Financial Accounting Principles Report: Client Case Studies

VerifiedAdded on 2020/12/09

|27

|4169

|486

Report

AI Summary

This report delves into the core principles of financial accounting, providing a comprehensive overview of its regulations and practical applications. It examines various aspects, including journal entries, ledger accounts, trial balances, and the preparation of financial statements for multiple clients. The report explores key concepts such as consistency and prudence, along with depreciation methods and the purpose of bank reconciliation statements. It also covers suspense accounts and their features, offering a detailed analysis of financial accounting practices. The report includes client-specific case studies, demonstrating the practical application of accounting principles. The report also covers the regulations of financial accounting and the accounting principles and rules that are used in the preparation of all types of financial statements.

FINANCIAL ACCOUNTING

PRINCIPLES

PRINCIPLES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

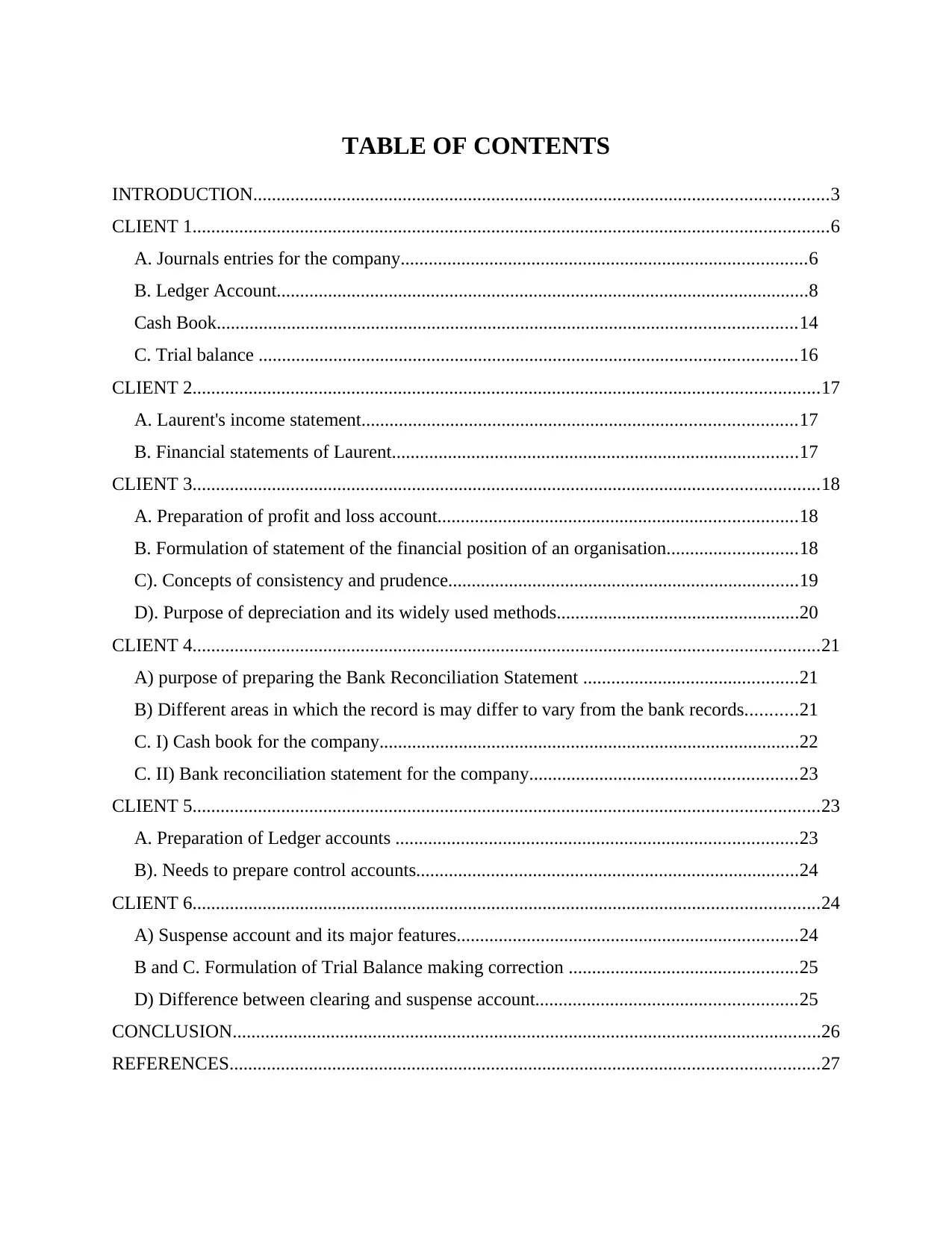

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

CLIENT 1........................................................................................................................................6

A. Journals entries for the company.......................................................................................6

B. Ledger Account..................................................................................................................8

Cash Book............................................................................................................................14

C. Trial balance ...................................................................................................................16

CLIENT 2......................................................................................................................................17

A. Laurent's income statement.............................................................................................17

B. Financial statements of Laurent.......................................................................................17

CLIENT 3......................................................................................................................................18

A. Preparation of profit and loss account.............................................................................18

B. Formulation of statement of the financial position of an organisation............................18

C). Concepts of consistency and prudence...........................................................................19

D). Purpose of depreciation and its widely used methods....................................................20

CLIENT 4......................................................................................................................................21

A) purpose of preparing the Bank Reconciliation Statement ..............................................21

B) Different areas in which the record is may differ to vary from the bank records...........21

C. I) Cash book for the company..........................................................................................22

C. II) Bank reconciliation statement for the company.........................................................23

CLIENT 5......................................................................................................................................23

A. Preparation of Ledger accounts ......................................................................................23

B). Needs to prepare control accounts..................................................................................24

CLIENT 6......................................................................................................................................24

A) Suspense account and its major features.........................................................................24

B and C. Formulation of Trial Balance making correction .................................................25

D) Difference between clearing and suspense account........................................................25

CONCLUSION..............................................................................................................................26

REFERENCES..............................................................................................................................27

INTRODUCTION...........................................................................................................................3

CLIENT 1........................................................................................................................................6

A. Journals entries for the company.......................................................................................6

B. Ledger Account..................................................................................................................8

Cash Book............................................................................................................................14

C. Trial balance ...................................................................................................................16

CLIENT 2......................................................................................................................................17

A. Laurent's income statement.............................................................................................17

B. Financial statements of Laurent.......................................................................................17

CLIENT 3......................................................................................................................................18

A. Preparation of profit and loss account.............................................................................18

B. Formulation of statement of the financial position of an organisation............................18

C). Concepts of consistency and prudence...........................................................................19

D). Purpose of depreciation and its widely used methods....................................................20

CLIENT 4......................................................................................................................................21

A) purpose of preparing the Bank Reconciliation Statement ..............................................21

B) Different areas in which the record is may differ to vary from the bank records...........21

C. I) Cash book for the company..........................................................................................22

C. II) Bank reconciliation statement for the company.........................................................23

CLIENT 5......................................................................................................................................23

A. Preparation of Ledger accounts ......................................................................................23

B). Needs to prepare control accounts..................................................................................24

CLIENT 6......................................................................................................................................24

A) Suspense account and its major features.........................................................................24

B and C. Formulation of Trial Balance making correction .................................................25

D) Difference between clearing and suspense account........................................................25

CONCLUSION..............................................................................................................................26

REFERENCES..............................................................................................................................27

INTRODUCTION

Accounting principles are general guidelines and rules that should be followed by all

organisations during the time of making financial statements. These are generally accepted rules

that are developed for showing the actual financial image of the particular company (Braun and

et.al., 2015). This report shows different financial issues and their proper solutions with usages

of all core financial principles, techniques and methods. It also covers regulations related to the

financial accounting and various accounting principles. Further, it includes concept of

depreciation and its core methods. Lastly, it covers the information about several accounts such

as suspense and clearing account.

Report to the Line Manager

To Line Manager,

From - Junior Accountant

Subject - Regulations and effectiveness of accountancy.

Financial accounting is a perfect way to understand the core position of an organisation in its

target market. It shows the performance or profitability of a firm that are useful for its stake

holders. It is a specific branch of accounting that shows an organisation’s financial transactions.

It is used for recording, summarizing and presenting all transactions in proper financial

statements for example profit and loss account, income and expenses statements and balance

sheet. According to generally accepted accounting principles(GAPP), in financial accounting

there are so many rules and techniques that should be followed by every organisation in the

same way so that business's external stakeholders can satisfy organisation’s work performance

(Downs, 2017). The core purpose of making these financial statements is to show original

image of a company in front of public. In this context, every business entity issues its financial

statements on a routine schedule over a time. Its main purpose is to provide sufficient data or

information to its related person or entities these are commonly utilized by a variety of persons

for their requirements and know about the financial position of that particular company. For

example, each person who wants to know about the equity share price of dividend rate of a

company then he or she sees at its past financial records and understand about the dividend

policy of company or value of firm in stock exchange. In this process of making its financial

statements, there are several accounting standards that are generally accepted all over the world.

In this context, each organisation should use double entry system that provides better result for

3

Accounting principles are general guidelines and rules that should be followed by all

organisations during the time of making financial statements. These are generally accepted rules

that are developed for showing the actual financial image of the particular company (Braun and

et.al., 2015). This report shows different financial issues and their proper solutions with usages

of all core financial principles, techniques and methods. It also covers regulations related to the

financial accounting and various accounting principles. Further, it includes concept of

depreciation and its core methods. Lastly, it covers the information about several accounts such

as suspense and clearing account.

Report to the Line Manager

To Line Manager,

From - Junior Accountant

Subject - Regulations and effectiveness of accountancy.

Financial accounting is a perfect way to understand the core position of an organisation in its

target market. It shows the performance or profitability of a firm that are useful for its stake

holders. It is a specific branch of accounting that shows an organisation’s financial transactions.

It is used for recording, summarizing and presenting all transactions in proper financial

statements for example profit and loss account, income and expenses statements and balance

sheet. According to generally accepted accounting principles(GAPP), in financial accounting

there are so many rules and techniques that should be followed by every organisation in the

same way so that business's external stakeholders can satisfy organisation’s work performance

(Downs, 2017). The core purpose of making these financial statements is to show original

image of a company in front of public. In this context, every business entity issues its financial

statements on a routine schedule over a time. Its main purpose is to provide sufficient data or

information to its related person or entities these are commonly utilized by a variety of persons

for their requirements and know about the financial position of that particular company. For

example, each person who wants to know about the equity share price of dividend rate of a

company then he or she sees at its past financial records and understand about the dividend

policy of company or value of firm in stock exchange. In this process of making its financial

statements, there are several accounting standards that are generally accepted all over the world.

In this context, each organisation should use double entry system that provides better result for

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

making these records or statements.

Regulations relating to the Financial Accounting: Regulations of financial accounting is a

common set of standards and principles that demonstrates core basis of financial values and

used for preparing such financial statements for the whole year or period of a company. In this

process, there are several rules, laws and techniques for identifying the original image of a

business. In this context, there are certain governmental bodies or authorities that describes the

different regulations relating to financial accounting (Hatfield, 2014). These are discussed as:

Financial Reporting Council (FRC), it is an independent regulatory body situated at United

Kingdom and governs all corporate reporting. Its main function is to supervise all organisations

including Auditing Practices Board and Accounting Standards Board. ASB is collaborated with

several accounting criteria that are useful for other countries. The second regulatory body is

International Accounting Standards Board (IASB). It is established in April 2001 and situated at

London, UK. It provides guarantee that its earlier made standards are accepted in the entire

world with regarding to international developments. ASB plays an autonomous role for issuing

such accounting standards. Accounting Standards Board creates different standards that are

known as Financial Reporting Standards(FRS). These are authoritative statements used in the

process of making financial statements (Henderson and et.al., 2015). These accounting

standards are applied for every organisation that have an intention to provide fair and true view

to its stakeholders. In this context, GAAP provides the corporate reporting model that consists

of financial statements and accompanying notes (Generally Accepted Accounting Principle,

2018). It is also known as procedure of better communication of all data related to the financial

position of a company to its external environment. As per overview of all regulatory and legal

needs for an organisation may be considered by way of the accounting standards.

Accounting principles and rules that are used in the preparation of all types of financial

statements - For all companies, accounting principles plays a significant role in making its

financial statements. Such general rules and concepts must control or govern the accounting

sector. In this context, there is a commonly used theory provided by the Generally Accepted

Accounting Principle(GAPP). These rules are described as follows:

Going Concern - To follow this accounting concept, it must assume that an

organisation will exist continuously throughout the period and carry out its business

activities to achieve all desired goals and objectives (Khan, 2015). In this context, every

4

Regulations relating to the Financial Accounting: Regulations of financial accounting is a

common set of standards and principles that demonstrates core basis of financial values and

used for preparing such financial statements for the whole year or period of a company. In this

process, there are several rules, laws and techniques for identifying the original image of a

business. In this context, there are certain governmental bodies or authorities that describes the

different regulations relating to financial accounting (Hatfield, 2014). These are discussed as:

Financial Reporting Council (FRC), it is an independent regulatory body situated at United

Kingdom and governs all corporate reporting. Its main function is to supervise all organisations

including Auditing Practices Board and Accounting Standards Board. ASB is collaborated with

several accounting criteria that are useful for other countries. The second regulatory body is

International Accounting Standards Board (IASB). It is established in April 2001 and situated at

London, UK. It provides guarantee that its earlier made standards are accepted in the entire

world with regarding to international developments. ASB plays an autonomous role for issuing

such accounting standards. Accounting Standards Board creates different standards that are

known as Financial Reporting Standards(FRS). These are authoritative statements used in the

process of making financial statements (Henderson and et.al., 2015). These accounting

standards are applied for every organisation that have an intention to provide fair and true view

to its stakeholders. In this context, GAAP provides the corporate reporting model that consists

of financial statements and accompanying notes (Generally Accepted Accounting Principle,

2018). It is also known as procedure of better communication of all data related to the financial

position of a company to its external environment. As per overview of all regulatory and legal

needs for an organisation may be considered by way of the accounting standards.

Accounting principles and rules that are used in the preparation of all types of financial

statements - For all companies, accounting principles plays a significant role in making its

financial statements. Such general rules and concepts must control or govern the accounting

sector. In this context, there is a commonly used theory provided by the Generally Accepted

Accounting Principle(GAPP). These rules are described as follows:

Going Concern - To follow this accounting concept, it must assume that an

organisation will exist continuously throughout the period and carry out its business

activities to achieve all desired goals and objectives (Khan, 2015). In this context, every

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company should make its all financial statements assuming that an entity is a going

concern and operates its entire business for the long time. So for this reason, it is

compulsory to make financial statements with using better accounting policies.

Accrual Concept - It refers as all the expenses and incomes should only be recorded

when it occurs in an organisation (Louwers and et.al., 2015). It is not applied in the case

of cash payments and receivables. This concept shows the actual image of a company.

Consistency - It is described that the organisation follows certain particular accounting

principles that are not changed if the overall policy will not change. These concepts are

widely used method applied appropriately and it is needed in every business for showing

effective financial statements to its potential stake holders. This idea is generated in

accounting for utilizing the particular policy or technique from one period to next.

Accounting Period - In this accounting principles, it assumes that the organisation

operates its business activities for a certain period (Macve, 2015). In general, this period

in approx. one year that starts from 1 April of current year to 31 march of next year. So

for this reason all financial records pertain only for specific period.

Prudence Concept - According to this concept, every business should consider only

expected expenditures and never make any assumption about income or revenue. It

should be conducted compulsorily because of accounting transaction are often uncertain

so for this reason never make any assumption about its revenue or income so that

management will able to show its financial statements.

Conservatism - This is an important concept that refers the critical situation, that if

there are two or more acceptable options for reporting an item then management of a

company should choose best option (Maskell, Baggaley and Grasso, 2016). It also

describes that organisation should choose the alternative that will result in less net

earnings or asset amount. It leads to the managers to disclose or anticipate losses and it

never allows for profits.

Full Discloser - By following this accounting principle, all companies should show the

actual image of its financial position in its target market. Every important information

related to the business should be provided in its final statements.

Realization - It states that if any change in organisational asset or liability should not

measure as profit or loss until that asset is sold or liability amount is paid. It is useful in

5

concern and operates its entire business for the long time. So for this reason, it is

compulsory to make financial statements with using better accounting policies.

Accrual Concept - It refers as all the expenses and incomes should only be recorded

when it occurs in an organisation (Louwers and et.al., 2015). It is not applied in the case

of cash payments and receivables. This concept shows the actual image of a company.

Consistency - It is described that the organisation follows certain particular accounting

principles that are not changed if the overall policy will not change. These concepts are

widely used method applied appropriately and it is needed in every business for showing

effective financial statements to its potential stake holders. This idea is generated in

accounting for utilizing the particular policy or technique from one period to next.

Accounting Period - In this accounting principles, it assumes that the organisation

operates its business activities for a certain period (Macve, 2015). In general, this period

in approx. one year that starts from 1 April of current year to 31 march of next year. So

for this reason all financial records pertain only for specific period.

Prudence Concept - According to this concept, every business should consider only

expected expenditures and never make any assumption about income or revenue. It

should be conducted compulsorily because of accounting transaction are often uncertain

so for this reason never make any assumption about its revenue or income so that

management will able to show its financial statements.

Conservatism - This is an important concept that refers the critical situation, that if

there are two or more acceptable options for reporting an item then management of a

company should choose best option (Maskell, Baggaley and Grasso, 2016). It also

describes that organisation should choose the alternative that will result in less net

earnings or asset amount. It leads to the managers to disclose or anticipate losses and it

never allows for profits.

Full Discloser - By following this accounting principle, all companies should show the

actual image of its financial position in its target market. Every important information

related to the business should be provided in its final statements.

Realization - It states that if any change in organisational asset or liability should not

measure as profit or loss until that asset is sold or liability amount is paid. It is useful in

5

estimating the original value of an asset or liability.

Matching - This concept is systematically derived to use the accrual basis of

accounting. It needs that all revenues will be matched with all expenses (Mullinova,

2016). No business can measure future economic profit so that it would apply for

gaining uncertain revenue in the upcoming.

Materiality - It refers that management should record only those transactions that are

important for the company. An organisation can ignore minor events but it should

consider that major events should be fully recorded and disclosed.

All these core principles are useful in making the financial statements for a particular period of

a company.

Consistency - It derives that organisation should operate its business activities throughout the

period and never end it until all legal formalities are fulfilled. Every business should assume

that it operates for a long period.

Materiality – This principle should apply for all companies and it describes all major

transactions and give up all immaterial or small transactions (Nobes, 2014). In this context,

management team of an organisation should record only those transactions that are useful in

providing appropriate image of the entity and it is not essential to record any minor events.

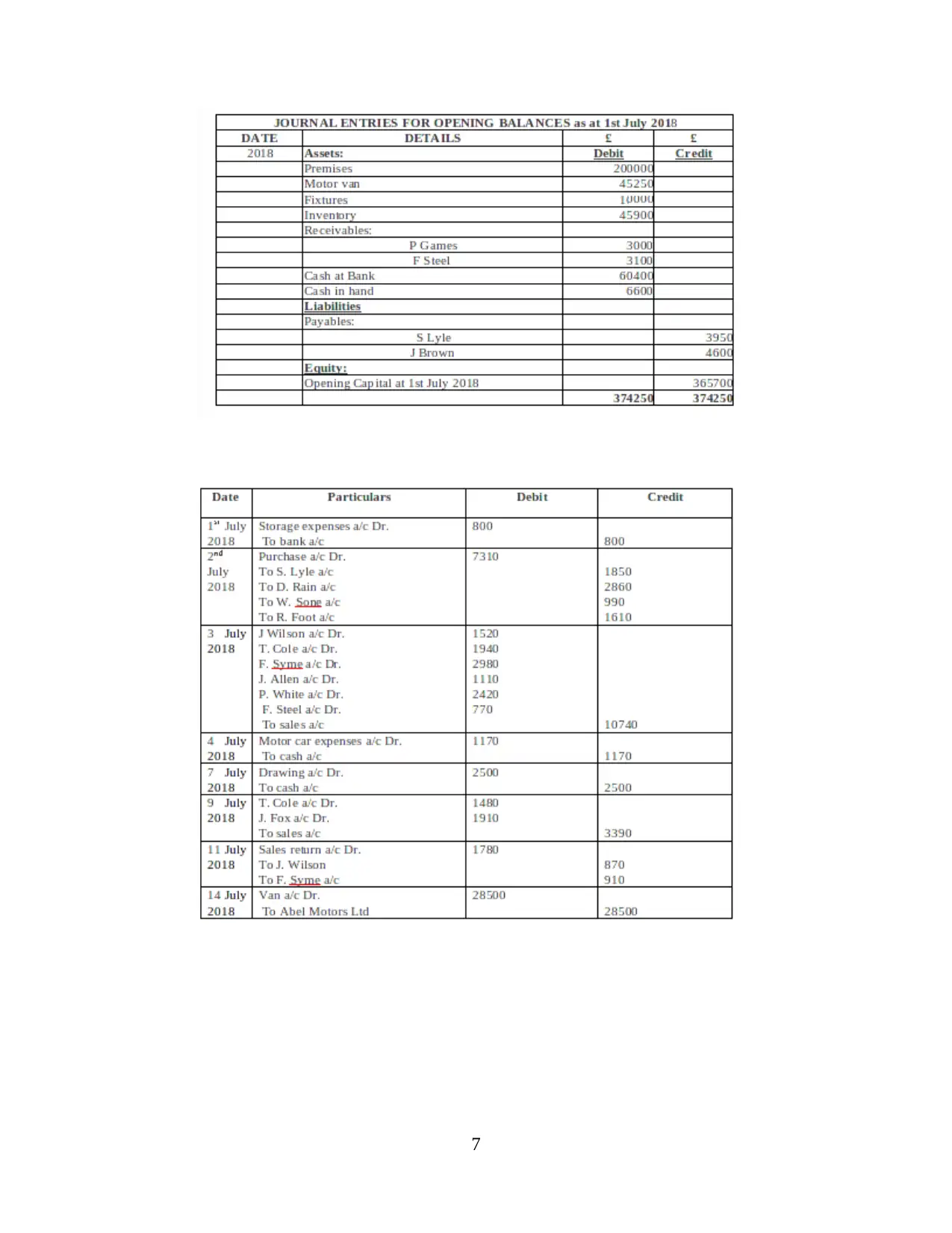

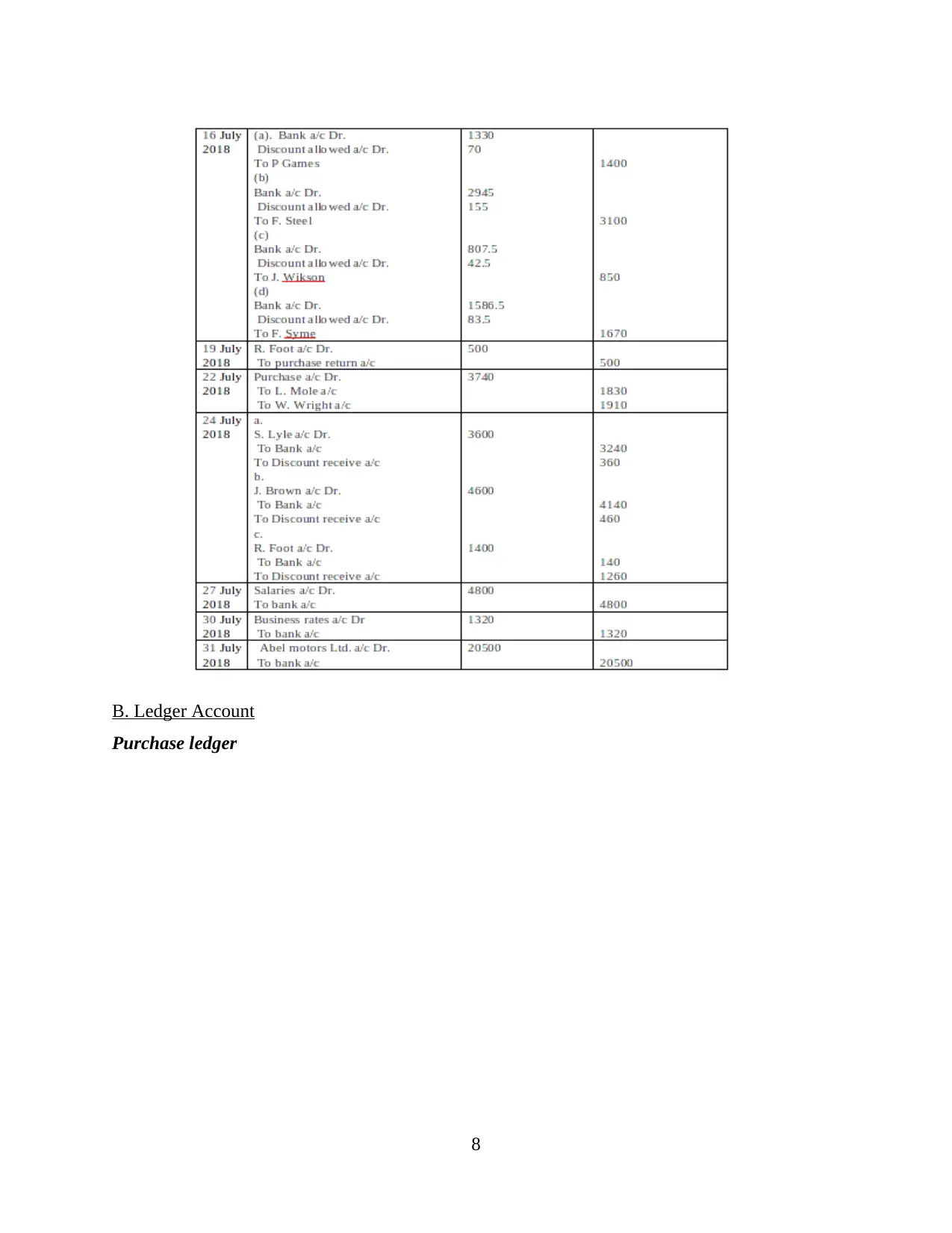

CLIENT 1

A. Journals entries for the company

6

Matching - This concept is systematically derived to use the accrual basis of

accounting. It needs that all revenues will be matched with all expenses (Mullinova,

2016). No business can measure future economic profit so that it would apply for

gaining uncertain revenue in the upcoming.

Materiality - It refers that management should record only those transactions that are

important for the company. An organisation can ignore minor events but it should

consider that major events should be fully recorded and disclosed.

All these core principles are useful in making the financial statements for a particular period of

a company.

Consistency - It derives that organisation should operate its business activities throughout the

period and never end it until all legal formalities are fulfilled. Every business should assume

that it operates for a long period.

Materiality – This principle should apply for all companies and it describes all major

transactions and give up all immaterial or small transactions (Nobes, 2014). In this context,

management team of an organisation should record only those transactions that are useful in

providing appropriate image of the entity and it is not essential to record any minor events.

CLIENT 1

A. Journals entries for the company

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

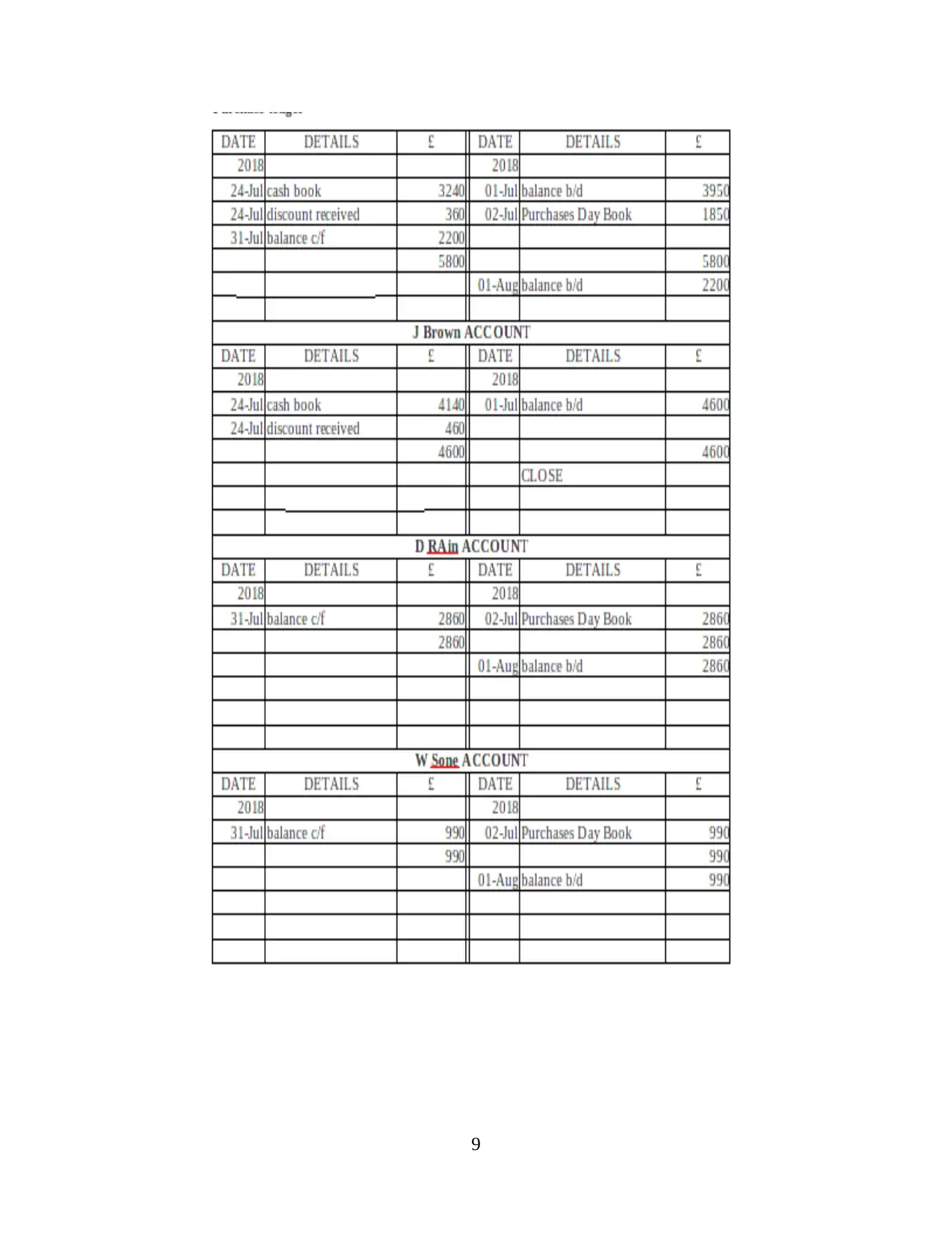

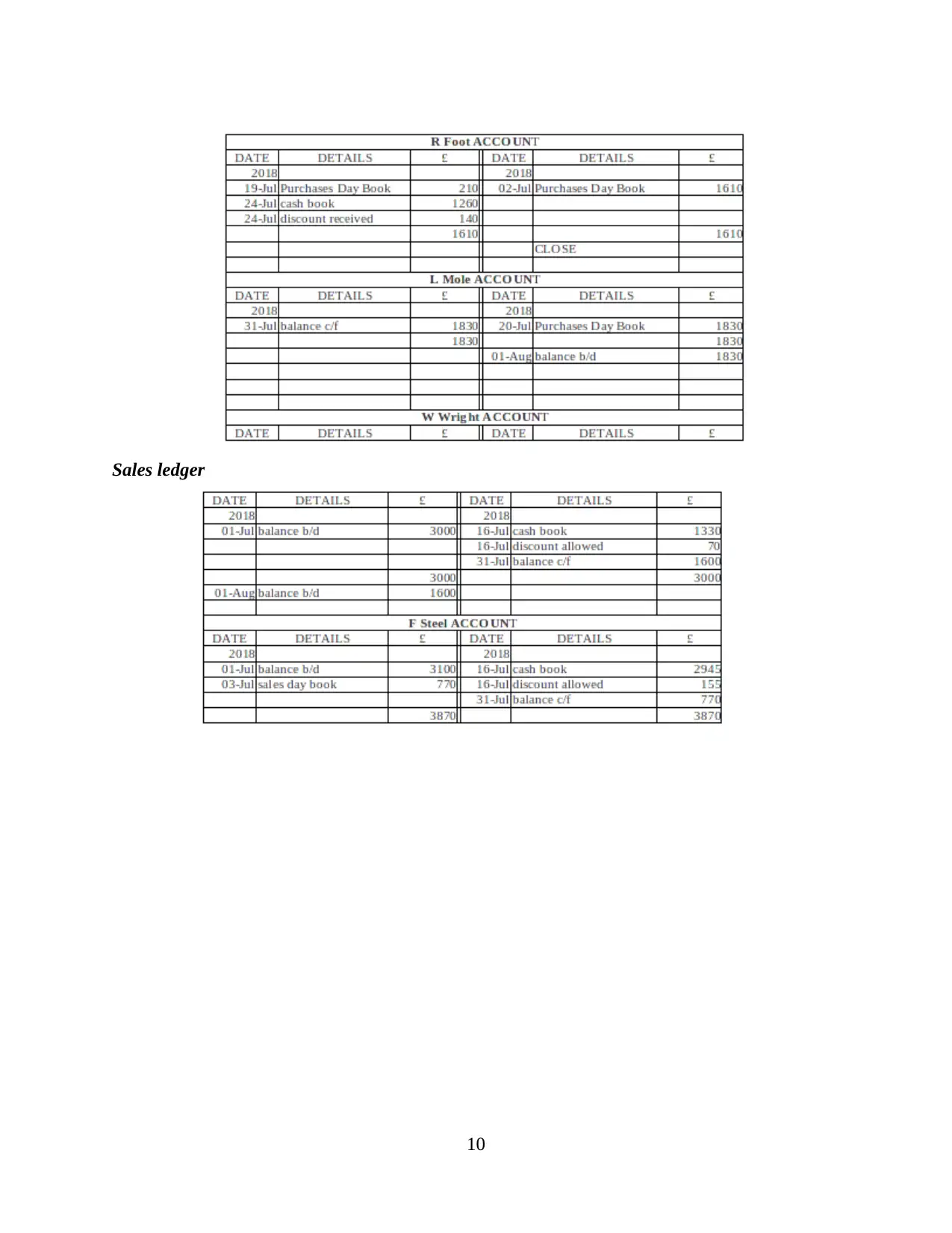

B. Ledger Account

Purchase ledger

8

Purchase ledger

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

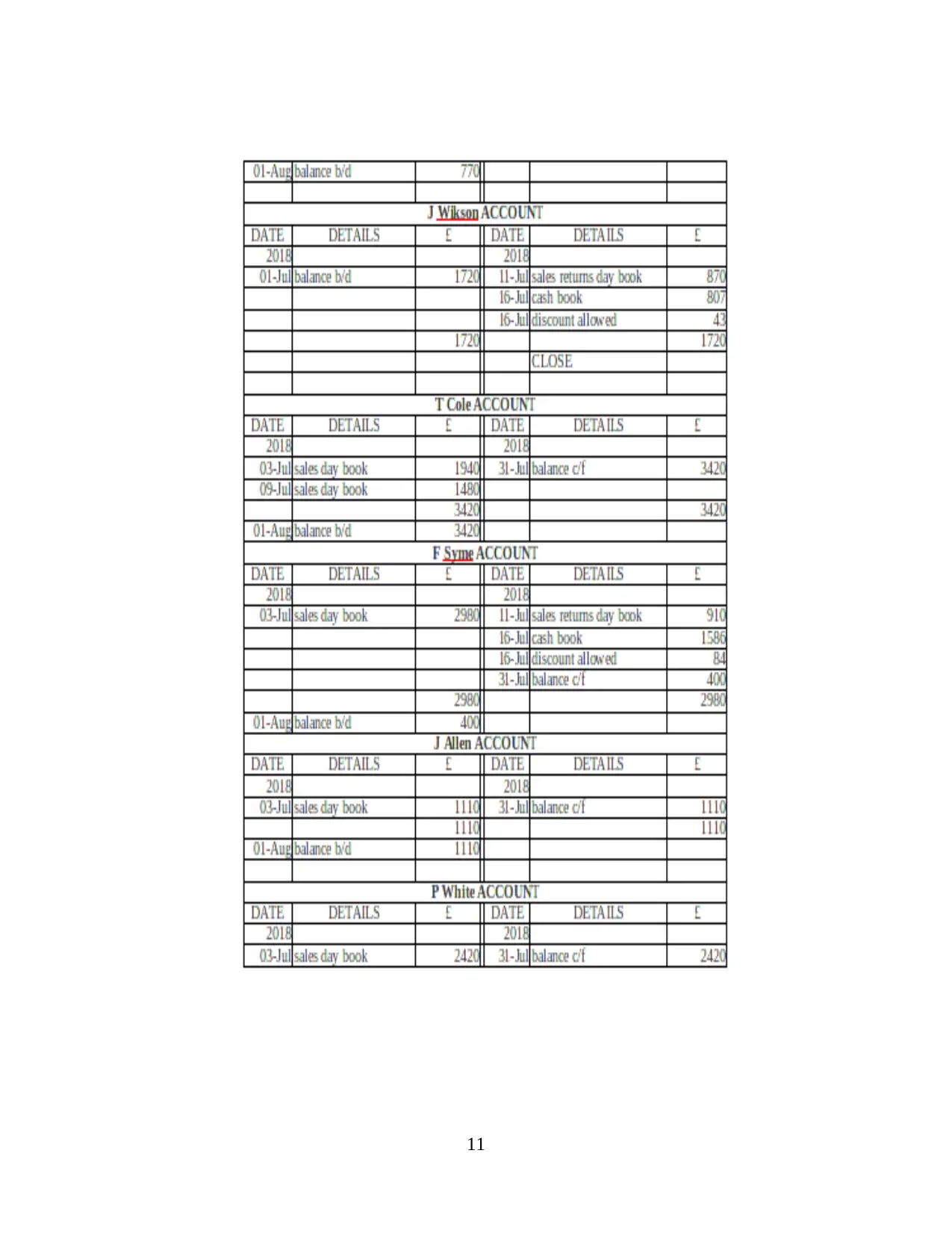

Sales ledger

10

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

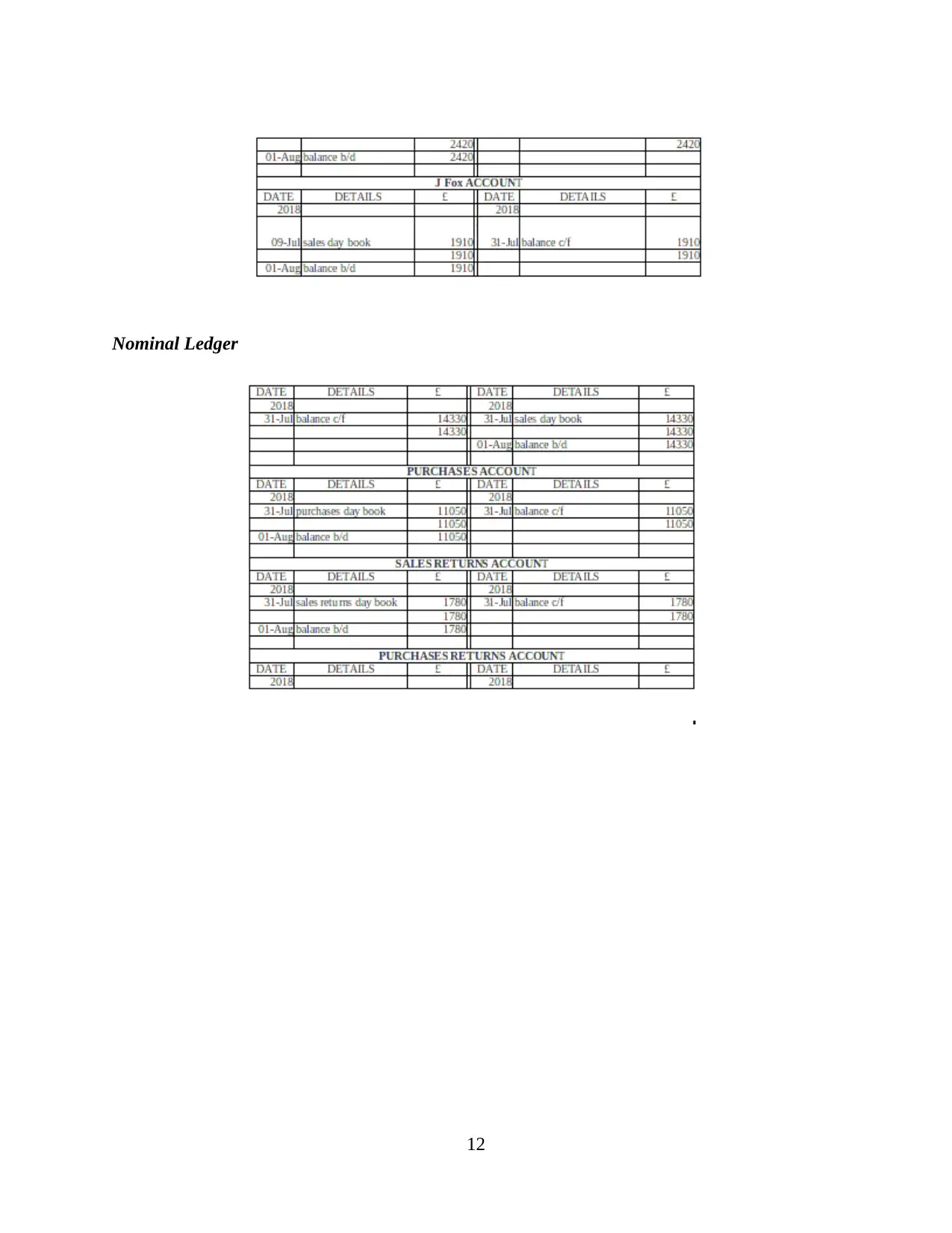

Nominal Ledger

12

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.