Financial Accounting Report: Double-Entry Bookkeeping and Ratios

VerifiedAdded on 2020/01/16

|10

|2138

|359

Report

AI Summary

This report provides a detailed overview of financial accounting principles and their application, focusing on the context of Mark & Spencer. It begins with an introduction to financial accounting, its importance, and the various systems used, including double-entry bookkeeping, prime entry books, and the nominal ledger. The report then explores the preparation of financial statements, including the income statement and statement of financial position, in accordance with IAS. It includes calculations of ratios such as return on capital employed, gross profit margin, and net profit margin. Further, the report discusses the Bank Reconciliation Statement (BRS), its purpose, and the process of updating the cash book. It also covers the calculation of debtors' balances, reconciliation statements, and the correction of errors in trial balances. Finally, the report concludes by summarizing the key findings and referencing relevant sources.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Various financial accounting System used by the company............................................3

1.2 Double Entry Book Keeping............................................................................................4

1.3 Trail balance with is advantages and the errors................................................................4

1.4 Benefits of the accounting standards................................................................................5

TASK 2............................................................................................................................................5

2.1 Financial accounting statements.......................................................................................5

2.2 Preparation of the statement of profit or loss in accordance with IAS.............................6

2.3 Preparation of the statement of Financial position in accordance with IAS....................6

2.4 Calculation of ratios.........................................................................................................7

TASK 3............................................................................................................................................8

3.1 Define BRS and why it is required...................................................................................8

3.2Updation of cash book.......................................................................................................8

3.3 BRS...................................................................................................................................8

TASK 4............................................................................................................................................9

4.1 Calculate the Total of the Debtors’ balances at 31 Dec 2016 as it was extracted from the

Sales Ledger...........................................................................................................................9

4.2 Prepare a Statement of Reconciliation of the Totals of the customers’ balances in the Sales

Ledger with the balances in the Debtors Control Account.....................................................9

4.3 Redrafting trial balance and suspense account.................................................................9

4.4 correcting the errors..........................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Various financial accounting System used by the company............................................3

1.2 Double Entry Book Keeping............................................................................................4

1.3 Trail balance with is advantages and the errors................................................................4

1.4 Benefits of the accounting standards................................................................................5

TASK 2............................................................................................................................................5

2.1 Financial accounting statements.......................................................................................5

2.2 Preparation of the statement of profit or loss in accordance with IAS.............................6

2.3 Preparation of the statement of Financial position in accordance with IAS....................6

2.4 Calculation of ratios.........................................................................................................7

TASK 3............................................................................................................................................8

3.1 Define BRS and why it is required...................................................................................8

3.2Updation of cash book.......................................................................................................8

3.3 BRS...................................................................................................................................8

TASK 4............................................................................................................................................9

4.1 Calculate the Total of the Debtors’ balances at 31 Dec 2016 as it was extracted from the

Sales Ledger...........................................................................................................................9

4.2 Prepare a Statement of Reconciliation of the Totals of the customers’ balances in the Sales

Ledger with the balances in the Debtors Control Account.....................................................9

4.3 Redrafting trial balance and suspense account.................................................................9

4.4 correcting the errors..........................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

This project report is all about explaining the Financial accounting and the need and

importance of the it to the Mark & Spencer. It includes various business transaction with using

double entry book keeping and the trail balance with that advantages in the preparation of the

final accounts for the company (Weil, Schipper and Francis., 2013).

TASK 1

1.1 Various financial accounting System used by the company

Financial Accounting : It refers to the tracking of the financial transaction of a

company. Under which the data are record ,summarized and analysed while preparing the final

account statement of the company Mark & Spencer.

Need of Financial accounting

To record the information and the important data of the business transaction.

Book of Prime entry : For any business the ledger is the prime source of entering the

financial transaction and help to prepare the financial statement for the Marks & Spencer.

Book of Double entry : It is based on the concept that each financial transaction are equal

and opposite reaction in two different account.

Purchase ledger : It is used to record the purchase items and the expense whether they

have buy or still owe .

Sales Ledger : It is used to record the sales made by the Marks & Spencer.

Nominal ledger contain all the record of the transaction related to the company account.

1.2 Double Entry Book Keeping

The Book keeping or the Accounting says that every business transaction contain two

effect . For Example if the company take Loan from bank it bill increase the cash account of the

company and the liability of the loan account will increased(Gassen and Schwedler., 2010.

As fro the name suggested every entry in the books requires two entry as corresponding

and opposite to the other accounts.

Under this the accounting equation is expressed as Assets = Capital + Liabilities.

Benefit of the Double accounting or book keeping:

The first benefit is to the help in preparation of the financial statement with the ability of

the double accounting it will easy to make.

This project report is all about explaining the Financial accounting and the need and

importance of the it to the Mark & Spencer. It includes various business transaction with using

double entry book keeping and the trail balance with that advantages in the preparation of the

final accounts for the company (Weil, Schipper and Francis., 2013).

TASK 1

1.1 Various financial accounting System used by the company

Financial Accounting : It refers to the tracking of the financial transaction of a

company. Under which the data are record ,summarized and analysed while preparing the final

account statement of the company Mark & Spencer.

Need of Financial accounting

To record the information and the important data of the business transaction.

Book of Prime entry : For any business the ledger is the prime source of entering the

financial transaction and help to prepare the financial statement for the Marks & Spencer.

Book of Double entry : It is based on the concept that each financial transaction are equal

and opposite reaction in two different account.

Purchase ledger : It is used to record the purchase items and the expense whether they

have buy or still owe .

Sales Ledger : It is used to record the sales made by the Marks & Spencer.

Nominal ledger contain all the record of the transaction related to the company account.

1.2 Double Entry Book Keeping

The Book keeping or the Accounting says that every business transaction contain two

effect . For Example if the company take Loan from bank it bill increase the cash account of the

company and the liability of the loan account will increased(Gassen and Schwedler., 2010.

As fro the name suggested every entry in the books requires two entry as corresponding

and opposite to the other accounts.

Under this the accounting equation is expressed as Assets = Capital + Liabilities.

Benefit of the Double accounting or book keeping:

The first benefit is to the help in preparation of the financial statement with the ability of

the double accounting it will easy to make.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It includes the Assets and the liability it take the basic advantage from the single

accounting by entering the dual aspect of the items(Introduction to Financial Accounting

2017).

It help to prevent the Fraud in the books of account because it is checked on the regular

basis. It help to easy detect he account manipulation in the journal entries as found in the

similar transaction.

1.3 Trail balance with is advantages and the errors

Trail Balance is a worksheet in which all the records of the transaction or the journal

entries are compiled into the debit and the credit columns. It is prepared at the particular period

mostly at the end of the financial year.

Advantages

It help to present the person a consolidated format of all the balances shown in the ledger

account.

It is the simplest method of identify the accuracy of the entries made in the ledger

account of the Marks & Spencer(Edwards., 2013).

Errors in the Trail balance

Error of the original entry when the both the sides are include wrong amount.

An error of omission when the transaction is completely omitted from the records of the

book keeping.

An error of reversal when the entries are written in the correct amount but debited in spite

of credit.

1.4 Benefits of the accounting standards

The Accounting Standards are mostly based on the GAAP principles of the financial

accounts. According to the need of the organisation the standards are followed.

Benefits

The Flow of the capital across the international market are the basic part of the

shareholders.

To globalized the scope of the accounting standards (Beatty and Liao., 2014).

Unexpected changes in the global businesses can help to design the minimal format of

preparing the financial statements.

accounting by entering the dual aspect of the items(Introduction to Financial Accounting

2017).

It help to prevent the Fraud in the books of account because it is checked on the regular

basis. It help to easy detect he account manipulation in the journal entries as found in the

similar transaction.

1.3 Trail balance with is advantages and the errors

Trail Balance is a worksheet in which all the records of the transaction or the journal

entries are compiled into the debit and the credit columns. It is prepared at the particular period

mostly at the end of the financial year.

Advantages

It help to present the person a consolidated format of all the balances shown in the ledger

account.

It is the simplest method of identify the accuracy of the entries made in the ledger

account of the Marks & Spencer(Edwards., 2013).

Errors in the Trail balance

Error of the original entry when the both the sides are include wrong amount.

An error of omission when the transaction is completely omitted from the records of the

book keeping.

An error of reversal when the entries are written in the correct amount but debited in spite

of credit.

1.4 Benefits of the accounting standards

The Accounting Standards are mostly based on the GAAP principles of the financial

accounts. According to the need of the organisation the standards are followed.

Benefits

The Flow of the capital across the international market are the basic part of the

shareholders.

To globalized the scope of the accounting standards (Beatty and Liao., 2014).

Unexpected changes in the global businesses can help to design the minimal format of

preparing the financial statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

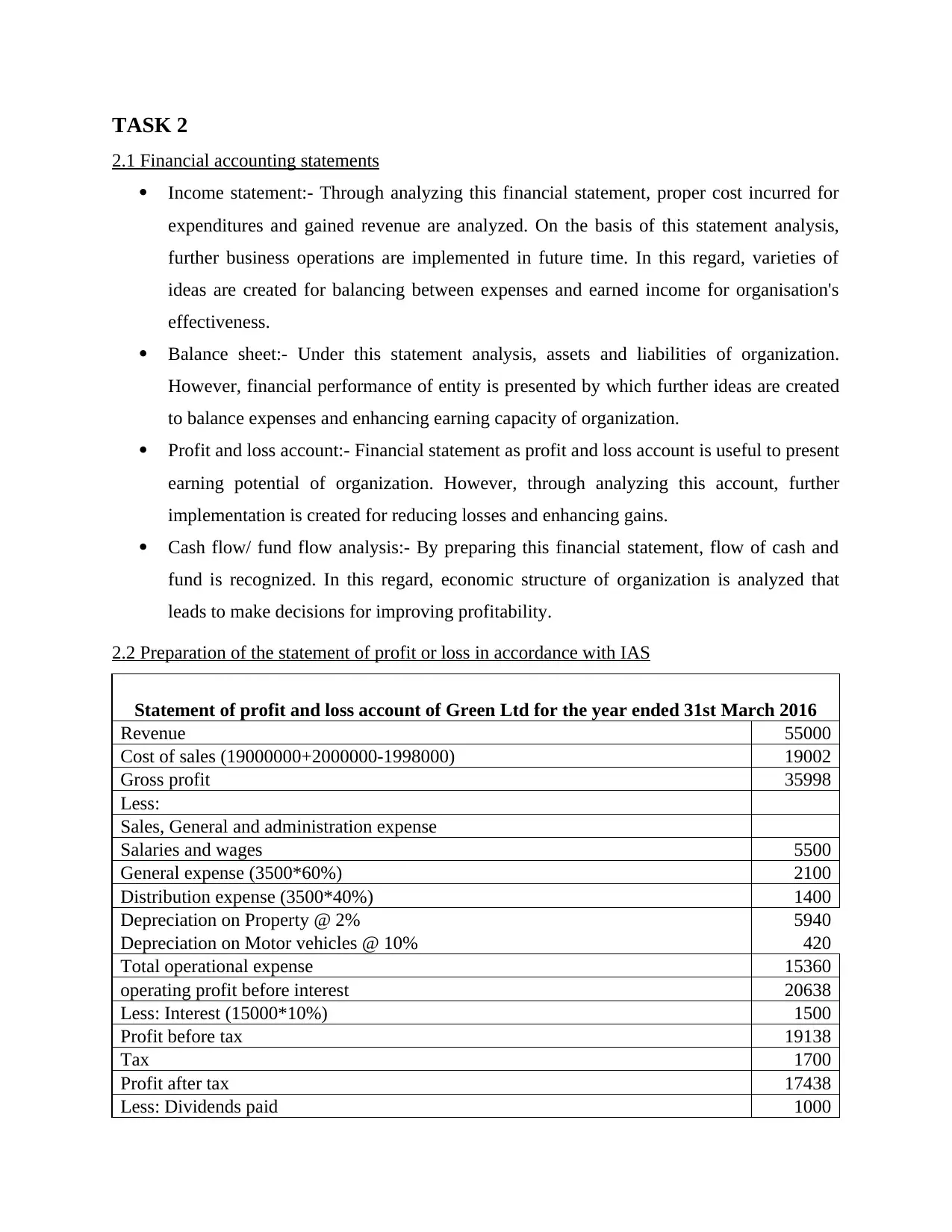

2.1 Financial accounting statements

Income statement:- Through analyzing this financial statement, proper cost incurred for

expenditures and gained revenue are analyzed. On the basis of this statement analysis,

further business operations are implemented in future time. In this regard, varieties of

ideas are created for balancing between expenses and earned income for organisation's

effectiveness.

Balance sheet:- Under this statement analysis, assets and liabilities of organization.

However, financial performance of entity is presented by which further ideas are created

to balance expenses and enhancing earning capacity of organization.

Profit and loss account:- Financial statement as profit and loss account is useful to present

earning potential of organization. However, through analyzing this account, further

implementation is created for reducing losses and enhancing gains.

Cash flow/ fund flow analysis:- By preparing this financial statement, flow of cash and

fund is recognized. In this regard, economic structure of organization is analyzed that

leads to make decisions for improving profitability.

2.2 Preparation of the statement of profit or loss in accordance with IAS

Statement of profit and loss account of Green Ltd for the year ended 31st March 2016

Revenue 55000

Cost of sales (19000000+2000000-1998000) 19002

Gross profit 35998

Less:

Sales, General and administration expense

Salaries and wages 5500

General expense (3500*60%) 2100

Distribution expense (3500*40%) 1400

Depreciation on Property @ 2% 5940

Depreciation on Motor vehicles @ 10% 420

Total operational expense 15360

operating profit before interest 20638

Less: Interest (15000*10%) 1500

Profit before tax 19138

Tax 1700

Profit after tax 17438

Less: Dividends paid 1000

2.1 Financial accounting statements

Income statement:- Through analyzing this financial statement, proper cost incurred for

expenditures and gained revenue are analyzed. On the basis of this statement analysis,

further business operations are implemented in future time. In this regard, varieties of

ideas are created for balancing between expenses and earned income for organisation's

effectiveness.

Balance sheet:- Under this statement analysis, assets and liabilities of organization.

However, financial performance of entity is presented by which further ideas are created

to balance expenses and enhancing earning capacity of organization.

Profit and loss account:- Financial statement as profit and loss account is useful to present

earning potential of organization. However, through analyzing this account, further

implementation is created for reducing losses and enhancing gains.

Cash flow/ fund flow analysis:- By preparing this financial statement, flow of cash and

fund is recognized. In this regard, economic structure of organization is analyzed that

leads to make decisions for improving profitability.

2.2 Preparation of the statement of profit or loss in accordance with IAS

Statement of profit and loss account of Green Ltd for the year ended 31st March 2016

Revenue 55000

Cost of sales (19000000+2000000-1998000) 19002

Gross profit 35998

Less:

Sales, General and administration expense

Salaries and wages 5500

General expense (3500*60%) 2100

Distribution expense (3500*40%) 1400

Depreciation on Property @ 2% 5940

Depreciation on Motor vehicles @ 10% 420

Total operational expense 15360

operating profit before interest 20638

Less: Interest (15000*10%) 1500

Profit before tax 19138

Tax 1700

Profit after tax 17438

Less: Dividends paid 1000

Net profit 16438

2.3 Preparation of the statement of Financial position in accordance with IAS

Statement of financial position of Green Ltd as on 31st March 2017

Current assets

Cash and bank 17500

Trade receivables 4000

Inventory

2000000-2600+600 1998

Current assets 23498

Non-current assets

Property at valuation 300000

Motor vehicles 5000

Total non-current assets 305000

Total assets 328498

less; Liabilities

Current liabilities

Accumulated depreciation on proerty 8940

Accumulated depreciation on motor vehicles 1220

Trade payables 5200

Revaluation reserves 200000

Accrued interest 1500

Provision for taxation 1700

Total current liabilities 218560

Long-term liabilities

10% Redeemable 2025 15000

Total long-term liabilities 15000

Total liabilities 233560

Net assets (Total assets - Total liabilities) 94938

Financed by

Ordinary share capital 50000

Add; Retained earnings 39938

Share premium 5000

Total equity capital 94938

2.4 Calculation of ratios

Ratio Formula Calculation

Result

s

Return on capital employed

(%)

Operating profit/capital

employed

20638/(328498-

218560)*100

18.77

%

2.3 Preparation of the statement of Financial position in accordance with IAS

Statement of financial position of Green Ltd as on 31st March 2017

Current assets

Cash and bank 17500

Trade receivables 4000

Inventory

2000000-2600+600 1998

Current assets 23498

Non-current assets

Property at valuation 300000

Motor vehicles 5000

Total non-current assets 305000

Total assets 328498

less; Liabilities

Current liabilities

Accumulated depreciation on proerty 8940

Accumulated depreciation on motor vehicles 1220

Trade payables 5200

Revaluation reserves 200000

Accrued interest 1500

Provision for taxation 1700

Total current liabilities 218560

Long-term liabilities

10% Redeemable 2025 15000

Total long-term liabilities 15000

Total liabilities 233560

Net assets (Total assets - Total liabilities) 94938

Financed by

Ordinary share capital 50000

Add; Retained earnings 39938

Share premium 5000

Total equity capital 94938

2.4 Calculation of ratios

Ratio Formula Calculation

Result

s

Return on capital employed

(%)

Operating profit/capital

employed

20638/(328498-

218560)*100

18.77

%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

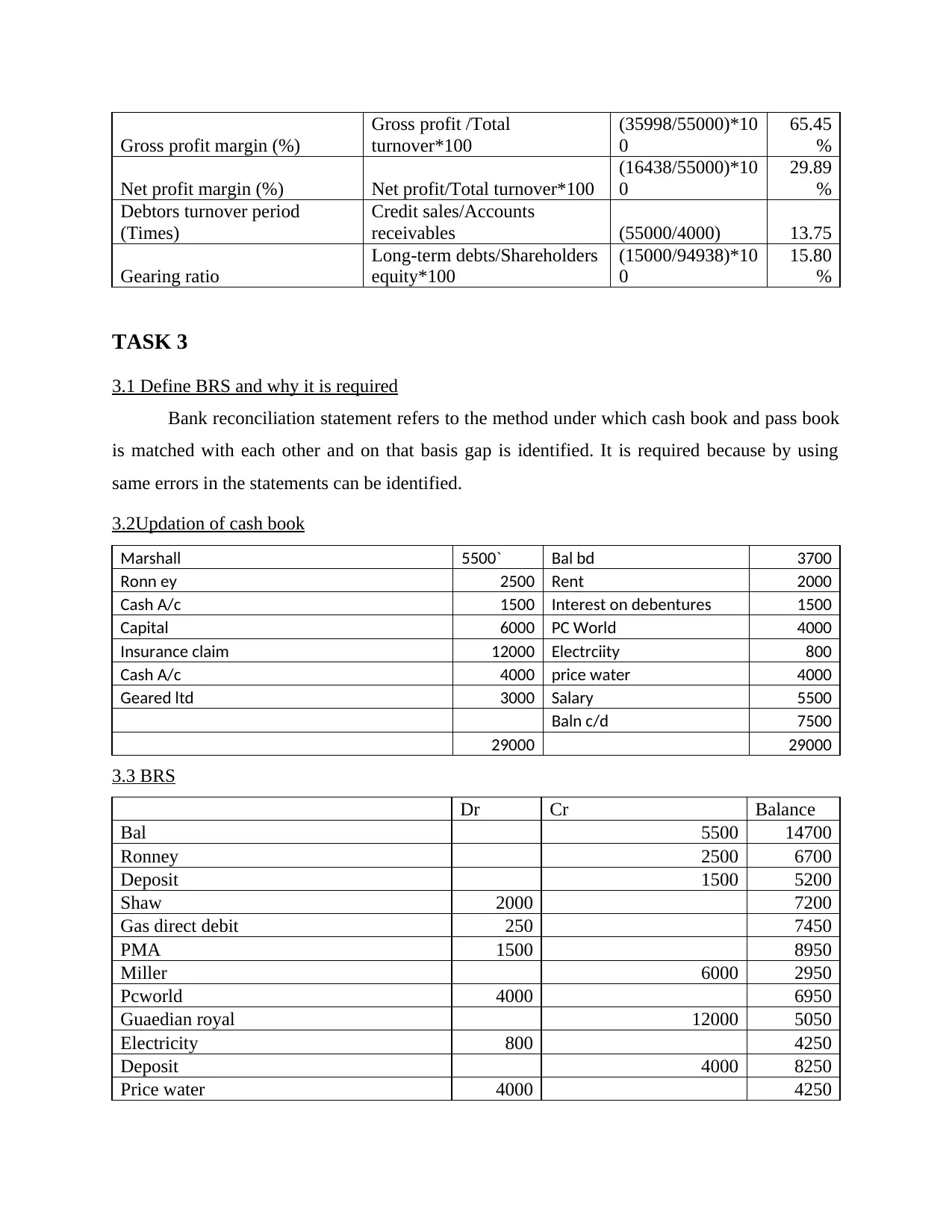

Gross profit margin (%)

Gross profit /Total

turnover*100

(35998/55000)*10

0

65.45

%

Net profit margin (%) Net profit/Total turnover*100

(16438/55000)*10

0

29.89

%

Debtors turnover period

(Times)

Credit sales/Accounts

receivables (55000/4000) 13.75

Gearing ratio

Long-term debts/Shareholders

equity*100

(15000/94938)*10

0

15.80

%

TASK 3

3.1 Define BRS and why it is required

Bank reconciliation statement refers to the method under which cash book and pass book

is matched with each other and on that basis gap is identified. It is required because by using

same errors in the statements can be identified.

3.2Updation of cash book

Marshall 5500` Bal bd 3700

Ronn ey 2500 Rent 2000

Cash A/c 1500 Interest on debentures 1500

Capital 6000 PC World 4000

Insurance claim 12000 Electrciity 800

Cash A/c 4000 price water 4000

Geared ltd 3000 Salary 5500

Baln c/d 7500

29000 29000

3.3 BRS

Dr Cr Balance

Bal 5500 14700

Ronney 2500 6700

Deposit 1500 5200

Shaw 2000 7200

Gas direct debit 250 7450

PMA 1500 8950

Miller 6000 2950

Pcworld 4000 6950

Guaedian royal 12000 5050

Electricity 800 4250

Deposit 4000 8250

Price water 4000 4250

Gross profit /Total

turnover*100

(35998/55000)*10

0

65.45

%

Net profit margin (%) Net profit/Total turnover*100

(16438/55000)*10

0

29.89

%

Debtors turnover period

(Times)

Credit sales/Accounts

receivables (55000/4000) 13.75

Gearing ratio

Long-term debts/Shareholders

equity*100

(15000/94938)*10

0

15.80

%

TASK 3

3.1 Define BRS and why it is required

Bank reconciliation statement refers to the method under which cash book and pass book

is matched with each other and on that basis gap is identified. It is required because by using

same errors in the statements can be identified.

3.2Updation of cash book

Marshall 5500` Bal bd 3700

Ronn ey 2500 Rent 2000

Cash A/c 1500 Interest on debentures 1500

Capital 6000 PC World 4000

Insurance claim 12000 Electrciity 800

Cash A/c 4000 price water 4000

Geared ltd 3000 Salary 5500

Baln c/d 7500

29000 29000

3.3 BRS

Dr Cr Balance

Bal 5500 14700

Ronney 2500 6700

Deposit 1500 5200

Shaw 2000 7200

Gas direct debit 250 7450

PMA 1500 8950

Miller 6000 2950

Pcworld 4000 6950

Guaedian royal 12000 5050

Electricity 800 4250

Deposit 4000 8250

Price water 4000 4250

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

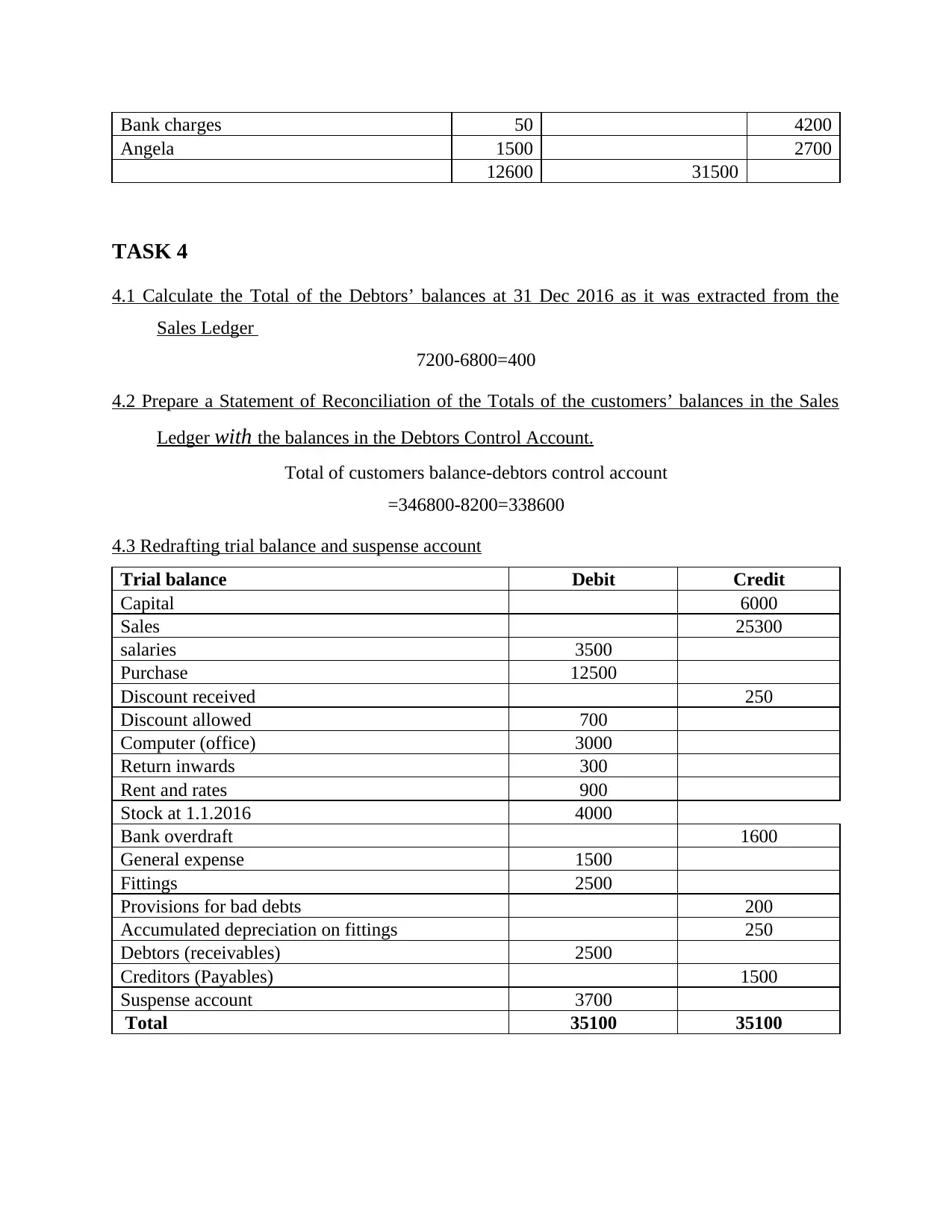

Bank charges 50 4200

Angela 1500 2700

12600 31500

TASK 4

4.1 Calculate the Total of the Debtors’ balances at 31 Dec 2016 as it was extracted from the

Sales Ledger

7200-6800=400

4.2 Prepare a Statement of Reconciliation of the Totals of the customers’ balances in the Sales

Ledger with the balances in the Debtors Control Account.

Total of customers balance-debtors control account

=346800-8200=338600

4.3 Redrafting trial balance and suspense account

Trial balance Debit Credit

Capital 6000

Sales 25300

salaries 3500

Purchase 12500

Discount received 250

Discount allowed 700

Computer (office) 3000

Return inwards 300

Rent and rates 900

Stock at 1.1.2016 4000

Bank overdraft 1600

General expense 1500

Fittings 2500

Provisions for bad debts 200

Accumulated depreciation on fittings 250

Debtors (receivables) 2500

Creditors (Payables) 1500

Suspense account 3700

Total 35100 35100

Angela 1500 2700

12600 31500

TASK 4

4.1 Calculate the Total of the Debtors’ balances at 31 Dec 2016 as it was extracted from the

Sales Ledger

7200-6800=400

4.2 Prepare a Statement of Reconciliation of the Totals of the customers’ balances in the Sales

Ledger with the balances in the Debtors Control Account.

Total of customers balance-debtors control account

=346800-8200=338600

4.3 Redrafting trial balance and suspense account

Trial balance Debit Credit

Capital 6000

Sales 25300

salaries 3500

Purchase 12500

Discount received 250

Discount allowed 700

Computer (office) 3000

Return inwards 300

Rent and rates 900

Stock at 1.1.2016 4000

Bank overdraft 1600

General expense 1500

Fittings 2500

Provisions for bad debts 200

Accumulated depreciation on fittings 250

Debtors (receivables) 2500

Creditors (Payables) 1500

Suspense account 3700

Total 35100 35100

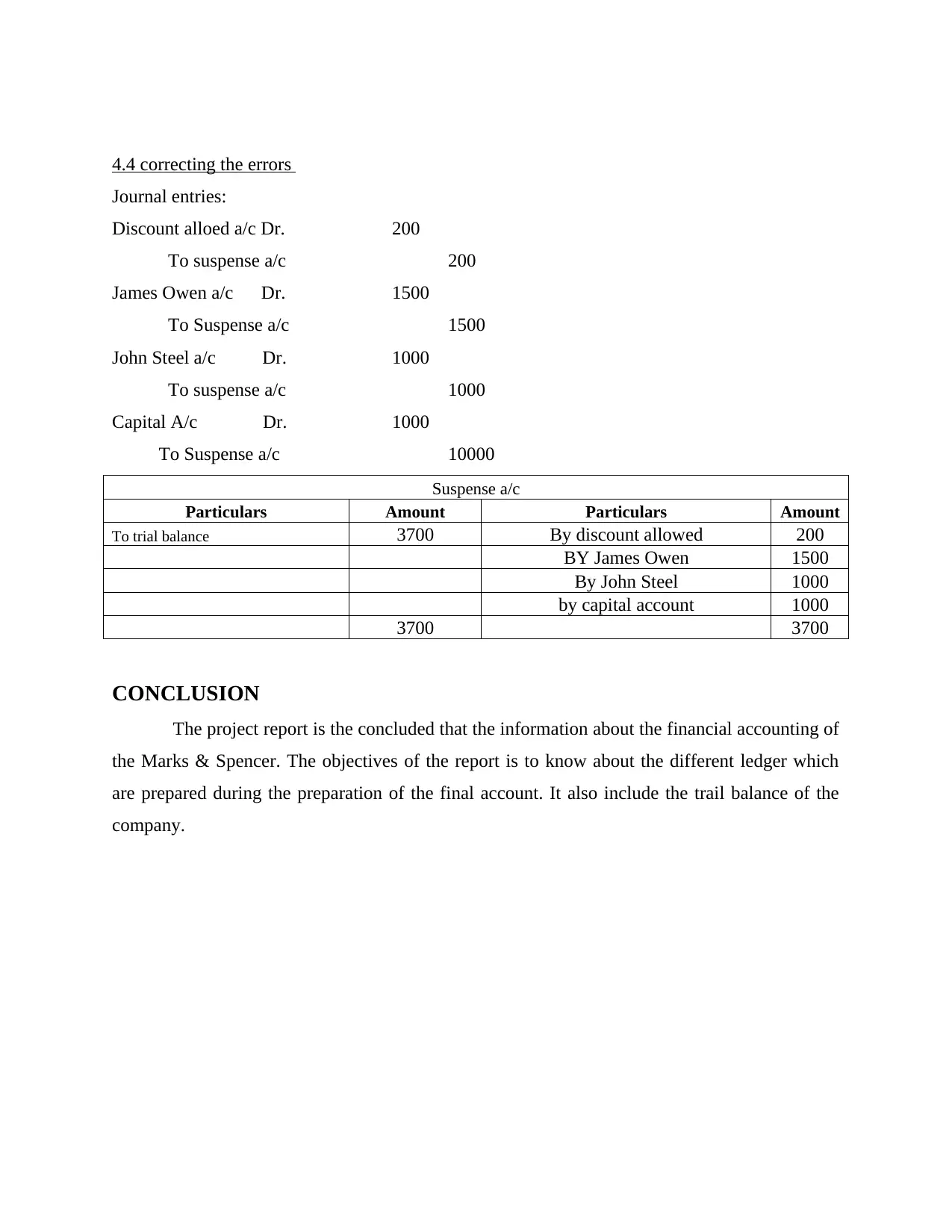

4.4 correcting the errors

Journal entries:

Discount alloed a/c Dr. 200

To suspense a/c 200

James Owen a/c Dr. 1500

To Suspense a/c 1500

John Steel a/c Dr. 1000

To suspense a/c 1000

Capital A/c Dr. 1000

To Suspense a/c 10000

Suspense a/c

Particulars Amount Particulars Amount

To trial balance 3700 By discount allowed 200

BY James Owen 1500

By John Steel 1000

by capital account 1000

3700 3700

CONCLUSION

The project report is the concluded that the information about the financial accounting of

the Marks & Spencer. The objectives of the report is to know about the different ledger which

are prepared during the preparation of the final account. It also include the trail balance of the

company.

Journal entries:

Discount alloed a/c Dr. 200

To suspense a/c 200

James Owen a/c Dr. 1500

To Suspense a/c 1500

John Steel a/c Dr. 1000

To suspense a/c 1000

Capital A/c Dr. 1000

To Suspense a/c 10000

Suspense a/c

Particulars Amount Particulars Amount

To trial balance 3700 By discount allowed 200

BY James Owen 1500

By John Steel 1000

by capital account 1000

3700 3700

CONCLUSION

The project report is the concluded that the information about the financial accounting of

the Marks & Spencer. The objectives of the report is to know about the different ledger which

are prepared during the preparation of the final account. It also include the trail balance of the

company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journal

Beatty, A and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature.Journal of Accounting and Economics.58(2). pp.339-383.

Edwards, J.R., 2013.A History of Financial Accounting (RLE Accounting)(Vol. 29). Routledge.

Gassen, J and Schwedler, K., 2010. The decision usefulness of financial accounting

measurement concepts: Evidence from an online survey of professional investors and

their advisors.European Accounting Review.19(3). pp.495-509.

Weil, R.L., Schipper, K and Francis, J., 2013.Financial accounting: an introduction to concepts,

methods and uses. Cengage Learning.

Online

Introduction to Financial Accounting 2017. [Online]. Available

through:<https://www.accountingcoach.com/financial-accounting/explanation>.

[Accessed on 13th May 2017].

Books and Journal

Beatty, A and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature.Journal of Accounting and Economics.58(2). pp.339-383.

Edwards, J.R., 2013.A History of Financial Accounting (RLE Accounting)(Vol. 29). Routledge.

Gassen, J and Schwedler, K., 2010. The decision usefulness of financial accounting

measurement concepts: Evidence from an online survey of professional investors and

their advisors.European Accounting Review.19(3). pp.495-509.

Weil, R.L., Schipper, K and Francis, J., 2013.Financial accounting: an introduction to concepts,

methods and uses. Cengage Learning.

Online

Introduction to Financial Accounting 2017. [Online]. Available

through:<https://www.accountingcoach.com/financial-accounting/explanation>.

[Accessed on 13th May 2017].

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.