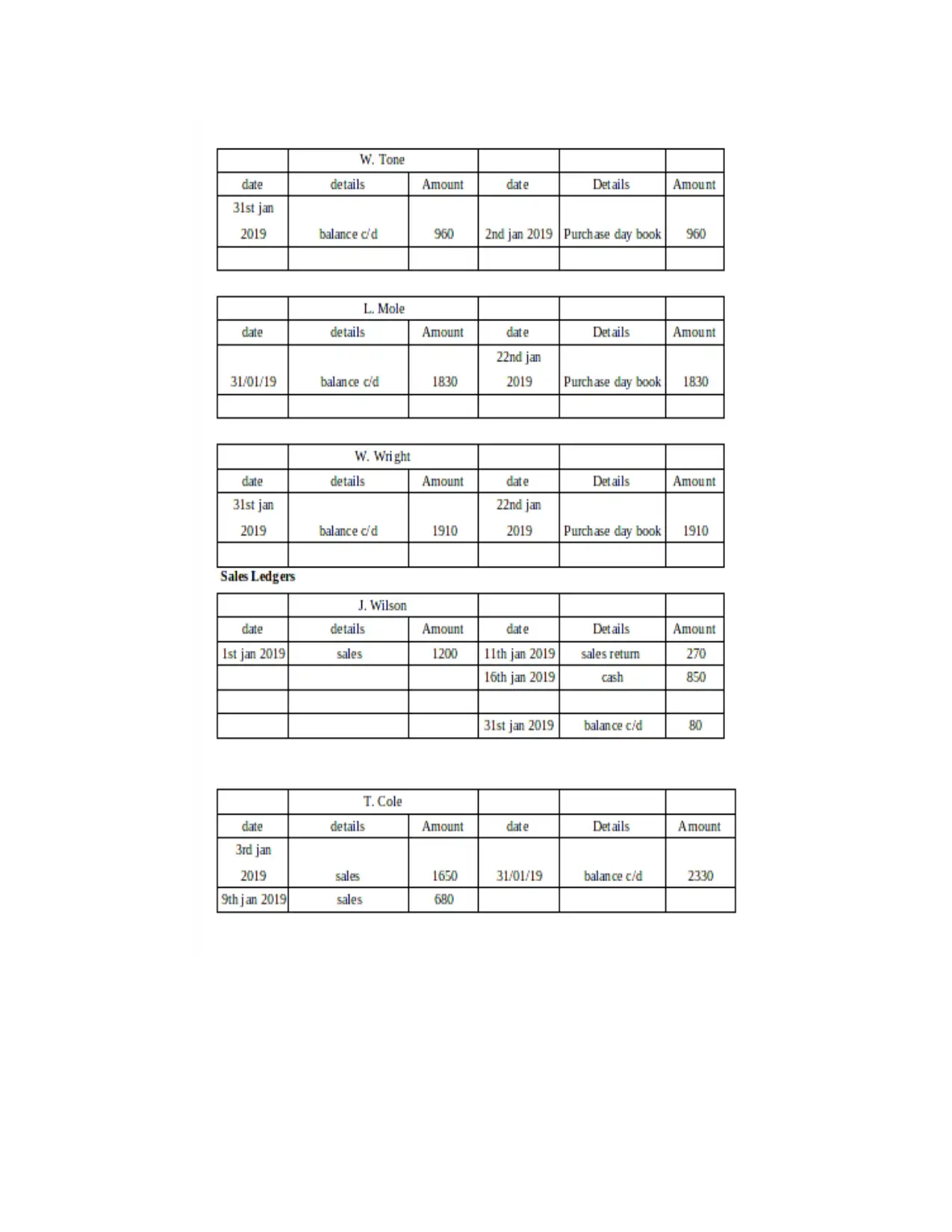

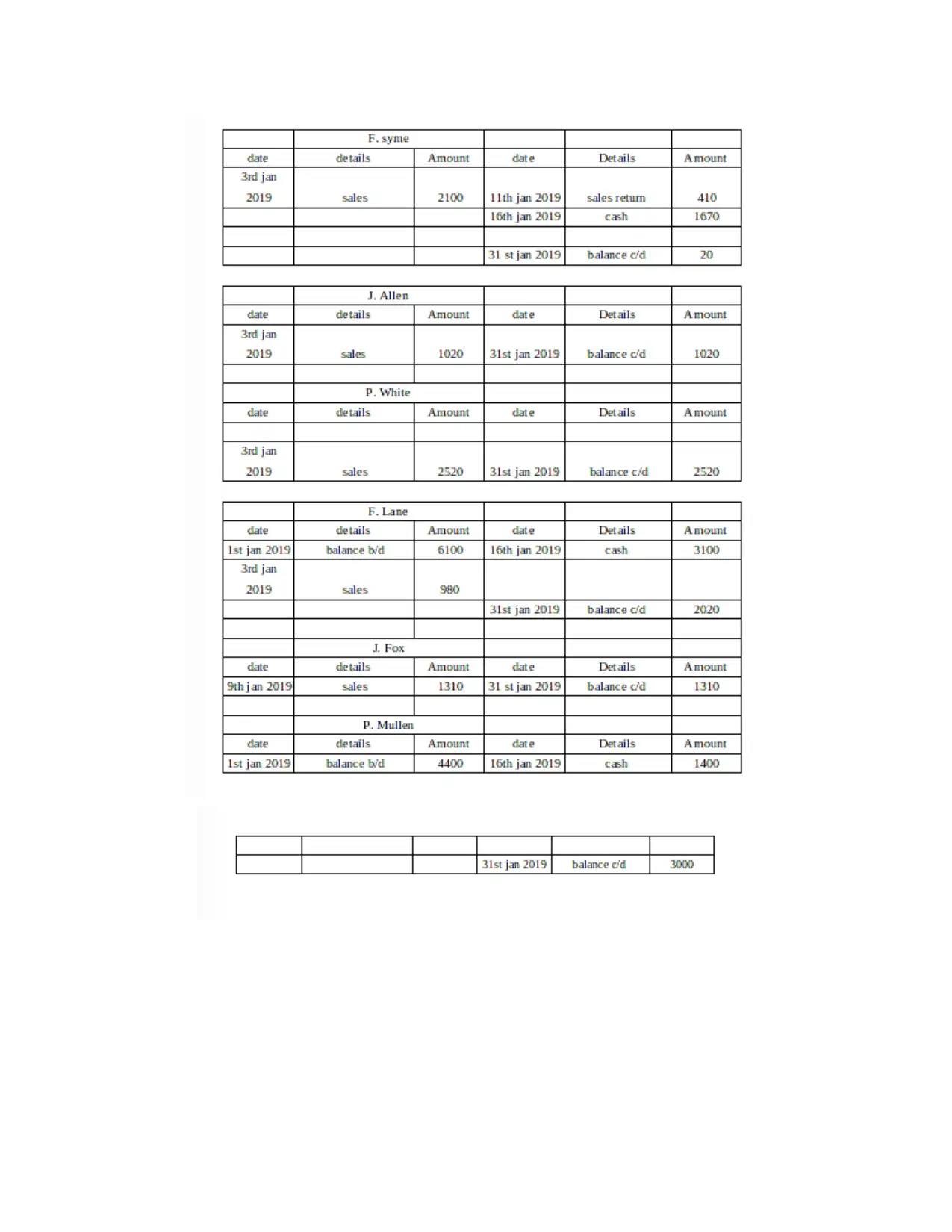

This financial accounting report provides a comprehensive overview of financial accounting principles and practices. It begins with an introduction to financial accounting, its purpose, and the identification of internal and external stakeholders, along with their respective interests in financial information. The report then delves into specific client scenarios, including journal entries, profit and loss accounts, balance sheets, and explanations of key accounting concepts such as going concern, accrual, consistency, and prudence. The purpose of depreciation in accounting statements is explained, along with the differences in financial statements prepared by sole traders and limited companies. Furthermore, the report covers bank reconciliation statements, imprest systems, and control accounts. It concludes with an analysis of suspense accounts and trial balances, and the importance of journal entries and corrections. The report uses examples from the small business accounting firm, Brookscity, to illustrate the practical application of these concepts. Overall, the report provides a detailed analysis of financial accounting principles and their application in various business contexts.

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.