Financial Accounting Report: Principles, Regulations, and Analysis

VerifiedAdded on 2020/10/22

|19

|4093

|395

Report

AI Summary

This report provides a comprehensive overview of financial accounting principles, regulations, and their practical application through six client case studies. It begins with an introduction to financial accounting and its purpose, followed by an examination of relevant regulations and accounting rules, including the double-entry system, trial balances, and financial statements like the statement of profit and loss. The report delves into accounting principles such as going concern, separate entity, and revenue recognition, alongside conventions like consistency and material disclosure. Client-specific sections illustrate the application of these concepts, covering topics such as depreciation, bank reconciliation, and control accounts. The report concludes with a summary of key concepts and a list of references.

FINANCIAL

ACCOUNTING

PRINCIPLES

ACCOUNTING

PRINCIPLES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Financial Accounting..................................................................................................................3

Regulation relating to financial accounting................................................................................3

Accounting Rules and principles................................................................................................4

Conventions and concepts relating to consistency and material disclosure................................6

CLIENT 1........................................................................................................................................6

Double entry system....................................................................................................................6

Trial balance................................................................................................................................6

CLIENT 2........................................................................................................................................7

Statement of profit and loss.........................................................................................................7

Financial statement......................................................................................................................7

CLIENT 3........................................................................................................................................7

Consistency.................................................................................................................................7

Prudency......................................................................................................................................7

Purpose of depreciation...............................................................................................................7

Method of calculating depreciation.............................................................................................8

CLIENT 4........................................................................................................................................8

Bank Reconciliation Statement...................................................................................................8

Explain areas of to record bank records......................................................................................8

CLIENT 5........................................................................................................................................8

Sales ledger control account........................................................................................................8

Purchase ledger control account..................................................................................................8

Need to prepare control accounts................................................................................................9

CLIENT 6........................................................................................................................................9

Suspense account........................................................................................................................9

Differentiate between a suspense account and a clearing account..............................................9

CONCLUSION................................................................................................................................9

REFERENCERS ...........................................................................................................................10

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Financial Accounting..................................................................................................................3

Regulation relating to financial accounting................................................................................3

Accounting Rules and principles................................................................................................4

Conventions and concepts relating to consistency and material disclosure................................6

CLIENT 1........................................................................................................................................6

Double entry system....................................................................................................................6

Trial balance................................................................................................................................6

CLIENT 2........................................................................................................................................7

Statement of profit and loss.........................................................................................................7

Financial statement......................................................................................................................7

CLIENT 3........................................................................................................................................7

Consistency.................................................................................................................................7

Prudency......................................................................................................................................7

Purpose of depreciation...............................................................................................................7

Method of calculating depreciation.............................................................................................8

CLIENT 4........................................................................................................................................8

Bank Reconciliation Statement...................................................................................................8

Explain areas of to record bank records......................................................................................8

CLIENT 5........................................................................................................................................8

Sales ledger control account........................................................................................................8

Purchase ledger control account..................................................................................................8

Need to prepare control accounts................................................................................................9

CLIENT 6........................................................................................................................................9

Suspense account........................................................................................................................9

Differentiate between a suspense account and a clearing account..............................................9

CONCLUSION................................................................................................................................9

REFERENCERS ...........................................................................................................................10

INTRODUCTION

Financial accounting is the division of accounting that are direction on giving external

users with helpful information. It is a way to providing financial information with the help of

report of business activity (Christensen and Nikolaev, 2013). These reports are providing to

investors, creditors and other people are related to out side of the business. When prepare of

these reports that time using principles of accounting that are shows reports in effective way.

In this report covers prepare report on financial accounting, regulations, rules and

principles, conventions and concepts of consistency and material disclosure. These report

prepare to according six clients that are wants to different requirement.

MAIN BODY

Financial Accounting

It is the procedure of recording, sum-up and reporting the uncounted of transactions

resulting from business operations over a period of time. These transactions are are recorded and

shows that in financial statement are prepare of the company. In the financial statement are

including profit and loss account, cash flow statement and balance sheet. It is recording the

performance of the company in a specified period. It is include all system that are supervisor and

control of money as it flows out of an organization as an assets and liabilities, income and

expenses.

Regulation relating to financial accounting

Regulation means it is a set of rules that is planned to regulate conduct and control by the

authority. According to definition regulations are related to financial accounting as a rules that

are formulated by independent authoritative body to govern the preparation of financial

statements which are related to accounting standards. The regulation of financial accounting are

divided in to two parts first one is international and second is domestic (Collins, Pasewark, and

Riley, 2012).

In domestic regulation was largely absent in Ireland and the UK prior to the 1970s. The

institute of charted accountant

The international accounting standards committee (IASC) was established in 1973. It is

issued by the accounting standards that are calling to international accounting standards (IAS).

Financial accounting is the division of accounting that are direction on giving external

users with helpful information. It is a way to providing financial information with the help of

report of business activity (Christensen and Nikolaev, 2013). These reports are providing to

investors, creditors and other people are related to out side of the business. When prepare of

these reports that time using principles of accounting that are shows reports in effective way.

In this report covers prepare report on financial accounting, regulations, rules and

principles, conventions and concepts of consistency and material disclosure. These report

prepare to according six clients that are wants to different requirement.

MAIN BODY

Financial Accounting

It is the procedure of recording, sum-up and reporting the uncounted of transactions

resulting from business operations over a period of time. These transactions are are recorded and

shows that in financial statement are prepare of the company. In the financial statement are

including profit and loss account, cash flow statement and balance sheet. It is recording the

performance of the company in a specified period. It is include all system that are supervisor and

control of money as it flows out of an organization as an assets and liabilities, income and

expenses.

Regulation relating to financial accounting

Regulation means it is a set of rules that is planned to regulate conduct and control by the

authority. According to definition regulations are related to financial accounting as a rules that

are formulated by independent authoritative body to govern the preparation of financial

statements which are related to accounting standards. The regulation of financial accounting are

divided in to two parts first one is international and second is domestic (Collins, Pasewark, and

Riley, 2012).

In domestic regulation was largely absent in Ireland and the UK prior to the 1970s. The

institute of charted accountant

The international accounting standards committee (IASC) was established in 1973. It is

issued by the accounting standards that are calling to international accounting standards (IAS).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Rules and principles

The accounting system based on double entry system related to debit and credit. It is very

useful but in the reality its not perfectly to maintain. For maintain this system need to three

golden rules of accounting help to identify particular item. They are as follows -

Debit the receiver, credit the giver

This principle relating to the personal accounts. If a person giving something to any other

organization so that time who is receiving like organization is recorded that transaction as a debit

section but that person who is giving that is recorded as the credit section in the books of

accounts.

Debit what comes in and credit what goes out

This types principles are applied on real accounts, in this accounts are including land and

building and land. All of these accounts already have debit balance by default so when getting

any property that are increasing amount in debit balance but when sale out of property that

amounts shows in credit section (Edwards, 2013).

Debit all expenses and losses, credit all incomes and gains

It is applied on nominal account and in this account presents as a question. These types of

accounts have credit balance by default. When all the incomes and gains are acquired by the

company so it will increase in relating account as a credit balance. But when all expenses and

losses are bear by the company on particular amount that time decreases and shows in debit side.

Example of nominal account is Capital account.

Accounting principles – It is a general concepts and rules are applied on accounting to recoded

transactions of any companies. These principles “generally accepted accounting principle”

(GAAP) are included of principles, are the following as -1. Going concern principle – This accounting concept based on that business will continue

going on for long time period. So depreciation are calculation based on this principle

because the business will not to functioning and pay off for its assets at flaming sale

value.2. Separate entity concept – It is describe that entity of the business and individual are kept

separate. The transactions also keep separate related to entities and in this including

assets and liabilities.

The accounting system based on double entry system related to debit and credit. It is very

useful but in the reality its not perfectly to maintain. For maintain this system need to three

golden rules of accounting help to identify particular item. They are as follows -

Debit the receiver, credit the giver

This principle relating to the personal accounts. If a person giving something to any other

organization so that time who is receiving like organization is recorded that transaction as a debit

section but that person who is giving that is recorded as the credit section in the books of

accounts.

Debit what comes in and credit what goes out

This types principles are applied on real accounts, in this accounts are including land and

building and land. All of these accounts already have debit balance by default so when getting

any property that are increasing amount in debit balance but when sale out of property that

amounts shows in credit section (Edwards, 2013).

Debit all expenses and losses, credit all incomes and gains

It is applied on nominal account and in this account presents as a question. These types of

accounts have credit balance by default. When all the incomes and gains are acquired by the

company so it will increase in relating account as a credit balance. But when all expenses and

losses are bear by the company on particular amount that time decreases and shows in debit side.

Example of nominal account is Capital account.

Accounting principles – It is a general concepts and rules are applied on accounting to recoded

transactions of any companies. These principles “generally accepted accounting principle”

(GAAP) are included of principles, are the following as -1. Going concern principle – This accounting concept based on that business will continue

going on for long time period. So depreciation are calculation based on this principle

because the business will not to functioning and pay off for its assets at flaming sale

value.2. Separate entity concept – It is describe that entity of the business and individual are kept

separate. The transactions also keep separate related to entities and in this including

assets and liabilities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Money measurement – This concepts describes that when transactions are measured in

money so recorded in financial statements but when not measures so they did not

recorded like as services and other things.4. Dual concept – It is main concept that are adopted by the all companies according to the

when any transaction happen in the organisation that time effected to both accounts.5. Revenue recognition principle – In this concept are revenues are recognise when

transactions are completed in gardening process.6. Reliability principle – In this principle transaction are recorded when they are actually

occur. For example when selling to goods of any organisation that time prepare of

invoice so the is proof to recoding of the transaction (Glover, 2014).7. Matching concept – It is telling that when recorded revenues related transactions in

financial statement that time also recoded expenses at the same time. The inventors was

charge according to cost of goods sold. But not including cash related accounting in this

principle.8. Full disclosure principle – According to this concept business will be disclose of

financial statements and accounting statements are impact to rears mentality. These

statements are providing to investors, creditors and other persons need to be know about

that. It is also depended to types of companies.9. Consistency principle – This concept says all enterprises not apply same principle so

they are applying different Principe. And company adopted a particular principle so it

will going to continue to future while not getting new principle to company.10. Conservatism principle – This concept says that when identify expenses and liabilities

are recoded as soon as possible. In opposite when identify revenues and profit that are

recorded when sure about them. It may be effected to financial statement but revenue and

assets recognise and encourage for future (Profit and Loss account. 2018).11. Cost principle – According to this concept recorded cost of each transaction like as assets

and liabilities and equity investments. These items are recorded related to accounts and

on the purchase cost. In this assets and liabilities are asset according to fair value.12. Accrual principle – In this concept those transactions are recorded are actually occur in

related to financial year. It is important to cash flow are associated to them. In this

concept transactions are recorded on accrual basis.

money so recorded in financial statements but when not measures so they did not

recorded like as services and other things.4. Dual concept – It is main concept that are adopted by the all companies according to the

when any transaction happen in the organisation that time effected to both accounts.5. Revenue recognition principle – In this concept are revenues are recognise when

transactions are completed in gardening process.6. Reliability principle – In this principle transaction are recorded when they are actually

occur. For example when selling to goods of any organisation that time prepare of

invoice so the is proof to recoding of the transaction (Glover, 2014).7. Matching concept – It is telling that when recorded revenues related transactions in

financial statement that time also recoded expenses at the same time. The inventors was

charge according to cost of goods sold. But not including cash related accounting in this

principle.8. Full disclosure principle – According to this concept business will be disclose of

financial statements and accounting statements are impact to rears mentality. These

statements are providing to investors, creditors and other persons need to be know about

that. It is also depended to types of companies.9. Consistency principle – This concept says all enterprises not apply same principle so

they are applying different Principe. And company adopted a particular principle so it

will going to continue to future while not getting new principle to company.10. Conservatism principle – This concept says that when identify expenses and liabilities

are recoded as soon as possible. In opposite when identify revenues and profit that are

recorded when sure about them. It may be effected to financial statement but revenue and

assets recognise and encourage for future (Profit and Loss account. 2018).11. Cost principle – According to this concept recorded cost of each transaction like as assets

and liabilities and equity investments. These items are recorded related to accounts and

on the purchase cost. In this assets and liabilities are asset according to fair value.12. Accrual principle – In this concept those transactions are recorded are actually occur in

related to financial year. It is important to cash flow are associated to them. In this

concept transactions are recorded on accrual basis.

13. Materiality concept – this concept described that in the financial statement recorded that

transaction are not happen but sure to occur in future so included that because when

shows to public these statement so it will effect in positive way.

Conventions and concepts relating to consistency and material disclosure

The convention of consistency describes that accounting practices should showing that

amount are not charging from one to another period. According to concepts are in business

consistency will be continue to operate business activities. For example depreciation are charged

on fixed assets with the particular method.

It is a one of the most significant convection that are related to materiality. This terms

applies only when provide sufficient information because in this not fully material details giving

to any one. In this recorded those items that are internally bearing and insignificant are ignored

by the company (Hatfield, 2014). It is matter relating to judgement and on the basis this taking

decision.

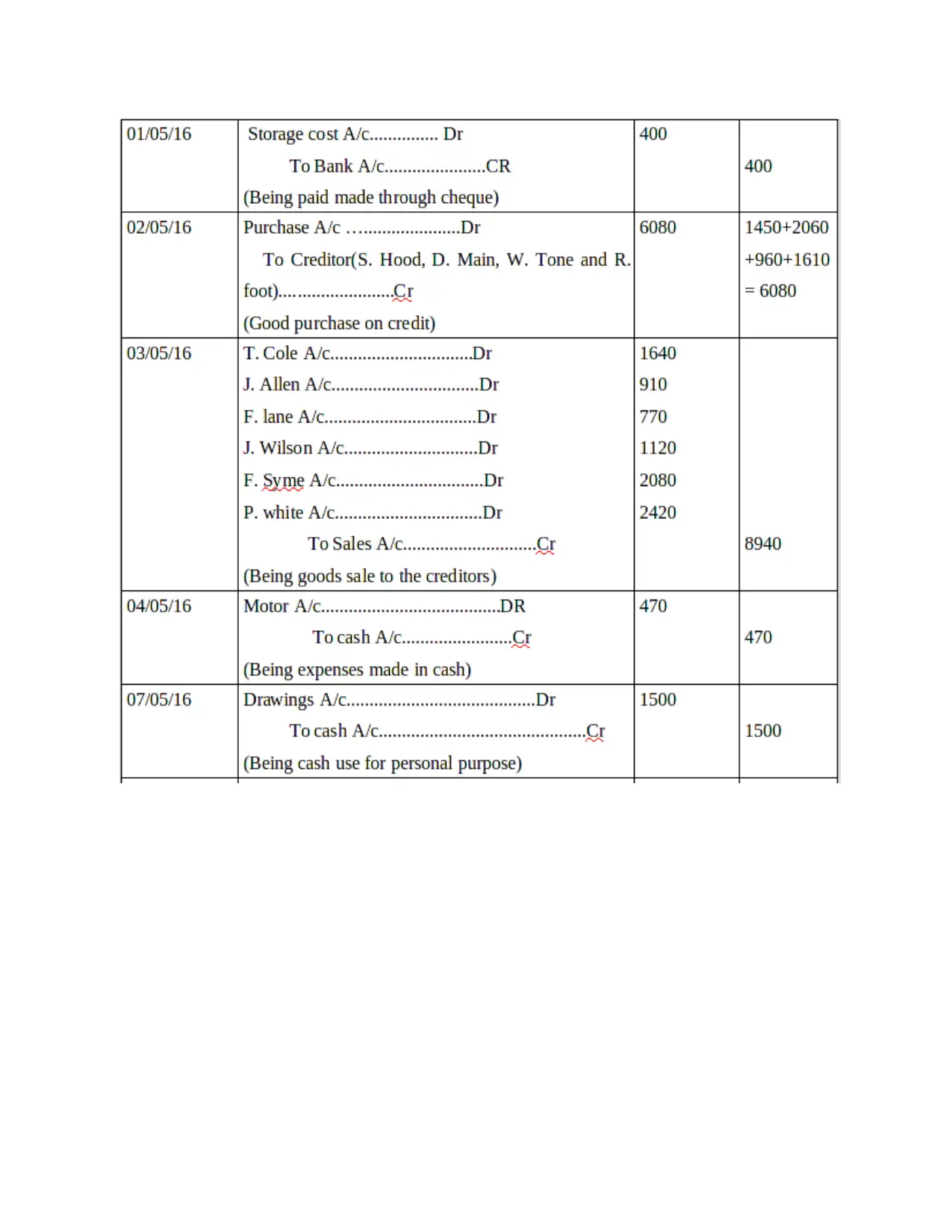

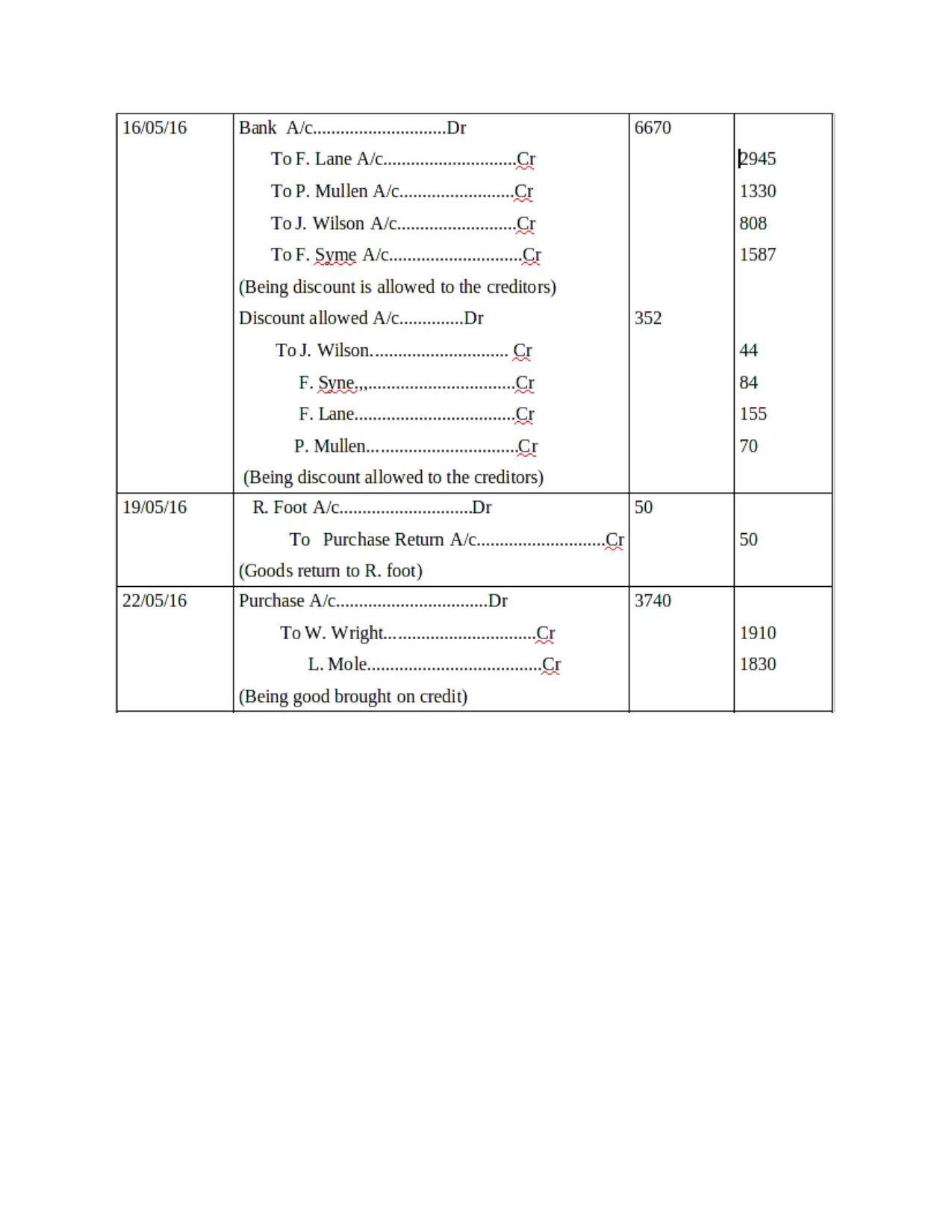

CLIENT 1

Double entry system

The system of double entry are relating to accounting that means every business

transaction every transaction that are related to business effect to both sides. These both sides

means both accounts that are created regarding to transaction. For example when an enterprises

taking loan from bank, so effects shows in the company's cash accounts and accounts or payable.

Both accounts are effected as cash account is increases and coming head in asset side and

accounts payable that are coming to liability side is also increases (Purchase ledger control

account. 2018). This systems helps to create balance in shows by accounting equation is -

Assets = Liabilities + Owner's equity

Double entry system recoding the transactions according to debit item and credit item. When

record a debit entry in one account that time also effected to another account that are related to

credit entry. It means that the total of all debit accounts equivalent to total of credit accounts.

This method of accounting and book keeping carry out accurate result and provide description of

financial statements. Hence, it helping to detecting error when prepare financial statements.

transaction are not happen but sure to occur in future so included that because when

shows to public these statement so it will effect in positive way.

Conventions and concepts relating to consistency and material disclosure

The convention of consistency describes that accounting practices should showing that

amount are not charging from one to another period. According to concepts are in business

consistency will be continue to operate business activities. For example depreciation are charged

on fixed assets with the particular method.

It is a one of the most significant convection that are related to materiality. This terms

applies only when provide sufficient information because in this not fully material details giving

to any one. In this recorded those items that are internally bearing and insignificant are ignored

by the company (Hatfield, 2014). It is matter relating to judgement and on the basis this taking

decision.

CLIENT 1

Double entry system

The system of double entry are relating to accounting that means every business

transaction every transaction that are related to business effect to both sides. These both sides

means both accounts that are created regarding to transaction. For example when an enterprises

taking loan from bank, so effects shows in the company's cash accounts and accounts or payable.

Both accounts are effected as cash account is increases and coming head in asset side and

accounts payable that are coming to liability side is also increases (Purchase ledger control

account. 2018). This systems helps to create balance in shows by accounting equation is -

Assets = Liabilities + Owner's equity

Double entry system recoding the transactions according to debit item and credit item. When

record a debit entry in one account that time also effected to another account that are related to

credit entry. It means that the total of all debit accounts equivalent to total of credit accounts.

This method of accounting and book keeping carry out accurate result and provide description of

financial statements. Hence, it helping to detecting error when prepare financial statements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

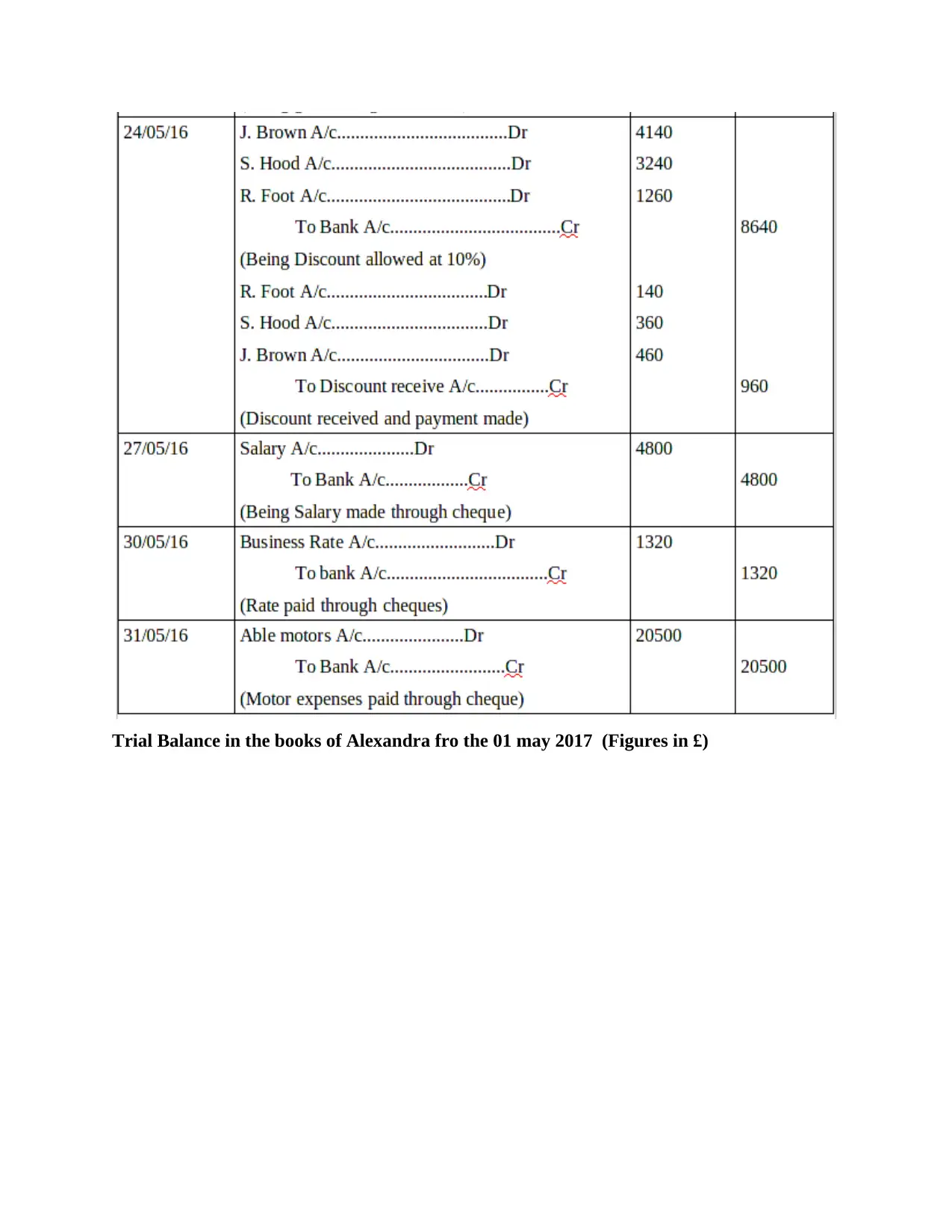

Trial balance

It is a accounting report that are prepare list of all accounts balance that are related to

particular organization. If accounts have not balance so it will be omitted. Trial balance divided

in two parts first one is debit balance and second one credit balance. This accounts and amounts

are related to debit that are record in debit head and opposite to those are related to credit that are

record as credit balance. In the end calculated total of both heads, that are identical (Horngren,

and et. al., 2012).

It is extremity system of trial balance that are prepared by the accountant in order to

shows whether including some maths and posting errors. In the present time coming accounting

software that are reduce these errors. So these software are decrease values of trial balance since

it is mostly calculating the sum of debit and credit columns are equal or not.

It is a accounting report that are prepare list of all accounts balance that are related to

particular organization. If accounts have not balance so it will be omitted. Trial balance divided

in two parts first one is debit balance and second one credit balance. This accounts and amounts

are related to debit that are record in debit head and opposite to those are related to credit that are

record as credit balance. In the end calculated total of both heads, that are identical (Horngren,

and et. al., 2012).

It is extremity system of trial balance that are prepared by the accountant in order to

shows whether including some maths and posting errors. In the present time coming accounting

software that are reduce these errors. So these software are decrease values of trial balance since

it is mostly calculating the sum of debit and credit columns are equal or not.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

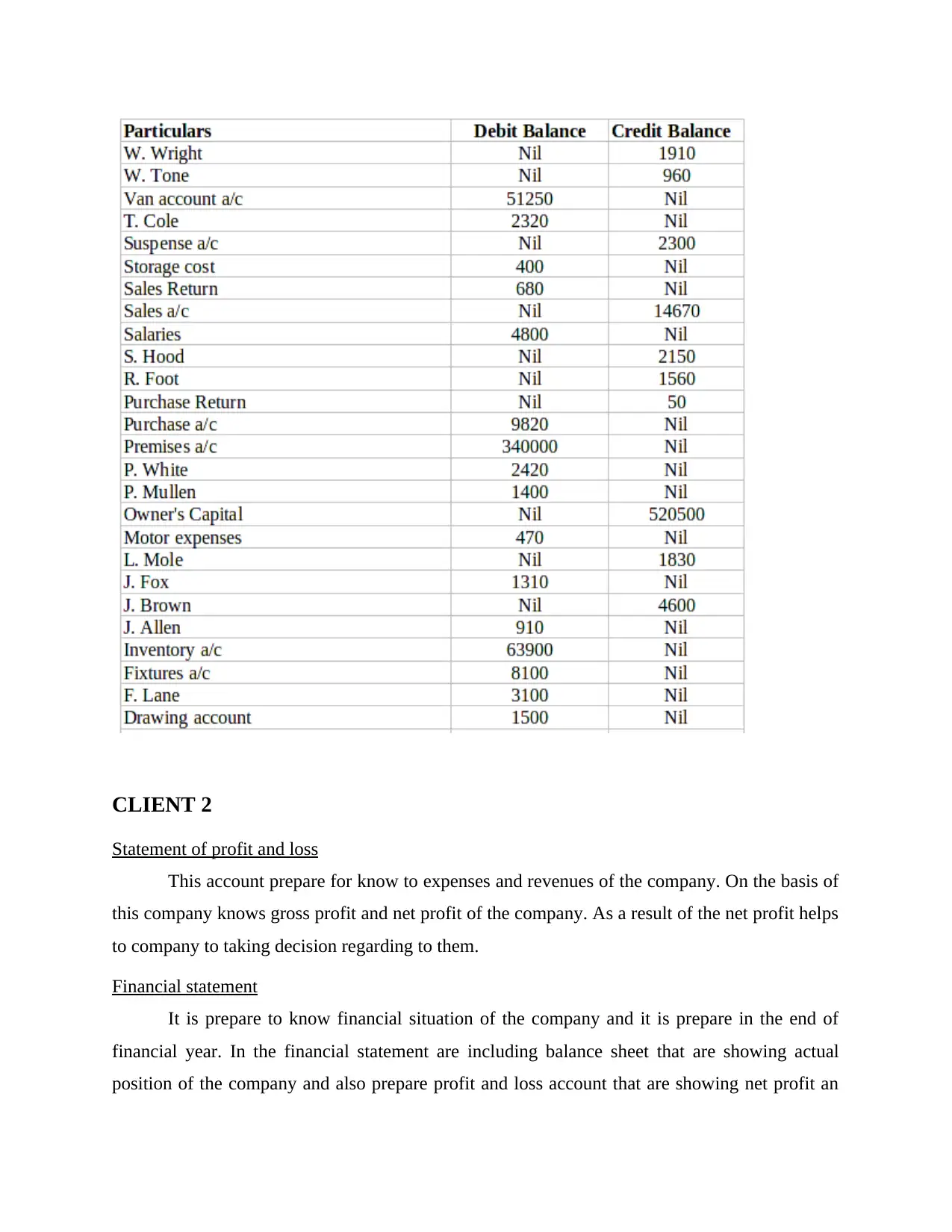

Trial Balance in the books of Alexandra fro the 01 may 2017 (Figures in £)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CLIENT 2

Statement of profit and loss

This account prepare for know to expenses and revenues of the company. On the basis of

this company knows gross profit and net profit of the company. As a result of the net profit helps

to company to taking decision regarding to them.

Financial statement

It is prepare to know financial situation of the company and it is prepare in the end of

financial year. In the financial statement are including balance sheet that are showing actual

position of the company and also prepare profit and loss account that are showing net profit an

Statement of profit and loss

This account prepare for know to expenses and revenues of the company. On the basis of

this company knows gross profit and net profit of the company. As a result of the net profit helps

to company to taking decision regarding to them.

Financial statement

It is prepare to know financial situation of the company and it is prepare in the end of

financial year. In the financial statement are including balance sheet that are showing actual

position of the company and also prepare profit and loss account that are showing net profit an

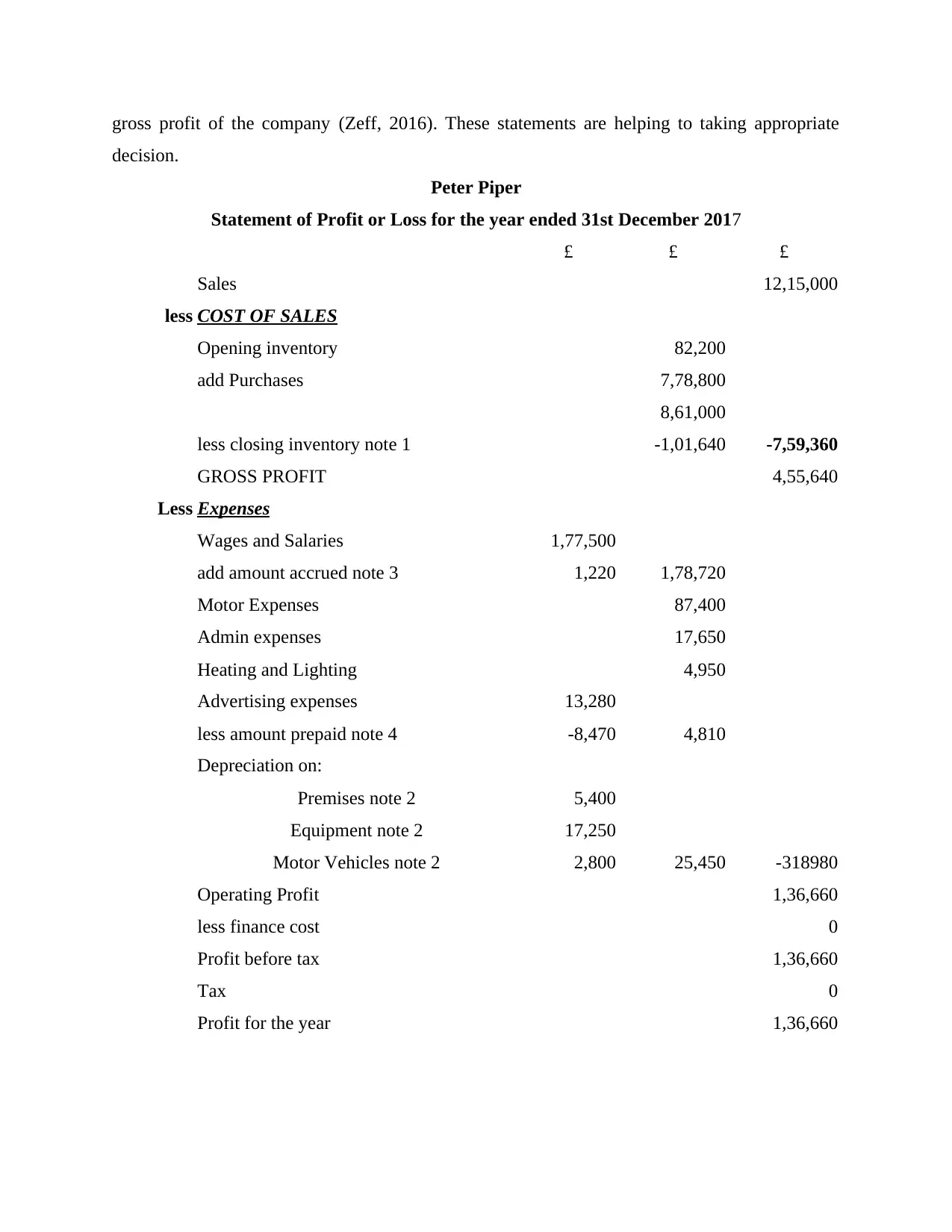

gross profit of the company (Zeff, 2016). These statements are helping to taking appropriate

decision.

Peter Piper

Statement of Profit or Loss for the year ended 31st December 2017

£ £ £

Sales 12,15,000

less COST OF SALES

Opening inventory 82,200

add Purchases 7,78,800

8,61,000

less closing inventory note 1 -1,01,640 -7,59,360

GROSS PROFIT 4,55,640

Less Expenses

Wages and Salaries 1,77,500

add amount accrued note 3 1,220 1,78,720

Motor Expenses 87,400

Admin expenses 17,650

Heating and Lighting 4,950

Advertising expenses 13,280

less amount prepaid note 4 -8,470 4,810

Depreciation on:

Premises note 2 5,400

Equipment note 2 17,250

Motor Vehicles note 2 2,800 25,450 -318980

Operating Profit 1,36,660

less finance cost 0

Profit before tax 1,36,660

Tax 0

Profit for the year 1,36,660

decision.

Peter Piper

Statement of Profit or Loss for the year ended 31st December 2017

£ £ £

Sales 12,15,000

less COST OF SALES

Opening inventory 82,200

add Purchases 7,78,800

8,61,000

less closing inventory note 1 -1,01,640 -7,59,360

GROSS PROFIT 4,55,640

Less Expenses

Wages and Salaries 1,77,500

add amount accrued note 3 1,220 1,78,720

Motor Expenses 87,400

Admin expenses 17,650

Heating and Lighting 4,950

Advertising expenses 13,280

less amount prepaid note 4 -8,470 4,810

Depreciation on:

Premises note 2 5,400

Equipment note 2 17,250

Motor Vehicles note 2 2,800 25,450 -318980

Operating Profit 1,36,660

less finance cost 0

Profit before tax 1,36,660

Tax 0

Profit for the year 1,36,660

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.