Financial Accounting Principles: Business Report, Journal Entries

VerifiedAdded on 2020/11/12

|27

|4346

|118

Report

AI Summary

This business report delves into the core principles of financial accounting, providing a comprehensive overview of essential concepts and practices. It begins by defining financial accounting and its importance in business, followed by an exploration of relevant regulations and accounting principles. The report then examines key conventions such as materiality and consistency, which are crucial for accurate financial reporting. Practical applications are demonstrated through the analysis of journal entries for multiple clients, including double-entry bookkeeping, trial balances, and the preparation of financial statements. The report also covers bank reconciliation processes and reconciliation of control accounts, providing a detailed understanding of these critical accounting procedures. Furthermore, the report includes an analysis of suspense accounts and concludes with a summary of the key findings and insights.

Financial Accounting

Principles

Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

BUSINESS REPORT......................................................................................................................1

(a): Concept of Financial accounting.....................................................................................1

(b): Regulation related with financial accounting..................................................................2

C): Principles and regulations used in accounting.................................................................3

(d): Various convention and concept of materiality and consistency.....................................4

CLIENT 1: Journal Entries..............................................................................................................5

P1: Information regarding double entry bookkeeping............................................................5

P2: Concept of trail balance and its balancing measure.......................................................14

CLIENT 2......................................................................................................................................15

P3: (a): Formulation of financial account and related trail balance.....................................15

(b): Financial statements of peter piper................................................................................15

CLIENT 3......................................................................................................................................16

P4: Formulation of financial statements and wide number of examples..............................16

P5: Bank Reconciliation process..........................................................................................19

CLIENT 4......................................................................................................................................20

BRS statements as one 1st December, 2017..........................................................................20

CLIENT 5......................................................................................................................................20

P6: Procedure of Reconcile control account........................................................................20

CLIENT 6......................................................................................................................................22

(a): Main feature of suspense account..................................................................................22

b) Trial balance (£)...............................................................................................................22

(c) suspense account.............................................................................................................22

(d): Comparison....................................................................................................................22

CONCLUSION..............................................................................................................................23

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

BUSINESS REPORT......................................................................................................................1

(a): Concept of Financial accounting.....................................................................................1

(b): Regulation related with financial accounting..................................................................2

C): Principles and regulations used in accounting.................................................................3

(d): Various convention and concept of materiality and consistency.....................................4

CLIENT 1: Journal Entries..............................................................................................................5

P1: Information regarding double entry bookkeeping............................................................5

P2: Concept of trail balance and its balancing measure.......................................................14

CLIENT 2......................................................................................................................................15

P3: (a): Formulation of financial account and related trail balance.....................................15

(b): Financial statements of peter piper................................................................................15

CLIENT 3......................................................................................................................................16

P4: Formulation of financial statements and wide number of examples..............................16

P5: Bank Reconciliation process..........................................................................................19

CLIENT 4......................................................................................................................................20

BRS statements as one 1st December, 2017..........................................................................20

CLIENT 5......................................................................................................................................20

P6: Procedure of Reconcile control account........................................................................20

CLIENT 6......................................................................................................................................22

(a): Main feature of suspense account..................................................................................22

b) Trial balance (£)...............................................................................................................22

(c) suspense account.............................................................................................................22

(d): Comparison....................................................................................................................22

CONCLUSION..............................................................................................................................23

REFERENCES..............................................................................................................................24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance is considering as life blood of business. The company used to collect funds from

various sources in order to manage and operate their everyday transactions that are done within

an accounting period of time. Financial accounting is one of the appropriate process that will be

helpful for the owner as well as accountant in order to record all the essential transactions those

are incurred during the time. These entries are posted into their respective statements as per their

data of occurrence. This project module aims as analyzing financial condition and health of the

company (Ward, 2012). For this purpose, regular recording of business transactions is being

done. On the basis of collected records, its legers posting, trail balance and other crucial

statements is being prepared under this report. In order to keep accuracy of the data, every

records must be recorded as per the accounting principle as well as other specific standards.

Evaluation of bank reconciliation is prepared in reliable order to examine total cash amount

balance available to the company during the end of accounting period.

BUSINESS REPORT

(a): Concept of Financial accounting

In every organization, it is necessary for them are organize sufficient amount of capital

for the purpose of planning their future projects in effective manner. In this process, managers

need to organize capital from various sources. Financial accounting is said to be appropriate art

of recording, dividing and evaluating in important way in respect to capital, transaction and

activity that are done within an organization. It is also considering as reliable branch of

accounting that used to provide right direction to a company’s financial transaction by recording,

summarizing and present in financial report. Some of them are profit and loss statements,

balance sheet and cash flow statements (Francis, Hasan and Wu, 2013). Most of the company

used to release its financial statements on continuous basis.

The statements are taken into consideration as external because they used to provide

specific information to the people from outside the company. It is necessary to point out the

valuable purpose of financial accounting that is not reported as value of the company. In-spite of

their objective which is provided for other to assess the interest of an organization. These

financial report is being done with the aim of attaining specific aims that are set by the company.

there are some crucial firms those are using various accounting systems by using IFRS standards.

Financial accounting is considering as one of the effective aspects which will be considered for

1

Finance is considering as life blood of business. The company used to collect funds from

various sources in order to manage and operate their everyday transactions that are done within

an accounting period of time. Financial accounting is one of the appropriate process that will be

helpful for the owner as well as accountant in order to record all the essential transactions those

are incurred during the time. These entries are posted into their respective statements as per their

data of occurrence. This project module aims as analyzing financial condition and health of the

company (Ward, 2012). For this purpose, regular recording of business transactions is being

done. On the basis of collected records, its legers posting, trail balance and other crucial

statements is being prepared under this report. In order to keep accuracy of the data, every

records must be recorded as per the accounting principle as well as other specific standards.

Evaluation of bank reconciliation is prepared in reliable order to examine total cash amount

balance available to the company during the end of accounting period.

BUSINESS REPORT

(a): Concept of Financial accounting

In every organization, it is necessary for them are organize sufficient amount of capital

for the purpose of planning their future projects in effective manner. In this process, managers

need to organize capital from various sources. Financial accounting is said to be appropriate art

of recording, dividing and evaluating in important way in respect to capital, transaction and

activity that are done within an organization. It is also considering as reliable branch of

accounting that used to provide right direction to a company’s financial transaction by recording,

summarizing and present in financial report. Some of them are profit and loss statements,

balance sheet and cash flow statements (Francis, Hasan and Wu, 2013). Most of the company

used to release its financial statements on continuous basis.

The statements are taken into consideration as external because they used to provide

specific information to the people from outside the company. It is necessary to point out the

valuable purpose of financial accounting that is not reported as value of the company. In-spite of

their objective which is provided for other to assess the interest of an organization. These

financial report is being done with the aim of attaining specific aims that are set by the company.

there are some crucial firms those are using various accounting systems by using IFRS standards.

Financial accounting is considering as one of the effective aspects which will be considered for

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

attaining maximum return in near future. Financial report are being taken into account in order to

keep all the standard and responsibility of manager and accountant. Some of the vital statement

those are used in financial accounting purpose are mentioned underneath:

Profit and loss statements: It is known as one of the effective report that is being

prepared by the accountant by summarizing the revenue, cost and expenditure of the company

incurred during the time. It would indicate total earning and expenses in the mentioned period of

time, usually a fiscal year. It will assist companies in analyzing, whether the company is making

appropriate revenue, income statements of an organization (Edwards, 2013).

Balance sheet: It would be happening as one of the crucial statements that is being used

as particular data those are done by the company during the time. It is considering as company’s

main statements which would provide overall health position as well as liquidity state. Financial

firms and other stakeholder used to present specific data about assets and liability of the

company. This seems to be effective financial statements for delivery available loans and

investment done in an accounting period.

Cash flow statement: It seems to taken into account valuable information about all cash

inflows and outflows that are incurred during the time. These amounts are collected from various

activity such as operating, investing and financing. These are prepared to make evaluation of

whether company is having sufficient amount of capital to make future investment in near

project.

(b): Regulation related with financial accounting

Financial accounting board is considering as one of the private, non-private business

standard imposing bodies that primary aim is to establish better outcomes to the company. The

required needs rules and regulations which would assist in formulating financial statements in

essential manner for various reasons. Such as to ensure that requirement of users of financial

records must be met with at least a simple data that are prepare by the company within an

accounting period of time (Beatty and Liao, 2014). There are not any other issues required by the

company in order to report various activities that are necessary for making sustainable demand of

the company. present reporting and practices are having more link with future growth and

financial balance of an organization. Although, financial reports are reliable for making

comparison of company’s performance on the basis of last year condition. The financial

information parties are large enough and having diversified impacts as per the financial

2

keep all the standard and responsibility of manager and accountant. Some of the vital statement

those are used in financial accounting purpose are mentioned underneath:

Profit and loss statements: It is known as one of the effective report that is being

prepared by the accountant by summarizing the revenue, cost and expenditure of the company

incurred during the time. It would indicate total earning and expenses in the mentioned period of

time, usually a fiscal year. It will assist companies in analyzing, whether the company is making

appropriate revenue, income statements of an organization (Edwards, 2013).

Balance sheet: It would be happening as one of the crucial statements that is being used

as particular data those are done by the company during the time. It is considering as company’s

main statements which would provide overall health position as well as liquidity state. Financial

firms and other stakeholder used to present specific data about assets and liability of the

company. This seems to be effective financial statements for delivery available loans and

investment done in an accounting period.

Cash flow statement: It seems to taken into account valuable information about all cash

inflows and outflows that are incurred during the time. These amounts are collected from various

activity such as operating, investing and financing. These are prepared to make evaluation of

whether company is having sufficient amount of capital to make future investment in near

project.

(b): Regulation related with financial accounting

Financial accounting board is considering as one of the private, non-private business

standard imposing bodies that primary aim is to establish better outcomes to the company. The

required needs rules and regulations which would assist in formulating financial statements in

essential manner for various reasons. Such as to ensure that requirement of users of financial

records must be met with at least a simple data that are prepare by the company within an

accounting period of time (Beatty and Liao, 2014). There are not any other issues required by the

company in order to report various activities that are necessary for making sustainable demand of

the company. present reporting and practices are having more link with future growth and

financial balance of an organization. Although, financial reports are reliable for making

comparison of company’s performance on the basis of last year condition. The financial

information parties are large enough and having diversified impacts as per the financial

2

accounting. In case of any modification change in the data those are required as an individual for

plenty of ways. In order to maintain appropriate rules and regulation that are based on certain

norms such as IASB. The main motive of IASC which was used to promote global consistency

among financial statements which would prepared through company at national level. It does not

have to force by law because, every information that are mentioned under the report are based on

certain polices and rules. These standard are considered while recording of various transaction

into different statements.

C): Principles and regulations used in accounting

In accordance with various transactions that are done within an accounting period of time,

accounts are using various rules and regulations that are utilized or proposed through using

various guidelines that are required to be taken into account while recording of data into the

statements. It has been observed that there are various types of rules and concept which will be

use by manger while recording or posting of any kind of financial transactions. In case of using

accounting records, detailed regulations and laws that are being use by FASB (Barron, Chung

and Yong, 2016). It has been found that some of the effective distributes its financial records to

public and required to make impacts on GAAP principles during the time of developing their

reports. Likewise, in accordance with company’s overall inventory which is public traded and

need as financial record through audited through an appropriate accounting skills. Some of the

valuable principles are mentioned underneath:

Cost principles: According to this accounting norms, it has been known as that cost

which would be based on historical cost aspects. It required that all assets must be

recorded only at cash basis during the time of acquisition.

Going concern principle: The seems to be assumptions that every entity would remain

as effective business for specific aspects for foreseeable future. As business would

continuous for longer period of time.

Full disclosure principle: It is said to be vital information that would be made by

stakeholders by using financial report which data will be disclosure during prepared data.

This seems to be primary aim of manager to provide all essential data which are

mentioned under different reports. It is needed for every organization to make future

planning by using various data of the company in reliable and accurate manner.

3

plenty of ways. In order to maintain appropriate rules and regulation that are based on certain

norms such as IASB. The main motive of IASC which was used to promote global consistency

among financial statements which would prepared through company at national level. It does not

have to force by law because, every information that are mentioned under the report are based on

certain polices and rules. These standard are considered while recording of various transaction

into different statements.

C): Principles and regulations used in accounting

In accordance with various transactions that are done within an accounting period of time,

accounts are using various rules and regulations that are utilized or proposed through using

various guidelines that are required to be taken into account while recording of data into the

statements. It has been observed that there are various types of rules and concept which will be

use by manger while recording or posting of any kind of financial transactions. In case of using

accounting records, detailed regulations and laws that are being use by FASB (Barron, Chung

and Yong, 2016). It has been found that some of the effective distributes its financial records to

public and required to make impacts on GAAP principles during the time of developing their

reports. Likewise, in accordance with company’s overall inventory which is public traded and

need as financial record through audited through an appropriate accounting skills. Some of the

valuable principles are mentioned underneath:

Cost principles: According to this accounting norms, it has been known as that cost

which would be based on historical cost aspects. It required that all assets must be

recorded only at cash basis during the time of acquisition.

Going concern principle: The seems to be assumptions that every entity would remain

as effective business for specific aspects for foreseeable future. As business would

continuous for longer period of time.

Full disclosure principle: It is said to be vital information that would be made by

stakeholders by using financial report which data will be disclosure during prepared data.

This seems to be primary aim of manager to provide all essential data which are

mentioned under different reports. It is needed for every organization to make future

planning by using various data of the company in reliable and accurate manner.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Rules and regulations: There are various types of accounting rules which will be taken into

consideration while recording of essential transactions. Some of them are discussed underneath:

Personal account: It is said to be one of the reliable account that will be taken into

account as an individual as per the demand of the company. The accounting rules said

that Debit all receivers and credit the giver. Few examples are, drawings and capital etc.

Real account: Under this account that is related with the nature of assets which will be

used by the firms (Weygandt, Kimmel and Kieso, 2015). According to this rules, debit all

the amount which is coming inside the company, while credit all of them that are goes

outside. Like cash.

Nominal account: It seems to be essential financial transactions those are done during

the period of time. In this rules, debit all expenses or losses and credit all the income and

gains.

(d): Various convention and concept of materiality and consistency

In finance term, accounting conventions would be considering as one of the common

aspects that would be considers with the recording of every business entry. It would be

considered as one of the effective norms which will be not a definitive guideline in overall

accounting rules that are govern as one of the specific condition. Convention in accounting that

has been associated with bring regarding uniformity in the overall maintenances of accounts

statements. This would be consider as commonly accepted convention which would be customs

and framed to assist accountants to reduce practical issues those are arises out of preparation of

financial records. This would be reliable in case of any critical situation that is not related with

any kind of rules and standard which are governed during an accounting period. There are

different types of profitable aspects which will be considered by an organization. Some of them

are discussed below:

Consistency: In financial accounting, convention of regularity principles which would be

same accounting that should be considered for formulating financial transaction over the period

of time (Hillier, Grinblatt and Titman, 2011). Any modification can be considering as valuable

examples which will be taken into account for evaluating strength and weakness of the company.

Materiality: It would be considered as effective convention that can be considered for

making analyzing of impacts that are used by users in proper decision making. Financial account

4

consideration while recording of essential transactions. Some of them are discussed underneath:

Personal account: It is said to be one of the reliable account that will be taken into

account as an individual as per the demand of the company. The accounting rules said

that Debit all receivers and credit the giver. Few examples are, drawings and capital etc.

Real account: Under this account that is related with the nature of assets which will be

used by the firms (Weygandt, Kimmel and Kieso, 2015). According to this rules, debit all

the amount which is coming inside the company, while credit all of them that are goes

outside. Like cash.

Nominal account: It seems to be essential financial transactions those are done during

the period of time. In this rules, debit all expenses or losses and credit all the income and

gains.

(d): Various convention and concept of materiality and consistency

In finance term, accounting conventions would be considering as one of the common

aspects that would be considers with the recording of every business entry. It would be

considered as one of the effective norms which will be not a definitive guideline in overall

accounting rules that are govern as one of the specific condition. Convention in accounting that

has been associated with bring regarding uniformity in the overall maintenances of accounts

statements. This would be consider as commonly accepted convention which would be customs

and framed to assist accountants to reduce practical issues those are arises out of preparation of

financial records. This would be reliable in case of any critical situation that is not related with

any kind of rules and standard which are governed during an accounting period. There are

different types of profitable aspects which will be considered by an organization. Some of them

are discussed below:

Consistency: In financial accounting, convention of regularity principles which would be

same accounting that should be considered for formulating financial transaction over the period

of time (Hillier, Grinblatt and Titman, 2011). Any modification can be considering as valuable

examples which will be taken into account for evaluating strength and weakness of the company.

Materiality: It would be considered as effective convention that can be considered for

making analyzing of impacts that are used by users in proper decision making. Financial account

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

items are taken into account as material if they would influence economic decision in proper

ways.

Concept: Accounting managers need to follow certain amount of concept which would

be helpful while recording of various transactions into the books of account. Some of them vital

concepts are explained below:

Money measurement: It is said to be one of the effective and easy concept which will be

taken as guide for business by the managers. Every recording of events or transactions

can be analyses in terms of money. It is mainly measures in terms of local currency.

Conservatism: As per this principle which is helpful for the company in recognizing

expenses and debts as early as possible in case of uncertainty regarding the results. It is

also said be prudence which is a policy use for anticipating best possible outcomes in

near future period of time. The policy tends to understands various aspects of net assets

and incomes incurred by the company.

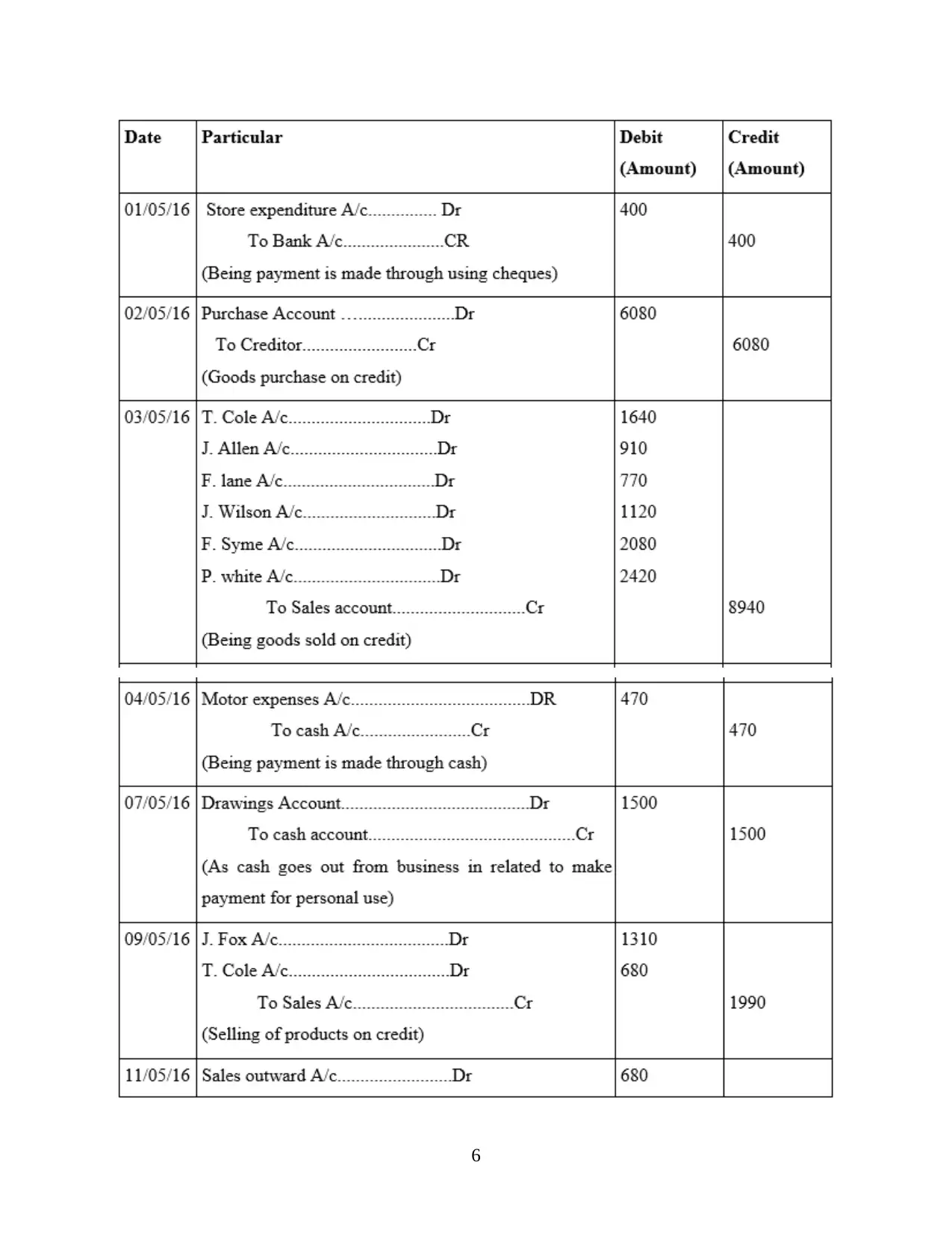

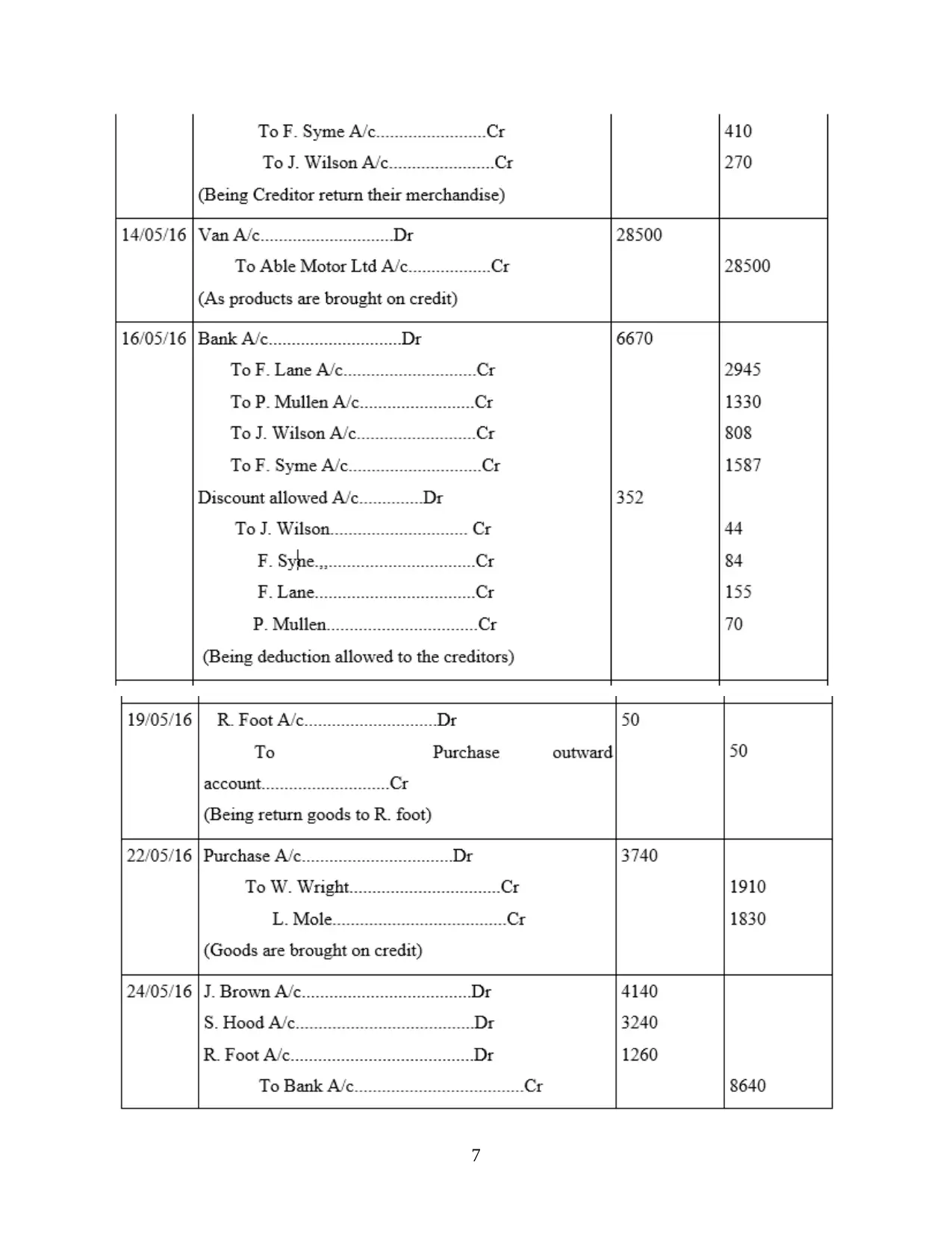

CLIENT 1: Journal Entries

P1: Information regarding double entry bookkeeping

Financial accounting is considered as one of the primary aspects for the company. Each

financial or non-financial transactions those are done by the company will be recorded with the

help of using double entry bookkeeping. It is said to be crucial term that means that all

transaction affects mainly two books of account of an organization. Double entry is said to be

one of the reliable accounts that must have entered as debit balance and another one is recorded

with credit (Christensen and Nikolaev, 2013). The major benefit of using this statements is that

company overall assets will be equal to debt balance. The Fundamental reason for underlying

effects need to be recorded as day to day bookkeeping and other detail related with accounting

transaction in two different accounts.

Asset= Liabilities + Equity.

5

ways.

Concept: Accounting managers need to follow certain amount of concept which would

be helpful while recording of various transactions into the books of account. Some of them vital

concepts are explained below:

Money measurement: It is said to be one of the effective and easy concept which will be

taken as guide for business by the managers. Every recording of events or transactions

can be analyses in terms of money. It is mainly measures in terms of local currency.

Conservatism: As per this principle which is helpful for the company in recognizing

expenses and debts as early as possible in case of uncertainty regarding the results. It is

also said be prudence which is a policy use for anticipating best possible outcomes in

near future period of time. The policy tends to understands various aspects of net assets

and incomes incurred by the company.

CLIENT 1: Journal Entries

P1: Information regarding double entry bookkeeping

Financial accounting is considered as one of the primary aspects for the company. Each

financial or non-financial transactions those are done by the company will be recorded with the

help of using double entry bookkeeping. It is said to be crucial term that means that all

transaction affects mainly two books of account of an organization. Double entry is said to be

one of the reliable accounts that must have entered as debit balance and another one is recorded

with credit (Christensen and Nikolaev, 2013). The major benefit of using this statements is that

company overall assets will be equal to debt balance. The Fundamental reason for underlying

effects need to be recorded as day to day bookkeeping and other detail related with accounting

transaction in two different accounts.

Asset= Liabilities + Equity.

5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

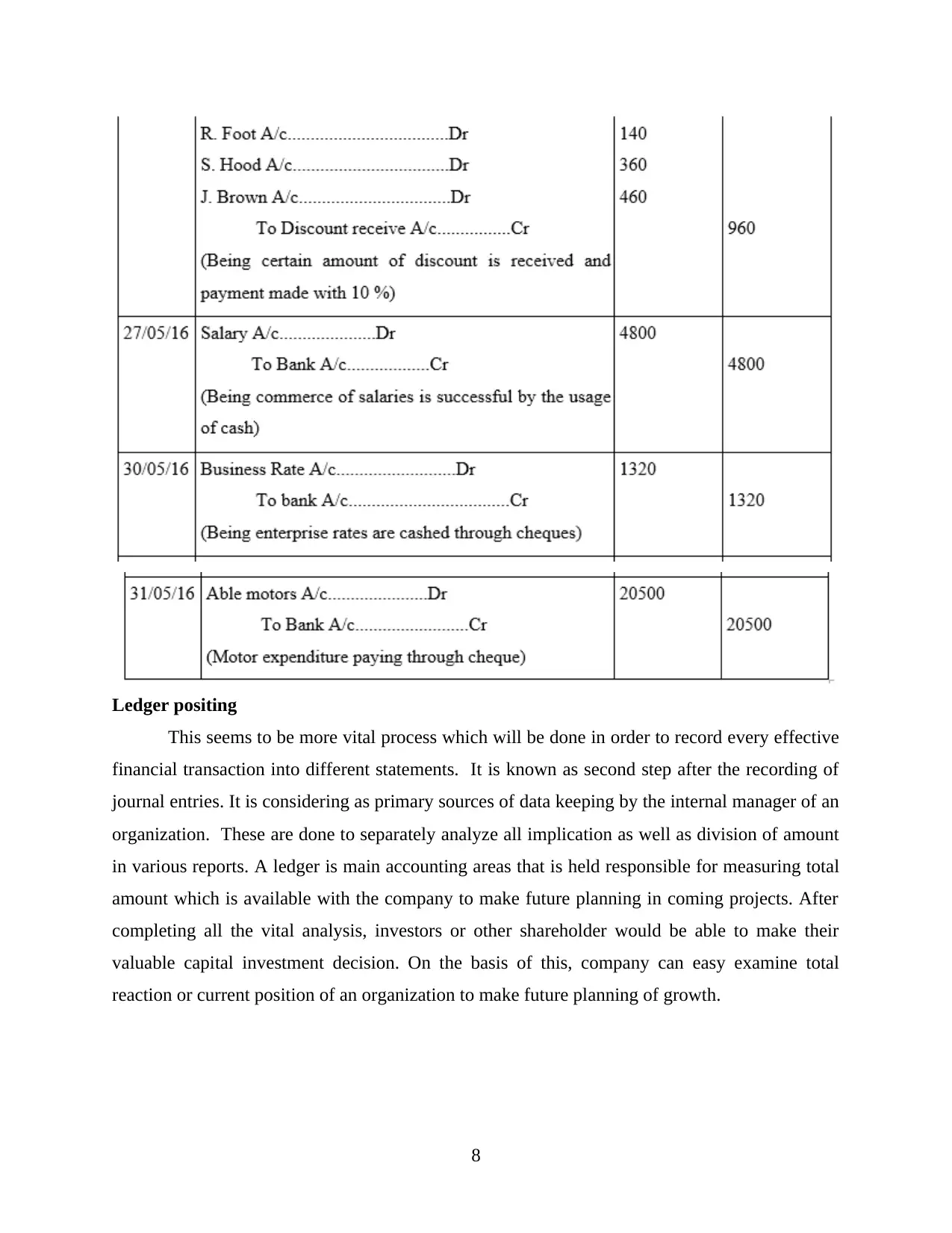

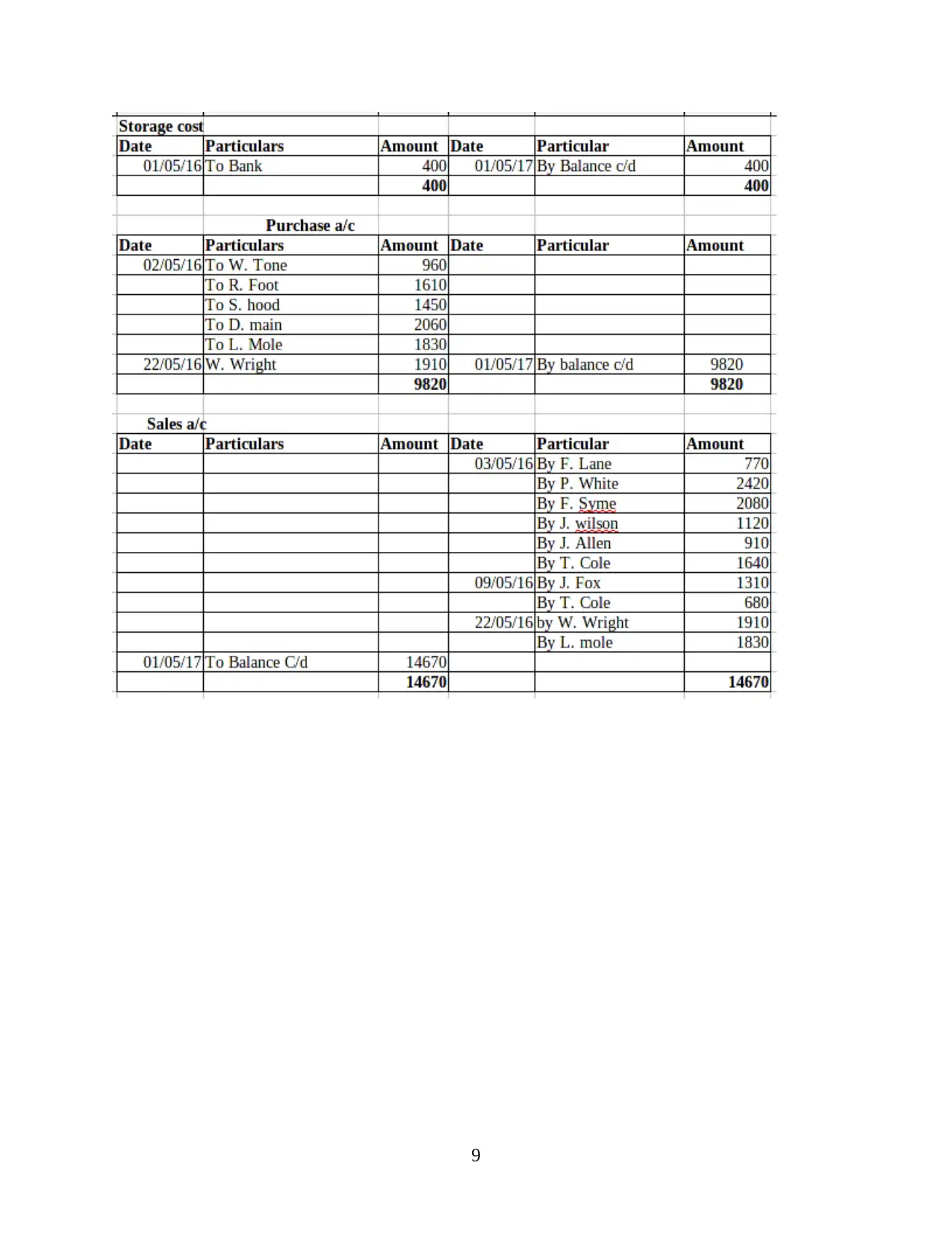

Ledger positing

This seems to be more vital process which will be done in order to record every effective

financial transaction into different statements. It is known as second step after the recording of

journal entries. It is considering as primary sources of data keeping by the internal manager of an

organization. These are done to separately analyze all implication as well as division of amount

in various reports. A ledger is main accounting areas that is held responsible for measuring total

amount which is available with the company to make future planning in coming projects. After

completing all the vital analysis, investors or other shareholder would be able to make their

valuable capital investment decision. On the basis of this, company can easy examine total

reaction or current position of an organization to make future planning of growth.

8

This seems to be more vital process which will be done in order to record every effective

financial transaction into different statements. It is known as second step after the recording of

journal entries. It is considering as primary sources of data keeping by the internal manager of an

organization. These are done to separately analyze all implication as well as division of amount

in various reports. A ledger is main accounting areas that is held responsible for measuring total

amount which is available with the company to make future planning in coming projects. After

completing all the vital analysis, investors or other shareholder would be able to make their

valuable capital investment decision. On the basis of this, company can easy examine total

reaction or current position of an organization to make future planning of growth.

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.