Financial Accounting Report: Principles, Standards, and Statements

VerifiedAdded on 2020/10/05

|44

|4861

|462

Report

AI Summary

This report provides a comprehensive overview of financial accounting principles and practices. It begins with an introduction to financial accounting, its purpose, and the regulations governing it, including IFRS and GAAP. The report then details ten key accounting principles, such as the business entity concept, going concern, and matching concept. It further explores the conventions of consistency, materiality, and full disclosure. The report includes practical applications through journal entries, ledger accounts, and trial balances, using examples from various clients. It presents profit and loss statements and statements of financial position. Additionally, the report explains the concepts of consistency and prudence in accounting, the purpose and methods of depreciation, bank reconciliation statements, and control and suspense accounts. The document also explores the difference between clearing and suspense accounts, providing a complete guide to understanding financial accounting concepts and their practical applications.

FINANCIAL ACCOUNTING

PRINCIPLES

PRINCIPLES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1.1. The financial accounting and its purpose.............................................................................1

1.2. Regulations on Financial Accounting..................................................................................2

1.3. The 10 accounting rules and principles................................................................................3

1.4. The convention and concepts of consistency and material , disclosure...............................4

Client 1.............................................................................................................................................5

1. Presenting journal entries of specified transactions................................................................5

2. Presenting ledger accounts with context of double entry........................................................6

3. Presenting level of accuracy with context of trial balance....................................................22

Client 2...........................................................................................................................................23

A. Presenting profit and loss statement of Sierra Laurent of July 2018...................................23

B. Presenting statement of financial position of Sierra Laurent for July 2018.........................24

Client 3...........................................................................................................................................25

A. Presenting income statement of July for LMS Limited.......................................................25

B. Presenting statement of financial position of LMS Limited for July 2018..........................26

C. The consistency and Prudence concepts of accounting principle.......................................26

D. The purpose of depreciation and method of calculating depreciation.................................27

Client 4...........................................................................................................................................29

A. The need for preparing Bank-reconciliation-statement and its purpose of preparing on

monthly basis............................................................................................................................29

B. The reason for difference in record of bank book................................................................29

C. Presenting cash book for Kendal with its Bank reconciliation statement............................31

Client 5...........................................................................................................................................33

A. Presenting Sales and purchase ledger control account.........................................................33

B. The importance of Control account......................................................................................34

Client 6...........................................................................................................................................35

A. The importance of suspense account and features of suspense account..............................35

Presenting trial balance.............................................................................................................36

B. The difference between clearing account and suspense account..........................................37

CONCLUSION..............................................................................................................................38

REFERENCES..............................................................................................................................39

INTRODUCTION...........................................................................................................................1

1.1. The financial accounting and its purpose.............................................................................1

1.2. Regulations on Financial Accounting..................................................................................2

1.3. The 10 accounting rules and principles................................................................................3

1.4. The convention and concepts of consistency and material , disclosure...............................4

Client 1.............................................................................................................................................5

1. Presenting journal entries of specified transactions................................................................5

2. Presenting ledger accounts with context of double entry........................................................6

3. Presenting level of accuracy with context of trial balance....................................................22

Client 2...........................................................................................................................................23

A. Presenting profit and loss statement of Sierra Laurent of July 2018...................................23

B. Presenting statement of financial position of Sierra Laurent for July 2018.........................24

Client 3...........................................................................................................................................25

A. Presenting income statement of July for LMS Limited.......................................................25

B. Presenting statement of financial position of LMS Limited for July 2018..........................26

C. The consistency and Prudence concepts of accounting principle.......................................26

D. The purpose of depreciation and method of calculating depreciation.................................27

Client 4...........................................................................................................................................29

A. The need for preparing Bank-reconciliation-statement and its purpose of preparing on

monthly basis............................................................................................................................29

B. The reason for difference in record of bank book................................................................29

C. Presenting cash book for Kendal with its Bank reconciliation statement............................31

Client 5...........................................................................................................................................33

A. Presenting Sales and purchase ledger control account.........................................................33

B. The importance of Control account......................................................................................34

Client 6...........................................................................................................................................35

A. The importance of suspense account and features of suspense account..............................35

Presenting trial balance.............................................................................................................36

B. The difference between clearing account and suspense account..........................................37

CONCLUSION..............................................................................................................................38

REFERENCES..............................................................................................................................39

INTRODUCTION

Financial accounting is referred as a very important concept for every industry along with

its organization and industry. The accounting and financial principles are the key elements of

business life. The fundamental principles of accounting and the ways in which accounting is

regulated is an important topic for the business entity.

The present report will show the importance of financial accounting for preparing

financial statement and its purpose. The report dictates about the regulations on financial

reporting and will show accounting standards by International Financial Recording system and

General Accepted Accounting principles.

Present report highlights the main concepts and principles of accountancy. In this report,

various financial statements have been discussed which helps in decision making for every

investor and manager. In the same series, it had justified option of depreciation with its

implication of both methods. It had also discussed about control account with its sales and

purchase ledger control account. There is a presence of comparison and similarity of suspense

and clearing account with its appropriate implication.

1.1financial accounting and its purpose.

Financial accounting is a branch of accounting which records each and every financial

transaction of a company. Financial recording is a standardized process in which transaction are

recorded, summarized and presented in a financial report or financial statements which records

the company's overall financial position and performance in a specific accounting principle.

Financial accounting focuses on providing external users with useful information. It transfers

financial transaction and activity of a company in a form of information to the external parties

like investors, shareholders, creditors etc.

The purpose of financial accounting:

Financial accounting is done to keep systematic record of financial transaction. So it

would help in getting correct information at the time of preparing income statements or

financial statements (May, 2013).

Financial accounting assists in finding the net profit earned and loss suffered on account

of carrying business, by keeping proper record of financial activity of a particular time.

1

Financial accounting is referred as a very important concept for every industry along with

its organization and industry. The accounting and financial principles are the key elements of

business life. The fundamental principles of accounting and the ways in which accounting is

regulated is an important topic for the business entity.

The present report will show the importance of financial accounting for preparing

financial statement and its purpose. The report dictates about the regulations on financial

reporting and will show accounting standards by International Financial Recording system and

General Accepted Accounting principles.

Present report highlights the main concepts and principles of accountancy. In this report,

various financial statements have been discussed which helps in decision making for every

investor and manager. In the same series, it had justified option of depreciation with its

implication of both methods. It had also discussed about control account with its sales and

purchase ledger control account. There is a presence of comparison and similarity of suspense

and clearing account with its appropriate implication.

1.1financial accounting and its purpose.

Financial accounting is a branch of accounting which records each and every financial

transaction of a company. Financial recording is a standardized process in which transaction are

recorded, summarized and presented in a financial report or financial statements which records

the company's overall financial position and performance in a specific accounting principle.

Financial accounting focuses on providing external users with useful information. It transfers

financial transaction and activity of a company in a form of information to the external parties

like investors, shareholders, creditors etc.

The purpose of financial accounting:

Financial accounting is done to keep systematic record of financial transaction. So it

would help in getting correct information at the time of preparing income statements or

financial statements (May, 2013).

Financial accounting assists in finding the net profit earned and loss suffered on account

of carrying business, by keeping proper record of financial activity of a particular time.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The main purpose of financial accounting is to help in ascertaining financial position of a

company during a particular period of time. The balance sheet of a company shows total

assets and total liability of a company on a particular date. It assists the external users to

know the financial position of company.

Financial accounting helps in making an overall decision to management of the company

by providing systematic record of financial transactions of a company.

1.2 Regulations on Financial Accounting.

Accounting standards are authoritative standards for reporting financial transaction.

Accounting standards specify how transactions and other activities are presented and displayed

in financial statements. The objectives of accounting standards or regulations is to provide

financial information to the investors, lenders, creditors, shareholders so that they can make

decisions regarding their investments in company.

Different boards for accounting regulations are:

IFRS: International Financial Reporting Standards is a board of accounting method that

has been practised in many countries across the world. IFRS is globally accepted standard for

accounting and is used in more than 110 countries. It helps the company which does business

internationally and sets standards on preparing the financial statements of their company. IFRS

covers wide range of accounting activities, which includes regulations on the statements of

financial statements (Giordano-Spring, Maurice and Cho, 2018). In addition to financial

statements, the company has to give summary of its accounting policies.

GAAP: General Accounting Accepted Practice is a commonly followed practice in UK

and EU for the financial reporting. GAAP is exclusively used within the domestic boundaries

and has a different set of rules for accounting than most of the world. Under GAAP regulations,

all the transaction has to be recorded under a specific set of rules. Its main aim is to make the

financial statement more transparent and consistent. The new UK GAAP aims to make the

financial reporting cheaper and easier. GAAP provides characteristics like relevance, reliability,

comparability and understand ability.

1.3. The 10 accounting rules and principles

GAAP has founded the basic of accounting principles and guidelines.

2

company during a particular period of time. The balance sheet of a company shows total

assets and total liability of a company on a particular date. It assists the external users to

know the financial position of company.

Financial accounting helps in making an overall decision to management of the company

by providing systematic record of financial transactions of a company.

1.2 Regulations on Financial Accounting.

Accounting standards are authoritative standards for reporting financial transaction.

Accounting standards specify how transactions and other activities are presented and displayed

in financial statements. The objectives of accounting standards or regulations is to provide

financial information to the investors, lenders, creditors, shareholders so that they can make

decisions regarding their investments in company.

Different boards for accounting regulations are:

IFRS: International Financial Reporting Standards is a board of accounting method that

has been practised in many countries across the world. IFRS is globally accepted standard for

accounting and is used in more than 110 countries. It helps the company which does business

internationally and sets standards on preparing the financial statements of their company. IFRS

covers wide range of accounting activities, which includes regulations on the statements of

financial statements (Giordano-Spring, Maurice and Cho, 2018). In addition to financial

statements, the company has to give summary of its accounting policies.

GAAP: General Accounting Accepted Practice is a commonly followed practice in UK

and EU for the financial reporting. GAAP is exclusively used within the domestic boundaries

and has a different set of rules for accounting than most of the world. Under GAAP regulations,

all the transaction has to be recorded under a specific set of rules. Its main aim is to make the

financial statement more transparent and consistent. The new UK GAAP aims to make the

financial reporting cheaper and easier. GAAP provides characteristics like relevance, reliability,

comparability and understand ability.

1.3. The 10 accounting rules and principles

GAAP has founded the basic of accounting principles and guidelines.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The following is the list of ten main accounting principles and guidelines:

Business as a single entity: a business will be treated as a different entity from its owner.

The law states that the business entity and business owner should be consider as separate from

each other. In legal terms, a business entity will exist even after the retirement or death of the

business owners.

Going concern principle: this principle states that the business entity will continue to

function indefinite time period. According to this principle the liability can be accounted in next

accounting period and assets value are recorded on this principle.

Monetary Unit: According to the monetary principle, only those transactions will be

recorded that can be measured in a specific form of money or currency. If company records the

financial transaction is USD then it cannot change its monetary unit.

Matching concept: this principle dictates that sales and revenue which are actually

realised should be included in the same accounting period. The transaction recorded should give

the actual profit.

Historical Cost: the value of the fixed assets should be recorded in financial statement

on their actual cost or at original value and not on the current market price.

Full Disclosure Principle: This principle states that company should disclose all

information related to the function of financial statements in the note under the statements

(Shroff, 2017).

Accounting period: The business entity has to complete its business accounting process

within a specific accounting period like quarterly, half yearly or annually.

Conservatism: This principle dictates while recording a transaction if two amounts for

similar transaction are there, and where the lower amount would be recorded in final statement.

Consistent: The accounting method once adopted should be used for different

accounting period. And it cannot be changed without any specific reasons (Zeff, 2016). The

newly adopted method should be disclosed in financial statement and must show better picture of

financial performance.

3

Business as a single entity: a business will be treated as a different entity from its owner.

The law states that the business entity and business owner should be consider as separate from

each other. In legal terms, a business entity will exist even after the retirement or death of the

business owners.

Going concern principle: this principle states that the business entity will continue to

function indefinite time period. According to this principle the liability can be accounted in next

accounting period and assets value are recorded on this principle.

Monetary Unit: According to the monetary principle, only those transactions will be

recorded that can be measured in a specific form of money or currency. If company records the

financial transaction is USD then it cannot change its monetary unit.

Matching concept: this principle dictates that sales and revenue which are actually

realised should be included in the same accounting period. The transaction recorded should give

the actual profit.

Historical Cost: the value of the fixed assets should be recorded in financial statement

on their actual cost or at original value and not on the current market price.

Full Disclosure Principle: This principle states that company should disclose all

information related to the function of financial statements in the note under the statements

(Shroff, 2017).

Accounting period: The business entity has to complete its business accounting process

within a specific accounting period like quarterly, half yearly or annually.

Conservatism: This principle dictates while recording a transaction if two amounts for

similar transaction are there, and where the lower amount would be recorded in final statement.

Consistent: The accounting method once adopted should be used for different

accounting period. And it cannot be changed without any specific reasons (Zeff, 2016). The

newly adopted method should be disclosed in financial statement and must show better picture of

financial performance.

3

Objectivity: According to this principle, every transaction amount in financial

statement should have some form of evidence.

1.4. The convention and concepts of consistency and material, disclosure.

Consistency concept: The concept dictates that accounting method once adopted should

not be changed and continuously followed after every financial year. This concept provides a

consistent basis for the external users to compare and understand financial statement. If a method

is adopted in first year and another method is adopted in next year, then it would be difficult for

the user of financial statement to analyse the statement with previous one and hence correct

position will not be reported to investors and shareholders (Schaltegger and Burritt, 2017). It

doesn't mean that you cannot change the accounting method ever, a company can change its

accounting method only and only if there is more than a specific reasonable grounds to change it.

But the reason for changing accounting method should be mentioned in the note

section of financial statements and method which are being adopted has to reflect the accurate

picture of financial position of company than the previous method.

Materiality Concept: this concepts dictates that company should disclose each and

every information in financial statement that could be useful to the end users. The transaction or

event happened in the accounting year cannot be avoided, even if company thinks it’s not much

important. The information can only be avoided if it has no or little impact on financial statement

of the year.

Full Disclosure Concept: This concept states that each financial detail like accounting

policies, method of calculation should be mentioned in the note section of financial statement.

The investors should have a full knowledge about the relevant information of the business

activity. This principle helps outside world to know the relevant and financial information of the

business entity (Carey, Knowles and Towers-Clark, 2017). This information could be anything

that could change the decisions of investors or shareholders about their investment in the

company. It emphasis the company to be transparent in their financial statements. It will be

added as footnotes with financial statements of the company.

4

statement should have some form of evidence.

1.4. The convention and concepts of consistency and material, disclosure.

Consistency concept: The concept dictates that accounting method once adopted should

not be changed and continuously followed after every financial year. This concept provides a

consistent basis for the external users to compare and understand financial statement. If a method

is adopted in first year and another method is adopted in next year, then it would be difficult for

the user of financial statement to analyse the statement with previous one and hence correct

position will not be reported to investors and shareholders (Schaltegger and Burritt, 2017). It

doesn't mean that you cannot change the accounting method ever, a company can change its

accounting method only and only if there is more than a specific reasonable grounds to change it.

But the reason for changing accounting method should be mentioned in the note

section of financial statements and method which are being adopted has to reflect the accurate

picture of financial position of company than the previous method.

Materiality Concept: this concepts dictates that company should disclose each and

every information in financial statement that could be useful to the end users. The transaction or

event happened in the accounting year cannot be avoided, even if company thinks it’s not much

important. The information can only be avoided if it has no or little impact on financial statement

of the year.

Full Disclosure Concept: This concept states that each financial detail like accounting

policies, method of calculation should be mentioned in the note section of financial statement.

The investors should have a full knowledge about the relevant information of the business

activity. This principle helps outside world to know the relevant and financial information of the

business entity (Carey, Knowles and Towers-Clark, 2017). This information could be anything

that could change the decisions of investors or shareholders about their investment in the

company. It emphasis the company to be transparent in their financial statements. It will be

added as footnotes with financial statements of the company.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Client 1

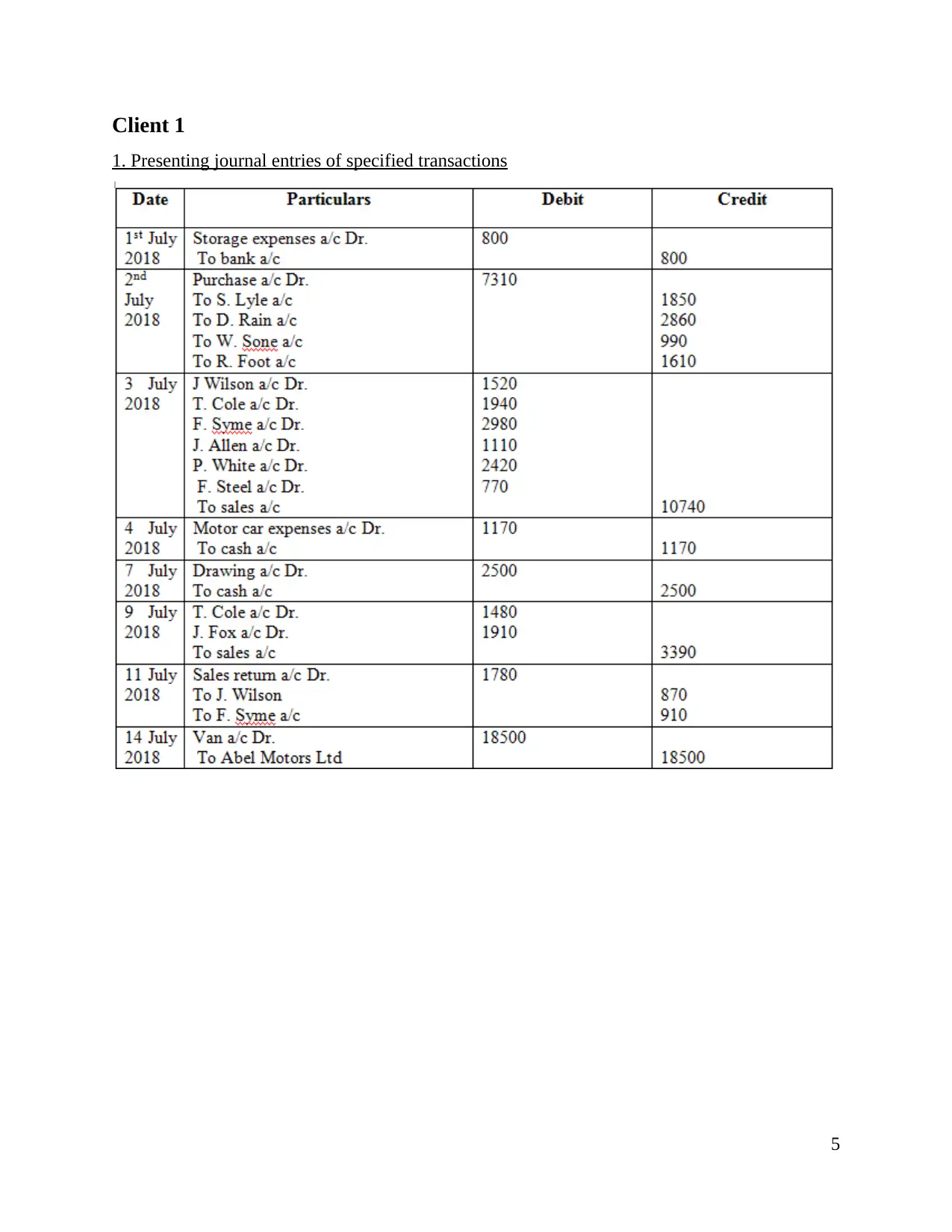

1. Presenting journal entries of specified transactions

5

1. Presenting journal entries of specified transactions

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

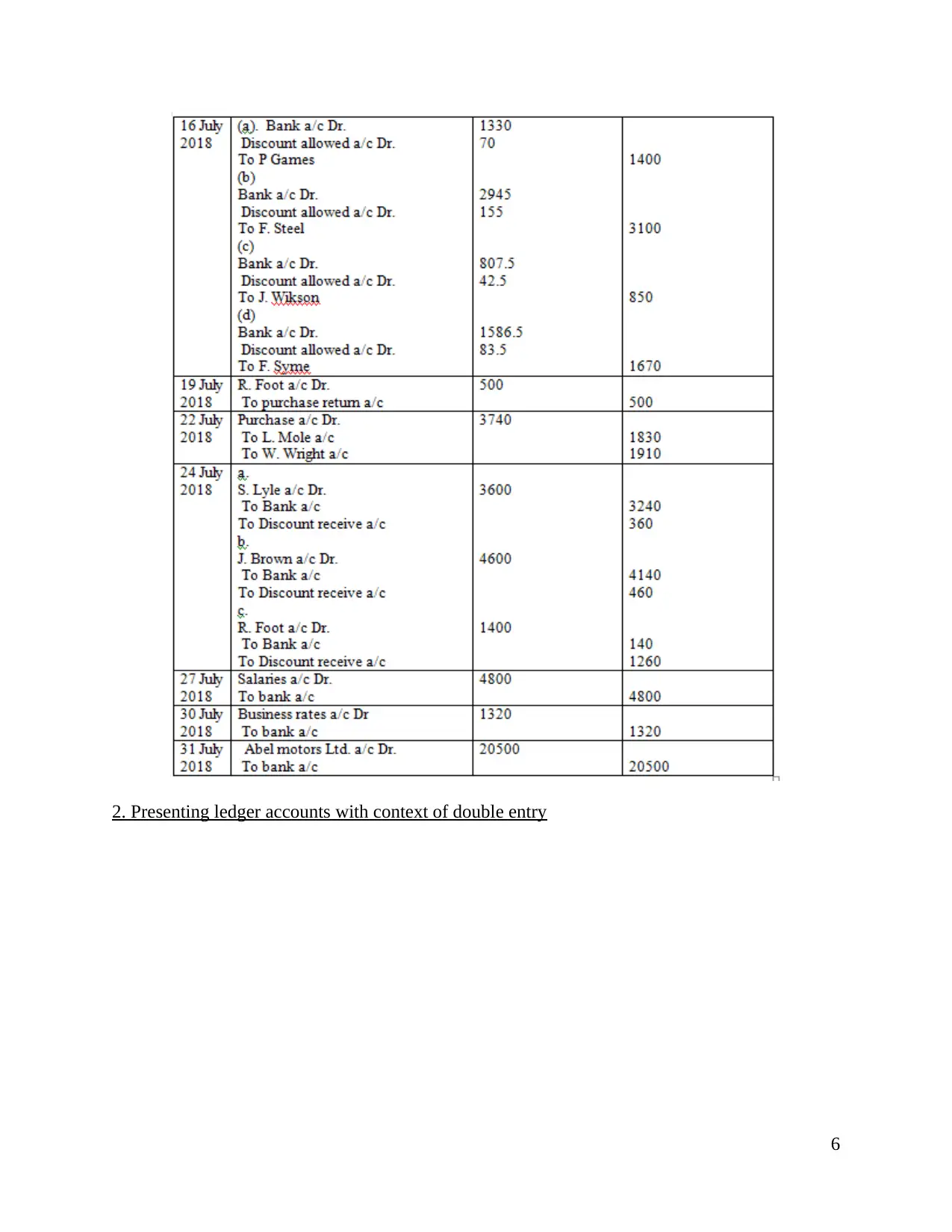

2. Presenting ledger accounts with context of double entry

6

6

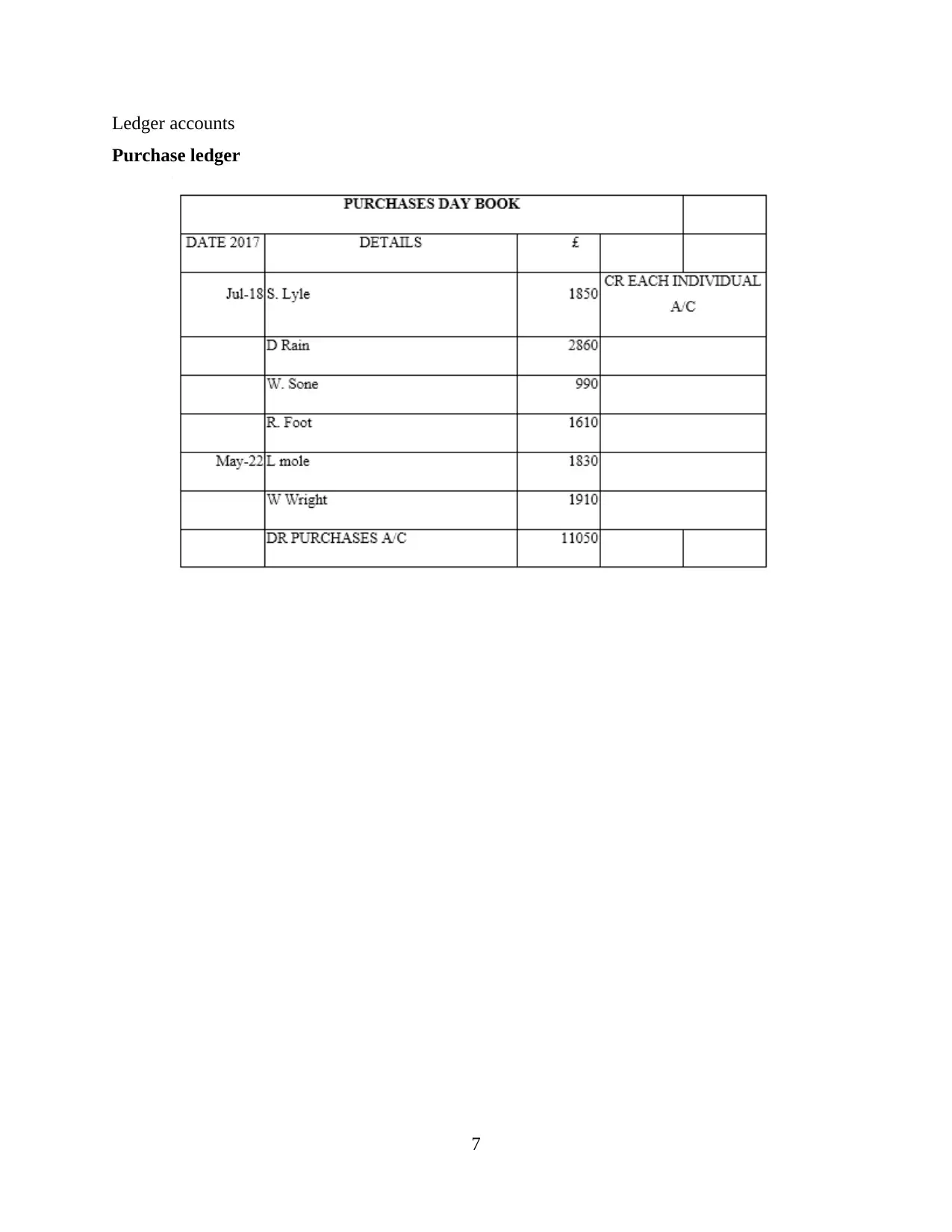

Ledger accounts

Purchase ledger

7

Purchase ledger

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

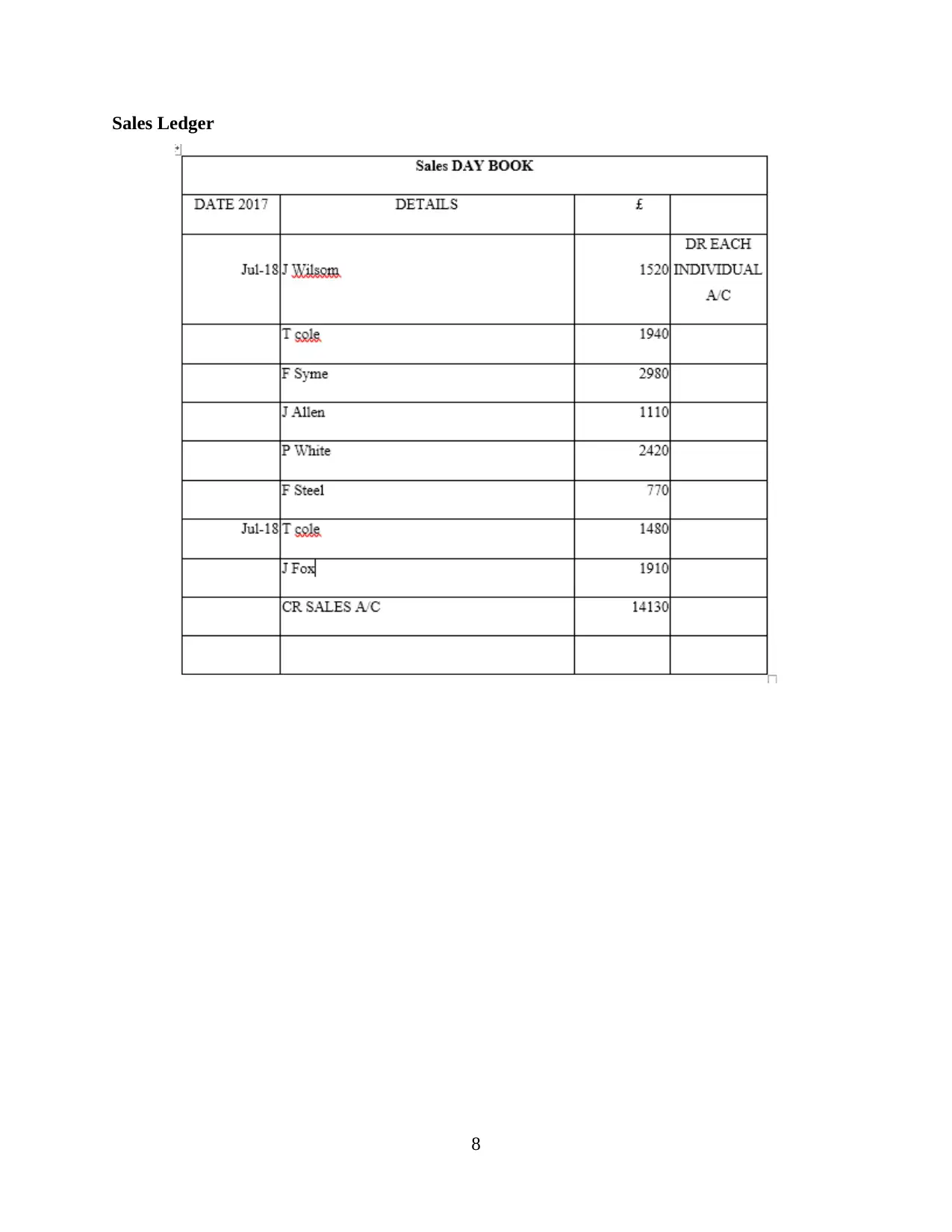

Sales Ledger

8

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

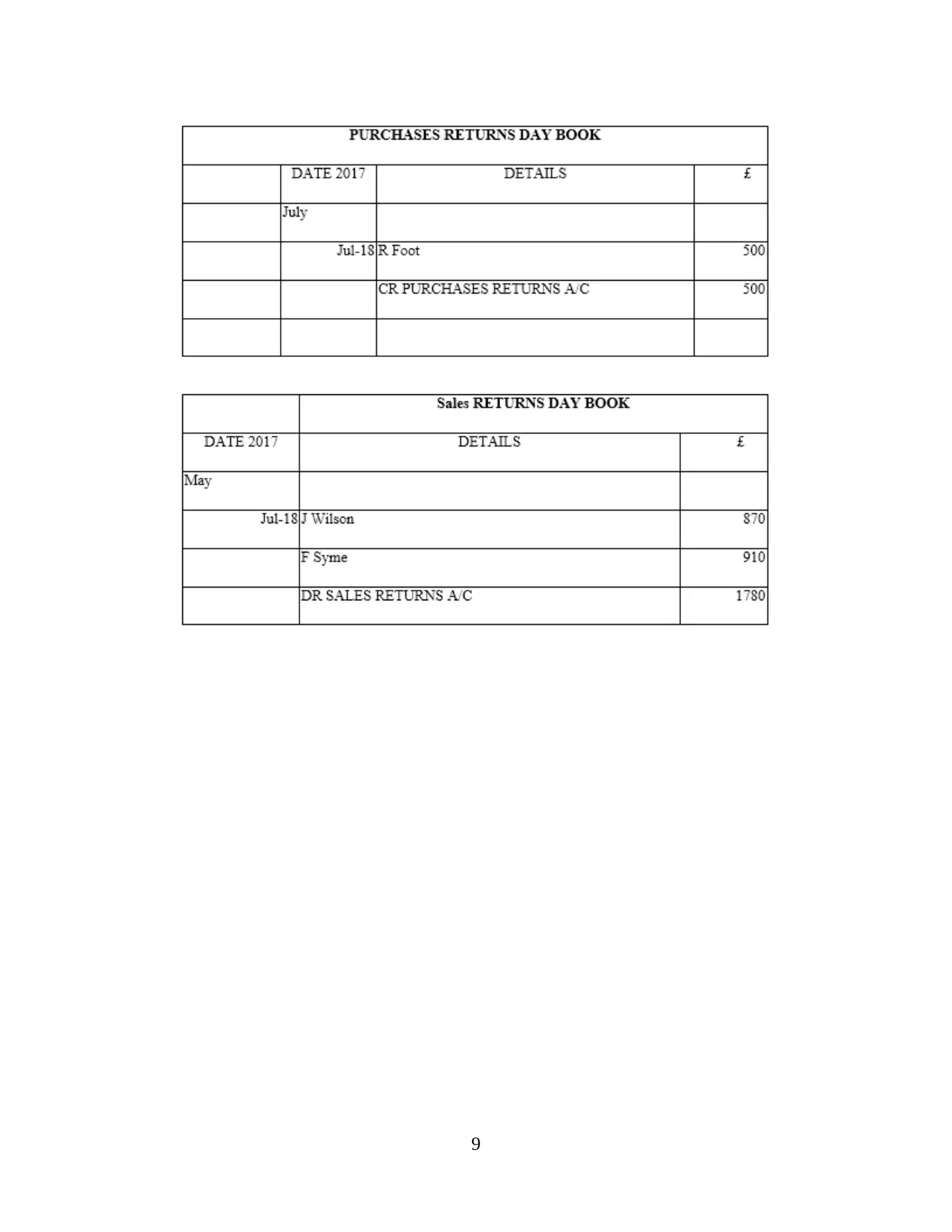

9

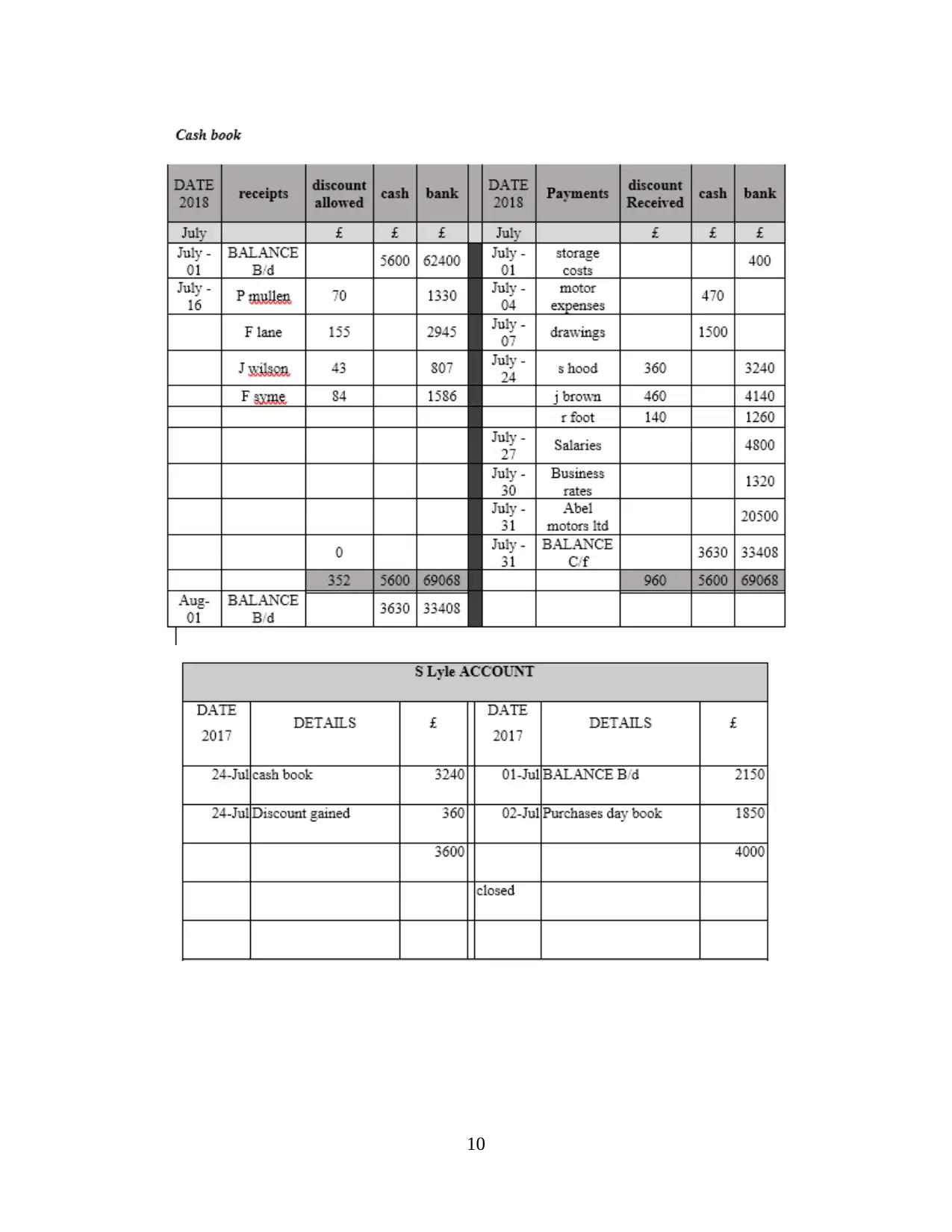

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 44

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.