Financial Accounting: Report on Principles, Concepts, and Clients

VerifiedAdded on 2020/10/05

|16

|4181

|110

Report

AI Summary

This financial accounting report offers a comprehensive overview of key concepts and principles. It begins with an introduction to financial accounting, its purpose, and relevant regulations, including a discussion of accounting principles such as separate legal entity, going concern, and money measurement. The report then explores the conventions of consistency and material disclosure. Client-specific sections delve into sole trader structures, capital, and the advantages and disadvantages associated with each. It also examines the purpose of financial statements as per IAS 1, comparing sole trader financial statements with those of a company. The report covers inventory valuation methods according to IAS 2, the consistency and prudence concepts of accounting, and the purpose and methods of depreciation. Furthermore, it analyzes bank reconciliation statements and the reasons for differences in cash balances, along with the need to prepare control accounts, suspense accounts, and clearing accounts. The report concludes with a summary of the key topics covered and provides a solid foundation for understanding the core elements of financial accounting.

Financial accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

...................................................................................................................1

INTRODUCTION ..........................................................................................................................1

TASK A...........................................................................................................................................1

Financial accounting and its purpose ..........................................................................................1

Regulation related with the financial accounting ........................................................................1

Accounting principles .................................................................................................................2

The conventions and concepts relating to consistency and material disclosure..........................3

B. CLIENT 1....................................................................................................................................3

1. What is sole trader, what is capital with its advantage and disadvantage................................3

CLIENT 2........................................................................................................................................5

2: Purpose of statement as per IAS 1 and difference between sole trader financial statements

and financial statements of a company........................................................................................5

3: The inventory valuation according to IAS 2............................................................................6

CLIENT 3........................................................................................................................................6

C. Consistency and Prudence concept of accounting..................................................................6

D. The purpose of depreciation and the methods of computing depreciation.............................7

CLIENT 4........................................................................................................................................9

A. The purpose of making bank-reconciliation-statement...........................................................9

B. The reason which may cause difference in cash balance vary from bank statements............9

CLIENT 5......................................................................................................................................10

B. What are the need to prepare control account.......................................................................10

CLIENT 6......................................................................................................................................10

A. The different purpose of preparing suspense accounts.........................................................10

D. The difference between suspense account and clearing account..........................................11

CONCLUSION................................................................................................................................1

REFERENCES................................................................................................................................2

...................................................................................................................1

INTRODUCTION ..........................................................................................................................1

TASK A...........................................................................................................................................1

Financial accounting and its purpose ..........................................................................................1

Regulation related with the financial accounting ........................................................................1

Accounting principles .................................................................................................................2

The conventions and concepts relating to consistency and material disclosure..........................3

B. CLIENT 1....................................................................................................................................3

1. What is sole trader, what is capital with its advantage and disadvantage................................3

CLIENT 2........................................................................................................................................5

2: Purpose of statement as per IAS 1 and difference between sole trader financial statements

and financial statements of a company........................................................................................5

3: The inventory valuation according to IAS 2............................................................................6

CLIENT 3........................................................................................................................................6

C. Consistency and Prudence concept of accounting..................................................................6

D. The purpose of depreciation and the methods of computing depreciation.............................7

CLIENT 4........................................................................................................................................9

A. The purpose of making bank-reconciliation-statement...........................................................9

B. The reason which may cause difference in cash balance vary from bank statements............9

CLIENT 5......................................................................................................................................10

B. What are the need to prepare control account.......................................................................10

CLIENT 6......................................................................................................................................10

A. The different purpose of preparing suspense accounts.........................................................10

D. The difference between suspense account and clearing account..........................................11

CONCLUSION................................................................................................................................1

REFERENCES................................................................................................................................2

INTRODUCTION

Financial accounting plays an important role to analyse the financial position of the

company. Present report will provide the deeper insight of the financial accounting with its

terminologies. This assignment is consisted of brief synopsis of the sole trader-ship and its

advantages. The report also provides the different types of inventory valuation methods. It

criticizes the purpose of depreciation, bank reconciliation statements, suspense account. The

report will give the information about the differences between clearing and suspense account.

TASK A

Financial accounting and its purpose

It is a field of accounting that focuses on the analysis of the financial transaction of the

business organization. Financial accounting includes the preparation of the financial statements

available for the public consumption. Financial accounting is that field of accounting which deals

with the business tracks of monetary transaction (Ali and Ahmed, 2017 ). Branch of accounting

which examines all the operations of financial transactions in the organization. It is that branch

which concern with the analysis, summary and reporting of financial statements. A financial

statement on a routine schedule are issued by the company. Every enterprise has the financial

department, and that part of the business is not for everyone. Finance department of the

organization is only handle by the finance manager or the finance executives

The purpose of the financial accounting is to provide the data that is necessary for the

sound decision making. The important purpose of the financial accounting is to make the report

and analyse it so that the organization's financial health can be determined (Bragg, 2017).

Regulation related with the financial accounting

There are number of regulatory bodies that guides the accounting. The regulatory bodies

of accounting includes the certain norms which organization is bound to be follow. There are

some predefined set standard, which decides the working of an organisation. These predefined

norms helps organization to perform better analysis of the financials of the organization. The

regulatory bodies include association, commission, boards etc. they are consisted the specific

working which need to be follow. Some governing bodies of accounting are discussed under-

Security and exchange commission

US. Securities and the exchange commission focuses the objectives to save the investors,

to maintain the fair market working and also ease the formation of the capital (Clarke, Dean and

1

Financial accounting plays an important role to analyse the financial position of the

company. Present report will provide the deeper insight of the financial accounting with its

terminologies. This assignment is consisted of brief synopsis of the sole trader-ship and its

advantages. The report also provides the different types of inventory valuation methods. It

criticizes the purpose of depreciation, bank reconciliation statements, suspense account. The

report will give the information about the differences between clearing and suspense account.

TASK A

Financial accounting and its purpose

It is a field of accounting that focuses on the analysis of the financial transaction of the

business organization. Financial accounting includes the preparation of the financial statements

available for the public consumption. Financial accounting is that field of accounting which deals

with the business tracks of monetary transaction (Ali and Ahmed, 2017 ). Branch of accounting

which examines all the operations of financial transactions in the organization. It is that branch

which concern with the analysis, summary and reporting of financial statements. A financial

statement on a routine schedule are issued by the company. Every enterprise has the financial

department, and that part of the business is not for everyone. Finance department of the

organization is only handle by the finance manager or the finance executives

The purpose of the financial accounting is to provide the data that is necessary for the

sound decision making. The important purpose of the financial accounting is to make the report

and analyse it so that the organization's financial health can be determined (Bragg, 2017).

Regulation related with the financial accounting

There are number of regulatory bodies that guides the accounting. The regulatory bodies

of accounting includes the certain norms which organization is bound to be follow. There are

some predefined set standard, which decides the working of an organisation. These predefined

norms helps organization to perform better analysis of the financials of the organization. The

regulatory bodies include association, commission, boards etc. they are consisted the specific

working which need to be follow. Some governing bodies of accounting are discussed under-

Security and exchange commission

US. Securities and the exchange commission focuses the objectives to save the investors,

to maintain the fair market working and also ease the formation of the capital (Clarke, Dean and

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Graves, 2017). The main motto of security and exchange commission is that to adopt the law that

are passed for the relevant working and guide the enterprise to implement these laws.

The financial accounting standard boards

The financial accounting standard boards were formed in 1973 by the security exchange

commission. It is formed to incorporate the accounting practices by improving the guidelines

made for the accounting reports, finding and resolving the areas in timely manner.

International finance reporting system

International financial reporting system was formed for providing a common business

language which could be understand across the world (Ali and Ahmed, 2017).

Accounting principles

1. Separate legal entity

An enterprise is different from its owner in the eye of accounting law. This principle of

accounting says that the identity of the business is separate from its owner. All the work of the

organization is undertaken individually from that of its owner.

2. Ongoing process

It identifies that organization keeps on working until it does not wind up by the

accounting provisions. More specifically, one cannot close the business with mutual discussion.

Any death or accident cannot stop the working of business or close the business.

3.The specific time period principles

The accounting is always concern with the specific time that is the beginning and the

closing date for the financial statement. It helps reader to identify at what time the particular

transaction has taken place (Bragg, 2017).

4.The historical cost principles

The historical cost is used for the valuation of the items. These are not taken for the

reporting purposes but value of price due change due to recession , inflation.

5.The full disclosure principles

For a business, the full disclosure principle needs a company to give the essential

information so that people who are conventional in reading the financial information can make

the decision.

6. The recognition principles

2

are passed for the relevant working and guide the enterprise to implement these laws.

The financial accounting standard boards

The financial accounting standard boards were formed in 1973 by the security exchange

commission. It is formed to incorporate the accounting practices by improving the guidelines

made for the accounting reports, finding and resolving the areas in timely manner.

International finance reporting system

International financial reporting system was formed for providing a common business

language which could be understand across the world (Ali and Ahmed, 2017).

Accounting principles

1. Separate legal entity

An enterprise is different from its owner in the eye of accounting law. This principle of

accounting says that the identity of the business is separate from its owner. All the work of the

organization is undertaken individually from that of its owner.

2. Ongoing process

It identifies that organization keeps on working until it does not wind up by the

accounting provisions. More specifically, one cannot close the business with mutual discussion.

Any death or accident cannot stop the working of business or close the business.

3.The specific time period principles

The accounting is always concern with the specific time that is the beginning and the

closing date for the financial statement. It helps reader to identify at what time the particular

transaction has taken place (Bragg, 2017).

4.The historical cost principles

The historical cost is used for the valuation of the items. These are not taken for the

reporting purposes but value of price due change due to recession , inflation.

5.The full disclosure principles

For a business, the full disclosure principle needs a company to give the essential

information so that people who are conventional in reading the financial information can make

the decision.

6. The recognition principles

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This principle of accounting says that organization should recognise its revenue and

expenditure at the time whey are accrued.

7. The matching principles

This principal of accounting says that all the income and expenditures are equally treated.

It works on the accrual system of accounting which means for every credit there should be debit

also and vice versa.

8. Money measurement concept

This principal focuses that all the transaction in an organization should be done in the

monetary terms (Clarke, Dean and Graves, 2017).

9. Principle of materiality

It takes place when the bookkeepers has to make the use of their judgement. These

principles of accounting help to correct the in accuracies.

10. Principles of conservative accounting

This principle has been adopted for the betterment of the organization. It says that when the

expenses takes place must be recorded immediately, but in case of income when the actual cash

is being received than only the income has to be record.

The conventions and concepts relating to consistency and material disclosure.

Convention of consistency

This convention on the consistency focus on the accounting practices which are using by

the organisation. This convention says that once the organisation has adopted the accounting

practises will be remain same throughout the time. Consistency doesn't mean inflexibility, if the

requirement of change arises it should be done and its effect should be stated clearly (Bragg,

2017).

Convention of material disclosure

This convention includes that at the time of disclosure of the account all the transactions

have valid proof that from where they are arrives.

B. CLIENT 1

1. What is sole trader, what is capital with its advantage and disadvantage.

Sole trader: It is a business structure where one person is an owner and runs the entire

business. Sole trader is easy to setup as there is only a sole trader who would be liable to all legal

responsibilities related to all aspects of business (Ali and Ahmed, 2017). The sole trader is a self-

3

expenditure at the time whey are accrued.

7. The matching principles

This principal of accounting says that all the income and expenditures are equally treated.

It works on the accrual system of accounting which means for every credit there should be debit

also and vice versa.

8. Money measurement concept

This principal focuses that all the transaction in an organization should be done in the

monetary terms (Clarke, Dean and Graves, 2017).

9. Principle of materiality

It takes place when the bookkeepers has to make the use of their judgement. These

principles of accounting help to correct the in accuracies.

10. Principles of conservative accounting

This principle has been adopted for the betterment of the organization. It says that when the

expenses takes place must be recorded immediately, but in case of income when the actual cash

is being received than only the income has to be record.

The conventions and concepts relating to consistency and material disclosure.

Convention of consistency

This convention on the consistency focus on the accounting practices which are using by

the organisation. This convention says that once the organisation has adopted the accounting

practises will be remain same throughout the time. Consistency doesn't mean inflexibility, if the

requirement of change arises it should be done and its effect should be stated clearly (Bragg,

2017).

Convention of material disclosure

This convention includes that at the time of disclosure of the account all the transactions

have valid proof that from where they are arrives.

B. CLIENT 1

1. What is sole trader, what is capital with its advantage and disadvantage.

Sole trader: It is a business structure where one person is an owner and runs the entire

business. Sole trader is easy to setup as there is only a sole trader who would be liable to all legal

responsibilities related to all aspects of business (Ali and Ahmed, 2017). The sole trader is a self-

3

employed who generally makes all the decisions regarding business activities. A sole trader can

set up his business to buy register on his name, and can hire employees but he will remain the

owner of the company.

Advantage of a sole-trader:

A sole trader has a complete control over the assets and business activities. He will take

the decisions regarding the business.

It is easy to change any business activity as and when it is required for business growth. Sole trader is the simplest form of business to set up and operate.

Disadvantage of sole-trader:

A sole trader has unlimited liability, which means all his income will be at risk if a

business plan fails.

As a sole-trader is alone who is liable to all the risks associated with business activities.

The responsibility of failure is the responsibility of sole-trader only.

Capital: The money which is invested in the business to generate income is refereed as

capital invested (Bragg, 2017.). Capital can be cash or can be considered as financial resources

or assets by which an owner is invested in the business for development and growth of business.

Advantages of capital:

There will be full control on the use of capital invested and how it is used. An owner needs to pay an interest on capital to anyone as it is only the owner's

investment.

Disadvantage of capital:

An owner can lose all its financial resources or assets if business plan fails.

A single person invest money in business that can put his personal property on stakes

which can bring his personal assets on risk.

4

set up his business to buy register on his name, and can hire employees but he will remain the

owner of the company.

Advantage of a sole-trader:

A sole trader has a complete control over the assets and business activities. He will take

the decisions regarding the business.

It is easy to change any business activity as and when it is required for business growth. Sole trader is the simplest form of business to set up and operate.

Disadvantage of sole-trader:

A sole trader has unlimited liability, which means all his income will be at risk if a

business plan fails.

As a sole-trader is alone who is liable to all the risks associated with business activities.

The responsibility of failure is the responsibility of sole-trader only.

Capital: The money which is invested in the business to generate income is refereed as

capital invested (Bragg, 2017.). Capital can be cash or can be considered as financial resources

or assets by which an owner is invested in the business for development and growth of business.

Advantages of capital:

There will be full control on the use of capital invested and how it is used. An owner needs to pay an interest on capital to anyone as it is only the owner's

investment.

Disadvantage of capital:

An owner can lose all its financial resources or assets if business plan fails.

A single person invest money in business that can put his personal property on stakes

which can bring his personal assets on risk.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CLIENT 2

2: Purpose of statement as per IAS 1 and difference between sole trader financial statements and

financial statements of a company

A statement is the report of a company which shows the result of different financial

activities of the business. The accounting data of a company is recording in various types of

statements which are prepared to show different perspective of the position and growth of a

company, that are usually referred as financial statements.

International Accounting Standards set guidelines and according to which, a company

needs to prepare all its financial statements (Clarke, Dean and Graves, 2017). According to the

IAS 1 adopted by IFRS, the financial statements must be presented fairly and should include the

necessary information which can be used by external users like investors, creditors, stakeholders

to make decisions about investing in the company or not.

The purpose of financial statements by IAS are:

The main purpose of financial statements is to provide fair and relevant information

about financial position of a company to the outsider users.

It helps the management of a company to make decisions regarding financial and

operational growth of a company.

Financial statements are prepared that should be understandable and comparable to the

external users of statements.

Difference between sole trader and Ltd. companies’ financial statements:

Basis of Difference Sole trader Limited company

Fillings accounts Sole traders are not required to

submit such accounts.

It prepares the annual accounts

at the end of every accounting

year.

Tax Tax lies on the income of the owner Tax will be imposed on the

company as its a separate legal

entity.

Audit Sole trader's financial statements are Limited company's financial

5

2: Purpose of statement as per IAS 1 and difference between sole trader financial statements and

financial statements of a company

A statement is the report of a company which shows the result of different financial

activities of the business. The accounting data of a company is recording in various types of

statements which are prepared to show different perspective of the position and growth of a

company, that are usually referred as financial statements.

International Accounting Standards set guidelines and according to which, a company

needs to prepare all its financial statements (Clarke, Dean and Graves, 2017). According to the

IAS 1 adopted by IFRS, the financial statements must be presented fairly and should include the

necessary information which can be used by external users like investors, creditors, stakeholders

to make decisions about investing in the company or not.

The purpose of financial statements by IAS are:

The main purpose of financial statements is to provide fair and relevant information

about financial position of a company to the outsider users.

It helps the management of a company to make decisions regarding financial and

operational growth of a company.

Financial statements are prepared that should be understandable and comparable to the

external users of statements.

Difference between sole trader and Ltd. companies’ financial statements:

Basis of Difference Sole trader Limited company

Fillings accounts Sole traders are not required to

submit such accounts.

It prepares the annual accounts

at the end of every accounting

year.

Tax Tax lies on the income of the owner Tax will be imposed on the

company as its a separate legal

entity.

Audit Sole trader's financial statements are Limited company's financial

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

not subjected to audit statements need to be audited

and has to be prepared

according to the regulatory

framework.

Statements Sole traders usually prepares profit

and loss statements.

Limited company has to

prepare balance sheet along

with profit and loss statements.

3: The inventory valuation according to IAS 2

It is the practise of calculating the cost of goods sold and cost of ending inventory

valuation as a monetary value that is assigned to inventory for recording purpose. As per the IAS

2 inventory, it should be valued at the lower cost and net realisable value (Cotton and Dark,

2017.). Net realisable value is the expected amount from selling of the inventory. Cost of

inventory includes all expenditure incurred in bringing the products to its present location and

condition such as transportation, production overheads etc.

Valuation of inventories can be done by three methods as per IAS 2:

First in first out: When there is a large quantity involved, FIFO is considered as a good

method of valuation. In FIFO method, the oldest product will be considered to be sold first, so

the recent value of goods will be recorded in the financial statement. It will help in providing

good valuation of the inventory.

Weighted average cost: This method is used where the inventory's is all same or very similar.

In weighted average method the average cost of production will be assigned to each product.

Actual Cost: It is recording of the product on the basis of the actual cost of material, actual

cost of labour, actual overhead cost incurred etc.

CLIENT 3

C. Consistency and Prudence concept of accounting

Consistency concept: It has the fundamental principle in the preparation for financial

statements. According to this principle, a business entity once adopted an accounting method that

should be used in every accounting year consistently. This principle ensures the consistency of

6

and has to be prepared

according to the regulatory

framework.

Statements Sole traders usually prepares profit

and loss statements.

Limited company has to

prepare balance sheet along

with profit and loss statements.

3: The inventory valuation according to IAS 2

It is the practise of calculating the cost of goods sold and cost of ending inventory

valuation as a monetary value that is assigned to inventory for recording purpose. As per the IAS

2 inventory, it should be valued at the lower cost and net realisable value (Cotton and Dark,

2017.). Net realisable value is the expected amount from selling of the inventory. Cost of

inventory includes all expenditure incurred in bringing the products to its present location and

condition such as transportation, production overheads etc.

Valuation of inventories can be done by three methods as per IAS 2:

First in first out: When there is a large quantity involved, FIFO is considered as a good

method of valuation. In FIFO method, the oldest product will be considered to be sold first, so

the recent value of goods will be recorded in the financial statement. It will help in providing

good valuation of the inventory.

Weighted average cost: This method is used where the inventory's is all same or very similar.

In weighted average method the average cost of production will be assigned to each product.

Actual Cost: It is recording of the product on the basis of the actual cost of material, actual

cost of labour, actual overhead cost incurred etc.

CLIENT 3

C. Consistency and Prudence concept of accounting

Consistency concept: It has the fundamental principle in the preparation for financial

statements. According to this principle, a business entity once adopted an accounting method that

should be used in every accounting year consistently. This principle ensures the consistency of

6

accounting policies and make it easy for the external users to compare the past financial year's

statements over the period.

If a company would change its accounting policies and treatment every year then it would

not be possible to understand and compare the financial statements due to inconsistency (Elkins,

Entwistle, Vaidyanathan and Bastiaansen, 2017.). For example, depreciation can be calculated

through different methods, and if a company is using declining method for two years and

change the method to straight line, it would be difficult to value the fixed assets as comparison

will not be easy for external users.

The consistency concept does allow to change the accounting policies if there are more

than a reasonable ground to do so (Accounting principle, 2018). The principle is admissible if

change in policies or new method will give better, true and fair presentation of company's

financial position.

Prudence Concept: Every share holder will expect the accounting system to fairly show

the facts about financial performance in statements of a company. The prudence concepts of

financial accounting states that financial statements should not overate the assets and income of

company and should not underrate the liability and losses in financial statements. The reports

should not mislead the stakeholders with an over-inflated financial reports (Ioannidou, Ongena,

and Peydró, 2014.) This principle states that expenses of the company should be recorded first,

but the income or revenue should be recorded only once it is realised actually. The financial

statements under prudence concept will give realistic information about performance in a

particular financial year.

D. The purpose of depreciation and the methods of computing depreciation.

Depreciation is used to describe the reduction in the value of fixed assets over a period of

time. The value declines because of the usage, wear and tear and obsolescence. The value of

assets starts decreasing after the date when it is brought. Depreciation is also termed as allocation

of cost of fixed assets as it gives the current value of fixed assets in financial statements.

The purpose of depreciation:

It helps to match the cost of a productive assets to the revenue earned from that assets.

7

statements over the period.

If a company would change its accounting policies and treatment every year then it would

not be possible to understand and compare the financial statements due to inconsistency (Elkins,

Entwistle, Vaidyanathan and Bastiaansen, 2017.). For example, depreciation can be calculated

through different methods, and if a company is using declining method for two years and

change the method to straight line, it would be difficult to value the fixed assets as comparison

will not be easy for external users.

The consistency concept does allow to change the accounting policies if there are more

than a reasonable ground to do so (Accounting principle, 2018). The principle is admissible if

change in policies or new method will give better, true and fair presentation of company's

financial position.

Prudence Concept: Every share holder will expect the accounting system to fairly show

the facts about financial performance in statements of a company. The prudence concepts of

financial accounting states that financial statements should not overate the assets and income of

company and should not underrate the liability and losses in financial statements. The reports

should not mislead the stakeholders with an over-inflated financial reports (Ioannidou, Ongena,

and Peydró, 2014.) This principle states that expenses of the company should be recorded first,

but the income or revenue should be recorded only once it is realised actually. The financial

statements under prudence concept will give realistic information about performance in a

particular financial year.

D. The purpose of depreciation and the methods of computing depreciation.

Depreciation is used to describe the reduction in the value of fixed assets over a period of

time. The value declines because of the usage, wear and tear and obsolescence. The value of

assets starts decreasing after the date when it is brought. Depreciation is also termed as allocation

of cost of fixed assets as it gives the current value of fixed assets in financial statements.

The purpose of depreciation:

It helps to match the cost of a productive assets to the revenue earned from that assets.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Depreciation helps in allocating the cost of assets from balance sheet to expense in profit

and loss statements.

It helps to ascertain the current value of assets.

The main inputs which are required to calculate depreciation is, useful life which is the

productive life period of an asset (Ioannidou, Ongena, and Peydró, 2014). Salvage value, which

the amount company received after disposal of assets. Cost of the assets, it includes the cost like

setup expenses, shipping charges, tax etc.

Main methods of calculating depreciation are:

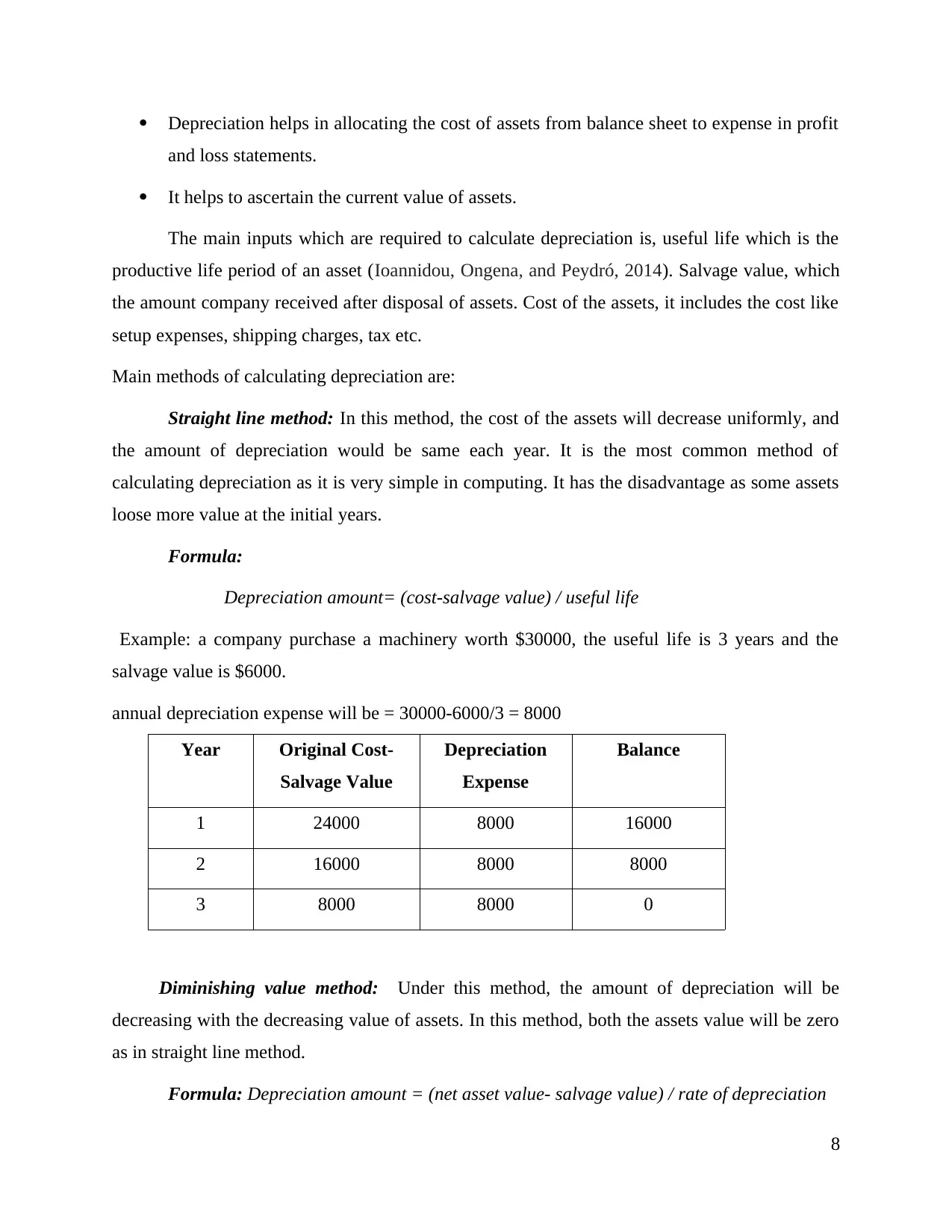

Straight line method: In this method, the cost of the assets will decrease uniformly, and

the amount of depreciation would be same each year. It is the most common method of

calculating depreciation as it is very simple in computing. It has the disadvantage as some assets

loose more value at the initial years.

Formula:

Depreciation amount= (cost-salvage value) / useful life

Example: a company purchase a machinery worth $30000, the useful life is 3 years and the

salvage value is $6000.

annual depreciation expense will be = 30000-6000/3 = 8000

Year Original Cost-

Salvage Value

Depreciation

Expense

Balance

1 24000 8000 16000

2 16000 8000 8000

3 8000 8000 0

Diminishing value method: Under this method, the amount of depreciation will be

decreasing with the decreasing value of assets. In this method, both the assets value will be zero

as in straight line method.

Formula: Depreciation amount = (net asset value- salvage value) / rate of depreciation

8

and loss statements.

It helps to ascertain the current value of assets.

The main inputs which are required to calculate depreciation is, useful life which is the

productive life period of an asset (Ioannidou, Ongena, and Peydró, 2014). Salvage value, which

the amount company received after disposal of assets. Cost of the assets, it includes the cost like

setup expenses, shipping charges, tax etc.

Main methods of calculating depreciation are:

Straight line method: In this method, the cost of the assets will decrease uniformly, and

the amount of depreciation would be same each year. It is the most common method of

calculating depreciation as it is very simple in computing. It has the disadvantage as some assets

loose more value at the initial years.

Formula:

Depreciation amount= (cost-salvage value) / useful life

Example: a company purchase a machinery worth $30000, the useful life is 3 years and the

salvage value is $6000.

annual depreciation expense will be = 30000-6000/3 = 8000

Year Original Cost-

Salvage Value

Depreciation

Expense

Balance

1 24000 8000 16000

2 16000 8000 8000

3 8000 8000 0

Diminishing value method: Under this method, the amount of depreciation will be

decreasing with the decreasing value of assets. In this method, both the assets value will be zero

as in straight line method.

Formula: Depreciation amount = (net asset value- salvage value) / rate of depreciation

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

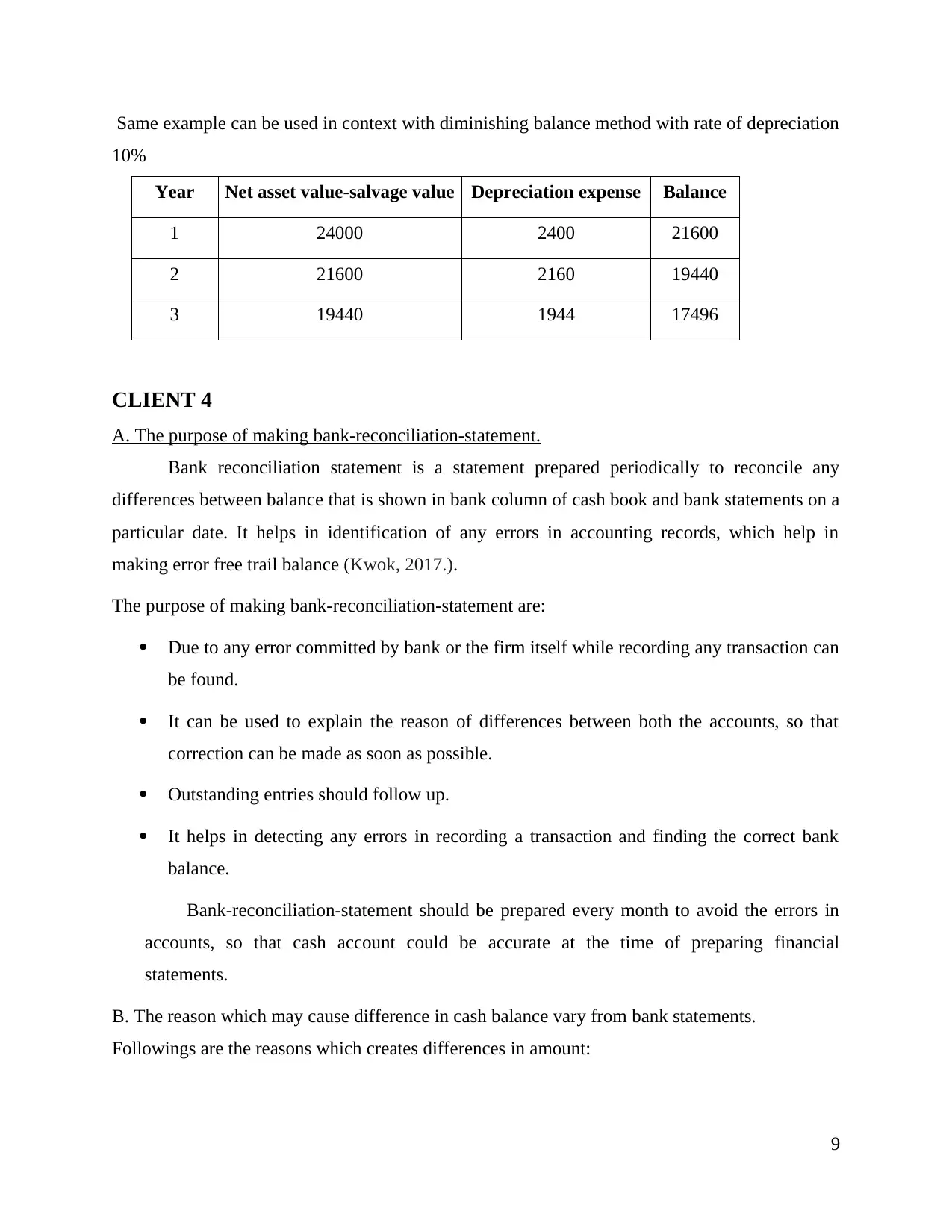

Same example can be used in context with diminishing balance method with rate of depreciation

10%

Year Net asset value-salvage value Depreciation expense Balance

1 24000 2400 21600

2 21600 2160 19440

3 19440 1944 17496

CLIENT 4

A. The purpose of making bank-reconciliation-statement.

Bank reconciliation statement is a statement prepared periodically to reconcile any

differences between balance that is shown in bank column of cash book and bank statements on a

particular date. It helps in identification of any errors in accounting records, which help in

making error free trail balance (Kwok, 2017.).

The purpose of making bank-reconciliation-statement are:

Due to any error committed by bank or the firm itself while recording any transaction can

be found.

It can be used to explain the reason of differences between both the accounts, so that

correction can be made as soon as possible.

Outstanding entries should follow up.

It helps in detecting any errors in recording a transaction and finding the correct bank

balance.

Bank-reconciliation-statement should be prepared every month to avoid the errors in

accounts, so that cash account could be accurate at the time of preparing financial

statements.

B. The reason which may cause difference in cash balance vary from bank statements.

Followings are the reasons which creates differences in amount:

9

10%

Year Net asset value-salvage value Depreciation expense Balance

1 24000 2400 21600

2 21600 2160 19440

3 19440 1944 17496

CLIENT 4

A. The purpose of making bank-reconciliation-statement.

Bank reconciliation statement is a statement prepared periodically to reconcile any

differences between balance that is shown in bank column of cash book and bank statements on a

particular date. It helps in identification of any errors in accounting records, which help in

making error free trail balance (Kwok, 2017.).

The purpose of making bank-reconciliation-statement are:

Due to any error committed by bank or the firm itself while recording any transaction can

be found.

It can be used to explain the reason of differences between both the accounts, so that

correction can be made as soon as possible.

Outstanding entries should follow up.

It helps in detecting any errors in recording a transaction and finding the correct bank

balance.

Bank-reconciliation-statement should be prepared every month to avoid the errors in

accounts, so that cash account could be accurate at the time of preparing financial

statements.

B. The reason which may cause difference in cash balance vary from bank statements.

Followings are the reasons which creates differences in amount:

9

Uncredited items: There are some items which are deposited in banks which are closed

to the cut-off date of bank statements. Hence, they do not appear in bank statements of this

month. While these transactions are recorded by firm in bank column which creates differences

in both accounts.

Unrepresented Cheques: Sometimes, the firm issues the cheque to clients which may not

be presented in bank for payment on same date. It can create differences in recording of

transaction.

Bank charges: There are some services for which the bank charges payment, which firms

come to know after it received statements from bank at the end of month.

Direct Debit: There are some payments which banks made on behalf of firms, to the

customers or suppliers.

Interest allowed by bank: These are interest which are received for deposit or fixed

deposit in bank.

CLIENT 5

B. What are the need to prepare control account.

Control accounts are general ledger accounts which contain the summary of all creditors

and debtors’ balances. There could be hundreds of similar types of general ledger accounts. It

would be very difficult to manage and time consuming for accountant. All the similar type of

accounts is entered in a sub ledger accounts whose total would be equal to control account, like

sales ledger account, purchase ledger accounts etc.

The need to prepare control accounts are:

To check the accuracy of the totals of the accounts.

To locate any errors found in while preparing trail balance.

Control accounts provides an internal check of accountant performance.

Control account helps to manage the general ledger and eliminate the bulky information.

10

to the cut-off date of bank statements. Hence, they do not appear in bank statements of this

month. While these transactions are recorded by firm in bank column which creates differences

in both accounts.

Unrepresented Cheques: Sometimes, the firm issues the cheque to clients which may not

be presented in bank for payment on same date. It can create differences in recording of

transaction.

Bank charges: There are some services for which the bank charges payment, which firms

come to know after it received statements from bank at the end of month.

Direct Debit: There are some payments which banks made on behalf of firms, to the

customers or suppliers.

Interest allowed by bank: These are interest which are received for deposit or fixed

deposit in bank.

CLIENT 5

B. What are the need to prepare control account.

Control accounts are general ledger accounts which contain the summary of all creditors

and debtors’ balances. There could be hundreds of similar types of general ledger accounts. It

would be very difficult to manage and time consuming for accountant. All the similar type of

accounts is entered in a sub ledger accounts whose total would be equal to control account, like

sales ledger account, purchase ledger accounts etc.

The need to prepare control accounts are:

To check the accuracy of the totals of the accounts.

To locate any errors found in while preparing trail balance.

Control accounts provides an internal check of accountant performance.

Control account helps to manage the general ledger and eliminate the bulky information.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.