Comprehensive Report on Financial Accounting: An Overview

VerifiedAdded on 2020/02/03

|40

|6864

|47

Report

AI Summary

This report provides a comprehensive introduction to financial accounting. It begins by defining financial accounting and its importance in business for stakeholders, partners, and decision-making. The report delves into the regulations governing financial accounting, including the roles of the International Financial Reporting Council and the Accounting Standards Board, as well as specific UK regulations like IFRS. It then details key accounting rules and principles, such as the economic entity assumption, monetary unit assumption, full disclosure principle, going concern principle, and revenue recognition principle. The report explains how these principles are applied in preparing financial statements like income statements and balance sheets. It also provides an overview of journal entries, balance sheets, income transaction statements, trial balance sheets, and bank reconciliation statements, along with a discussion of accounting conventions and methods of depreciation. The report emphasizes the significance of financial accounting in evaluating business performance, making investment decisions, and strategic planning. This information is crucial for understanding financial statements and making informed decisions.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

For communicating financial information in business accounting is the basic language.

The relevant financial information of business is written and recorded in the final accounts which

are utilized by the stakeholders, business partners and parties associated with the organization for

expanding the business. The financial details are used in order to evaluate the business

performance and to take the important business decision. In order to complete this task every

organisation have accounting department where financial accounting is managed and all the sales

and expenditure are recorded in an appropriate way. Financial accounting very necessary for the

stakeholder and person associated with the organisation in order to understand the business

statement, which contain the details related to the profit and loss of the organisation (Brown,

Preiato, and Tarca, 2014.). The accountant role is to record the cash flow, performance and

financial position of the company. The collected information is then processed with decision

making by organization members and then relative measure are taken invest or lend money.

Following report concentrates on the financial accounting of business transaction momentary

which are being discussed and accessed by organization. The organisation utilizes this

information in order to make profitability and uplifting the market position. Further more, the

report contains the journal data-entries, balance sheet, income transaction statement and trial

balance sheet. The scenario also provide details about the Bank reconciliation Statement along

with other two general accounting principles such as consistency and prudence. Moreover, other

financial details which are utilized by the accounting manager such as depreciation methods;

clearing account together with suspense is being discussed in details. Mentioned report contains

data-analysis of financial account in complete description and step procedure of the accounting

so that the organization can increase profit together with revenue and minimize the losses.

A

1) Definition of financial accounting

For the evaluation purpose and expanding business, financial accounting consist of the

financial records and information. Fiscal data of every company is made, recorded and analysed

in financial accounting. The organization uses the accounting information in order to record the

business activities which is completed by ledger. The record are written in double entry method.

It is extremely important in business development. Financial accounting details are used by the

external parties and internal users of the organization. Through this business information can be

For communicating financial information in business accounting is the basic language.

The relevant financial information of business is written and recorded in the final accounts which

are utilized by the stakeholders, business partners and parties associated with the organization for

expanding the business. The financial details are used in order to evaluate the business

performance and to take the important business decision. In order to complete this task every

organisation have accounting department where financial accounting is managed and all the sales

and expenditure are recorded in an appropriate way. Financial accounting very necessary for the

stakeholder and person associated with the organisation in order to understand the business

statement, which contain the details related to the profit and loss of the organisation (Brown,

Preiato, and Tarca, 2014.). The accountant role is to record the cash flow, performance and

financial position of the company. The collected information is then processed with decision

making by organization members and then relative measure are taken invest or lend money.

Following report concentrates on the financial accounting of business transaction momentary

which are being discussed and accessed by organization. The organisation utilizes this

information in order to make profitability and uplifting the market position. Further more, the

report contains the journal data-entries, balance sheet, income transaction statement and trial

balance sheet. The scenario also provide details about the Bank reconciliation Statement along

with other two general accounting principles such as consistency and prudence. Moreover, other

financial details which are utilized by the accounting manager such as depreciation methods;

clearing account together with suspense is being discussed in details. Mentioned report contains

data-analysis of financial account in complete description and step procedure of the accounting

so that the organization can increase profit together with revenue and minimize the losses.

A

1) Definition of financial accounting

For the evaluation purpose and expanding business, financial accounting consist of the

financial records and information. Fiscal data of every company is made, recorded and analysed

in financial accounting. The organization uses the accounting information in order to record the

business activities which is completed by ledger. The record are written in double entry method.

It is extremely important in business development. Financial accounting details are used by the

external parties and internal users of the organization. Through this business information can be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

shared with the organization members which may include the strengths, weakness. Data sheet of

goods and service transaction are produced in the entity form. For completing this task, various

calculation and tools are needed in order to mention balance sheet or income statement for

revenue gained and incurred business expense. The details stored in the financial accounting are

income statement, balance sheet, gain and loss of organization. Moreover, it also contains the

details, which are given by the ledger as well as financial notes written in journal. The records

are utilized in order to expand the business and evaluate the company performance in the market.

For such things, transaction details like sales, cash flow, goods and services purchased and

capital expansion are being recorded. Mentioned above information are used by the shareholders

and other organization members in order to make decision for the investment to make further

profit. It also helps in identifying the growing market position and evaluating as well as

expanding the economic position of the company to make future strategic planning (Hitz,

Ernstberger and Stich, 2012).

Financial accounting is record and prepared to express monetary performance which are

vary important for the organisation. It also contain the details which are mentioned by the ledger

in there previous record and are evaluated with the current data which provided the data of the

companies profit making potential. Important decision like future investment, allocation of

money for several other benefit are mentioned as primary part by the organization. All the sets

and records are mentioned through the specified rules and principles which are mentioned in the

GAAP. The balance sheet prepared is updated at the regular period so that final details can be

collected at the time of fiscal year. The calculation and records are very necessary are done by

the accounting section which is separately presented in every organization.

2) Regulations regarding financial accounting

For recording the financial accounting there is need of regulation which are common for

all the organization. Following are the some of the regulation, which are related to financial

accounting such as International Financial Reporting Council and Accounting Standard Board.

The Accounting standard board is being replaced by the Accounting Council. The FRS

framework for financial reporting contains details like which standards is applicable for which

entity; when an entity can be utilized for the reduction of disclosure framework as well as which

entity must follow a SORP. The complete transaction arrangement are recorded in it. For

overseeing the corporate reporting review, conduct committee is responsible. This standards are

goods and service transaction are produced in the entity form. For completing this task, various

calculation and tools are needed in order to mention balance sheet or income statement for

revenue gained and incurred business expense. The details stored in the financial accounting are

income statement, balance sheet, gain and loss of organization. Moreover, it also contains the

details, which are given by the ledger as well as financial notes written in journal. The records

are utilized in order to expand the business and evaluate the company performance in the market.

For such things, transaction details like sales, cash flow, goods and services purchased and

capital expansion are being recorded. Mentioned above information are used by the shareholders

and other organization members in order to make decision for the investment to make further

profit. It also helps in identifying the growing market position and evaluating as well as

expanding the economic position of the company to make future strategic planning (Hitz,

Ernstberger and Stich, 2012).

Financial accounting is record and prepared to express monetary performance which are

vary important for the organisation. It also contain the details which are mentioned by the ledger

in there previous record and are evaluated with the current data which provided the data of the

companies profit making potential. Important decision like future investment, allocation of

money for several other benefit are mentioned as primary part by the organization. All the sets

and records are mentioned through the specified rules and principles which are mentioned in the

GAAP. The balance sheet prepared is updated at the regular period so that final details can be

collected at the time of fiscal year. The calculation and records are very necessary are done by

the accounting section which is separately presented in every organization.

2) Regulations regarding financial accounting

For recording the financial accounting there is need of regulation which are common for

all the organization. Following are the some of the regulation, which are related to financial

accounting such as International Financial Reporting Council and Accounting Standard Board.

The Accounting standard board is being replaced by the Accounting Council. The FRS

framework for financial reporting contains details like which standards is applicable for which

entity; when an entity can be utilized for the reduction of disclosure framework as well as which

entity must follow a SORP. The complete transaction arrangement are recorded in it. For

overseeing the corporate reporting review, conduct committee is responsible. This standards are

made in order to operated the business related activities in an effective manner. The systematic

ways of collecting the information and ethical transaction made by the organization in order to

maintain the record of goods and services. This are needed to improve the business standards and

operation of the organization to take different decision regarding profit earning. The methods is

useful in improving the financial as well as corporate standards (Adibah Wan Ismail and et.al.,

2013). Through this the actual business position and economic position of the organization is

mentioned in the market. The following are the regulation which are utilized in the UK

organization for recording the financial accountancy: IFRS:- It consist of fourteen representatives in the society. Their fundamental aim is to

approach the consensus on the accounting issues, which might have grown within the

context of the IFRSs. The organization Independent and provides the information in order

to support the structural framework of companies in preparation of the financials

accounting. The details may contain about how to record the financials transaction such

as balance-sheet, income statements, etc. Other than this the organization contains details

and guideline for cost implementation which are needed for credit rating. The

organization is effectively maintain the regulatory details of financial accounting.

Accounting Standard Board (ASB):- Following organization keeps the record about the

financial information and provision. Moreover, ASB is used to understand following:

It is helpful I formulation of Accounting standards

It also provides details about the rules, various terms and condition for presenting the

financial information.

ways of collecting the information and ethical transaction made by the organization in order to

maintain the record of goods and services. This are needed to improve the business standards and

operation of the organization to take different decision regarding profit earning. The methods is

useful in improving the financial as well as corporate standards (Adibah Wan Ismail and et.al.,

2013). Through this the actual business position and economic position of the organization is

mentioned in the market. The following are the regulation which are utilized in the UK

organization for recording the financial accountancy: IFRS:- It consist of fourteen representatives in the society. Their fundamental aim is to

approach the consensus on the accounting issues, which might have grown within the

context of the IFRSs. The organization Independent and provides the information in order

to support the structural framework of companies in preparation of the financials

accounting. The details may contain about how to record the financials transaction such

as balance-sheet, income statements, etc. Other than this the organization contains details

and guideline for cost implementation which are needed for credit rating. The

organization is effectively maintain the regulatory details of financial accounting.

Accounting Standard Board (ASB):- Following organization keeps the record about the

financial information and provision. Moreover, ASB is used to understand following:

It is helpful I formulation of Accounting standards

It also provides details about the rules, various terms and condition for presenting the

financial information.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In the current report different accounts are prepared like journal, ledger and cash budget are

prepared. Apart from this, accounting conventions are explained in detail in the report. Along

with this, in the report different principles are explained in

3 Describe accounting rules and principles

FASB is the one of the main institute that is responsible for the preparing rules and

regulations that are taken in to account to prepare the income statement and balance sheet for the

business firms. FASB time to time issue the guidelines that must be followed to for entering facts

related to the business transactions. In order to prepare the financial statements like details of

cash flows, statement of financial position varied principles are followed like GAAP general

accepted accounting principles (Agoglia, Doupnik and Tsakumis, 2011). The accounting rules

and principles are explained below. Economic entity assumption: It is usually assumed that firm and its owner are same as

name of the company is represented by the owner and both identifies are related to each

other. However, in the accounting all transactions are recorded from point of view of

firm. This means that accounts are prepared from the firm side and by considering firm

name. Whoever is the owner of the business does not matter in record of transactions in

to company books of accounts. It can be said that it is assumed that firm and its owners

are different from each other. In other words it can be said that company and its owners

are not considered same by the business firm. Due to this reason all transactions are

recorded on name of the firm not on the name of owners. This is the reason due to which

all transactions related to the firms are recorded on their name non on their owner name.

It can be said that economic entity principle clearly state all firm activities must be kept

separate from the owners activity. Monetary unit assumption: This principle of accountings that only those transactions

must be recorded in the business that can be expressed in monetary transaction. This

means that if any transaction happened but for same money is not received then in that

case that transaction cannot be recorded in the books of accounts (Hail, Leuz and

Wysocki, 2010). Main language of the finance and business is money. It is the amount on

the basis of which profitability in measured in the business. If any transaction cannot be

measured in monetary terms then it is not possible to consider as cash inflow activity in

prepared. Apart from this, accounting conventions are explained in detail in the report. Along

with this, in the report different principles are explained in

3 Describe accounting rules and principles

FASB is the one of the main institute that is responsible for the preparing rules and

regulations that are taken in to account to prepare the income statement and balance sheet for the

business firms. FASB time to time issue the guidelines that must be followed to for entering facts

related to the business transactions. In order to prepare the financial statements like details of

cash flows, statement of financial position varied principles are followed like GAAP general

accepted accounting principles (Agoglia, Doupnik and Tsakumis, 2011). The accounting rules

and principles are explained below. Economic entity assumption: It is usually assumed that firm and its owner are same as

name of the company is represented by the owner and both identifies are related to each

other. However, in the accounting all transactions are recorded from point of view of

firm. This means that accounts are prepared from the firm side and by considering firm

name. Whoever is the owner of the business does not matter in record of transactions in

to company books of accounts. It can be said that it is assumed that firm and its owners

are different from each other. In other words it can be said that company and its owners

are not considered same by the business firm. Due to this reason all transactions are

recorded on name of the firm not on the name of owners. This is the reason due to which

all transactions related to the firms are recorded on their name non on their owner name.

It can be said that economic entity principle clearly state all firm activities must be kept

separate from the owners activity. Monetary unit assumption: This principle of accountings that only those transactions

must be recorded in the business that can be expressed in monetary transaction. This

means that if any transaction happened but for same money is not received then in that

case that transaction cannot be recorded in the books of accounts (Hail, Leuz and

Wysocki, 2010). Main language of the finance and business is money. It is the amount on

the basis of which profitability in measured in the business. If any transaction cannot be

measured in monetary terms then it is not possible to consider as cash inflow activity in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the business. It can be said that it is the one of the most important principle that is used in

the accounting. Full disclosure principles: Full disclosure principle state that in the accounting reports

and the annual reports firm must give explanation of each and every thing. For example

sales is valued at 1 billion then firm must reveal its classification in terms of sales

received from different products or different geographic area. Similarly, if merger and

acquisition takes place between the business firms then in that case it is mandatory for the

firm to disclose relevant information in its annual report (Radebaugh, 2014). From these

reports stakeholders receive valuable information from the firm about its varied business

transactions. Disclosures are identified in number of places including financial statements

and sections management discussion as well as analysis section of the annual report.

Apart from this in the quarterly report also disclosures are made available about the

business transaction by the business firms. Disclosures in the reports may be related to

the foreign currencies, liabilities that are contingent in nature, leasing and other business

transactions. It can be said that through disclosures stakeholders comes to known about

various aspects of the business firm. On this basis they can make business and investment

decisions. This is because in the annual report all things are clearly explained and there is

transparency in the operations of the business firm. Going concern principles: Going concern principles is the assumption under which it is

assumed that business will remain in existence in the world consistently. This means that

it is possible that business ownership get changed but its existence will remain

continuously. It is possible that through merger fir goes in hand of outsiders but its

existence will not come to end. In case the company accountant think that it is not

possible for an organization to survive consistently then in that case may issue in front of

same is that whether asset must be impaired under which asset value is reduced to the

carrying amount to their liquidation value (Schroeder, Clark and Cathey, 2011). It can be

said that going concern concept is followed to great extent by the business firms.

Revenue recognition principles: Revenue recognition principle is one which is

considered as cornerstone of accrual accounting and matching principle. These both

principles help accountant in determining the revenue that is earned and expenses that are

made in the business. According to this principle, revenues must be recognized in the

the accounting. Full disclosure principles: Full disclosure principle state that in the accounting reports

and the annual reports firm must give explanation of each and every thing. For example

sales is valued at 1 billion then firm must reveal its classification in terms of sales

received from different products or different geographic area. Similarly, if merger and

acquisition takes place between the business firms then in that case it is mandatory for the

firm to disclose relevant information in its annual report (Radebaugh, 2014). From these

reports stakeholders receive valuable information from the firm about its varied business

transactions. Disclosures are identified in number of places including financial statements

and sections management discussion as well as analysis section of the annual report.

Apart from this in the quarterly report also disclosures are made available about the

business transaction by the business firms. Disclosures in the reports may be related to

the foreign currencies, liabilities that are contingent in nature, leasing and other business

transactions. It can be said that through disclosures stakeholders comes to known about

various aspects of the business firm. On this basis they can make business and investment

decisions. This is because in the annual report all things are clearly explained and there is

transparency in the operations of the business firm. Going concern principles: Going concern principles is the assumption under which it is

assumed that business will remain in existence in the world consistently. This means that

it is possible that business ownership get changed but its existence will remain

continuously. It is possible that through merger fir goes in hand of outsiders but its

existence will not come to end. In case the company accountant think that it is not

possible for an organization to survive consistently then in that case may issue in front of

same is that whether asset must be impaired under which asset value is reduced to the

carrying amount to their liquidation value (Schroeder, Clark and Cathey, 2011). It can be

said that going concern concept is followed to great extent by the business firms.

Revenue recognition principles: Revenue recognition principle is one which is

considered as cornerstone of accrual accounting and matching principle. These both

principles help accountant in determining the revenue that is earned and expenses that are

made in the business. According to this principle, revenues must be recognized in the

business only when same is realized or earned in the business. It does not matter that in

which time period cash is received in the business. There is cash accounting under which

revenue is recognized only when cash is received in the business. It can be said that

revenue recognition concept is widely used by the accountants in accounting of the

accounting of records. It must be noted that revenue from the sale of inventory is taken in

to consideration or recognized at date of sale (Judge, Li and Pinsker, 2010). On other

hand, revenue from services are recognized when same are fully delivered to the

customer or client completely. Apart from this, any revenue is recognized when any

income is received from the assets that are permitted to be use by the business firm.

These assets obviously are fixed assets like plant and machinery etc. Along with this any

revenue that is obtained from sale of asset is considered or recognized when its sale takes

place in the business.

which time period cash is received in the business. There is cash accounting under which

revenue is recognized only when cash is received in the business. It can be said that

revenue recognition concept is widely used by the accountants in accounting of the

accounting of records. It must be noted that revenue from the sale of inventory is taken in

to consideration or recognized at date of sale (Judge, Li and Pinsker, 2010). On other

hand, revenue from services are recognized when same are fully delivered to the

customer or client completely. Apart from this, any revenue is recognized when any

income is received from the assets that are permitted to be use by the business firm.

These assets obviously are fixed assets like plant and machinery etc. Along with this any

revenue that is obtained from sale of asset is considered or recognized when its sale takes

place in the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4 Explaining the convention and concepts in respect to consistency and material disclosure

Accounting convention are considered as a guideline that are followed by the accountant

in order to define the facts and figures related to the business firm. It can be said that accounting

convention is the term that include guidelines which originate from the accounting principles that

are applied practically by the accountant. It is not necessary to follow the accounting convention

but it is widely accepted by the accountants across the globe. It is the convention that was

designed to help accountants to help them to overcome the problems that that face while

preparing the financial statements. It can be said that accounting convention is full of

assumptions, concepts and standards. There are number of concepts that are widely supported by

accounting conventions like relevance, reliability, materiality and comparability. All these

concepts are explained below. Conventions in terms of consistency: Convention of consistency refers that same

principles must be followed in the business to record the transactions in the business. It

can be said that same principles must be followed in order to prepare details of cash

inflow and outflow, statement of financial position in the business (Richardson and

Eberlein, 2011). This is because if different principles will be followed then in that case

different values of same variable in different manner will appear in the financial

statements. Due to this reason it will not be possible to compare performance of the firm

over the past years in fair manner. Hence, it is very important for the business firms that

they follow same rules and conventions over the years regularly so that in fair manner

firm performance can be compared with each other on year on year basis in systematic

way. Business firm if prepare a rule that stock must be valued at cost or market price

whoever is low then same principle must be followed in all financial years. If in specific

year firm determine a rule that stock will be valued at market price then it will not be

possible to compare stock value for two or more financial years. This is because base for

valuation of asset in two fiscal years get change to some extent and due to this reason it is

not possible to make fair comparison of assets during relevant years.

Convention in respect to materiality: Convention of materiality refers to the accounting

of only those transactions must be recorded which have any impact on the business. This

means that any business transaction that does not have any impact on the business must

Accounting convention are considered as a guideline that are followed by the accountant

in order to define the facts and figures related to the business firm. It can be said that accounting

convention is the term that include guidelines which originate from the accounting principles that

are applied practically by the accountant. It is not necessary to follow the accounting convention

but it is widely accepted by the accountants across the globe. It is the convention that was

designed to help accountants to help them to overcome the problems that that face while

preparing the financial statements. It can be said that accounting convention is full of

assumptions, concepts and standards. There are number of concepts that are widely supported by

accounting conventions like relevance, reliability, materiality and comparability. All these

concepts are explained below. Conventions in terms of consistency: Convention of consistency refers that same

principles must be followed in the business to record the transactions in the business. It

can be said that same principles must be followed in order to prepare details of cash

inflow and outflow, statement of financial position in the business (Richardson and

Eberlein, 2011). This is because if different principles will be followed then in that case

different values of same variable in different manner will appear in the financial

statements. Due to this reason it will not be possible to compare performance of the firm

over the past years in fair manner. Hence, it is very important for the business firms that

they follow same rules and conventions over the years regularly so that in fair manner

firm performance can be compared with each other on year on year basis in systematic

way. Business firm if prepare a rule that stock must be valued at cost or market price

whoever is low then same principle must be followed in all financial years. If in specific

year firm determine a rule that stock will be valued at market price then it will not be

possible to compare stock value for two or more financial years. This is because base for

valuation of asset in two fiscal years get change to some extent and due to this reason it is

not possible to make fair comparison of assets during relevant years.

Convention in respect to materiality: Convention of materiality refers to the accounting

of only those transactions must be recorded which have any impact on the business. This

means that any business transaction that does not have any impact on the business must

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be totally ignored from the books of accounts. This convention is prepared because in the

business so many transactions are performed and some of them may have insignificant

impact on the business. Inclusion of all transactions in books of accounts may accounting

work overburden. Hence, it is very important to consider only those transactions in the

accounting that have significant impact on the business firm. However, there are some

limitations of this concept as it is totally matter of judgment (Demerjian, 2011). It is

possible that specific sort of transaction may be insignificant for the business firm but

same in the next year may prove significant. Thus, it can be said that there is chance that

one can make mistake in assuming any transaction as material or immaterial for the

specific accounting year.

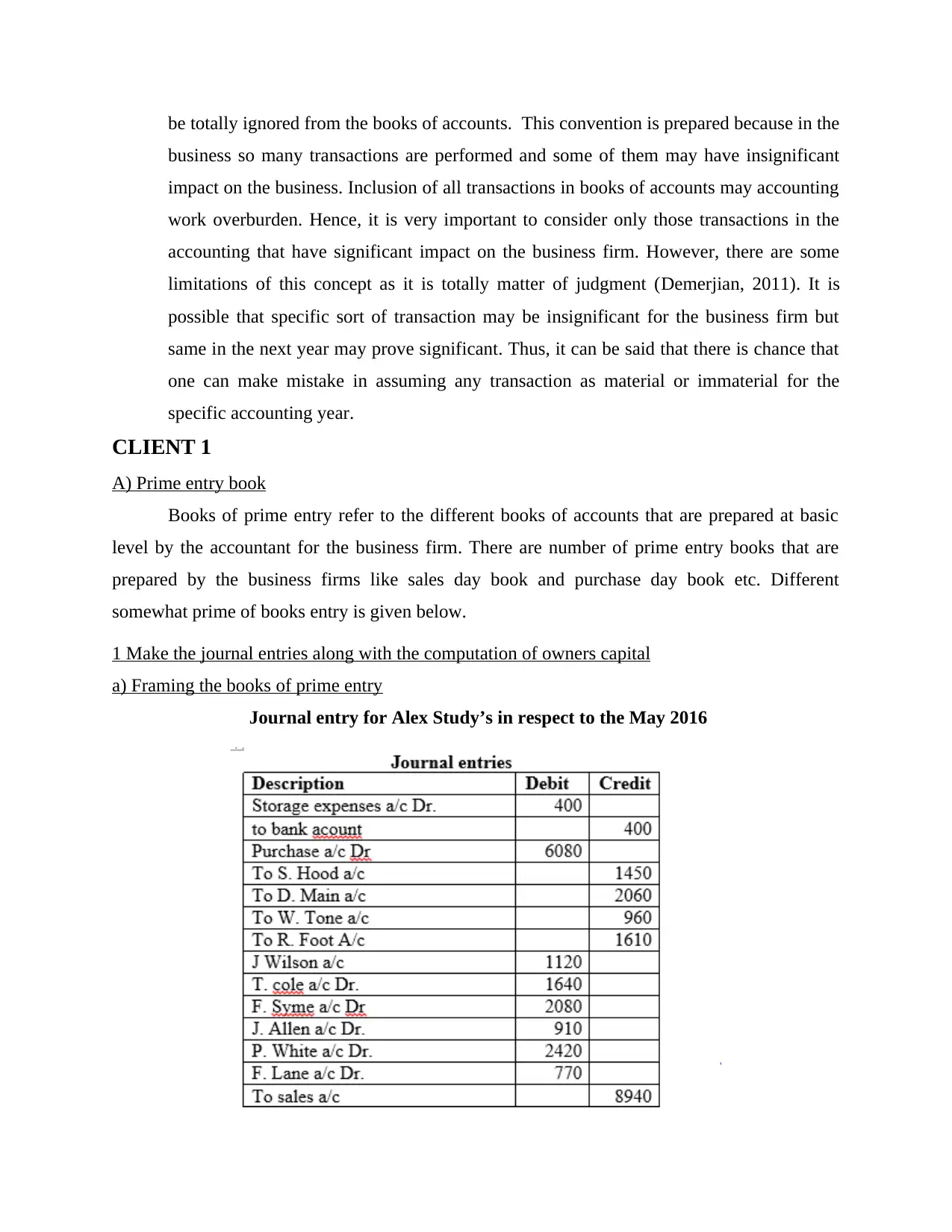

CLIENT 1

A) Prime entry book

Books of prime entry refer to the different books of accounts that are prepared at basic

level by the accountant for the business firm. There are number of prime entry books that are

prepared by the business firms like sales day book and purchase day book etc. Different

somewhat prime of books entry is given below.

1 Make the journal entries along with the computation of owners capital

a) Framing the books of prime entry

Journal entry for Alex Study’s in respect to the May 2016

business so many transactions are performed and some of them may have insignificant

impact on the business. Inclusion of all transactions in books of accounts may accounting

work overburden. Hence, it is very important to consider only those transactions in the

accounting that have significant impact on the business firm. However, there are some

limitations of this concept as it is totally matter of judgment (Demerjian, 2011). It is

possible that specific sort of transaction may be insignificant for the business firm but

same in the next year may prove significant. Thus, it can be said that there is chance that

one can make mistake in assuming any transaction as material or immaterial for the

specific accounting year.

CLIENT 1

A) Prime entry book

Books of prime entry refer to the different books of accounts that are prepared at basic

level by the accountant for the business firm. There are number of prime entry books that are

prepared by the business firms like sales day book and purchase day book etc. Different

somewhat prime of books entry is given below.

1 Make the journal entries along with the computation of owners capital

a) Framing the books of prime entry

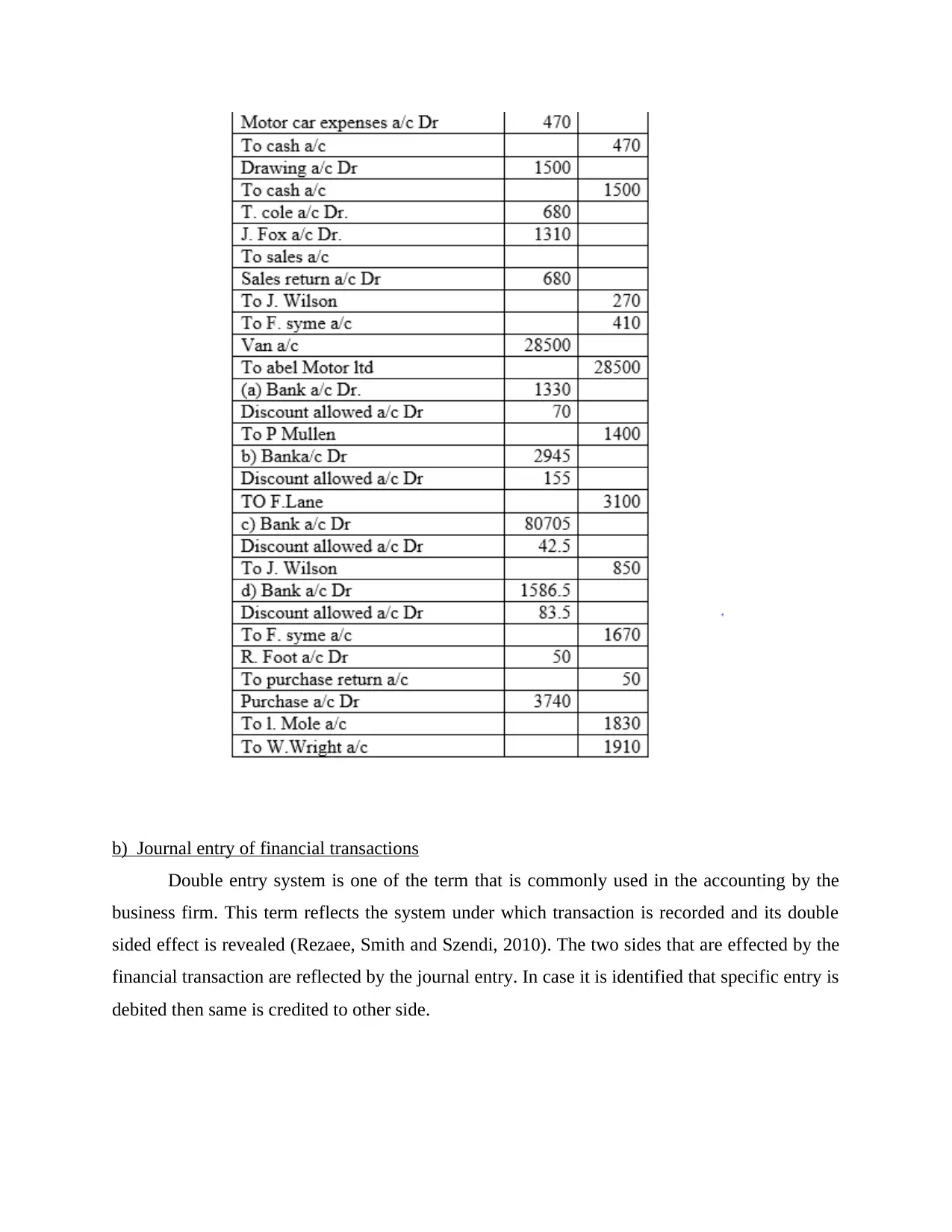

Journal entry for Alex Study’s in respect to the May 2016

b) Journal entry of financial transactions

Double entry system is one of the term that is commonly used in the accounting by the

business firm. This term reflects the system under which transaction is recorded and its double

sided effect is revealed (Rezaee, Smith and Szendi, 2010). The two sides that are effected by the

financial transaction are reflected by the journal entry. In case it is identified that specific entry is

debited then same is credited to other side.

Double entry system is one of the term that is commonly used in the accounting by the

business firm. This term reflects the system under which transaction is recorded and its double

sided effect is revealed (Rezaee, Smith and Szendi, 2010). The two sides that are effected by the

financial transaction are reflected by the journal entry. In case it is identified that specific entry is

debited then same is credited to other side.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 40

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.