Financial Accounting Principles, Stakeholders, and Statements Report

VerifiedAdded on 2020/12/18

|26

|4436

|180

Report

AI Summary

This report provides a comprehensive overview of financial accounting principles, focusing on their purpose and application. It explores the core concepts, including the importance of financial accounting in recording and summarizing transactions, as well as the preparation of financial statements such as the income statement and balance sheet. The report highlights the significance of generally accepted accounting principles (GAAP) and their role in ensuring the accuracy and reliability of financial information for stakeholders. Furthermore, the report delves into the analysis of internal and external stakeholders, detailing their interests and influence on business decisions. It includes practical examples like journal entries, ledgers, trial balance, profit and loss accounts, balance sheets, depreciation methods, and bank reconciliation statements. The report also examines the differences between financial statements prepared by sole traders and limited companies, along with control accounts and their role in financial accounting.

Financial Accounting

Principles

Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................1

Business Report...............................................................................................................................1

1. Financial accounting principles and its purpose.....................................................................1

2. Internal and external Stakeholders..........................................................................................2

Client 1.............................................................................................................................................5

(a) Journal Entry in the books of Alexandra Study:...................................................................5

(b). Ledgers:................................................................................................................................5

(c). Trail Balance in the books of Alexandra Study:...................................................................5

CLIENT 2........................................................................................................................................6

(a) Profit and loss account of Munteanu Limited........................................................................6

(b) Balance Sheet of Munteanu Limited.....................................................................................6

(c) Accounting Concepts: Consistency and Prudence:...............................................................7

(d) Purpose of Depreciation and its Methods:.............................................................................8

(e) Evaluation of difference between financial statements prepared by sole traders and limited

companies:...................................................................................................................................8

CLIENT 3........................................................................................................................................9

1. Purpose of preparation of Bank Reconciliation Statement:....................................................9

2 . Areas where bank records vary from personal records..........................................................9

3. Imprest:.................................................................................................................................10

4. Bank-reconciliation statements of Burcu Ltd, for September 2018......................................10

CLIENT 4......................................................................................................................................13

(a) Sales Ledger Control and Purchase Ledger Control Account:............................................13

(b) Control account...................................................................................................................13

Client 5...........................................................................................................................................14

(a) Suspense account and its features:.......................................................................................14

(b) Preparation of Trail Balance:...............................................................................................14

(c) Journal entries in order to show necessary corrections for eliminating suspense account

balance:.....................................................................................................................................15

A control account is a general ledger account containing only summary amounts.......................15

Introduction......................................................................................................................................1

Business Report...............................................................................................................................1

1. Financial accounting principles and its purpose.....................................................................1

2. Internal and external Stakeholders..........................................................................................2

Client 1.............................................................................................................................................5

(a) Journal Entry in the books of Alexandra Study:...................................................................5

(b). Ledgers:................................................................................................................................5

(c). Trail Balance in the books of Alexandra Study:...................................................................5

CLIENT 2........................................................................................................................................6

(a) Profit and loss account of Munteanu Limited........................................................................6

(b) Balance Sheet of Munteanu Limited.....................................................................................6

(c) Accounting Concepts: Consistency and Prudence:...............................................................7

(d) Purpose of Depreciation and its Methods:.............................................................................8

(e) Evaluation of difference between financial statements prepared by sole traders and limited

companies:...................................................................................................................................8

CLIENT 3........................................................................................................................................9

1. Purpose of preparation of Bank Reconciliation Statement:....................................................9

2 . Areas where bank records vary from personal records..........................................................9

3. Imprest:.................................................................................................................................10

4. Bank-reconciliation statements of Burcu Ltd, for September 2018......................................10

CLIENT 4......................................................................................................................................13

(a) Sales Ledger Control and Purchase Ledger Control Account:............................................13

(b) Control account...................................................................................................................13

Client 5...........................................................................................................................................14

(a) Suspense account and its features:.......................................................................................14

(b) Preparation of Trail Balance:...............................................................................................14

(c) Journal entries in order to show necessary corrections for eliminating suspense account

balance:.....................................................................................................................................15

A control account is a general ledger account containing only summary amounts.......................15

Conclusion.....................................................................................................................................15

References .....................................................................................................................................16

Appendix........................................................................................................................................17

References .....................................................................................................................................16

Appendix........................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Financial accounting principles are considered as the rules and the guidelines that the

organisation or the companies has to follow while reporting the financial statement of the

company. The process of financial accounting includes recording the transactions in the form of

journals, ledgers and summarising these transactions in form of income statement and balance

sheets. The common set of accounting principles includes generally accepted accounting

principles on the basis of which recording is done. These accounting process provide the

groundwork for analysing the financial aspects of business organisation. The company which is

selected is IAC accountants which is based in UK. The company is working and having the

experience of 15 years in accounting. This report helps to provide information on double entry

book keeping and how to extract the trial balance. Also final accounts of sole trader would be

made. The bank reconciliation that ensure company to consider the bank account have done and

at last reconciliation of control accounts is prepared.

Business Report

1. Financial accounting principles and its purpose

Financial accounting is considered as the specialised branch of accounting which keeps in

line of the companies’ financial transactions. Through these standardised guidelines, the

transactions are recorded and summarised through which they are presented in a financial report

and or in financial statements (Edwards, 2013). Various companies issue financial statement on a

regular schedule. These financial transactions are classified systematically so that final accounts

such as balance sheets, profit and loss accounts, income statement and cash flows of the

company can be determined. If the company follows the financial process of accounting then it

would be easy for them to present the actual and the true figures of the financial performance and

the position before the shareholders, government, employees, creditors and total stakeholders etc.

The accounts in financial accounting are prepared by the organisation on the basis of accounting

principles, various assumptions and the different guidelines which are made by the accounting

body of the state or country.

Financial accounting principles helps to govern the accounting of the organisation

according to the general rules and concepts (Fourie and et. al., 2015). These are considered as the

groundwork which helps the organisation in preparing the financial accounts more legalised and

1

Financial accounting principles are considered as the rules and the guidelines that the

organisation or the companies has to follow while reporting the financial statement of the

company. The process of financial accounting includes recording the transactions in the form of

journals, ledgers and summarising these transactions in form of income statement and balance

sheets. The common set of accounting principles includes generally accepted accounting

principles on the basis of which recording is done. These accounting process provide the

groundwork for analysing the financial aspects of business organisation. The company which is

selected is IAC accountants which is based in UK. The company is working and having the

experience of 15 years in accounting. This report helps to provide information on double entry

book keeping and how to extract the trial balance. Also final accounts of sole trader would be

made. The bank reconciliation that ensure company to consider the bank account have done and

at last reconciliation of control accounts is prepared.

Business Report

1. Financial accounting principles and its purpose

Financial accounting is considered as the specialised branch of accounting which keeps in

line of the companies’ financial transactions. Through these standardised guidelines, the

transactions are recorded and summarised through which they are presented in a financial report

and or in financial statements (Edwards, 2013). Various companies issue financial statement on a

regular schedule. These financial transactions are classified systematically so that final accounts

such as balance sheets, profit and loss accounts, income statement and cash flows of the

company can be determined. If the company follows the financial process of accounting then it

would be easy for them to present the actual and the true figures of the financial performance and

the position before the shareholders, government, employees, creditors and total stakeholders etc.

The accounts in financial accounting are prepared by the organisation on the basis of accounting

principles, various assumptions and the different guidelines which are made by the accounting

body of the state or country.

Financial accounting principles helps to govern the accounting of the organisation

according to the general rules and concepts (Fourie and et. al., 2015). These are considered as the

groundwork which helps the organisation in preparing the financial accounts more legalised and

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

widely accepted. There are various number of accounting principles some of which includes the

going concern, revenue recognition, matching concept and many other. There are different

accounting principles which differs from country to country.

Purpose of Financial accounting: There are various tools in the financial accounting which

helps organisation to achieve the objective of making financial accounting more reliable. These

includes the following:

The purpose of financial accounting is to accumulate the report on financial information

and its performance to the stakeholders. This information helps in reaching the further

decision about how to manage the business and what are the departments where further

plans are to be made (Hale, Hale and Held, 2012).

The activities which are prepared in financial reporting helps in a systematic way so that

it would provide smoothness in the accounting operations.

The financial accounting helps in ensuring the compliance of rule and regulations which

relates to relevant laws and standards.

The strategy that are prepared and are implemented in this process all depends upon the

performance and the results of the financial accounting.

The preparation of accounting process helps to make the decisions to invest in the other

businesses or not.

This also helps in assuring that accounting policies and procedures helps in adoption of

business organisation and are uniformly followed by them.

2. Internal and external Stakeholders

The term ‘stakeholders’ is defined as a person or an organisation which has interest in the

success or failure of business or a project. Stakeholders of the company has a significant impact

on the decisions that are made by them through which the operations and the finances of an

organisation is made (Hall, 2012). The stakeholders of the business organisation depend on the

actions of organisation, its goals and its objectives. The stakeholders are classified into two

different parts which includes the following: Internal stakeholders and the External Stakeholders.

Companies has a direct and indirect influence on the decision of the stakeholders. For example,

some of the stakeholders includes shareholders, creditors, government, employees, suppliers,

consumers etc. The internal stakeholders are considered as the stakeholder which are individuals,

persons, or the organisation which has the influence on the business organisation. These includes

2

going concern, revenue recognition, matching concept and many other. There are different

accounting principles which differs from country to country.

Purpose of Financial accounting: There are various tools in the financial accounting which

helps organisation to achieve the objective of making financial accounting more reliable. These

includes the following:

The purpose of financial accounting is to accumulate the report on financial information

and its performance to the stakeholders. This information helps in reaching the further

decision about how to manage the business and what are the departments where further

plans are to be made (Hale, Hale and Held, 2012).

The activities which are prepared in financial reporting helps in a systematic way so that

it would provide smoothness in the accounting operations.

The financial accounting helps in ensuring the compliance of rule and regulations which

relates to relevant laws and standards.

The strategy that are prepared and are implemented in this process all depends upon the

performance and the results of the financial accounting.

The preparation of accounting process helps to make the decisions to invest in the other

businesses or not.

This also helps in assuring that accounting policies and procedures helps in adoption of

business organisation and are uniformly followed by them.

2. Internal and external Stakeholders

The term ‘stakeholders’ is defined as a person or an organisation which has interest in the

success or failure of business or a project. Stakeholders of the company has a significant impact

on the decisions that are made by them through which the operations and the finances of an

organisation is made (Hall, 2012). The stakeholders of the business organisation depend on the

actions of organisation, its goals and its objectives. The stakeholders are classified into two

different parts which includes the following: Internal stakeholders and the External Stakeholders.

Companies has a direct and indirect influence on the decision of the stakeholders. For example,

some of the stakeholders includes shareholders, creditors, government, employees, suppliers,

consumers etc. The internal stakeholders are considered as the stakeholder which are individuals,

persons, or the organisation which has the influence on the business organisation. These includes

2

the directors, owners, employees and the management of the company. Whereas external

stakeholder includes customers, suppliers, creditors, government or the regulatory body or the

society etc.

Internal stakeholders and their interest in the large business organisation as a whole:

Some of the major internal stakeholders of a large business organisation includes the

following:

Employees: These are considered as the main internal stakeholders who gets affected or

be affected by the actions, objectives and the policies of the organisation. As they have

the monetary interest in form of salary, bonus and the incentives which forms the part of

organisational goals (Jönsson, 2013). The employees in the company plays major role in

formulation of the strategies which are related to the working of the company. As it is

seen that any business organisation while formulating the business strategy takes into

consideration the opinions of the employees as well as their concerns.

Shareholders: These are the subset of the stake holder's category. Shareholders are

considered as the group of individuals who owns or holds the shares of the company.

These are considered as the sole owner of the company and has a complete interest in the

performance of the company. The shareholders of the company have monetary interest as

they hold the share of the company which gets valued if the performance of the business

increases. The decision that are made to owners or the shareholders of the company can

impact the organisation in different ways. As the owner of the company are responsible

for making decision which affects both the internal as well as the external stakeholders of

the company.

External stakeholders and their interest in the business organisation:

There are various external stakeholders which have interest in the working of

organisation. These includes the following:

Customers: These are the main stakeholders who has the direct impact on the operations

of the business. They are the form of external stakeholders and in the large business

organisation. As they affect the demand of the product that company produces.

Customers are considered as the most important stakeholders who depends on the

financial performance of the company as if the company is performing well it would

provide heavy discount on their products which would make them achieve success. Also

3

stakeholder includes customers, suppliers, creditors, government or the regulatory body or the

society etc.

Internal stakeholders and their interest in the large business organisation as a whole:

Some of the major internal stakeholders of a large business organisation includes the

following:

Employees: These are considered as the main internal stakeholders who gets affected or

be affected by the actions, objectives and the policies of the organisation. As they have

the monetary interest in form of salary, bonus and the incentives which forms the part of

organisational goals (Jönsson, 2013). The employees in the company plays major role in

formulation of the strategies which are related to the working of the company. As it is

seen that any business organisation while formulating the business strategy takes into

consideration the opinions of the employees as well as their concerns.

Shareholders: These are the subset of the stake holder's category. Shareholders are

considered as the group of individuals who owns or holds the shares of the company.

These are considered as the sole owner of the company and has a complete interest in the

performance of the company. The shareholders of the company have monetary interest as

they hold the share of the company which gets valued if the performance of the business

increases. The decision that are made to owners or the shareholders of the company can

impact the organisation in different ways. As the owner of the company are responsible

for making decision which affects both the internal as well as the external stakeholders of

the company.

External stakeholders and their interest in the business organisation:

There are various external stakeholders which have interest in the working of

organisation. These includes the following:

Customers: These are the main stakeholders who has the direct impact on the operations

of the business. They are the form of external stakeholders and in the large business

organisation. As they affect the demand of the product that company produces.

Customers are considered as the most important stakeholders who depends on the

financial performance of the company as if the company is performing well it would

provide heavy discount on their products which would make them achieve success. Also

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the assets and the liabilities of company would enhance the performance in relevant

manner. They have the interest in the business operations through the products that they

purchase they also have the interest in the brand image and the quality of the product that

company offers to them. The business organisation operates to fulfil the demands of the

customers so that they are able to produce maximum profit from sales.

Suppliers: These are also known as the external stakeholders as they impact the

operation of the business organisation (Bushman and Smith, 2012). it is seen that the

financial information of the company would give the suppliers a brief about how much

debt company is having on them. Which will impact the decision of giving credit supplies

to them. As they have the potential substantial proportion of their revenues which may

come from company. Also they impact the business organisation through their activities.

As they provide the raw material for the working of the company so they have a high

amount of importance for company to follow.

Regulators: The organisation or any business concerns are regulated by certain

governmental norms or the departments which impacts the business of the company as a

whole. The financial information is essential for them to know whether the company is

giving the tax on time or not and this would also help them to know whether company is

working for the benefit of the shareholders or not. These are considered as the external

stakeholders which tries to monitor the operations of the business and watch that whether

the business organisation is complying with the regulations or the formalities. The

regulators of the company have the interest to comply with the operations of the

organisation so that there is no impact on its performance.

Government: these are considered as one of the main stakeholder of business

organisation who have significant impact on the performance of business (Holthausen

and Watts, 2012). The government prepare various policies and the rules which are

related to the working of the organisation. They also make various departments which

helps the government to ensure the compliance of laws is done by the company. They

also provide the framework for the organisational suitable growth.

Investors: Generally the term stakeholders are categorised as investors who either

increase their stake in the company or decrease it according to the performance of the

business entity (Mullinova, 2016). The decision of investment is based on performance of

4

manner. They have the interest in the business operations through the products that they

purchase they also have the interest in the brand image and the quality of the product that

company offers to them. The business organisation operates to fulfil the demands of the

customers so that they are able to produce maximum profit from sales.

Suppliers: These are also known as the external stakeholders as they impact the

operation of the business organisation (Bushman and Smith, 2012). it is seen that the

financial information of the company would give the suppliers a brief about how much

debt company is having on them. Which will impact the decision of giving credit supplies

to them. As they have the potential substantial proportion of their revenues which may

come from company. Also they impact the business organisation through their activities.

As they provide the raw material for the working of the company so they have a high

amount of importance for company to follow.

Regulators: The organisation or any business concerns are regulated by certain

governmental norms or the departments which impacts the business of the company as a

whole. The financial information is essential for them to know whether the company is

giving the tax on time or not and this would also help them to know whether company is

working for the benefit of the shareholders or not. These are considered as the external

stakeholders which tries to monitor the operations of the business and watch that whether

the business organisation is complying with the regulations or the formalities. The

regulators of the company have the interest to comply with the operations of the

organisation so that there is no impact on its performance.

Government: these are considered as one of the main stakeholder of business

organisation who have significant impact on the performance of business (Holthausen

and Watts, 2012). The government prepare various policies and the rules which are

related to the working of the organisation. They also make various departments which

helps the government to ensure the compliance of laws is done by the company. They

also provide the framework for the organisational suitable growth.

Investors: Generally the term stakeholders are categorised as investors who either

increase their stake in the company or decrease it according to the performance of the

business entity (Mullinova, 2016). The decision of investment is based on performance of

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business. As they are the core investors other than shareholders of the company. They

charge interest against the investment made in the company.

Client 1

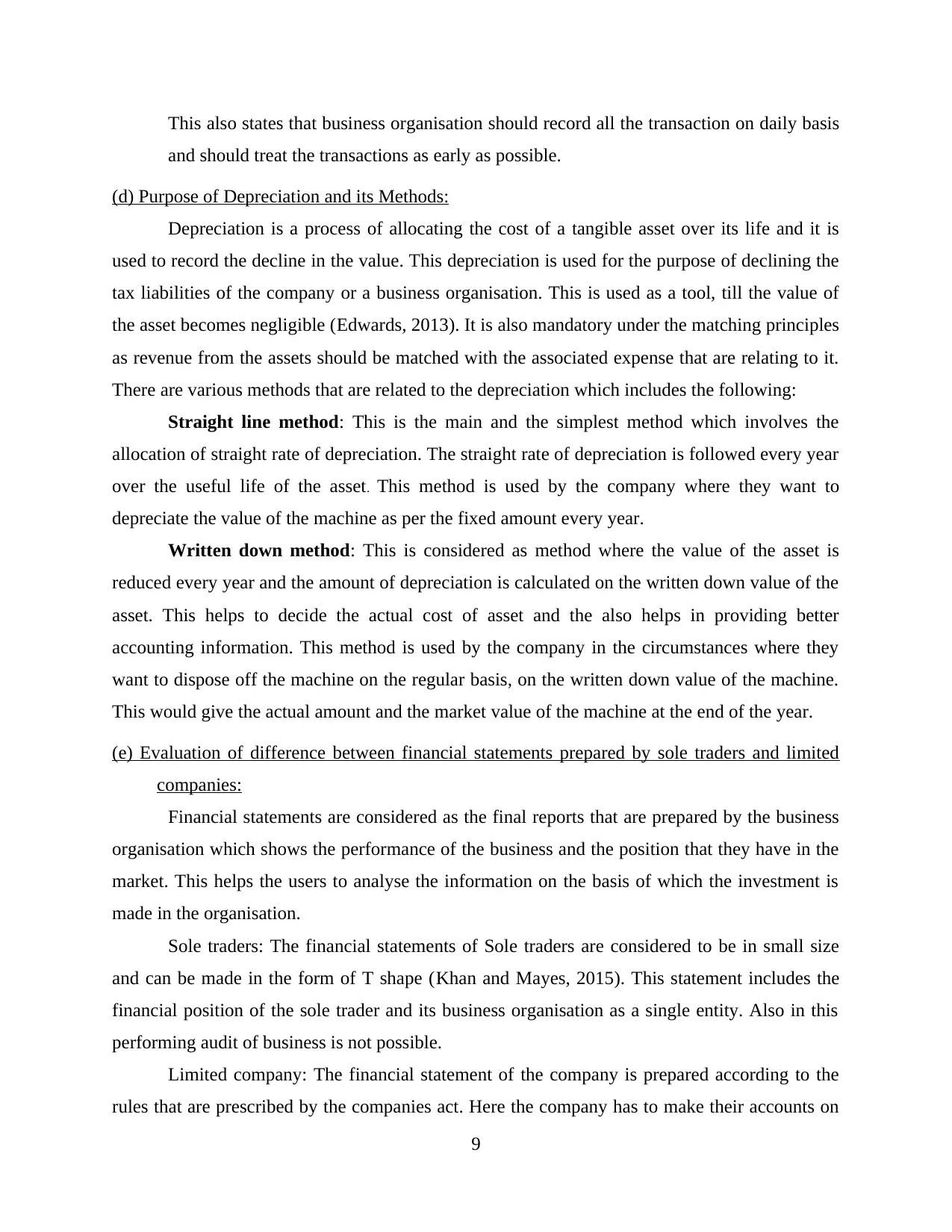

(a) Journal Entry in the books of Alexandra Study:

See Appendix

(b). Ledgers:

See Appendix

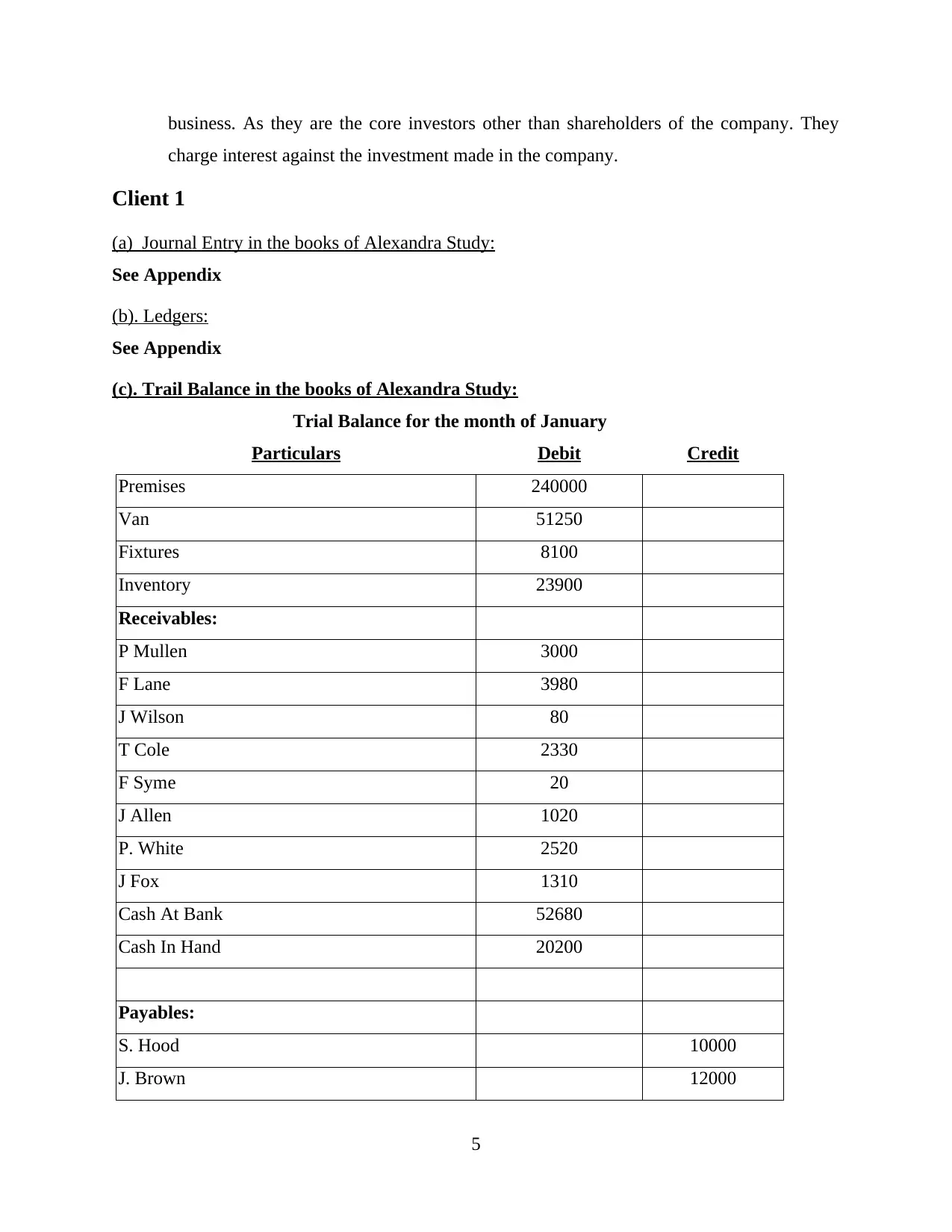

(c). Trail Balance in the books of Alexandra Study:

Trial Balance for the month of January

Particulars Debit Credit

Premises 240000

Van 51250

Fixtures 8100

Inventory 23900

Receivables:

P Mullen 3000

F Lane 3980

J Wilson 80

T Cole 2330

F Syme 20

J Allen 1020

P. White 2520

J Fox 1310

Cash At Bank 52680

Cash In Hand 20200

Payables:

S. Hood 10000

J. Brown 12000

5

charge interest against the investment made in the company.

Client 1

(a) Journal Entry in the books of Alexandra Study:

See Appendix

(b). Ledgers:

See Appendix

(c). Trail Balance in the books of Alexandra Study:

Trial Balance for the month of January

Particulars Debit Credit

Premises 240000

Van 51250

Fixtures 8100

Inventory 23900

Receivables:

P Mullen 3000

F Lane 3980

J Wilson 80

T Cole 2330

F Syme 20

J Allen 1020

P. White 2520

J Fox 1310

Cash At Bank 52680

Cash In Hand 20200

Payables:

S. Hood 10000

J. Brown 12000

5

W Tone 960

R Foot 160

L Mole 1830

W. Wright 1910

D Main 2060

Storage Cost 450

Purchase 9820

Sales 11460

Motor Expenses 470

Sales Return 680

Purchase Return 50

Salaries 4800

Business Rates 1320

Capital 387500

Total 427930 427930

CLIENT 2

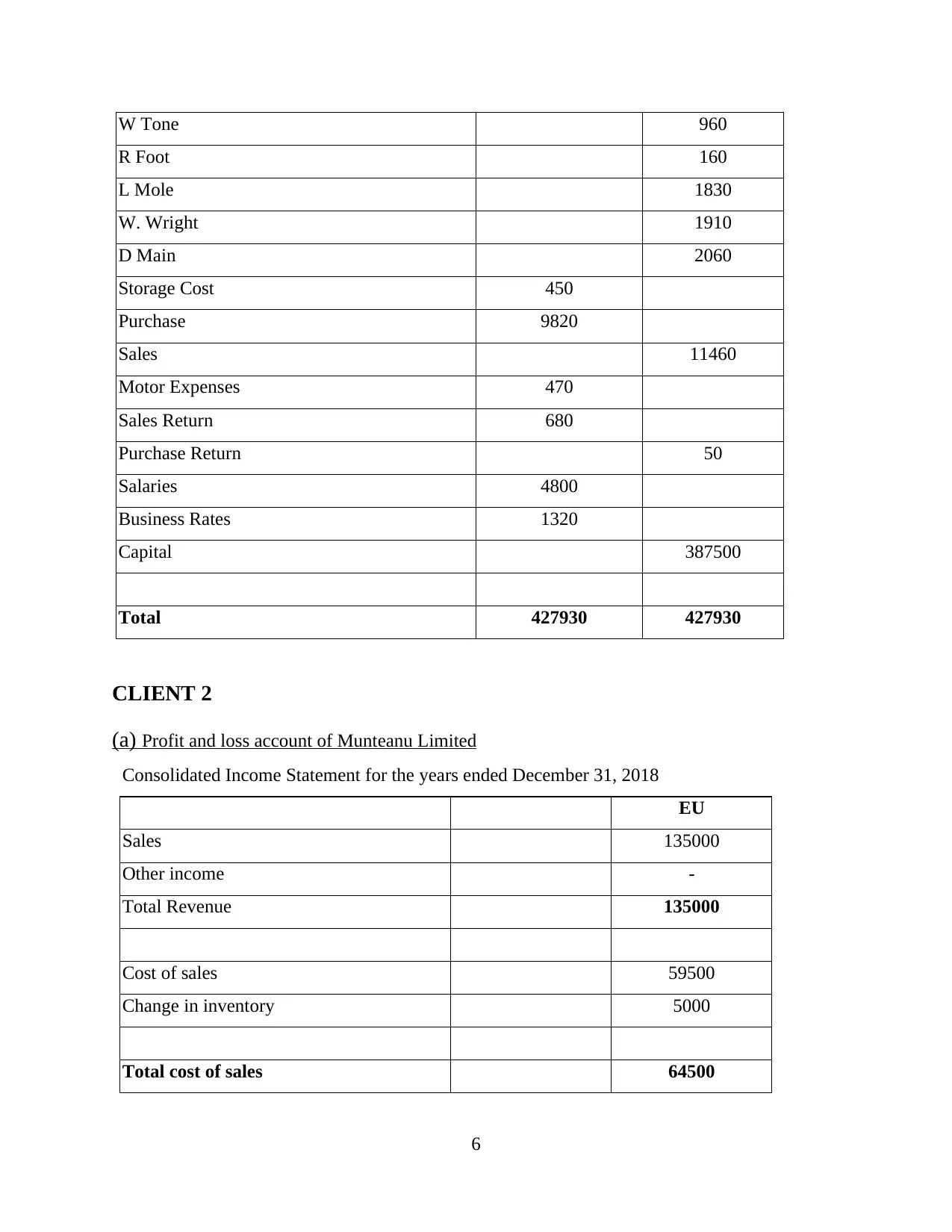

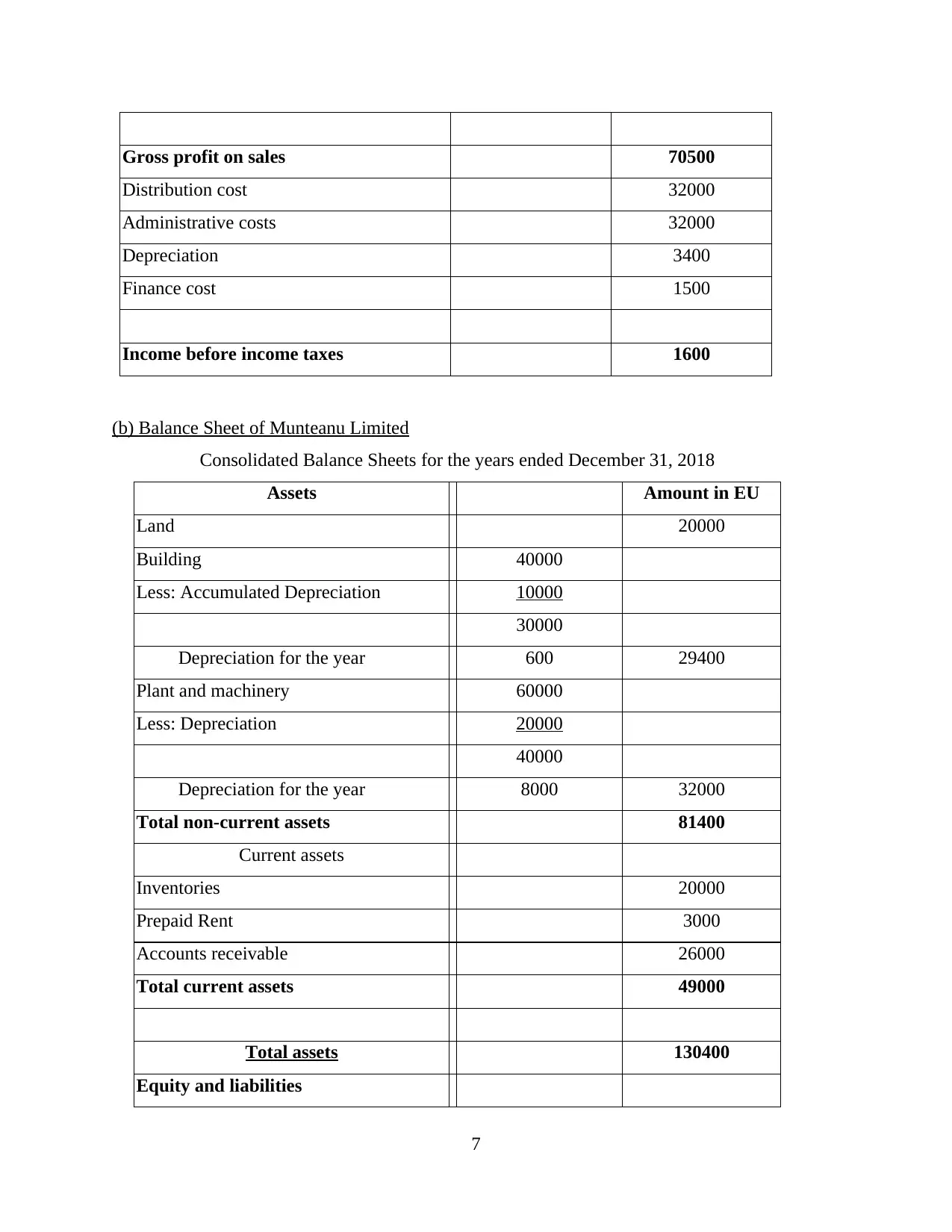

(a) Profit and loss account of Munteanu Limited

Consolidated Income Statement for the years ended December 31, 2018

EU

Sales 135000

Other income -

Total Revenue 135000

Cost of sales 59500

Change in inventory 5000

Total cost of sales 64500

6

R Foot 160

L Mole 1830

W. Wright 1910

D Main 2060

Storage Cost 450

Purchase 9820

Sales 11460

Motor Expenses 470

Sales Return 680

Purchase Return 50

Salaries 4800

Business Rates 1320

Capital 387500

Total 427930 427930

CLIENT 2

(a) Profit and loss account of Munteanu Limited

Consolidated Income Statement for the years ended December 31, 2018

EU

Sales 135000

Other income -

Total Revenue 135000

Cost of sales 59500

Change in inventory 5000

Total cost of sales 64500

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Gross profit on sales 70500

Distribution cost 32000

Administrative costs 32000

Depreciation 3400

Finance cost 1500

Income before income taxes 1600

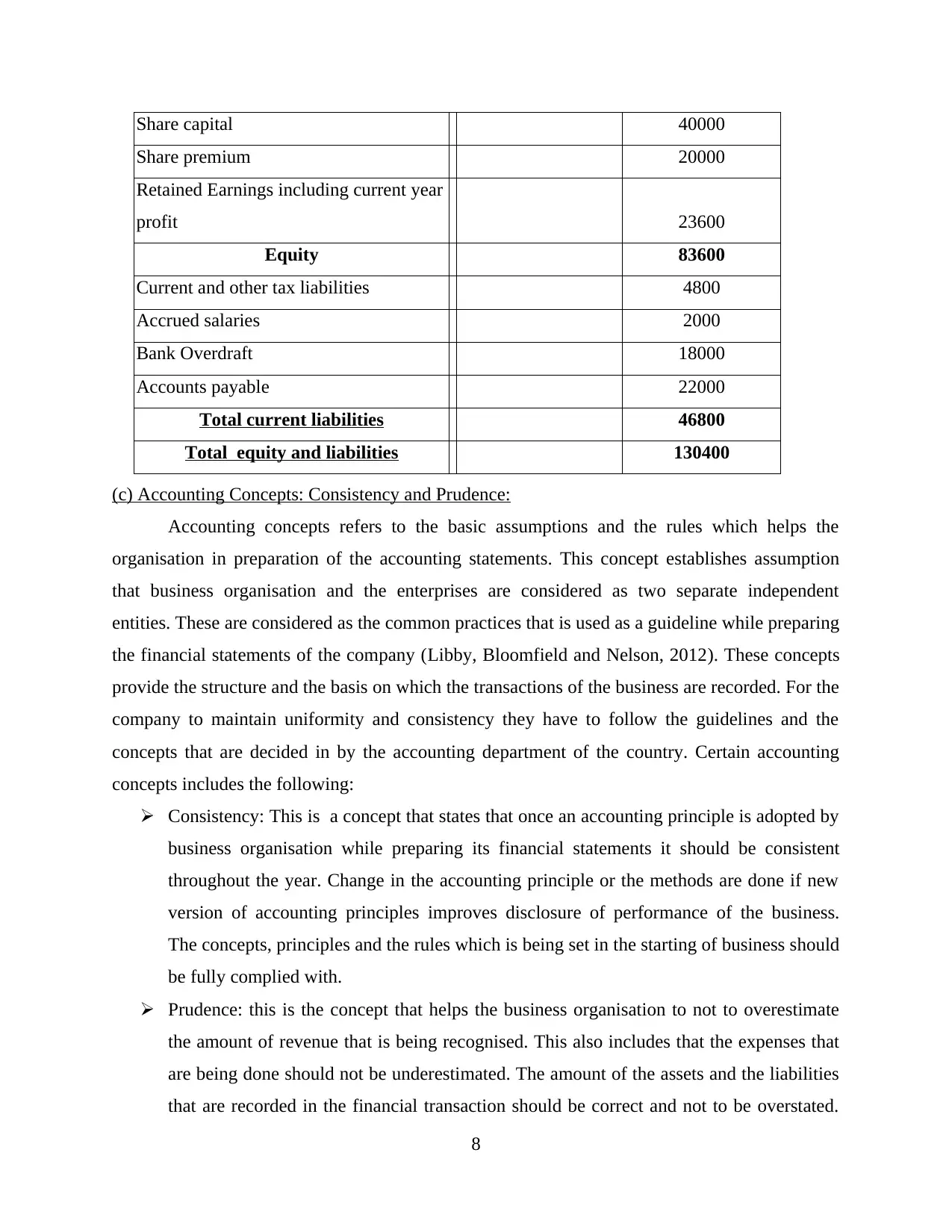

(b) Balance Sheet of Munteanu Limited

Consolidated Balance Sheets for the years ended December 31, 2018

Assets Amount in EU

Land 20000

Building 40000

Less: Accumulated Depreciation 10000

30000

Depreciation for the year 600 29400

Plant and machinery 60000

Less: Depreciation 20000

40000

Depreciation for the year 8000 32000

Total non-current assets 81400

Current assets

Inventories 20000

Prepaid Rent 3000

Accounts receivable 26000

Total current assets 49000

Total assets 130400

Equity and liabilities

7

Distribution cost 32000

Administrative costs 32000

Depreciation 3400

Finance cost 1500

Income before income taxes 1600

(b) Balance Sheet of Munteanu Limited

Consolidated Balance Sheets for the years ended December 31, 2018

Assets Amount in EU

Land 20000

Building 40000

Less: Accumulated Depreciation 10000

30000

Depreciation for the year 600 29400

Plant and machinery 60000

Less: Depreciation 20000

40000

Depreciation for the year 8000 32000

Total non-current assets 81400

Current assets

Inventories 20000

Prepaid Rent 3000

Accounts receivable 26000

Total current assets 49000

Total assets 130400

Equity and liabilities

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Share capital 40000

Share premium 20000

Retained Earnings including current year

profit 23600

Equity 83600

Current and other tax liabilities 4800

Accrued salaries 2000

Bank Overdraft 18000

Accounts payable 22000

Total current liabilities 46800

Total equity and liabilities 130400

(c) Accounting Concepts: Consistency and Prudence:

Accounting concepts refers to the basic assumptions and the rules which helps the

organisation in preparation of the accounting statements. This concept establishes assumption

that business organisation and the enterprises are considered as two separate independent

entities. These are considered as the common practices that is used as a guideline while preparing

the financial statements of the company (Libby, Bloomfield and Nelson, 2012). These concepts

provide the structure and the basis on which the transactions of the business are recorded. For the

company to maintain uniformity and consistency they have to follow the guidelines and the

concepts that are decided in by the accounting department of the country. Certain accounting

concepts includes the following:

Consistency: This is a concept that states that once an accounting principle is adopted by

business organisation while preparing its financial statements it should be consistent

throughout the year. Change in the accounting principle or the methods are done if new

version of accounting principles improves disclosure of performance of the business.

The concepts, principles and the rules which is being set in the starting of business should

be fully complied with.

Prudence: this is the concept that helps the business organisation to not to overestimate

the amount of revenue that is being recognised. This also includes that the expenses that

are being done should not be underestimated. The amount of the assets and the liabilities

that are recorded in the financial transaction should be correct and not to be overstated.

8

Share premium 20000

Retained Earnings including current year

profit 23600

Equity 83600

Current and other tax liabilities 4800

Accrued salaries 2000

Bank Overdraft 18000

Accounts payable 22000

Total current liabilities 46800

Total equity and liabilities 130400

(c) Accounting Concepts: Consistency and Prudence:

Accounting concepts refers to the basic assumptions and the rules which helps the

organisation in preparation of the accounting statements. This concept establishes assumption

that business organisation and the enterprises are considered as two separate independent

entities. These are considered as the common practices that is used as a guideline while preparing

the financial statements of the company (Libby, Bloomfield and Nelson, 2012). These concepts

provide the structure and the basis on which the transactions of the business are recorded. For the

company to maintain uniformity and consistency they have to follow the guidelines and the

concepts that are decided in by the accounting department of the country. Certain accounting

concepts includes the following:

Consistency: This is a concept that states that once an accounting principle is adopted by

business organisation while preparing its financial statements it should be consistent

throughout the year. Change in the accounting principle or the methods are done if new

version of accounting principles improves disclosure of performance of the business.

The concepts, principles and the rules which is being set in the starting of business should

be fully complied with.

Prudence: this is the concept that helps the business organisation to not to overestimate

the amount of revenue that is being recognised. This also includes that the expenses that

are being done should not be underestimated. The amount of the assets and the liabilities

that are recorded in the financial transaction should be correct and not to be overstated.

8

This also states that business organisation should record all the transaction on daily basis

and should treat the transactions as early as possible.

(d) Purpose of Depreciation and its Methods:

Depreciation is a process of allocating the cost of a tangible asset over its life and it is

used to record the decline in the value. This depreciation is used for the purpose of declining the

tax liabilities of the company or a business organisation. This is used as a tool, till the value of

the asset becomes negligible (Edwards, 2013). It is also mandatory under the matching principles

as revenue from the assets should be matched with the associated expense that are relating to it.

There are various methods that are related to the depreciation which includes the following:

Straight line method: This is the main and the simplest method which involves the

allocation of straight rate of depreciation. The straight rate of depreciation is followed every year

over the useful life of the asset. This method is used by the company where they want to

depreciate the value of the machine as per the fixed amount every year.

Written down method: This is considered as method where the value of the asset is

reduced every year and the amount of depreciation is calculated on the written down value of the

asset. This helps to decide the actual cost of asset and the also helps in providing better

accounting information. This method is used by the company in the circumstances where they

want to dispose off the machine on the regular basis, on the written down value of the machine.

This would give the actual amount and the market value of the machine at the end of the year.

(e) Evaluation of difference between financial statements prepared by sole traders and limited

companies:

Financial statements are considered as the final reports that are prepared by the business

organisation which shows the performance of the business and the position that they have in the

market. This helps the users to analyse the information on the basis of which the investment is

made in the organisation.

Sole traders: The financial statements of Sole traders are considered to be in small size

and can be made in the form of T shape (Khan and Mayes, 2015). This statement includes the

financial position of the sole trader and its business organisation as a single entity. Also in this

performing audit of business is not possible.

Limited company: The financial statement of the company is prepared according to the

rules that are prescribed by the companies act. Here the company has to make their accounts on

9

and should treat the transactions as early as possible.

(d) Purpose of Depreciation and its Methods:

Depreciation is a process of allocating the cost of a tangible asset over its life and it is

used to record the decline in the value. This depreciation is used for the purpose of declining the

tax liabilities of the company or a business organisation. This is used as a tool, till the value of

the asset becomes negligible (Edwards, 2013). It is also mandatory under the matching principles

as revenue from the assets should be matched with the associated expense that are relating to it.

There are various methods that are related to the depreciation which includes the following:

Straight line method: This is the main and the simplest method which involves the

allocation of straight rate of depreciation. The straight rate of depreciation is followed every year

over the useful life of the asset. This method is used by the company where they want to

depreciate the value of the machine as per the fixed amount every year.

Written down method: This is considered as method where the value of the asset is

reduced every year and the amount of depreciation is calculated on the written down value of the

asset. This helps to decide the actual cost of asset and the also helps in providing better

accounting information. This method is used by the company in the circumstances where they

want to dispose off the machine on the regular basis, on the written down value of the machine.

This would give the actual amount and the market value of the machine at the end of the year.

(e) Evaluation of difference between financial statements prepared by sole traders and limited

companies:

Financial statements are considered as the final reports that are prepared by the business

organisation which shows the performance of the business and the position that they have in the

market. This helps the users to analyse the information on the basis of which the investment is

made in the organisation.

Sole traders: The financial statements of Sole traders are considered to be in small size

and can be made in the form of T shape (Khan and Mayes, 2015). This statement includes the

financial position of the sole trader and its business organisation as a single entity. Also in this

performing audit of business is not possible.

Limited company: The financial statement of the company is prepared according to the

rules that are prescribed by the companies act. Here the company has to make their accounts on

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.