Financial Accounting Report: Principles, Statements, and Application

VerifiedAdded on 2020/06/06

|44

|4858

|52

Report

AI Summary

This report provides a comprehensive overview of financial accounting, focusing on the preparation of financial statements such as the balance sheet, income statement, and cash flow statement. It begins with an introduction to financial accounting and its importance, followed by a detailed discussion of accounting principles and concepts, including the roles of professional bodies like the FRC, IASB, and IFRS, and the application of GAAP rules. The report emphasizes the significance of financial accounting for stakeholders' decision-making. It covers topics such as journal entries, ledger accounts, trial balance preparation, and the application of accounting concepts like consistency, prudence, and materiality. Furthermore, the report includes examples of bank statements, cash books, and reconciliation processes. The report highlights the importance of preparing financial statements in compliance with accounting principles and regulations and provides a practical guide to various financial accounting aspects.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A. Preparation of report for Line Manager on accounting principles....................................1

CLIENT 1........................................................................................................................................6

1. Journal entries for firm.......................................................................................................6

2. Preparation of ledger accounts...........................................................................................6

3. Producing trial balance.......................................................................................................6

M1. Transaction of purchase and sale to prepare trial balance..............................................6

D1. Producing trial balance by using accounting concepts....................................................6

CLIENT 2........................................................................................................................................7

A Preparation of Income statement for the organisation........................................................7

B Statement of financial position for Peter Piper organisation..............................................7

CLIENT 3........................................................................................................................................7

A Income statement for Raintree organisation.......................................................................7

B Statement of financial position for organisation.................................................................7

C Consistency and Prudence concept.....................................................................................8

D Highlighting purpose of deprecation and methods of charging deprecation......................8

M2 P&L account, balance sheet and cash flow statement.....................................................9

D2 Preparation of the financial statements.............................................................................9

CLIENT 4........................................................................................................................................9

A Bank statement...................................................................................................................9

B Outlining causes of recording bank statements..................................................................9

C. Cash books.........................................................................................................................9

M3 Reconciliation process and relevant terms.......................................................................9

D3 Producing BRS.................................................................................................................9

CLIENT 5........................................................................................................................................9

A Sales and purchase ledger account for Henderson.............................................................9

B. Control account................................................................................................................10

CLIENT 6......................................................................................................................................10

A Suspense account and highlighting features of the same.................................................10

INTRODUCTION...........................................................................................................................1

A. Preparation of report for Line Manager on accounting principles....................................1

CLIENT 1........................................................................................................................................6

1. Journal entries for firm.......................................................................................................6

2. Preparation of ledger accounts...........................................................................................6

3. Producing trial balance.......................................................................................................6

M1. Transaction of purchase and sale to prepare trial balance..............................................6

D1. Producing trial balance by using accounting concepts....................................................6

CLIENT 2........................................................................................................................................7

A Preparation of Income statement for the organisation........................................................7

B Statement of financial position for Peter Piper organisation..............................................7

CLIENT 3........................................................................................................................................7

A Income statement for Raintree organisation.......................................................................7

B Statement of financial position for organisation.................................................................7

C Consistency and Prudence concept.....................................................................................8

D Highlighting purpose of deprecation and methods of charging deprecation......................8

M2 P&L account, balance sheet and cash flow statement.....................................................9

D2 Preparation of the financial statements.............................................................................9

CLIENT 4........................................................................................................................................9

A Bank statement...................................................................................................................9

B Outlining causes of recording bank statements..................................................................9

C. Cash books.........................................................................................................................9

M3 Reconciliation process and relevant terms.......................................................................9

D3 Producing BRS.................................................................................................................9

CLIENT 5........................................................................................................................................9

A Sales and purchase ledger account for Henderson.............................................................9

B. Control account................................................................................................................10

CLIENT 6......................................................................................................................................10

A Suspense account and highlighting features of the same.................................................10

B. Trial balance....................................................................................................................10

C. Constructing journal entries.............................................................................................10

D. Distinguishing clearing and suspense account................................................................10

M4 Various types of accounts and reconciliation................................................................10

D4 Outlining accounting methods for firm..........................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................10

C. Constructing journal entries.............................................................................................10

D. Distinguishing clearing and suspense account................................................................10

M4 Various types of accounts and reconciliation................................................................10

D4 Outlining accounting methods for firm..........................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is the main branch of accounting which helps in preparation of

various financial statements such as balance sheet, income statement, cash flow statement and

statement of changes in equity. These statements are required to be prepared by complying with

the provisions and guidelines provided by professional bodies so that adequate financial

statements may be prepared quite effectively. The present report deals with financial accounting

principles and methods and importance to company. The report also highlights preparation of

trial balance and preparation of balance sheet and income statement for organisations. Moreover,

it also deals to comply with various accounting principles and concepts so that adequate financial

information may be prepared and provided to various stakeholders to take effective decisions.

A. Preparation of report for Line Manager on accounting principles

To: Line Manager

From: Junior Accountant

Subject: Providing accounting principles and regulations for adequate financials of the

company

Respected Sir,

Accounting principles are required to be adopted by company so that financial

statements may be prepared with much ease and carry proper information to be imparted to

various stakeholders' of the company. Accounting professionals or accountants are under duty

to prepare accounting records by complying accounting principles and concepts so that

adequate and proper records may be made and as such, financial statements may be

consecutively prepared. The financial statements must be prepared in proper manner so that true

and fair financial health of the company may be provided to stakeholders' for taking better and

effective decisions quite effectively (Warren and Jones, 2018). This task is not an easy one but

requires that accountants follow prescribed rules and concepts of accounting so that financial

statements may be prepared and as such, stakeholders' may take decisions with much ease. The

stakeholders consist of government, suppliers, investors, creditors, management and many

more. These stakeholders' whether internal or external are required to analyse financial health of

the company so that they may assess its financial position with much ease. This helps them to

1

Financial accounting is the main branch of accounting which helps in preparation of

various financial statements such as balance sheet, income statement, cash flow statement and

statement of changes in equity. These statements are required to be prepared by complying with

the provisions and guidelines provided by professional bodies so that adequate financial

statements may be prepared quite effectively. The present report deals with financial accounting

principles and methods and importance to company. The report also highlights preparation of

trial balance and preparation of balance sheet and income statement for organisations. Moreover,

it also deals to comply with various accounting principles and concepts so that adequate financial

information may be prepared and provided to various stakeholders to take effective decisions.

A. Preparation of report for Line Manager on accounting principles

To: Line Manager

From: Junior Accountant

Subject: Providing accounting principles and regulations for adequate financials of the

company

Respected Sir,

Accounting principles are required to be adopted by company so that financial

statements may be prepared with much ease and carry proper information to be imparted to

various stakeholders' of the company. Accounting professionals or accountants are under duty

to prepare accounting records by complying accounting principles and concepts so that

adequate and proper records may be made and as such, financial statements may be

consecutively prepared. The financial statements must be prepared in proper manner so that true

and fair financial health of the company may be provided to stakeholders' for taking better and

effective decisions quite effectively (Warren and Jones, 2018). This task is not an easy one but

requires that accountants follow prescribed rules and concepts of accounting so that financial

statements may be prepared and as such, stakeholders' may take decisions with much ease. The

stakeholders consist of government, suppliers, investors, creditors, management and many

more. These stakeholders' whether internal or external are required to analyse financial health of

the company so that they may assess its financial position with much ease. This helps them to

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

take effective decisions for their individual benefits.

1. Enumerating financial accounting

Financial accounting is a branch of accounting that records daily transactions of

business in books of accounts. As such, each and every record is maintained effectively. The

records are maintained in various books of accounts namely purchase book, day book, sales

book etc. Journal entries are made in chronological order and as such, entries are posted in

ledger. From this process, trial balance is prepared to check accuracy of the accounting records

maintained in these books of accounts. Finally, financial statements such as balance sheet,

Profit & Loss account and cash flow statement are prepared which clearly exhibits financial

health of organisation quite effectively. Thus, such information is then provided to various

stakeholders to take better and enhanced decisions. Financial accounting is also known as

historical accounting as it takes past data or summary of records which is then used to prepare

financial statements. Financial accounting is the base for preparing managerial reports which

are then utilised by managers to take better internal decisions by analysing financial statements

with much ease (Campbell, Khan and Pierce, 2017). External stakeholders such as creditors and

investors require financial statements of the firm so that they take decisions whether to provide

funds to firm or not. As financial position is provided to stakeholders', they take enhanced

decisions in the best possible way.

2

1. Enumerating financial accounting

Financial accounting is a branch of accounting that records daily transactions of

business in books of accounts. As such, each and every record is maintained effectively. The

records are maintained in various books of accounts namely purchase book, day book, sales

book etc. Journal entries are made in chronological order and as such, entries are posted in

ledger. From this process, trial balance is prepared to check accuracy of the accounting records

maintained in these books of accounts. Finally, financial statements such as balance sheet,

Profit & Loss account and cash flow statement are prepared which clearly exhibits financial

health of organisation quite effectively. Thus, such information is then provided to various

stakeholders to take better and enhanced decisions. Financial accounting is also known as

historical accounting as it takes past data or summary of records which is then used to prepare

financial statements. Financial accounting is the base for preparing managerial reports which

are then utilised by managers to take better internal decisions by analysing financial statements

with much ease (Campbell, Khan and Pierce, 2017). External stakeholders such as creditors and

investors require financial statements of the firm so that they take decisions whether to provide

funds to firm or not. As financial position is provided to stakeholders', they take enhanced

decisions in the best possible way.

2

The above diagram shows various financial statements which are prepared by business

so that financial information may be provided to users of it with much ease. External and

internal stakeholders' are enhanced by financial statements as it provides clear information to

them regarding financial health of organisation. Moreover, financial information is also used by

taxation authorities so that tax may be paid by company and no tax evasion may be made. As

such, they rely on accuracy of financial statements which provides required information to

them. As a result, it can be said that financial accounting is helpful for various stakeholders to

draw meaningful information for taking enhanced decisions.

2. Financial accounting concepts and rules

Accounting records are maintained so that financial statements are prepared quite easily.

But for achieving this task, certain accounting rules need to be followed by accountants so that

no errors may be made and final accounts of company may exhibit true information. As such,

3

so that financial information may be provided to users of it with much ease. External and

internal stakeholders' are enhanced by financial statements as it provides clear information to

them regarding financial health of organisation. Moreover, financial information is also used by

taxation authorities so that tax may be paid by company and no tax evasion may be made. As

such, they rely on accuracy of financial statements which provides required information to

them. As a result, it can be said that financial accounting is helpful for various stakeholders to

draw meaningful information for taking enhanced decisions.

2. Financial accounting concepts and rules

Accounting records are maintained so that financial statements are prepared quite easily.

But for achieving this task, certain accounting rules need to be followed by accountants so that

no errors may be made and final accounts of company may exhibit true information. As such,

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accounting concepts are required to be followed so that manipulation in accounting records may

not be made. As such manipulation leads to false and wrong financial information which is of

no use to accounting users of information. The manipulation in accounting means that firm

hides net profit or makes certain other tactics so that they may reveal false information to

taxation authorities and other stakeholders' to predict financial health of company sound enough

(Narayanaswamy, 2017). This leads to false information and as such, accounting rules and

concepts are provided by professional bodies so that true financial information may be imparted

by business quite effectively to stakeholders' for taking better decisions. In relation to this, UK's

corporate regulator has issued FRC guidelines to be followed by accountants so that they may

prepare financial statements with reference to such guidelines. The regulations help firm to

exhibit true information and as such, stakeholders' may take better decisions.

Legal frameworks imparted by professional bodies are as follows:

FRC (Financial Reporting Council) : This professional body is formed legally and is formed as

limited guarantee with respect to shares. FRC regulates government entities and organisations.

IT regulates organisations and indirectly helps economy as a whole. Fostering adequate

investment in UK is the main aim and objective of FRC. As such, company is required to abide

by laws of professional body to prepare adequate financial statements and reports quite

effectively.

IASB (International Accounting Standards Board) : This professional body provides legal

framework to organisation so that adequate financial statements may be prepared quite

effectively. It provides accounting procedures to be followed by accountants so that they may

prepare proper financial statements of the concern organisation. This is body under sight of

IFRS (International Financial Reporting Standards). The guidelines imparted by the body are

universally accepted by investors as well to take decisions. As such, accounting professionals

are delighted by accounting procedures provided by IASB.

IFRS (International Financial Reporting Standards) : IFRS is the body entitled to regulate

financial statements of the organisation (Richardson, 2017). This provides effective guidelines

which are then followed by accountants so that well-structured financial statements may be

prepared with much ease. As such, this helps accountants to follow legal structure and as such,

4

not be made. As such manipulation leads to false and wrong financial information which is of

no use to accounting users of information. The manipulation in accounting means that firm

hides net profit or makes certain other tactics so that they may reveal false information to

taxation authorities and other stakeholders' to predict financial health of company sound enough

(Narayanaswamy, 2017). This leads to false information and as such, accounting rules and

concepts are provided by professional bodies so that true financial information may be imparted

by business quite effectively to stakeholders' for taking better decisions. In relation to this, UK's

corporate regulator has issued FRC guidelines to be followed by accountants so that they may

prepare financial statements with reference to such guidelines. The regulations help firm to

exhibit true information and as such, stakeholders' may take better decisions.

Legal frameworks imparted by professional bodies are as follows:

FRC (Financial Reporting Council) : This professional body is formed legally and is formed as

limited guarantee with respect to shares. FRC regulates government entities and organisations.

IT regulates organisations and indirectly helps economy as a whole. Fostering adequate

investment in UK is the main aim and objective of FRC. As such, company is required to abide

by laws of professional body to prepare adequate financial statements and reports quite

effectively.

IASB (International Accounting Standards Board) : This professional body provides legal

framework to organisation so that adequate financial statements may be prepared quite

effectively. It provides accounting procedures to be followed by accountants so that they may

prepare proper financial statements of the concern organisation. This is body under sight of

IFRS (International Financial Reporting Standards). The guidelines imparted by the body are

universally accepted by investors as well to take decisions. As such, accounting professionals

are delighted by accounting procedures provided by IASB.

IFRS (International Financial Reporting Standards) : IFRS is the body entitled to regulate

financial statements of the organisation (Richardson, 2017). This provides effective guidelines

which are then followed by accountants so that well-structured financial statements may be

prepared with much ease. As such, this helps accountants to follow legal structure and as such,

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial statements are prepared and from it, financial reports are consecutively prepared which

are much useful to stakeholders' to take better and enhanced decisions.

3. Various rules for accounting

In this regard, GAAP (Generally Accepted Accounting Principles) has imparted certain

rules to be used by accounting professionals so that adequate financial statements may be

prepared by them and as such, true and fair information may be imparted for taking decisions.

Various rules of accounting are described below :

1. Monetary unit assumption : The underlying rule states that stable currency should be used by

company for dealing in business transactions. As such, universally accepted currency is US

dollar as it is more stable than any other currencies of the world. As a result, business

transactions must be made in this currency by the business.

2. Economic assumption : The economic assumption states that business should analyse

economic environment and in relation to this, economic assumptions may be made for a

particular period. This assumption is required so that business may predict the viability of the

project to be taken in future by the firm (Maynard, 2017).

3. Cost principle : The cost principle is states that organisation should analyse expenditures

requirement of various divisions and by assessing needs of them, budget should be prepared. As

such, budgets are required to be prepared so that costs may be controlled effectively by firm.

Thus, budgets are prepared in anticipation of the demand of the departments. This helps

company to control costs effectively.

4. Full disclosure principle : Full disclosure principle states that accounting records must be

maintained effectively so that effect of each and every transaction is reflected while preparation

of final accounts of the organisation. This principle states that accounting records should be

prepared effectively by complying with such rule and this will directly help to fully disclosed

financial information in various financial statements of the company. Thus, more reliability may

be attained.

5. Going concern Principle : This principle states that organisation will remain in the market for

longer period and will not shut down within shorter period. By complying with this principle,

financial statements are prepared by business. Thus, necessary information is imparted to users

5

are much useful to stakeholders' to take better and enhanced decisions.

3. Various rules for accounting

In this regard, GAAP (Generally Accepted Accounting Principles) has imparted certain

rules to be used by accounting professionals so that adequate financial statements may be

prepared by them and as such, true and fair information may be imparted for taking decisions.

Various rules of accounting are described below :

1. Monetary unit assumption : The underlying rule states that stable currency should be used by

company for dealing in business transactions. As such, universally accepted currency is US

dollar as it is more stable than any other currencies of the world. As a result, business

transactions must be made in this currency by the business.

2. Economic assumption : The economic assumption states that business should analyse

economic environment and in relation to this, economic assumptions may be made for a

particular period. This assumption is required so that business may predict the viability of the

project to be taken in future by the firm (Maynard, 2017).

3. Cost principle : The cost principle is states that organisation should analyse expenditures

requirement of various divisions and by assessing needs of them, budget should be prepared. As

such, budgets are required to be prepared so that costs may be controlled effectively by firm.

Thus, budgets are prepared in anticipation of the demand of the departments. This helps

company to control costs effectively.

4. Full disclosure principle : Full disclosure principle states that accounting records must be

maintained effectively so that effect of each and every transaction is reflected while preparation

of final accounts of the organisation. This principle states that accounting records should be

prepared effectively by complying with such rule and this will directly help to fully disclosed

financial information in various financial statements of the company. Thus, more reliability may

be attained.

5. Going concern Principle : This principle states that organisation will remain in the market for

longer period and will not shut down within shorter period. By complying with this principle,

financial statements are prepared by business. Thus, necessary information is imparted to users

5

of accounting to take better decisions.

6. Materiality concept : The materiality concept says that non-material items must be ignored by

business and only material items must be included in books of accounts. This is done by

analysing information requirement of users that whether this will affect their economic

decisions or not. As such, only material items related information is disclosed to them whch

might affect decisions of them (Brausch, 2017).

4. Material disclosure and consistency concepts

Consistency : This concept states that accounting policies should be followed consistently by

firm and should not change it frequently. This concept says that if frequent changes are made in

accounting policies, then reliability in financial information is lost. Thus, adhering to same

policies up to longer time provides reliable information which is then quite easier to compare

with past financial years. For instance, deprecation charged on fixed assets must be made with

same method only so that valuation may be ascertained else, profit will not be correctly

evaluated.

Material disclosure : This concepts states that material information must be recorded fully in

the books of accounts and as such, financial statements should reflect correct material

information. This helps to provide adequate financial information to various stakeholders' to

take enhanced decisions with much ease.

CLIENT 1

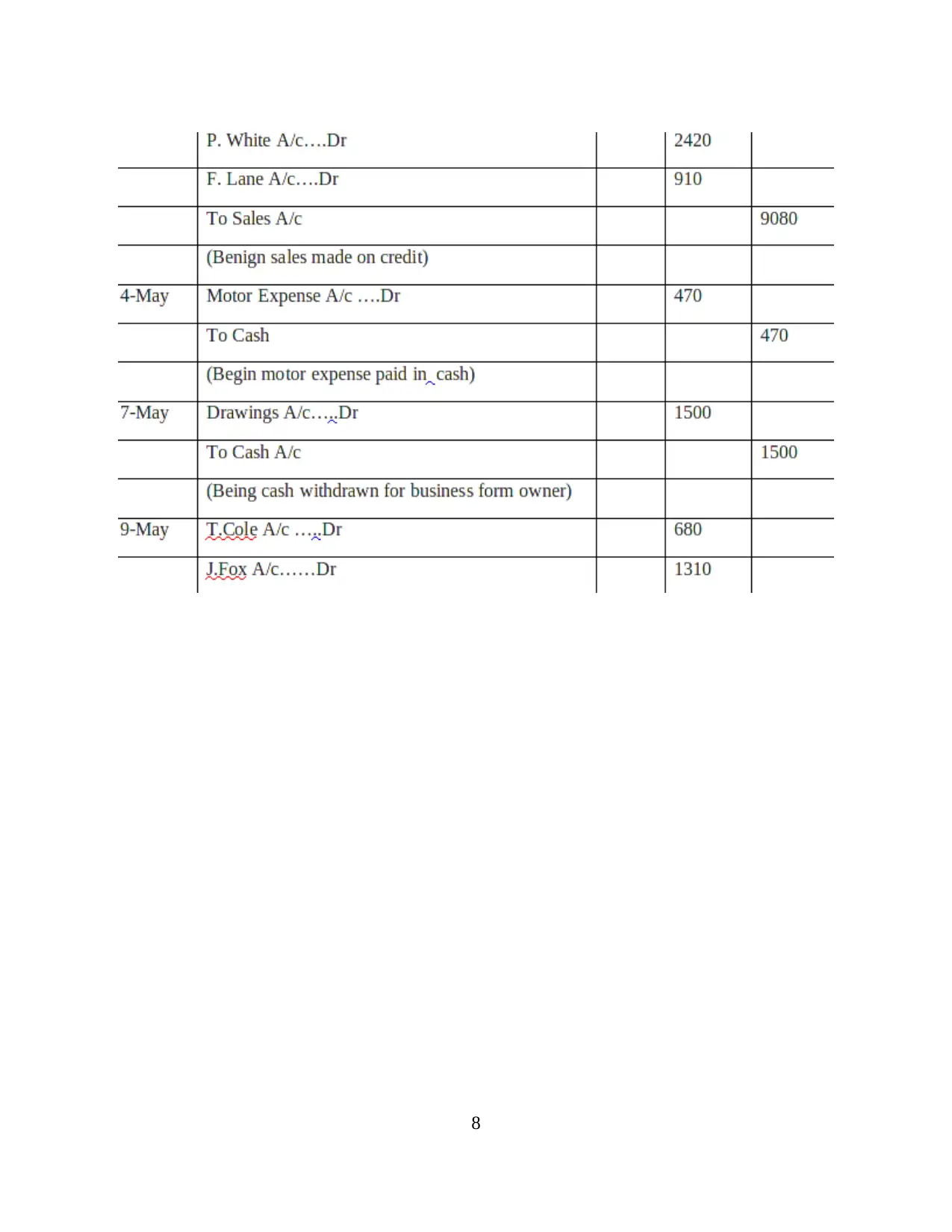

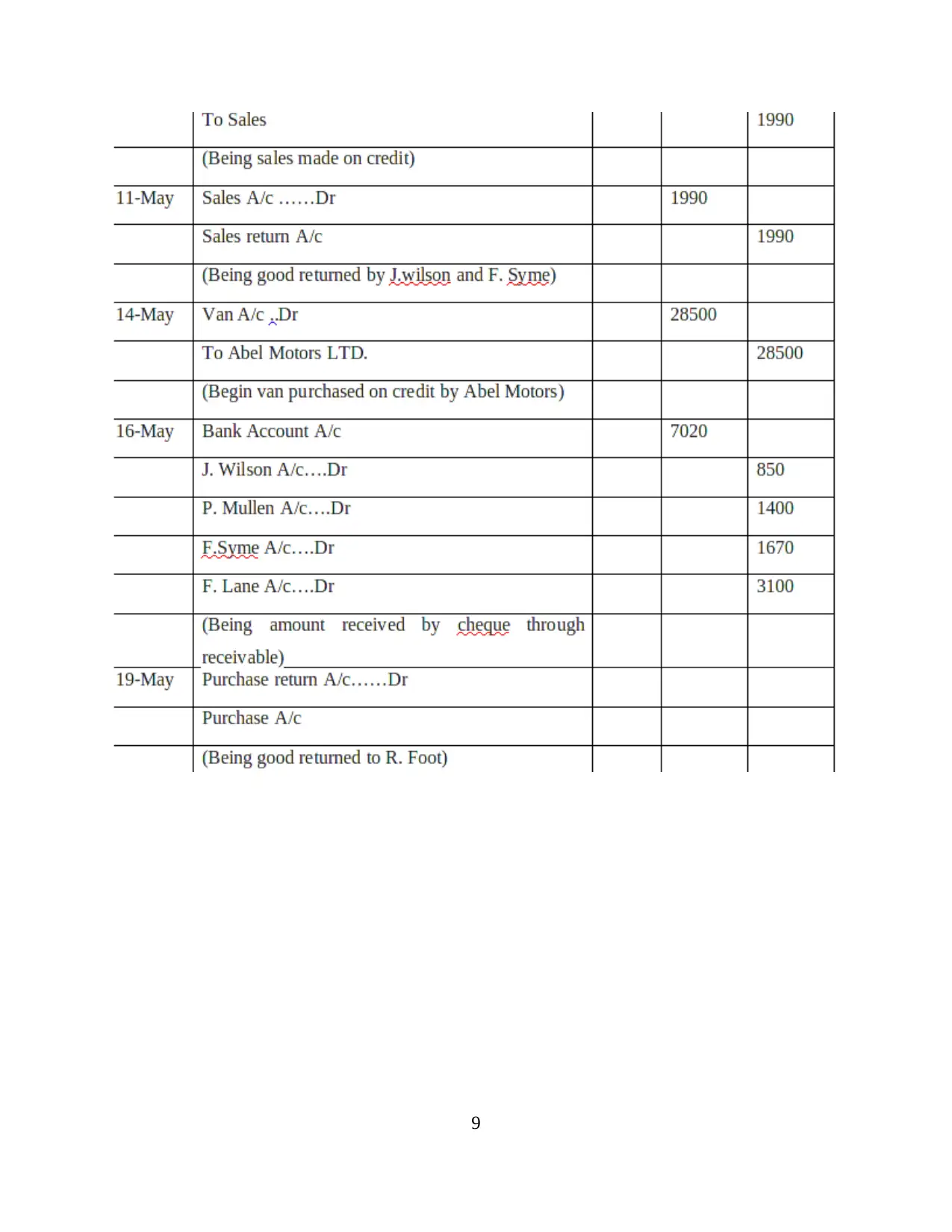

1. Journal entries for firm

Journal entries is the first step of financial accounting. It records various transactions that

take place in the business in daily operations. The main essence of journal is that records are

maintained in chronological order. This means that when transaction occurs, it is immediately

recorded in books of accounts. Journal entries shows various accounts maintained in the business

and ensures that every record is balanced by making relevant entries in debit and credit side. It

means that every transaction recorded must have dual effect (Brandau, Endenich, Luther and

6

6. Materiality concept : The materiality concept says that non-material items must be ignored by

business and only material items must be included in books of accounts. This is done by

analysing information requirement of users that whether this will affect their economic

decisions or not. As such, only material items related information is disclosed to them whch

might affect decisions of them (Brausch, 2017).

4. Material disclosure and consistency concepts

Consistency : This concept states that accounting policies should be followed consistently by

firm and should not change it frequently. This concept says that if frequent changes are made in

accounting policies, then reliability in financial information is lost. Thus, adhering to same

policies up to longer time provides reliable information which is then quite easier to compare

with past financial years. For instance, deprecation charged on fixed assets must be made with

same method only so that valuation may be ascertained else, profit will not be correctly

evaluated.

Material disclosure : This concepts states that material information must be recorded fully in

the books of accounts and as such, financial statements should reflect correct material

information. This helps to provide adequate financial information to various stakeholders' to

take enhanced decisions with much ease.

CLIENT 1

1. Journal entries for firm

Journal entries is the first step of financial accounting. It records various transactions that

take place in the business in daily operations. The main essence of journal is that records are

maintained in chronological order. This means that when transaction occurs, it is immediately

recorded in books of accounts. Journal entries shows various accounts maintained in the business

and ensures that every record is balanced by making relevant entries in debit and credit side. It

means that every transaction recorded must have dual effect (Brandau, Endenich, Luther and

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Trapp, 2017). As such, journal entries are said to be balanced when debit side equals credit side

of the transaction.

7

of the transaction.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 44

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.