Financial Accounting Report: FA, Frameworks, and Users

VerifiedAdded on 2021/02/21

|10

|2368

|159

Report

AI Summary

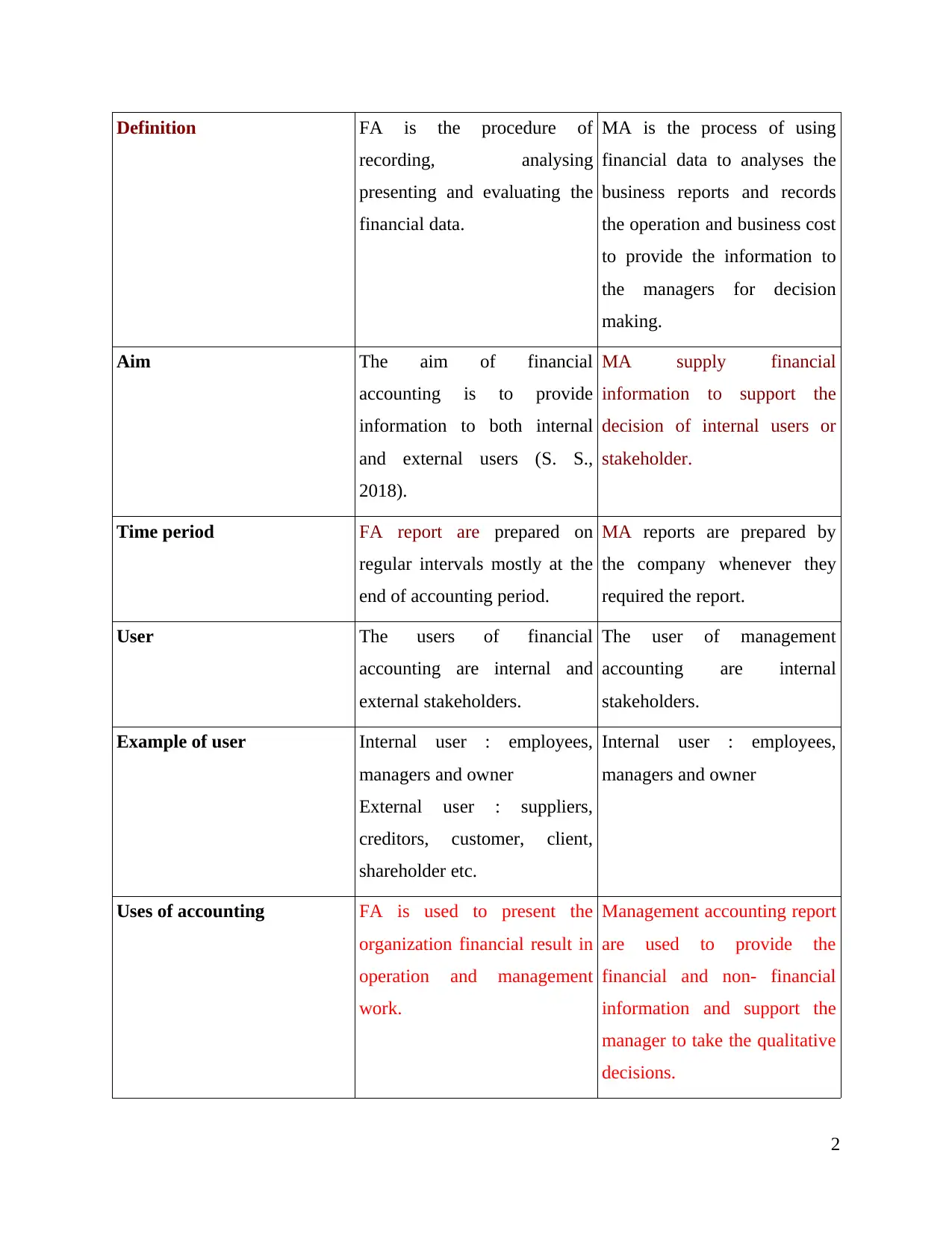

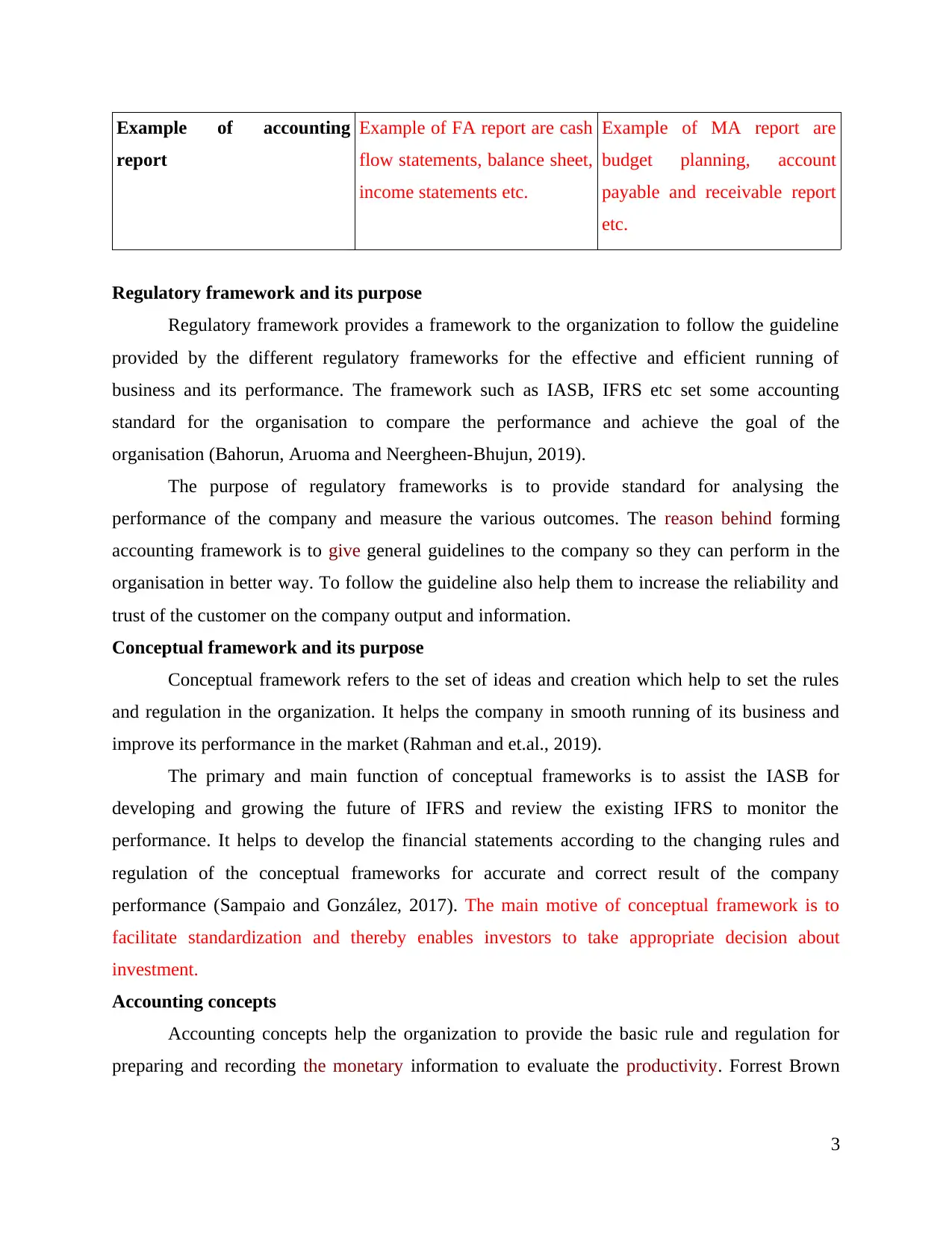

This report provides a comprehensive overview of financial accounting (FA), exploring its purpose, which includes analyzing, recording, and evaluating financial data to provide information to various stakeholders for effective decision-making. It distinguishes between financial accounting and management accounting, highlighting their differences in terms of users, time periods, and the nature of the information provided. The report delves into regulatory and conceptual frameworks, such as IASB and IFRS, emphasizing their role in setting accounting standards and guiding the preparation of financial statements. Furthermore, it explains key accounting concepts like the going concern and accruals concepts, and the qualitative characteristics like relevance, reliability, comparability, and consistency. The report also identifies and describes the different users of financial information, including internal stakeholders (employees and management) and external stakeholders (investors, suppliers, customers, and creditors), detailing their specific interests and how they utilize financial data for their respective purposes. In conclusion, the report summarizes the importance of FA in organizations, its frameworks, concepts, and the diverse needs of its users.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.