Financial Accounting Report: Principles, Analysis and Reporting

VerifiedAdded on 2020/09/03

|36

|4351

|33

Report

AI Summary

This financial accounting report provides a comprehensive overview of financial accounting principles, concepts, and their practical application. It begins with an introduction to financial accounting, including its importance, relevant regulations (IASB, FASB, IFRS), and fundamental concepts like time and monetary assumptions, economic entity, cost principles, and going concern. The report then delves into practical examples, analyzing journal entries, preparing ledger accounts, and constructing trial balances for various clients. It includes the preparation of profit and loss statements, balance sheets, and bank reconciliation statements. The report also explores the concepts of consistency and prudence, the purpose and methods of depreciation, and the use of control and suspense accounts. Through these examples, the report demonstrates how accounting principles are applied in real-world scenarios, providing a solid foundation for understanding financial reporting and analysis. The report also includes the analysis of material and consistency conventions.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A. Reporting the principles and concepts as well as importance of financial accounting to the

line manager...........................................................................................................................1

1 Describing financial accounting..........................................................................................1

2 financial accounting and the relevant regulations...............................................................2

3 Defining the regulations and principle concepts of accounting..........................................3

4 Analysing the concepts relevant to material and consistency conventions.........................4

CLIENT 1........................................................................................................................................5

A Measuring the journal entries.............................................................................................5

B Ledger accounts for the journal entries...............................................................................8

C Following the journal and ledger the trail balance of Alexandra is prepared as..............16

M1 ........................................................................................................................................16

D1.........................................................................................................................................16

CLIENT 2......................................................................................................................................17

A Measuring elements for presenting profit and loss statement..........................................17

B presenting the balance sheet for Peter Pipe......................................................................18

CLIENT 3......................................................................................................................................19

A Presenting the income statement......................................................................................19

B Presenting the balance sheet.............................................................................................20

C Determining the concepts of consistency and prudence in accounting............................24

D Analysing the purpose of calculating depreciation as well as evaluating the methods of

depreciation and their importance........................................................................................25

M2.........................................................................................................................................25

D2.........................................................................................................................................25

CLIENT 4......................................................................................................................................26

A Analysing the purpose of presenting the bank statement and determining the reason for

preparing it for the monthly basis.........................................................................................26

B Determining the areas which varies the recording of bank statements.............................26

C Presenting the bank reconciliation statement....................................................................26

INTRODUCTION...........................................................................................................................1

A. Reporting the principles and concepts as well as importance of financial accounting to the

line manager...........................................................................................................................1

1 Describing financial accounting..........................................................................................1

2 financial accounting and the relevant regulations...............................................................2

3 Defining the regulations and principle concepts of accounting..........................................3

4 Analysing the concepts relevant to material and consistency conventions.........................4

CLIENT 1........................................................................................................................................5

A Measuring the journal entries.............................................................................................5

B Ledger accounts for the journal entries...............................................................................8

C Following the journal and ledger the trail balance of Alexandra is prepared as..............16

M1 ........................................................................................................................................16

D1.........................................................................................................................................16

CLIENT 2......................................................................................................................................17

A Measuring elements for presenting profit and loss statement..........................................17

B presenting the balance sheet for Peter Pipe......................................................................18

CLIENT 3......................................................................................................................................19

A Presenting the income statement......................................................................................19

B Presenting the balance sheet.............................................................................................20

C Determining the concepts of consistency and prudence in accounting............................24

D Analysing the purpose of calculating depreciation as well as evaluating the methods of

depreciation and their importance........................................................................................25

M2.........................................................................................................................................25

D2.........................................................................................................................................25

CLIENT 4......................................................................................................................................26

A Analysing the purpose of presenting the bank statement and determining the reason for

preparing it for the monthly basis.........................................................................................26

B Determining the areas which varies the recording of bank statements.............................26

C Presenting the bank reconciliation statement....................................................................26

M3.........................................................................................................................................27

D3.........................................................................................................................................28

CLIENT 5......................................................................................................................................28

A Presenting various ledger control account........................................................................28

b Determining the requirement of drawing the control account...........................................29

CLIENT 6......................................................................................................................................29

A Describing the suspense account as well as its main features..........................................29

B Measuring the trail balance of the provided figures.........................................................30

C presenting the journal entries for the trail balance adjustments........................................30

D Analysing the differences between clearing and suspense accounts................................31

M4.........................................................................................................................................31

D4.........................................................................................................................................31

CONCLUSION..............................................................................................................................31

REFERENCES..............................................................................................................................33

BIBLIOGRAPHY..........................................................................................................................34

D3.........................................................................................................................................28

CLIENT 5......................................................................................................................................28

A Presenting various ledger control account........................................................................28

b Determining the requirement of drawing the control account...........................................29

CLIENT 6......................................................................................................................................29

A Describing the suspense account as well as its main features..........................................29

B Measuring the trail balance of the provided figures.........................................................30

C presenting the journal entries for the trail balance adjustments........................................30

D Analysing the differences between clearing and suspense accounts................................31

M4.........................................................................................................................................31

D4.........................................................................................................................................31

CONCLUSION..............................................................................................................................31

REFERENCES..............................................................................................................................33

BIBLIOGRAPHY..........................................................................................................................34

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is consists of preparing and presenting the all the transactions which

are incurred in the organisation during the assessment period. Thus, the presentation of the such

transaction will be in the various accounts or statements which will help the business in making

the adequate growth as well as professionals will become able to plan for expansion in industrial

operations, changes in policies and procedures and plans budgets or costs for managing

profitability of firm. In the present assessment there has been determination of various

accounting principles, concepts, rule and regulations as well as there will be preparation of

various accounts, statement and reports that will help the clients to fetch the adequate

informations about the transactions incurred in such period. The report will also shed some lights

over the uses of various accounting techniques and tools to analyse the better outcomes and

valuation of the various elements or items stated in the statements.

A. Reporting the principles and concepts as well as importance of financial accounting to the line

manager

To: Line manager

From: Junior Accountant

Subject: Importance of financial accounting and its implications

1 Describing financial accounting

In consideration with recording the transactions in the books, preparation of various

accounts or statements, analysing, measuring and then evaluating the profitable outcomes are

known as the financial accounting. Hence, there will be use of various accounts for different

units in the firm which in turn helpful for making appropriate record of all the inflows and

outflows of the cash and articles (Zeff, 2016). However, at the end of the period all the accounts

were being summarized and audited by the accounting professionals in the business into the 4

major financial statements. Thus, the disclosure of such data set will be beneficial for internal

and external stakeholders in terms of making the investment decisions. There has been

preparation of the various financial statements such as balance sheet, income statements, cash

flow statements and the changes in the owner's equity which are listed below in the chart as:

1

Financial accounting is consists of preparing and presenting the all the transactions which

are incurred in the organisation during the assessment period. Thus, the presentation of the such

transaction will be in the various accounts or statements which will help the business in making

the adequate growth as well as professionals will become able to plan for expansion in industrial

operations, changes in policies and procedures and plans budgets or costs for managing

profitability of firm. In the present assessment there has been determination of various

accounting principles, concepts, rule and regulations as well as there will be preparation of

various accounts, statement and reports that will help the clients to fetch the adequate

informations about the transactions incurred in such period. The report will also shed some lights

over the uses of various accounting techniques and tools to analyse the better outcomes and

valuation of the various elements or items stated in the statements.

A. Reporting the principles and concepts as well as importance of financial accounting to the line

manager

To: Line manager

From: Junior Accountant

Subject: Importance of financial accounting and its implications

1 Describing financial accounting

In consideration with recording the transactions in the books, preparation of various

accounts or statements, analysing, measuring and then evaluating the profitable outcomes are

known as the financial accounting. Hence, there will be use of various accounts for different

units in the firm which in turn helpful for making appropriate record of all the inflows and

outflows of the cash and articles (Zeff, 2016). However, at the end of the period all the accounts

were being summarized and audited by the accounting professionals in the business into the 4

major financial statements. Thus, the disclosure of such data set will be beneficial for internal

and external stakeholders in terms of making the investment decisions. There has been

preparation of the various financial statements such as balance sheet, income statements, cash

flow statements and the changes in the owner's equity which are listed below in the chart as:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Illustration 1: financial statements

source: (Marshall, 2016)

2 financial accounting and the relevant regulations

In terms of preparing various financial of the business there are need to follow various

accounting principles which helps in preparing such statement with the help of such

authenticated framework (Deegan, 2016). Hence, there has been various institutions in the

accounting environment and they are facilitating the guidance, formate and procedure under

which all the financial accounts of business are being prepared. These principles are helpful for

every business in terms of attracting the large numbers of investors which will be out of the

national boundaries. Therefore, such institutions and the regulations facilitated by them can be

understand as follows:

IASB: This accounting standard presents the regulations of principles under which all

the accounting transactional process were made. Hence, the main motive of such institution is

that all the business or corporations which are facilitating the trade practices as well as making

the operational efforts there is need to make disclosure of financial of the business which in turn

beneficial for the firm and it stakeholder to fetch informations regarding profitability, liquidity

and the overall sale and purchase were made during the period (International Accounting

Standards Board (IASB), 2016). Therefore, the main motive of such principles and regulations

are to help the society with the adequate informations and have the faire trade practices.

FASB: in terms with this standard which in turn facilitate the framework and guidance

to disclose the various financial statements of the business. The main motive of such accounting

board is to improve the implication of GAAP principles in the daily accounting tasks of the

business operations. Hence, such techniques are helpful for business for generating the adequate

2

source: (Marshall, 2016)

2 financial accounting and the relevant regulations

In terms of preparing various financial of the business there are need to follow various

accounting principles which helps in preparing such statement with the help of such

authenticated framework (Deegan, 2016). Hence, there has been various institutions in the

accounting environment and they are facilitating the guidance, formate and procedure under

which all the financial accounts of business are being prepared. These principles are helpful for

every business in terms of attracting the large numbers of investors which will be out of the

national boundaries. Therefore, such institutions and the regulations facilitated by them can be

understand as follows:

IASB: This accounting standard presents the regulations of principles under which all

the accounting transactional process were made. Hence, the main motive of such institution is

that all the business or corporations which are facilitating the trade practices as well as making

the operational efforts there is need to make disclosure of financial of the business which in turn

beneficial for the firm and it stakeholder to fetch informations regarding profitability, liquidity

and the overall sale and purchase were made during the period (International Accounting

Standards Board (IASB), 2016). Therefore, the main motive of such principles and regulations

are to help the society with the adequate informations and have the faire trade practices.

FASB: in terms with this standard which in turn facilitate the framework and guidance

to disclose the various financial statements of the business. The main motive of such accounting

board is to improve the implication of GAAP principles in the daily accounting tasks of the

business operations. Hence, such techniques are helpful for business for generating the adequate

2

ideas and make the fruitful plans (Gordon and et.al., 2017).

IFRS: This institution is present in the market as to provide legally approved frame

work and process of presenting the disclosure of the financial statement. Hence, it has the

universally accepted formate for income statement, cash flows, balance sheet and the change in

equity. Thus, it considers that all the business must follow the principles and regulations which

are need to be mentioned while presenting the data set in front of the external users such as

investors, shareholders, consumers, government, bank and various financial institutions

(Thornton, 2016). Therefore, it also helps in improving the internal control of organisation such

as making the adequate changes in industrial operations and prepare policies procedure to

reduce the costs of such daily operations.

3 Defining the regulations and principle concepts of accounting

The motive behind presenting the principles and concepts of the management

accounting is that it brings the adequate, specific and relevant data set which are come through

the authenticated sources such as purchase of material, sales made during the period as well as

profit generated in the period (Marshall, 2016). Hence, such data set will be beneficial for

organisation in recording all the informations in authorised manner and present the fruitful

disclosure. Therefore, there are many principles which are need to be understand by the

professional in the various organisation in terms with analysing the financial statements of the

business such as:

Time assumption: All the disclosure of the accounts must be prepared in consideration

with the financial period such as many country presents the disclosure for the period started on

1 January to 31st December each year, many nations uses 1 April to 31st march of the next year.

Hence, the main motive of the time duration set by principle is that the annual report of the

organisation must be displayed so the actual analysis can be made over the profitability of the

organisation (Oulasvirta, 2016). Thus, the preparation of such data base can be annually,

quarterly and half yearly.

Monetary assumption: In terms with presenting data set on the international level there

will be use of Dollar as the most preferable currency (Evans, 2016). Thus, the value and rate of

such currency will not fluctuate frequently as it has the constant rates and facilitate stakeholders

3

IFRS: This institution is present in the market as to provide legally approved frame

work and process of presenting the disclosure of the financial statement. Hence, it has the

universally accepted formate for income statement, cash flows, balance sheet and the change in

equity. Thus, it considers that all the business must follow the principles and regulations which

are need to be mentioned while presenting the data set in front of the external users such as

investors, shareholders, consumers, government, bank and various financial institutions

(Thornton, 2016). Therefore, it also helps in improving the internal control of organisation such

as making the adequate changes in industrial operations and prepare policies procedure to

reduce the costs of such daily operations.

3 Defining the regulations and principle concepts of accounting

The motive behind presenting the principles and concepts of the management

accounting is that it brings the adequate, specific and relevant data set which are come through

the authenticated sources such as purchase of material, sales made during the period as well as

profit generated in the period (Marshall, 2016). Hence, such data set will be beneficial for

organisation in recording all the informations in authorised manner and present the fruitful

disclosure. Therefore, there are many principles which are need to be understand by the

professional in the various organisation in terms with analysing the financial statements of the

business such as:

Time assumption: All the disclosure of the accounts must be prepared in consideration

with the financial period such as many country presents the disclosure for the period started on

1 January to 31st December each year, many nations uses 1 April to 31st march of the next year.

Hence, the main motive of the time duration set by principle is that the annual report of the

organisation must be displayed so the actual analysis can be made over the profitability of the

organisation (Oulasvirta, 2016). Thus, the preparation of such data base can be annually,

quarterly and half yearly.

Monetary assumption: In terms with presenting data set on the international level there

will be use of Dollar as the most preferable currency (Evans, 2016). Thus, the value and rate of

such currency will not fluctuate frequently as it has the constant rates and facilitate stakeholders

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of organisation in terms with making the fruitful assumptions.

Economic assumption: In consideration with the legal structure of the organisation it is

being assumed that an entity is itself a person apart from its members or owners. Hence, the

business is itself making efforts and earning the turnover as well as performing in the day to day

industrial operations. Thus, it can be denoted as the septate individual.

Cost principles: the cost principle will be helpful for the manufacturing units in terms

with analysing the costs incurred while producing the units, article or delivering the services.

Hence, this concept lies over adequate analysis of the various terms and principles which in turn

affect the decision making as well as innovative ideas will be generated by managerial

professionals of organisation in respect with improving the operational capacity of business.

Going concern concept: It is assumed that the business which are come into existence

and have created an identity in the market, which will have the operational activities for the

long period. Thus, the going concern will help the managers to liquidate analysis which will be

fruitful for the future time of firm (Li, Sougiannis and Wang, 2017).

Revenue recognition: This concept follows the regulation that all the transactions which

are relevant With the industrial operations and present the revenue gathering of the firm such as

sale of products delivery of services are to e recognised and mentioned in the books of

accounts. Therefore, such transactions will be helpful for organisation in allocating the revenue

and reverse entity and managers will become able plan the expansion and investment in the new

projects.

Matching principles: All the entries and transactions held in the premises in the

assessment year must have the double entries of all the transactions. Thus, it is assumed that if

the income or expenses has the entries in the journal and ledger they must have the counter

entries with the relevant account of such particular transactions. Thus, on the other side the

matching of trail balance and balance sheet of organisation for the period is necessary and it

must reflect the fruitful disclosure of the accounts.

4 Analysing the concepts relevant to material and consistency conventions

Material: in accordance with such conventions it can be said that with the help of such

operational activities the business will be beneficial in making the adequate use of various

4

Economic assumption: In consideration with the legal structure of the organisation it is

being assumed that an entity is itself a person apart from its members or owners. Hence, the

business is itself making efforts and earning the turnover as well as performing in the day to day

industrial operations. Thus, it can be denoted as the septate individual.

Cost principles: the cost principle will be helpful for the manufacturing units in terms

with analysing the costs incurred while producing the units, article or delivering the services.

Hence, this concept lies over adequate analysis of the various terms and principles which in turn

affect the decision making as well as innovative ideas will be generated by managerial

professionals of organisation in respect with improving the operational capacity of business.

Going concern concept: It is assumed that the business which are come into existence

and have created an identity in the market, which will have the operational activities for the

long period. Thus, the going concern will help the managers to liquidate analysis which will be

fruitful for the future time of firm (Li, Sougiannis and Wang, 2017).

Revenue recognition: This concept follows the regulation that all the transactions which

are relevant With the industrial operations and present the revenue gathering of the firm such as

sale of products delivery of services are to e recognised and mentioned in the books of

accounts. Therefore, such transactions will be helpful for organisation in allocating the revenue

and reverse entity and managers will become able plan the expansion and investment in the new

projects.

Matching principles: All the entries and transactions held in the premises in the

assessment year must have the double entries of all the transactions. Thus, it is assumed that if

the income or expenses has the entries in the journal and ledger they must have the counter

entries with the relevant account of such particular transactions. Thus, on the other side the

matching of trail balance and balance sheet of organisation for the period is necessary and it

must reflect the fruitful disclosure of the accounts.

4 Analysing the concepts relevant to material and consistency conventions

Material: in accordance with such conventions it can be said that with the help of such

operational activities the business will be beneficial in making the adequate use of various

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting principles as well as make the adequate use of such resources. Hence, all the

element which are included in the transaction of such operational activities there is need to

manage the profitably of organisation.

Consistency: this concept follows the rule that all the business must be relevant with the

adequate utilisation of the resources and make the efforts in the operational activities on the

regular basis. Hence, such principles lies that the business be constantly making operational

activities and have the favourable earnings.

CLIENT 1

The presented case is belongs to the client Alexandra study which has facilitated the

various transactional details for the period of May 2017. Thus, there will be measurements which

are relevant to the journal, ledger and trail balances. Hence, all the transactions are to be

analysed and respected entries will be made in the following listed tables such as:

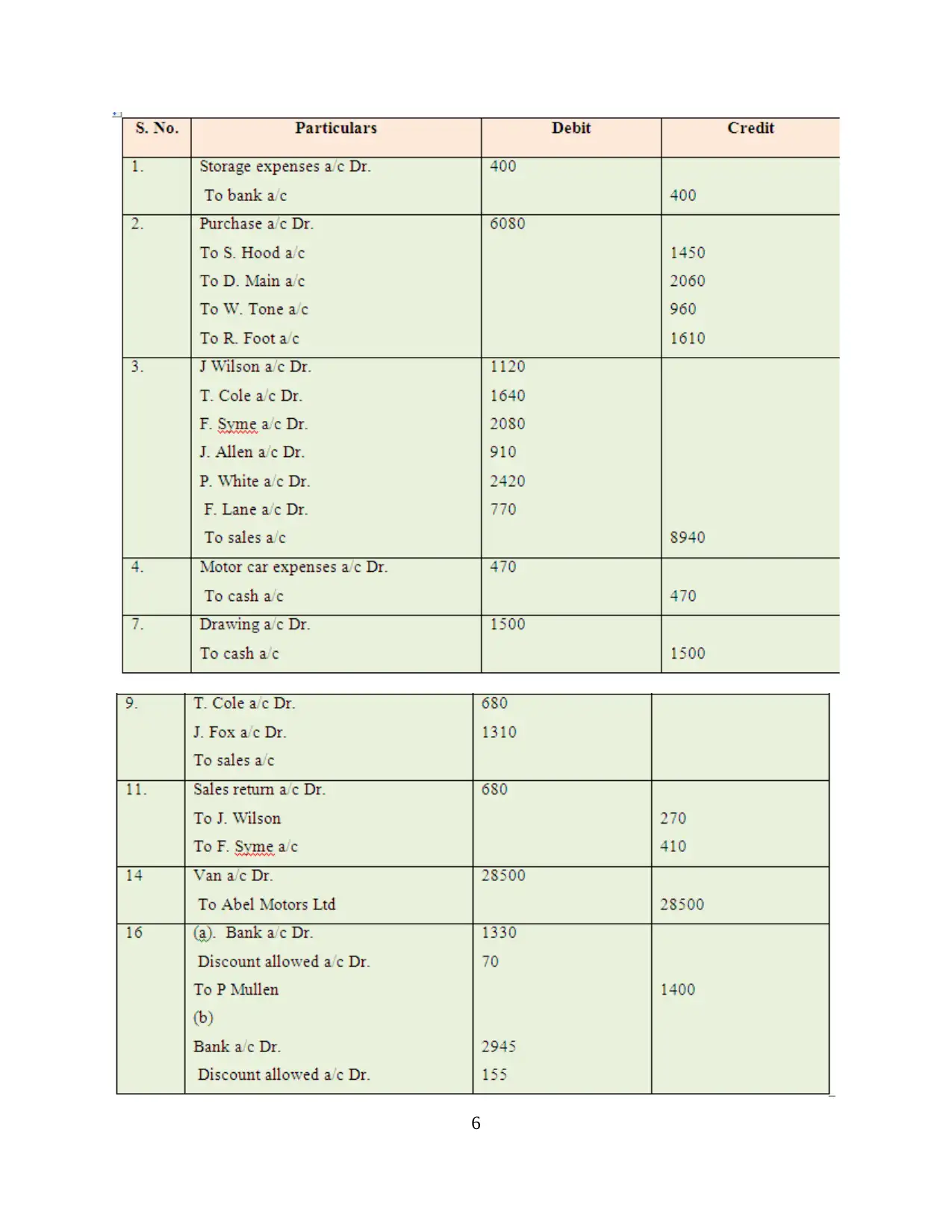

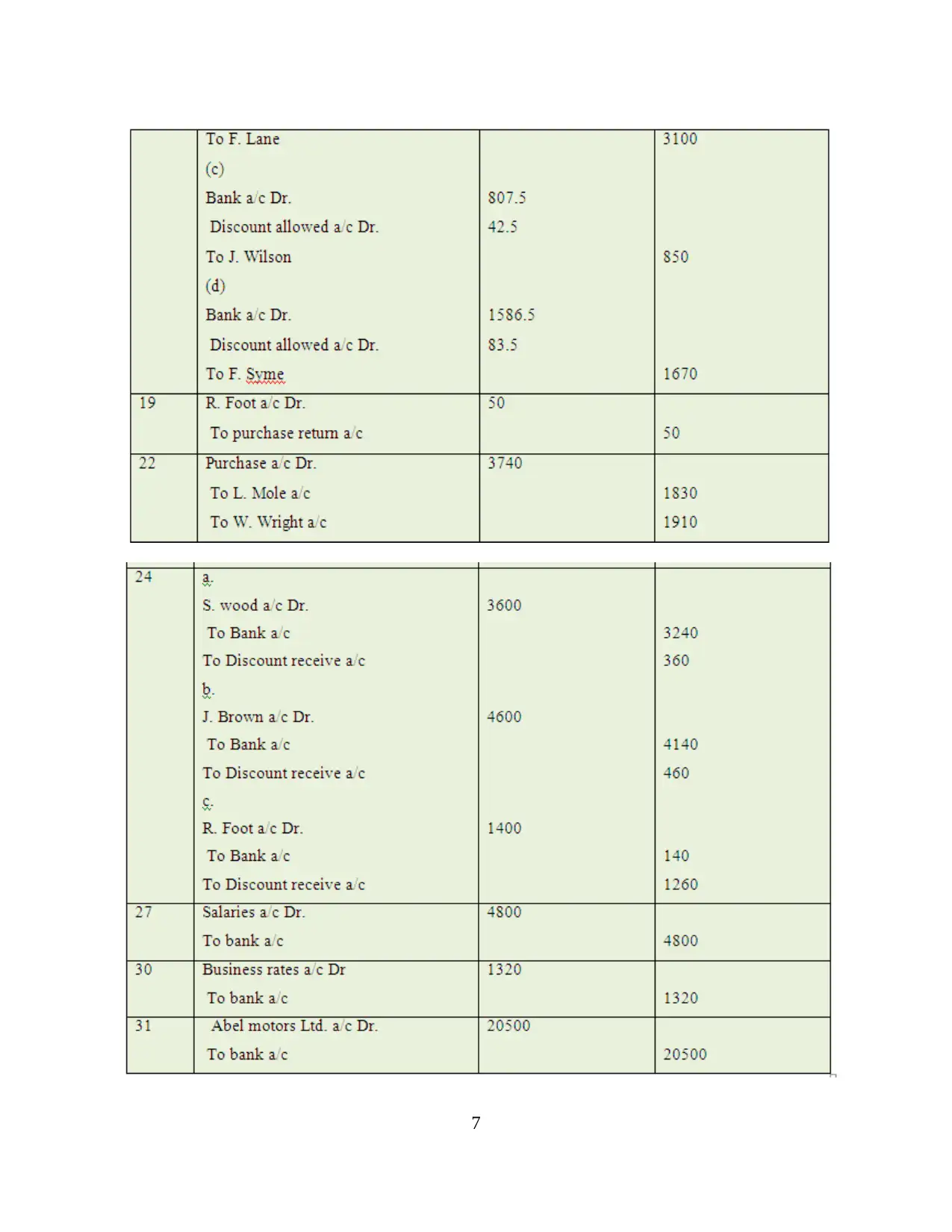

A Measuring the journal entries

There are some calculations are presents in the journal entries of the Alexandra study for

the period May 2017. Thus, such entries will be helpful for the further financial analysis of

business. Therefore, the following table will reflect the adequate measurements of such journal

entries are as follows:

5

element which are included in the transaction of such operational activities there is need to

manage the profitably of organisation.

Consistency: this concept follows the rule that all the business must be relevant with the

adequate utilisation of the resources and make the efforts in the operational activities on the

regular basis. Hence, such principles lies that the business be constantly making operational

activities and have the favourable earnings.

CLIENT 1

The presented case is belongs to the client Alexandra study which has facilitated the

various transactional details for the period of May 2017. Thus, there will be measurements which

are relevant to the journal, ledger and trail balances. Hence, all the transactions are to be

analysed and respected entries will be made in the following listed tables such as:

A Measuring the journal entries

There are some calculations are presents in the journal entries of the Alexandra study for

the period May 2017. Thus, such entries will be helpful for the further financial analysis of

business. Therefore, the following table will reflect the adequate measurements of such journal

entries are as follows:

5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

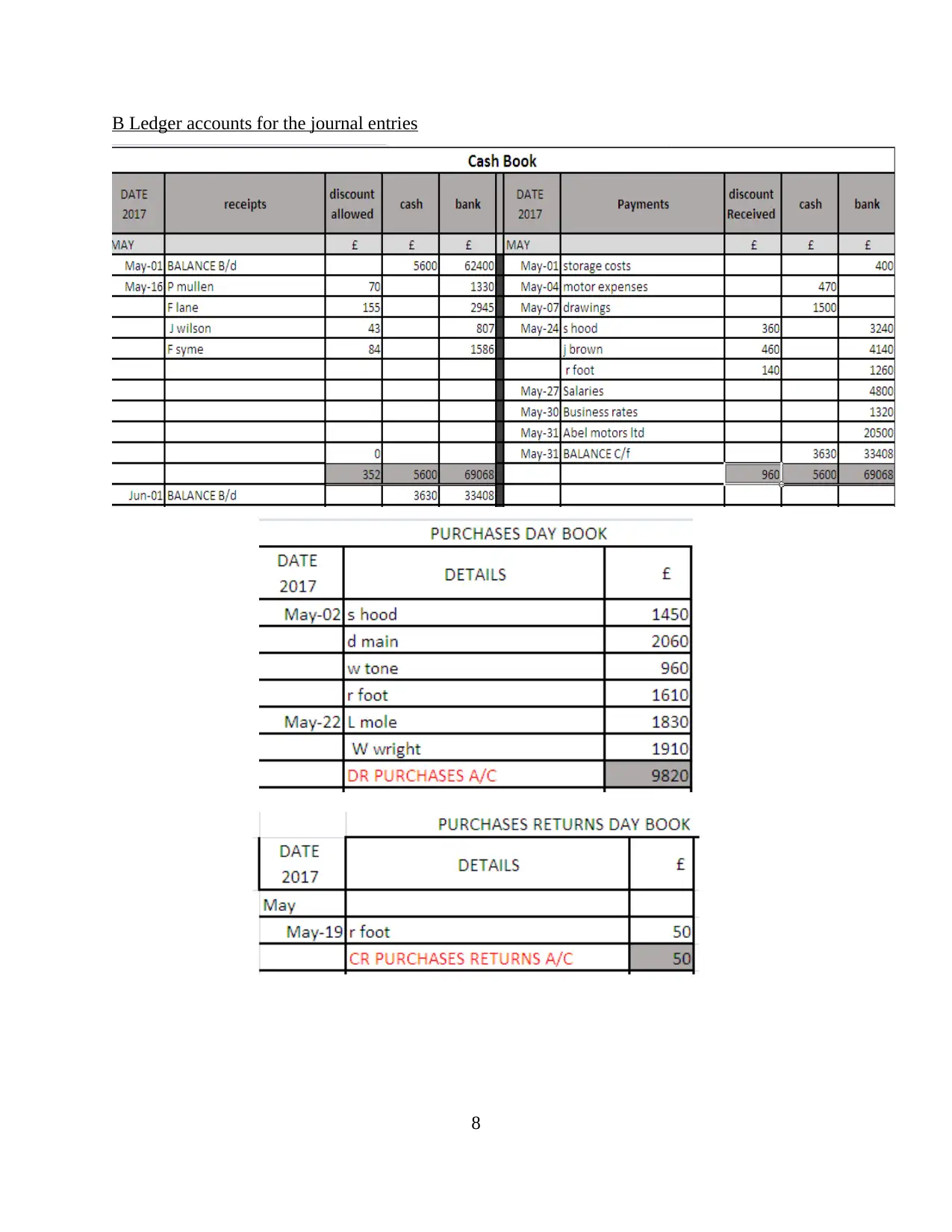

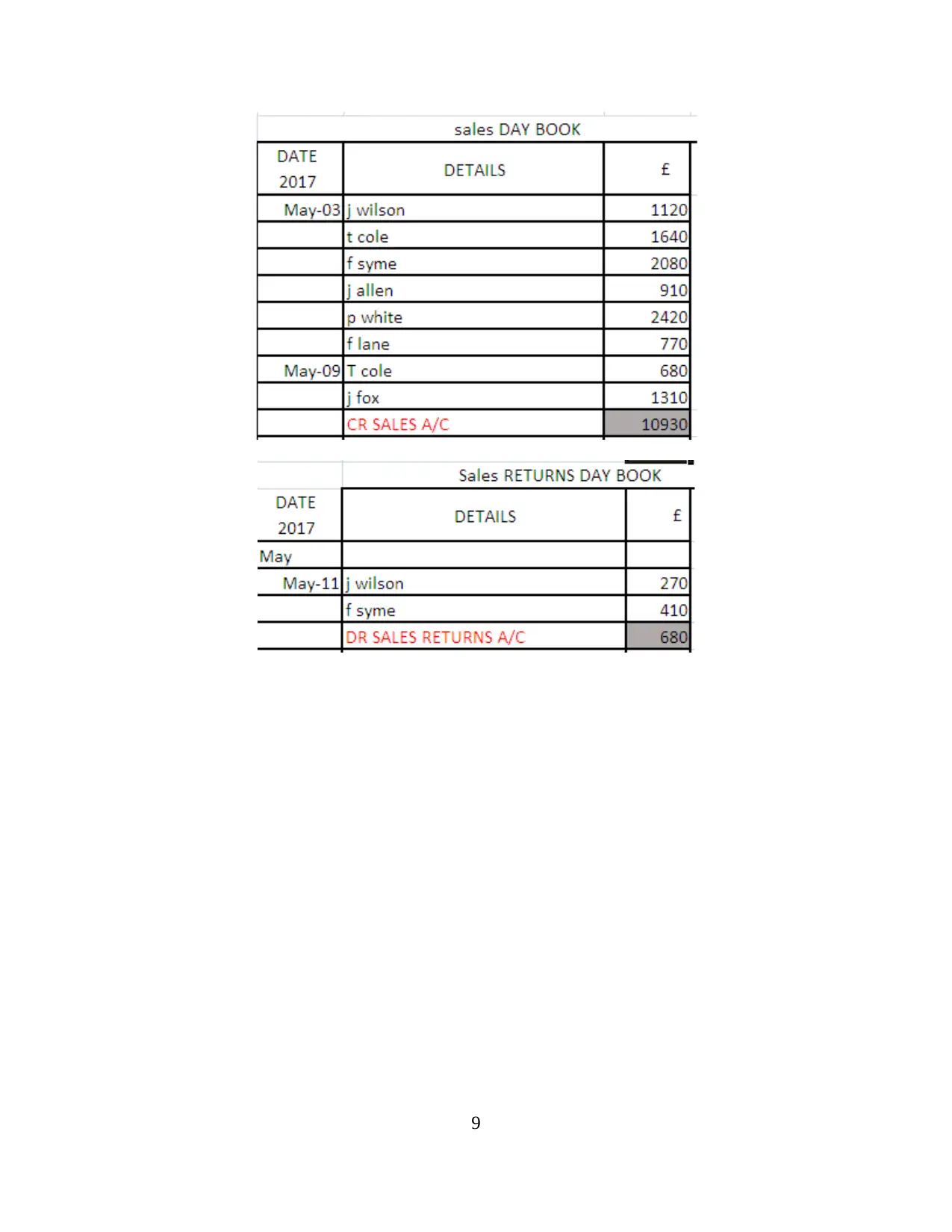

B Ledger accounts for the journal entries

8

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 36

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.