Financial Accounting Report: Analysis of Financial Statements

VerifiedAdded on 2020/12/10

|31

|4394

|349

Report

AI Summary

This report delves into the core concepts of financial accounting, offering a comprehensive overview of its purpose, regulations, and fundamental principles. It explores various financial statements, including the Cash Flow Statement, Income and Expenditure Account, Balance Sheet, and Statement of Changes in Equity, highlighting their significance in assessing an organization's financial performance and position. The report emphasizes key accounting rules, such as debit and credit systems, and outlines essential principles like conservatism, cost principle, and going concern. Furthermore, it examines conventions related to consistency and material disclosure. The report includes practical examples, such as journal entries, balance sheets, and profit and loss statements, to illustrate real-world applications of accounting principles. Several client scenarios are analyzed, covering topics like bank reconciliation statements and suspense accounts. The report is designed to provide a thorough understanding of financial accounting and its practical application.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

(A) REPORT ...................................................................................................................................1

1: Financial accounting and its purpose......................................................................................1

2: The regulations relating to financial accounting.....................................................................2

3: Accounting rules and principles..............................................................................................2

4: Conventions and concepts related to consistency and materiel disclosure.............................4

CLIENT 1........................................................................................................................................5

(a) Definitions:............................................................................................................................5

(b): Double entry system.............................................................................................................5

(c): Trial Balance in the books of Amstel's D the 01 may 2017 (Figures in £)........................14

CLIENT 2......................................................................................................................................16

(a) The Statement of profit or loss for Sierra Laurent for the year ended 31st July 2018........16

Working notes:..........................................................................................................................16

(b) The Statement of Financial Position for Sierra Laurent as at 31st July 2018.....................17

Working note:............................................................................................................................18

CLIENT 3......................................................................................................................................19

(a): Profit and loss statement.....................................................................................................19

(d): Purpose of Depreciation.....................................................................................................21

CLIENT 4......................................................................................................................................21

(a): BRS (Bank Reconciliation statement)................................................................................21

(b): Areas which may cause the record to vary from the bank pass book................................22

(c): Bank reconciliation statement............................................................................................22

(d): Cash Book..........................................................................................................................23

CLIENT 5......................................................................................................................................23

(a): Entries in the books of Henderson for July 2018...............................................................23

CLIENT 6......................................................................................................................................24

(a): Main features and term of suspense account......................................................................24

(b): Trial Balance (£).................................................................................................................24

(c): suspense account.................................................................................................................25

d) Difference between a Suspense Account and a Clearing Account.......................................25

CONCLUSION..............................................................................................................................25

REFERENCES..............................................................................................................................26

INTRODUCTION...........................................................................................................................1

(A) REPORT ...................................................................................................................................1

1: Financial accounting and its purpose......................................................................................1

2: The regulations relating to financial accounting.....................................................................2

3: Accounting rules and principles..............................................................................................2

4: Conventions and concepts related to consistency and materiel disclosure.............................4

CLIENT 1........................................................................................................................................5

(a) Definitions:............................................................................................................................5

(b): Double entry system.............................................................................................................5

(c): Trial Balance in the books of Amstel's D the 01 may 2017 (Figures in £)........................14

CLIENT 2......................................................................................................................................16

(a) The Statement of profit or loss for Sierra Laurent for the year ended 31st July 2018........16

Working notes:..........................................................................................................................16

(b) The Statement of Financial Position for Sierra Laurent as at 31st July 2018.....................17

Working note:............................................................................................................................18

CLIENT 3......................................................................................................................................19

(a): Profit and loss statement.....................................................................................................19

(d): Purpose of Depreciation.....................................................................................................21

CLIENT 4......................................................................................................................................21

(a): BRS (Bank Reconciliation statement)................................................................................21

(b): Areas which may cause the record to vary from the bank pass book................................22

(c): Bank reconciliation statement............................................................................................22

(d): Cash Book..........................................................................................................................23

CLIENT 5......................................................................................................................................23

(a): Entries in the books of Henderson for July 2018...............................................................23

CLIENT 6......................................................................................................................................24

(a): Main features and term of suspense account......................................................................24

(b): Trial Balance (£).................................................................................................................24

(c): suspense account.................................................................................................................25

d) Difference between a Suspense Account and a Clearing Account.......................................25

CONCLUSION..............................................................................................................................25

REFERENCES..............................................................................................................................26

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is an integral part of an organisation which assists them in

identifying their actual financial position in market through preparing different forms of financial

reports such as Profit & Loss a/c, Balance sheet, Cash Flow statement etc. It is necessarily

required to follow accounting rules and principles to prepare all such accounts which are

explained in this report.

The present assignment report covers all aspects related with financial accounting. It

consists of business reports which include business reports describing meaning, purpose and

objectives of financial accounting. In addition, with this, financial and accounting calculations

such as Book-keeping system, ledger accounting, double entry system etc. Along with this,

financial statements include income and expenditure a/c, Balance sheet are also prepared with

practical evaluation (Badolato, Donelson and Ege, 2014).

(A) REPORT

1: Financial accounting and its purpose

Financial accounting: It is an activity of preparing financial reports which assist an

organisation to identify their actual financial performance to the involved parties to an

organisation such as investors, creditors, suppliers and customers. It facilitates managers to

forecast the company's financial position through making proper analysis of such reports.

For this, various accounting rules and concepts are formulated which required to be

follow by the accountant while preparing financial statements. It can be made on quarterly or

annual basis. It is mandatory for managers to prepare financial reports so that interested parties

such as investors, creditors, shareholders etc. may provide support to them in achieving growth

and success.

There are different types of financial accounts which are briefly mentioned under the following:

Cash Flow statement: It is a statement showing the details of cash generation and spent

on particular time period such as monthly, quarterly or yearly. It includes three heading such as

cash flow operations, cash flow from investing and cash flow from financial activity. The

statement includes only those transactions which are transacted in monetary terms (Bayou,

Reinstein and Williams, 2011).

1

Financial accounting is an integral part of an organisation which assists them in

identifying their actual financial position in market through preparing different forms of financial

reports such as Profit & Loss a/c, Balance sheet, Cash Flow statement etc. It is necessarily

required to follow accounting rules and principles to prepare all such accounts which are

explained in this report.

The present assignment report covers all aspects related with financial accounting. It

consists of business reports which include business reports describing meaning, purpose and

objectives of financial accounting. In addition, with this, financial and accounting calculations

such as Book-keeping system, ledger accounting, double entry system etc. Along with this,

financial statements include income and expenditure a/c, Balance sheet are also prepared with

practical evaluation (Badolato, Donelson and Ege, 2014).

(A) REPORT

1: Financial accounting and its purpose

Financial accounting: It is an activity of preparing financial reports which assist an

organisation to identify their actual financial performance to the involved parties to an

organisation such as investors, creditors, suppliers and customers. It facilitates managers to

forecast the company's financial position through making proper analysis of such reports.

For this, various accounting rules and concepts are formulated which required to be

follow by the accountant while preparing financial statements. It can be made on quarterly or

annual basis. It is mandatory for managers to prepare financial reports so that interested parties

such as investors, creditors, shareholders etc. may provide support to them in achieving growth

and success.

There are different types of financial accounts which are briefly mentioned under the following:

Cash Flow statement: It is a statement showing the details of cash generation and spent

on particular time period such as monthly, quarterly or yearly. It includes three heading such as

cash flow operations, cash flow from investing and cash flow from financial activity. The

statement includes only those transactions which are transacted in monetary terms (Bayou,

Reinstein and Williams, 2011).

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income and expenditure account: It is a statement containing all details regarding

expenses incurred and revenue generated by company in doing business activities. It is more

helpful for company to prepare as it assists an organisation to calculate net profit/loss thus

preparing on annual basis.

Financial position statement: It is a statement presenting actual financial position of

company through considering all assets and liabilities. It is also known as Balance sheet

containing two heading i.e. assets and liabilities which should be equal. It assists parties outside

of an organisation to make decision whether it become profitable to invest capital in business.

Change in equity statement: It is a statement that assisting manager must manage

financial reports and information which are related with capital structure of an organisation. It

helps in identifying the fluctuations in equities and share capital of company (Edwards and et.

al., 2013).

2. Regulations relating to financial accounting

Accounting is mandatory for every organisation thus it is important to prepare financial

accounting reports in better way. For this, the accountant must require to follow prescribed all

accounting rules and concepts so as to eliminate any errors or deviations. Through considering

all concepts and rules in briefly manner, the manager is more capable to prepare financial

statements and assist an organisation to provide their actual financial position at current time in

market.

There are mainly two international bodies such as IASB and IFRS which were formed to

develop specific formats and structures for financial statements. Developing frameworks help in

ensuring whether an organisation can get useful information from such financial reports. Here

are the same rules and regulations which are introduced by such authorities:

AS 1: As per this standard, all policies are required to disclosed to parties outside of an

organisation. Such policies are related with pricing policies, target audience, marketing policies

etc. which should be disclosed towards related parties such as investors, creditors and many more

which further help in making an effective decision.

AS 2: According to such standards, the inventory available in an organisation should

require to be recognised and recorded so as to determine its actual value. Its main motive is to

ascertain cost of stock, their written don cost and their net reliable value.

2

expenses incurred and revenue generated by company in doing business activities. It is more

helpful for company to prepare as it assists an organisation to calculate net profit/loss thus

preparing on annual basis.

Financial position statement: It is a statement presenting actual financial position of

company through considering all assets and liabilities. It is also known as Balance sheet

containing two heading i.e. assets and liabilities which should be equal. It assists parties outside

of an organisation to make decision whether it become profitable to invest capital in business.

Change in equity statement: It is a statement that assisting manager must manage

financial reports and information which are related with capital structure of an organisation. It

helps in identifying the fluctuations in equities and share capital of company (Edwards and et.

al., 2013).

2. Regulations relating to financial accounting

Accounting is mandatory for every organisation thus it is important to prepare financial

accounting reports in better way. For this, the accountant must require to follow prescribed all

accounting rules and concepts so as to eliminate any errors or deviations. Through considering

all concepts and rules in briefly manner, the manager is more capable to prepare financial

statements and assist an organisation to provide their actual financial position at current time in

market.

There are mainly two international bodies such as IASB and IFRS which were formed to

develop specific formats and structures for financial statements. Developing frameworks help in

ensuring whether an organisation can get useful information from such financial reports. Here

are the same rules and regulations which are introduced by such authorities:

AS 1: As per this standard, all policies are required to disclosed to parties outside of an

organisation. Such policies are related with pricing policies, target audience, marketing policies

etc. which should be disclosed towards related parties such as investors, creditors and many more

which further help in making an effective decision.

AS 2: According to such standards, the inventory available in an organisation should

require to be recognised and recorded so as to determine its actual value. Its main motive is to

ascertain cost of stock, their written don cost and their net reliable value.

2

3: Accounting rules and principles

Accounting rules: It is a process of directing accounting manager to record all business

transactions in financial statements; after taking all rules and regulations into consideration so

that reliable and accurate information are provided which facilitate management to make an

effective decisions and plans for betterment of an organisation. Such rules are listed under the

below:

Debit the receiver, credit the giver: Such rule says that an individual who receives goods

or services i.e. debtor will be recorded as debit transaction whereas an individual transfer goods

i.e. creditor will be recorded as credit transactions. Under this rule, personal accounts shall be

considered (Francis and et. al., 2015).

Debit all expenses and losses, credit all income and gains: This rule communicate that

all expenses incurred in business operations are recorded as debit transaction whereas income

earned will be recorded as credit transaction. Under this rule, nominal account will be

considered.

Debit what comes in, credit what goes out: Such rule says that if an individual or

company acquires or purchases assets then it will be recorded as debit transaction whereas any

sale or transfer of assets will be recorded as credit transaction. Under this rule, real accounts will

be considered (Gupta, 2011).

Accounting principles

Principles of Conservatism: This is the concept which communicate to accountant that

expenses and liabilities will be recorded when they are recognised and not when the outcomes

have been received. On the other hand, assets and revenues will be recorded when it has been

actually received.

Cost Principle: In this principle, all the assets, liabilities and equity investment shall be

recorded at their acquisition or original cost and ignore market price. Thus, it is also known as

historical cost principle. For example, the cost of machinery at the time of purchasing is 200000

and after two years, the price is increased to 250000 then using this principle, the accountant

shall require to consider actual cost price i.e. 200000.

Going Concern: It is the principle based on assumption that an organisation will

successfully continuing business operation till the next accounting period. It allows company to

3

Accounting rules: It is a process of directing accounting manager to record all business

transactions in financial statements; after taking all rules and regulations into consideration so

that reliable and accurate information are provided which facilitate management to make an

effective decisions and plans for betterment of an organisation. Such rules are listed under the

below:

Debit the receiver, credit the giver: Such rule says that an individual who receives goods

or services i.e. debtor will be recorded as debit transaction whereas an individual transfer goods

i.e. creditor will be recorded as credit transactions. Under this rule, personal accounts shall be

considered (Francis and et. al., 2015).

Debit all expenses and losses, credit all income and gains: This rule communicate that

all expenses incurred in business operations are recorded as debit transaction whereas income

earned will be recorded as credit transaction. Under this rule, nominal account will be

considered.

Debit what comes in, credit what goes out: Such rule says that if an individual or

company acquires or purchases assets then it will be recorded as debit transaction whereas any

sale or transfer of assets will be recorded as credit transaction. Under this rule, real accounts will

be considered (Gupta, 2011).

Accounting principles

Principles of Conservatism: This is the concept which communicate to accountant that

expenses and liabilities will be recorded when they are recognised and not when the outcomes

have been received. On the other hand, assets and revenues will be recorded when it has been

actually received.

Cost Principle: In this principle, all the assets, liabilities and equity investment shall be

recorded at their acquisition or original cost and ignore market price. Thus, it is also known as

historical cost principle. For example, the cost of machinery at the time of purchasing is 200000

and after two years, the price is increased to 250000 then using this principle, the accountant

shall require to consider actual cost price i.e. 200000.

Going Concern: It is the principle based on assumption that an organisation will

successfully continuing business operation till the next accounting period. It allows company to

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

purchase goods on credit with an intention to make repayment in future period of time (Libby,

2017).

Monetary unit: Such principle directs the accountant to record all the transactions which

are expressed and measured in monetary terms. For an illustration, purchasing goods in cash

should be recorded whereas if transaction made in other form of payment method such as barter

system then should not be recorded.

Fill disclosure: This is the accounting principle tells that the transactions shall be

recorded with brief descriptions. If the brief description is not provided, then it should be

recorded under the head of foot note of financial statements.

Matching principle: This is the principle states that the revenues and expenses incurred

in business activities that to be recorded in financial statements must be matched or equal.

Revenue recognition principle: This is the principle which states that the revenues shall

be recorded in books of accounts when it has been identified and not when the outcome has been

received. For example, at the time of sale of goods, revenue should be recorded instead of the

fact whether payment has been received or not.

Materiality: This is the principle which states that only relevant and material information

shall be recorded in financial statement and irrelevant information which are not useful for

company shall be ignored (McEnroe and Sullivan, 2013).

Time period assumption principle: This is the principle which states that the accounts

shall require to record transactions in financial statements within given time period for particular

transactions.

Economic entity assumption: This is the principle which states that an organisation and

owners are two different identities thus not responsible to pay debts for each other. Due to

having number of owners called as shareholders such principle is more preferable by company.

4: Conventions and concepts related to consistency and materiel disclosure

Accounting is a mandatory activity required to perform by an organisation in order to

determine their actual financial position in market. It includes financial statements such as profit

& loss a/c, balance sheet, cash flow statement etc. For this, there are different concepts and

conventions which are required to be follow at the time of record of transactions. Some of are

given as under:

4

2017).

Monetary unit: Such principle directs the accountant to record all the transactions which

are expressed and measured in monetary terms. For an illustration, purchasing goods in cash

should be recorded whereas if transaction made in other form of payment method such as barter

system then should not be recorded.

Fill disclosure: This is the accounting principle tells that the transactions shall be

recorded with brief descriptions. If the brief description is not provided, then it should be

recorded under the head of foot note of financial statements.

Matching principle: This is the principle states that the revenues and expenses incurred

in business activities that to be recorded in financial statements must be matched or equal.

Revenue recognition principle: This is the principle which states that the revenues shall

be recorded in books of accounts when it has been identified and not when the outcome has been

received. For example, at the time of sale of goods, revenue should be recorded instead of the

fact whether payment has been received or not.

Materiality: This is the principle which states that only relevant and material information

shall be recorded in financial statement and irrelevant information which are not useful for

company shall be ignored (McEnroe and Sullivan, 2013).

Time period assumption principle: This is the principle which states that the accounts

shall require to record transactions in financial statements within given time period for particular

transactions.

Economic entity assumption: This is the principle which states that an organisation and

owners are two different identities thus not responsible to pay debts for each other. Due to

having number of owners called as shareholders such principle is more preferable by company.

4: Conventions and concepts related to consistency and materiel disclosure

Accounting is a mandatory activity required to perform by an organisation in order to

determine their actual financial position in market. It includes financial statements such as profit

& loss a/c, balance sheet, cash flow statement etc. For this, there are different concepts and

conventions which are required to be follow at the time of record of transactions. Some of are

given as under:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Consistency concept: This is the accounting concept which states that an organisation

will continuing its business consistently without any interruptions through following policies and

standard. This enable company and outside parties to make transaction with one another with a

hope of receiving repayment in future time period (Oulasvirta, 2014).

Material Disclosure: This is the concept which states that it is essentially required for

accountant to disclose all relevant information related with made transaction under financial

statements so that it brings true and fair information about actual financial position of company

towards interested parties such as creditors, investors etc.

Accrual concept: This is the concept which states that the revenues should be recorded

when it has been earned and not when it has been actually received. On the other hand, in case of

expenses, the record to be done when incurred and not when they are actually paid.

CLIENT 1

(a) Definitions

Sole trader: It is the simplest form of business structure in which an individual solely

decide to run and operate business operations thus legally responsible for all aspects of the

business. As ownership is attached with single individual thus personally liable for their

business's finances which means they can keep profits himself and also repays any debts out their

own pocket (Peytcheva, Wright and Majoor, 2014).

Capital: It is form of assets or money which are needed to produce the products and

services that an organisation offered to their targeted customers. Therefore, it is essential for

company to have sufficient amount of capital in acquiring assets and maintain their business

operations.

Assets = Equity + Liabilities; It is called as Balance sheet equation, which represents the

relationship between assets, liabilities and owner's equity of a business. It is considered as the

foundation for the double entry bookkeeping system.

(b) Double entry system

a) Book of prime entry

Journal entries in the books of Amstel D for July 2018

Date Particular Dr Cr

5

will continuing its business consistently without any interruptions through following policies and

standard. This enable company and outside parties to make transaction with one another with a

hope of receiving repayment in future time period (Oulasvirta, 2014).

Material Disclosure: This is the concept which states that it is essentially required for

accountant to disclose all relevant information related with made transaction under financial

statements so that it brings true and fair information about actual financial position of company

towards interested parties such as creditors, investors etc.

Accrual concept: This is the concept which states that the revenues should be recorded

when it has been earned and not when it has been actually received. On the other hand, in case of

expenses, the record to be done when incurred and not when they are actually paid.

CLIENT 1

(a) Definitions

Sole trader: It is the simplest form of business structure in which an individual solely

decide to run and operate business operations thus legally responsible for all aspects of the

business. As ownership is attached with single individual thus personally liable for their

business's finances which means they can keep profits himself and also repays any debts out their

own pocket (Peytcheva, Wright and Majoor, 2014).

Capital: It is form of assets or money which are needed to produce the products and

services that an organisation offered to their targeted customers. Therefore, it is essential for

company to have sufficient amount of capital in acquiring assets and maintain their business

operations.

Assets = Equity + Liabilities; It is called as Balance sheet equation, which represents the

relationship between assets, liabilities and owner's equity of a business. It is considered as the

foundation for the double entry bookkeeping system.

(b) Double entry system

a) Book of prime entry

Journal entries in the books of Amstel D for July 2018

Date Particular Dr Cr

5

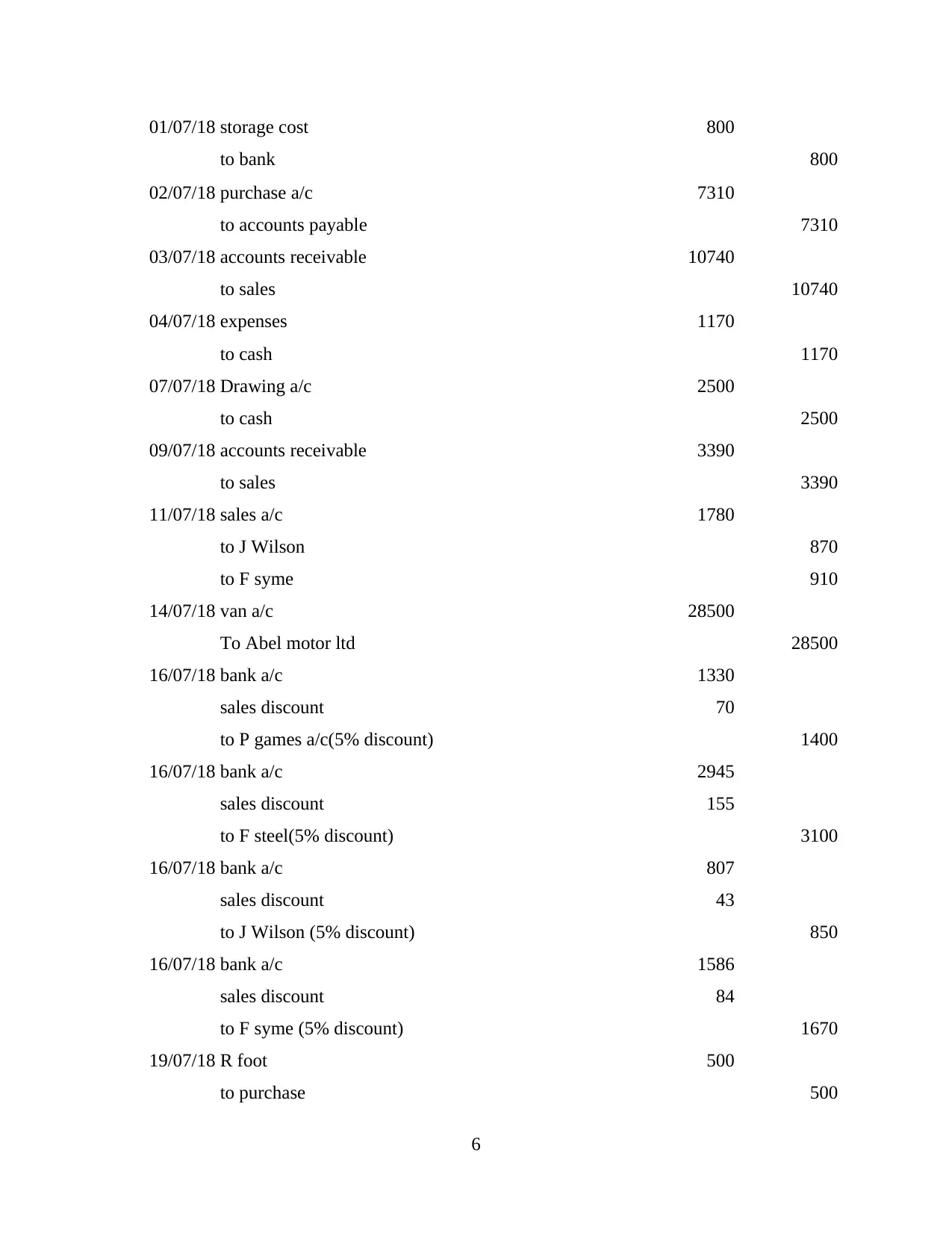

01/07/18 storage cost 800

to bank 800

02/07/18 purchase a/c 7310

to accounts payable 7310

03/07/18 accounts receivable 10740

to sales 10740

04/07/18 expenses 1170

to cash 1170

07/07/18 Drawing a/c 2500

to cash 2500

09/07/18 accounts receivable 3390

to sales 3390

11/07/18 sales a/c 1780

to J Wilson 870

to F syme 910

14/07/18 van a/c 28500

To Abel motor ltd 28500

16/07/18 bank a/c 1330

sales discount 70

to P games a/c(5% discount) 1400

16/07/18 bank a/c 2945

sales discount 155

to F steel(5% discount) 3100

16/07/18 bank a/c 807

sales discount 43

to J Wilson (5% discount) 850

16/07/18 bank a/c 1586

sales discount 84

to F syme (5% discount) 1670

19/07/18 R foot 500

to purchase 500

6

to bank 800

02/07/18 purchase a/c 7310

to accounts payable 7310

03/07/18 accounts receivable 10740

to sales 10740

04/07/18 expenses 1170

to cash 1170

07/07/18 Drawing a/c 2500

to cash 2500

09/07/18 accounts receivable 3390

to sales 3390

11/07/18 sales a/c 1780

to J Wilson 870

to F syme 910

14/07/18 van a/c 28500

To Abel motor ltd 28500

16/07/18 bank a/c 1330

sales discount 70

to P games a/c(5% discount) 1400

16/07/18 bank a/c 2945

sales discount 155

to F steel(5% discount) 3100

16/07/18 bank a/c 807

sales discount 43

to J Wilson (5% discount) 850

16/07/18 bank a/c 1586

sales discount 84

to F syme (5% discount) 1670

19/07/18 R foot 500

to purchase 500

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

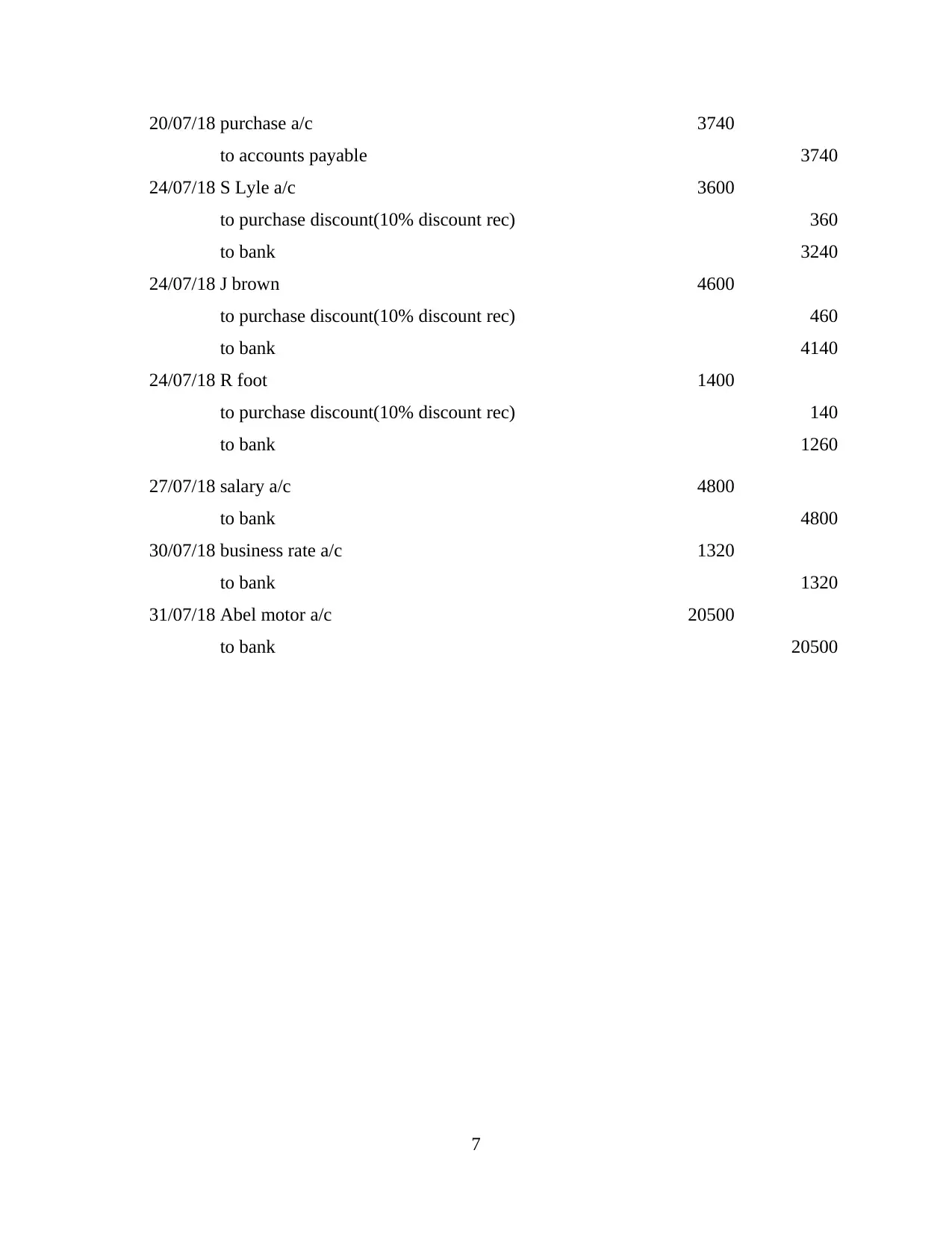

20/07/18 purchase a/c 3740

to accounts payable 3740

24/07/18 S Lyle a/c 3600

to purchase discount(10% discount rec) 360

to bank 3240

24/07/18 J brown 4600

to purchase discount(10% discount rec) 460

to bank 4140

24/07/18 R foot 1400

to purchase discount(10% discount rec) 140

to bank 1260

27/07/18 salary a/c 4800

to bank 4800

30/07/18 business rate a/c 1320

to bank 1320

31/07/18 Abel motor a/c 20500

to bank 20500

7

to accounts payable 3740

24/07/18 S Lyle a/c 3600

to purchase discount(10% discount rec) 360

to bank 3240

24/07/18 J brown 4600

to purchase discount(10% discount rec) 460

to bank 4140

24/07/18 R foot 1400

to purchase discount(10% discount rec) 140

to bank 1260

27/07/18 salary a/c 4800

to bank 4800

30/07/18 business rate a/c 1320

to bank 1320

31/07/18 Abel motor a/c 20500

to bank 20500

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

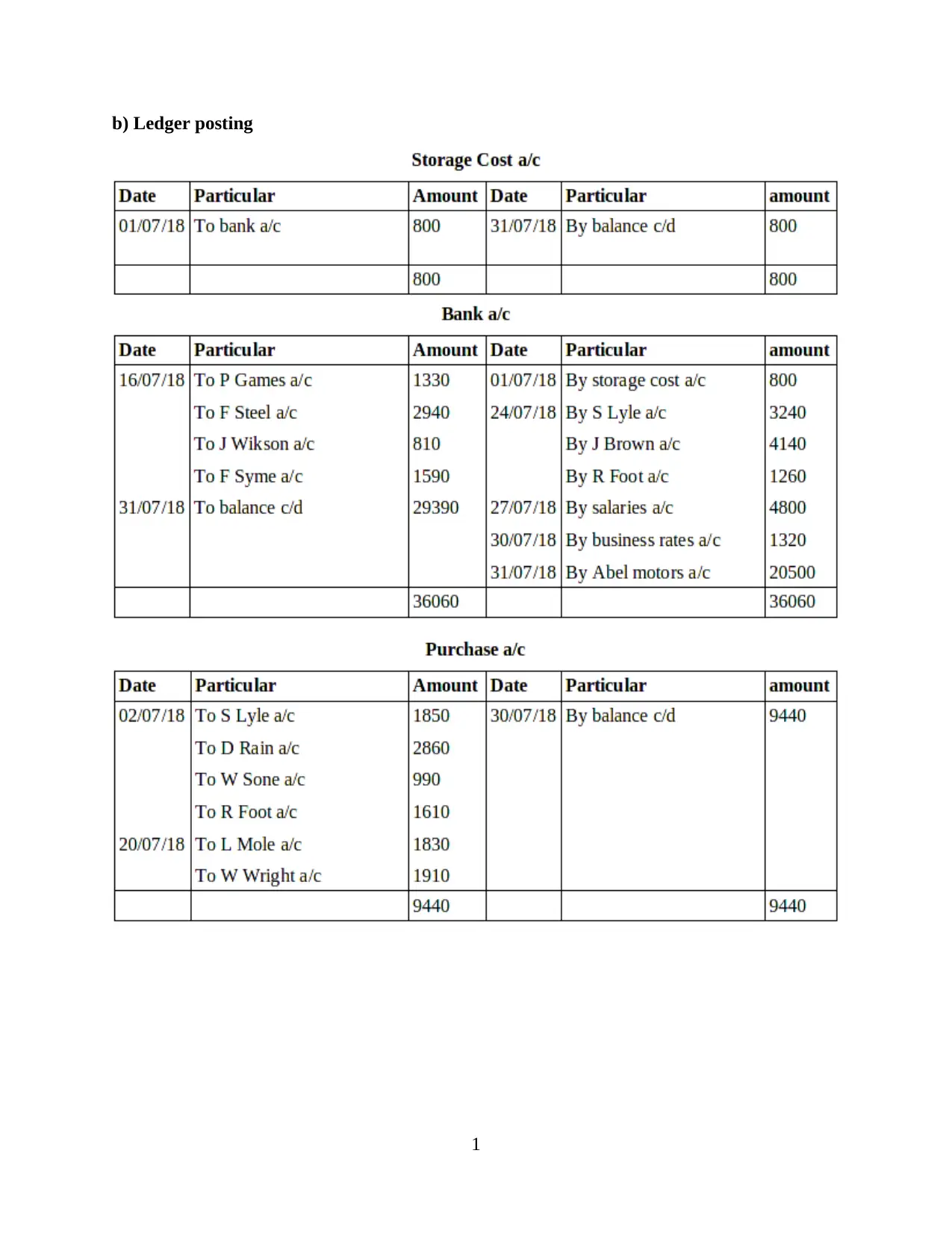

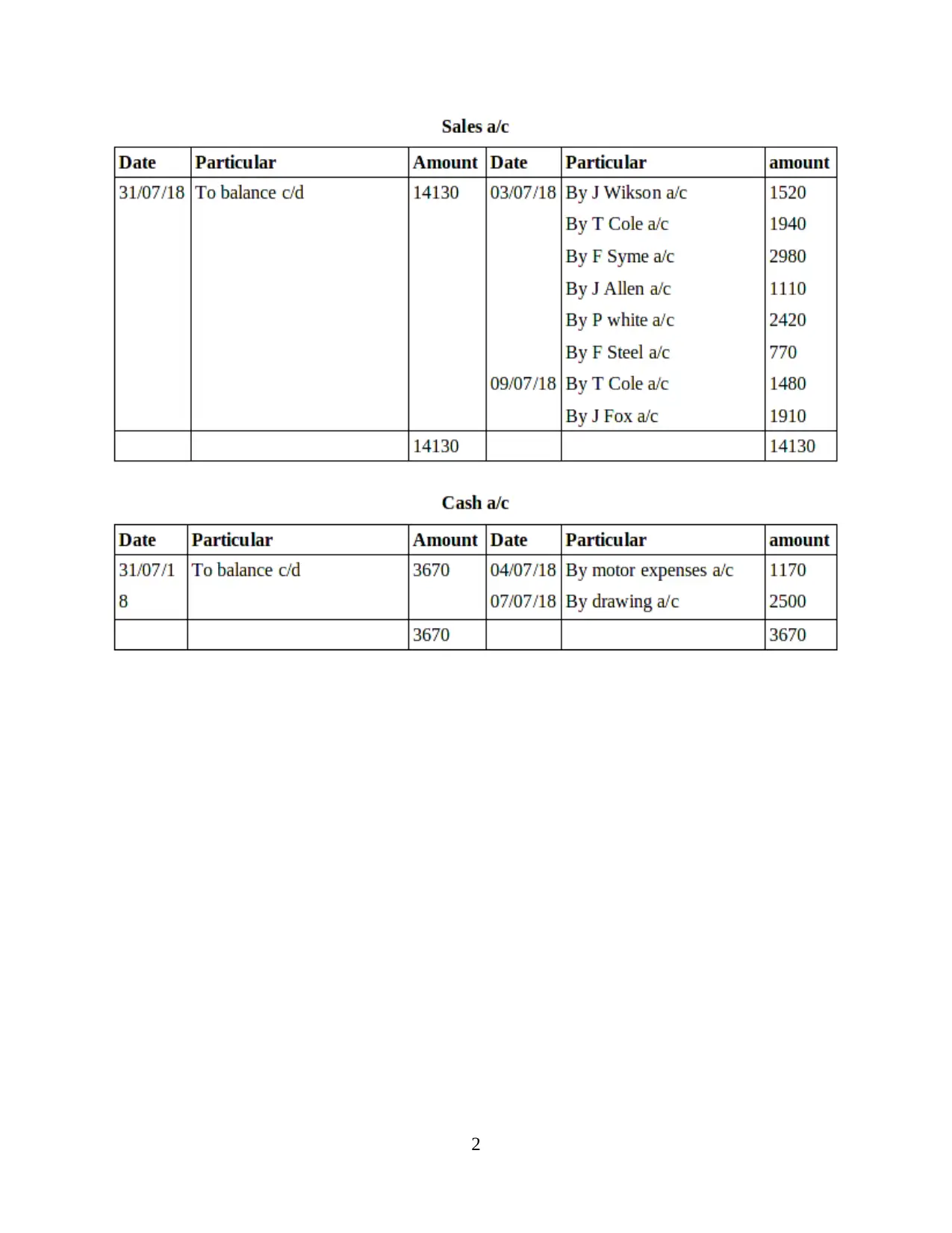

b) Ledger posting

1

1

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 31

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.