Comprehensive Management Accounting Report: Airdri Ltd Financials

VerifiedAdded on 2021/02/19

|17

|5088

|170

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within Airdri Ltd. It begins with an introduction to management accounting and its importance, followed by an analysis of different management accounting systems like price optimization, cost accounting, and inventory management. The report then explores various management accounting reporting methods, including budget reports, inventory reports, and cost accounting reports. The benefits of these systems are evaluated, highlighting their role in integrating organizational processes. The report delves into cost accounting techniques, comparing marginal and absorption costing through income statements for Airdri Ltd. It further examines planning tools for budgetary control and concludes with a discussion on how organizations adapt management accounting systems to address financial problems. The report utilizes examples and calculations to illustrate key concepts, making it a valuable resource for understanding financial management.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and need of management accounting system................................1

P2. Explain different method of management accounting reporting...........................................2

M1. Evaluation of benefits of various management accounting systems....................................3

D1 Management accounting system and management accounting reporting are integrated with

organisation process.....................................................................................................................4

TASK 2............................................................................................................................................4

P3: Cost accounting techniques to prepare an income statement................................................4

M2: Management accounting techniques and financial reporting documents............................8

D2. Financial reports which applies to interpret many business activities..................................9

TASK 3............................................................................................................................................9

P4: Advantages and disadvantages of different kind of planning tools of budgetary control.....9

M3: Evaluation of planning tools..............................................................................................10

TASK 4..........................................................................................................................................11

P5 Comparison of how organisation adopt management accounting system so as to respond to

financial problems.....................................................................................................................11

M4: Evaluation of financial issues............................................................................................13

D3: Critical analysis of financial issues.....................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and need of management accounting system................................1

P2. Explain different method of management accounting reporting...........................................2

M1. Evaluation of benefits of various management accounting systems....................................3

D1 Management accounting system and management accounting reporting are integrated with

organisation process.....................................................................................................................4

TASK 2............................................................................................................................................4

P3: Cost accounting techniques to prepare an income statement................................................4

M2: Management accounting techniques and financial reporting documents............................8

D2. Financial reports which applies to interpret many business activities..................................9

TASK 3............................................................................................................................................9

P4: Advantages and disadvantages of different kind of planning tools of budgetary control.....9

M3: Evaluation of planning tools..............................................................................................10

TASK 4..........................................................................................................................................11

P5 Comparison of how organisation adopt management accounting system so as to respond to

financial problems.....................................................................................................................11

M4: Evaluation of financial issues............................................................................................13

D3: Critical analysis of financial issues.....................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is defined as a concept in which business operations and costs

are analysed so that appropriate financial accounts, reports and records can be prepared in a

proper manner. This will benefits the business organisation in taking strategically right decisions

so that high growth can be achieved (Adler, 2013). In order to achieve this, the accounts manager

needs help from financial manager so that annual financial statements can be prepared in a

reliable manner. It will benefits the account manager in taking decisions as per financial position

of firm. This report is written in context with Airdri Ltd that operates in manufacturing and

designing of air dryers that have unique features and consumes less energy. This report is going

to cover about the concepts associated with managerial accounting, managerial reports and their

benefits to a business firm. Beside this, different costing methods and planning tools to control

budget are discussed. At last, measures to resolve financial problems are mentioned.

TASK 1

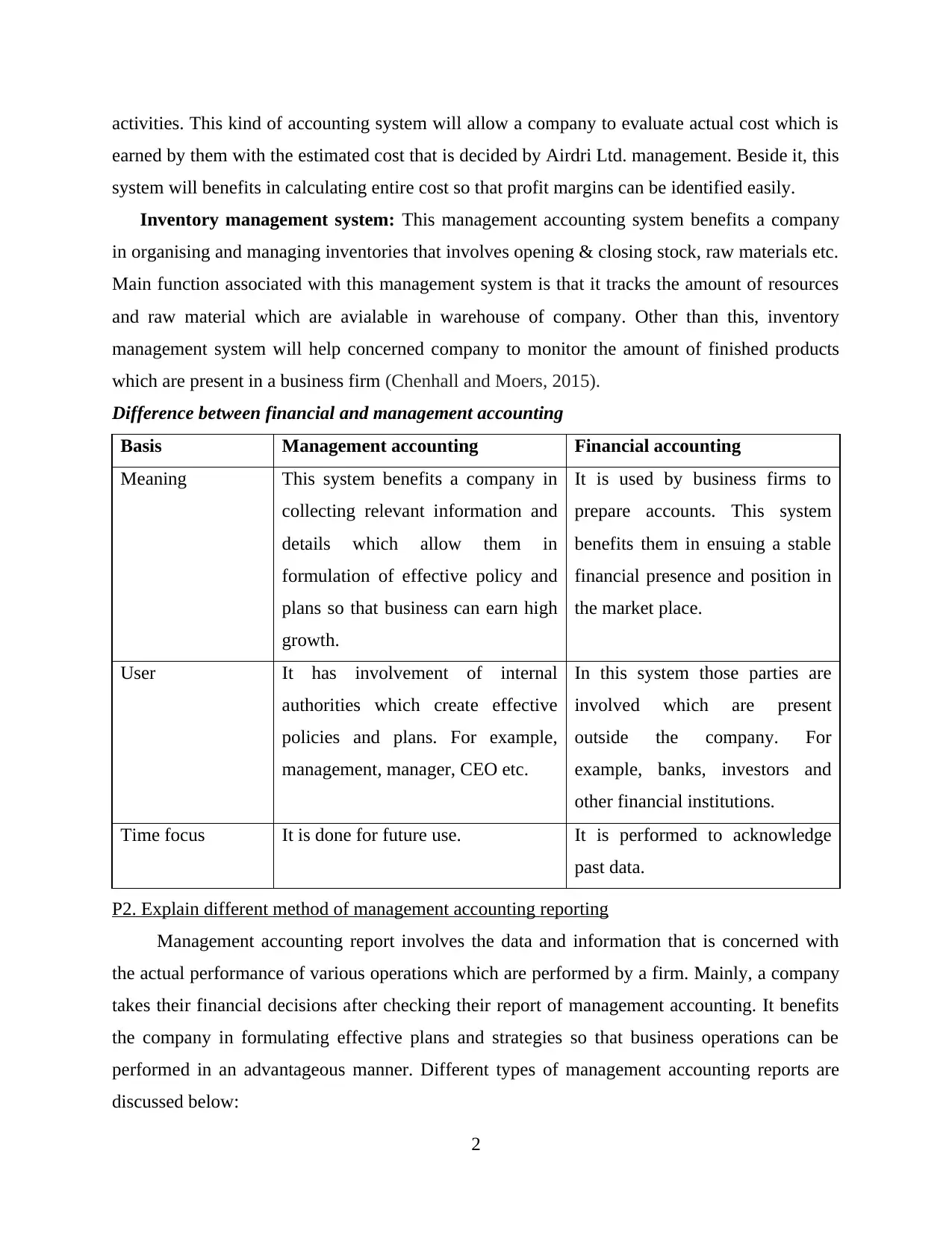

P1 Management accounting and need of management accounting system

Management accounting is defined as the way to communicate and analyse the financial

data to managers of an organisation so that timely and appropriate decisions can be taken. It

involve different types of accounting systems which are related with the financial terms of a

company associated with internal management. With the help of an efficient management

system, a firm takes important decisions by formulating effective procedures and policies. In

relation with Airdri Ltd., the management accounting systems are going to manage different

activities and functions so that work can be performed desirably. It depends on different methods

which are discussed below:

Price optimisation system: This kind of account management system benefits a firm in

developing an efficient framework which allow to regulate the prices of products or service

properly. This accounting system is vital for a business firm to determine appropriate rates for

specific services or product at equal level. This system is also beneficial in context with

customers as both organisation and client agrees at same price for the services & products which

are offered by firm (Arnaboldi, Lapsley and Steccolini, 2015).

Cost accounting system: In this kind of accounting system, total capital and finances are

calculated which are needed by a business firm to perform different business operations and

1

Management accounting is defined as a concept in which business operations and costs

are analysed so that appropriate financial accounts, reports and records can be prepared in a

proper manner. This will benefits the business organisation in taking strategically right decisions

so that high growth can be achieved (Adler, 2013). In order to achieve this, the accounts manager

needs help from financial manager so that annual financial statements can be prepared in a

reliable manner. It will benefits the account manager in taking decisions as per financial position

of firm. This report is written in context with Airdri Ltd that operates in manufacturing and

designing of air dryers that have unique features and consumes less energy. This report is going

to cover about the concepts associated with managerial accounting, managerial reports and their

benefits to a business firm. Beside this, different costing methods and planning tools to control

budget are discussed. At last, measures to resolve financial problems are mentioned.

TASK 1

P1 Management accounting and need of management accounting system

Management accounting is defined as the way to communicate and analyse the financial

data to managers of an organisation so that timely and appropriate decisions can be taken. It

involve different types of accounting systems which are related with the financial terms of a

company associated with internal management. With the help of an efficient management

system, a firm takes important decisions by formulating effective procedures and policies. In

relation with Airdri Ltd., the management accounting systems are going to manage different

activities and functions so that work can be performed desirably. It depends on different methods

which are discussed below:

Price optimisation system: This kind of account management system benefits a firm in

developing an efficient framework which allow to regulate the prices of products or service

properly. This accounting system is vital for a business firm to determine appropriate rates for

specific services or product at equal level. This system is also beneficial in context with

customers as both organisation and client agrees at same price for the services & products which

are offered by firm (Arnaboldi, Lapsley and Steccolini, 2015).

Cost accounting system: In this kind of accounting system, total capital and finances are

calculated which are needed by a business firm to perform different business operations and

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

activities. This kind of accounting system will allow a company to evaluate actual cost which is

earned by them with the estimated cost that is decided by Airdri Ltd. management. Beside it, this

system will benefits in calculating entire cost so that profit margins can be identified easily.

Inventory management system: This management accounting system benefits a company

in organising and managing inventories that involves opening & closing stock, raw materials etc.

Main function associated with this management system is that it tracks the amount of resources

and raw material which are avialable in warehouse of company. Other than this, inventory

management system will help concerned company to monitor the amount of finished products

which are present in a business firm (Chenhall and Moers, 2015).

Difference between financial and management accounting

Basis Management accounting Financial accounting

Meaning This system benefits a company in

collecting relevant information and

details which allow them in

formulation of effective policy and

plans so that business can earn high

growth.

It is used by business firms to

prepare accounts. This system

benefits them in ensuing a stable

financial presence and position in

the market place.

User It has involvement of internal

authorities which create effective

policies and plans. For example,

management, manager, CEO etc.

In this system those parties are

involved which are present

outside the company. For

example, banks, investors and

other financial institutions.

Time focus It is done for future use. It is performed to acknowledge

past data.

P2. Explain different method of management accounting reporting

Management accounting report involves the data and information that is concerned with

the actual performance of various operations which are performed by a firm. Mainly, a company

takes their financial decisions after checking their report of management accounting. It benefits

the company in formulating effective plans and strategies so that business operations can be

performed in an advantageous manner. Different types of management accounting reports are

discussed below:

2

earned by them with the estimated cost that is decided by Airdri Ltd. management. Beside it, this

system will benefits in calculating entire cost so that profit margins can be identified easily.

Inventory management system: This management accounting system benefits a company

in organising and managing inventories that involves opening & closing stock, raw materials etc.

Main function associated with this management system is that it tracks the amount of resources

and raw material which are avialable in warehouse of company. Other than this, inventory

management system will help concerned company to monitor the amount of finished products

which are present in a business firm (Chenhall and Moers, 2015).

Difference between financial and management accounting

Basis Management accounting Financial accounting

Meaning This system benefits a company in

collecting relevant information and

details which allow them in

formulation of effective policy and

plans so that business can earn high

growth.

It is used by business firms to

prepare accounts. This system

benefits them in ensuing a stable

financial presence and position in

the market place.

User It has involvement of internal

authorities which create effective

policies and plans. For example,

management, manager, CEO etc.

In this system those parties are

involved which are present

outside the company. For

example, banks, investors and

other financial institutions.

Time focus It is done for future use. It is performed to acknowledge

past data.

P2. Explain different method of management accounting reporting

Management accounting report involves the data and information that is concerned with

the actual performance of various operations which are performed by a firm. Mainly, a company

takes their financial decisions after checking their report of management accounting. It benefits

the company in formulating effective plans and strategies so that business operations can be

performed in an advantageous manner. Different types of management accounting reports are

discussed below:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budget report- With the help of this report, a company can find out the estimated expanses

and actual earning by performing different activities and business operations. In accordance with

this budget reports, Airdri Ltd. Can measure and calculate the accurate outcomes for their

expenditure and income. Due to this, organisation will be capable to estimate the price for next

years. In case of Airdri Ltd., this report will allow the company to measure their true

performance in market (Evans, Burritt and Guthrie, 2013).

Inventory report- This accounting report covers complete information about the stock

which are presented in the warehouse of a company. Beside this, inventory report helps in

measuring the costs which is generated because of inventory such as transportation cost that

incurred due to supply of raw material, ordering cost etc. In case of concerns company, this

report will allow in recording current inventory and associated costs.

Cost accounting report- This kind of report involve detailed information related with the

total expanses incurred by a company. This report is used in all kind of activities and operations

which is performed by company. This report helps in analysing if the cost for an aspect is viable

or fixed. In context with Airdri Ltd., this report allows to cover the costs before the sale

procedure and the income which is received after selling (Grabner and Moers, 2013).

M1. Evaluation of benefits of various management accounting systems

Management accounting system provides huge benefits to the organisation because they

are incurred with proper financial data record that helps to generate effective results for the

organisation. Moreover it also helps them to accomplish their goal with objective with high

efficiency and effectiveness. Some benefits for management accounting system are as follow:

Advantage of inventory management

AirDri implemented this system because it helps them to manage the inventory according

to the needs of the consumer. Example- Inventory management system helps them to

maintain their effective asset liability ratio through monitoring their current asset position

in organisation.

Another benefit is that it helps an organisation to order required inventory through which

it is unnecessary cost to manage them will be reduced.

Advantage of cost accounting system

3

and actual earning by performing different activities and business operations. In accordance with

this budget reports, Airdri Ltd. Can measure and calculate the accurate outcomes for their

expenditure and income. Due to this, organisation will be capable to estimate the price for next

years. In case of Airdri Ltd., this report will allow the company to measure their true

performance in market (Evans, Burritt and Guthrie, 2013).

Inventory report- This accounting report covers complete information about the stock

which are presented in the warehouse of a company. Beside this, inventory report helps in

measuring the costs which is generated because of inventory such as transportation cost that

incurred due to supply of raw material, ordering cost etc. In case of concerns company, this

report will allow in recording current inventory and associated costs.

Cost accounting report- This kind of report involve detailed information related with the

total expanses incurred by a company. This report is used in all kind of activities and operations

which is performed by company. This report helps in analysing if the cost for an aspect is viable

or fixed. In context with Airdri Ltd., this report allows to cover the costs before the sale

procedure and the income which is received after selling (Grabner and Moers, 2013).

M1. Evaluation of benefits of various management accounting systems

Management accounting system provides huge benefits to the organisation because they

are incurred with proper financial data record that helps to generate effective results for the

organisation. Moreover it also helps them to accomplish their goal with objective with high

efficiency and effectiveness. Some benefits for management accounting system are as follow:

Advantage of inventory management

AirDri implemented this system because it helps them to manage the inventory according

to the needs of the consumer. Example- Inventory management system helps them to

maintain their effective asset liability ratio through monitoring their current asset position

in organisation.

Another benefit is that it helps an organisation to order required inventory through which

it is unnecessary cost to manage them will be reduced.

Advantage of cost accounting system

3

The cost accounting system is more useful for AirDri as it helps them to predict out those

factors due to which there cost will be increased in the market. It results that it helps them

to cut extra cost and increase profit for the organisation.

Cost accounting system helps financial department in order to find out actual cost that is

invested by them to produce their product or service that is delivered to customers.

D1 Management accounting system and management accounting reporting are integrated with

organisation process

AirDri focuses on management accounting and management reporting due to which it is

easy for them to integrate between different activities of them. Through this financial department

of the organisation develops and executed the plan due to enhance more productivity in their

organisation. Example- it helps them to record the cost of inventory along with the stock that is

present in organisation warehouse. So in future they order sufficient amount of inventory.

TASK 2

P3: Cost accounting techniques to prepare an income statement

Cost: It refers to an amount which is paid or sacrificed to gain something. It is usually

valuation of different aspects that include efforts, resources, time invested, material used, risk

incurred and opportunity sacrificed in manufacturing and delivery of products and services. All

th expenditures a costs but all costs are not expenses. It is classified into two types which are

discussed as under:

Marginal costing: It is a principle in which the variable costs are charged against the cost

unit and fixed costs of the period are written off in full against the overall contribution. Due to

adding only variable cost while making calculation of net profits of company, the profitability

has been increased through which the investors can easily be attracted (Hartmann, Perego, and

Young, 2013).

Absorption costing: It is a method which mainly considers both fixed and variable costs

as products costs. It is mainly used for reporting purposes which includes both financial and

taxation reporting. Due to adding both marginal and absorption cost, the profitability has been

decreased but reflects actual financial position of company through its financial statement. Thus,

it can help company in retaining trust and loyalty of existing shareholders (Absorption costing,

2018).

4

factors due to which there cost will be increased in the market. It results that it helps them

to cut extra cost and increase profit for the organisation.

Cost accounting system helps financial department in order to find out actual cost that is

invested by them to produce their product or service that is delivered to customers.

D1 Management accounting system and management accounting reporting are integrated with

organisation process

AirDri focuses on management accounting and management reporting due to which it is

easy for them to integrate between different activities of them. Through this financial department

of the organisation develops and executed the plan due to enhance more productivity in their

organisation. Example- it helps them to record the cost of inventory along with the stock that is

present in organisation warehouse. So in future they order sufficient amount of inventory.

TASK 2

P3: Cost accounting techniques to prepare an income statement

Cost: It refers to an amount which is paid or sacrificed to gain something. It is usually

valuation of different aspects that include efforts, resources, time invested, material used, risk

incurred and opportunity sacrificed in manufacturing and delivery of products and services. All

th expenditures a costs but all costs are not expenses. It is classified into two types which are

discussed as under:

Marginal costing: It is a principle in which the variable costs are charged against the cost

unit and fixed costs of the period are written off in full against the overall contribution. Due to

adding only variable cost while making calculation of net profits of company, the profitability

has been increased through which the investors can easily be attracted (Hartmann, Perego, and

Young, 2013).

Absorption costing: It is a method which mainly considers both fixed and variable costs

as products costs. It is mainly used for reporting purposes which includes both financial and

taxation reporting. Due to adding both marginal and absorption cost, the profitability has been

decreased but reflects actual financial position of company through its financial statement. Thus,

it can help company in retaining trust and loyalty of existing shareholders (Absorption costing,

2018).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

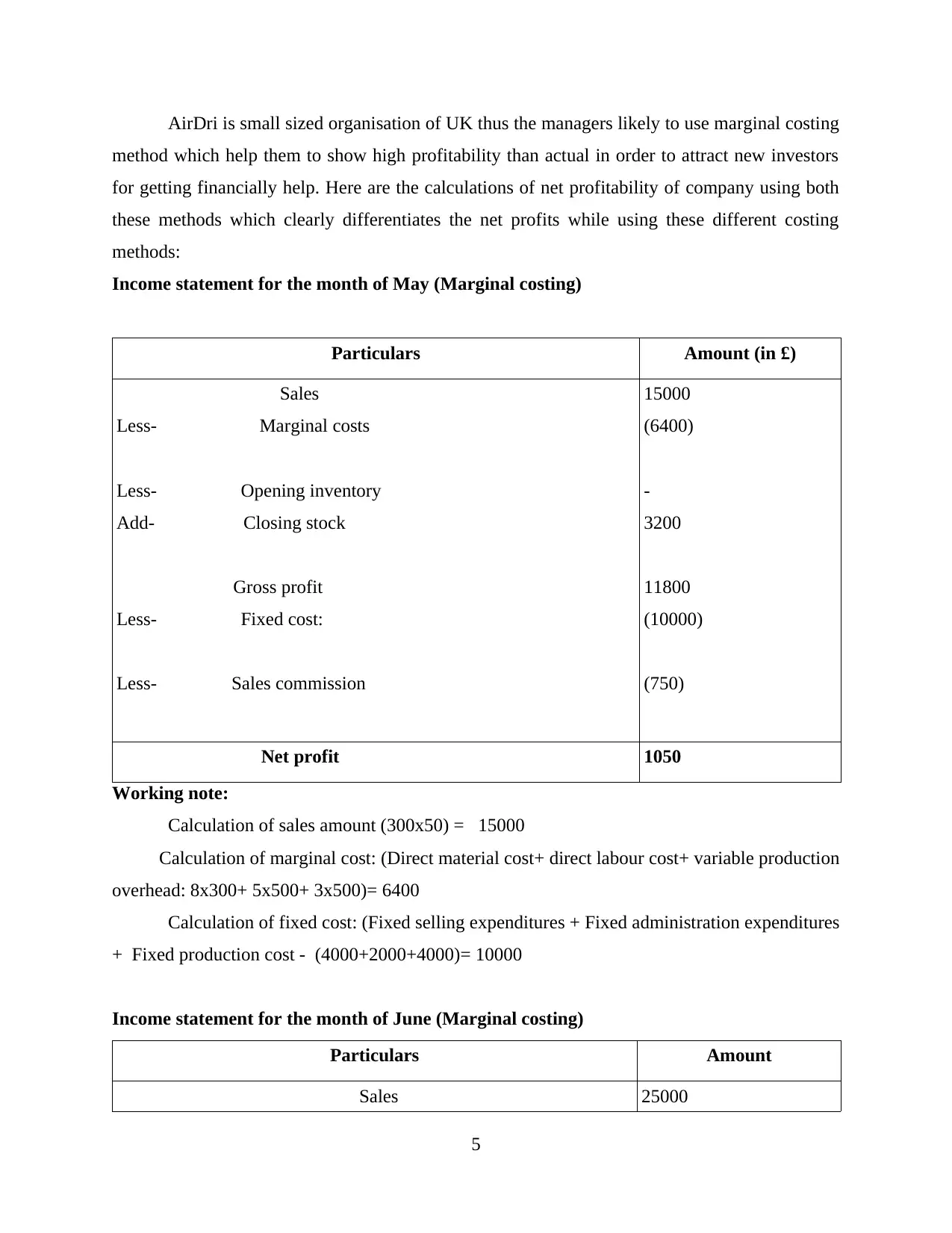

AirDri is small sized organisation of UK thus the managers likely to use marginal costing

method which help them to show high profitability than actual in order to attract new investors

for getting financially help. Here are the calculations of net profitability of company using both

these methods which clearly differentiates the net profits while using these different costing

methods:

Income statement for the month of May (Marginal costing)

Particulars Amount (in £)

Sales

Less- Marginal costs

Less- Opening inventory

Add- Closing stock

Gross profit

Less- Fixed cost:

Less- Sales commission

15000

(6400)

-

3200

11800

(10000)

(750)

Net profit 1050

Working note:

Calculation of sales amount (300x50) = 15000

Calculation of marginal cost: (Direct material cost+ direct labour cost+ variable production

overhead: 8x300+ 5x500+ 3x500)= 6400

Calculation of fixed cost: (Fixed selling expenditures + Fixed administration expenditures

+ Fixed production cost - (4000+2000+4000)= 10000

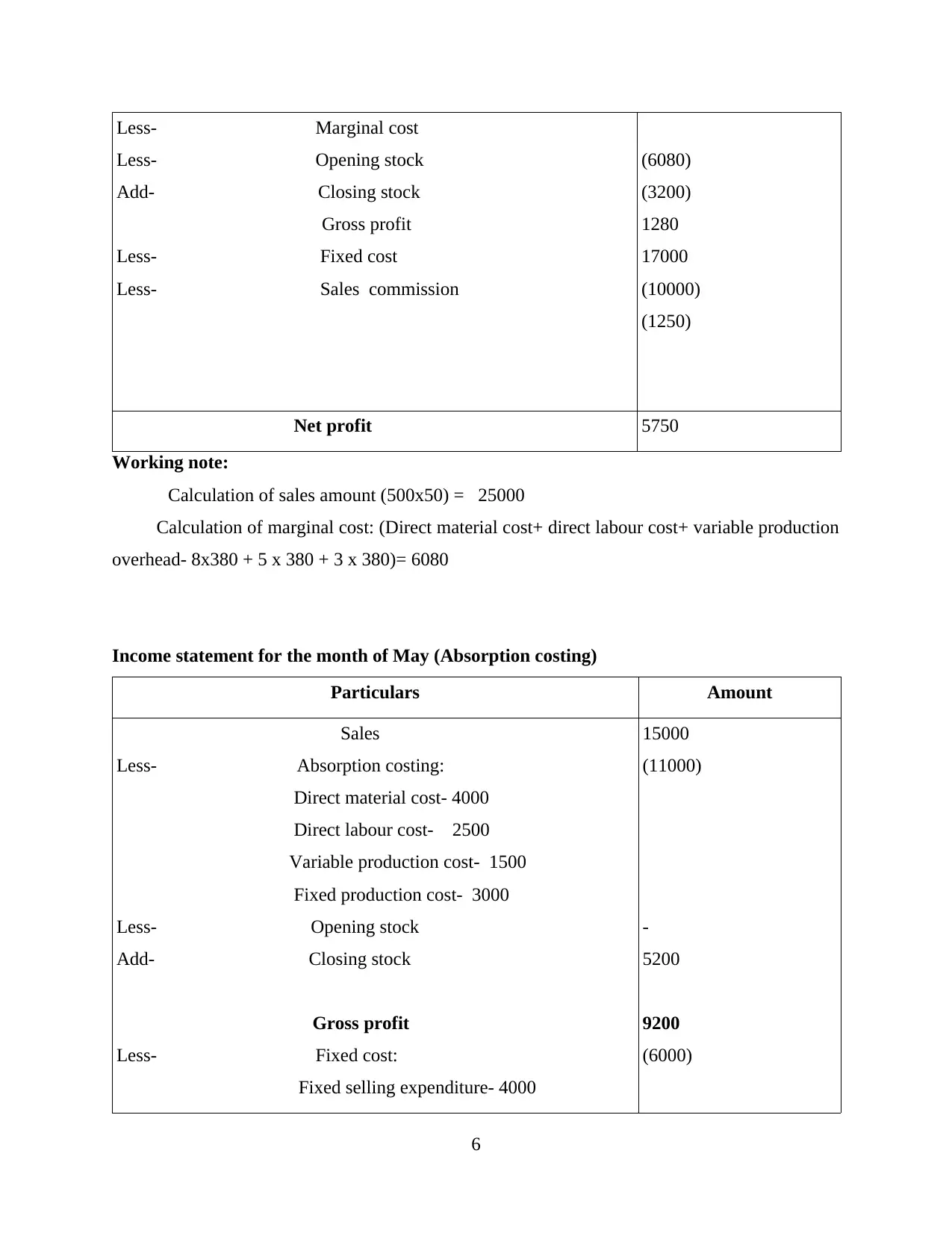

Income statement for the month of June (Marginal costing)

Particulars Amount

Sales 25000

5

method which help them to show high profitability than actual in order to attract new investors

for getting financially help. Here are the calculations of net profitability of company using both

these methods which clearly differentiates the net profits while using these different costing

methods:

Income statement for the month of May (Marginal costing)

Particulars Amount (in £)

Sales

Less- Marginal costs

Less- Opening inventory

Add- Closing stock

Gross profit

Less- Fixed cost:

Less- Sales commission

15000

(6400)

-

3200

11800

(10000)

(750)

Net profit 1050

Working note:

Calculation of sales amount (300x50) = 15000

Calculation of marginal cost: (Direct material cost+ direct labour cost+ variable production

overhead: 8x300+ 5x500+ 3x500)= 6400

Calculation of fixed cost: (Fixed selling expenditures + Fixed administration expenditures

+ Fixed production cost - (4000+2000+4000)= 10000

Income statement for the month of June (Marginal costing)

Particulars Amount

Sales 25000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less- Marginal cost

Less- Opening stock

Add- Closing stock

Gross profit

Less- Fixed cost

Less- Sales commission

(6080)

(3200)

1280

17000

(10000)

(1250)

Net profit 5750

Working note:

Calculation of sales amount (500x50) = 25000

Calculation of marginal cost: (Direct material cost+ direct labour cost+ variable production

overhead- 8x380 + 5 x 380 + 3 x 380)= 6080

Income statement for the month of May (Absorption costing)

Particulars Amount

Sales

Less- Absorption costing:

Direct material cost- 4000

Direct labour cost- 2500

Variable production cost- 1500

Fixed production cost- 3000

Less- Opening stock

Add- Closing stock

Gross profit

Less- Fixed cost:

Fixed selling expenditure- 4000

15000

(11000)

-

5200

9200

(6000)

6

Less- Opening stock

Add- Closing stock

Gross profit

Less- Fixed cost

Less- Sales commission

(6080)

(3200)

1280

17000

(10000)

(1250)

Net profit 5750

Working note:

Calculation of sales amount (500x50) = 25000

Calculation of marginal cost: (Direct material cost+ direct labour cost+ variable production

overhead- 8x380 + 5 x 380 + 3 x 380)= 6080

Income statement for the month of May (Absorption costing)

Particulars Amount

Sales

Less- Absorption costing:

Direct material cost- 4000

Direct labour cost- 2500

Variable production cost- 1500

Fixed production cost- 3000

Less- Opening stock

Add- Closing stock

Gross profit

Less- Fixed cost:

Fixed selling expenditure- 4000

15000

(11000)

-

5200

9200

(6000)

6

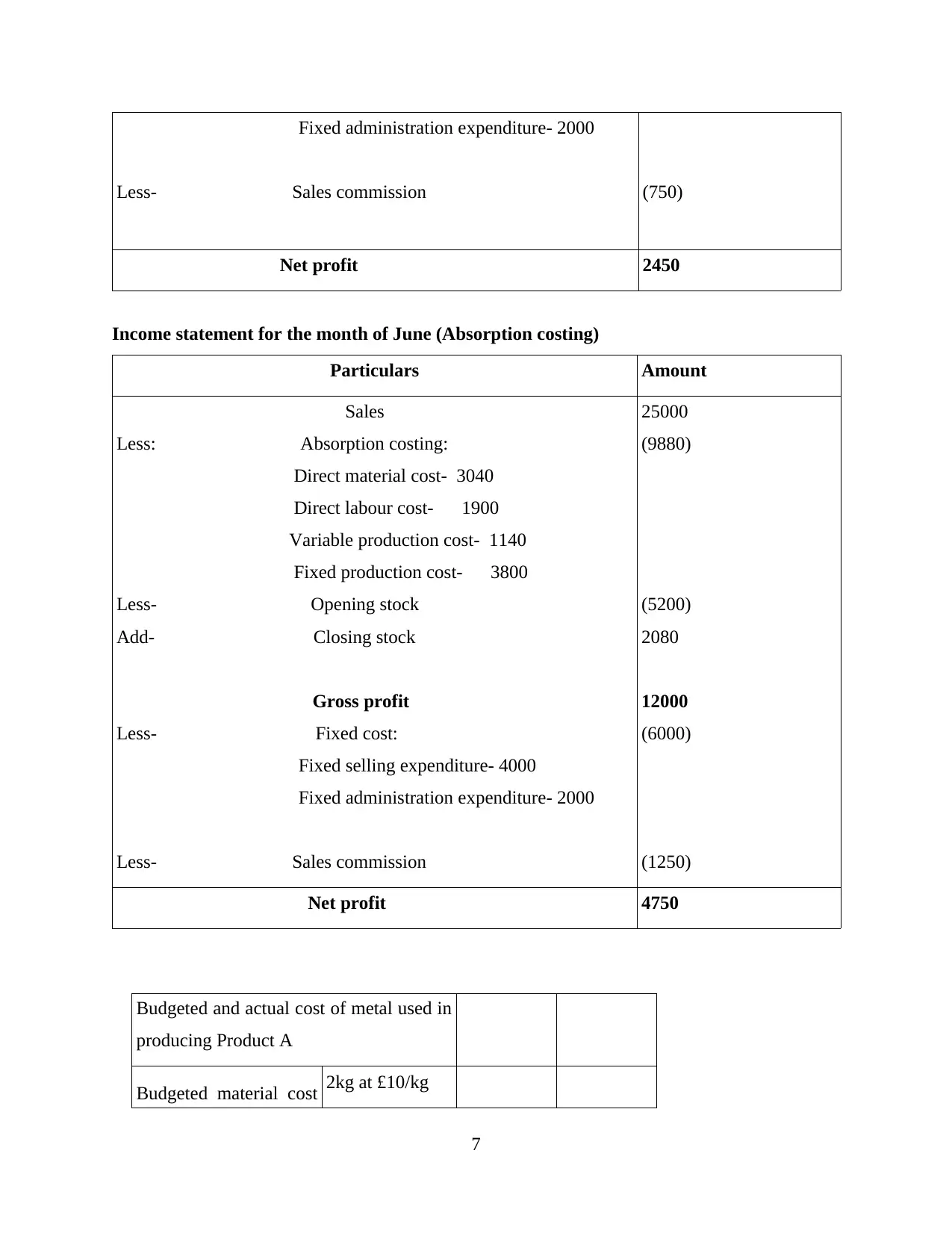

Fixed administration expenditure- 2000

Less- Sales commission (750)

Net profit 2450

Income statement for the month of June (Absorption costing)

Particulars Amount

Sales

Less: Absorption costing:

Direct material cost- 3040

Direct labour cost- 1900

Variable production cost- 1140

Fixed production cost- 3800

Less- Opening stock

Add- Closing stock

Gross profit

Less- Fixed cost:

Fixed selling expenditure- 4000

Fixed administration expenditure- 2000

Less- Sales commission

25000

(9880)

(5200)

2080

12000

(6000)

(1250)

Net profit 4750

Budgeted and actual cost of metal used in

producing Product A

Budgeted material cost 2kg at £10/kg

7

Less- Sales commission (750)

Net profit 2450

Income statement for the month of June (Absorption costing)

Particulars Amount

Sales

Less: Absorption costing:

Direct material cost- 3040

Direct labour cost- 1900

Variable production cost- 1140

Fixed production cost- 3800

Less- Opening stock

Add- Closing stock

Gross profit

Less- Fixed cost:

Fixed selling expenditure- 4000

Fixed administration expenditure- 2000

Less- Sales commission

25000

(9880)

(5200)

2080

12000

(6000)

(1250)

Net profit 4750

Budgeted and actual cost of metal used in

producing Product A

Budgeted material cost 2kg at £10/kg

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

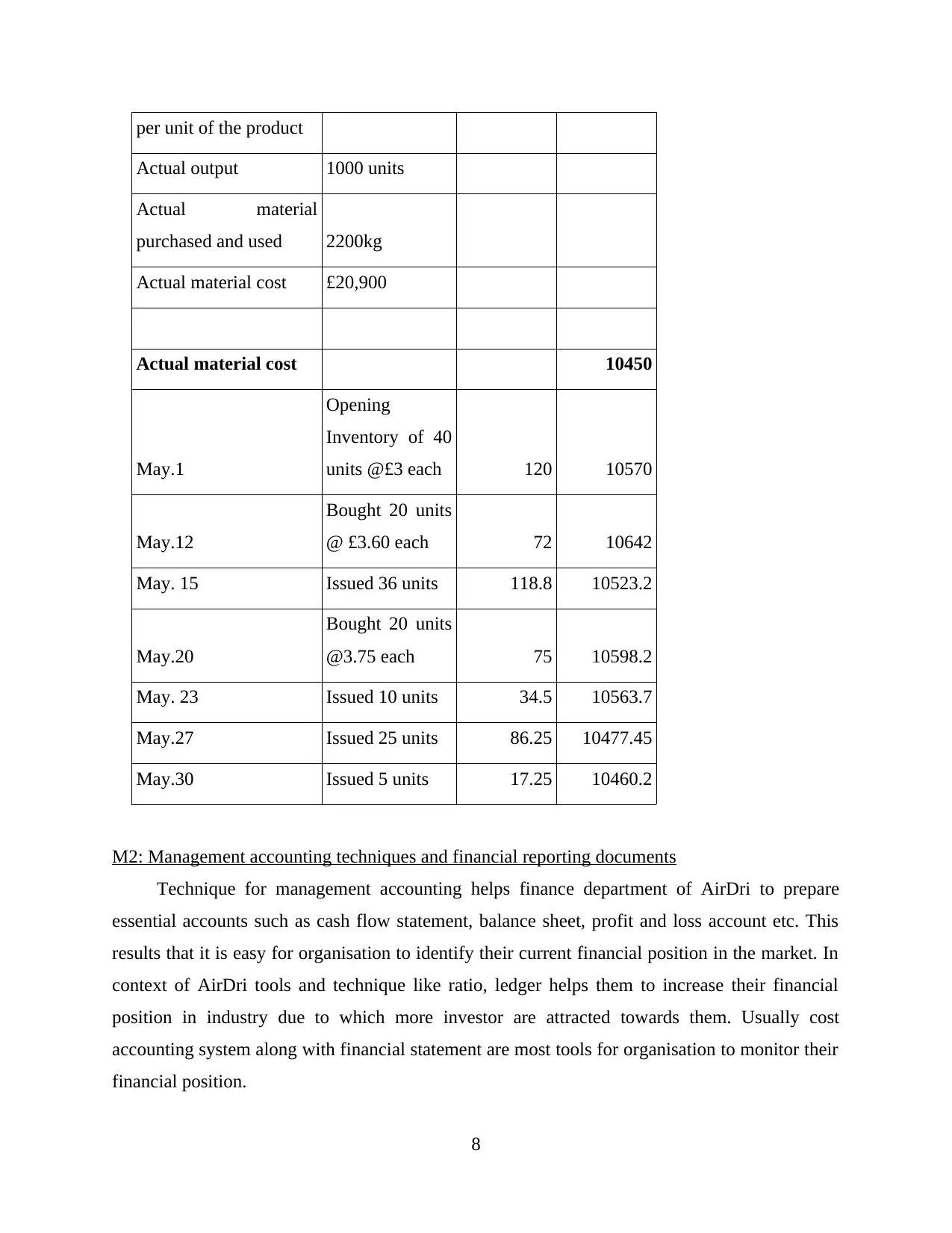

per unit of the product

Actual output 1000 units

Actual material

purchased and used 2200kg

Actual material cost £20,900

Actual material cost 10450

May.1

Opening

Inventory of 40

units @£3 each 120 10570

May.12

Bought 20 units

@ £3.60 each 72 10642

May. 15 Issued 36 units 118.8 10523.2

May.20

Bought 20 units

@3.75 each 75 10598.2

May. 23 Issued 10 units 34.5 10563.7

May.27 Issued 25 units 86.25 10477.45

May.30 Issued 5 units 17.25 10460.2

M2: Management accounting techniques and financial reporting documents

Technique for management accounting helps finance department of AirDri to prepare

essential accounts such as cash flow statement, balance sheet, profit and loss account etc. This

results that it is easy for organisation to identify their current financial position in the market. In

context of AirDri tools and technique like ratio, ledger helps them to increase their financial

position in industry due to which more investor are attracted towards them. Usually cost

accounting system along with financial statement are most tools for organisation to monitor their

financial position.

8

Actual output 1000 units

Actual material

purchased and used 2200kg

Actual material cost £20,900

Actual material cost 10450

May.1

Opening

Inventory of 40

units @£3 each 120 10570

May.12

Bought 20 units

@ £3.60 each 72 10642

May. 15 Issued 36 units 118.8 10523.2

May.20

Bought 20 units

@3.75 each 75 10598.2

May. 23 Issued 10 units 34.5 10563.7

May.27 Issued 25 units 86.25 10477.45

May.30 Issued 5 units 17.25 10460.2

M2: Management accounting techniques and financial reporting documents

Technique for management accounting helps finance department of AirDri to prepare

essential accounts such as cash flow statement, balance sheet, profit and loss account etc. This

results that it is easy for organisation to identify their current financial position in the market. In

context of AirDri tools and technique like ratio, ledger helps them to increase their financial

position in industry due to which more investor are attracted towards them. Usually cost

accounting system along with financial statement are most tools for organisation to monitor their

financial position.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D2. Financial reports which applies to interpret many business activities

It is essential for every organisation to maintain the proper record of their financial

transaction such as purchasing of raw material, revenue and expenses etc. As it is necessary for

AirDri because it helps them to evaluates the current financial position of the organisation.

Further it also analysis or measure the actual cost that is invested by organisation to complete

their project and business activities.

TASK 3

P4: Advantages and disadvantages of different kind of planning tools of budgetary control

Budget- It work as an internal tool for the organisation that is mainly used to measure or

calculate the expenses and income for the upcoming year. In context of AirDri it is useful for

them as it monitor the target or goals on regular basis such as monthly, half-yearly and quarterly.

Apart from this it helps them to evaluate the cost that is incurred to attain their desired gaols.

Types of budget- Budgets that are generated by AirDri are as follow:

Cash flow budget- The main function of this cash flow budget is to record all the cash

transaction whether they are income or expense for the organisation. So in the future it is easy for

the organisation to manage and invest their properly that helps to increase their profits by cutting

down extra expenses that are incurred in their operations (Lachmann, Knauer and Trapp, 2013).

Financial budget- The main function of financial budget is to evaluate and maintain the

proper records of financial that are present in the organisation. For this fund flow, cash flow,

financial ratio etc. are the major tool to prepare an effective budget. AirDri develops their budget

which are beneficial for organisation, employees and customers.

Budgetary control- This is the process through which it is easy for organisation to utilize

their budget for the whole year in optimum way. Finance department of AirDri develops budget

in order to complete their activities effectively. While they also formulates budget for the small

organisation that help them to control their expenses by completing their operations within the

decide budget.

Contingency tool- AirDri uses this tool to control the negative situation that create

barrier in the organisation. With formulating contingency tools it is easy for organisation to

respond positively in complex situations (Lambert and Sponem, 2012).

Advantages

9

It is essential for every organisation to maintain the proper record of their financial

transaction such as purchasing of raw material, revenue and expenses etc. As it is necessary for

AirDri because it helps them to evaluates the current financial position of the organisation.

Further it also analysis or measure the actual cost that is invested by organisation to complete

their project and business activities.

TASK 3

P4: Advantages and disadvantages of different kind of planning tools of budgetary control

Budget- It work as an internal tool for the organisation that is mainly used to measure or

calculate the expenses and income for the upcoming year. In context of AirDri it is useful for

them as it monitor the target or goals on regular basis such as monthly, half-yearly and quarterly.

Apart from this it helps them to evaluate the cost that is incurred to attain their desired gaols.

Types of budget- Budgets that are generated by AirDri are as follow:

Cash flow budget- The main function of this cash flow budget is to record all the cash

transaction whether they are income or expense for the organisation. So in the future it is easy for

the organisation to manage and invest their properly that helps to increase their profits by cutting

down extra expenses that are incurred in their operations (Lachmann, Knauer and Trapp, 2013).

Financial budget- The main function of financial budget is to evaluate and maintain the

proper records of financial that are present in the organisation. For this fund flow, cash flow,

financial ratio etc. are the major tool to prepare an effective budget. AirDri develops their budget

which are beneficial for organisation, employees and customers.

Budgetary control- This is the process through which it is easy for organisation to utilize

their budget for the whole year in optimum way. Finance department of AirDri develops budget

in order to complete their activities effectively. While they also formulates budget for the small

organisation that help them to control their expenses by completing their operations within the

decide budget.

Contingency tool- AirDri uses this tool to control the negative situation that create

barrier in the organisation. With formulating contingency tools it is easy for organisation to

respond positively in complex situations (Lambert and Sponem, 2012).

Advantages

9

It helps an organisation to deal with difficult situation by maintain their regular profits

which result that does not loss their stability at time of up and down in industry.

Management of AirDri find out that which department or individual is responsible for

this difficult situation.

Dis-advantage This type of budget are hard to maintain which determines that it is complex to prepare

and implement them in the organisation.

Contingency budget are developed for uncertainties which is not sure that they take place

in the organisation.

Forecasting tool- This tool is most useful for the organisation because it helps them to

formulate effective business strategy for the organisation. AirDri uses this quantitative and

qualitative tool to implement forecasting tool in the organisation. for this they take the base of

present and past data that is stored by the organisation (Morden, 2016).

Advantage Forecasting tool helps an organisation to deliver their essential information between all

departments of the organisation.

Another benefit to execute forecasting tool that it helps them to formulate budget

according to the market conditions.

Dis-advantage

The major drawback of this that they uses only present scenario and aspect that impact

on budget of the organisation.

In present scenario there is high competition exists in market due to which there are

regular changes in market conditions. It creates difficulty for AirDri to predict the

industry.

M3: Evaluation of planning tools

Planning tools help company to control unnecessary expenses that are not covered in

budget process. AirDri use these tool to reduce cost of operation and complete operational

activities with allotted budget. Like forecasting tool help management to make estimation about

future expenses and to prepare budget to formulate future policy by control this expenses (Nitzl,

2016).

Planning tools are executed by an organisation to monitor and control the unnecessary the

expenses which are not involved in the budget process. AirDri implement this tool to minimize

their operating cost. This results that all departments of the organisation accomplished their

10

which result that does not loss their stability at time of up and down in industry.

Management of AirDri find out that which department or individual is responsible for

this difficult situation.

Dis-advantage This type of budget are hard to maintain which determines that it is complex to prepare

and implement them in the organisation.

Contingency budget are developed for uncertainties which is not sure that they take place

in the organisation.

Forecasting tool- This tool is most useful for the organisation because it helps them to

formulate effective business strategy for the organisation. AirDri uses this quantitative and

qualitative tool to implement forecasting tool in the organisation. for this they take the base of

present and past data that is stored by the organisation (Morden, 2016).

Advantage Forecasting tool helps an organisation to deliver their essential information between all

departments of the organisation.

Another benefit to execute forecasting tool that it helps them to formulate budget

according to the market conditions.

Dis-advantage

The major drawback of this that they uses only present scenario and aspect that impact

on budget of the organisation.

In present scenario there is high competition exists in market due to which there are

regular changes in market conditions. It creates difficulty for AirDri to predict the

industry.

M3: Evaluation of planning tools

Planning tools help company to control unnecessary expenses that are not covered in

budget process. AirDri use these tool to reduce cost of operation and complete operational

activities with allotted budget. Like forecasting tool help management to make estimation about

future expenses and to prepare budget to formulate future policy by control this expenses (Nitzl,

2016).

Planning tools are executed by an organisation to monitor and control the unnecessary the

expenses which are not involved in the budget process. AirDri implement this tool to minimize

their operating cost. This results that all departments of the organisation accomplished their

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.