Financial Accounting Report: Purpose, Stakeholders, and Clients

VerifiedAdded on 2020/12/26

|25

|7840

|446

Report

AI Summary

This report delves into the realm of financial accounting, commencing with a comprehensive definition of the subject and an exploration of its fundamental purpose within business organizations. It meticulously outlines the significance of financial accounting, particularly in the context of large business entities and limited companies, emphasizing its role in reporting financial performance to stakeholders. The report then categorizes and elucidates the roles of both internal and external stakeholders, providing insights into their respective interests and influence. Furthermore, the document includes detailed journal entries and ledger accounts for multiple clients, offering practical examples of accounting procedures. The report touches upon key accounting concepts such as the double-entry system and the importance of financial statements. Overall, the report provides a practical overview of financial accounting principles and their application. The report also includes a discussion of the role of financial accounting in decision making and compliance with regulations.

Finance and Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

BUSINESS REPORT......................................................................................................................4

A. Financial Accounting and its purpose:..............................................................................4

B. Internal and external stakeholder:......................................................................................5

CLIENT 1........................................................................................................................................7

CLIENT 2......................................................................................................................................20

CLIENT 3......................................................................................................................................23

CLIENT 4......................................................................................................................................25

CLIENT 5......................................................................................................................................26

CONCLUSION..............................................................................................................................28

REFERENCES..............................................................................................................................29

INTRODUCTION...........................................................................................................................4

BUSINESS REPORT......................................................................................................................4

A. Financial Accounting and its purpose:..............................................................................4

B. Internal and external stakeholder:......................................................................................5

CLIENT 1........................................................................................................................................7

CLIENT 2......................................................................................................................................20

CLIENT 3......................................................................................................................................23

CLIENT 4......................................................................................................................................25

CLIENT 5......................................................................................................................................26

CONCLUSION..............................................................................................................................28

REFERENCES..............................................................................................................................29

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting refers to formation of final accounts of business organisation or

entity for internal or external stakeholders like investors, shareholders etc. on periodical basis.

Accounting includes a systematic summary and analysis of account and records of all inflow and

outflow of funds to and from business organization for a particular period. Financial accounting

process starts with recording of financial or accounting transactions and ends with finalisation of

accounts and reporting to various users of financial information (Ahn, Amiti and Weinstein,

2011). It assists business organisation to define its goals and objectives and ensure correct

decisions and future course of action based on previous performance of business organisation.

Relevance of financial accounting is more in case of large business organisations and limited

companies as compare to sole traders. Reporting is main feature of financial accounting which

helps to describe actual financial position and performance of business organisation in front of

different stakeholders. Mazars is small accounting firm based on UK is dealing in auditing, tax

advisory services. In addition, Mazars is a leading independent enterprise that is specialised in

providing tax advisory services. This report exhibits a complete definition of financial

accounting, purpose of financial accounting, internal or external stakeholders, purpose of control

accounts and bank reconciliation statement, explanation about term Imprest and suspense

account and its main features.

BUSINESS REPORT

A. Financial Accounting and its purpose:

Financial accounting is the process of accounting that includes summary, reporting of

financial transaction and analysing performance of business. Basically, it is an area of doing

business that focuses on internal and external users with useful information. In other words,

creditors and investors are known as external users because they help to make decision out of the

organisation by using company's financial information. Financial transaction states

systematically classification to prepare final accounts such as trading account, profit and loss

account or income statement, balance sheet, cash flow statement, change in equity statement and

other relevant statements that are using by any organisation to analysis actual financial

performance and situation of company (Archer, Ahmed and Sundararajan, 2010). In financial

accounting accounts are prepared by enterprises as per accounting principles (UK GAAP),

Financial accounting refers to formation of final accounts of business organisation or

entity for internal or external stakeholders like investors, shareholders etc. on periodical basis.

Accounting includes a systematic summary and analysis of account and records of all inflow and

outflow of funds to and from business organization for a particular period. Financial accounting

process starts with recording of financial or accounting transactions and ends with finalisation of

accounts and reporting to various users of financial information (Ahn, Amiti and Weinstein,

2011). It assists business organisation to define its goals and objectives and ensure correct

decisions and future course of action based on previous performance of business organisation.

Relevance of financial accounting is more in case of large business organisations and limited

companies as compare to sole traders. Reporting is main feature of financial accounting which

helps to describe actual financial position and performance of business organisation in front of

different stakeholders. Mazars is small accounting firm based on UK is dealing in auditing, tax

advisory services. In addition, Mazars is a leading independent enterprise that is specialised in

providing tax advisory services. This report exhibits a complete definition of financial

accounting, purpose of financial accounting, internal or external stakeholders, purpose of control

accounts and bank reconciliation statement, explanation about term Imprest and suspense

account and its main features.

BUSINESS REPORT

A. Financial Accounting and its purpose:

Financial accounting is the process of accounting that includes summary, reporting of

financial transaction and analysing performance of business. Basically, it is an area of doing

business that focuses on internal and external users with useful information. In other words,

creditors and investors are known as external users because they help to make decision out of the

organisation by using company's financial information. Financial transaction states

systematically classification to prepare final accounts such as trading account, profit and loss

account or income statement, balance sheet, cash flow statement, change in equity statement and

other relevant statements that are using by any organisation to analysis actual financial

performance and situation of company (Archer, Ahmed and Sundararajan, 2010). In financial

accounting accounts are prepared by enterprises as per accounting principles (UK GAAP),

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

guidelines, concept, convention and assumptions, that is administered and governed by

international and local guidelines and standards. Most considerable purpose of financial

accounting are as follows-

Financial accounting helps to create information or financial statements that may be used

by creditors and investors for making financial decisions.

It helps to maintain double entry system (debit and credit) by using financial information.

It helps to analysis the actual performance and position of business enterprises.

It makes sure about compliance of statuary requirements, structure, rules and regulations

and policies.

Financial information gives a comparative data and records that help to compare with

previous year data and perform effectively.

It helps to classification organisation's assets and liabilities in order to manage

profitability and efficiency.

Clear financial transaction and information helps to increase balances in organisation's

accounts.

It also helps to measures the events in monetary terms by using s transaction effects.

Its main purpose is taxation decision that is based on business assets or income, may be

derive from financial accounting information.

B. Internal and external stakeholder:

Stakeholders are an independent person or group of people that has an interest in an

organisation. In other words, any person, organisation and society who owns shares in a business

such as an employee, customer, or citizen that are connected with business activity. Stakeholders

are classified as internal and external stakeholders (Needles and Powers, 2010). Organisation

involves internal stakeholders such as individual or group of person whose having substantial

interest within the organisation, whereas external holders having direct or indirect interest

outside the business organisation.

Internal Stakeholder: These are entities or corporate body within a business that includes

managers, board of directors, investors, employees and managers. Following are the key

stakeholders, as follows:

Employees: Employees plays an important role at every place to formulate strategy and

other essential operation work. A big size of organisation considers employee opinions and their

international and local guidelines and standards. Most considerable purpose of financial

accounting are as follows-

Financial accounting helps to create information or financial statements that may be used

by creditors and investors for making financial decisions.

It helps to maintain double entry system (debit and credit) by using financial information.

It helps to analysis the actual performance and position of business enterprises.

It makes sure about compliance of statuary requirements, structure, rules and regulations

and policies.

Financial information gives a comparative data and records that help to compare with

previous year data and perform effectively.

It helps to classification organisation's assets and liabilities in order to manage

profitability and efficiency.

Clear financial transaction and information helps to increase balances in organisation's

accounts.

It also helps to measures the events in monetary terms by using s transaction effects.

Its main purpose is taxation decision that is based on business assets or income, may be

derive from financial accounting information.

B. Internal and external stakeholder:

Stakeholders are an independent person or group of people that has an interest in an

organisation. In other words, any person, organisation and society who owns shares in a business

such as an employee, customer, or citizen that are connected with business activity. Stakeholders

are classified as internal and external stakeholders (Needles and Powers, 2010). Organisation

involves internal stakeholders such as individual or group of person whose having substantial

interest within the organisation, whereas external holders having direct or indirect interest

outside the business organisation.

Internal Stakeholder: These are entities or corporate body within a business that includes

managers, board of directors, investors, employees and managers. Following are the key

stakeholders, as follows:

Employees: Employees plays an important role at every place to formulate strategy and

other essential operation work. A big size of organisation considers employee opinions and their

perception in formulating strategies. In an organisation employee means a person who has

specific job that is defined by job description and they work collectively. Employees are

interested in financial information because their salary, bonus, incentive and other employment

benefits are closely related with organisation's growth and performance. Employees are holding

stake in form of salary and career growth.

Owners or shareholders: Owners are the main pillar of any organisation who having

more substantial interest in form of shares held by them, voting rights, profits, dividend on shares

and making decisions. Owners are called real stakeholders of any entity because of holding

majority of shares. Owners or Shareholders are holding stake in organisation in form of

dividends or share in profits.

External stakeholders: These are entities or corporate body not within a business that includes

consumers, regulators, investors, government and suppliers. In other words, external

stakeholders are group of people outside a business who do not work within enterprises. These

are the major external stakeholder:

Government: Government get their share in an organisation's profit though taxes and

duties. Government is the system or group of person that regulates or governs an organised or

qualified community. It contains legislature, executive and judiciary that helps to make effective

decision. Each government has a kind of formation and legislation that helps in business related

policies and making financial statement such as taxation, VAT, truthful reporting, legalities,

externalities and legislations. Government is interested in financial information of entity to

(Dyreng and Lindsey, 2009).

Customers: Customers are essential external stakeholders in large size of business

organisation, that affects demands, supply and marketing strategies of business. It has an interest

in any organisation in the form of quality of product and services, price sensitiveness, brand

popularity, and availability of products. The main aim of any enterprises is to fulfils the need and

wants of their customers and provide maximum customer satisfaction.

Regulators: A regulator is an organisation or person that is appointed by government to

regulate and formulate an area of business activity like as manufacturing industry and banking. It

also involves a body that is used to control things such work speed of an organisation, production

activity and controlling the working rate of machinery in any business enterprises. Regulators are

specific job that is defined by job description and they work collectively. Employees are

interested in financial information because their salary, bonus, incentive and other employment

benefits are closely related with organisation's growth and performance. Employees are holding

stake in form of salary and career growth.

Owners or shareholders: Owners are the main pillar of any organisation who having

more substantial interest in form of shares held by them, voting rights, profits, dividend on shares

and making decisions. Owners are called real stakeholders of any entity because of holding

majority of shares. Owners or Shareholders are holding stake in organisation in form of

dividends or share in profits.

External stakeholders: These are entities or corporate body not within a business that includes

consumers, regulators, investors, government and suppliers. In other words, external

stakeholders are group of people outside a business who do not work within enterprises. These

are the major external stakeholder:

Government: Government get their share in an organisation's profit though taxes and

duties. Government is the system or group of person that regulates or governs an organised or

qualified community. It contains legislature, executive and judiciary that helps to make effective

decision. Each government has a kind of formation and legislation that helps in business related

policies and making financial statement such as taxation, VAT, truthful reporting, legalities,

externalities and legislations. Government is interested in financial information of entity to

(Dyreng and Lindsey, 2009).

Customers: Customers are essential external stakeholders in large size of business

organisation, that affects demands, supply and marketing strategies of business. It has an interest

in any organisation in the form of quality of product and services, price sensitiveness, brand

popularity, and availability of products. The main aim of any enterprises is to fulfils the need and

wants of their customers and provide maximum customer satisfaction.

Regulators: A regulator is an organisation or person that is appointed by government to

regulate and formulate an area of business activity like as manufacturing industry and banking. It

also involves a body that is used to control things such work speed of an organisation, production

activity and controlling the working rate of machinery in any business enterprises. Regulators are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

also interested in financial information because it helps to adopt restrictions and guidelines,

certain requirements and the integrity of financial system.

Investors: Investors means a person or group of person who invest their money or

deposits in order to receive return. It plays a vital role in any organisation for contributing in

growth and expansion of business by investing amount. Investors are affected by performance

and rating of any business organisation, hence they are actual stakeholders of any enterprises

who are always tries to make maximum return from investment made. It can use the information

to take decision whether to invest or not, and to develop a business organisation. Financial

information is very important for investors because it helps to take decision in further investment

in that company, interest payments and capital gains.

CLIENT 1

a. Journal Entries and Ledgers in the book of Alexandra Study:

Date Particulars..... Debit Credit

01/01/19 Premises A/c....................................................................Dr. 240000

Motor Van A/c.................................................................Dr. 51250

fixtures A/c................................................................ Dr. 8100

Inventory A/c................................................................ Dr. 23900

P Mole A/c................................................................ Dr. 4400

F Lane A/c................................................................ Dr. 6100

Bank A/c................................................................ Dr. 68400

Cash A/c................................................................ Dr. 15600

To S Hood A/c 12150

To J. Brown A/c 16600

To Capital A/c (Balancing Figure) 389000

(Being Owner's Capital is calculated )

Therefore, Alexandra Study's Capital at 1st January

= £ 389000

certain requirements and the integrity of financial system.

Investors: Investors means a person or group of person who invest their money or

deposits in order to receive return. It plays a vital role in any organisation for contributing in

growth and expansion of business by investing amount. Investors are affected by performance

and rating of any business organisation, hence they are actual stakeholders of any enterprises

who are always tries to make maximum return from investment made. It can use the information

to take decision whether to invest or not, and to develop a business organisation. Financial

information is very important for investors because it helps to take decision in further investment

in that company, interest payments and capital gains.

CLIENT 1

a. Journal Entries and Ledgers in the book of Alexandra Study:

Date Particulars..... Debit Credit

01/01/19 Premises A/c....................................................................Dr. 240000

Motor Van A/c.................................................................Dr. 51250

fixtures A/c................................................................ Dr. 8100

Inventory A/c................................................................ Dr. 23900

P Mole A/c................................................................ Dr. 4400

F Lane A/c................................................................ Dr. 6100

Bank A/c................................................................ Dr. 68400

Cash A/c................................................................ Dr. 15600

To S Hood A/c 12150

To J. Brown A/c 16600

To Capital A/c (Balancing Figure) 389000

(Being Owner's Capital is calculated )

Therefore, Alexandra Study's Capital at 1st January

= £ 389000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

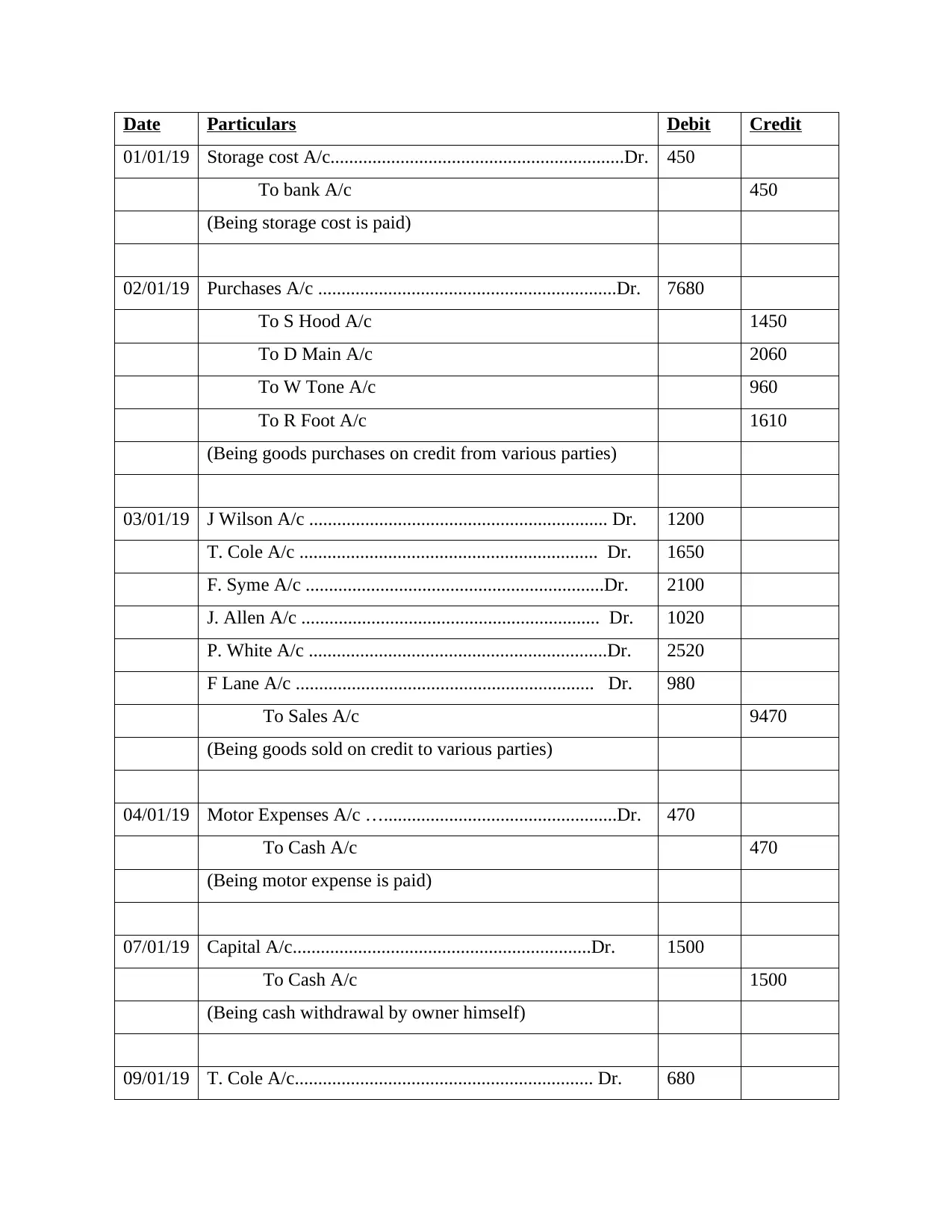

Date Particulars Debit Credit

01/01/19 Storage cost A/c...............................................................Dr. 450

To bank A/c 450

(Being storage cost is paid)

02/01/19 Purchases A/c ................................................................Dr. 7680

To S Hood A/c 1450

To D Main A/c 2060

To W Tone A/c 960

To R Foot A/c 1610

(Being goods purchases on credit from various parties)

03/01/19 J Wilson A/c ................................................................ Dr. 1200

T. Cole A/c ................................................................ Dr. 1650

F. Syme A/c ................................................................Dr. 2100

J. Allen A/c ................................................................ Dr. 1020

P. White A/c ................................................................Dr. 2520

F Lane A/c ................................................................ Dr. 980

To Sales A/c 9470

(Being goods sold on credit to various parties)

04/01/19 Motor Expenses A/c …..................................................Dr. 470

To Cash A/c 470

(Being motor expense is paid)

07/01/19 Capital A/c................................................................Dr. 1500

To Cash A/c 1500

(Being cash withdrawal by owner himself)

09/01/19 T. Cole A/c................................................................ Dr. 680

01/01/19 Storage cost A/c...............................................................Dr. 450

To bank A/c 450

(Being storage cost is paid)

02/01/19 Purchases A/c ................................................................Dr. 7680

To S Hood A/c 1450

To D Main A/c 2060

To W Tone A/c 960

To R Foot A/c 1610

(Being goods purchases on credit from various parties)

03/01/19 J Wilson A/c ................................................................ Dr. 1200

T. Cole A/c ................................................................ Dr. 1650

F. Syme A/c ................................................................Dr. 2100

J. Allen A/c ................................................................ Dr. 1020

P. White A/c ................................................................Dr. 2520

F Lane A/c ................................................................ Dr. 980

To Sales A/c 9470

(Being goods sold on credit to various parties)

04/01/19 Motor Expenses A/c …..................................................Dr. 470

To Cash A/c 470

(Being motor expense is paid)

07/01/19 Capital A/c................................................................Dr. 1500

To Cash A/c 1500

(Being cash withdrawal by owner himself)

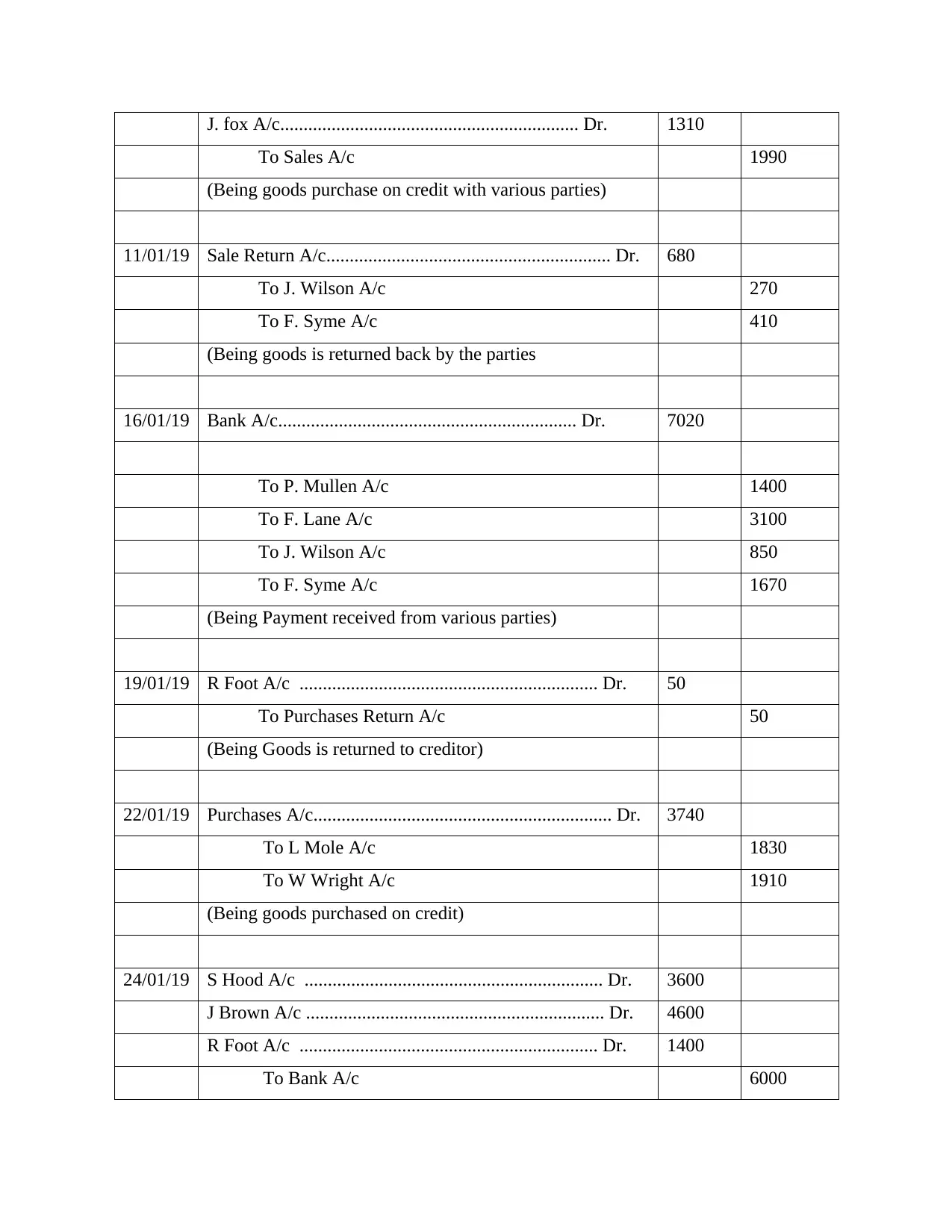

09/01/19 T. Cole A/c................................................................ Dr. 680

J. fox A/c................................................................ Dr. 1310

To Sales A/c 1990

(Being goods purchase on credit with various parties)

11/01/19 Sale Return A/c............................................................. Dr. 680

To J. Wilson A/c 270

To F. Syme A/c 410

(Being goods is returned back by the parties

16/01/19 Bank A/c................................................................ Dr. 7020

To P. Mullen A/c 1400

To F. Lane A/c 3100

To J. Wilson A/c 850

To F. Syme A/c 1670

(Being Payment received from various parties)

19/01/19 R Foot A/c ................................................................ Dr. 50

To Purchases Return A/c 50

(Being Goods is returned to creditor)

22/01/19 Purchases A/c................................................................ Dr. 3740

To L Mole A/c 1830

To W Wright A/c 1910

(Being goods purchased on credit)

24/01/19 S Hood A/c ................................................................ Dr. 3600

J Brown A/c ................................................................ Dr. 4600

R Foot A/c ................................................................ Dr. 1400

To Bank A/c 6000

To Sales A/c 1990

(Being goods purchase on credit with various parties)

11/01/19 Sale Return A/c............................................................. Dr. 680

To J. Wilson A/c 270

To F. Syme A/c 410

(Being goods is returned back by the parties

16/01/19 Bank A/c................................................................ Dr. 7020

To P. Mullen A/c 1400

To F. Lane A/c 3100

To J. Wilson A/c 850

To F. Syme A/c 1670

(Being Payment received from various parties)

19/01/19 R Foot A/c ................................................................ Dr. 50

To Purchases Return A/c 50

(Being Goods is returned to creditor)

22/01/19 Purchases A/c................................................................ Dr. 3740

To L Mole A/c 1830

To W Wright A/c 1910

(Being goods purchased on credit)

24/01/19 S Hood A/c ................................................................ Dr. 3600

J Brown A/c ................................................................ Dr. 4600

R Foot A/c ................................................................ Dr. 1400

To Bank A/c 6000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

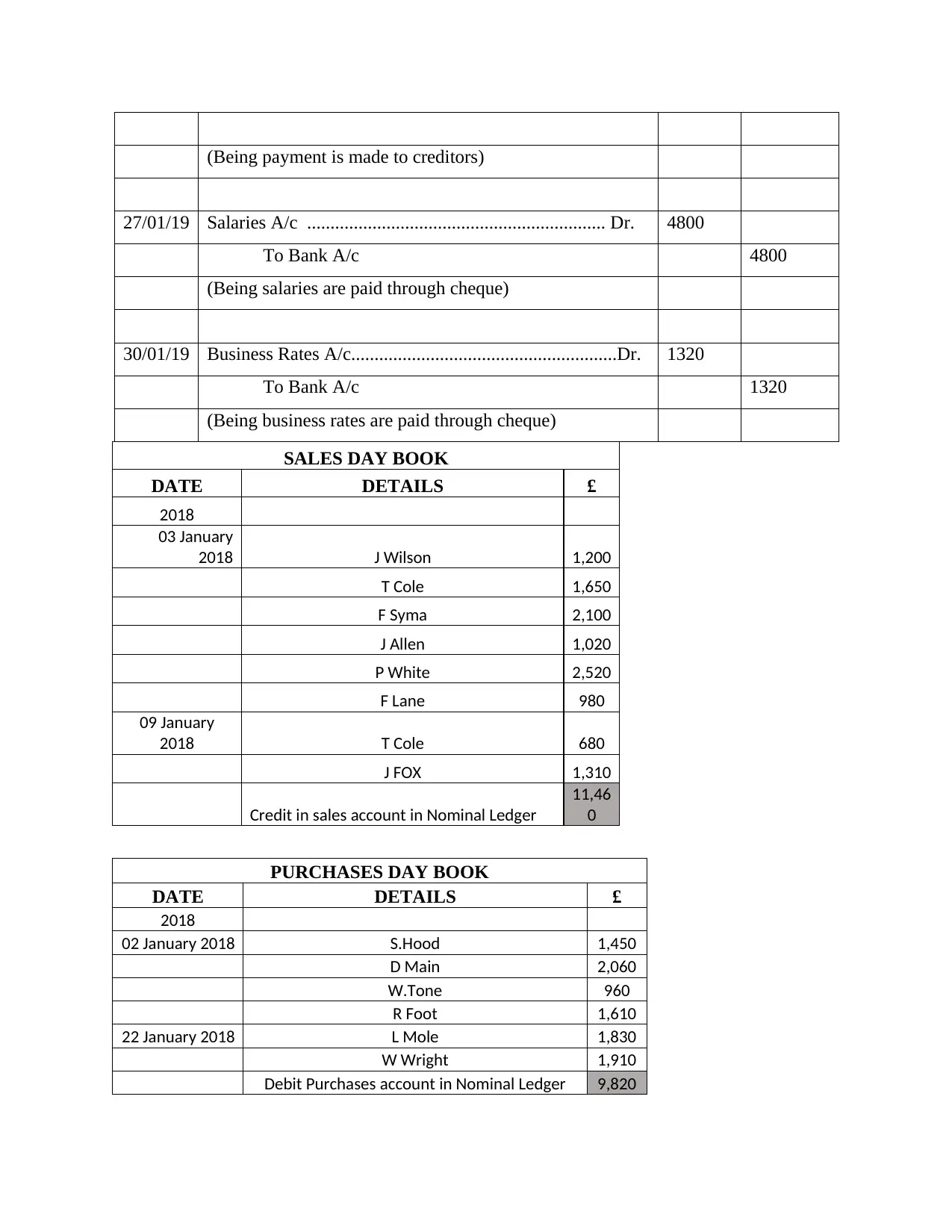

(Being payment is made to creditors)

27/01/19 Salaries A/c ................................................................ Dr. 4800

To Bank A/c 4800

(Being salaries are paid through cheque)

30/01/19 Business Rates A/c.........................................................Dr. 1320

To Bank A/c 1320

(Being business rates are paid through cheque)

SALES DAY BOOK

DATE DETAILS £

2018

03 January

2018 J Wilson 1,200

T Cole 1,650

F Syma 2,100

J Allen 1,020

P White 2,520

F Lane 980

09 January

2018 T Cole 680

J FOX 1,310

Credit in sales account in Nominal Ledger

11,46

0

PURCHASES DAY BOOK

DATE DETAILS £

2018

02 January 2018 S.Hood 1,450

D Main 2,060

W.Tone 960

R Foot 1,610

22 January 2018 L Mole 1,830

W Wright 1,910

Debit Purchases account in Nominal Ledger 9,820

27/01/19 Salaries A/c ................................................................ Dr. 4800

To Bank A/c 4800

(Being salaries are paid through cheque)

30/01/19 Business Rates A/c.........................................................Dr. 1320

To Bank A/c 1320

(Being business rates are paid through cheque)

SALES DAY BOOK

DATE DETAILS £

2018

03 January

2018 J Wilson 1,200

T Cole 1,650

F Syma 2,100

J Allen 1,020

P White 2,520

F Lane 980

09 January

2018 T Cole 680

J FOX 1,310

Credit in sales account in Nominal Ledger

11,46

0

PURCHASES DAY BOOK

DATE DETAILS £

2018

02 January 2018 S.Hood 1,450

D Main 2,060

W.Tone 960

R Foot 1,610

22 January 2018 L Mole 1,830

W Wright 1,910

Debit Purchases account in Nominal Ledger 9,820

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

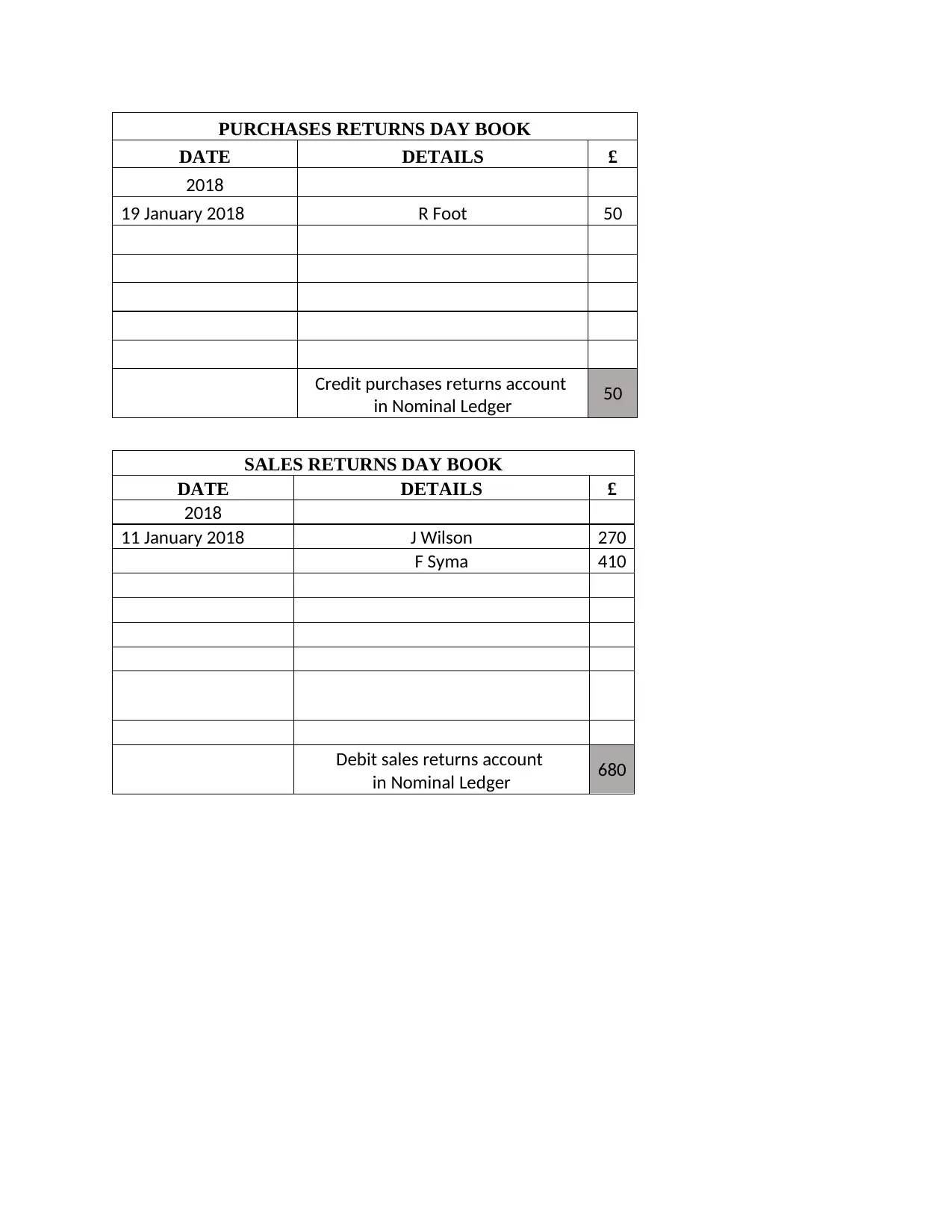

PURCHASES RETURNS DAY BOOK

DATE DETAILS £

2018

19 January 2018 R Foot 50

Credit purchases returns account

in Nominal Ledger 50

SALES RETURNS DAY BOOK

DATE DETAILS £

2018

11 January 2018 J Wilson 270

F Syma 410

Debit sales returns account

in Nominal Ledger 680

DATE DETAILS £

2018

19 January 2018 R Foot 50

Credit purchases returns account

in Nominal Ledger 50

SALES RETURNS DAY BOOK

DATE DETAILS £

2018

11 January 2018 J Wilson 270

F Syma 410

Debit sales returns account

in Nominal Ledger 680

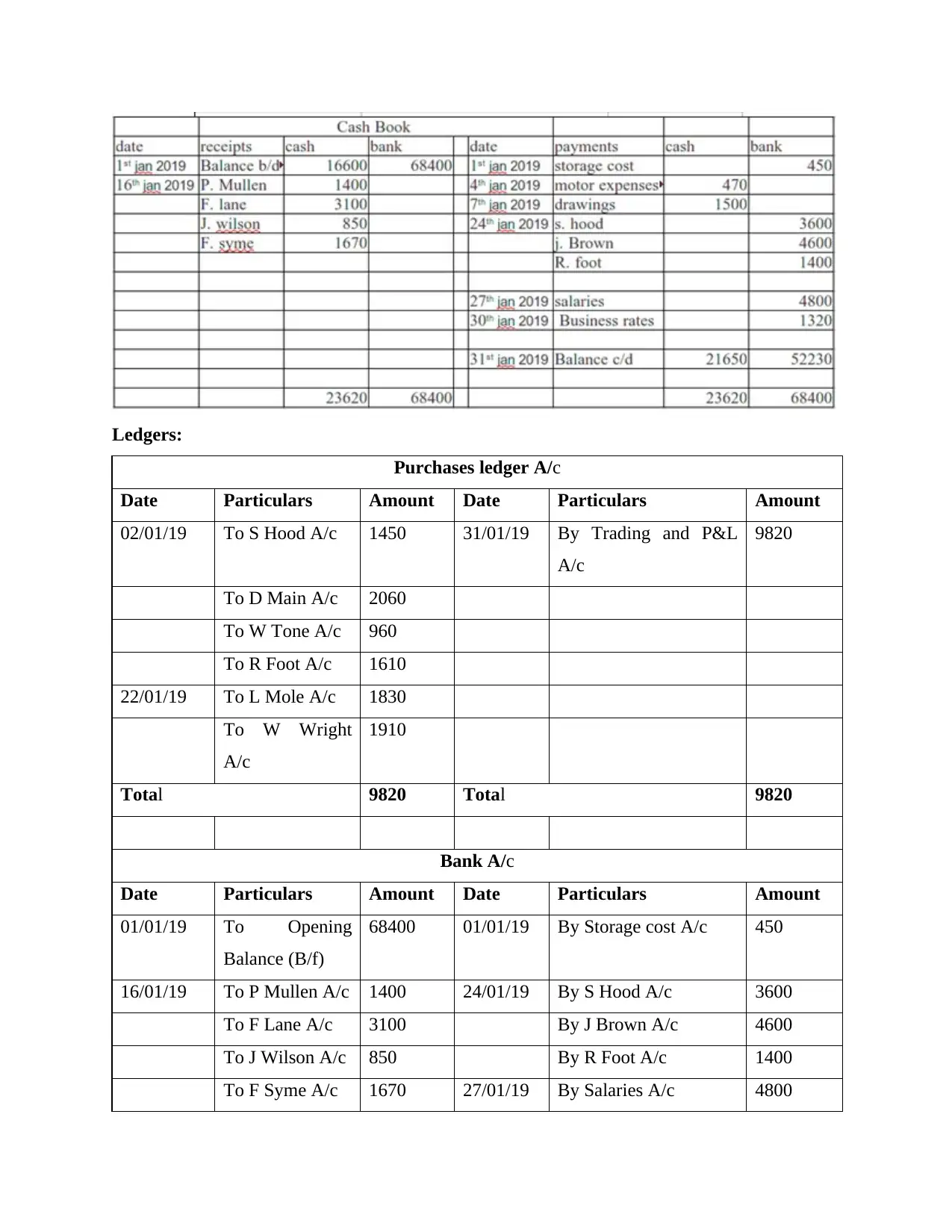

Ledgers:

Purchases ledger A/c

Date Particulars Amount Date Particulars Amount

02/01/19 To S Hood A/c 1450 31/01/19 By Trading and P&L

A/c

9820

To D Main A/c 2060

To W Tone A/c 960

To R Foot A/c 1610

22/01/19 To L Mole A/c 1830

To W Wright

A/c

1910

Total 9820 Total 9820

Bank A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

68400 01/01/19 By Storage cost A/c 450

16/01/19 To P Mullen A/c 1400 24/01/19 By S Hood A/c 3600

To F Lane A/c 3100 By J Brown A/c 4600

To J Wilson A/c 850 By R Foot A/c 1400

To F Syme A/c 1670 27/01/19 By Salaries A/c 4800

Purchases ledger A/c

Date Particulars Amount Date Particulars Amount

02/01/19 To S Hood A/c 1450 31/01/19 By Trading and P&L

A/c

9820

To D Main A/c 2060

To W Tone A/c 960

To R Foot A/c 1610

22/01/19 To L Mole A/c 1830

To W Wright

A/c

1910

Total 9820 Total 9820

Bank A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

68400 01/01/19 By Storage cost A/c 450

16/01/19 To P Mullen A/c 1400 24/01/19 By S Hood A/c 3600

To F Lane A/c 3100 By J Brown A/c 4600

To J Wilson A/c 850 By R Foot A/c 1400

To F Syme A/c 1670 27/01/19 By Salaries A/c 4800

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.