Management Accounting Report: Financial and Cost Analysis of ABC Ltd.

VerifiedAdded on 2021/02/20

|16

|5189

|35

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and practices, focusing on their application within a manufacturing company, ABC Ltd. It begins with an introduction to management accounting, defining its role in organizational planning, policy-making, and operational control, with an emphasis on the importance of both financial and non-financial data. The report then delves into the different types of management accounting systems, including inventory management, cost accounting, and job costing systems, highlighting their essential requirements and benefits, particularly within the context of ABC Ltd. Task 2 focuses on the application of marginal and absorption costing techniques, providing detailed calculations and analysis of production costs, profitability, and the preparation of budgeted profit and loss statements. The report also explores the advantages and disadvantages of various planning tools used in budgetary control, and how management accounting systems can contribute to sustainable financial success. The report concludes by summarizing key findings and providing references for further study. This report is contributed by a student to be published on the website Desklib. Desklib is a platform which provides all the necessary AI based study tools for students.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Meaning of management accounting and essential requirements of different types of

management accounting systems................................................................................................3

Different methods for management accounting reporting..........................................................4

Benefits of management accounting system...............................................................................5

Integration of management accounting system with reporting...................................................5

TASK 2............................................................................................................................................6

Application of marginal and absorption costing techniques.......................................................6

TASK 3............................................................................................................................................9

Advantages and disadvantages of various types of planning tools of budgetary control.........10

TASK 4..........................................................................................................................................13

Management accounting system can lead to the sustainable success in relation to solving the

financial issues..........................................................................................................................14

Planning tools for accounting respond accurately to solve the financial issues that leads to the

sustainable success....................................................................................................................14

CONCLUSION .............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Meaning of management accounting and essential requirements of different types of

management accounting systems................................................................................................3

Different methods for management accounting reporting..........................................................4

Benefits of management accounting system...............................................................................5

Integration of management accounting system with reporting...................................................5

TASK 2............................................................................................................................................6

Application of marginal and absorption costing techniques.......................................................6

TASK 3............................................................................................................................................9

Advantages and disadvantages of various types of planning tools of budgetary control.........10

TASK 4..........................................................................................................................................13

Management accounting system can lead to the sustainable success in relation to solving the

financial issues..........................................................................................................................14

Planning tools for accounting respond accurately to solve the financial issues that leads to the

sustainable success....................................................................................................................14

CONCLUSION .............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management Accounting is that part of accounting in which professional knowledge,

techniques and methods are applied to make plans, policies, and managing the operations of an

organization. This information is needed for making managerial decisions which are applied to

internal management. These are based made by considering financial as well as non-financial

data. Generally, these are taken to increase profit of the company (Arnaboldi, Lapsley and

Steccolini, 2015). These are important from the point of view of shareholders as they want to

know where their money is being invested into. The company chosen in this file is ABC Ltd.

which is a medium company operating in manufacturing sector. Furthermore, the report consists

of meaning of management accounting, along with its methods and advantages. The report

further includes preparation of total production cost, per unit cost and income statement. In

addition to this, the advantages and disadvantages of –planning tools and many more matters are

covered.

TASK 1

Meaning of management accounting and essential requirements of different types of

management accounting systems

Definition given by Institute of Cost and Management Accountants defined management

accounting as the application of professional knowledge and skill in the preparation of

accounting information in such a way as to assist management in the formulation of policies and

in the planning and control of the operation of the undertakings. It is a branch of accounting

which deals with internal matters. The main objective of management accounting is to help

establishing plans, policies and decisions which will be applicable within the entity. With regard

to ABC Ltd., management accounting will help in making decisions in carrying out its operations

smoothly along with making higher profit (Booth, 2018). There are different types of

management accounting system which are as follows:

Inventory management system: This system of management accounting has been

developed to handle the inventories or stock of an entity. In other words, it can be defined as

handling the movement of goods into and out of a company. This system is essential as every

organization needs raw materials for turning them into a final product. In the context of ABC

Ltd., this system can provide the accurate information about existing input, WIP and finished

Management Accounting is that part of accounting in which professional knowledge,

techniques and methods are applied to make plans, policies, and managing the operations of an

organization. This information is needed for making managerial decisions which are applied to

internal management. These are based made by considering financial as well as non-financial

data. Generally, these are taken to increase profit of the company (Arnaboldi, Lapsley and

Steccolini, 2015). These are important from the point of view of shareholders as they want to

know where their money is being invested into. The company chosen in this file is ABC Ltd.

which is a medium company operating in manufacturing sector. Furthermore, the report consists

of meaning of management accounting, along with its methods and advantages. The report

further includes preparation of total production cost, per unit cost and income statement. In

addition to this, the advantages and disadvantages of –planning tools and many more matters are

covered.

TASK 1

Meaning of management accounting and essential requirements of different types of

management accounting systems

Definition given by Institute of Cost and Management Accountants defined management

accounting as the application of professional knowledge and skill in the preparation of

accounting information in such a way as to assist management in the formulation of policies and

in the planning and control of the operation of the undertakings. It is a branch of accounting

which deals with internal matters. The main objective of management accounting is to help

establishing plans, policies and decisions which will be applicable within the entity. With regard

to ABC Ltd., management accounting will help in making decisions in carrying out its operations

smoothly along with making higher profit (Booth, 2018). There are different types of

management accounting system which are as follows:

Inventory management system: This system of management accounting has been

developed to handle the inventories or stock of an entity. In other words, it can be defined as

handling the movement of goods into and out of a company. This system is essential as every

organization needs raw materials for turning them into a final product. In the context of ABC

Ltd., this system can provide the accurate information about existing input, WIP and finished

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

goods as well as tracking of all the orders so as to make right decisions in respect to

replenishment of inventories.

Cost accounting system: Cost accounting is one of the financial method, which is about

allocating the costs in manufacturing a product. It takes into account the manufacturing costs

which are attributed to different activities. In the manufacturing process, the making of raw

material to finished goods, have been prepared from estimated cost framed by the finance

department. On the basis of demand required in the market, the marketing manager collaborate

with finance and manufacture department in decision-making for allocation and forecasting of

funds to be used in the manufacturing process.

Job Costing System: Job costing is a technique used for assigning funds for

manufacturing of a job/unit to produce an effective output. Regarding with ABC Ltd., the job

ordering cost is technically used when there is a special order placed on the client based

demands, the cost which are required are measured by the finance department of the company

(Bryer, 2013).

The job costing system is applied on the ABC Ltd., for instance when a custom based

product has to be manufactured, like designing of customised building or customization of trucks

on the basis of client requirement on urgent orders. Then the manufacturing department

communicate with finance manager, for allocation of funds to complete the orders and deliver to

the consumers for effective relationships.

Different methods for management accounting reporting

Inventory report: The inventory report includes the current stock of raw material and how

much to be used in future on the basis of demand in the market. In other words, this reports are

helpful in managing with a transparency of flow of liquidity in the firm. The ABC Ltd., company

uses this report, in such a way that the liquidity flow in overall company gets impacted in

allocating the funds in a single department. With the help of this, the company can manage its

funds accordingly.

Budget report: Budget managerial report are very important in assessing ABC Ltd.,

company through overall function by manufacturing process of finished goods. The finance

department has to allocate funds in an accurate manner so that there is no shortage and surplus of

liquidity in the company. The budgeting reports help the ABC Ltd., company by measuring the

replenishment of inventories.

Cost accounting system: Cost accounting is one of the financial method, which is about

allocating the costs in manufacturing a product. It takes into account the manufacturing costs

which are attributed to different activities. In the manufacturing process, the making of raw

material to finished goods, have been prepared from estimated cost framed by the finance

department. On the basis of demand required in the market, the marketing manager collaborate

with finance and manufacture department in decision-making for allocation and forecasting of

funds to be used in the manufacturing process.

Job Costing System: Job costing is a technique used for assigning funds for

manufacturing of a job/unit to produce an effective output. Regarding with ABC Ltd., the job

ordering cost is technically used when there is a special order placed on the client based

demands, the cost which are required are measured by the finance department of the company

(Bryer, 2013).

The job costing system is applied on the ABC Ltd., for instance when a custom based

product has to be manufactured, like designing of customised building or customization of trucks

on the basis of client requirement on urgent orders. Then the manufacturing department

communicate with finance manager, for allocation of funds to complete the orders and deliver to

the consumers for effective relationships.

Different methods for management accounting reporting

Inventory report: The inventory report includes the current stock of raw material and how

much to be used in future on the basis of demand in the market. In other words, this reports are

helpful in managing with a transparency of flow of liquidity in the firm. The ABC Ltd., company

uses this report, in such a way that the liquidity flow in overall company gets impacted in

allocating the funds in a single department. With the help of this, the company can manage its

funds accordingly.

Budget report: Budget managerial report are very important in assessing ABC Ltd.,

company through overall function by manufacturing process of finished goods. The finance

department has to allocate funds in an accurate manner so that there is no shortage and surplus of

liquidity in the company. The budgeting reports help the ABC Ltd., company by measuring the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cost incurred for generating expenses and revenue of the company. Also providing appropriate

salary to their work force.

Cost accounting report: This report involves, the actual cost that has to be used in the

manufacturing department for purchasing raw material, cost if required for repairing of

machines, labour cost to be paid on daily basis. With the context of ABC Ltd., this cost

accounting report can help the management, by forecasting of ample liquidity to be used in

buying raw material and for the process to be initialised in the manufacturing department.

Benefits of management accounting system

Cost accounting system: This system is concerned with computation of various costs which

are used in making a product in the organization. In this, cost in respect of each product is

computed with different activities (Evans, Burritt, R.O.G.E.R. and Guthrie, 2013). This helps in

making better decision regarding allocating costs in the products. ABC Ltd. can use this

information to have better control on manufacturing cost for increased profit. In producing a

product more than one costs are applied which are in the form of fixed and variable costs, the

identification of these costs are important so that cost can be compared and difference can be

found.

Job costing method: This takes into account the cost that have been spent in producing one

single unit. This system of management accounting helps in tracking the cost so that proper

allocation of remaining costs can be so as to avoid any wastage. In the context of ABC Ltd., they

can have better access to such information so that any unnecessary costs can be avoided. This

will help in increasing the efficiency and more products can be produced with available

resources. When cost of an individual product is ascertained, then better decisions can be made

by making increase of decrease in various costs associated with an individual product.

Inventory management system: This system is very useful for every manufacturing unit

which is engaged in making goods to be sold to customers. Through this system, ABC Ltd. can

have accurate status of its stock so that purchasing decisions can be made (Grabner and Moers,

2013). Every organization is required to keep information which assist it in making decisions by

which inventory can be reorder within prescribed time. Accurate planning regarding inventory

level can be done through this on the basis of trends going on in the market.

salary to their work force.

Cost accounting report: This report involves, the actual cost that has to be used in the

manufacturing department for purchasing raw material, cost if required for repairing of

machines, labour cost to be paid on daily basis. With the context of ABC Ltd., this cost

accounting report can help the management, by forecasting of ample liquidity to be used in

buying raw material and for the process to be initialised in the manufacturing department.

Benefits of management accounting system

Cost accounting system: This system is concerned with computation of various costs which

are used in making a product in the organization. In this, cost in respect of each product is

computed with different activities (Evans, Burritt, R.O.G.E.R. and Guthrie, 2013). This helps in

making better decision regarding allocating costs in the products. ABC Ltd. can use this

information to have better control on manufacturing cost for increased profit. In producing a

product more than one costs are applied which are in the form of fixed and variable costs, the

identification of these costs are important so that cost can be compared and difference can be

found.

Job costing method: This takes into account the cost that have been spent in producing one

single unit. This system of management accounting helps in tracking the cost so that proper

allocation of remaining costs can be so as to avoid any wastage. In the context of ABC Ltd., they

can have better access to such information so that any unnecessary costs can be avoided. This

will help in increasing the efficiency and more products can be produced with available

resources. When cost of an individual product is ascertained, then better decisions can be made

by making increase of decrease in various costs associated with an individual product.

Inventory management system: This system is very useful for every manufacturing unit

which is engaged in making goods to be sold to customers. Through this system, ABC Ltd. can

have accurate status of its stock so that purchasing decisions can be made (Grabner and Moers,

2013). Every organization is required to keep information which assist it in making decisions by

which inventory can be reorder within prescribed time. Accurate planning regarding inventory

level can be done through this on the basis of trends going on in the market.

Integration of management accounting system with reporting

Management accounting system is a wide concept which involves number of systems in it

which have already been described above. These are inventory accounting system, job costing

system, and many more. Every system is based on some information which are required to

prepared in a report form, hence, reporting in necessary in every type of systems. In the case of

ABC Ltd. is a manufacturing thus, it is important to prepare report to keep all the data in a

concise form. Reports like inventory, cost accounting etc. are prepared with the existing data of

cost, hence it these two are integrated with each other.

TASK 2

Application of marginal and absorption costing techniques

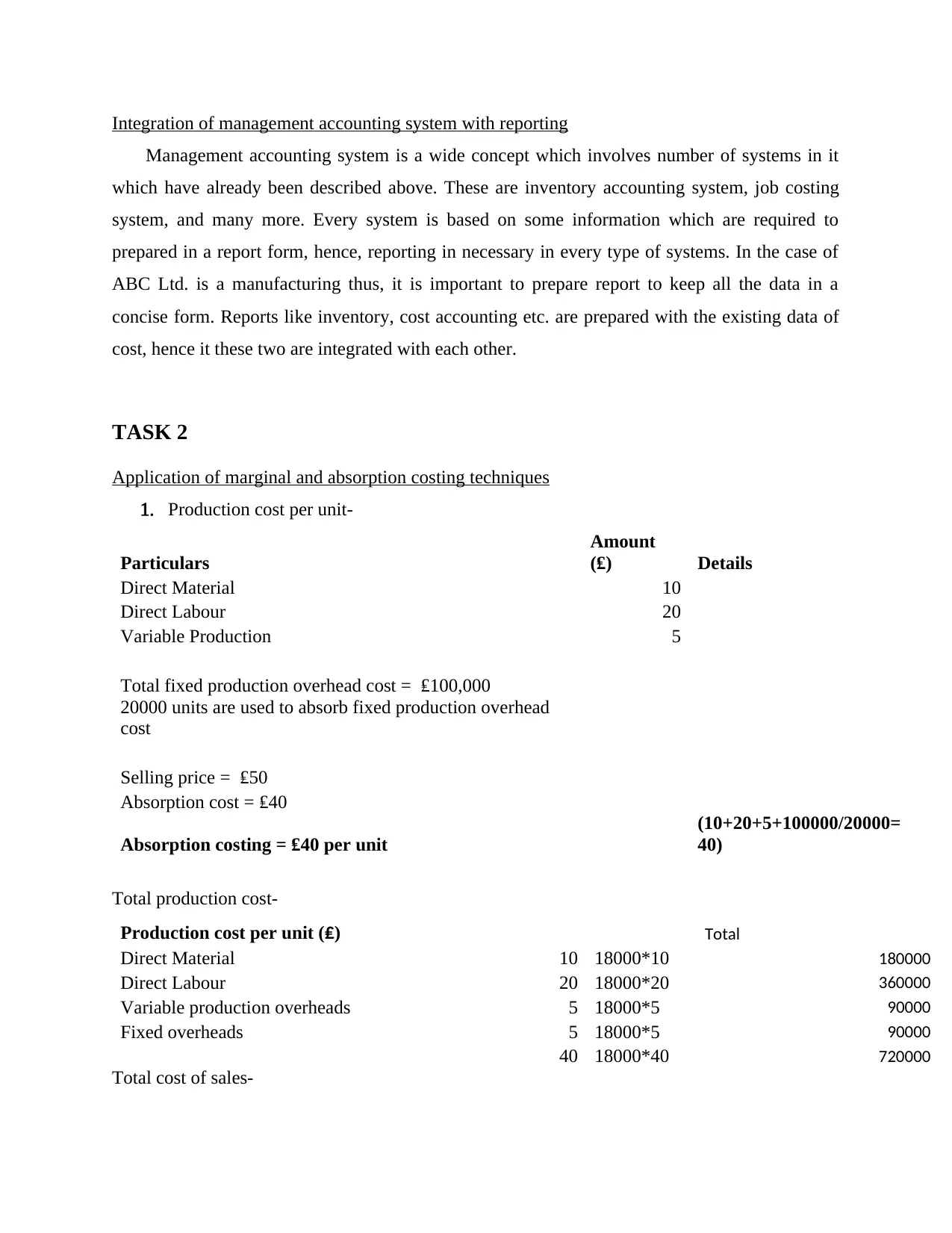

1. Production cost per unit-

Particulars

Amount

(₤) Details

Direct Material 10

Direct Labour 20

Variable Production 5

Total fixed production overhead cost = ₤100,000

20000 units are used to absorb fixed production overhead

cost

Selling price = ₤50

Absorption cost = ₤40

Absorption costing = ₤40 per unit

(10+20+5+100000/20000=

40)

Total production cost-

Production cost per unit (₤) Total

Direct Material 10 18000*10 180000

Direct Labour 20 18000*20 360000

Variable production overheads 5 18000*5 90000

Fixed overheads 5 18000*5 90000

40 18000*40 720000

Total cost of sales-

Management accounting system is a wide concept which involves number of systems in it

which have already been described above. These are inventory accounting system, job costing

system, and many more. Every system is based on some information which are required to

prepared in a report form, hence, reporting in necessary in every type of systems. In the case of

ABC Ltd. is a manufacturing thus, it is important to prepare report to keep all the data in a

concise form. Reports like inventory, cost accounting etc. are prepared with the existing data of

cost, hence it these two are integrated with each other.

TASK 2

Application of marginal and absorption costing techniques

1. Production cost per unit-

Particulars

Amount

(₤) Details

Direct Material 10

Direct Labour 20

Variable Production 5

Total fixed production overhead cost = ₤100,000

20000 units are used to absorb fixed production overhead

cost

Selling price = ₤50

Absorption cost = ₤40

Absorption costing = ₤40 per unit

(10+20+5+100000/20000=

40)

Total production cost-

Production cost per unit (₤) Total

Direct Material 10 18000*10 180000

Direct Labour 20 18000*20 360000

Variable production overheads 5 18000*5 90000

Fixed overheads 5 18000*5 90000

40 18000*40 720000

Total cost of sales-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

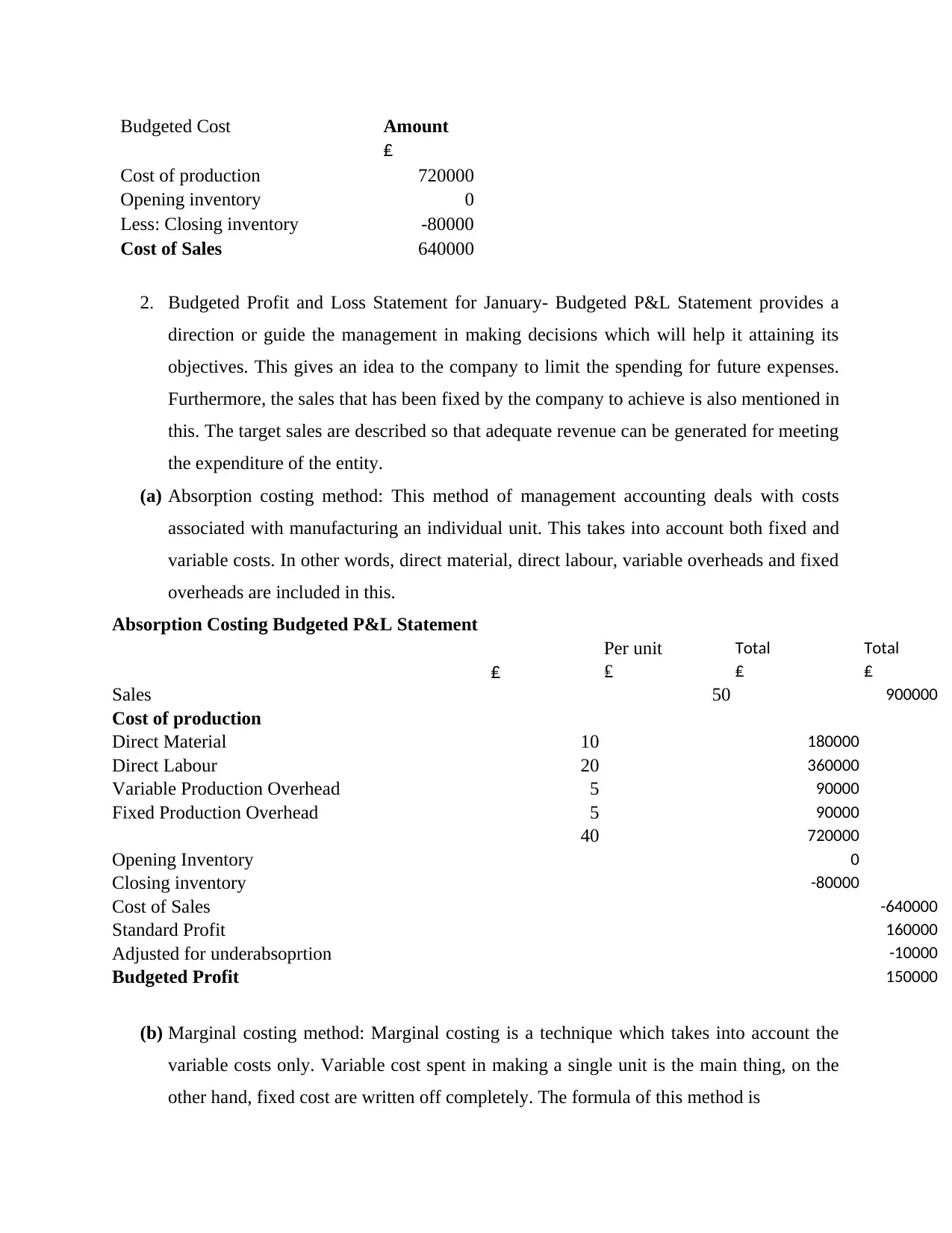

Budgeted Cost Amount

₤

Cost of production 720000

Opening inventory 0

Less: Closing inventory -80000

Cost of Sales 640000

2. Budgeted Profit and Loss Statement for January- Budgeted P&L Statement provides a

direction or guide the management in making decisions which will help it attaining its

objectives. This gives an idea to the company to limit the spending for future expenses.

Furthermore, the sales that has been fixed by the company to achieve is also mentioned in

this. The target sales are described so that adequate revenue can be generated for meeting

the expenditure of the entity.

(a) Absorption costing method: This method of management accounting deals with costs

associated with manufacturing an individual unit. This takes into account both fixed and

variable costs. In other words, direct material, direct labour, variable overheads and fixed

overheads are included in this.

Absorption Costing Budgeted P&L Statement

Per unit Total Total

₤ ₤ ₤ ₤

Sales 50 900000

Cost of production

Direct Material 10 180000

Direct Labour 20 360000

Variable Production Overhead 5 90000

Fixed Production Overhead 5 90000

40 720000

Opening Inventory 0

Closing inventory -80000

Cost of Sales -640000

Standard Profit 160000

Adjusted for underabsoprtion -10000

Budgeted Profit 150000

(b) Marginal costing method: Marginal costing is a technique which takes into account the

variable costs only. Variable cost spent in making a single unit is the main thing, on the

other hand, fixed cost are written off completely. The formula of this method is

₤

Cost of production 720000

Opening inventory 0

Less: Closing inventory -80000

Cost of Sales 640000

2. Budgeted Profit and Loss Statement for January- Budgeted P&L Statement provides a

direction or guide the management in making decisions which will help it attaining its

objectives. This gives an idea to the company to limit the spending for future expenses.

Furthermore, the sales that has been fixed by the company to achieve is also mentioned in

this. The target sales are described so that adequate revenue can be generated for meeting

the expenditure of the entity.

(a) Absorption costing method: This method of management accounting deals with costs

associated with manufacturing an individual unit. This takes into account both fixed and

variable costs. In other words, direct material, direct labour, variable overheads and fixed

overheads are included in this.

Absorption Costing Budgeted P&L Statement

Per unit Total Total

₤ ₤ ₤ ₤

Sales 50 900000

Cost of production

Direct Material 10 180000

Direct Labour 20 360000

Variable Production Overhead 5 90000

Fixed Production Overhead 5 90000

40 720000

Opening Inventory 0

Closing inventory -80000

Cost of Sales -640000

Standard Profit 160000

Adjusted for underabsoprtion -10000

Budgeted Profit 150000

(b) Marginal costing method: Marginal costing is a technique which takes into account the

variable costs only. Variable cost spent in making a single unit is the main thing, on the

other hand, fixed cost are written off completely. The formula of this method is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marginal cost = Direct Material + Direct Labour + direct Expenses + Variable

Overheads

variable costing: budgeted profit or

loss statement

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 35 630000

OPENING INVENTORY 0

CLOSING INVENTORY -70000

COST OF SALES 35 560000

CONTRIBUTION 15 240000

FOH PRODUCTION -100000

BUDGETED PROFIT 140000

Actual P&L statement: Absorption costing method

ABSORPTION COSTING: ACTUAL

PROFIT OR LOSS STATEMENT

SEP 2018

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 190000

DL 20 380000

Overheads

variable costing: budgeted profit or

loss statement

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 35 630000

OPENING INVENTORY 0

CLOSING INVENTORY -70000

COST OF SALES 35 560000

CONTRIBUTION 15 240000

FOH PRODUCTION -100000

BUDGETED PROFIT 140000

Actual P&L statement: Absorption costing method

ABSORPTION COSTING: ACTUAL

PROFIT OR LOSS STATEMENT

SEP 2018

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 190000

DL 20 380000

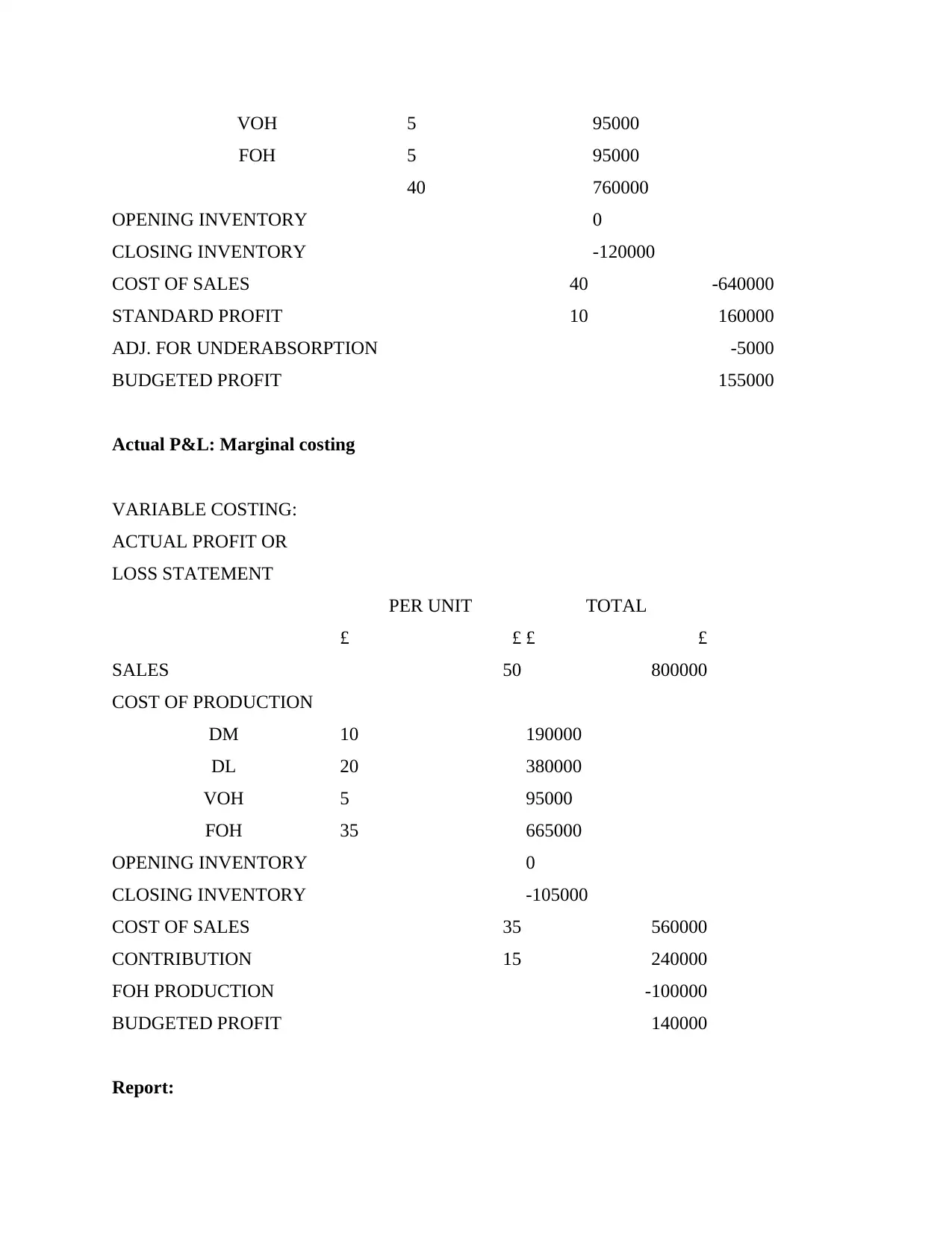

VOH 5 95000

FOH 5 95000

40 760000

OPENING INVENTORY 0

CLOSING INVENTORY -120000

COST OF SALES 40 -640000

STANDARD PROFIT 10 160000

ADJ. FOR UNDERABSORPTION -5000

BUDGETED PROFIT 155000

Actual P&L: Marginal costing

VARIABLE COSTING:

ACTUAL PROFIT OR

LOSS STATEMENT

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 190000

DL 20 380000

VOH 5 95000

FOH 35 665000

OPENING INVENTORY 0

CLOSING INVENTORY -105000

COST OF SALES 35 560000

CONTRIBUTION 15 240000

FOH PRODUCTION -100000

BUDGETED PROFIT 140000

Report:

FOH 5 95000

40 760000

OPENING INVENTORY 0

CLOSING INVENTORY -120000

COST OF SALES 40 -640000

STANDARD PROFIT 10 160000

ADJ. FOR UNDERABSORPTION -5000

BUDGETED PROFIT 155000

Actual P&L: Marginal costing

VARIABLE COSTING:

ACTUAL PROFIT OR

LOSS STATEMENT

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 190000

DL 20 380000

VOH 5 95000

FOH 35 665000

OPENING INVENTORY 0

CLOSING INVENTORY -105000

COST OF SALES 35 560000

CONTRIBUTION 15 240000

FOH PRODUCTION -100000

BUDGETED PROFIT 140000

Report:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

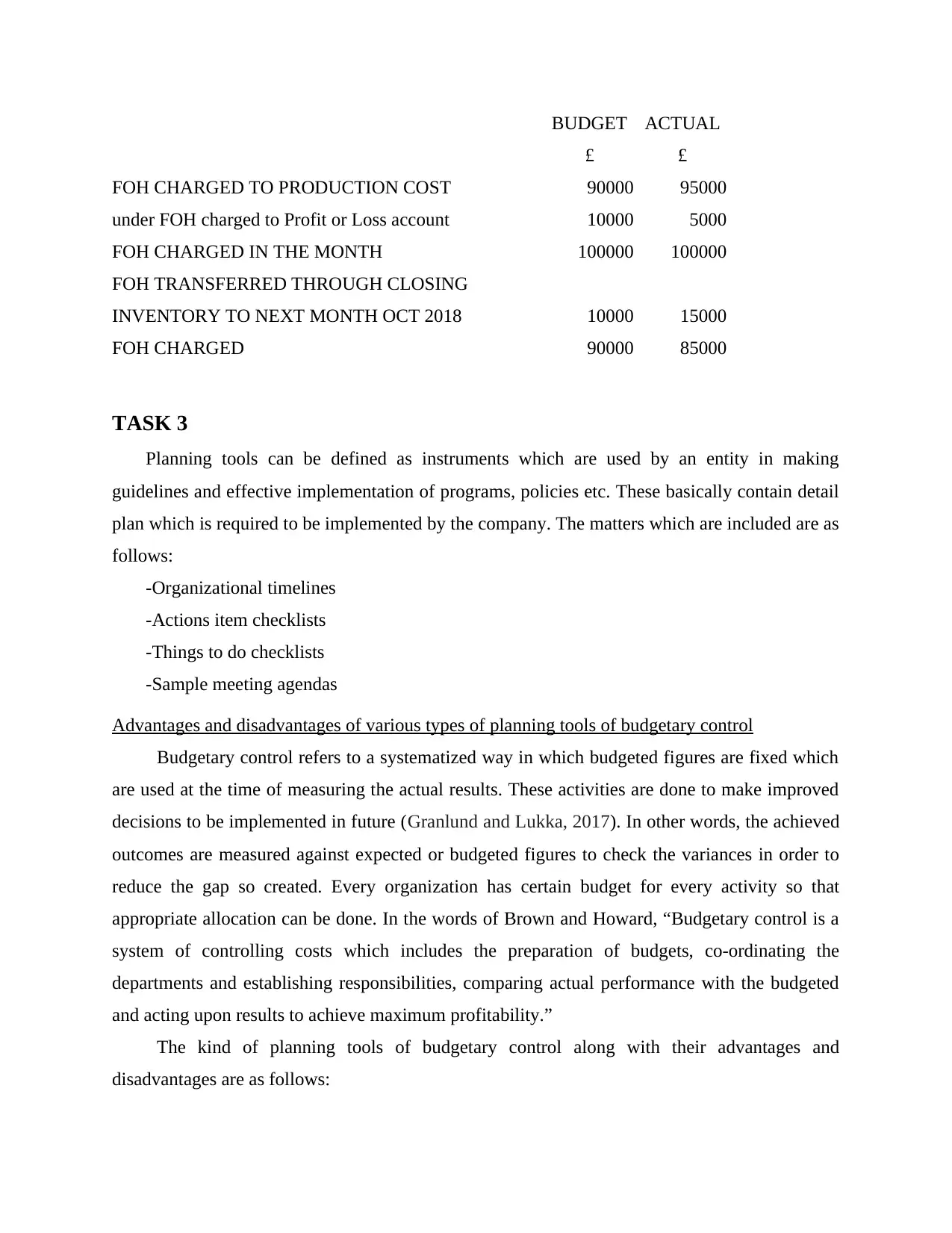

BUDGET ACTUAL

£ £

FOH CHARGED TO PRODUCTION COST 90000 95000

under FOH charged to Profit or Loss account 10000 5000

FOH CHARGED IN THE MONTH 100000 100000

FOH TRANSFERRED THROUGH CLOSING

INVENTORY TO NEXT MONTH OCT 2018 10000 15000

FOH CHARGED 90000 85000

TASK 3

Planning tools can be defined as instruments which are used by an entity in making

guidelines and effective implementation of programs, policies etc. These basically contain detail

plan which is required to be implemented by the company. The matters which are included are as

follows:

-Organizational timelines

-Actions item checklists

-Things to do checklists

-Sample meeting agendas

Advantages and disadvantages of various types of planning tools of budgetary control

Budgetary control refers to a systematized way in which budgeted figures are fixed which

are used at the time of measuring the actual results. These activities are done to make improved

decisions to be implemented in future (Granlund and Lukka, 2017). In other words, the achieved

outcomes are measured against expected or budgeted figures to check the variances in order to

reduce the gap so created. Every organization has certain budget for every activity so that

appropriate allocation can be done. In the words of Brown and Howard, “Budgetary control is a

system of controlling costs which includes the preparation of budgets, co-ordinating the

departments and establishing responsibilities, comparing actual performance with the budgeted

and acting upon results to achieve maximum profitability.”

The kind of planning tools of budgetary control along with their advantages and

disadvantages are as follows:

£ £

FOH CHARGED TO PRODUCTION COST 90000 95000

under FOH charged to Profit or Loss account 10000 5000

FOH CHARGED IN THE MONTH 100000 100000

FOH TRANSFERRED THROUGH CLOSING

INVENTORY TO NEXT MONTH OCT 2018 10000 15000

FOH CHARGED 90000 85000

TASK 3

Planning tools can be defined as instruments which are used by an entity in making

guidelines and effective implementation of programs, policies etc. These basically contain detail

plan which is required to be implemented by the company. The matters which are included are as

follows:

-Organizational timelines

-Actions item checklists

-Things to do checklists

-Sample meeting agendas

Advantages and disadvantages of various types of planning tools of budgetary control

Budgetary control refers to a systematized way in which budgeted figures are fixed which

are used at the time of measuring the actual results. These activities are done to make improved

decisions to be implemented in future (Granlund and Lukka, 2017). In other words, the achieved

outcomes are measured against expected or budgeted figures to check the variances in order to

reduce the gap so created. Every organization has certain budget for every activity so that

appropriate allocation can be done. In the words of Brown and Howard, “Budgetary control is a

system of controlling costs which includes the preparation of budgets, co-ordinating the

departments and establishing responsibilities, comparing actual performance with the budgeted

and acting upon results to achieve maximum profitability.”

The kind of planning tools of budgetary control along with their advantages and

disadvantages are as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Static Budget: This planning tool consider that budget is not increased or decreased

according to changes in the volume. This means that if the sales volumes is changed significantly

then also, the management do not expand or reduce its budget which is static in nature.

Generally, this model will give positive results if it is used in highly predictable sales and

expenses companies. Such companies assume that the targeted sales and expenditure will not

affected in the period specified by the entity. ABC Ltd. can use this method for developing

budgets for a limited time in which it can achieve its results and measure it with the budgeted

figures. This method has a limit that it cannot be used in evaluating the performance of cost

centres. However, this tool is effective in measuring sales performance during the budgeted

period. It has various advantages and disadvantages which are as follows:

Advantages:

Easy to use: This tool is easy to use as the budget is not changed in relation to changes in

volume or sales. Furthermore, it can be developed without any hurdle because there is no

requirement of making adjustments in volume or turnover (Kober, Subraamanniam and Watson,

2012). The calculation is also very simple which involves computing costs and estimate total

sales over the period of the budget. This is beneficial for small companies who do not take much

risk in increasing their budget according to sales volume. In addition to this, a person with low

expertise can also develop such budget.

Tax simplification: There no changes in the budget that has been fixed for the period

hence, this makes it easy for the company to calculate its tax obligations to be paid. This can

prove to be a great benefit for sole proprietor or small companies which find it difficult to to

compute the tax amount payable. They can easily perform the accounting functions for this

purpose. By applying this tool, entities can keep a provision or set aside the amount that it is

required to pay as tax.

Master Budget: Large organisations used static budget as a master budget. This help in

making prediction about various risks according to which the budget is prepared in a fixed form.

This form a base for preparing fixed budget for each department or unit of an organization.

Disadvantage

Lack of flexibility: The budget does not change with the changes in the volume or sales.

The factor of flexibility is low which makes it difficult for it to have advantages due to changes

in revenue or expenses in future year. The main problem that arise in this is that a company can

according to changes in the volume. This means that if the sales volumes is changed significantly

then also, the management do not expand or reduce its budget which is static in nature.

Generally, this model will give positive results if it is used in highly predictable sales and

expenses companies. Such companies assume that the targeted sales and expenditure will not

affected in the period specified by the entity. ABC Ltd. can use this method for developing

budgets for a limited time in which it can achieve its results and measure it with the budgeted

figures. This method has a limit that it cannot be used in evaluating the performance of cost

centres. However, this tool is effective in measuring sales performance during the budgeted

period. It has various advantages and disadvantages which are as follows:

Advantages:

Easy to use: This tool is easy to use as the budget is not changed in relation to changes in

volume or sales. Furthermore, it can be developed without any hurdle because there is no

requirement of making adjustments in volume or turnover (Kober, Subraamanniam and Watson,

2012). The calculation is also very simple which involves computing costs and estimate total

sales over the period of the budget. This is beneficial for small companies who do not take much

risk in increasing their budget according to sales volume. In addition to this, a person with low

expertise can also develop such budget.

Tax simplification: There no changes in the budget that has been fixed for the period

hence, this makes it easy for the company to calculate its tax obligations to be paid. This can

prove to be a great benefit for sole proprietor or small companies which find it difficult to to

compute the tax amount payable. They can easily perform the accounting functions for this

purpose. By applying this tool, entities can keep a provision or set aside the amount that it is

required to pay as tax.

Master Budget: Large organisations used static budget as a master budget. This help in

making prediction about various risks according to which the budget is prepared in a fixed form.

This form a base for preparing fixed budget for each department or unit of an organization.

Disadvantage

Lack of flexibility: The budget does not change with the changes in the volume or sales.

The factor of flexibility is low which makes it difficult for it to have advantages due to changes

in revenue or expenses in future year. The main problem that arise in this is that a company can

not adjust its budget even when the sales is declining (Lachmann, Knauer and Trapp, 2013). This

is one main disadvantage which affect the profit in a significant way. Furthermore, an

organization works in a cross charging way so the loss suffered by one unit can not be shifted to

another.

Problem for new companies: The static budgets are based on historical data which may

create a problem for newly established companies in developing and implementing these within

the entity.

Flexible budget: A flexible budget is the one which is adjusted according to change in

the volume or activity. It is completely opposite to static budget as it is not fixed and can be

altered according to requirement and situation. The budget is decrease or increase on the basis of

fluctuations in output, turnover and other variable factors which have tendency to change with

the time.

Advantages:

Seasonal expenses: There are fixed season in which a business earn huge amount of

profit due to increased sales. An organization can adjust its budget according to requirements and

demands in the market. Generally, these are done for making large profits.

Irregular earnings: A year has ups and downs in demands and trends which makes it

necessary for the company to have flexibility in the budget according to expenses that are being

incurred in making a product. This help the organization in utilising the funds on time interval

when there is increased need of funds.

Disadvantages:

Makes prediction difficult: The internal management keeps changing the budget as per

the needs thus, there exist no common figures on which prediction can be made. This is a huge

shortcoming as the management can not make correct decision. Thus, it limits the ability to plan

which often makes the company suffer losses.

No estimation taxes: Flexible budget changes every now and then which makes it

difficult for the company to calculate the exact amount of tax which is payable. For computing

tax, there should be a fixed value on which applicable rate can be applied which will give the

amount of tax. Hence, this may cause problem in managing the budget as an organization will

have no idea about the amount which is to be kept aside (Lee, 2012).

is one main disadvantage which affect the profit in a significant way. Furthermore, an

organization works in a cross charging way so the loss suffered by one unit can not be shifted to

another.

Problem for new companies: The static budgets are based on historical data which may

create a problem for newly established companies in developing and implementing these within

the entity.

Flexible budget: A flexible budget is the one which is adjusted according to change in

the volume or activity. It is completely opposite to static budget as it is not fixed and can be

altered according to requirement and situation. The budget is decrease or increase on the basis of

fluctuations in output, turnover and other variable factors which have tendency to change with

the time.

Advantages:

Seasonal expenses: There are fixed season in which a business earn huge amount of

profit due to increased sales. An organization can adjust its budget according to requirements and

demands in the market. Generally, these are done for making large profits.

Irregular earnings: A year has ups and downs in demands and trends which makes it

necessary for the company to have flexibility in the budget according to expenses that are being

incurred in making a product. This help the organization in utilising the funds on time interval

when there is increased need of funds.

Disadvantages:

Makes prediction difficult: The internal management keeps changing the budget as per

the needs thus, there exist no common figures on which prediction can be made. This is a huge

shortcoming as the management can not make correct decision. Thus, it limits the ability to plan

which often makes the company suffer losses.

No estimation taxes: Flexible budget changes every now and then which makes it

difficult for the company to calculate the exact amount of tax which is payable. For computing

tax, there should be a fixed value on which applicable rate can be applied which will give the

amount of tax. Hence, this may cause problem in managing the budget as an organization will

have no idea about the amount which is to be kept aside (Lee, 2012).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.