Financial Accounting Report: Legal and Regulatory Framework Impact

VerifiedAdded on 2020/01/28

|17

|5098

|327

Report

AI Summary

This report delves into the realm of financial accounting, dissecting the influence of legal and regulatory frameworks on the preparation and interpretation of financial statements. The report meticulously examines key components such as the Companies Act 2006, Generally Accepted Accounting Principles (GAAP), International Accounting Standards (IAS), and International Financial Reporting Standards (IFRS). It elucidates the implications of these frameworks for various users, including managers, employees, investors, and lenders, highlighting their respective information needs. Furthermore, the report addresses specific accounting tasks, including the impact of legal and regulatory frameworks on financial statements, and provides practical examples, such as the preparation of financial statements for Atlas plc and the impact of share issuance on financial metrics.

FINANCIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction................................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.2, 1.4 Influence of legal and regulatory framework on financial statements and

dealing....................................................................................................................................1

With the accounting and reporting standards.........................................................................1

AC 1.1, 1.2, 3.1 Implication of laws and regulatory framework for the different type of

users........................................................................................................................................4

And their information needs...................................................................................................4

TASK 2......................................................................................................................................6

PART B....................................................................................................................................10

A and B). Stating the operating profit for the year..............................................................10

c). Preparing the statement for the year ended 31st January 2011 for Atlas plc. In relation

to the assessment of financial performance.........................................................................11

d). Stating the impact on bank account, ordinary share capital and share premium when

Atlas plc issues 10 million ordinary shares at £1.5 per share..............................................12

CONCLUSION........................................................................................................................13

REFRENCES...........................................................................................................................14

Introduction................................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.2, 1.4 Influence of legal and regulatory framework on financial statements and

dealing....................................................................................................................................1

With the accounting and reporting standards.........................................................................1

AC 1.1, 1.2, 3.1 Implication of laws and regulatory framework for the different type of

users........................................................................................................................................4

And their information needs...................................................................................................4

TASK 2......................................................................................................................................6

PART B....................................................................................................................................10

A and B). Stating the operating profit for the year..............................................................10

c). Preparing the statement for the year ended 31st January 2011 for Atlas plc. In relation

to the assessment of financial performance.........................................................................11

d). Stating the impact on bank account, ordinary share capital and share premium when

Atlas plc issues 10 million ordinary shares at £1.5 per share..............................................12

CONCLUSION........................................................................................................................13

REFRENCES...........................................................................................................................14

INTRODUCTION

Every business organization needs to keep detailed record of all the operations. The

process of recording, classifying, summarizing and interpreting the financial information is

called financial accounting. The aim of this is to determine company's operational as well as

financial position. The present project report will discuss different legal and regulatory

framework for preparation of financial statements. The framework consists of different

accounting and reporting legislations and regulations in drafting company's accounts.

Company Act, 2006 and Partnership Act, 1890 imposed legal obligations to the businesses

while International financial reporting standard (IFRS), International Accounting Standards

(IAS), Generally Accepted Accounting Principles (GAAP) and Financial Reporting

Standards (FRS) comprises of all the regulatory framework of accounting and reporting.

Along with this, the report also explains the different internal and external users of financial

statement who make use of company's financial information and take decisions accordingly.

TASK 1

AC 1.2, 1.4 Influence of legal and regulatory framework on financial statements and dealing

With the accounting and reporting standards

Company Act, 2006: UK parliament formed CA, 2006 which govern all the UK

companies. UK company law covers 1300 sections and 16 schedules, came into force on

November, 2006. The act is applied to both private and public listed companies. It make

provisions regarding registrations, preparing necessary document such as MOA and AOA,

incorporation certificate, minimum share capital, directors duties, responsibilities and

liabilities, auditing of company's accounts, auditor's duties, shareholders information right

and so on. Section 386 of the act imposes legal restrictions on the organizations to keep

detailed and updated records of each and every accounting transaction (Arlbjørn and Freytag,

2012). Further, the section mentioned that the directors have to prepare required accounts in

compliance with the Article 4 of International Accounting standard (IAS). According to the

law, company have to maintain adequate records of business expenses, incomes, assets,

liabilities and inventories. Moreover, parent companies need to combine their subsidiaries

accounts and publish consolidated financial statement. In case when company do not

compliance with section 386, default officer can be penalised or imprisoned (Harun, Peursem

and Eggleton, 2012). Section 388 mentioned that companies have to kept records at their

registered office or at any other place which can be inspected by its officers. Section 393

described that directors must approve the financial statement about their truth and fair

1 | P a g e

Every business organization needs to keep detailed record of all the operations. The

process of recording, classifying, summarizing and interpreting the financial information is

called financial accounting. The aim of this is to determine company's operational as well as

financial position. The present project report will discuss different legal and regulatory

framework for preparation of financial statements. The framework consists of different

accounting and reporting legislations and regulations in drafting company's accounts.

Company Act, 2006 and Partnership Act, 1890 imposed legal obligations to the businesses

while International financial reporting standard (IFRS), International Accounting Standards

(IAS), Generally Accepted Accounting Principles (GAAP) and Financial Reporting

Standards (FRS) comprises of all the regulatory framework of accounting and reporting.

Along with this, the report also explains the different internal and external users of financial

statement who make use of company's financial information and take decisions accordingly.

TASK 1

AC 1.2, 1.4 Influence of legal and regulatory framework on financial statements and dealing

With the accounting and reporting standards

Company Act, 2006: UK parliament formed CA, 2006 which govern all the UK

companies. UK company law covers 1300 sections and 16 schedules, came into force on

November, 2006. The act is applied to both private and public listed companies. It make

provisions regarding registrations, preparing necessary document such as MOA and AOA,

incorporation certificate, minimum share capital, directors duties, responsibilities and

liabilities, auditing of company's accounts, auditor's duties, shareholders information right

and so on. Section 386 of the act imposes legal restrictions on the organizations to keep

detailed and updated records of each and every accounting transaction (Arlbjørn and Freytag,

2012). Further, the section mentioned that the directors have to prepare required accounts in

compliance with the Article 4 of International Accounting standard (IAS). According to the

law, company have to maintain adequate records of business expenses, incomes, assets,

liabilities and inventories. Moreover, parent companies need to combine their subsidiaries

accounts and publish consolidated financial statement. In case when company do not

compliance with section 386, default officer can be penalised or imprisoned (Harun, Peursem

and Eggleton, 2012). Section 388 mentioned that companies have to kept records at their

registered office or at any other place which can be inspected by its officers. Section 393

described that directors must approve the financial statement about their truth and fair

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

presentation. Furthermore, the act imposes legal obligations for publishing their audited

statements. Therefore, they need to appoint an independent auditor who can investigate

company's accounts and express his/her opinion by preparing qualified or unqualified report.

Section 395 described that company's accounts must be prepared in accordance with

applicable accounting framework and IAS. According to section 386 of the act, it is

compulsory for the accountants to prepare balance sheet and profit and loss account which

measure company's profits and financial status. (Gupta and Gunasekaran, 2005). The section

also imposes legal restrictions to use specific format and mention all the content in the

accounts. Moreover, additional information which has not been reflected by the statements

should be provided in the way of explanatory notes.

According to section 403, holding companies have to prepare their financial accounts

in compliance with article 4 of IAS regulations. Moreover, the standards will be consistently

followed in all the subsequent financial years. However, section 407 made provisions about

the reporting framework. As per the section, holding company directors must ensure that

parent and subsidiary company's accounts have been prepared using the same financial

reporting framework. Section 414 imposes legal liabilities on the board of directors to sign

and approve the financial statements (Nyamori, 2009). Section 495 of legislation is about the

auditor's report. According to this section, private company need to send auditor's report to

members while in case of public company, it must be presented in annual general meeting

(AGM).

Generally Accepted Accounting Standards (GAAP): These are the standard guidelines

which should be complied in preparation of company's accounts. It includes all the

accounting standards, rules, conventions and principles which should be strictly followed in

the process of financial accounting. It described the accounting procedure for recording,

classifying, summarizing and interpreting the financial statements. In UK, new GAAP came

into force on 1st January, 2015. UK FRC published four standards FRS 100, 101, 102 and 103

as new regime. FRS 100 is about the application of financial reporting requirement; FRS 101

is about reduced disclosure framework, FRS 102 is about interim reporting while FRS 103 is

applied on insurance contracts (Peursem, 2008). It makes changes in the disclosure,

measurement and transaction recognition.

International Accounting standards (IAS): International Accounting Standard

Committee (IASC) issued a number of IAS to record company's transactions in an

appropriate manner. IAS makes rules for recording various business affairs in the company's

2 | P a g e

statements. Therefore, they need to appoint an independent auditor who can investigate

company's accounts and express his/her opinion by preparing qualified or unqualified report.

Section 395 described that company's accounts must be prepared in accordance with

applicable accounting framework and IAS. According to section 386 of the act, it is

compulsory for the accountants to prepare balance sheet and profit and loss account which

measure company's profits and financial status. (Gupta and Gunasekaran, 2005). The section

also imposes legal restrictions to use specific format and mention all the content in the

accounts. Moreover, additional information which has not been reflected by the statements

should be provided in the way of explanatory notes.

According to section 403, holding companies have to prepare their financial accounts

in compliance with article 4 of IAS regulations. Moreover, the standards will be consistently

followed in all the subsequent financial years. However, section 407 made provisions about

the reporting framework. As per the section, holding company directors must ensure that

parent and subsidiary company's accounts have been prepared using the same financial

reporting framework. Section 414 imposes legal liabilities on the board of directors to sign

and approve the financial statements (Nyamori, 2009). Section 495 of legislation is about the

auditor's report. According to this section, private company need to send auditor's report to

members while in case of public company, it must be presented in annual general meeting

(AGM).

Generally Accepted Accounting Standards (GAAP): These are the standard guidelines

which should be complied in preparation of company's accounts. It includes all the

accounting standards, rules, conventions and principles which should be strictly followed in

the process of financial accounting. It described the accounting procedure for recording,

classifying, summarizing and interpreting the financial statements. In UK, new GAAP came

into force on 1st January, 2015. UK FRC published four standards FRS 100, 101, 102 and 103

as new regime. FRS 100 is about the application of financial reporting requirement; FRS 101

is about reduced disclosure framework, FRS 102 is about interim reporting while FRS 103 is

applied on insurance contracts (Peursem, 2008). It makes changes in the disclosure,

measurement and transaction recognition.

International Accounting standards (IAS): International Accounting Standard

Committee (IASC) issued a number of IAS to record company's transactions in an

appropriate manner. IAS makes rules for recording various business affairs in the company's

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial statements. Different IAS makes provisions for recording incomes, revenues, losses,

gains, assets, liabilities and capital. 41 IAS had been issued by IASC from time to time. It

make provisions about recording inventories, preparing consolidated statements,

depreciation, cash flows statements, construction contract, lease contract, revenues, employee

benefits, borrowing costs, effects of foreign exchange rates, investment in associates and joint

ventures, financial reporting, earning per share, interim reporting, assets impairment,

intangible assets, provisions, contingent liabilities and contingent assets, property, plant and

equipment and so on.

International Financial Reporting Standards (IFRS): It has been issued by

International Accounting Standard Board, shortened as IASB. These are mandatory and

globally accepted standards that make company's accounts understandable and comparable

across various continents. It described the way that how transactions will be reported in the

company's accounts (Sisaye and Birnberg, 2010). Different nations adopt different AS for

drafting their financial statements therefore, it cannot be understood easily by all the users.

However, following same standards by all the entrepreneurs makes accounts comparable,

reliable, understandable and relevant for all the users. The main purpose of IFRS is to provide

all the information about comp any's assets, liabilities, equity, incomes, expenditures, gains,

losses, owner's contribution and cash flows. Thus, IFRS makes international transactions

possible. The general features of IFRS comprises of going concern concept, fair presentation,

materiality concept, offsetting, reporting frequency, consistency and accrual accounting basis.

As per the going concern concept, accountant construct financial statements on the going

concern basis thus, managers do not assume that business will be liquidate in future years.

However, accrual basis described that transactions must be recorded at the time of their

occurrences whether received in cash or not while as per the materiality concept, all the

significant information must be shown in the statements. Furthermore, consistency approach

says that firms have to follow same AS over the period. It assists users in making

comparative analysis. Another, IFRS required that all the UK listed companies have to

prepare a complete set of financial statements (Zhao and et. al., 2013). It comprises of

balance sheet, profit and loss account, statement of changes in equity, retained earnings and

cash flows. Moreover, the adopted accounting policies, conventions, rules and other

transactions which not have been reflected by financial statements must be disclosed in notes

to accounting. Thus, it can be said that IFRS helps to provide reliable and faithful

presentation of company's affairs. Moreover, it improves comparability, verifiability,

3 | P a g e

gains, assets, liabilities and capital. 41 IAS had been issued by IASC from time to time. It

make provisions about recording inventories, preparing consolidated statements,

depreciation, cash flows statements, construction contract, lease contract, revenues, employee

benefits, borrowing costs, effects of foreign exchange rates, investment in associates and joint

ventures, financial reporting, earning per share, interim reporting, assets impairment,

intangible assets, provisions, contingent liabilities and contingent assets, property, plant and

equipment and so on.

International Financial Reporting Standards (IFRS): It has been issued by

International Accounting Standard Board, shortened as IASB. These are mandatory and

globally accepted standards that make company's accounts understandable and comparable

across various continents. It described the way that how transactions will be reported in the

company's accounts (Sisaye and Birnberg, 2010). Different nations adopt different AS for

drafting their financial statements therefore, it cannot be understood easily by all the users.

However, following same standards by all the entrepreneurs makes accounts comparable,

reliable, understandable and relevant for all the users. The main purpose of IFRS is to provide

all the information about comp any's assets, liabilities, equity, incomes, expenditures, gains,

losses, owner's contribution and cash flows. Thus, IFRS makes international transactions

possible. The general features of IFRS comprises of going concern concept, fair presentation,

materiality concept, offsetting, reporting frequency, consistency and accrual accounting basis.

As per the going concern concept, accountant construct financial statements on the going

concern basis thus, managers do not assume that business will be liquidate in future years.

However, accrual basis described that transactions must be recorded at the time of their

occurrences whether received in cash or not while as per the materiality concept, all the

significant information must be shown in the statements. Furthermore, consistency approach

says that firms have to follow same AS over the period. It assists users in making

comparative analysis. Another, IFRS required that all the UK listed companies have to

prepare a complete set of financial statements (Zhao and et. al., 2013). It comprises of

balance sheet, profit and loss account, statement of changes in equity, retained earnings and

cash flows. Moreover, the adopted accounting policies, conventions, rules and other

transactions which not have been reflected by financial statements must be disclosed in notes

to accounting. Thus, it can be said that IFRS helps to provide reliable and faithful

presentation of company's affairs. Moreover, it improves comparability, verifiability,

3 | P a g e

timeliness and understandability of company's accounts. In the present emerging market,

IFRS provide huge assistance to investors in gathering reliable information and taking

strategic investment decisions.

AC 1.1, 1.2, 3.1 Implication of laws and regulatory framework for the different type of users

And their information needs

There are two types of users that are internal and external users. Internal users are the

person who is the part of organization such as managers, employees and owners while

external users are outsiders includes competitors’, investors, lenders, creditors, suppliers,

government and others. They use financial statements to satisfy their information needs.

Different kind of users and their information needs are explained hereunder:

Managers: Managers are those who manage business operations, make policies and

take effective decisions. Use company's financial statements to measure business

performance. Through using profit and loss account, managers determine firms’ operational

result in terms of profit and loss (Islam and Dellaportas, 2011). They make in-depth analysis

of revenues and expenditures and make policies to enhance incomes and reduce cost. Board

of Directors and Managing Executives monitor business operating functions and make

effective control over the cost. In context to legal and regulatory framework, IAS for

revenues and expenditures such as depreciation, borrowing cost and income tax helps to

provide more reliable and correct financial information. Thus, proper analysis of the

statement helps managers to make strategic and competent policies. Moreover, they evaluate

firm’s cash generating capacity though using SOCF. Thus, applicable IAS 7 assist managers

to present all the necessary information which affect company's cash balance. It measure cash

sources and application from various operational, financing and investing activities.

Furthermore, they make evaluation of company's financial performance on the basis of

balance sheet. They measure business liquidity, solvency and efficiency ratios and take

decisions to enhance the performance (DeBondt and et. al., 2010). IAS for inventories,

propoerty, plant and equipment, investment, provisions, contingent liabilities, contingent

assets, impairment of assets, presentation of financial statement, lease contracts, intangible

assets, current assets and liabilities provide more consistent and reliable financial data helps

managers in their decision-making process.

Employees: Works are the essential part of the organizations as they give services to

the customers. Job security, better salary, bonus, increment, performance appraisal and other

non-monetary benefits are their objectives. Therefore, they assess company's profitability

4 | P a g e

IFRS provide huge assistance to investors in gathering reliable information and taking

strategic investment decisions.

AC 1.1, 1.2, 3.1 Implication of laws and regulatory framework for the different type of users

And their information needs

There are two types of users that are internal and external users. Internal users are the

person who is the part of organization such as managers, employees and owners while

external users are outsiders includes competitors’, investors, lenders, creditors, suppliers,

government and others. They use financial statements to satisfy their information needs.

Different kind of users and their information needs are explained hereunder:

Managers: Managers are those who manage business operations, make policies and

take effective decisions. Use company's financial statements to measure business

performance. Through using profit and loss account, managers determine firms’ operational

result in terms of profit and loss (Islam and Dellaportas, 2011). They make in-depth analysis

of revenues and expenditures and make policies to enhance incomes and reduce cost. Board

of Directors and Managing Executives monitor business operating functions and make

effective control over the cost. In context to legal and regulatory framework, IAS for

revenues and expenditures such as depreciation, borrowing cost and income tax helps to

provide more reliable and correct financial information. Thus, proper analysis of the

statement helps managers to make strategic and competent policies. Moreover, they evaluate

firm’s cash generating capacity though using SOCF. Thus, applicable IAS 7 assist managers

to present all the necessary information which affect company's cash balance. It measure cash

sources and application from various operational, financing and investing activities.

Furthermore, they make evaluation of company's financial performance on the basis of

balance sheet. They measure business liquidity, solvency and efficiency ratios and take

decisions to enhance the performance (DeBondt and et. al., 2010). IAS for inventories,

propoerty, plant and equipment, investment, provisions, contingent liabilities, contingent

assets, impairment of assets, presentation of financial statement, lease contracts, intangible

assets, current assets and liabilities provide more consistent and reliable financial data helps

managers in their decision-making process.

Employees: Works are the essential part of the organizations as they give services to

the customers. Job security, better salary, bonus, increment, performance appraisal and other

non-monetary benefits are their objectives. Therefore, they assess company's profitability

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

statement to measure business profits. Rising in profits indicate possibility of growth in

worker's salaries for FY henceforth, growth earning companies satisfy their employees and

vice versa. In accordance with the legislation and regulations, IAS 19 makes provisions for

employee benefits which can be used by workers to gather required information. Moreover,

companies who are performing well and have strong financial position will generate high

employee satisfaction.

Existed and potential investors: Current investors are those who invested their own funds

with the objective of getting maximum return on it. However, potential investors are those

who consider investing their funds in future period. Exiting investors make analysis of

business profits to ensure good return on investment. However, they analyse SOCF to

determine cash earning ability. Moreover, through using balance sheet, they evaluate

solvency position of the business and ensure safety of funds. However, potential investors

make use of company's published statement to predict future performance (Burns and et. al.,

2003). Risk reward relationship makes investors able to take qualitative decisions. UK

company law provide high information power to the shareholders. Moreover, published

audited financial statements provide reliable and authentic information to the investors.

Statements which have been constructed through adopting IAS provide detailed and updated

records of company's operation. Further, attending AGM and voting rights make shareholders

able to take part in company's management. Thus, they can assess operational hazards and

evaluate manager's effectiveness. In addition to it, IFRS provide huge assistance to investors

who undertake to invest in distinct lands. The reason behind this is it provides convenience to

compare the financial statement of different organizations.

Lenders: They provide funds to the businesses at an interest rate. They need information

about company's profitability, cash generating ability, solvency and interest bearing capacity.

Thus, profit and loss account provides information about business revenues and profits.

Moreover, through using profitability statement, lenders assess the interest bearing capacity.

It measures that how much business is able to bear fixed financial burden in terms of interest

out of its available profits (chaltegger, Bennett and Burrit, 2006). SOCF has been used to

determine business ability to pay interest loan on time hence, high cash earning companies

will be able to generate funds through borrowings. Moreover, they make analysis of balance

sheet to identify the capital structure. They evaluate solvency position and ensure their funds

safety and security. In accordance with legislation and regulatory framework, IAS 7 for

preparation of SOCF will assist lenders to measure assets net realisable value. Moreover,

5 | P a g e

worker's salaries for FY henceforth, growth earning companies satisfy their employees and

vice versa. In accordance with the legislation and regulations, IAS 19 makes provisions for

employee benefits which can be used by workers to gather required information. Moreover,

companies who are performing well and have strong financial position will generate high

employee satisfaction.

Existed and potential investors: Current investors are those who invested their own funds

with the objective of getting maximum return on it. However, potential investors are those

who consider investing their funds in future period. Exiting investors make analysis of

business profits to ensure good return on investment. However, they analyse SOCF to

determine cash earning ability. Moreover, through using balance sheet, they evaluate

solvency position of the business and ensure safety of funds. However, potential investors

make use of company's published statement to predict future performance (Burns and et. al.,

2003). Risk reward relationship makes investors able to take qualitative decisions. UK

company law provide high information power to the shareholders. Moreover, published

audited financial statements provide reliable and authentic information to the investors.

Statements which have been constructed through adopting IAS provide detailed and updated

records of company's operation. Further, attending AGM and voting rights make shareholders

able to take part in company's management. Thus, they can assess operational hazards and

evaluate manager's effectiveness. In addition to it, IFRS provide huge assistance to investors

who undertake to invest in distinct lands. The reason behind this is it provides convenience to

compare the financial statement of different organizations.

Lenders: They provide funds to the businesses at an interest rate. They need information

about company's profitability, cash generating ability, solvency and interest bearing capacity.

Thus, profit and loss account provides information about business revenues and profits.

Moreover, through using profitability statement, lenders assess the interest bearing capacity.

It measures that how much business is able to bear fixed financial burden in terms of interest

out of its available profits (chaltegger, Bennett and Burrit, 2006). SOCF has been used to

determine business ability to pay interest loan on time hence, high cash earning companies

will be able to generate funds through borrowings. Moreover, they make analysis of balance

sheet to identify the capital structure. They evaluate solvency position and ensure their funds

safety and security. In accordance with legislation and regulatory framework, IAS 7 for

preparation of SOCF will assist lenders to measure assets net realisable value. Moreover,

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting and reporting framework for presentation and preparation of financial statements

assist lenders in generating all the information about company's affairs. On contrary, IAS 23

make provisions for recording borrowings cost. The form, content and structure of company's

accounts provide prominent and updated information and satisfy their information need.

Creditors: They provide goods on credit and need information about credit worthiness and

operational performance. They access and analyse profits though using profitability statement

whilst balance sheet provide assistance to measure liquidity position (Hill, 2003). They

measure company's ability to pay short-term liabilities by evaluating current assets, inventory

and current liabilities. IAS 2, IAS 13 and IAS 18 make provisions for recording inventories,

CA, CL and revenues and provide authentic information. Better operational performance,

cash earning ability and liquidity will be able to attract creditors to the organizations.

Moreover, companies will be able to extent their credit terms.

Government: They collect tax revenues on the business profits. Thus, need information about

profit and loss account and growth of different sectors. Government determine firm's tax

obligations and match it with the paid taxes (Unhaenf, 2000). In case of any default,

government charge penalties and other kind of law suits. IAS 12 applied for recording

income taxes henceforth, it provides correct information to government. Furthermore,

government assess growth of different industries through analysing the audited financial

statements. It provides assistance to make better policies for economic growth and

development.

TASK 2

Capital 17000

Motor van 18000

Display equipment 4000

Trade payables 4460

Bank overdraft 1100

Sales 97300

Rent- Stall licenses 18900

Insurance 4040

Motor expenses 3150

6 | P a g e

assist lenders in generating all the information about company's affairs. On contrary, IAS 23

make provisions for recording borrowings cost. The form, content and structure of company's

accounts provide prominent and updated information and satisfy their information need.

Creditors: They provide goods on credit and need information about credit worthiness and

operational performance. They access and analyse profits though using profitability statement

whilst balance sheet provide assistance to measure liquidity position (Hill, 2003). They

measure company's ability to pay short-term liabilities by evaluating current assets, inventory

and current liabilities. IAS 2, IAS 13 and IAS 18 make provisions for recording inventories,

CA, CL and revenues and provide authentic information. Better operational performance,

cash earning ability and liquidity will be able to attract creditors to the organizations.

Moreover, companies will be able to extent their credit terms.

Government: They collect tax revenues on the business profits. Thus, need information about

profit and loss account and growth of different sectors. Government determine firm's tax

obligations and match it with the paid taxes (Unhaenf, 2000). In case of any default,

government charge penalties and other kind of law suits. IAS 12 applied for recording

income taxes henceforth, it provides correct information to government. Furthermore,

government assess growth of different industries through analysing the audited financial

statements. It provides assistance to make better policies for economic growth and

development.

TASK 2

Capital 17000

Motor van 18000

Display equipment 4000

Trade payables 4460

Bank overdraft 1100

Sales 97300

Rent- Stall licenses 18900

Insurance 4040

Motor expenses 3150

6 | P a g e

Other expenses 2750

Drawings 14880

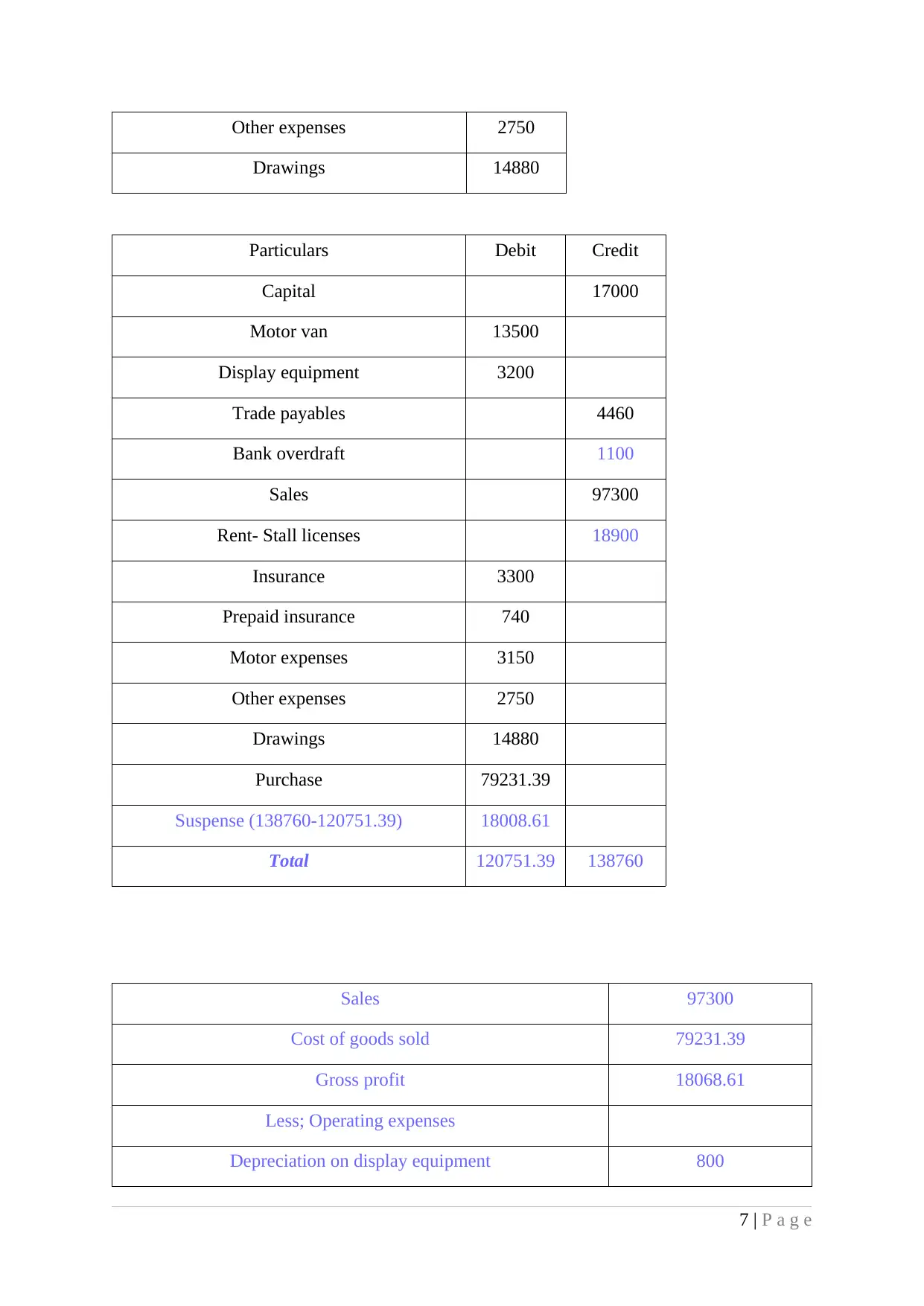

Particulars Debit Credit

Capital 17000

Motor van 13500

Display equipment 3200

Trade payables 4460

Bank overdraft 1100

Sales 97300

Rent- Stall licenses 18900

Insurance 3300

Prepaid insurance 740

Motor expenses 3150

Other expenses 2750

Drawings 14880

Purchase 79231.39

Suspense (138760-120751.39) 18008.61

Total 120751.39 138760

Sales 97300

Cost of goods sold 79231.39

Gross profit 18068.61

Less; Operating expenses

Depreciation on display equipment 800

7 | P a g e

Drawings 14880

Particulars Debit Credit

Capital 17000

Motor van 13500

Display equipment 3200

Trade payables 4460

Bank overdraft 1100

Sales 97300

Rent- Stall licenses 18900

Insurance 3300

Prepaid insurance 740

Motor expenses 3150

Other expenses 2750

Drawings 14880

Purchase 79231.39

Suspense (138760-120751.39) 18008.61

Total 120751.39 138760

Sales 97300

Cost of goods sold 79231.39

Gross profit 18068.61

Less; Operating expenses

Depreciation on display equipment 800

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

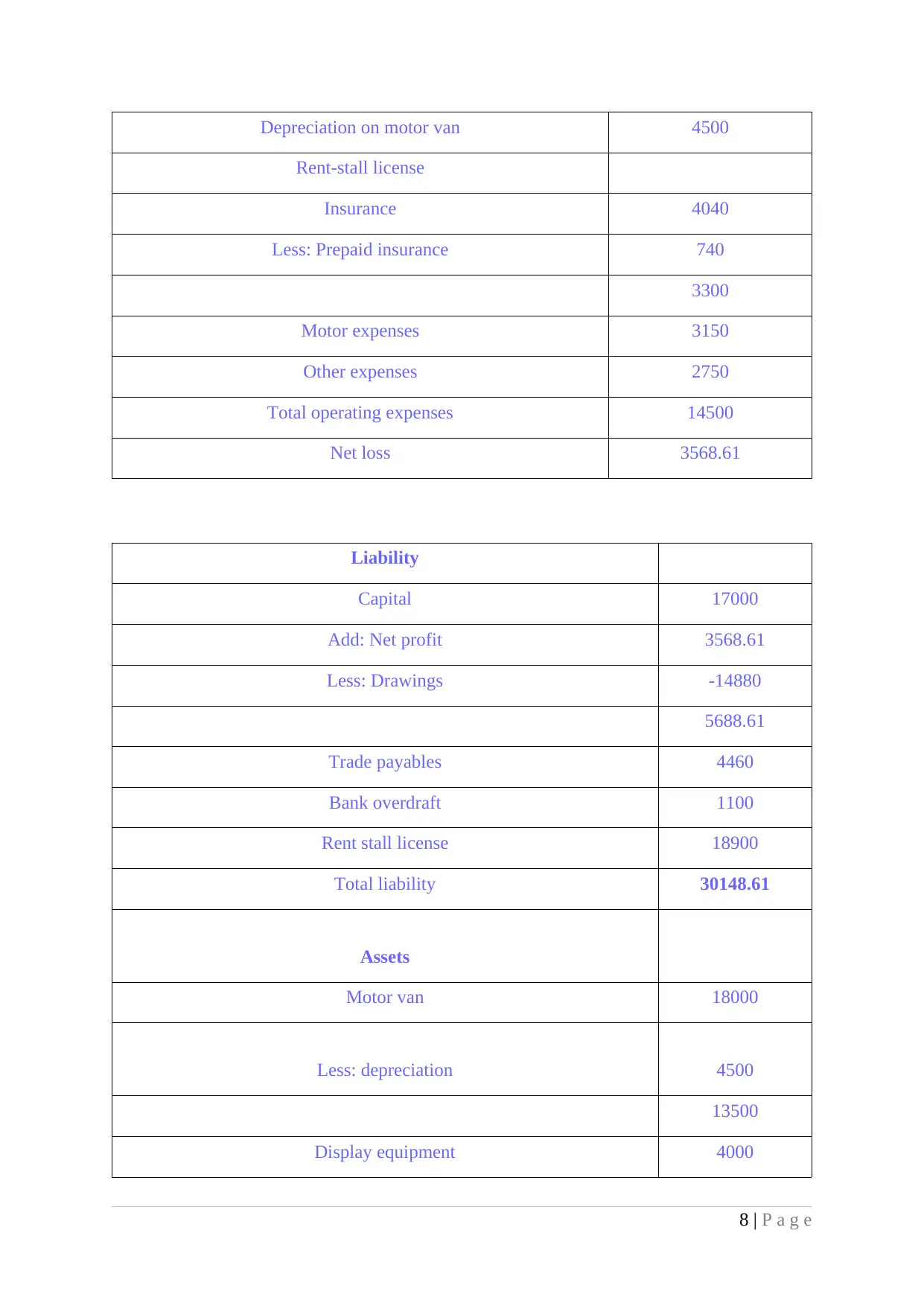

Depreciation on motor van 4500

Rent-stall license

Insurance 4040

Less: Prepaid insurance 740

3300

Motor expenses 3150

Other expenses 2750

Total operating expenses 14500

Net loss 3568.61

Liability

Capital 17000

Add: Net profit 3568.61

Less: Drawings -14880

5688.61

Trade payables 4460

Bank overdraft 1100

Rent stall license 18900

Total liability 30148.61

Assets

Motor van 18000

Less: depreciation 4500

13500

Display equipment 4000

8 | P a g e

Rent-stall license

Insurance 4040

Less: Prepaid insurance 740

3300

Motor expenses 3150

Other expenses 2750

Total operating expenses 14500

Net loss 3568.61

Liability

Capital 17000

Add: Net profit 3568.61

Less: Drawings -14880

5688.61

Trade payables 4460

Bank overdraft 1100

Rent stall license 18900

Total liability 30148.61

Assets

Motor van 18000

Less: depreciation 4500

13500

Display equipment 4000

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

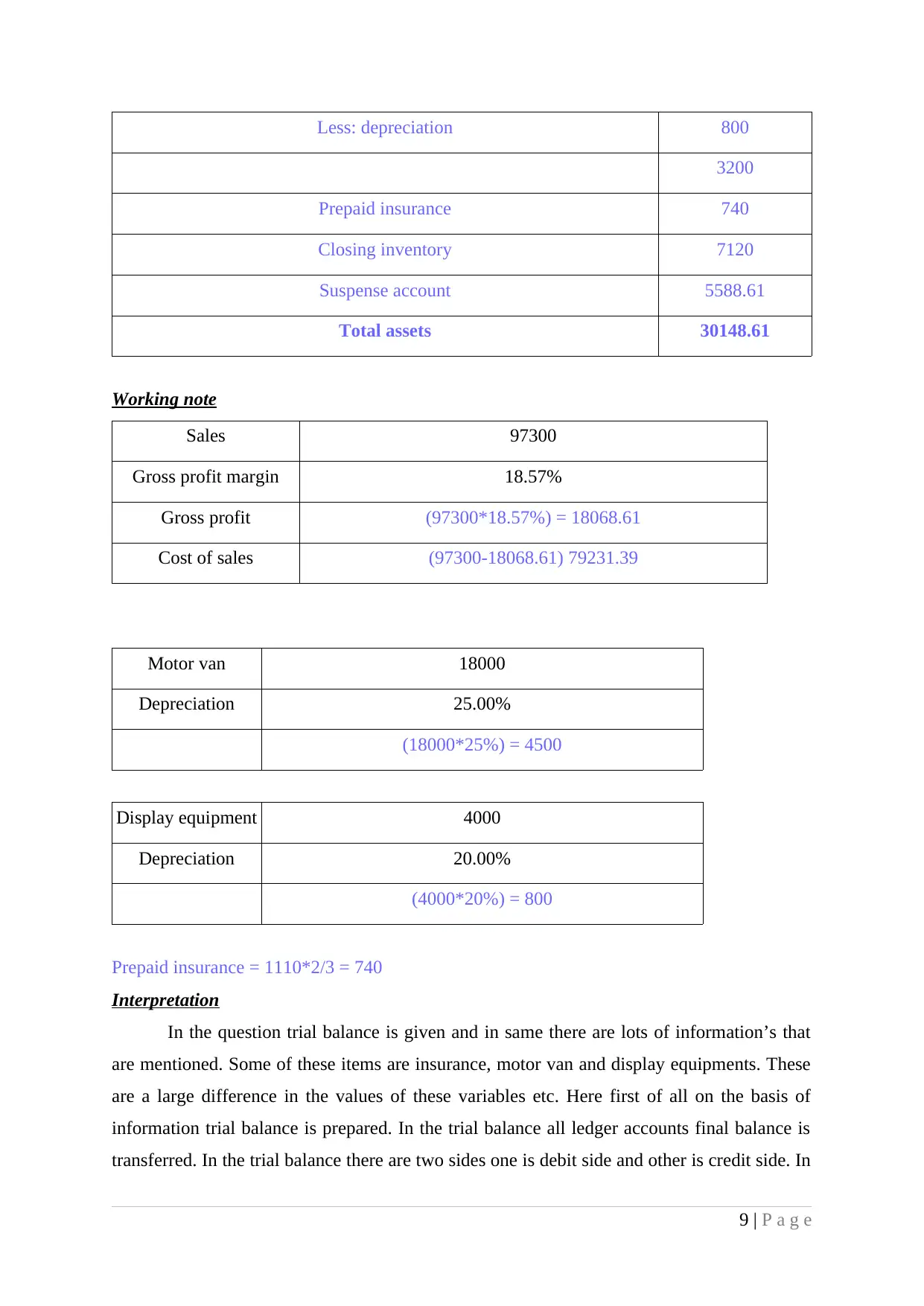

Less: depreciation 800

3200

Prepaid insurance 740

Closing inventory 7120

Suspense account 5588.61

Total assets 30148.61

Working note

Sales 97300

Gross profit margin 18.57%

Gross profit (97300*18.57%) = 18068.61

Cost of sales (97300-18068.61) 79231.39

Motor van 18000

Depreciation 25.00%

(18000*25%) = 4500

Display equipment 4000

Depreciation 20.00%

(4000*20%) = 800

Prepaid insurance = 1110*2/3 = 740

Interpretation

In the question trial balance is given and in same there are lots of information’s that

are mentioned. Some of these items are insurance, motor van and display equipments. These

are a large difference in the values of these variables etc. Here first of all on the basis of

information trial balance is prepared. In the trial balance all ledger accounts final balance is

transferred. In the trial balance there are two sides one is debit side and other is credit side. In

9 | P a g e

3200

Prepaid insurance 740

Closing inventory 7120

Suspense account 5588.61

Total assets 30148.61

Working note

Sales 97300

Gross profit margin 18.57%

Gross profit (97300*18.57%) = 18068.61

Cost of sales (97300-18068.61) 79231.39

Motor van 18000

Depreciation 25.00%

(18000*25%) = 4500

Display equipment 4000

Depreciation 20.00%

(4000*20%) = 800

Prepaid insurance = 1110*2/3 = 740

Interpretation

In the question trial balance is given and in same there are lots of information’s that

are mentioned. Some of these items are insurance, motor van and display equipments. These

are a large difference in the values of these variables etc. Here first of all on the basis of

information trial balance is prepared. In the trial balance all ledger accounts final balance is

transferred. In the trial balance there are two sides one is debit side and other is credit side. In

9 | P a g e

the debit side of the account all expenses are recorded. Whereas, on credit side of the balance

sheet all incomes are recorded. In case of assets and liabilities case is different because in this

case assets are shown in the assets side of the balance sheet. Whereas, liabilities are shown in

the credit side of the balance sheet. Hence, it can be said that the way of showing assets and

liability as well as income and expenditure is different in the trial balance. By following this

principle all expenses like insurance, motor expenses and other expenses etc are recorded in

the debit side of the trial balance. On other hand, all incomes are recorded at the credit side of

the balance sheet. In this regard sales are shown in the credit side of the trial balance. After

that assets and liabilities are shown in the trial balance. All assets are shown in the debit

side of the balance sheet. These assets are motor van and display equipments. Apart from

this, there were liabilities which include bank overdraft and trade payables etc. These values

are recorded in the assets side of the balance sheet. While preparing an account there was

some deficit in the balance and this comes in existence because some of the accounting

information’s were not available. In this way trial balance was prepared and balance were

matched with each other.

After preparing a trial balance income statement was prepared. Income statement is a

statement which provides information about the income and expenditures of an organization

during an accounting year. These expenses are recorded in the debit side of the income

statement. All those expenses that are done in day to day business are recorded in the income

statement. These expenses include office expenses, sales and distribution expenses and other

expenses. In the financial statement all expenses are recorded in proper manner.

After preparing an income statement balance sheet is prepared and in this statement

all assets and liabilities are recorded in proper manner (John, 2012). On the basis of trial

balance sheet is prepared. All things are arranged in systematic manner and due to this reason

balance of assets and liabilities are same. Net profit of the firm is negative and due to this

reason it is deducted from the capital section of the liability side of the balance sheet. Motor

van, display equipments and prep paid expenses are some of the assets that are on the assets

side of the balance sheet. After preparing a balance sheet working notes are attached and in

this some of the calculations are shown. In first working note cost of sales is computed and

under this gross profit margin on sales is computed by calculating percentage of sales that is

covered by the gross profit. After computing gross profit the calculated value is deducted

from the sales amount. In this way purchase value is calculated. The last working note is

related to the computation of depreciation. In this depreciation on motor vehicle is computed.

10 | P a g e

sheet all incomes are recorded. In case of assets and liabilities case is different because in this

case assets are shown in the assets side of the balance sheet. Whereas, liabilities are shown in

the credit side of the balance sheet. Hence, it can be said that the way of showing assets and

liability as well as income and expenditure is different in the trial balance. By following this

principle all expenses like insurance, motor expenses and other expenses etc are recorded in

the debit side of the trial balance. On other hand, all incomes are recorded at the credit side of

the balance sheet. In this regard sales are shown in the credit side of the trial balance. After

that assets and liabilities are shown in the trial balance. All assets are shown in the debit

side of the balance sheet. These assets are motor van and display equipments. Apart from

this, there were liabilities which include bank overdraft and trade payables etc. These values

are recorded in the assets side of the balance sheet. While preparing an account there was

some deficit in the balance and this comes in existence because some of the accounting

information’s were not available. In this way trial balance was prepared and balance were

matched with each other.

After preparing a trial balance income statement was prepared. Income statement is a

statement which provides information about the income and expenditures of an organization

during an accounting year. These expenses are recorded in the debit side of the income

statement. All those expenses that are done in day to day business are recorded in the income

statement. These expenses include office expenses, sales and distribution expenses and other

expenses. In the financial statement all expenses are recorded in proper manner.

After preparing an income statement balance sheet is prepared and in this statement

all assets and liabilities are recorded in proper manner (John, 2012). On the basis of trial

balance sheet is prepared. All things are arranged in systematic manner and due to this reason

balance of assets and liabilities are same. Net profit of the firm is negative and due to this

reason it is deducted from the capital section of the liability side of the balance sheet. Motor

van, display equipments and prep paid expenses are some of the assets that are on the assets

side of the balance sheet. After preparing a balance sheet working notes are attached and in

this some of the calculations are shown. In first working note cost of sales is computed and

under this gross profit margin on sales is computed by calculating percentage of sales that is

covered by the gross profit. After computing gross profit the calculated value is deducted

from the sales amount. In this way purchase value is calculated. The last working note is

related to the computation of depreciation. In this depreciation on motor vehicle is computed.

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.