Financial Accounting Report: Scenario Analysis and Term Clarification

VerifiedAdded on 2021/02/20

|16

|4350

|19

Report

AI Summary

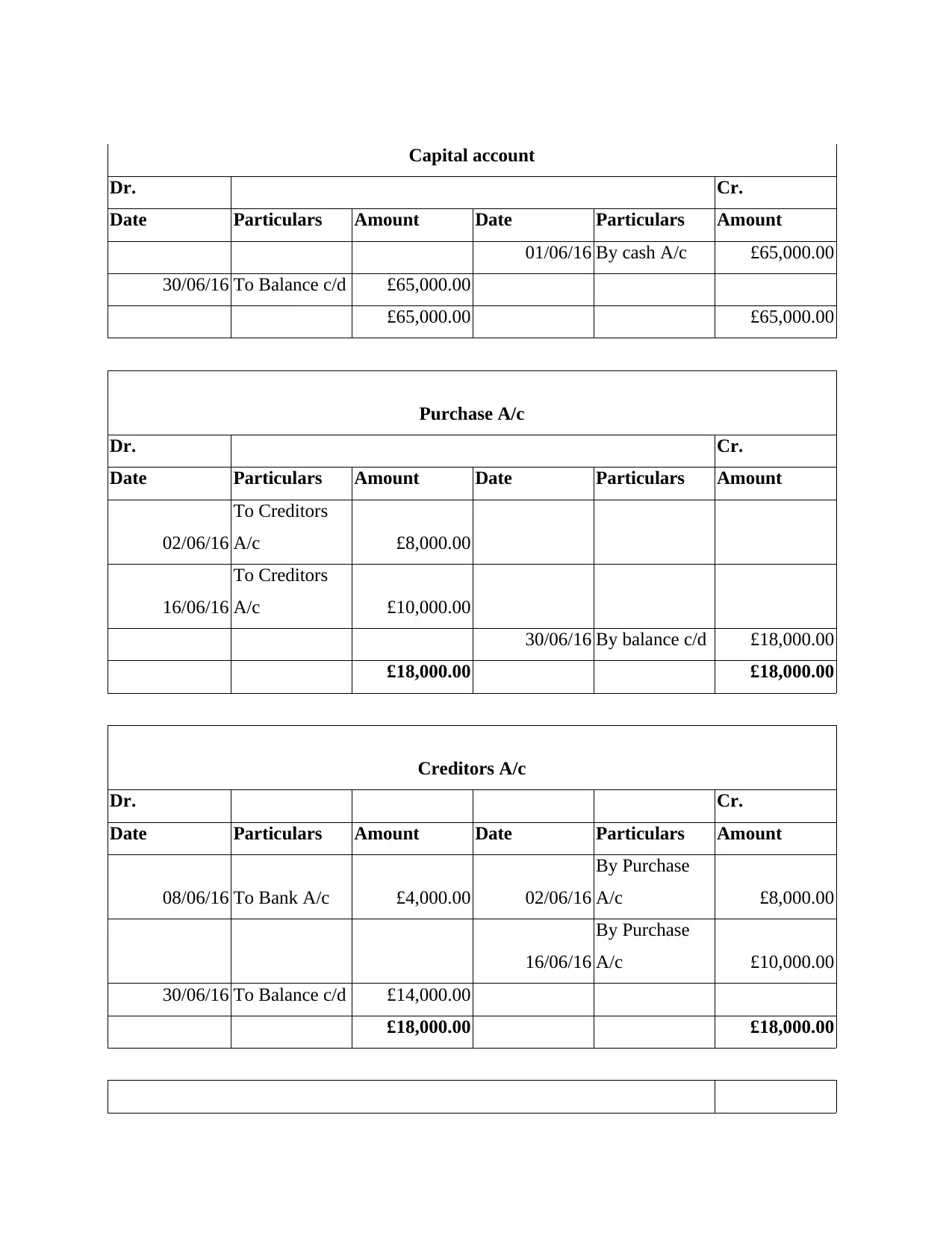

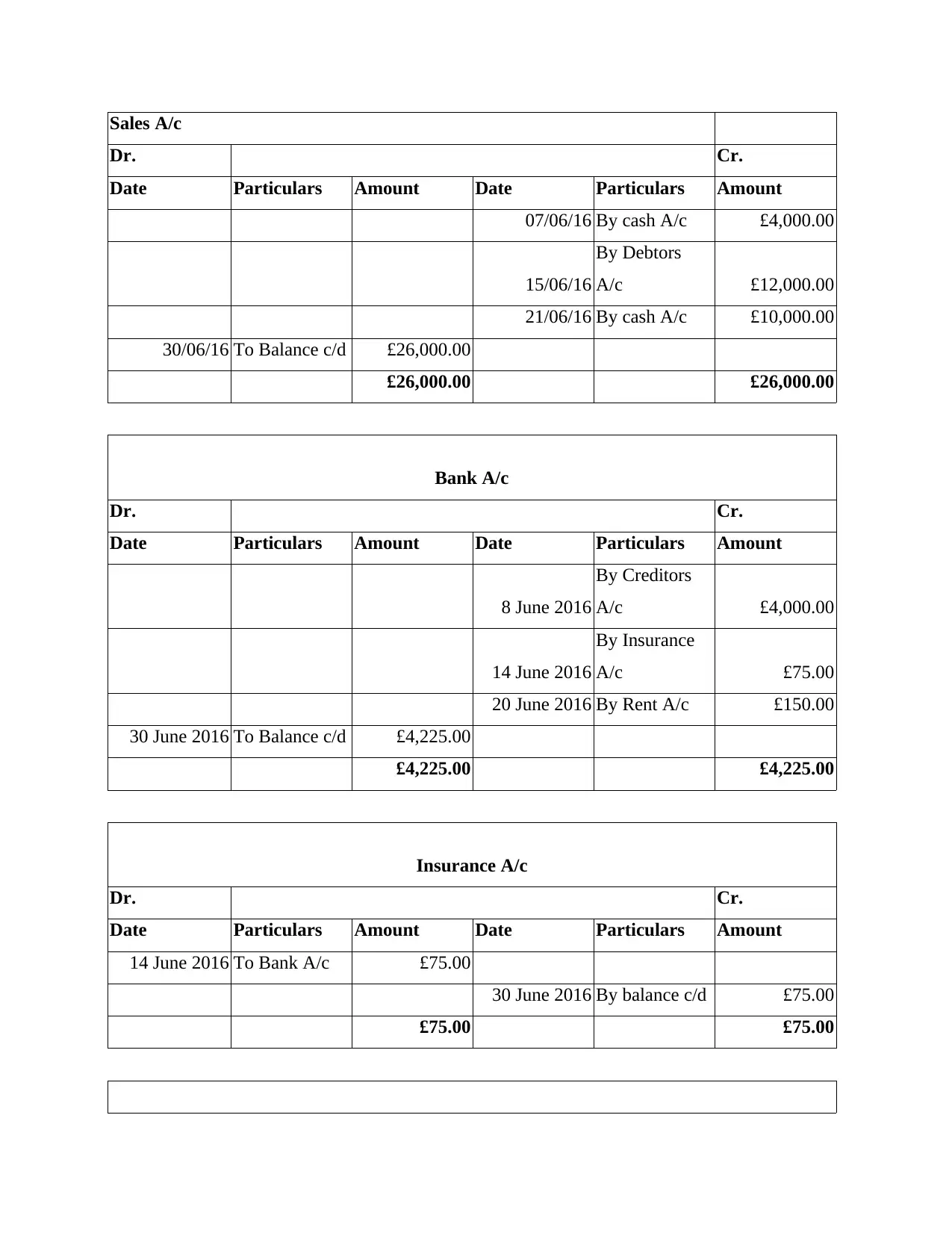

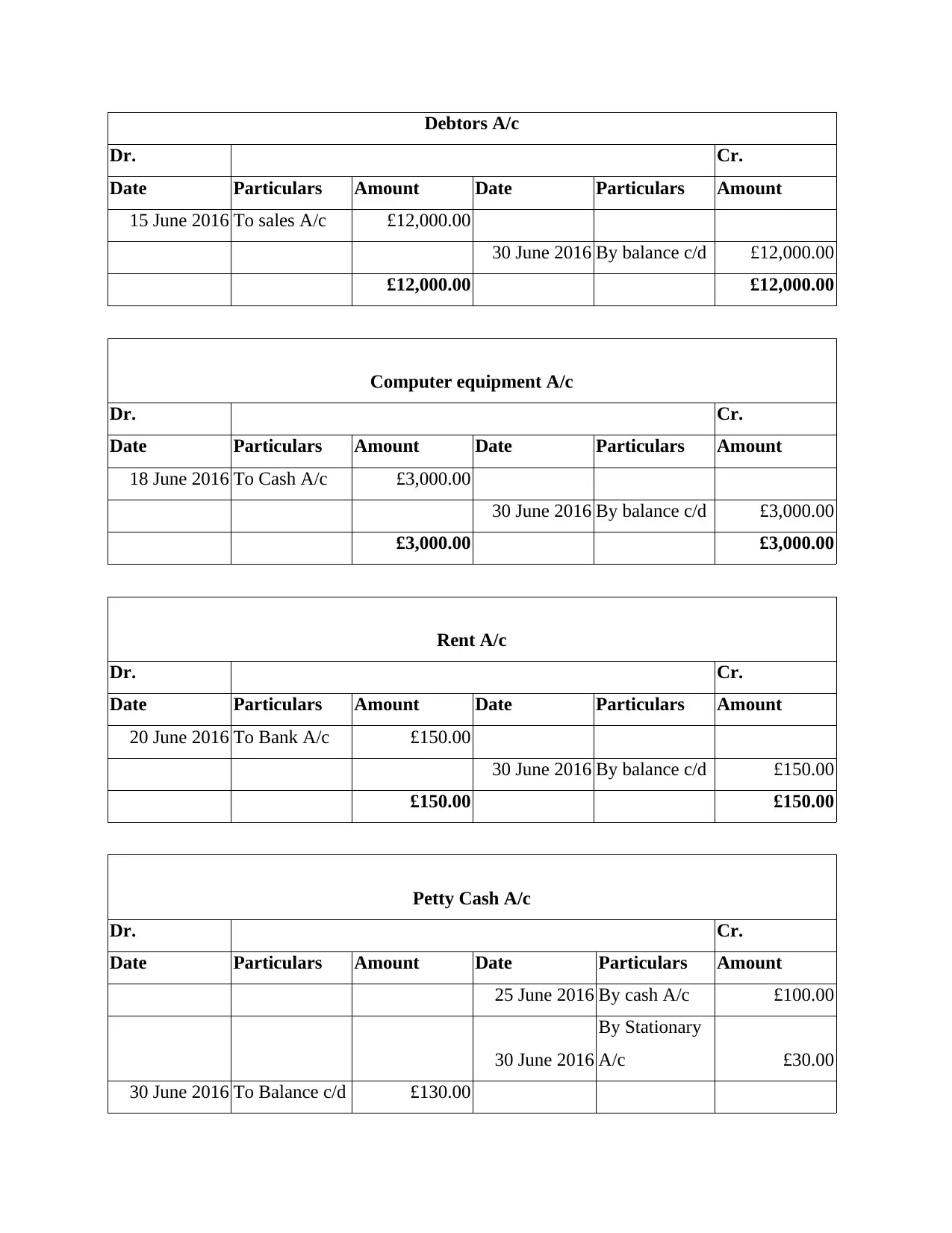

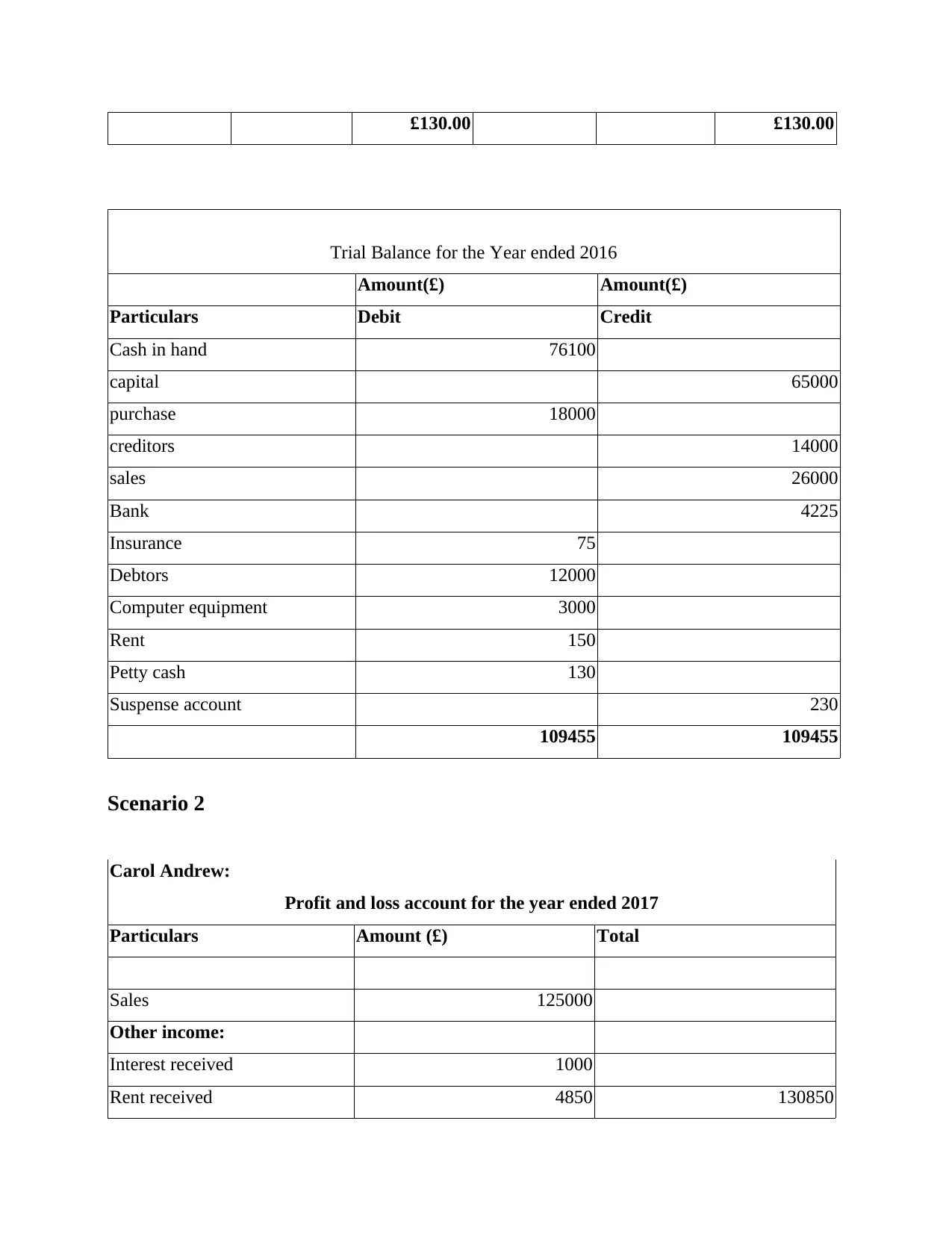

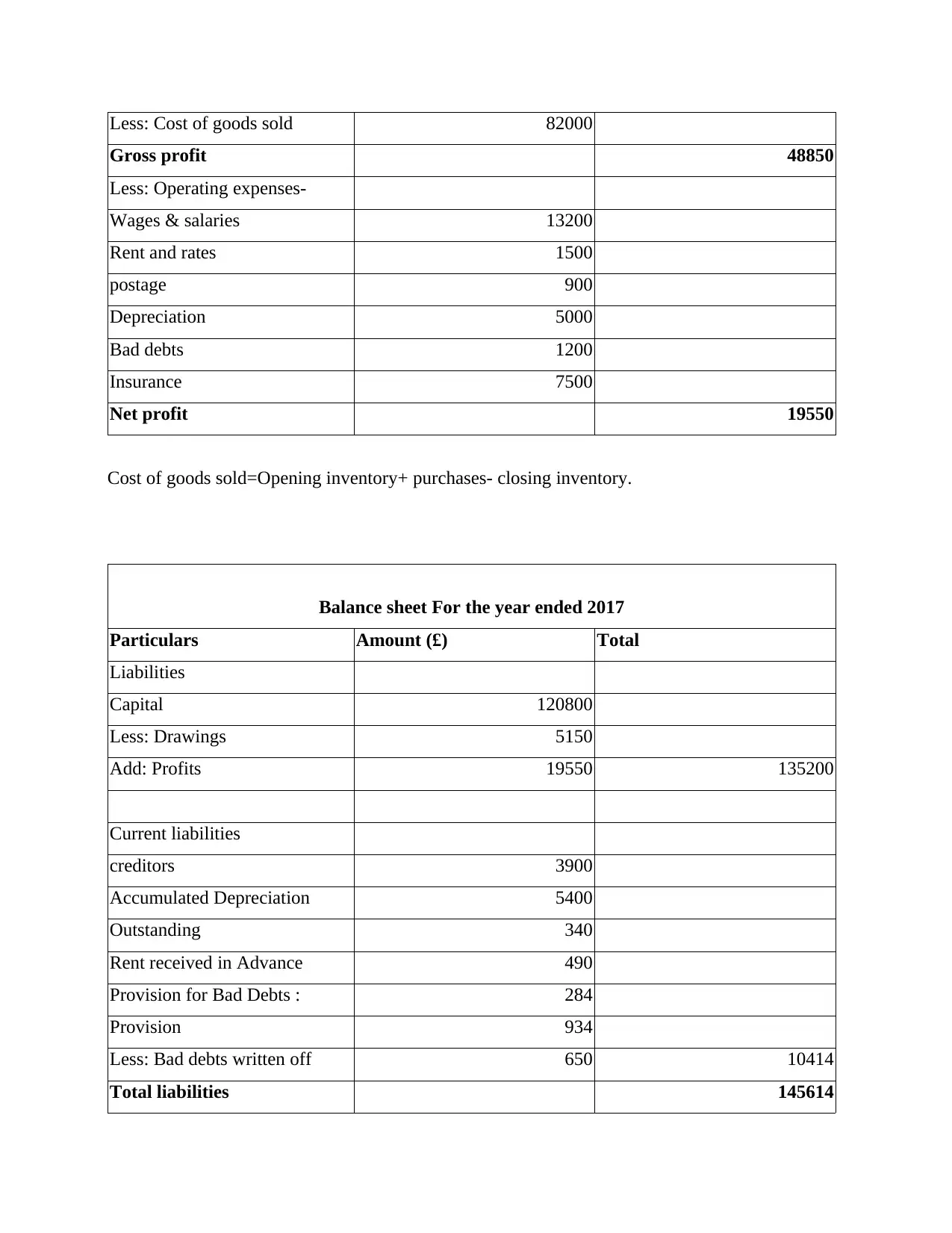

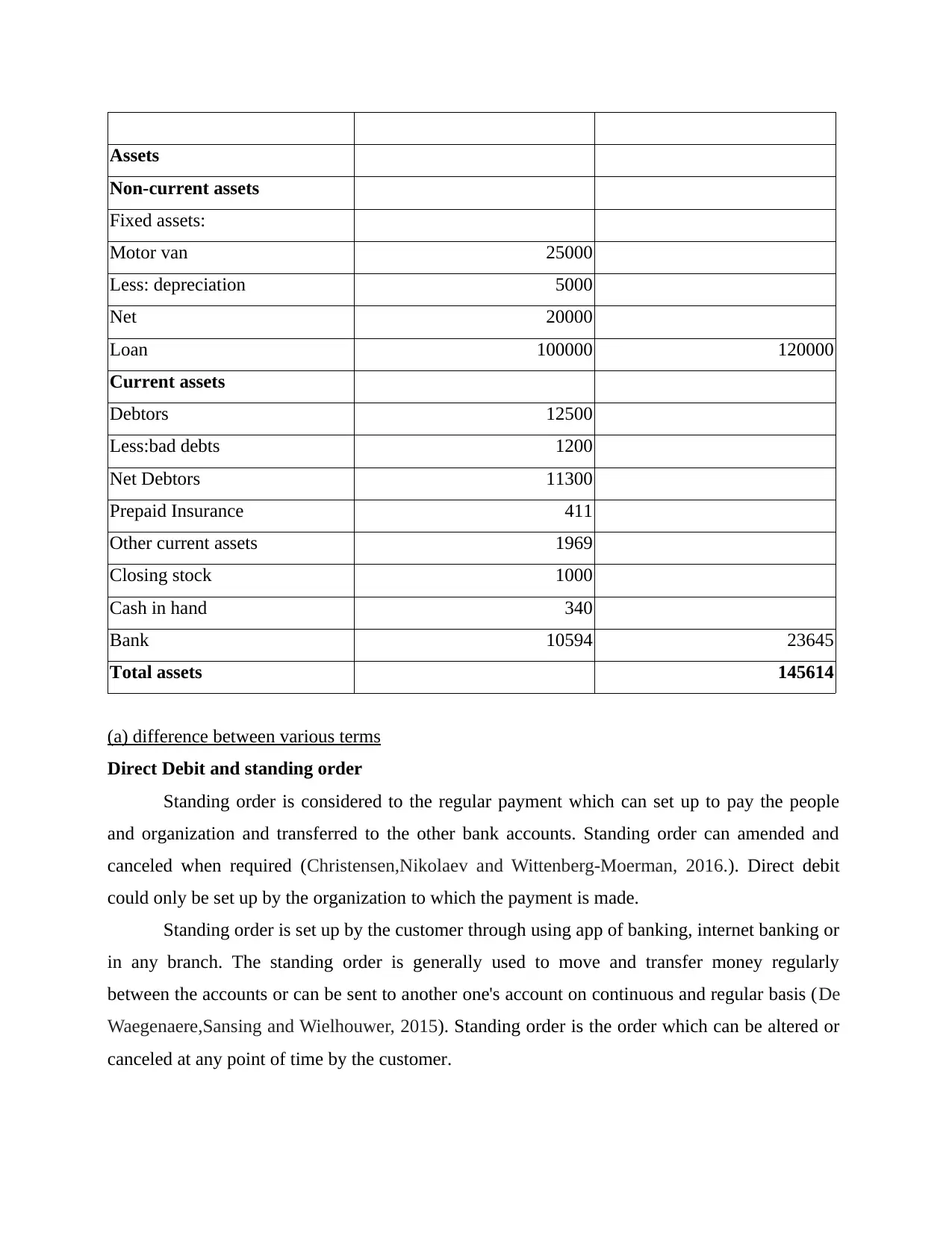

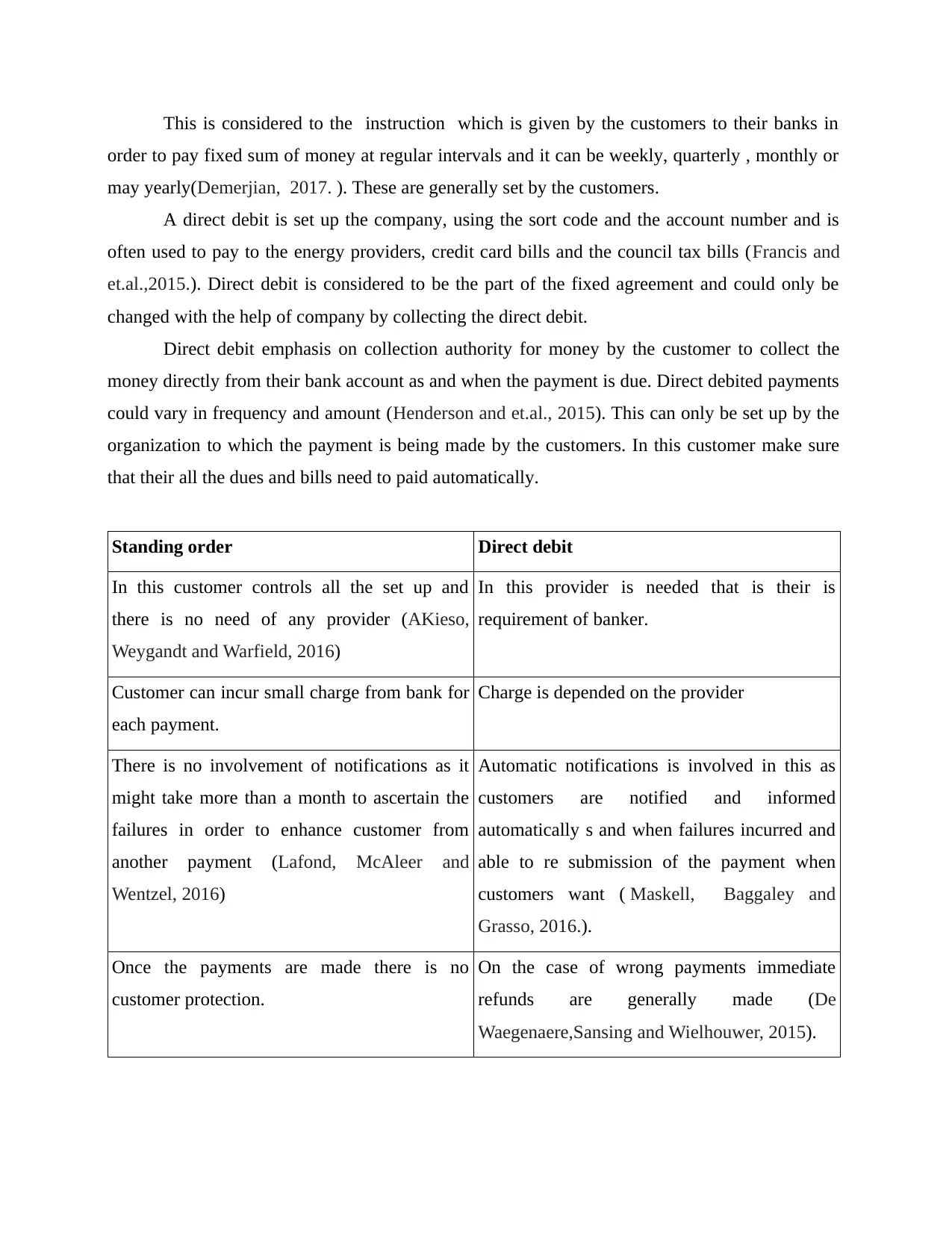

This financial accounting report provides a detailed analysis of financial transactions and the preparation of financial statements. The report begins with an introduction to financial accounting and its significance, followed by two scenarios demonstrating the recording of transactions through journal entries, ledger accounts, and trial balances. Scenario 1 includes the creation of journal entries, ledger accounts, and a trial balance, while Scenario 2 presents a profit and loss account and balance sheet. The report also includes explanations of key accounting terms such as standing orders, direct debits, dishonored checks, and bank charges. The report showcases the processes involved in financial accounting, including the preparation of financial statements and bank reconciliation, which aid businesses in decision-making. The content covers various aspects of financial accounting, providing a clear understanding of how financial transactions are recorded, classified, summarized, and presented in financial reports.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.