Financial Accounting Report: NAB and CBA Financial Analysis

VerifiedAdded on 2021/02/21

|15

|3652

|35

Report

AI Summary

This report provides a comprehensive financial accounting analysis of National Australia Bank Ltd (NAB) and Commonwealth Bank of Australia (CBA). Part A focuses on key balance sheet items such as shareholders' funds and liabilities, facilitating a comparative evaluation of their financial performance and aiding in decision-making. The analysis reveals that CBA operates at a larger scale than NAB, and the report explains fluctuations in financial statement items. Part B delves into the concepts of small and large proprietary companies, as well as reporting entities, evaluating compliance and implications of related regulations. The report examines items under owners' equity, including common stock, other equity, retained earnings, and accumulated other comprehensive income. It also explores the movement in these items and those under the liabilities section, such as deposits, derivative liabilities, payables, and both short and long-term borrowings, providing explanations for observed changes. The report concludes with a summary of the findings and references supporting the analysis.

Corporate

&

Financial

Accounting

&

Financial

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ABSTRACT

The study summarises in part A, analysis of key items of balance sheet like shareholder's

funds, different heads of liabilities etc. in National Australia Bank Ltd(NAB) and

Commonwealth Bank of Australia(CBA) which assist in making comparison, evaluation of

performance and in decision-making processes. Form this analysis it has been found that CBA is

operating at larger scale as compare to NAB and also main reason of fluctuations in different

items stated in financial statements of companies. Moreover in part B it covers core concept of

small and large proprietary company and reporting entity, form which evaluation of effective

compliance and implications of rules related to them is obtained.

The study summarises in part A, analysis of key items of balance sheet like shareholder's

funds, different heads of liabilities etc. in National Australia Bank Ltd(NAB) and

Commonwealth Bank of Australia(CBA) which assist in making comparison, evaluation of

performance and in decision-making processes. Form this analysis it has been found that CBA is

operating at larger scale as compare to NAB and also main reason of fluctuations in different

items stated in financial statements of companies. Moreover in part B it covers core concept of

small and large proprietary company and reporting entity, form which evaluation of effective

compliance and implications of rules related to them is obtained.

Table of Contents

ABSTRACT.....................................................................................................................................2

INTRODUCTION...........................................................................................................................4

ASSESSMENT TASK:...................................................................................................................4

PART A...........................................................................................................................................4

(1) Items recorded by selected companies under owners’ equity heading:.................................4

Explanation of understanding about each reported item:............................................................5

(2) Movement in items reported under owner equity section with reason:.................................5

(3) Items recorded by selected companies under liabilities section:............................................6

Explanation:.................................................................................................................................7

(4). Explanation about movement in items reported under liabilities head with reason:............8

PART B..........................................................................................................................................11

Concepts of small proprietary company, large proprietary company and reporting entity:......11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

ANNEXURE..................................................................................................................................14

ABSTRACT.....................................................................................................................................2

INTRODUCTION...........................................................................................................................4

ASSESSMENT TASK:...................................................................................................................4

PART A...........................................................................................................................................4

(1) Items recorded by selected companies under owners’ equity heading:.................................4

Explanation of understanding about each reported item:............................................................5

(2) Movement in items reported under owner equity section with reason:.................................5

(3) Items recorded by selected companies under liabilities section:............................................6

Explanation:.................................................................................................................................7

(4). Explanation about movement in items reported under liabilities head with reason:............8

PART B..........................................................................................................................................11

Concepts of small proprietary company, large proprietary company and reporting entity:......11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

ANNEXURE..................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In listed companies, financial accounting is essential task which gather and provide

crucial business data for financial reporting as well as preparation of financial statements.

Companies are required to adopt proper procedures relating to financial accounting along with

compliance requirements. It also assist stakeholder and investor to make momentous investment

decisions (Adesara, 2016). In part A of study, main aim is to provide a complete understanding

of each of the items reported by companies National Australia Bank Ltd and Commonwealth

Bank of Australia in their financial statements. It also covers merits and demerits of fund sources

reported by both corporations. Further part B of study evaluates the concepts of small proprietary

company, large proprietary company and reporting entity. Also, their classification on the basis

of compliance and reporting requirements.

ASSESSMENT TASK:

PART A

(1) Items recorded by selected companies under owners’ equity heading:

National Australia Bank Ltd (NAB):

(AUD in million)

2016 2017 2018

Stockholders' equity

Common stock 34285 34627 35982

Other Equity 617 492 307

Retained earnings 16378 16442 16673

Accumulated other comprehensive income 12 -255 -261

Total stockholders' equity 51292 51306 52701

Commonwealth Bank of Australia (CBA):

(AUD in million)

2016 2017 2018

Stockholders' equity

Common stock 33845 34971 37270

Other Equity 1822 1189 993

In listed companies, financial accounting is essential task which gather and provide

crucial business data for financial reporting as well as preparation of financial statements.

Companies are required to adopt proper procedures relating to financial accounting along with

compliance requirements. It also assist stakeholder and investor to make momentous investment

decisions (Adesara, 2016). In part A of study, main aim is to provide a complete understanding

of each of the items reported by companies National Australia Bank Ltd and Commonwealth

Bank of Australia in their financial statements. It also covers merits and demerits of fund sources

reported by both corporations. Further part B of study evaluates the concepts of small proprietary

company, large proprietary company and reporting entity. Also, their classification on the basis

of compliance and reporting requirements.

ASSESSMENT TASK:

PART A

(1) Items recorded by selected companies under owners’ equity heading:

National Australia Bank Ltd (NAB):

(AUD in million)

2016 2017 2018

Stockholders' equity

Common stock 34285 34627 35982

Other Equity 617 492 307

Retained earnings 16378 16442 16673

Accumulated other comprehensive income 12 -255 -261

Total stockholders' equity 51292 51306 52701

Commonwealth Bank of Australia (CBA):

(AUD in million)

2016 2017 2018

Stockholders' equity

Common stock 33845 34971 37270

Other Equity 1822 1189 993

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Retained earnings 23627 26330 28360

Accumulated other comprehensive income 912 680 683

Total stockholders' equity 60206 63170 67306

Explanation of understanding about each reported item:

Common Stock and Other Equity: Common stock implies to securities amount in any

corporation which reflects ownership. By appointing a board members and voting on

company policy, owners of common stock perform control. Common stakeholders are

at bottom of the ranking list in relation of ownership framework. At the time of

liquidation, after complete payment of bond holders, preferred investors as well as other

debt-holders has title to a corporation's assets or equity. In this head company has

reported securities issued. Other equity includes any other residual value of common

stock which is not specifically mentioned in other heads of equity.

Retained earnings: In financial reporting, retained earnings relate to part of net profit

that enterprise retains instead of distributes as dividend payments to its securities holders.

Likewise, if corporation loses, that deficit will be conserved and labelled losses which

have been retained accordingly, cumulative losses, or cumulative deficit. Retained

earnings and losses, with losses compensating income, are accumulated year by year.

These are recorded in balance sheet's shareholders ' equity portion (Jie, Xi and Chaoyang,

2015).

Accumulated other comprehensive income: This reported item under equity head of

balance sheet comprises amount and balance of any unrealized profits or loss including

any appropriation or other adjustment. Other-comprehensive earnings includes loss or

profit on any specific kind of investments, employees pension fund plans and foreign

exchange hedging event loss or income. This figure is superficially excluded out of net

profits since these profits and losses still not realized. Stakeholders and Investors by

analysing corporation's balance sheet can apply OCI balance as benchmark to asses any

forthcoming threats or decline in net profits. Unrealized profits and losses from the

pension scheme of a business are usually reported in OCI. Corporations have various

kinds of financing commitments related to pension plan For instance, in upcoming years,

Accumulated other comprehensive income 912 680 683

Total stockholders' equity 60206 63170 67306

Explanation of understanding about each reported item:

Common Stock and Other Equity: Common stock implies to securities amount in any

corporation which reflects ownership. By appointing a board members and voting on

company policy, owners of common stock perform control. Common stakeholders are

at bottom of the ranking list in relation of ownership framework. At the time of

liquidation, after complete payment of bond holders, preferred investors as well as other

debt-holders has title to a corporation's assets or equity. In this head company has

reported securities issued. Other equity includes any other residual value of common

stock which is not specifically mentioned in other heads of equity.

Retained earnings: In financial reporting, retained earnings relate to part of net profit

that enterprise retains instead of distributes as dividend payments to its securities holders.

Likewise, if corporation loses, that deficit will be conserved and labelled losses which

have been retained accordingly, cumulative losses, or cumulative deficit. Retained

earnings and losses, with losses compensating income, are accumulated year by year.

These are recorded in balance sheet's shareholders ' equity portion (Jie, Xi and Chaoyang,

2015).

Accumulated other comprehensive income: This reported item under equity head of

balance sheet comprises amount and balance of any unrealized profits or loss including

any appropriation or other adjustment. Other-comprehensive earnings includes loss or

profit on any specific kind of investments, employees pension fund plans and foreign

exchange hedging event loss or income. This figure is superficially excluded out of net

profits since these profits and losses still not realized. Stakeholders and Investors by

analysing corporation's balance sheet can apply OCI balance as benchmark to asses any

forthcoming threats or decline in net profits. Unrealized profits and losses from the

pension scheme of a business are usually reported in OCI. Corporations have various

kinds of financing commitments related to pension plan For instance, in upcoming years,

a defined benefit plan needs the employee to scheme certain retirement benefits. If

insufficient costs have been deposited in the scheme, liability of pension scheme rises

(Kai, 2015).

(2) Movement in items reported under owner equity section with reason:

Common Stock and other equity:

NAB has reported 34285 million of common stock in year 2016 which is increased to

34627 million and 35982 million in year 2017 and 2018 respectively. In CBA company has

reported common stock of 37270 million in year 2018 which was in 2017 and 2016 of 34971

million and 33845 million respectively. Core reason of increase in common stock is fresh issue

of shares by companies in during 2017 and 2016.

Retained Earnings:

NAB has shown balance of retained earning in year 2018 of 16673 million while in year

2017 and 2016 it was 16442 million and 16378 million respectively. This increase in during the

respective period is net effect of net profit of from continuing operations and net loss from

discontinued operations, dividend payments, Redemption of National Capital Instruments and

transfer in retained earnings. While in CBA retained earning of company was 23627 million in

year 2016 which has been increased to 26330 in year 2017 and 28360 million in year 2018. Here

in this banking company such increase is net impact of Actuarial gains of defined benefit

superannuation-plans, Losses on liabilities (at fair value) due to fluctuation in credit-risk, transfer

to reserves and payment of interim dividends.

Accumulated other-comprehensive income:

CBA has shown in balance sheet -261 million of loss under head of accumulate other-

comprehensive income which was -225 million and 12 million in year 2017 and 2016. Here this

decline is resulted due to other-comprehensive loss in year 2017 and year 2018. While CBA has

reported 683 million of accumulated other-comprehensive income which was 680 million and

912 million in year 2016 and 2017 respectively. This decreasing trend is due to foreign exchange

loss and deficit in head of other-comprehensive income in respective periods (Levi and Newton,

2016).

(3) Items recorded by selected companies under liabilities section:

National Australia Bank Ltd (NAB):

(AUD in million)

insufficient costs have been deposited in the scheme, liability of pension scheme rises

(Kai, 2015).

(2) Movement in items reported under owner equity section with reason:

Common Stock and other equity:

NAB has reported 34285 million of common stock in year 2016 which is increased to

34627 million and 35982 million in year 2017 and 2018 respectively. In CBA company has

reported common stock of 37270 million in year 2018 which was in 2017 and 2016 of 34971

million and 33845 million respectively. Core reason of increase in common stock is fresh issue

of shares by companies in during 2017 and 2016.

Retained Earnings:

NAB has shown balance of retained earning in year 2018 of 16673 million while in year

2017 and 2016 it was 16442 million and 16378 million respectively. This increase in during the

respective period is net effect of net profit of from continuing operations and net loss from

discontinued operations, dividend payments, Redemption of National Capital Instruments and

transfer in retained earnings. While in CBA retained earning of company was 23627 million in

year 2016 which has been increased to 26330 in year 2017 and 28360 million in year 2018. Here

in this banking company such increase is net impact of Actuarial gains of defined benefit

superannuation-plans, Losses on liabilities (at fair value) due to fluctuation in credit-risk, transfer

to reserves and payment of interim dividends.

Accumulated other-comprehensive income:

CBA has shown in balance sheet -261 million of loss under head of accumulate other-

comprehensive income which was -225 million and 12 million in year 2017 and 2016. Here this

decline is resulted due to other-comprehensive loss in year 2017 and year 2018. While CBA has

reported 683 million of accumulated other-comprehensive income which was 680 million and

912 million in year 2016 and 2017 respectively. This decreasing trend is due to foreign exchange

loss and deficit in head of other-comprehensive income in respective periods (Levi and Newton,

2016).

(3) Items recorded by selected companies under liabilities section:

National Australia Bank Ltd (NAB):

(AUD in million)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

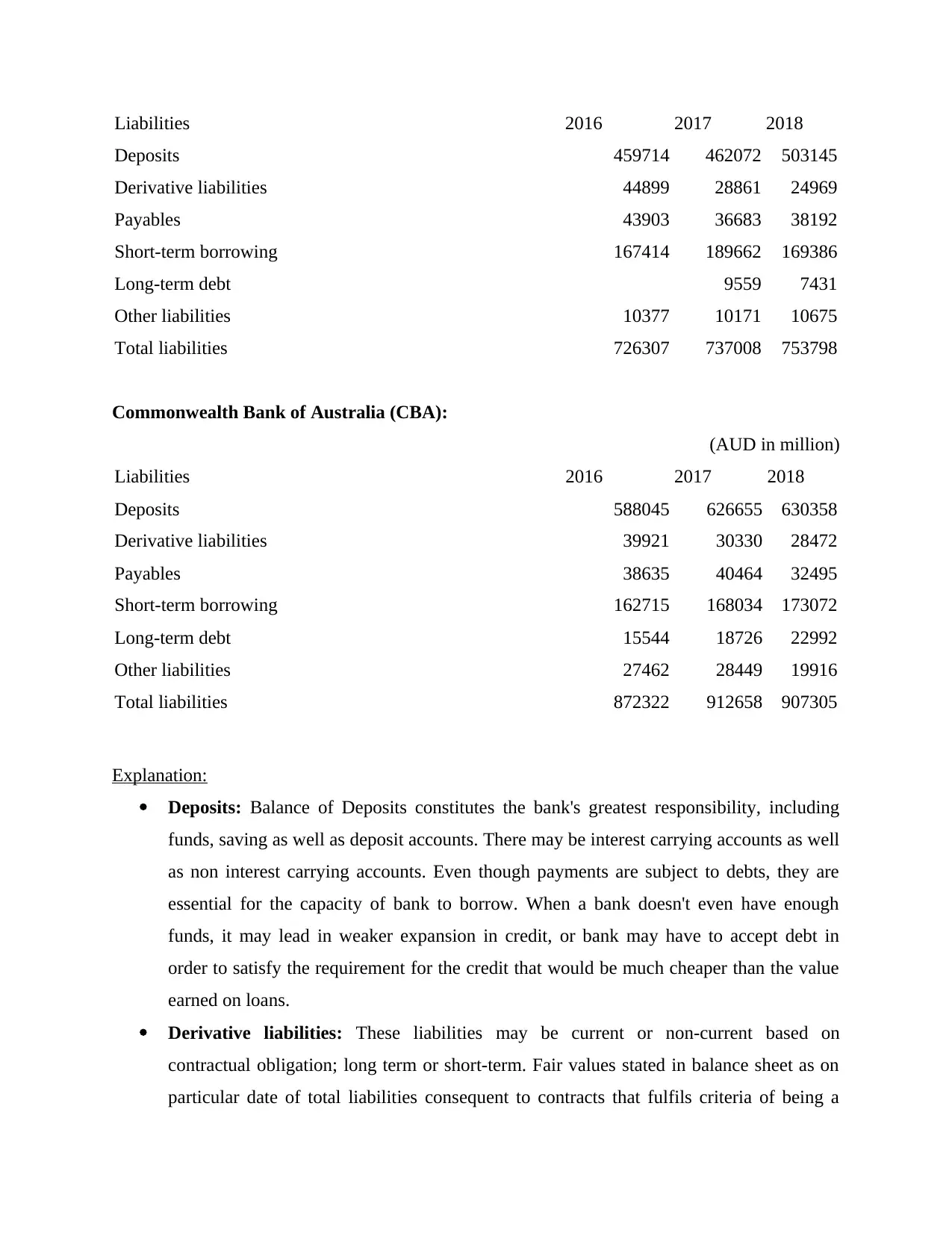

Liabilities 2016 2017 2018

Deposits 459714 462072 503145

Derivative liabilities 44899 28861 24969

Payables 43903 36683 38192

Short-term borrowing 167414 189662 169386

Long-term debt 9559 7431

Other liabilities 10377 10171 10675

Total liabilities 726307 737008 753798

Commonwealth Bank of Australia (CBA):

(AUD in million)

Liabilities 2016 2017 2018

Deposits 588045 626655 630358

Derivative liabilities 39921 30330 28472

Payables 38635 40464 32495

Short-term borrowing 162715 168034 173072

Long-term debt 15544 18726 22992

Other liabilities 27462 28449 19916

Total liabilities 872322 912658 907305

Explanation:

Deposits: Balance of Deposits constitutes the bank's greatest responsibility, including

funds, saving as well as deposit accounts. There may be interest carrying accounts as well

as non interest carrying accounts. Even though payments are subject to debts, they are

essential for the capacity of bank to borrow. When a bank doesn't even have enough

funds, it may lead in weaker expansion in credit, or bank may have to accept debt in

order to satisfy the requirement for the credit that would be much cheaper than the value

earned on loans.

Derivative liabilities: These liabilities may be current or non-current based on

contractual obligation; long term or short-term. Fair values stated in balance sheet as on

particular date of total liabilities consequent to contracts that fulfils criteria of being a

Deposits 459714 462072 503145

Derivative liabilities 44899 28861 24969

Payables 43903 36683 38192

Short-term borrowing 167414 189662 169386

Long-term debt 9559 7431

Other liabilities 10377 10171 10675

Total liabilities 726307 737008 753798

Commonwealth Bank of Australia (CBA):

(AUD in million)

Liabilities 2016 2017 2018

Deposits 588045 626655 630358

Derivative liabilities 39921 30330 28472

Payables 38635 40464 32495

Short-term borrowing 162715 168034 173072

Long-term debt 15544 18726 22992

Other liabilities 27462 28449 19916

Total liabilities 872322 912658 907305

Explanation:

Deposits: Balance of Deposits constitutes the bank's greatest responsibility, including

funds, saving as well as deposit accounts. There may be interest carrying accounts as well

as non interest carrying accounts. Even though payments are subject to debts, they are

essential for the capacity of bank to borrow. When a bank doesn't even have enough

funds, it may lead in weaker expansion in credit, or bank may have to accept debt in

order to satisfy the requirement for the credit that would be much cheaper than the value

earned on loans.

Derivative liabilities: These liabilities may be current or non-current based on

contractual obligation; long term or short-term. Fair values stated in balance sheet as on

particular date of total liabilities consequent to contracts that fulfils criteria of being a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

derivative instruments or contract, and which are anticipated to be disposed off within or

after one year (Peerapongpipath and Hensawang, 2019).

Accounts Payable: It is short-term debt in nature and just opposite of company's

accounts receivable. It occur when corporation acquire or buy product before paying any

amount with respect to such product. Accounts payable is one of the major part of

company's current liabilities and continuous by nature as company orders products on

credit at continuous basis. A listed institution put its effort to sustain accounts payable

balance at high enough in order to cover all current inventories.

Short-term Borrowings: Amount stated in this head in financial statement reflects

aggregate carrying amount of debt carrying initial term of below one year or average one

year of operating cycle. Due to short term repayment cycle debts, these are shown under

this head. In listed companies, these borrowings may go higher in number so managing

and tracking payments of these borrowing is key task for them. In banking corporations

timely payments of short-term borrowings is important as per regulatory compliance.

Long term debts: It includes amount of balance owed for term of more than 12 months.

These debt in bank's balance sheet could be mortgage bonds, inter-bank loan, issued

debentures, or some other obligations which are going to due after one year. Company

should disclose all long-term debts financial statement along with rate of interest and

maturity date. It assist in measurement of company's leverage. Balance and position of

long term debts in company determine it's liquidity position in company.

Other Liabilities: In this section company shows any other long term obligation amount

which are not shown in other headings like any long term contractual obligations.

(4). Explanation about movement in items reported under liabilities head with reason:

Deposits: Both companies belongs to banking sector so this is liability for them. NAB's

deposits are 503145 million, 462072 million and 459714 million in year 2018, 2017 and 2016.

Where as CBA has reported deposits amounting 630358 million, 626655 million and 588045

million in year 2018,2017 and 2016 respectively. In both companies deposits are increasing due

to increase in saving habits in Australians and increase in saving accounts.

Derivative liabilities: CBA has reported current derivative obligation of 28472 million,

30330 million and 39921 million in year 2018,2017 and 2016 respectively. While in NAB's

current liability related to derivative contacts is 24969 million, 28861 million and 44899 million

after one year (Peerapongpipath and Hensawang, 2019).

Accounts Payable: It is short-term debt in nature and just opposite of company's

accounts receivable. It occur when corporation acquire or buy product before paying any

amount with respect to such product. Accounts payable is one of the major part of

company's current liabilities and continuous by nature as company orders products on

credit at continuous basis. A listed institution put its effort to sustain accounts payable

balance at high enough in order to cover all current inventories.

Short-term Borrowings: Amount stated in this head in financial statement reflects

aggregate carrying amount of debt carrying initial term of below one year or average one

year of operating cycle. Due to short term repayment cycle debts, these are shown under

this head. In listed companies, these borrowings may go higher in number so managing

and tracking payments of these borrowing is key task for them. In banking corporations

timely payments of short-term borrowings is important as per regulatory compliance.

Long term debts: It includes amount of balance owed for term of more than 12 months.

These debt in bank's balance sheet could be mortgage bonds, inter-bank loan, issued

debentures, or some other obligations which are going to due after one year. Company

should disclose all long-term debts financial statement along with rate of interest and

maturity date. It assist in measurement of company's leverage. Balance and position of

long term debts in company determine it's liquidity position in company.

Other Liabilities: In this section company shows any other long term obligation amount

which are not shown in other headings like any long term contractual obligations.

(4). Explanation about movement in items reported under liabilities head with reason:

Deposits: Both companies belongs to banking sector so this is liability for them. NAB's

deposits are 503145 million, 462072 million and 459714 million in year 2018, 2017 and 2016.

Where as CBA has reported deposits amounting 630358 million, 626655 million and 588045

million in year 2018,2017 and 2016 respectively. In both companies deposits are increasing due

to increase in saving habits in Australians and increase in saving accounts.

Derivative liabilities: CBA has reported current derivative obligation of 28472 million,

30330 million and 39921 million in year 2018,2017 and 2016 respectively. While in NAB's

current liability related to derivative contacts is 24969 million, 28861 million and 44899 million

in year 2018, 2017 and 2016 respectively. In both companies, during three year company's

derivative liabilities have been declined due to disposal of derivative liabilities.

Payables: NAB's payables in year 2016 was 43903 million which is further reduced to

36683 million in year 2017. However company's payable in year 2018 has been reached to

38192 million. Whereas CBA has reported payables amounting 32495 million, 40464 million

and 38635 million in year 2018,2017 and 2016 respectively. This fluctuation is due to payment

and addition in creditors (Pozniak, Bellanca and Vullo, 2016).

Short-term Borrowings: NAB's short-term borrowings in year 2018 was 169386 million

which was in year 2017 and 2016 of 189622 million and 167414 million. While CBA has

reported short-term borrowing amounting of 162715 million, 168034 million and 173072 million

in year 2016,2017 and 2018 respectively. Main reason of fluctuation in case of both companies

in balance of short-term borrowings is repayment or disposal of short-term debts and addition of

new short-term debts.

Long-term borrowings: In NAB company has taken an inter-bank loan of 9559 million

in year 2017 which has been decreased to 7431 million due to repayment of loan principle.

While in CBA long term debt in year 2018 was 22992 which was 18726 million and 15544

million in year 2017 and year 2016. These increase is due to additional debt funding.

Other Liabilities(Long term): Other liabilities amount in CBA in respect of year 2018

is 19916 million which was 28449 million and 27462 million in year 2017 and 2016

respectively. This is due to disposal of some bank-guarantees and other long term contracts.

Whereas in NAB amount of other liabilities in year 2018 is 10675 million and, 10171 million

and 10377 million respectively in year 2017 and 2016. There has minor reduction due to

payment of other long-term obligations.

(5) Advantages and disadvantages of different sources of funding:

Funding is considerable thing for a listed corporation as it facilitates effective working

and in long run assure entities financial performance. Mainly in companies there are two sources

of funding equity and debt. Both these have specific merits and demerits. Consideration of these

merits and demerits is significant to take vital business decisions. A wrong funding decision can

lead to adverse impact on company's growth. Here in this context following are advantages and

disadvantages of sources from which these companies have raised funds:

derivative liabilities have been declined due to disposal of derivative liabilities.

Payables: NAB's payables in year 2016 was 43903 million which is further reduced to

36683 million in year 2017. However company's payable in year 2018 has been reached to

38192 million. Whereas CBA has reported payables amounting 32495 million, 40464 million

and 38635 million in year 2018,2017 and 2016 respectively. This fluctuation is due to payment

and addition in creditors (Pozniak, Bellanca and Vullo, 2016).

Short-term Borrowings: NAB's short-term borrowings in year 2018 was 169386 million

which was in year 2017 and 2016 of 189622 million and 167414 million. While CBA has

reported short-term borrowing amounting of 162715 million, 168034 million and 173072 million

in year 2016,2017 and 2018 respectively. Main reason of fluctuation in case of both companies

in balance of short-term borrowings is repayment or disposal of short-term debts and addition of

new short-term debts.

Long-term borrowings: In NAB company has taken an inter-bank loan of 9559 million

in year 2017 which has been decreased to 7431 million due to repayment of loan principle.

While in CBA long term debt in year 2018 was 22992 which was 18726 million and 15544

million in year 2017 and year 2016. These increase is due to additional debt funding.

Other Liabilities(Long term): Other liabilities amount in CBA in respect of year 2018

is 19916 million which was 28449 million and 27462 million in year 2017 and 2016

respectively. This is due to disposal of some bank-guarantees and other long term contracts.

Whereas in NAB amount of other liabilities in year 2018 is 10675 million and, 10171 million

and 10377 million respectively in year 2017 and 2016. There has minor reduction due to

payment of other long-term obligations.

(5) Advantages and disadvantages of different sources of funding:

Funding is considerable thing for a listed corporation as it facilitates effective working

and in long run assure entities financial performance. Mainly in companies there are two sources

of funding equity and debt. Both these have specific merits and demerits. Consideration of these

merits and demerits is significant to take vital business decisions. A wrong funding decision can

lead to adverse impact on company's growth. Here in this context following are advantages and

disadvantages of sources from which these companies have raised funds:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Raising Funds through common stock: Both companies have raised fund through issue

of securities or common stock. Under this method company invites application to raise funds by

selling its securities or by issuing new shares. This method is most commonly used by listed

companies and it is also refereed as inviting public deposits (ZHANG and ZHU, 2015).

Following are advantages and disadvantages of raising funds through common stock in context

of both corporations, as follows:

Advantages:

National Australia Bank Ltd (NAB):

This is banking company so raising funds though this source is cost effective and also it

acted as a means for company to generate cost free funds for making expansion in baking sector

and in opening of new branches.

Commonwealth Bank of Australia:

Australian commonwealth bank has unique place in banking sector, so main advantages

here for company is to raise funds by applying this source is enhancement in net-worth.

Disadvantages:

National Australia Bank Ltd (NAB): As company's common stock is continuously

increasing due to issue of share which in long may create disadvantage in term of loss of control

ownership control.

Commonwealth Bank of Australia: Due to inflation or any other reason securities of

company may go downward for a short period. So here disadvantage of company is that this cost

of downsizing in share price can be more than cost of debt.

Long term debts: It is another crucial and widely used method to obtain funds for business.

Both selected corporations have obtained funds through this source for business. Following are

key merits and demerits of raising funds through common stock in context of both corporations,

as follows:

Advantages:

National Australia Bank Ltd (NAB): Here major advantage of funding though this

long-term debt is interest paid by company in respect of loan is generally deductible in

calculation of tax payable while dividend payment are not.

of securities or common stock. Under this method company invites application to raise funds by

selling its securities or by issuing new shares. This method is most commonly used by listed

companies and it is also refereed as inviting public deposits (ZHANG and ZHU, 2015).

Following are advantages and disadvantages of raising funds through common stock in context

of both corporations, as follows:

Advantages:

National Australia Bank Ltd (NAB):

This is banking company so raising funds though this source is cost effective and also it

acted as a means for company to generate cost free funds for making expansion in baking sector

and in opening of new branches.

Commonwealth Bank of Australia:

Australian commonwealth bank has unique place in banking sector, so main advantages

here for company is to raise funds by applying this source is enhancement in net-worth.

Disadvantages:

National Australia Bank Ltd (NAB): As company's common stock is continuously

increasing due to issue of share which in long may create disadvantage in term of loss of control

ownership control.

Commonwealth Bank of Australia: Due to inflation or any other reason securities of

company may go downward for a short period. So here disadvantage of company is that this cost

of downsizing in share price can be more than cost of debt.

Long term debts: It is another crucial and widely used method to obtain funds for business.

Both selected corporations have obtained funds through this source for business. Following are

key merits and demerits of raising funds through common stock in context of both corporations,

as follows:

Advantages:

National Australia Bank Ltd (NAB): Here major advantage of funding though this

long-term debt is interest paid by company in respect of loan is generally deductible in

calculation of tax payable while dividend payment are not.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Commonwealth Bank of Australia: For company here benefit of funding through this

source is that timely repayment of loan can enhance company's creditability and performance in

market.

Disadvantages:

National Australia Bank Ltd (NAB): Any late payment of debt can impact company's

investors' trust and also credit rating.

Commonwealth Bank of Australia: So much dependence upon debt funding can lead to

adverse liquidity position in long run.

PART B

Concepts of small proprietary company, large proprietary company and reporting entity:

A proprietary corporation or company is basically a specific kind of company which is

wholly based on single private ownership or holdings without any public sector or government

influence may be limited in nature or unlimited. These short of corporations not require to

comply with rule of jurisdiction and any formal restrictions since these are not governed by any

specific regulatory. These companies are also further classified into two major kind based on

operations level or scale. These may be small-scale proprietary or large-scale proprietary

corporation. Following are implications of being classified as either one of these three types of

companies in terms of compliance and reporting requirements, as discussed below:

Small scale proprietary company: Small proprietary company/ corporation which meets any of

following discussed key parameters, is regarded as small proprietary enterprise, as follows:

The aggregated amount of revenue of any firm and corporation in any financial year has

reached at level of more than 25 million dollars.

The aggregated assets as on year end date in any financial year of corporation or any

controlled firm is more than the level of $12.5 million.

Employee number in any company is 50 or more at financial year end (ZHANG and

ZHU, 2015).

To become a proprietary company as large-scale proprietary corporation, following discussed

parameter should be fulfilled, as follows:

source is that timely repayment of loan can enhance company's creditability and performance in

market.

Disadvantages:

National Australia Bank Ltd (NAB): Any late payment of debt can impact company's

investors' trust and also credit rating.

Commonwealth Bank of Australia: So much dependence upon debt funding can lead to

adverse liquidity position in long run.

PART B

Concepts of small proprietary company, large proprietary company and reporting entity:

A proprietary corporation or company is basically a specific kind of company which is

wholly based on single private ownership or holdings without any public sector or government

influence may be limited in nature or unlimited. These short of corporations not require to

comply with rule of jurisdiction and any formal restrictions since these are not governed by any

specific regulatory. These companies are also further classified into two major kind based on

operations level or scale. These may be small-scale proprietary or large-scale proprietary

corporation. Following are implications of being classified as either one of these three types of

companies in terms of compliance and reporting requirements, as discussed below:

Small scale proprietary company: Small proprietary company/ corporation which meets any of

following discussed key parameters, is regarded as small proprietary enterprise, as follows:

The aggregated amount of revenue of any firm and corporation in any financial year has

reached at level of more than 25 million dollars.

The aggregated assets as on year end date in any financial year of corporation or any

controlled firm is more than the level of $12.5 million.

Employee number in any company is 50 or more at financial year end (ZHANG and

ZHU, 2015).

To become a proprietary company as large-scale proprietary corporation, following discussed

parameter should be fulfilled, as follows:

Companies having aggregate amount of turnover or revenue in any financial year entity

of $50 million and more.

Companies along with their controlled entities those stated in financial statement amount

of aggregate of its assets at financial year end of amounting $25 million or more.

Company or its group entity having number of employees 100 or more as on financial

year ending.

An annual report along with director's report in respect of each financial year required to be

formulated and filed by large proprietors. Also entire accounts required to be audited and

examined unless there any provision which grants exemption to organization.

Reporting Entity Concept: In 1992, in an effort to decrease disclosure demands by

applying accounting standards, Australian accountant industry embraced this idea. This idea

requires' reporting entity' to draw up a monetary document in conformity with all billing norms

and interpretations known to as General Financial Purpose Reports. On the other side,' non-

reporting entities or organizations' can produce special financial reports for their purposes.

Simply these are entities for those reporting of financial statement is compulsory. Further these

entities have some additional reporting liabilities imposed by concerned regulatory authority.

CONCLUSION

From above discussed study it has been articulated that a deep and walk-through check or

analysis is useful for both investors and owners of company. Evaluation of each balance sheet

item is necessary as it help to recognise some crucial and hidden fact about any particular

corporation. In listed corporates, managerial personnels perform analysis to take strategic and

commercial decisions. Compliance of relevant rules and criteria for different entities is

significant to avoid complexities in business.

of $50 million and more.

Companies along with their controlled entities those stated in financial statement amount

of aggregate of its assets at financial year end of amounting $25 million or more.

Company or its group entity having number of employees 100 or more as on financial

year ending.

An annual report along with director's report in respect of each financial year required to be

formulated and filed by large proprietors. Also entire accounts required to be audited and

examined unless there any provision which grants exemption to organization.

Reporting Entity Concept: In 1992, in an effort to decrease disclosure demands by

applying accounting standards, Australian accountant industry embraced this idea. This idea

requires' reporting entity' to draw up a monetary document in conformity with all billing norms

and interpretations known to as General Financial Purpose Reports. On the other side,' non-

reporting entities or organizations' can produce special financial reports for their purposes.

Simply these are entities for those reporting of financial statement is compulsory. Further these

entities have some additional reporting liabilities imposed by concerned regulatory authority.

CONCLUSION

From above discussed study it has been articulated that a deep and walk-through check or

analysis is useful for both investors and owners of company. Evaluation of each balance sheet

item is necessary as it help to recognise some crucial and hidden fact about any particular

corporation. In listed corporates, managerial personnels perform analysis to take strategic and

commercial decisions. Compliance of relevant rules and criteria for different entities is

significant to avoid complexities in business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.