Financial Accounting Report: Bank Financial Statement Analysis

VerifiedAdded on 2020/04/07

|21

|1435

|87

Report

AI Summary

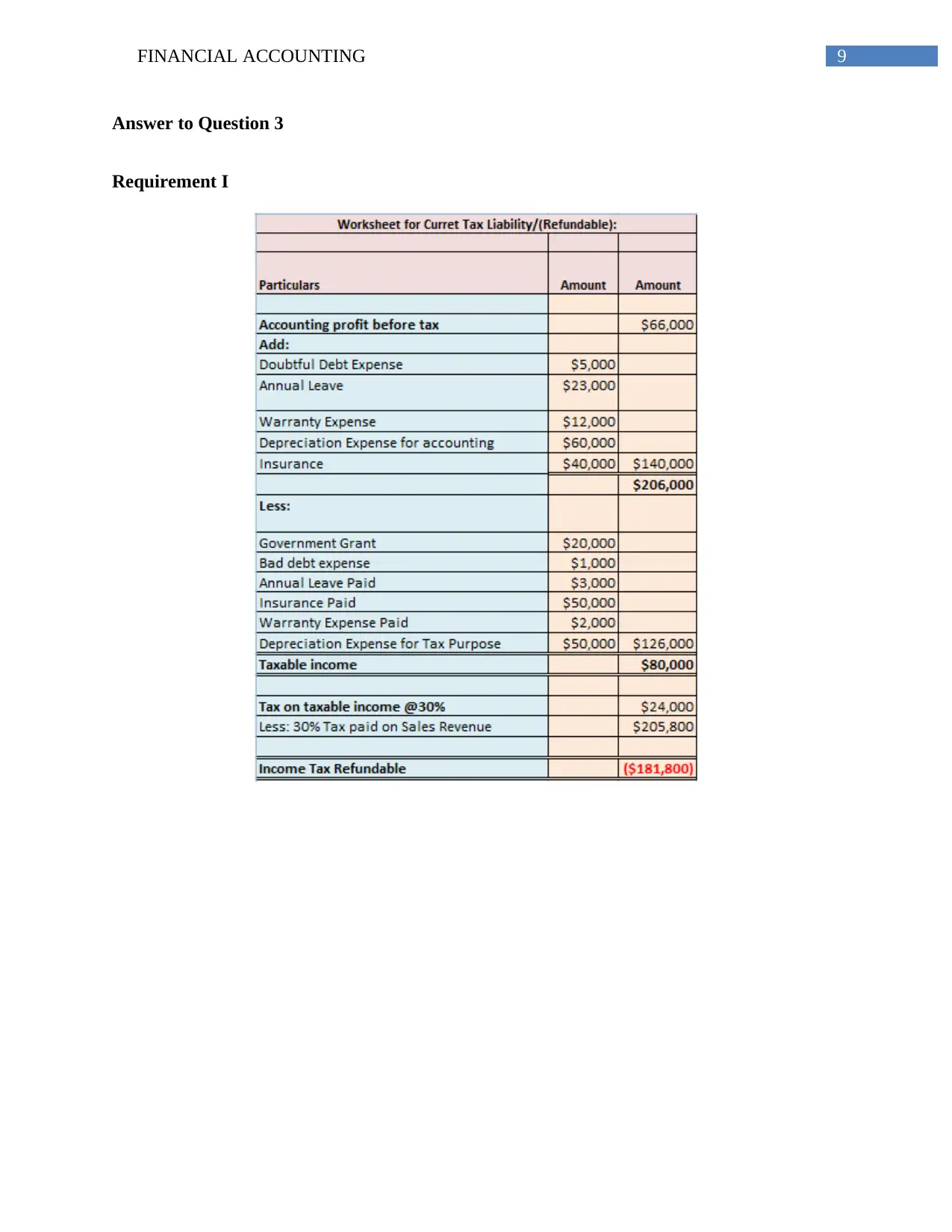

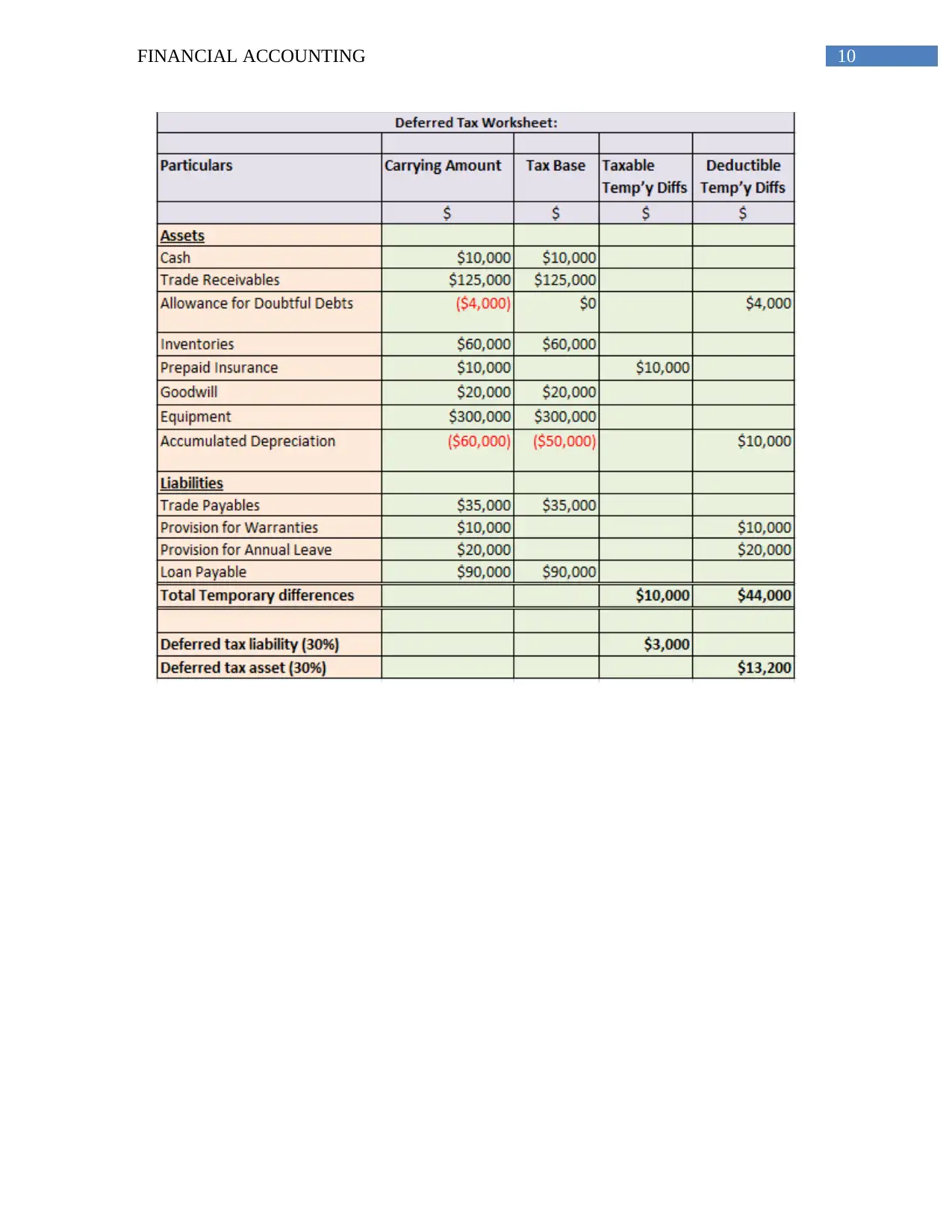

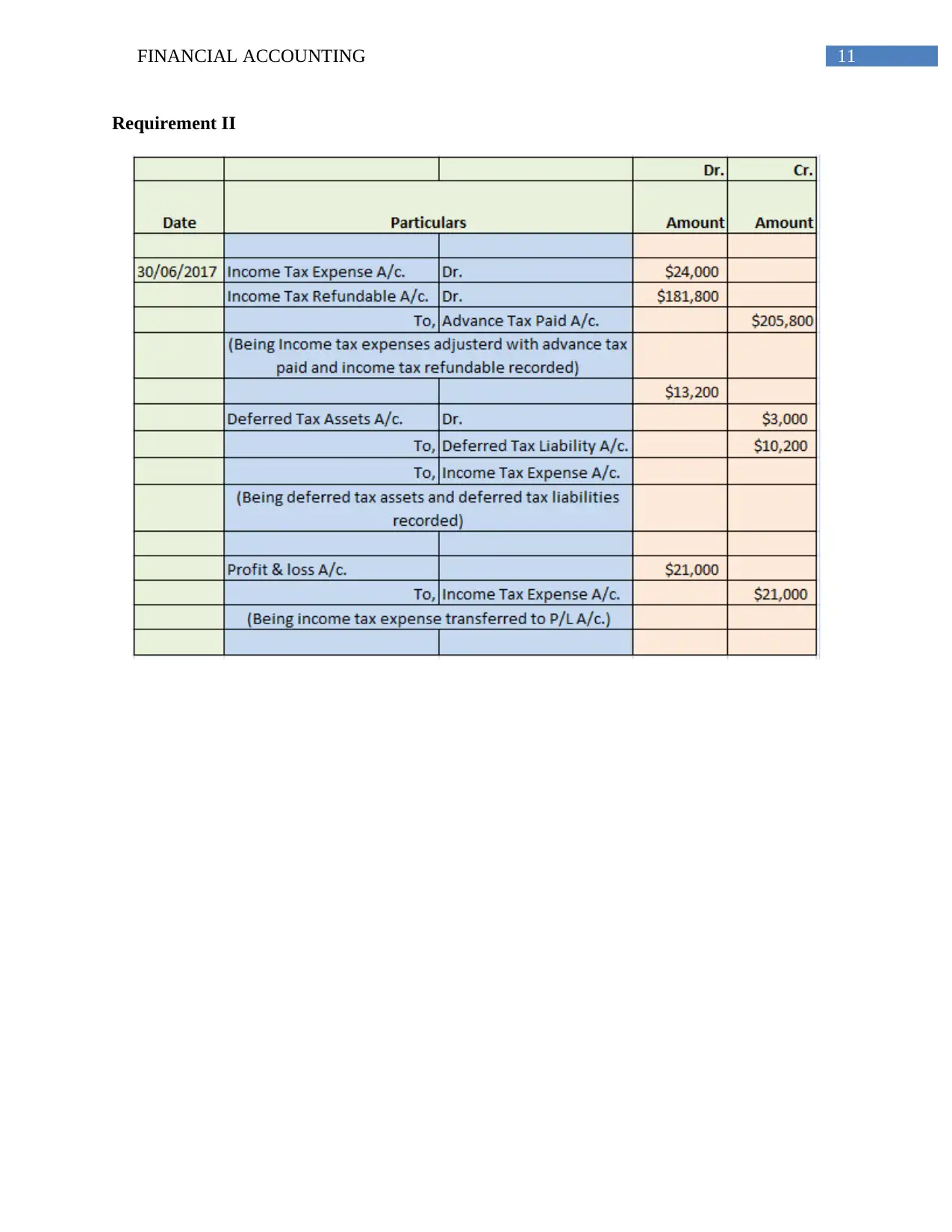

This financial accounting report analyzes the financial statements of ANZ Bank and Westpac Group, focusing on the application of International Accounting Standard Board (IASB) principles. The report evaluates the banks' compliance with disclosure requirements, including segment analysis, Basel regulations, and the presentation of Tier I and Tier II information. It highlights the importance of clear and entry-specific financial reporting, advocating for graphical presentations to aid investors in decision-making. The report provides recommendations to IASB, emphasizing the need for standardized formatting and comparable financial data, to enhance the communication effectiveness of financial information. The analysis covers specific areas where the banks either met or failed to meet the necessary disclosures, providing a comparative overview of their financial reporting practices. The report also includes working notes, journal entries, and references to support the findings and recommendations.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.