Financial Accounting Report: Analysis of Transactions and Statements

VerifiedAdded on 2020/07/22

|23

|5918

|49

Report

AI Summary

This report provides a comprehensive overview of financial accounting, encompassing key concepts, principles, and practical applications. It begins with an introduction to financial accounting and its significance in the business environment. The report delves into bookkeeping systems, including journal entries and the application of trial balances. It then proceeds to the preparation of final accounts, such as the profit and loss account, balance sheet, and cash flow statement, considering the specific requirements for sole traders, partnerships, and limited companies. The report further explores the bank reconciliation process, covering deposits in transit, checks, and insufficient funds, and the reconciliation of control accounts. Throughout the report, the application of accounting principles, conventions, and ethical considerations are discussed, providing a well-rounded understanding of financial accounting practices. The report also includes journal entries and their explanations and relevant accounting principles and practices, making it a valuable resource for students and professionals alike. This assignment is contributed by a student to be published on the website Desklib. Desklib is a platform which provides all the necessary AI based study tools for students.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

BUSINESS REPORT......................................................................................................................1

TASK 1............................................................................................................................................4

P1 Apply book keeping system...................................................................................................4

P2 Use of trial balance................................................................................................................7

M1 Analysation of sales and purchase transaction.....................................................................8

D1 Recording structure of transaction accurately.......................................................................8

TASK 2............................................................................................................................................8

P3 Preparation of Final accounts from trial balance...................................................................8

P4 Final accounts subject to sole traders, partnerships or limited companies............................9

M2 Analysation of profit and loss account, balance sheet and cash flow statement................11

D2 Calculation for constructing final accounts.........................................................................11

TASK 3..........................................................................................................................................11

P5 Application of bank reconciliation process..........................................................................11

M3 Reconciliation process subject to deposits in transit, cheques and insufficient funds........12

D3 Bank reconciliation statement.............................................................................................12

TASK 4..........................................................................................................................................13

P6 Process to reconcile control accounts..................................................................................13

M4 Different type of accounts and there consolidation............................................................14

D4 Application of appropriate method.....................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

BUSINESS REPORT......................................................................................................................1

TASK 1............................................................................................................................................4

P1 Apply book keeping system...................................................................................................4

P2 Use of trial balance................................................................................................................7

M1 Analysation of sales and purchase transaction.....................................................................8

D1 Recording structure of transaction accurately.......................................................................8

TASK 2............................................................................................................................................8

P3 Preparation of Final accounts from trial balance...................................................................8

P4 Final accounts subject to sole traders, partnerships or limited companies............................9

M2 Analysation of profit and loss account, balance sheet and cash flow statement................11

D2 Calculation for constructing final accounts.........................................................................11

TASK 3..........................................................................................................................................11

P5 Application of bank reconciliation process..........................................................................11

M3 Reconciliation process subject to deposits in transit, cheques and insufficient funds........12

D3 Bank reconciliation statement.............................................................................................12

TASK 4..........................................................................................................................................13

P6 Process to reconcile control accounts..................................................................................13

M4 Different type of accounts and there consolidation............................................................14

D4 Application of appropriate method.....................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Structure of business and has been altered as per the changing environment of business.

Same as per the accounting procedures and concept get moulded with the dynamic environment

of business (Francis and et. al., 2013). Multinational organisations adopt advanced tools and

method of financial to keep the financial and accounting reports in adequate manner. Financial

accounting is a branch which help to retain these accounts in designed formats and structures.

To achieve core competence and efficiency in financial management concepts and methods are

used. Financial accounting helps accountants and managers to prepare financial reports to

identify the financial strength of company. Accurate financial reports are helpful to financial

institutions, accountants, investors, shareholders and stakeholders of an organisation.

BUSINESS REPORT

Financial Accounting

Financial accounting is system used to record and present the financial position of

organisation. These system contains various rules, standards, concepts, principles. Financial

accounting helps to bifurcate the transaction as per their nature and type. Below are some basic

accounting formats are defined which are used to record the transaction and help in financial

reporting.

Cash flow statement

This statement is prepared to record cash and monetary transaction to analyse net inflow

and outflow of cash in the organisation. Three major activities are considered in this statement.

Cash inflow from operating activities, financing activities and investing activities. Daily

expenses and income which are happened on regular basis considered in operating expenses,

office expenses, payment of salaries, collections from debtors, payment to creditors are common

transactions which are happen on regular basis (Edwards and et. al., 2013). Issue of share capital,

redemption of debentures, interest on investments are the transactions considered in financing

activity and the transactions remain associated with sale of machinery, purchase of building,

installation of new plan and machinery are considered in investing activity.

Income statement

Basically two type of income and expenditure are found in normal business such as

revenue nature and capital nature. All the revenue nature income and expenditure are considered

in profit and loss accounts. Expenditures and income like operating expenses, electricity, daily

1

Structure of business and has been altered as per the changing environment of business.

Same as per the accounting procedures and concept get moulded with the dynamic environment

of business (Francis and et. al., 2013). Multinational organisations adopt advanced tools and

method of financial to keep the financial and accounting reports in adequate manner. Financial

accounting is a branch which help to retain these accounts in designed formats and structures.

To achieve core competence and efficiency in financial management concepts and methods are

used. Financial accounting helps accountants and managers to prepare financial reports to

identify the financial strength of company. Accurate financial reports are helpful to financial

institutions, accountants, investors, shareholders and stakeholders of an organisation.

BUSINESS REPORT

Financial Accounting

Financial accounting is system used to record and present the financial position of

organisation. These system contains various rules, standards, concepts, principles. Financial

accounting helps to bifurcate the transaction as per their nature and type. Below are some basic

accounting formats are defined which are used to record the transaction and help in financial

reporting.

Cash flow statement

This statement is prepared to record cash and monetary transaction to analyse net inflow

and outflow of cash in the organisation. Three major activities are considered in this statement.

Cash inflow from operating activities, financing activities and investing activities. Daily

expenses and income which are happened on regular basis considered in operating expenses,

office expenses, payment of salaries, collections from debtors, payment to creditors are common

transactions which are happen on regular basis (Edwards and et. al., 2013). Issue of share capital,

redemption of debentures, interest on investments are the transactions considered in financing

activity and the transactions remain associated with sale of machinery, purchase of building,

installation of new plan and machinery are considered in investing activity.

Income statement

Basically two type of income and expenditure are found in normal business such as

revenue nature and capital nature. All the revenue nature income and expenditure are considered

in profit and loss accounts. Expenditures and income like operating expenses, electricity, daily

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

expenses, office and administration expenses, interest on investments, discount received,

dividend received are the type of revenue nature. Capital nature of expenditures contains the

transactions and events like purchase of new plant and machinery, acquisition of new building

and land, purchase of new fixtures and furnitures. Maintenance and repair cost is considered as

revenue nature of expenditure and records in income statement.

Financial position statement

This statement remain useful to managers, auditors and accountants of company. It shows

the payment coverage and financial strength of organisation. All the assets are measures in

respect of liabilities. It provides figures related to finance requirement for upcoming years.

Majorly this statement is useful to stakeholder, brokers, bankers and financiers to analyse the

financial position of company.

Regulations related to financial accounting

Financial Reporting Council (FRC) regulatory authority in the UK which operates all the

rule and regulations subject to financial reporting and management (Horngren and et. al., 2012).

This provides a sources, methods, principles and rules subject to framing and preparing financial

statements for corporates and governance. This is one of the authority organised and managed by

chairman appointed by Bank of England.

The Accounting Standard Board (ASB) provides accounting rules to frame the accounts.

It helps to record different type of transactions in a managed structure. Rules remain focused

around treatment of deferred revenue expenditures and contingency reserves.

IASB is of the regulatory which issues guidelines, policies and standards subject to

financial accounting and accounting disclosure. IFRS which is known as International Financial

Reporting Standards are the rules issues by IASB. GAAP (Generally Accepted Accounting

Principle) are followed at international level. Global organisation which operates business

operations in various countries adopt the principles and standards of ISA and GAAP.

Accounting rules and principles

Below are some rule and principles defined subject to keep accounting records and

financial accounting

Accounting rules

Boundary rules – These rules indicates towards the existence and future stability of a

company. As per these structure of a business is bifurcated as per the vision and mission

2

dividend received are the type of revenue nature. Capital nature of expenditures contains the

transactions and events like purchase of new plant and machinery, acquisition of new building

and land, purchase of new fixtures and furnitures. Maintenance and repair cost is considered as

revenue nature of expenditure and records in income statement.

Financial position statement

This statement remain useful to managers, auditors and accountants of company. It shows

the payment coverage and financial strength of organisation. All the assets are measures in

respect of liabilities. It provides figures related to finance requirement for upcoming years.

Majorly this statement is useful to stakeholder, brokers, bankers and financiers to analyse the

financial position of company.

Regulations related to financial accounting

Financial Reporting Council (FRC) regulatory authority in the UK which operates all the

rule and regulations subject to financial reporting and management (Horngren and et. al., 2012).

This provides a sources, methods, principles and rules subject to framing and preparing financial

statements for corporates and governance. This is one of the authority organised and managed by

chairman appointed by Bank of England.

The Accounting Standard Board (ASB) provides accounting rules to frame the accounts.

It helps to record different type of transactions in a managed structure. Rules remain focused

around treatment of deferred revenue expenditures and contingency reserves.

IASB is of the regulatory which issues guidelines, policies and standards subject to

financial accounting and accounting disclosure. IFRS which is known as International Financial

Reporting Standards are the rules issues by IASB. GAAP (Generally Accepted Accounting

Principle) are followed at international level. Global organisation which operates business

operations in various countries adopt the principles and standards of ISA and GAAP.

Accounting rules and principles

Below are some rule and principles defined subject to keep accounting records and

financial accounting

Accounting rules

Boundary rules – These rules indicates towards the existence and future stability of a

company. As per these structure of a business is bifurcated as per the vision and mission

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

statement of company. Basically these rules defines the legal structure and compliance structure

of company. Guidelines are made in respect of preparing financial accounts with prudence and

materiality. Principles are made for specific pervasive boundaries in respect of behaviour.

Measurement rules- These rules are made to determine the value of assets and liabilities

of company. Value and price of assets are recognise at their historical coat rather then there

preset value. Securities, value of goods and services, insurance, valuation of land and building,

promises, patent value are the factors which are required to evaluate properly.

Ethical rules – to define the main objective and motive of an organisation these rules are

adopted by organisations. As per these rules objectives must be clearly defined in exurban and

prospectus of company. It helps investees and stakeholders to analyse the objective of

organisation. It also beneficial fro managers of organisation to understand the role and

dimensions.

Accounting Principles

Cost- Basically there are two methods used to record the value of assets in books such as

historical cost and net realisable cost. Historical cost indicates towards the cost which was

incurred in the beginning of year (Warren and et. al., 2018). Another rule which is considered in

cost principle is net realisable value. Assets are records in books after deducting depreciation and

as per net realisable value.

Full disclosure- This is one of the principle which tells about fair and clean

representation of accounting policies and financial rules using by organisation. In final reporting

it is important for a company to describe the rules and policies of company that which

accounting standards and rules are followed by company.

Going concern- This rule says that organisation is established to operate the business

operations and functions forever. These rules remain specified subject to long term objectives

and sustainability.

Matching principles- The balance of expenditures is m measured in respect of incomes

generated by an organisation. This principle also define the concept of matching the balance of

assets and liabilities in balance sheet.

Revenue recognition- this principle provides a path to accountants that how when the

income and expenditures must be considered in financial accounts and books.

Conventions and concepts relation to consistency and material disclosure

3

of company. Guidelines are made in respect of preparing financial accounts with prudence and

materiality. Principles are made for specific pervasive boundaries in respect of behaviour.

Measurement rules- These rules are made to determine the value of assets and liabilities

of company. Value and price of assets are recognise at their historical coat rather then there

preset value. Securities, value of goods and services, insurance, valuation of land and building,

promises, patent value are the factors which are required to evaluate properly.

Ethical rules – to define the main objective and motive of an organisation these rules are

adopted by organisations. As per these rules objectives must be clearly defined in exurban and

prospectus of company. It helps investees and stakeholders to analyse the objective of

organisation. It also beneficial fro managers of organisation to understand the role and

dimensions.

Accounting Principles

Cost- Basically there are two methods used to record the value of assets in books such as

historical cost and net realisable cost. Historical cost indicates towards the cost which was

incurred in the beginning of year (Warren and et. al., 2018). Another rule which is considered in

cost principle is net realisable value. Assets are records in books after deducting depreciation and

as per net realisable value.

Full disclosure- This is one of the principle which tells about fair and clean

representation of accounting policies and financial rules using by organisation. In final reporting

it is important for a company to describe the rules and policies of company that which

accounting standards and rules are followed by company.

Going concern- This rule says that organisation is established to operate the business

operations and functions forever. These rules remain specified subject to long term objectives

and sustainability.

Matching principles- The balance of expenditures is m measured in respect of incomes

generated by an organisation. This principle also define the concept of matching the balance of

assets and liabilities in balance sheet.

Revenue recognition- this principle provides a path to accountants that how when the

income and expenditures must be considered in financial accounts and books.

Conventions and concepts relation to consistency and material disclosure

3

Convention consistency

It is estimated that the policies and rules which are adopted by organisation should be

consistent for a specific duration and time. It is required to observe and analyse the consistency

of methods and principles (May, 2013.). It must be analysed whether organisation would remain

consistent with the rules and standards in future. Consistency of accounting policies and methods

helps accountants to prepare the reports in simple way. Variations in accounting and financial

procedures increase complexity and reduce the credibility of organisation in market. It not only

affect the decision making process but also affect the reliability of financial and accounting

records. This is the reason organisation should analyse the effectiveness of method before

implement in operations.

Convention of materiality

As per American Accounting Association materiality is defined as a reason behind

business activities. Objectives must be cleared in prospectus and report that helps investors and

financiers to understand the nature of business. It affect the decisions and strategies which are

made around investors. Importance of events and transactions should be described clearly in

accounts. Materiality depends on amount of risk and nature of business (Skogstad and et. al.,

2011). It implies that the economic nature of an event or item contains specific treatment.

Information should be subject to the point, no any kind of irrelevant informations should be

considered as per this convention.

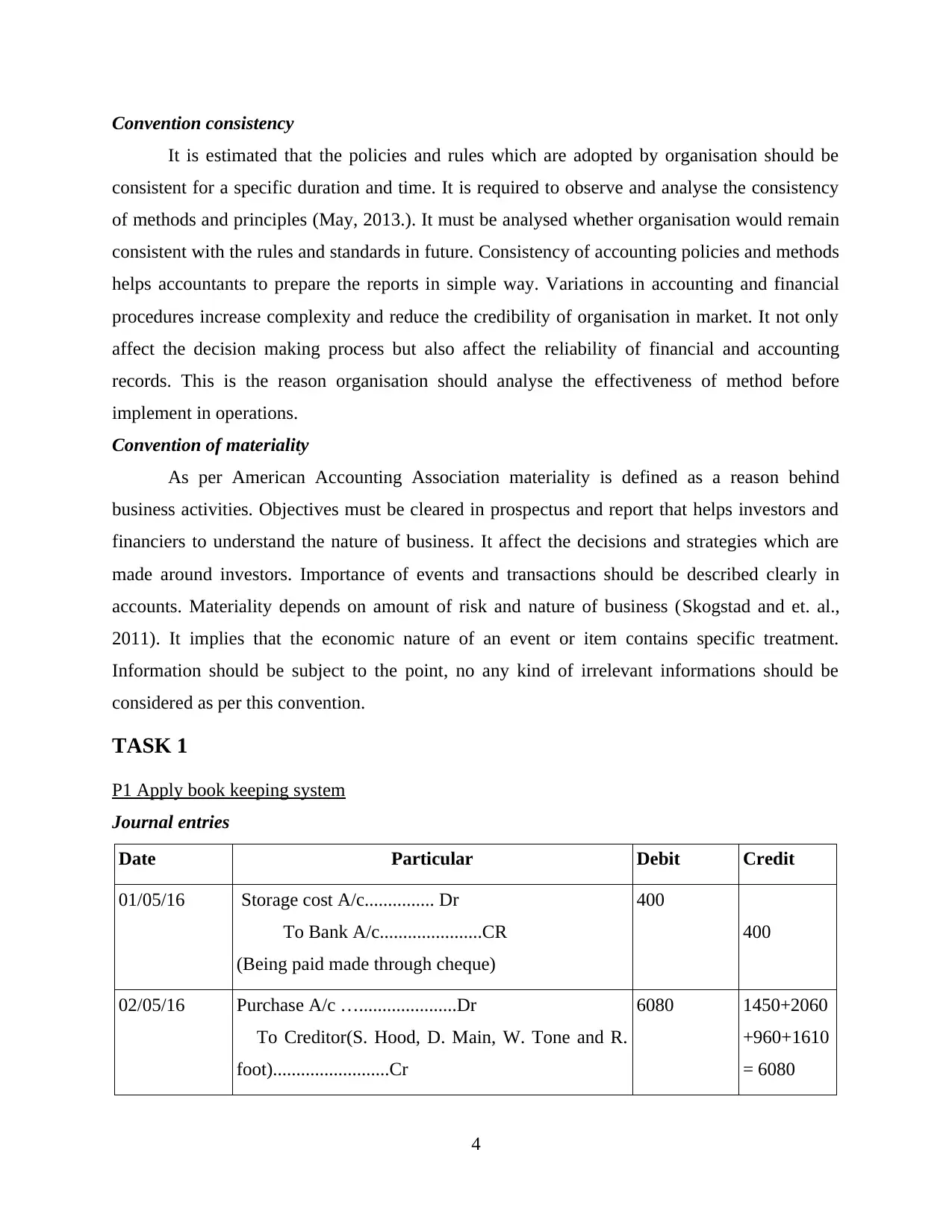

TASK 1

P1 Apply book keeping system

Journal entries

Date Particular Debit Credit

01/05/16 Storage cost A/c............... Dr

To Bank A/c......................CR

(Being paid made through cheque)

400

400

02/05/16 Purchase A/c ….....................Dr

To Creditor(S. Hood, D. Main, W. Tone and R.

foot).........................Cr

6080 1450+2060

+960+1610

= 6080

4

It is estimated that the policies and rules which are adopted by organisation should be

consistent for a specific duration and time. It is required to observe and analyse the consistency

of methods and principles (May, 2013.). It must be analysed whether organisation would remain

consistent with the rules and standards in future. Consistency of accounting policies and methods

helps accountants to prepare the reports in simple way. Variations in accounting and financial

procedures increase complexity and reduce the credibility of organisation in market. It not only

affect the decision making process but also affect the reliability of financial and accounting

records. This is the reason organisation should analyse the effectiveness of method before

implement in operations.

Convention of materiality

As per American Accounting Association materiality is defined as a reason behind

business activities. Objectives must be cleared in prospectus and report that helps investors and

financiers to understand the nature of business. It affect the decisions and strategies which are

made around investors. Importance of events and transactions should be described clearly in

accounts. Materiality depends on amount of risk and nature of business (Skogstad and et. al.,

2011). It implies that the economic nature of an event or item contains specific treatment.

Information should be subject to the point, no any kind of irrelevant informations should be

considered as per this convention.

TASK 1

P1 Apply book keeping system

Journal entries

Date Particular Debit Credit

01/05/16 Storage cost A/c............... Dr

To Bank A/c......................CR

(Being paid made through cheque)

400

400

02/05/16 Purchase A/c ….....................Dr

To Creditor(S. Hood, D. Main, W. Tone and R.

foot).........................Cr

6080 1450+2060

+960+1610

= 6080

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

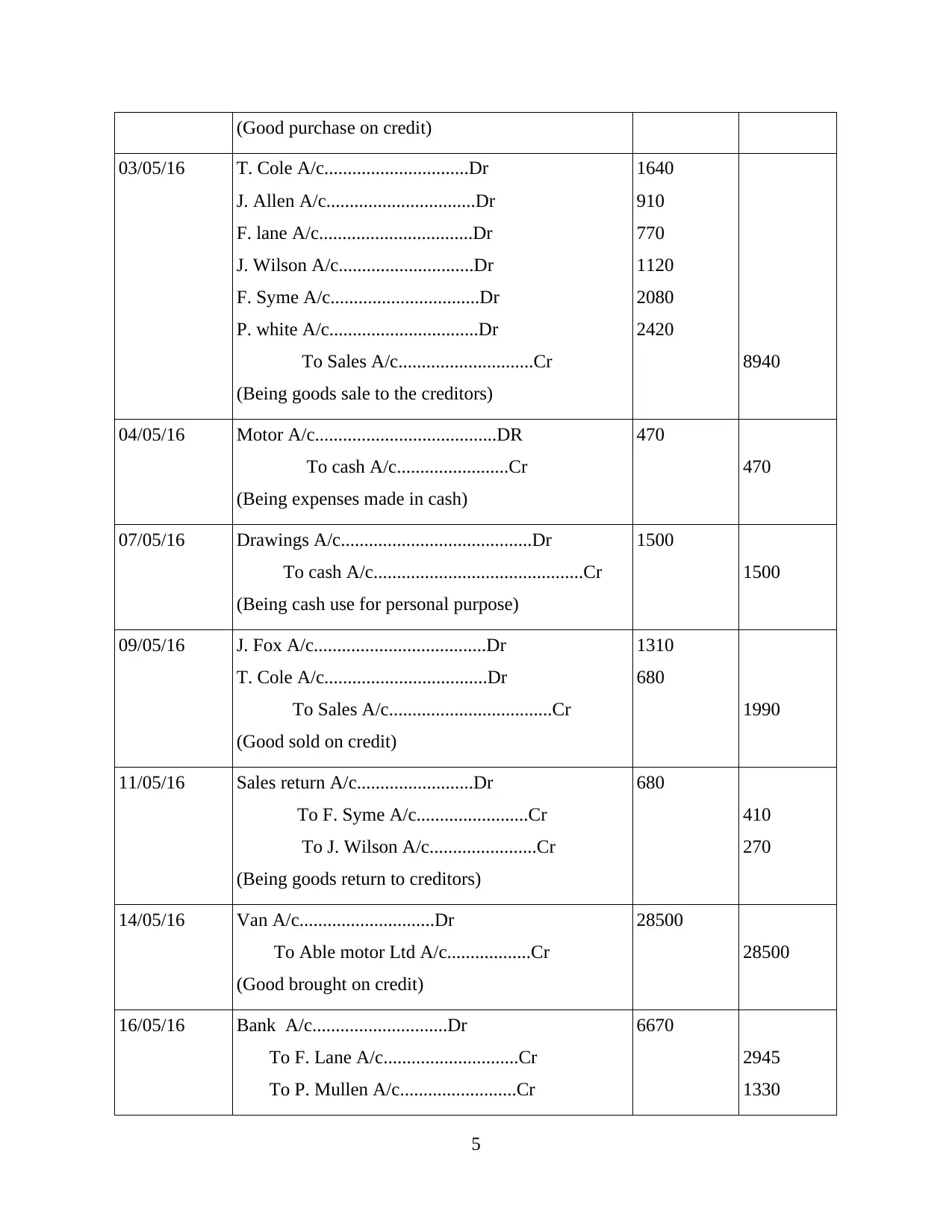

(Good purchase on credit)

03/05/16 T. Cole A/c...............................Dr

J. Allen A/c................................Dr

F. lane A/c.................................Dr

J. Wilson A/c.............................Dr

F. Syme A/c................................Dr

P. white A/c................................Dr

To Sales A/c.............................Cr

(Being goods sale to the creditors)

1640

910

770

1120

2080

2420

8940

04/05/16 Motor A/c.......................................DR

To cash A/c........................Cr

(Being expenses made in cash)

470

470

07/05/16 Drawings A/c.........................................Dr

To cash A/c.............................................Cr

(Being cash use for personal purpose)

1500

1500

09/05/16 J. Fox A/c.....................................Dr

T. Cole A/c...................................Dr

To Sales A/c...................................Cr

(Good sold on credit)

1310

680

1990

11/05/16 Sales return A/c.........................Dr

To F. Syme A/c........................Cr

To J. Wilson A/c.......................Cr

(Being goods return to creditors)

680

410

270

14/05/16 Van A/c.............................Dr

To Able motor Ltd A/c..................Cr

(Good brought on credit)

28500

28500

16/05/16 Bank A/c.............................Dr

To F. Lane A/c.............................Cr

To P. Mullen A/c.........................Cr

6670

2945

1330

5

03/05/16 T. Cole A/c...............................Dr

J. Allen A/c................................Dr

F. lane A/c.................................Dr

J. Wilson A/c.............................Dr

F. Syme A/c................................Dr

P. white A/c................................Dr

To Sales A/c.............................Cr

(Being goods sale to the creditors)

1640

910

770

1120

2080

2420

8940

04/05/16 Motor A/c.......................................DR

To cash A/c........................Cr

(Being expenses made in cash)

470

470

07/05/16 Drawings A/c.........................................Dr

To cash A/c.............................................Cr

(Being cash use for personal purpose)

1500

1500

09/05/16 J. Fox A/c.....................................Dr

T. Cole A/c...................................Dr

To Sales A/c...................................Cr

(Good sold on credit)

1310

680

1990

11/05/16 Sales return A/c.........................Dr

To F. Syme A/c........................Cr

To J. Wilson A/c.......................Cr

(Being goods return to creditors)

680

410

270

14/05/16 Van A/c.............................Dr

To Able motor Ltd A/c..................Cr

(Good brought on credit)

28500

28500

16/05/16 Bank A/c.............................Dr

To F. Lane A/c.............................Cr

To P. Mullen A/c.........................Cr

6670

2945

1330

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To J. Wilson A/c..........................Cr

To F. Syme A/c.............................Cr

(Being discount is allowed to the creditors)

Discount allowed A/c..............Dr

To J. Wilson.............................. Cr

F. Syne.,,................................Cr

F. Lane...................................Cr

P. Mullen.................................Cr

(Being discount allowed to the creditors)

352

808

1587

44

84

155

70

19/05/16 R. Foot A/c.............................Dr

To Purchase Return A/c............................Cr

(Goods return to R. foot)

50

50

22/05/16 Purchase A/c.................................Dr

To W. Wright.................................Cr

L. Mole......................................Cr

(Being good brought on credit)

3740

1910

1830

24/05/16 J. Brown A/c.....................................Dr

S. Hood A/c.......................................Dr

R. Foot A/c........................................Dr

To Bank A/c.....................................Cr

(Being Discount allowed at 10%)

R. Foot A/c...................................Dr

S. Hood A/c..................................Dr

J. Brown A/c.................................Dr

To Discount receive A/c................Cr

(Discount received and payment made)

4140

3240

1260

140

360

460

8640

960

27/05/16 Salary A/c.....................Dr

To Bank A/c..................Cr

(Being Salary made through cheque)

4800

4800

6

To F. Syme A/c.............................Cr

(Being discount is allowed to the creditors)

Discount allowed A/c..............Dr

To J. Wilson.............................. Cr

F. Syne.,,................................Cr

F. Lane...................................Cr

P. Mullen.................................Cr

(Being discount allowed to the creditors)

352

808

1587

44

84

155

70

19/05/16 R. Foot A/c.............................Dr

To Purchase Return A/c............................Cr

(Goods return to R. foot)

50

50

22/05/16 Purchase A/c.................................Dr

To W. Wright.................................Cr

L. Mole......................................Cr

(Being good brought on credit)

3740

1910

1830

24/05/16 J. Brown A/c.....................................Dr

S. Hood A/c.......................................Dr

R. Foot A/c........................................Dr

To Bank A/c.....................................Cr

(Being Discount allowed at 10%)

R. Foot A/c...................................Dr

S. Hood A/c..................................Dr

J. Brown A/c.................................Dr

To Discount receive A/c................Cr

(Discount received and payment made)

4140

3240

1260

140

360

460

8640

960

27/05/16 Salary A/c.....................Dr

To Bank A/c..................Cr

(Being Salary made through cheque)

4800

4800

6

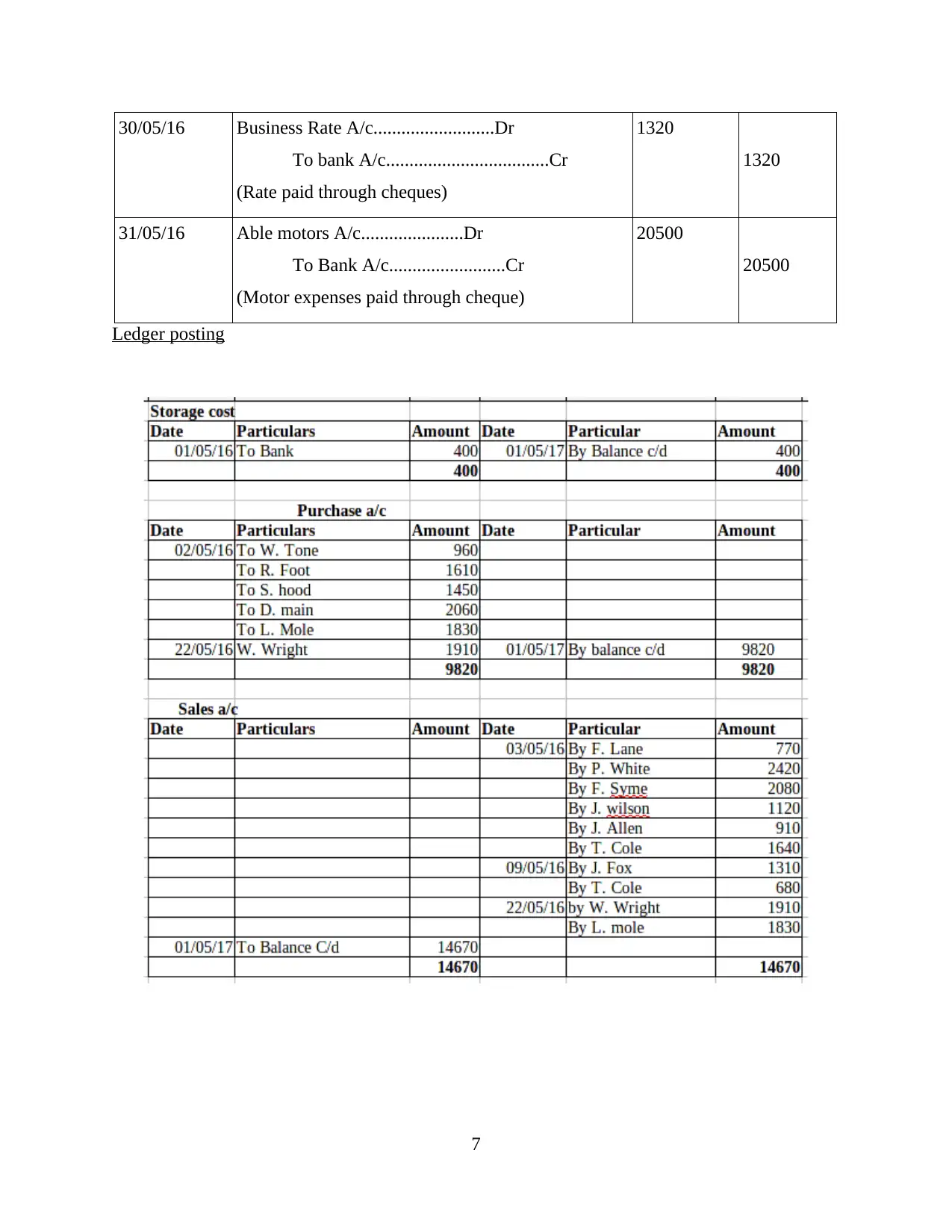

30/05/16 Business Rate A/c..........................Dr

To bank A/c...................................Cr

(Rate paid through cheques)

1320

1320

31/05/16 Able motors A/c......................Dr

To Bank A/c.........................Cr

(Motor expenses paid through cheque)

20500

20500

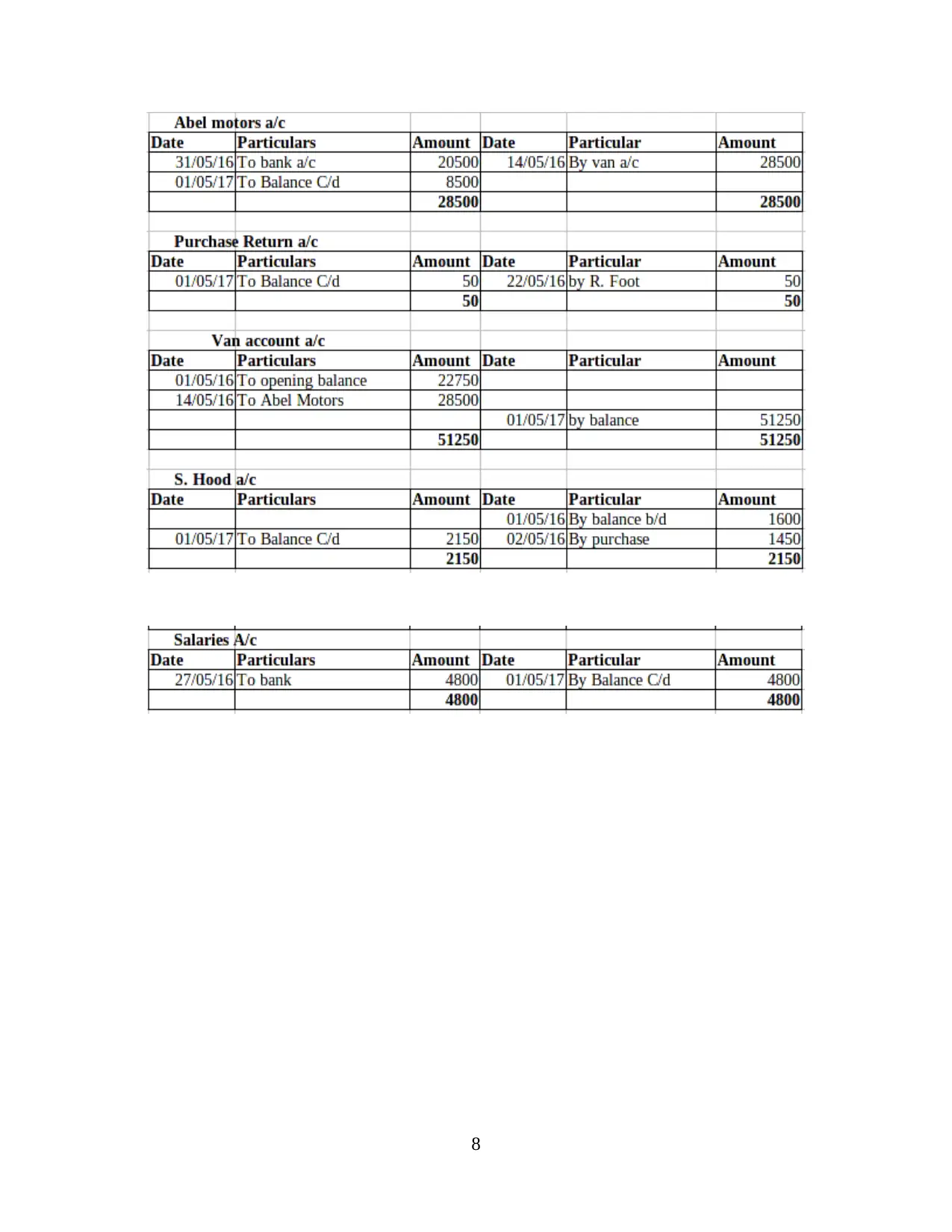

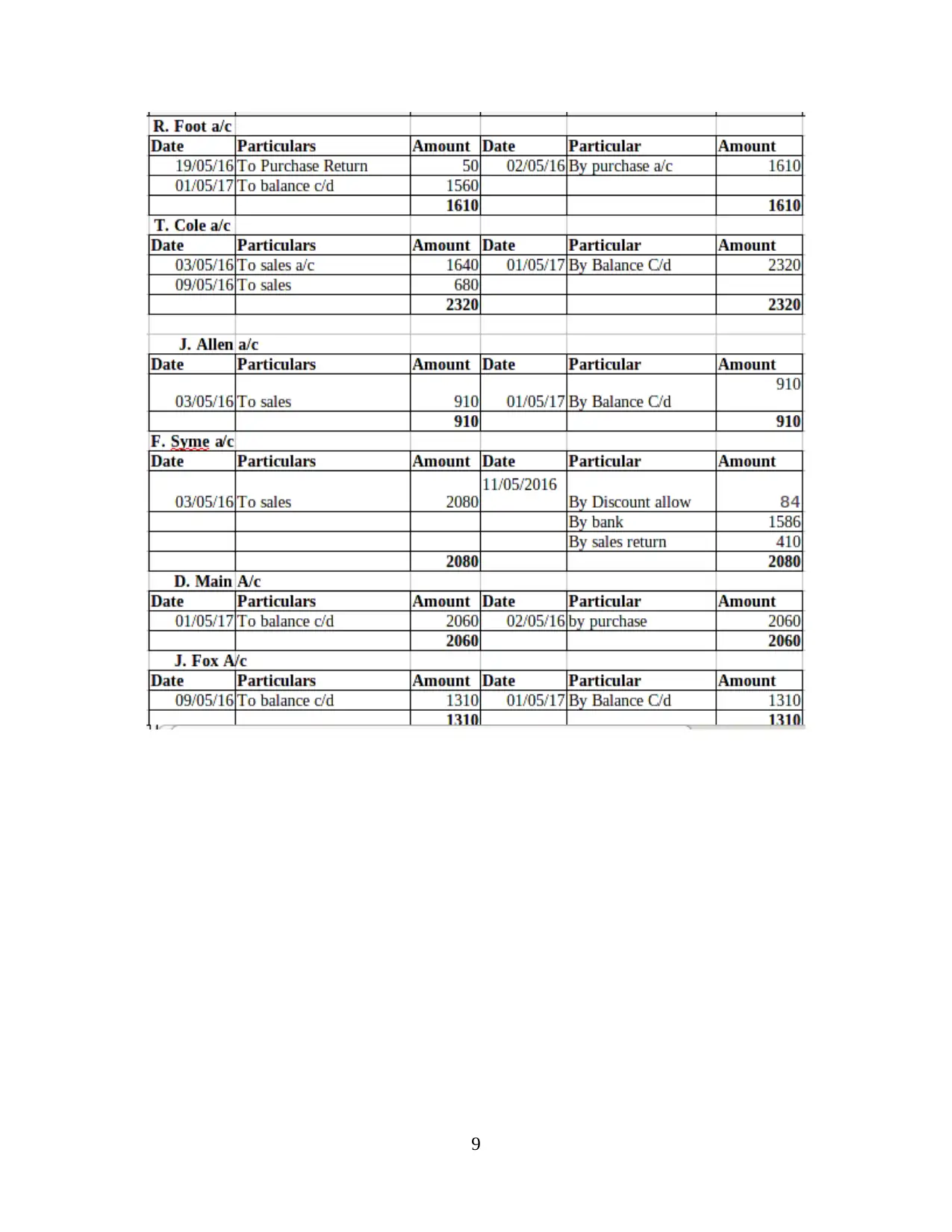

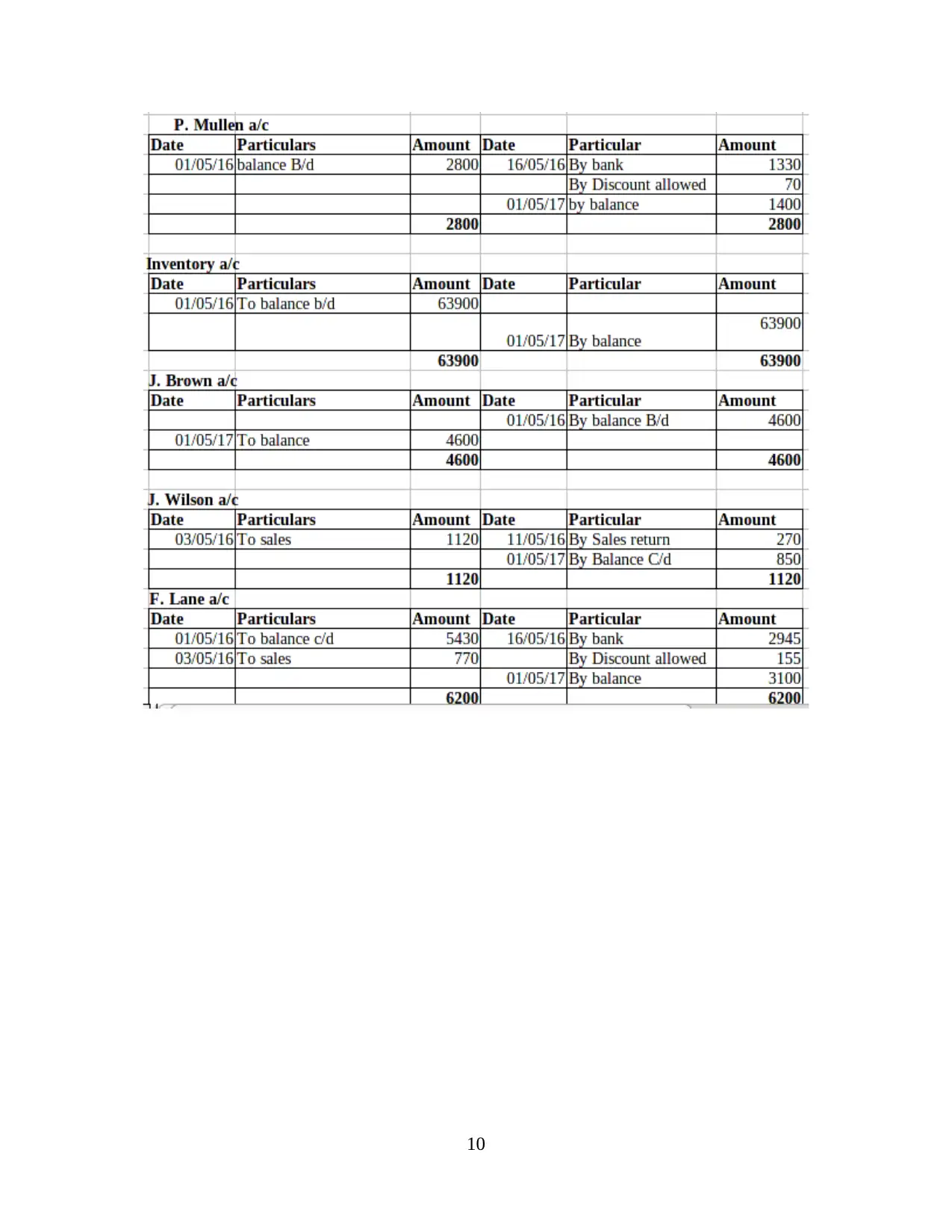

Ledger posting

7

To bank A/c...................................Cr

(Rate paid through cheques)

1320

1320

31/05/16 Able motors A/c......................Dr

To Bank A/c.........................Cr

(Motor expenses paid through cheque)

20500

20500

Ledger posting

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.