Financial Accounting Report: Principles, Stakeholders, and Statements

VerifiedAdded on 2021/02/21

|27

|4954

|48

Report

AI Summary

This report delves into the core principles of financial accounting, emphasizing its purpose in recording, summarizing, and reporting business transactions. It explores the roles of internal and external stakeholders and their interests in financial information. The report includes practical applications through client case studies, demonstrating the preparation of journal entries, trial balances, profit and loss statements, and balance sheets. It covers crucial accounting concepts like consistency and prudence, along with topics such as depreciation, bank reconciliation, and control accounts. The document also differentiates between limited companies and sole traders, offering a comprehensive overview of financial accounting practices and their significance in decision-making.

Financial Accounting

Principles

Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

Part A...............................................................................................................................................4

Define financial accounting and its purposes..............................................................................4

Two internal and four external stakeholders of a large organisation and the reason behind their

interest in the financial information of a company......................................................................6

Part B...............................................................................................................................................7

Client 1.............................................................................................................................................7

a.) Recording journal entries........................................................................................................7

b.) Preparation of Trial balance.................................................................................................15

Client 2...........................................................................................................................................16

a.) Profits and loss statement.....................................................................................................16

b.) Financial position statement.................................................................................................16

c.) Accounting concepts.............................................................................................................18

d.) Purpose of depreciation........................................................................................................18

e.) Distinguish between limited companies and Sole traders....................................................19

Client 3...........................................................................................................................................20

a.) Purpose of BRS....................................................................................................................20

b.) List of factors which vary the records..................................................................................20

c.) Assessment on term “Imprest”.............................................................................................21

d.) Cash book of Burcu Ltd.......................................................................................................21

Client 4...........................................................................................................................................23

a.) Preparation of control account..............................................................................................23

b.) Explanation on term Control account...................................................................................24

Client 5...........................................................................................................................................24

a.) Assessment on term “Suspense account”.............................................................................24

b.) Trial balance.........................................................................................................................25

c.) Rectification of errors in trial balance..................................................................................25

CONCLUSION..............................................................................................................................26

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................4

Part A...............................................................................................................................................4

Define financial accounting and its purposes..............................................................................4

Two internal and four external stakeholders of a large organisation and the reason behind their

interest in the financial information of a company......................................................................6

Part B...............................................................................................................................................7

Client 1.............................................................................................................................................7

a.) Recording journal entries........................................................................................................7

b.) Preparation of Trial balance.................................................................................................15

Client 2...........................................................................................................................................16

a.) Profits and loss statement.....................................................................................................16

b.) Financial position statement.................................................................................................16

c.) Accounting concepts.............................................................................................................18

d.) Purpose of depreciation........................................................................................................18

e.) Distinguish between limited companies and Sole traders....................................................19

Client 3...........................................................................................................................................20

a.) Purpose of BRS....................................................................................................................20

b.) List of factors which vary the records..................................................................................20

c.) Assessment on term “Imprest”.............................................................................................21

d.) Cash book of Burcu Ltd.......................................................................................................21

Client 4...........................................................................................................................................23

a.) Preparation of control account..............................................................................................23

b.) Explanation on term Control account...................................................................................24

Client 5...........................................................................................................................................24

a.) Assessment on term “Suspense account”.............................................................................24

b.) Trial balance.........................................................................................................................25

c.) Rectification of errors in trial balance..................................................................................25

CONCLUSION..............................................................................................................................26

REFERENCES................................................................................................................................1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is a branch of commerce basically concerned with recording,

summarizing and reporting the transactions that are resulted from the business operations over a

period of time. These transactions are used in the preparation of financial statements that include

income statement, balance sheet and cash flow analysis which are useful for both company as

well as outsiders. Double entry concept of book keeping states that every transaction or financial

entry has equal and opposite effects in two different accounts. All the transactions are recorded

in the terms of debit and credit in order to balance the books of accounts. As a junior accountant

of Haines Watts, a small accountancy firm in the United Kingdom that mainly deals with tax

matters and general business services, it is important to identify the rules, principles and

conventions related to accountancy. The current report will emphasize on the purpose of

financial accounting, its effect on stakeholders, preparation of financial statements for different

types of businesses, bank reconciliation and the process to reconcile control accounts.

Part A

Define financial accounting and its purposes.

Financial accounting is basically an organized process through which an organisation's

revenue and expenses are collected, measured, recorded and reported. It is also required by

shareholders, investors and creditors of the company in order to analyse their growth prospects

and overall profitability of the company.

The purpose and objectives of financial accounting are as follows:

Recording: The main purpose of accounting is to keep a record of all the financial

transactions in order to evaluate the overall performance of the company. Systematic

recording helps a company in their growth by evaluating their short comings and working

on them.

Planning: Financial accounting plays an important role in systematic planning regarding

the utilisation of resources. It helps in the preparation of budgets which further leads to

proper coordination within different resources of the company. Hence, it is another

important purpose of financial accounting.

In the view point of Robinson and et.al., (2015) accounting also helps in comparison of

current financial performance with the previous year's and then develop budget or trends

Financial accounting is a branch of commerce basically concerned with recording,

summarizing and reporting the transactions that are resulted from the business operations over a

period of time. These transactions are used in the preparation of financial statements that include

income statement, balance sheet and cash flow analysis which are useful for both company as

well as outsiders. Double entry concept of book keeping states that every transaction or financial

entry has equal and opposite effects in two different accounts. All the transactions are recorded

in the terms of debit and credit in order to balance the books of accounts. As a junior accountant

of Haines Watts, a small accountancy firm in the United Kingdom that mainly deals with tax

matters and general business services, it is important to identify the rules, principles and

conventions related to accountancy. The current report will emphasize on the purpose of

financial accounting, its effect on stakeholders, preparation of financial statements for different

types of businesses, bank reconciliation and the process to reconcile control accounts.

Part A

Define financial accounting and its purposes.

Financial accounting is basically an organized process through which an organisation's

revenue and expenses are collected, measured, recorded and reported. It is also required by

shareholders, investors and creditors of the company in order to analyse their growth prospects

and overall profitability of the company.

The purpose and objectives of financial accounting are as follows:

Recording: The main purpose of accounting is to keep a record of all the financial

transactions in order to evaluate the overall performance of the company. Systematic

recording helps a company in their growth by evaluating their short comings and working

on them.

Planning: Financial accounting plays an important role in systematic planning regarding

the utilisation of resources. It helps in the preparation of budgets which further leads to

proper coordination within different resources of the company. Hence, it is another

important purpose of financial accounting.

In the view point of Robinson and et.al., (2015) accounting also helps in comparison of

current financial performance with the previous year's and then develop budget or trends

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accordingly. Also, the budget acts as a roadmap for the achievement of organisational goals and

objectives efficiently and effectively.

Decision: Another important purpose of financial accounting is that it helps the business

managers in decision-making regarding various aspects of the company. The decisions

can be related to financing, profit or sales maximization or some other business

operations.

According to Legrand, (2017) financial accounting not only helps the company but also

the investors, creditors and shareholders in taking various decisions. This is why financial

accounting is called the backbone of an organisation.

Position: Accounting is concerned with the preparation of financial statements that help

in evaluating the overall performance of the company. It not only helps in inter-firm

comparison but also in intra-firm comparison which is beneficial for the business as it

helps them in identifying their key points and take necessary actions accordingly. In

accordance with Fusch, Hall and Fusch, (2018) the financial position of an organisation

also provides a clear view to its members regarding their actual performance and future

growth prospects.

Financing: The major purpose of financial accounting and statements is to secure funds

for the company, Collison and et.al., (2016) has stated that that the most practical use of

financial statements is to secure finance from commercial banks, financial institutions

and creditors. Also, in order to secure funds from the shareholders and other investors it

is imperative for an organisation to showcase their history of financial performance.

Legal: Financial accounting also serves its legal purpose by acting as an important

document for every business and it is the fundamental duty of a company to follow it

otherwise it may have to face legal consequences. Also Brumbaugh, (2016) has stated

that systematic reporting of financial statements minimizes government intervention and

ensures smooth working of an organisation in the long run. Liquidity: Improper management of cash is one of the most important reason for failure

of a business. Therefore, systematic recording of financial transactions helps an

organisation to keep a regular check on their cash inflows and outflows and manage them

adequately.

Difference between management accounting and financial accounting.

objectives efficiently and effectively.

Decision: Another important purpose of financial accounting is that it helps the business

managers in decision-making regarding various aspects of the company. The decisions

can be related to financing, profit or sales maximization or some other business

operations.

According to Legrand, (2017) financial accounting not only helps the company but also

the investors, creditors and shareholders in taking various decisions. This is why financial

accounting is called the backbone of an organisation.

Position: Accounting is concerned with the preparation of financial statements that help

in evaluating the overall performance of the company. It not only helps in inter-firm

comparison but also in intra-firm comparison which is beneficial for the business as it

helps them in identifying their key points and take necessary actions accordingly. In

accordance with Fusch, Hall and Fusch, (2018) the financial position of an organisation

also provides a clear view to its members regarding their actual performance and future

growth prospects.

Financing: The major purpose of financial accounting and statements is to secure funds

for the company, Collison and et.al., (2016) has stated that that the most practical use of

financial statements is to secure finance from commercial banks, financial institutions

and creditors. Also, in order to secure funds from the shareholders and other investors it

is imperative for an organisation to showcase their history of financial performance.

Legal: Financial accounting also serves its legal purpose by acting as an important

document for every business and it is the fundamental duty of a company to follow it

otherwise it may have to face legal consequences. Also Brumbaugh, (2016) has stated

that systematic reporting of financial statements minimizes government intervention and

ensures smooth working of an organisation in the long run. Liquidity: Improper management of cash is one of the most important reason for failure

of a business. Therefore, systematic recording of financial transactions helps an

organisation to keep a regular check on their cash inflows and outflows and manage them

adequately.

Difference between management accounting and financial accounting.

Financial accounting is a branch of commerce basically concerned with recording,

summarizing and reporting the transactions that are resulted from the business operations over a

period of time. It is very important in analysing the financial position of the organization for

strategic decision making. It complies with various accounting standards such as IAS, IFRS and

GAAP for smooth functioning and reliable information. Financial statements are to be prepared

at the end of every financial year. Financial statements are useful for both external as well as

internal stakeholders. On the contrary, management accounting is an effective process as it helps

in planning, organizing, monitoring and controlling the functioning of the company. It is not

necessary to prepare management reports every year and it does not have to comply with various

accounting standards. Management accounting reports are useful for internal stakeholders of the

company in order to take strategic decision.

Two internal and four external stakeholders of a large organisation and the reason behind their

interest in the financial information of a company.

A stakeholder is an individual or a party that has an interest in the operations of the

organisation and have the power to either affect or get affected by the working of the business.

Stakeholders can be internal as well as external. Internal stakeholders are usually directly

in touch with the company such as employees, investors and board of directors whereas external

stakeholders are not directly related with the company but can be affected by their actions or

changes in operations like suppliers, competitors and customers.

Every stakeholder has a separate reason behind their interest in the financial information

of the company.

Internal stakeholders Employees: Financial statement is the only source of information for the employees of

the company in order to identify the profitability and current position of their business.

Like, the management of the company employees are also interested in financial

information in order to get assurance that the organisation is financially stable to pay

them their salaries and other incentives. Moreover, employees and the workforce of any

organisation are always keen to know the future growth prospects of the company and

their expansion possibilities (Andriof and Waddock, 2017).

Board of directors: Board of directors of the company includes its owners and other

permanent members that take decisions, make policies and control the overall working of

summarizing and reporting the transactions that are resulted from the business operations over a

period of time. It is very important in analysing the financial position of the organization for

strategic decision making. It complies with various accounting standards such as IAS, IFRS and

GAAP for smooth functioning and reliable information. Financial statements are to be prepared

at the end of every financial year. Financial statements are useful for both external as well as

internal stakeholders. On the contrary, management accounting is an effective process as it helps

in planning, organizing, monitoring and controlling the functioning of the company. It is not

necessary to prepare management reports every year and it does not have to comply with various

accounting standards. Management accounting reports are useful for internal stakeholders of the

company in order to take strategic decision.

Two internal and four external stakeholders of a large organisation and the reason behind their

interest in the financial information of a company.

A stakeholder is an individual or a party that has an interest in the operations of the

organisation and have the power to either affect or get affected by the working of the business.

Stakeholders can be internal as well as external. Internal stakeholders are usually directly

in touch with the company such as employees, investors and board of directors whereas external

stakeholders are not directly related with the company but can be affected by their actions or

changes in operations like suppliers, competitors and customers.

Every stakeholder has a separate reason behind their interest in the financial information

of the company.

Internal stakeholders Employees: Financial statement is the only source of information for the employees of

the company in order to identify the profitability and current position of their business.

Like, the management of the company employees are also interested in financial

information in order to get assurance that the organisation is financially stable to pay

them their salaries and other incentives. Moreover, employees and the workforce of any

organisation are always keen to know the future growth prospects of the company and

their expansion possibilities (Andriof and Waddock, 2017).

Board of directors: Board of directors of the company includes its owners and other

permanent members that take decisions, make policies and control the overall working of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

an organisation. Therefore, it is their fundamental right to know about the position of the

company and their overall performance. It also helps them to identify the returns

generated on their investment, growth rate and the profitability of the business.

According to Brem and Viardot, (2015) financial statements and other related

information also help the directors in determining the level of risk and uncertainty

associated with project which helps them to take other important decisions.

External stakeholders Suppliers: Suppliers are the parties that provide raw materials to the business and it is

essential for them to study the financial information in order to identify the position of

the business, their profitability and growth rate. All these factors further help them in

making decisions related to credit facility, discounts, quality and level of risk. It is

imperative for a supplier to ensure that the company has a healthy financial situation and

growth prospects. Government: It helps in determining and effectively evaluating the tax of the company. It

helps government in effectively tracking the progress of the economy. Financial

statement is useful for the government in evaluating whether the company is paying

appropriate amount of tax or not. Managers: Financial statements are very crucial for the owners and managers of the

company. It helps them in analysing the financial position of the company and make

strategic decision for long term sustainable growth and development of the business

(Purpose of Financial Statements, 2017). It helps in determining various factors of the

business and how profitable are they in the long run.

Competitors: Competitors are interested in the financial statements of the company as it

helps them to analyse their performance and develop strategies to improve the

competitiveness.

Part B

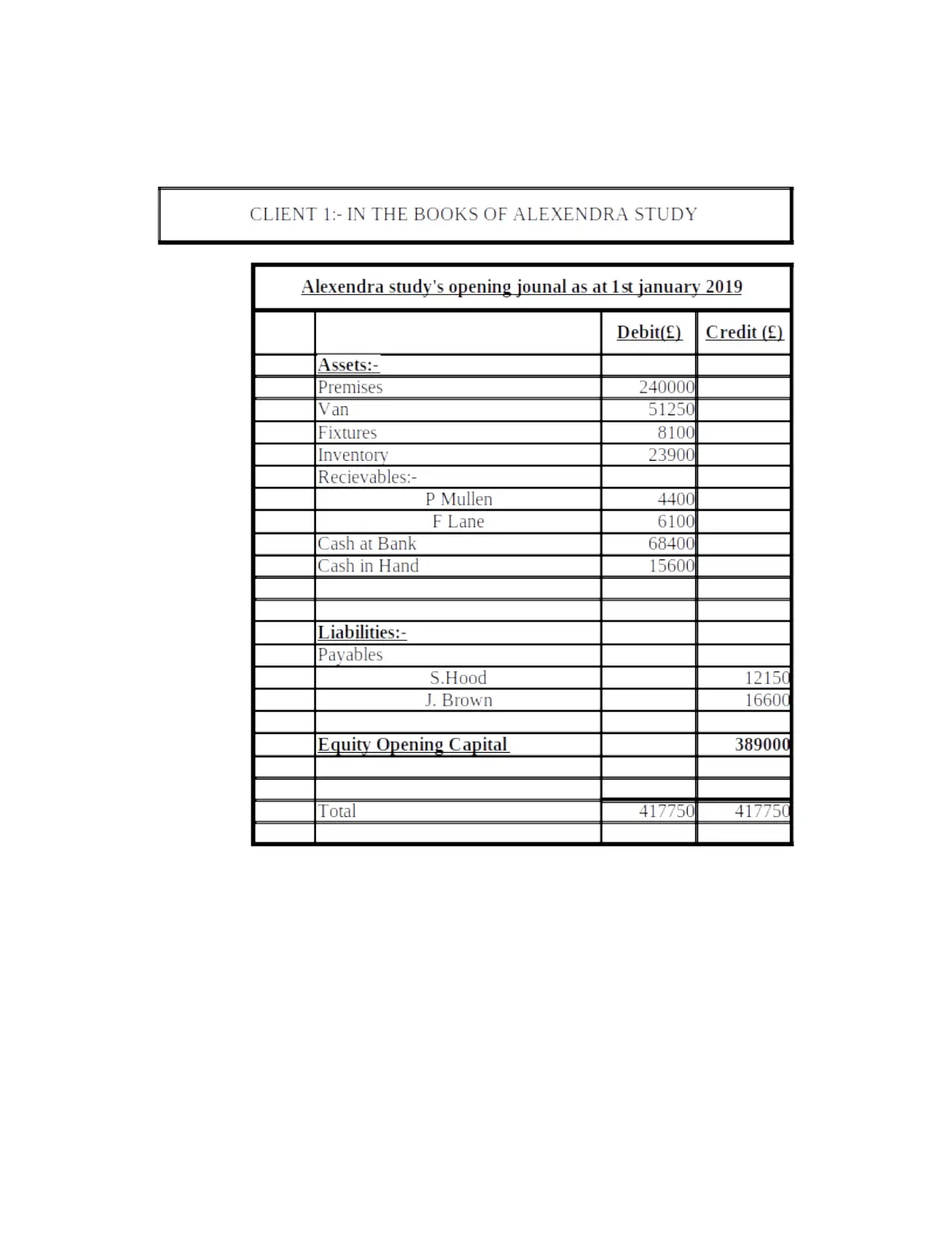

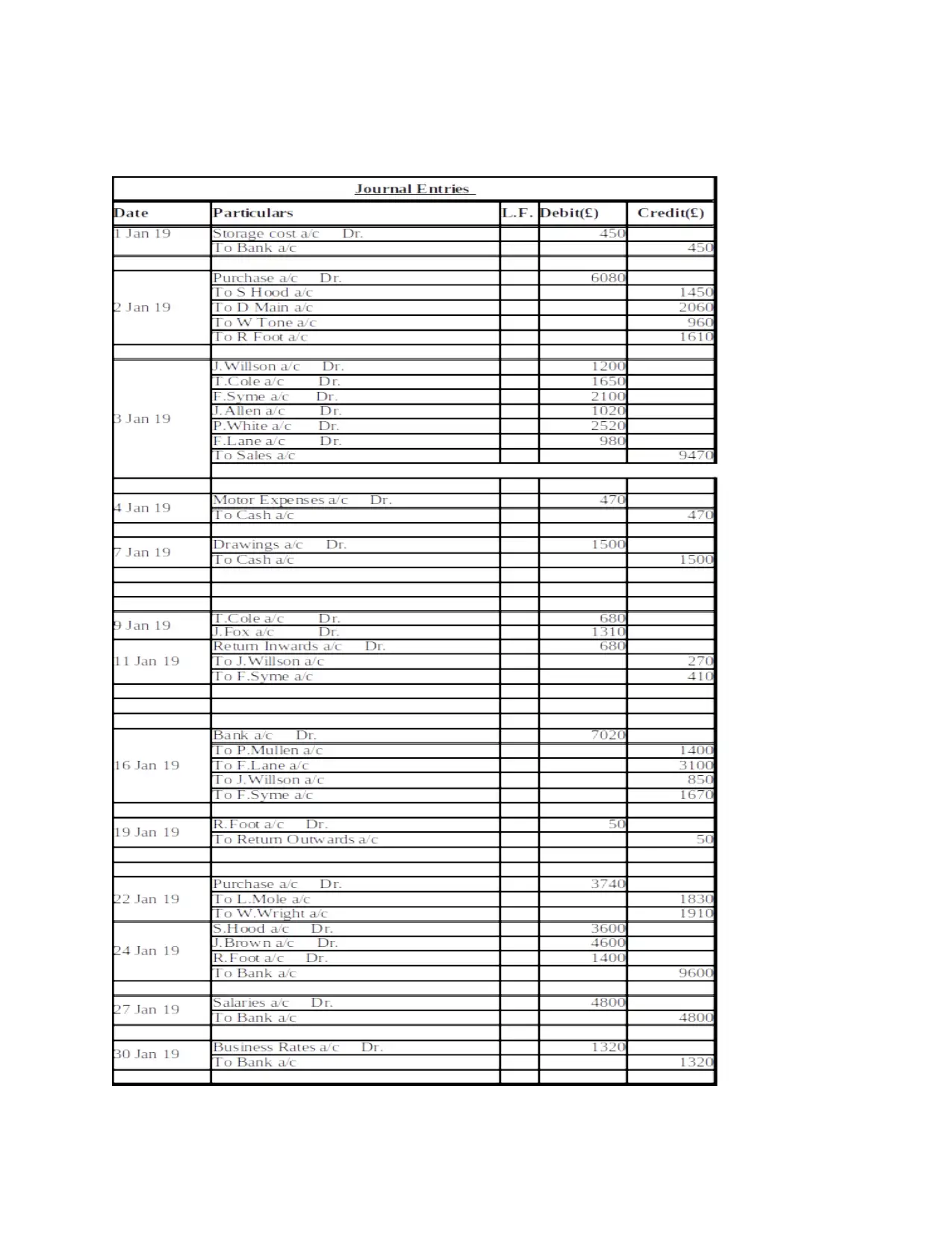

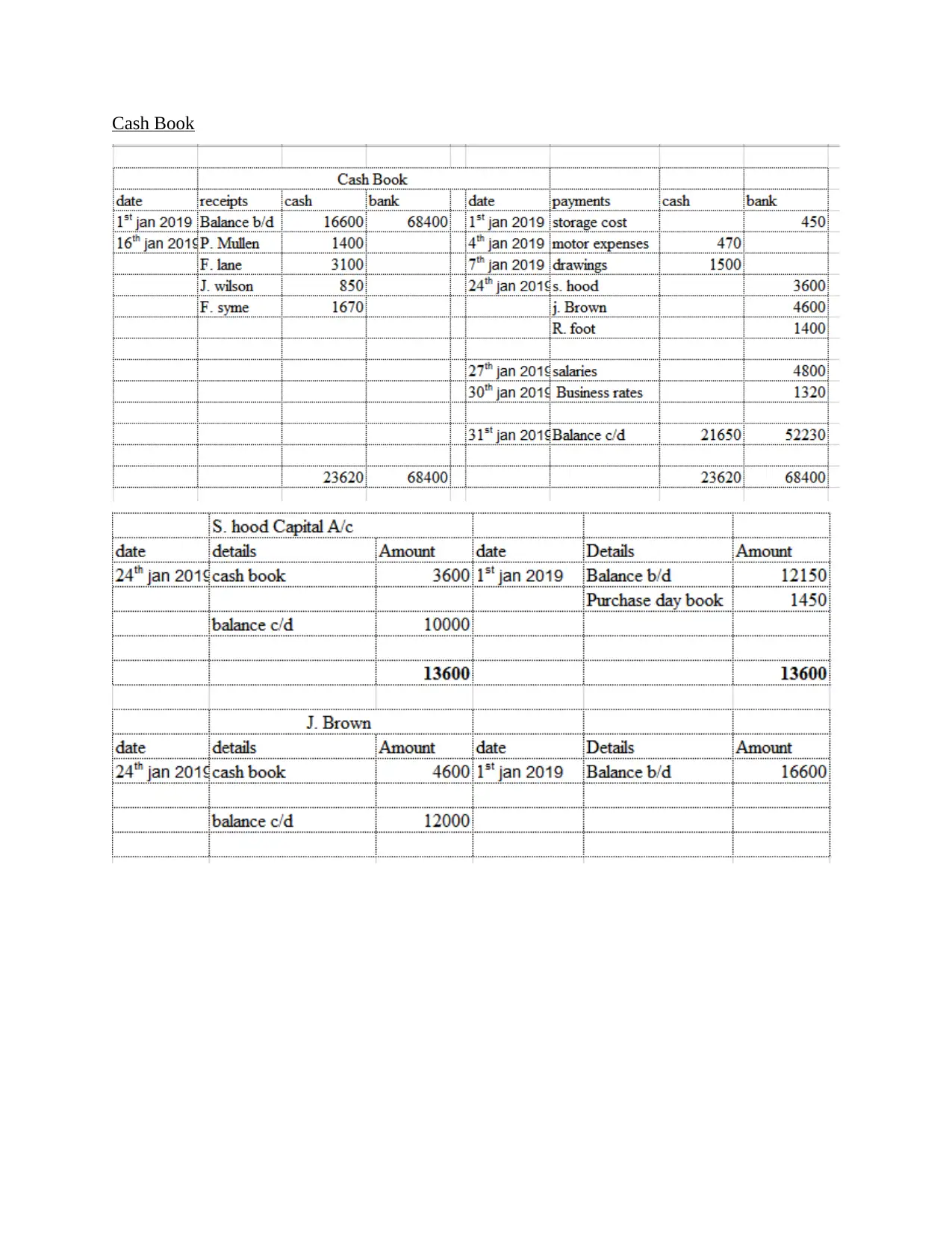

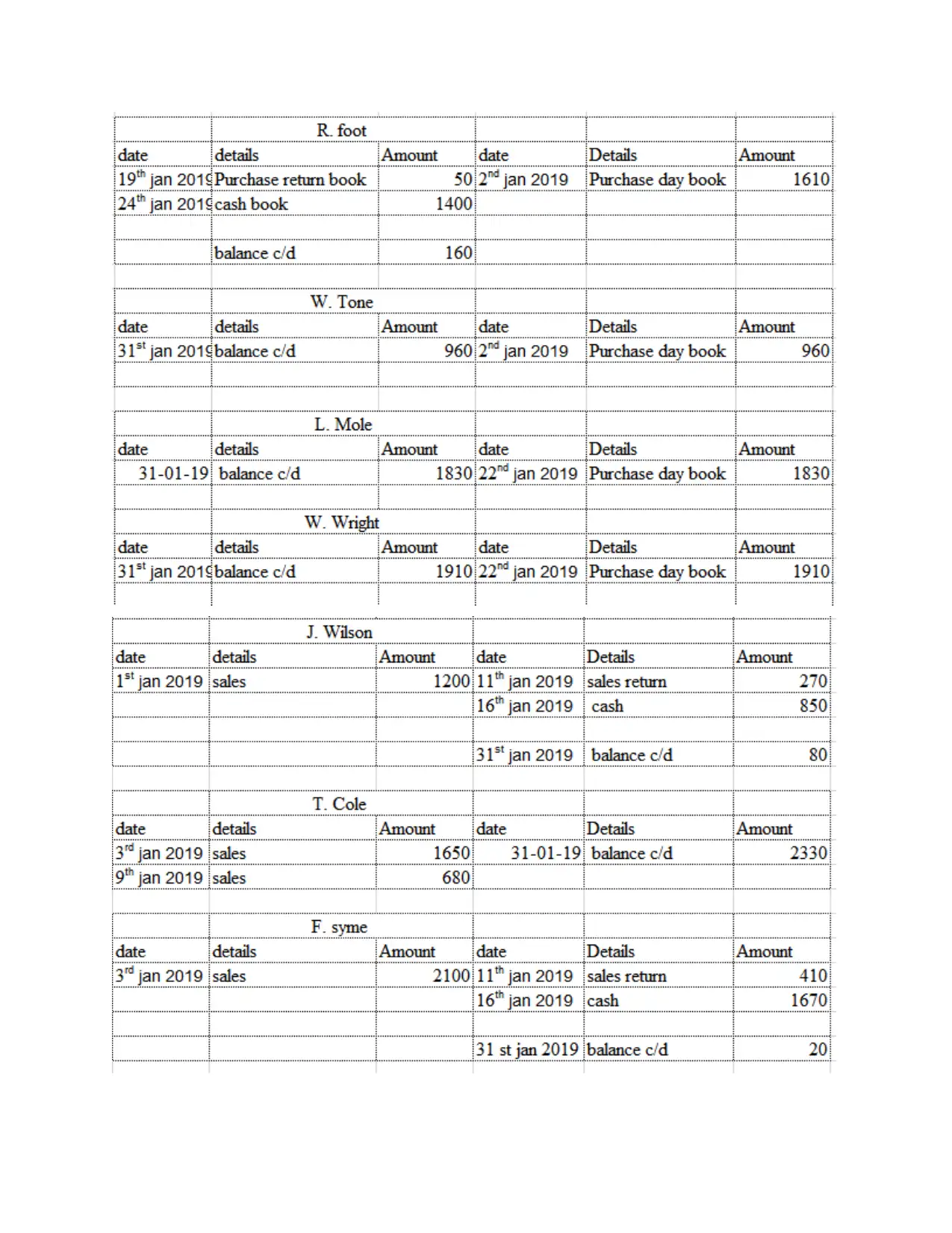

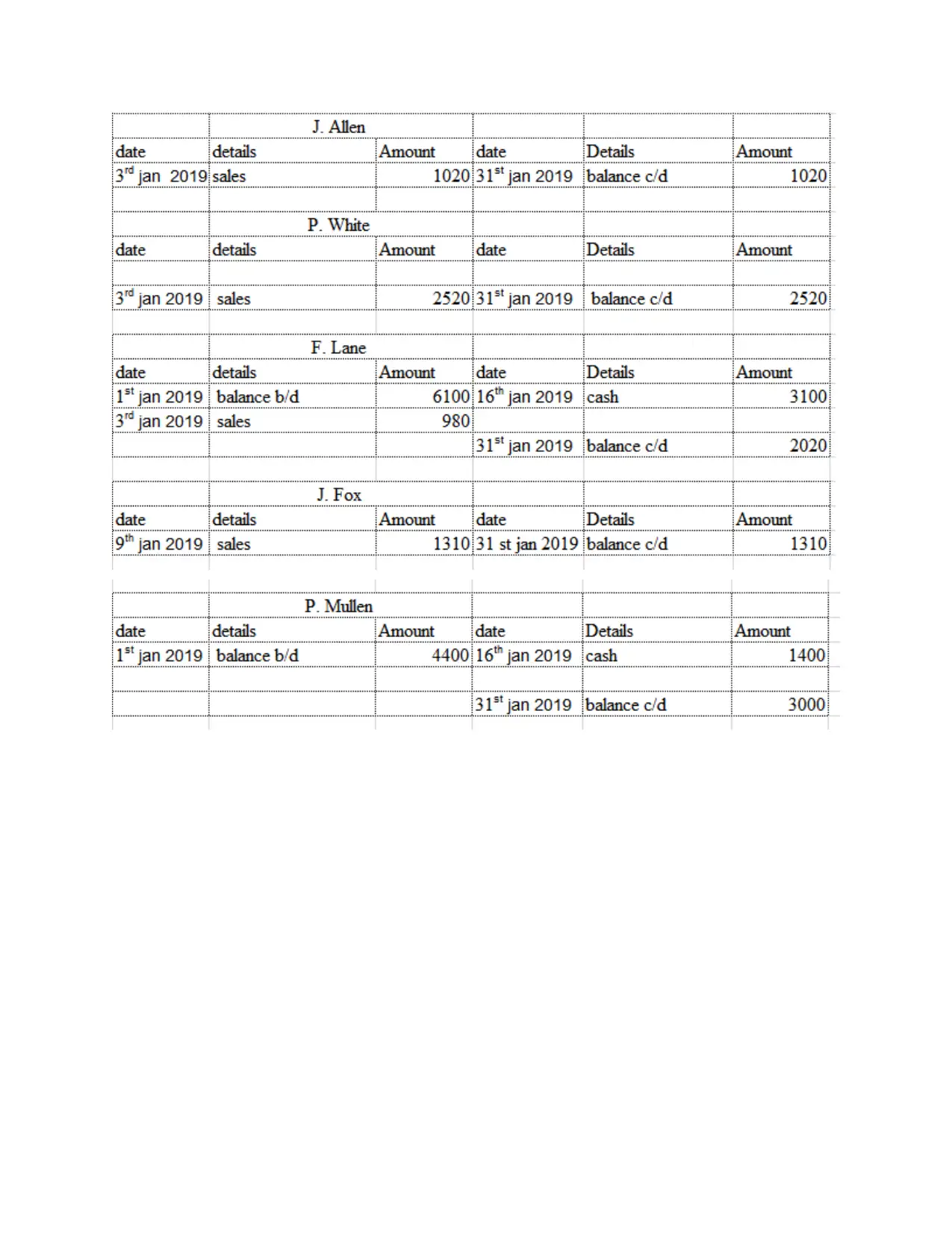

Client 1

a.) Recording journal entries.

company and their overall performance. It also helps them to identify the returns

generated on their investment, growth rate and the profitability of the business.

According to Brem and Viardot, (2015) financial statements and other related

information also help the directors in determining the level of risk and uncertainty

associated with project which helps them to take other important decisions.

External stakeholders Suppliers: Suppliers are the parties that provide raw materials to the business and it is

essential for them to study the financial information in order to identify the position of

the business, their profitability and growth rate. All these factors further help them in

making decisions related to credit facility, discounts, quality and level of risk. It is

imperative for a supplier to ensure that the company has a healthy financial situation and

growth prospects. Government: It helps in determining and effectively evaluating the tax of the company. It

helps government in effectively tracking the progress of the economy. Financial

statement is useful for the government in evaluating whether the company is paying

appropriate amount of tax or not. Managers: Financial statements are very crucial for the owners and managers of the

company. It helps them in analysing the financial position of the company and make

strategic decision for long term sustainable growth and development of the business

(Purpose of Financial Statements, 2017). It helps in determining various factors of the

business and how profitable are they in the long run.

Competitors: Competitors are interested in the financial statements of the company as it

helps them to analyse their performance and develop strategies to improve the

competitiveness.

Part B

Client 1

a.) Recording journal entries.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash Book

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.